The bill (S. 7275) was proposed in January by state senator David Carlucci, but I just came across it:

1. As used in this section, the following terms shall have the following meanings:

(a) “hate speech” means a public expression, either verbally, in writing or through images, which intentionally makes an insulting statement about a group of persons because of race, ethnicity, nationality, religion or beliefs, sexual orientation, gender identity or physical, mental or intellectual disability….

3. (a) The provider of a social media network shall maintain an effective and transparent procedure for handling complaints about hate speech content in accordance with this subdivision….

(b) Such procedure shall ensure that the provider of the social media network:

(i) takes immediate note of the complaint and checks whether the content reported in the complaint is hate speech and subject to removal or whether access to the content must be blocked;

(ii) removes or blocks access to content that is hate speech within twenty-four hours of receiving the complaint; this shall not apply if the social media network has reached agreement with the competent law enforcement authority on a longer period for deleting or blocking any hate speech content;

(iii) removes or blocks access to all hate speech content immediately, this generally being within seven days of receiving the complaint; the seven day time limit may be exceeded if the decision regarding the hatefulness of the content is dependent on the falsity of a factual allegation or is clearly dependent on other factual circumstances; in such cases, the social media network can give the user an opportunity to respond to the complaint before the decision is rendered; and

(iv) immediately notifies the person submitting the complaint and the user about any decision, while also providing reasons for its decision….

5. (a) The attorney general may bring an action against a provider that violates the provisions of this section:

(i) to enjoin further violation of the provisions of this section; and

(ii) to recover up to one million dollars for any violation of this section, including any offense not committed in this state [or up to three million dollars {where the defendant has been found to have engaged in a pattern and practice of violating the provisions of this section}….

As best I can tell, the bill doesn’t seem to be going anywhere, but it struck me as noteworthy that Sen. Carlucci submitted it.

from Latest – Reason.com https://ift.tt/38hTvkK

via IFTTT

The bill (S. 7275) was proposed in January by state senator David Carlucci, but I just came across it:

1. As used in this section, the following terms shall have the following meanings:

(a) “hate speech” means a public expression, either verbally, in writing or through images, which intentionally makes an insulting statement about a group of persons because of race, ethnicity, nationality, religion or beliefs, sexual orientation, gender identity or physical, mental or intellectual disability….

3. (a) The provider of a social media network shall maintain an effective and transparent procedure for handling complaints about hate speech content in accordance with this subdivision….

(b) Such procedure shall ensure that the provider of the social media network:

(i) takes immediate note of the complaint and checks whether the content reported in the complaint is hate speech and subject to removal or whether access to the content must be blocked;

(ii) removes or blocks access to content that is hate speech within twenty-four hours of receiving the complaint; this shall not apply if the social media network has reached agreement with the competent law enforcement authority on a longer period for deleting or blocking any hate speech content;

(iii) removes or blocks access to all hate speech content immediately, this generally being within seven days of receiving the complaint; the seven day time limit may be exceeded if the decision regarding the hatefulness of the content is dependent on the falsity of a factual allegation or is clearly dependent on other factual circumstances; in such cases, the social media network can give the user an opportunity to respond to the complaint before the decision is rendered; and

(iv) immediately notifies the person submitting the complaint and the user about any decision, while also providing reasons for its decision….

5. (a) The attorney general may bring an action against a provider that violates the provisions of this section:

(i) to enjoin further violation of the provisions of this section; and

(ii) to recover up to one million dollars for any violation of this section, including any offense not committed in this state [or up to three million dollars {where the defendant has been found to have engaged in a pattern and practice of violating the provisions of this section}….

As best I can tell, the bill doesn’t seem to be going anywhere, but it struck me as noteworthy that Sen. Carlucci submitted it.

from Latest – Reason.com https://ift.tt/38hTvkK

via IFTTT

“The general synopsis at midnight: High Iceland 1015 expected just west of Bailey 1013 by midnight tonight. New low expected Oslo 996 by same time”

July 1st…

So… that was the first half of 2020. What an extraordinary 6 months. A record panicked tumble followed by a record exuberant rise. The next 6 months are likely to prove just as … Exciting? This morning’s Porridge will cover some of the major outlook issues ahead, while tomorrow I will follow up with Reasons to be Fearful; looking at areas of concern, including banking and aviation. Friday? Who knows where we will be by then!

