Flattening the curve on COVID-19 has meant flattening the curve on tax season, too, pushing everything down the line a bit so that the final day to hand over the government’s cut of our hard-earned income comes up on July 15. That’s given us an unparalleled opportunity in a time of crisis to assess what we’re getting for our money. Amidst the smoking ruins of 2020, it’s understandable if you regret every penny you’ve ever surrendered to a tax collector.

The year 2020 should stand forever as evidence that, rather than a solution, government is often a cup of gasoline just waiting to be thrown on a fire. The spark this time was a tiny, but deadly, virus.

From the beginning, President Trump minimized the danger posed by COVID-19 even as the Centers for Disease Control and Prevention (CDC) and the Food and Drug Administration (FDA)—agencies of the federal government over which he presides—fumbled developing a test for the disease and kneecapped academic, commercial, and hospital efforts that could do better. The FDA only belatedly eased rules standing in the way of expanding the supply of ventilators, masks, hand sanitizer, and other supplies.

When companies found it challenging to navigate the ever-shifting regulatory landscape, the president invoked the Defense Production Act to force them to produce what the government wanted, when it was wanted.

To add to the fun, the CDC kept Americans entertained with contradictory advice as to whether or not wearing masks could be helpful.

Taking the chaos in D.C. as a challenge to their own abilities at confusing and dismaying the public, state governors feuded with the Trump administration as well as with local officials who were busy baffling us with their own efforts.

Perhaps the CDC’s test-fumbling was seen as insufficiently deadly; governors of some states, including New Jersey and New York, required nursing homes to accept COVID-19 patients against all advice. Such facilities have accounted for about 40 percent of all U.S. deaths during the pandemic.

In the name of delaying the spread of COVID-19, states and localities issued draconian and arbitrary shutdown rules that closed businesses, choked-off travel, interrupted personal relationships, and threatened many people with economic ruin and despair. To make it worse, some of the governors issuing them promptly ignored or gamed their own rules.

That this has been to questionable benefit should go without saying—we’re seeing a new round of mandated closures now, after Americans’ patience and limited ability to weather orders that shut businesses and kill jobs is greatly eroded. In fact, by the end of May, Americans were unemployed, aggravated, at wit’s end and ready to explode.

Despite spending years fueling conflict between police and the public, and then confining the population to stew at home over health concerns and the prospect of unpaid bills and poverty, officials seemed astonished that the country erupted in anger at the latest law-enforcement outrage.

“Police abuse remains a problem that needs to be addressed by policymakers and police professionals,” the federal government’s National Institute of Justice warned in 2000.

Twenty years later, with little done to address the issue and lots of time and frustration on their hands, Americans marched, protested, and some also rioted. The killing of George Floyd, mistreatment of African-Americans, and anger at police brutality in general, sent people into the streets to demand change—in forms good, bad, indifferent, and undefined.

How that change will shake out is anybody’s guess; as with the pandemic, Republicans and Democrats have turned dealing with police reform and racism into new excuses for political point-scoring. Will officials back enforcers to the hilt, go with tearing down random statues misunderstood by the mob, or make the difficult effort to rein-in their own out-of-control enforcers? Hang on while political professionals wet their fingers and hold them in the air.

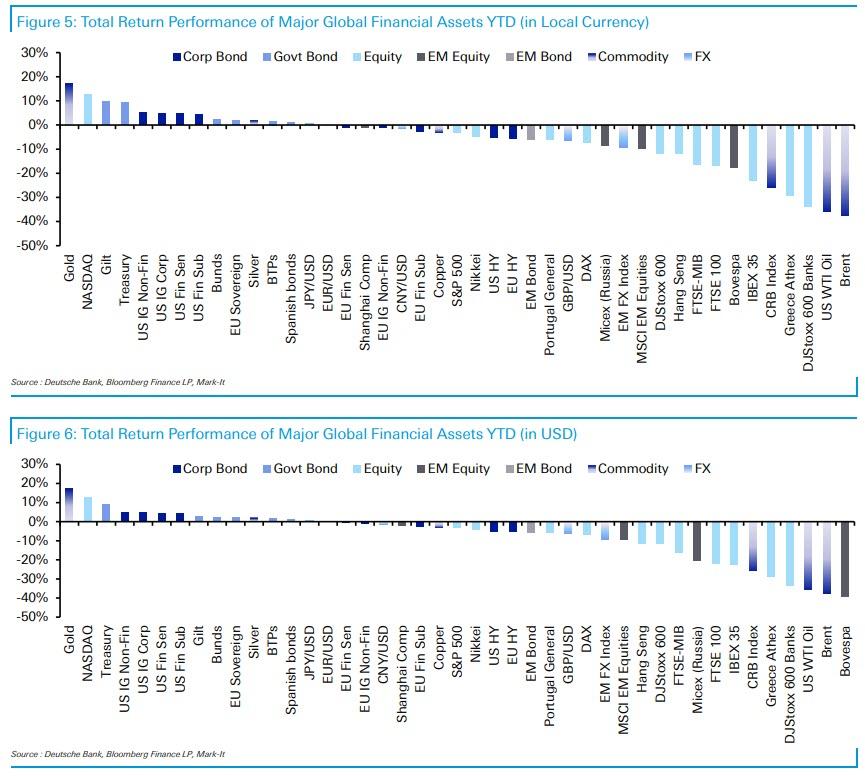

What is clear is that this turmoil has a big price tag, which will probably generate more turmoil. As of June 26, the Federal Reserve Bank of Atlanta projects a 39.5 percent decline in GDP for the second quarter.

For the year overall, the Federal Reserve Bank’s projection of a 6.5 percent decline in GDP is actually optimistic compared to the roughly 8 percent drops predicted by the International Monetary Fund (IMF) and the Organization for Economic Cooperation and Development (OECD).

“The COVID-19 pandemic pushed economies into a Great Lockdown, which helped contain the virus and save lives, but also triggered the worst recession since the Great Depression,” writes Gita Gopinath, director of the IMF’s research department.

The U.S. government tried to offset the economic fallout of the pandemic and of the lockdown orders, but it did so very badly. Of the money paid out to alleviate the pain, $1.4 billion went to dead people who are already well beyond the reach of stimulus efforts, according to the U.S. Government Accountability Office.

The checks that went to living recipients didn’t do much more good.

“Stimulus checks increase spending particularly among low-income households, but very little of the additional spending flows to the businesses most affected by the COVID shock; and loans to small businesses have little impact on employment rates,” concludes a paper from a Harvard University economic research team published earlier this month.

For all of this, we’ll be paying over the course of many years to come.

The Congressional Budget Office “projects that over the 11-year horizon, cumulative real output (in 2019 dollars) will be $7.9 trillion, or 3.0 percent of cumulative real GDP, less than what the agency projected in January.” That is, America over the next decade is expected to be a poorer place than it was on track to be. That’s not entirely because of matters under human control—COVID-19 is a creation of nature—but human government officials played an enormous role in creating the conditions in which we find ourselves.

So we’re getting quite a lot for our money. Whether all of that incompetence, in-fighting, obstructionism, authoritarianism, and waste is worth what we’re paying is a matter for each of us to decide. We’ll have time to contemplate the return on our investment as we await the arrival of this year’s tax day, and to consider if we’re happy with what we’re getting for our money.

from Latest – Reason.com https://ift.tt/3ggwbXp

via IFTTT