What the Pandemic/Lockdown co-dependency is demonstrating is that nothing is predictable. Economic models are obsolete. Goals posts have never been as mobile. “A single worker coughing in Korea might result in a town being lockdown in Germany”… It’s that sort of thing that’s setting the economic agenda.

The situation is fluid.

Even if we could see moment-by-moment economic data, we still can’t predict what follows with certainty. The economic snapshots provided by tomorrow’s US Non-Farm payrolls employment reports or IMF prognostications have never been less helpful.

The best we can do is discern trends through a glass darkly. Everything I predict this morning could unravel by this afternoon. The current flare-ups of first-wave virus outbreaks in the US highlight how expectations will move with new news!

Regard this morning’s ramblings as nothing more than crystal ball pontification for the next 6 months:

General Synopsis:

Recovery will prove stronger than worse case predictions.

Government pandemic support measures have successfully laid foundations for a confident renewal of economic activity. Coronavirus fatigue is making it easier.

Recovery won’t be V-Shaped.

Some sectors are likely to suffer a longer slow-down, but will likely adapt accordingly.

Some sectors will actively benefit as new technologies, working practices and supply chains are more quickly adopted.

There are major market risks – which will be mitigated by QE infinity measures, FOMO and the weight of investment funds available.

Rising NPLs and Market risk could impact banking and financial services – requiring long-term Central Bank interventions.

Highly overvalued Stocks and the level of corporate and sovereign debt will remain major investment concerns.

We need to understand the consequences of The New Age of Financial Stagflation: financial asset price inflation and declining returns.

Perhaps the biggest questions are those around the scale of new government debt and central bank interventions. What will be the implications and consequences of how Modern Monetary Theories play out in practice on economies and on individuals’ pension and savings planning?

The 6 Month Outlook

Markets will remain on a RoRo (Risk On/Off) rollercoaster, bouncing up or down on each piece of perceived good or bad news. They aren’t really paying attention to the underlying economic trend – but reacting tick-by-tick to the news flow. If the news turns unremittingly bad – for instance on a rising wave of cornonavirus outbreaks, negative company earnings reports, rising trade tensions, or political shocks, the downside could be exacerbated.

The tone of market commentary in the last 3 months has been fearful. Analysis has focused on how dangerously detached markets have become from the underlying economic doom and gloom. Market talking heads have been predicting a massive sell-off, and blaming QE Infinity for creating a dangerously false high market.

However, such negativity is missing the underlying narrative. The virus was bad, but not nearly as bad as predicted. There are plenty of factors supporting markets, and building some confidence.

First and foremost, Central Banks simply can’t afford the economic dislocation that would follow a major stock and bond crash. Any weakness is likely to be countered by further “do-whatever-it-takes” announcements on Central Bank purchasing programmes – right up to equity ETF purchase programmes. (That doesn’t condone the distortions of QE Infinity as a good thing – they have all-but slain the functioning of free markets, but they are a necessary evil.)

Second, market pundits are a gloomy bearish crowd. Do not go to parties with them. They delight in underestimating the potential upside. The truth lies between. Paste a copy of Blain’s Mantra No 4 to your laptop: “Things are never as bad as you fear, but never as good as you hope.”

Third, there is no shortage of investment funds – parked in cash, gold or zero-yielding bonds. It’s looking to be put back to work.

The promise of Central Bank unlimited support, together with an improving outlook on economic activity, and FOMO, should ensure “buy-the-dip” buyers quickly set market bottoms.

I remain seriously amazed at just how detached markets are from the economic reality. Stock prices are not pricing in a recovery – they are pricing in an economic boom! Prices are too optimistic. The reality is there is still plenty of Coronavirus bad news to come, rising unemployment and corporate defaults. That’s why I won’t predict a much higher upside level for stocks – at least not until we’ve got the all clear on the virus and clear economic recovery.

It’s likely stocks will remain RoRo volatile through the coming months, and trend around current levels in a surprisingly wide and volatile band. I suspect the recovery in US prices is probably done. Europe has done much better on handling the Virus, but stocks have massively lagged – mainly on doubts about whether the ECB can actually revive moribund economies, and whether the EU can deliver its massive new mutualised support package.

One sector that has really struggled is banking. US Bank are down 30%, while Europe is even worse. I can’t see any reasons to be positive on the sector, but if bank prices start to rise, that may be another recovery signal. (Or it might just be punters looking for cheap stocks on the hope a rising tide will lift all boats… not if they are holed below the waterline with exploding NPLs, they won’t!)

While its less likely markets will lose their faith in Central Banks and the explicit free put they’ve granted markets, there is still the big unknown. We just don’t know enough about the virus, its economic power, and its effects on economic behaviour.

The Big Unknown – The Virus

We can’t predict with any real certainty what the Virus does next. We don’t know the likelihood of a proper second wave in the autumn, or even the effect of the ignitions of first-wave hotspots. It’s clear many individuals remain intensely fearful of the disease – and their behaviours will colour recovery.

The economic power of the virus is Lockdown. I suspect that will lessen in coming months as governments persuade most workers its safe to resume work. Poeple are bored and tired of it now. But its influence will be felt strongly across some sectors. How the virus develops will determine how quickly tourism and aerospace recover, but also hospitality – which employs over one million in the UK.

Extended lockdowns will result in lost jobs, lost skillsets, and multiplier effects across the whole economy, which will depress consumption. There are clear dangers in how long Governments can sustain furlough schemes – at what point to workers lose their skills and incentives to work.

Recovery – on or off?

I’m increasingly positive the last 4 months of lockdown repression has triggered a stronger than expected and sustainable growth rebound. It’s based around the consumer snapback, driven by the amount of money folk unexpectedly found themselves saving by not commuting, not shopping, not eating out, and the pubs being closed.

The strength of the snapback is illustrated by many indicators which have positively surprised markets, including rising PMIs, consumer confidence, retail sales and home buying.

It feels like there is something of a COVID Spring underway – even though the weather on the first of July is pretty wintery! New companies are being created at record rates. Surprisingly – given the virus – there is a sense of increasing confidence which has been fuelled by the willingness of conservative governments to spend, and extend rental and loan holidays.

There are also indications that government fiscal measures; including furloughs, bailouts and support packages aren’t just lifeboats, but are actually acting as proper growth multipliers on both individual and corporate behaviours. Infrastructure spending binges will also help in terms of multiplier effects – if properly managed and coordinated. We wouldn’t want building HS2 – the railway to nowhere – crowding out more important housing provision.

There was a general fear companies would seek to rein back investment, hiring and product development spending, preparing for potential solvency issues over a lengthy slowdown. Instead, corporate confidence is improving. Many companies are choosing to regard the Pandemic as an opportunity for growth – actively going out seeking new markets, and hiring staff, rather than contracting. (That business confidence is also vulnerable to virus badnews..)

There remains a high degree of risk many jobs will be lost in sectors most impacted by the crisis as companies seek to rationalise and right-size for the new economy. We know it won’t be a sharp V-shaped recovery. Many self-employed workers have received zero cash through lockdown, and sectors like tourism and aerospace remain shuttered. They account for up to 18% of the economy – and will dilute growth potential.

What are the big issues?

The obvious ones are trade – the UK and Europe failing to find a Brexit accommodation, or the China/US spat – which could create a whole new series of questions. (The Chinese escalation of tension via its Security Law/annexation of Hong Kong is one factor – picking its moment against a distracted US.)

I’d identify politics as the major risk. The UK and US governments have had a miserable virus bulging with policy failures and confusion. In the UK much of that seems down to bureaucracy – and, as I predicted, heads are being lopped. In the US, well…. That’s a whole other story about a nation increasingly divided against itself…

The ability of governments to deliver will be critical. If they fail… we get another phase of political populism and all the policy wobbles that will entail.

However, I suspect the biggest unknown risk might be the long-term implications of QE and Government debt. Markets are not functioning effectively. There has been massive inflation in financial assets. Will rising government debt cause inflation in the real economy? To some extent it must – more money chasing the same number of goods? Or is something extraordinary occurring – where the velocity of money around the economy is matched off against the degree of debt/leverage in the economy?

Smoke and mirrors? Perhaps it might be best not to ask to many questions… just in case the current monetary illusion shatters…

via ZeroHedge News https://ift.tt/38t1QCB Tyler Durden

After Massive Upward Revision, ADP Employment Data Shows Job Rebound Slowing In June Tyler Durden

Wed, 07/01/2020 – 08:21

After the last two month’s big drop in ADP employment (which was still dramatically different from BLS data), analysts expected a rebound surge in employment in June.

ADP saw 19.5mm people lose their jobs in April, another 2.8 million lost jobs in May (which has now been revised to +3.065mm!), and now sees the US economy adding 2.369 million in June (disappointing expectations of a 2.9 million gain)…

Source: Bloomberg

Both Goods and Services jobs rebounded but the pace of rebound slowed…

Source: Bloomberg

So, based on the revisions, job additions are slowing!

“Small business hiring picked up in the month of June,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute.

“As the economy slowly continues to recover,we are seeing a significant rebound in industries that once experienced the greatest joblosses. In fact, 70 percent of the jobs added this month were in the leisure and hospitality, trade and construction industries.”

* * *

So… if you put any credence in today’s data, just remember last month’s data was revised from a 2.76 million job loss to a 3.065 million job gain! Zandi?

via ZeroHedge News https://ift.tt/2Binlda Tyler Durden

Futures Slide In Downbeat Start To New Quarter Tyler Durden

Wed, 07/01/2020 – 08:10

Following Tuesday’s last 10 minute spike which only emerged as there were not as many sellers as some had predicted (such as JPMorgan whose forecast of $170BN in forced quarter-end selling failed to materialize), global markets have been under pressure to start the new quarter, and S&P futures fell on Wednesday as today the corona mood was one of concern over hope (this is sure to reverse tomorrow) as a record single-day spike in coronavirus cases in the country heightened fears of another lockdown, while fresh signs of geopolitical tensions involving Hong Kong where the first protesters were arrested under the new security law also triggered some selling.

After notching up its biggest three-month gains since 1998 in the previous session, the S&P 500 looked set to begin the third quarter on a glum note as COVID-19 cases rose by more than 47,000 on Tuesday, with California, Texas and Arizona emerging as new epicenters. A warning from Anthony Fauci that the number of daily cases could soon double to 100,000 also took the shine off data showing a slump in global manufacturing was easing as economies reopened from sweeping lockdowns imposed to contain the spread of the novel coronavirus.

US equity futures extended losses after the U.K.’s foreign secretary said China’s national security legislation constitutes a “clear violation” of the autonomy of Hong Kong. Battered cruise line operators Norwegian Cruise Line Holdings, Royal Caribbean Cruises and Carnival Corp tumbled between 2.3% and 2.6% in premarket trading. In a bright spot, FedEx jumped 11.5% after posting better-than-expected quarterly profit and revenue, helped by a surge in pandemic-fueled home deliveries.

“We feel like a lot of the good news is priced in,” Jim McDonald, chief investment strategist at Northern Trust, said on Bloomberg TV. “The market’s got some optimism that we are going to see more of a V-shaped recovery, so there is risk of some modest disappointment.”

The Stoxx Europe 600 Index erased an earlier advance as data showed German unemployment rose to the highest level in nearly five years and U.K. businesses reported a record slump in sales.

Asian stocks were little changed, with health care falling and energy rising, after rising in the last session. Most markets in the region were up, with Shanghai Composite gaining 1.4% and India’s S&P BSE Sensex Index rising 1.3%, while Japan’s Topix Index dropped 1.3% after data showed confidence among large manufacturers in Japan fell to the lowest since 2009, while stocks ticked higher in Shanghai and Sydney. The Shanghai Composite Index rose 1.4%, with Hebei Hengshui and Greenland Holdings posting the biggest advances. Trading volume for MSCI Asia Pacific Index members was 12% above the monthly average for this time of the day.

Yield edged higher and the dollar was steady ahead of minutes from the Federal Open Market Committee’s June meeting. Gold was near $1,800 an ounce.

Treasuries pressured lower following a wider bear-steepening move across the German curve. Gilts also pressured lower following drop in demand for U.K. 30-year bond sale, also weighing on Treasuries. Upside pressure on yields emerged from the cash open as month- and quarter-end support evaporates. Yields were cheaper by as much as 3bp across the curve with long-end- led losses steepening 2s10s, 5s30s by~2bp; 10-year yields around 0.68%, cheaper by ~2.5bp. Bunds and gilts underperform by around 1.5bp each vs. Treasuries, weighing into the early New York session. Five-year note’s yield declined to a record low 0.264% on June 30 with outperformance driven by expectations for Federal Reserve policy, specifically the prospect of yield-curve control.

In FX, the dollar reversed an earlier drop as risk assets slumped into the European trading session; the euro slumped to the lowest level in months while Norway’s krone was largely unchanged before rallying with oil prices. The yen gained against almost Group-of-10 currencies as Japanese shares declined and concerns over the spread of coronavirus spurred haven demand; the currency advanced agains the dollar for first time in six days. Sweden’s krona traded little changed against the euro after shrugging off the central bank’s decision to boost QE.

In commodities, oil rose after its best quarter in almost three decades following a report pointing to the first drop in U.S. crude stockpiles since May. Gold saw some modest weakness as risk assets rolled over.

Figures on U.S. manufacturing activity and private payrolls for June are due later in the day, followed by the Labor Department’s closely watched nonfarm payrolls report on Thursday. The closely watched FOMC minutes are also due at 2pm today.

Markets Snapshot

S&P 500 futures down 0.2% to 3,085.75

STOXX Europe 600 up 0.3% to 361.42

MXAP down 0.01% to 157.85

MXAPJ up 0.4% to 515.33

Nikkei down 0.8% to 22,121.73

Topix down 1.3% to 1,538.61

Hang Seng Index up 0.5% to 24,427.19

Shanghai Composite up 1.4% to 3,025.98

Sensex up 1.4% to 35,411.86

Australia S&P/ASX 200 up 0.6% to 5,934.40

Kospi down 0.08% to 2,106.70

German 10Y yield rose 1.7 bps to -0.437%

Euro up 0.04% to $1.1238

Brent Futures up 2.9% to $42.45/bbl

Italian 10Y yield fell 3.9 bps to 1.131%

Spanish 10Y yield rose 1.9 bps to 0.486%

Brent Futures up 2.9% to $42.45/bbl

Gold spot up 0.4% to $1,787.81

U.S. Dollar Index down 0.1% to 97.27

Top Overnight News from Bloomberg

German unemployment surged in June as one of the country’s leading economic research institutes warned of a slower-than- expected economic recovery from the coronavirus pandemic.

Factories across the euro area recorded a stronger performance than initially reported in June, a final manufacturing PMI showed, with consumer-goods producers growing again. But despite countries easing restrictions and life slowly returning to normal, output continued to contract and demand — especially among exporters — remained weak

China described Hong Kong’s new security law as a “sword of Damocles” hanging over its most strident critics, after Beijing asserted broad new powers to rein in sources of opposition, from pro-democracy protesters to news agencies to overseas dissidents

A spike in Libor rates at the height of the coronavirus crisis drove up financing costs and offset the benefits of interest-rate cuts, the Financial Stability Board said

The government of the euro zone’s third- biggest economy sold consumers a semi-retail bond called BTP Italia in May with record results, and now officials are marketing a first fully retail-based security for sale next week. This one is dubbed as BTP Futura

Russian President Vladimir Putin is on course to secure a resounding endorsement of his bid to extend his two-decade-long rule potentially up to 2036, as the Kremlin faces criticism for its heavy-handed efforts to marshal support

Asia’s factory managers saw glimmers of hope in June, with the region’s purchasing managers indexes turning up across the board as demand from China picked up

Asian equity markets began H2 with a mild positive bias after Wall St extended on gains to top off its best quarterly performance in over 2 decades amid vaccine optimism and outperformance in the energy and tech sectors, while better than expected Chinese Caixin PMI data also contributed to the upbeat mood in overnight trade. ASX 200 (+0.6%) and Nikkei 225 (-0.8%) both opened higher as they took impetus from their US counterparts with gold miners and tech front-running the gains in Australia, although the advances in Tokyo were later wiped out amid the negative BoJ Tankan survey which showed the outlook amongst the large manufacturers was at the weakest level since 2009. Elsewhere, Shanghai Comp. (+1.4%) was positive following reports the PBoC will lower rates for relending and rediscounting programs for small and agriculture-related firms by 25bps from today, and after Chinese Caixin Manufacturing PMI data topped estimates to print a 6-month high which conforms to the strong official PMI figures released yesterday. However, upside was capped given another firm liquidity drain by the PBoC and amid a holiday closure in Hong Kong for the anniversary of the handover to China, while the verbal tit-for-tat between the 2 largest economies in the world continues as China’s Foreign Ministry reiterated they will take retaliatory measures against the US removing preferential treatment for Hong Kong and with President Trump tweeting that he becomes more and more angry at China as the pandemic spreads globally and that tremendous damage has been done to the US. Finally, 10yr JGBs were lower after the bear steepening in US and as JGB yields continued to rise which saw the 30yr yield at its highest since March last year, while the BoJ’s presence in the market today and its increased purchases of 3yr-5yr maturities failed to spur prices.

Top Asian News

Najib’s 1MDB Trial on Hold to Let Him Join Malaysia Politics

Tokyo Offices Seen Facing Record Vacancies on Shift to Telework

Hundreds of Protesters Gather Despite Ban: Hong Kong Update

Secret Ballot Broke Deadlock in Vote on Samsung Heir’s Fate

A rocky start to the second half of the year with cash bourses opening flat/mixed whilst Eurex and Deutsche Boerse experienced an outage heading into the cash open. The APAC lead was mostly positive but the sentiment failed to sustain into European hours amid further tit-for-tat measures between US and China in which the latter tightened rules on four US media branches in China – a move that reciprocates US’ designation of four Chinese media outlets as foreign missions. Add to that the rising pushback against the Hong Kong National Security law which saw at least 30 people arrested hours after its implication. Furthermore, US House Speaker Pelosi called on US President Trump to sanction China under the Magnitsky act – which provides governmental sanctions against foreign individuals over human rights abuses or corruption, China said it will reciprocate if the US takes measures. Stocks are ultimately choppy in recent trade and have seen more pronounced downside after an earlier pickup, with France’s CAC (-0.9%) the current laggard, weighed on by shares in Renault (-4.3%) after the group stated it sees its French market contracting by some 20% this year, whilst Airbus (-2.3%) shares unwelcome the 15k global job cuts as the group does not expect a recovery to pre-crisis levels until 2023. Meanwhile, DAX Sept futures fell below a support level at 12,220 upon resumption of trade. Sectors are also mixed with no clear risk-tone to be derived; energy outpaces amid gains in the complex. In terms of individual movers, Wirecard (-26%) offices are said to be raided by investigators in relation to the deepening scandal, whilst sources noted that any sale of its subsidiaries needs to happen in weeks, which came after reports that chime with some last week regarding interests over parts of Wirecard. Sainsbury’s (-1.4%) failed to garner much traction despite noting that Q2 will mark the 11th consecutive quarter of strong double-digit online growth. Hammerson (-0.4%) is propped up after it announced steps to increase the covenant headroom and improve liquidity.

Top European News

Euro-Area Manufacturing Stems Its Slump With Jobs at Risk

Putin Set for Big Win in Vote That May Extend His Rule to 2036

Fighting Italy’s Next Crisis Means Enlisting Citizen Help

German Watchdog Faces Wirecard Grilling From Lawmakers

In FX, the SEK was not the biggest G10 mover, but in focus at the start of the new month given additional policy stimulus from the Riksbank in the form of an expanded and extended asset purchase remit and lower bank financing rates. However, the Bank left the benchmark repo unchanged as expected and its projected path steady at zero percent right through to Q3 2023 despite reiterating a ‘willingness’ to ease if necessary, although the fact that it opted to implement more QE rather than loosen conventional monetary policy indicates otherwise. Hence, Eur/Sek has remained relatively stable within a circa 10.4450-4870 range.

JPY – The major outperformer, or at least extending its recovery from yesterday’s late lows to revisit offers and resistance vs the Dollar around 107.50, irrespective of a disappointing Tankan survey overnight and pretty downbeat comments from the BoJ. The Yen may have regained an element of safe-haven demand due to renewed unrest in Hong Kong just a day after China officially implemented its new National Security legislation.

NZD/CAD/AUD – All firmer against their US counterpart as the DXY labours between tight 97.482-220 parameters well below Tuesday’s highs ahead of ADP jobs data, ISM manufacturing, construction spending and FOMC minutes. The Kiwi is pivoting 0.6450 where 1bn option expiries reside, the Loonie is meandering between 1.3586-46 and gleaning underlying support from firm crude prices, while the Aussie is clinging to the 0.6900 handle amidst conflicting drivers via another encouraging Chinese PMI in contrast to concerns over the situation in Melbourne caused by COVID-19.

GBP/CHF/EUR – Somewhat contrasting fortunes for the Pound, Franc and Euro, as Sterling straddles 1.2400 following a fleeting venture above the round number as stops were tripped in Cable around 1.2403, but Usd/Chf bouncing ahead of 0.9450 following a deeper sub-50 Swiss manufacturing PMI and Eur/Usd running into supply just shy of 1.1250 even though Eurozone manufacturing surveys were broadly firm, German retail sales smashed consensus and unemployment was not as bad as forecast. Perhaps the single currency is conscious about recent failed approaches towards 1.1300 and decent option expiry interest at 1.1270-75 (1.9 bn), not to mention the fact that it breached technical support at 1.1205 (100 WMA) yesterday on the way down through 1.1200 to 1.1191.

FIXED Bonds are extending losses in wake of another weak UK DMO auction that bucks the broad trend seen since funding requirements initially ballooned due to COVID-19 fiscal support. The 10 year UK benchmark has now been down to 136.96 (-68 ticks on the day), but still not as feeble as Bunds and the Eurozone semi-core that have succumbed to even more intense selling pressure since returning from their unscheduled Eurex break. Indeed, the 10-year German future is heading for a full point fall at 175.60 vs its previous 176.52 close, with French OATs not that far behind. Similarly, US Treasuries are feeling the weight of heavier bear-steepening impulses awaiting ADP, manufacturing ISM, construction spending and FOMC minutes.

In commodities, a session of solid gains thus far for the oil complex as WTI and Brent front month futures continue to feed off the substantially deeper-than-expected draw in Private Inventory Data (-8.2mln barrels vs. Exp. -0.7mln barrels), whilst the Iraqi total oil exports average decline markedly MM (2.8mln BPD vs. Prev. 3.44mln BPD); alluding to an improvement in compliance with the OPEC+ pact. WTI had extended on gains towards USD 40.50/bbl (vs. low 39.50/bbl) while its Brent Sep counterpart gains a footing over USD 42.50/bbl (low 41.55/bbl). Looking ahead, participants will be eyeing the weekly DoE’s in the absence of fresh macro news flow and ahead of the FOMC minutes. Elsewhere spot gold have given up recent gains to test 1780/oz to the downside albeit remains close to fresh 8yr highs amid safe-haven demand as COVID-19 cases resurface globally, with technicians eyeing 1789/oz for potential resistance (high 1788/oz). Shanghai copper meanwhile rose to its highest level in over five months amid rate cut hopes by the PBoC and better-than-forecast Chinese Caixin Manufacturing PMI. Finally, steel futures drifted lower with Shanghai rebar and hot-rolled coils prices declining amid seasonal demand drops.

US Event Calendar

7am: MBA Mortgage Applications -1.8%, prior -8.7%

7:30am: Challenger Job Cuts YoY, prior 577.8%

8:15am: ADP Employment Change, est. 2.9m, prior -2.76m

9:45am: Markit US Manufacturing PMI, est. 49.6, prior 49.6

10am: ISM Manufacturing, est. 49.7, prior 43.1

10am: Construction Spending MoM, est. 1.0%, prior -2.9%;

2pm: FOMC Meeting Minutes

Wards Total Vehicle Sales, est. 13m, prior 12.2m

DB’s Jim Reid concludes the overnight wrap

I’ve got my first parents evening of my life today and in keeping with the new world it’s going to be via Zoom. My father used parents evenings to suggest that I should be top of the class in everything and that if I wasn’t it was the teacher’s failings not mine. He meant well and was deadly serious but it was incredibly embarrassing for me, my mum and was sadly and wildly misinformed. I’ve vowed to not follow in his footsteps on this front but who knows whether those competitive juices will flow when I’m told that little Maisie is mid-table at something.

There was nothing mid-table about Q2 performance in markets. This morning we start the second half of the year and over the next hour we’ll publish our June, H1 and Q2 performance review. Q2 was the best quarter for many assets for a few decades. So watch out for the note from Henry. H2 starts with PMIs this morning so watch out for these.

We’ve also published our H2 outlook for credit this morning (link here) where we see a bright Q3 but potential for the gains to be given up in Q4. There has been more two-way price action in credit over the last month with the recent rise in covid-19 cases in several US states impacting confidence. It’s too early to make firm conclusions but there is some evidence to suggest that they aren’t picking up anywhere near as high as they did across the globe in March and April. So while the rising case numbers will stall US re-openings and impact short-term economic activity and market sentiment, it could at least give us some confidence that we are treating the virus better and that the demographics of who is getting infected are changing for the better. As such there could be a medium-term silver lining to these worrying new case developments. A spike in fatalities soon will be a big negative though as the US will be back closer to square one in terms of the public health element of this crisis. For now this is not our base case scenario but this will unfold relatively quickly.

The view is that there’s enough pent-up economic demand to keep Q3 a positive one for economies and risk assets. We think credit is following equities again since the Fed became the buyer of last resort and positioning is light in equities which helps the technicals of all risk assets. So we expect tighter spreads in Q3.

However by Q4 economies will hit a limit well below pre-covid levels as social distancing prevents normality. At the same time a northern hemisphere winter will likely lead to a more indoor life, more caution, and fears over a resurgence of the virus. So at this stage we think you’ll see a reversal of Q3’s gains. In the note we highlight our short-term recommendations.

As a turbulent first half of the year came to a close, negative newsflow on the coronavirus continued but risk assets fought through the gloom and ended the day on a strong footing with the S&P 500 +1.54% and ending the quarter up +18.70% on a total return basis – the best since Q4 1998. This comes after Q1 was the worst since Q4 2008. More on markets later but in terms of the latest virus developments, the US continued to be the main source of bad news, with Texas announcing a further expansion of its ban on elective surgery to save capacity, while New York added 8 new states to its list from which arrivals would need to quarantine for 2 weeks. Meanwhile in Florida, cases rose by a further 4.2% (versus 3.7% the day before), with Dr Fauci saying that he was “quite concerned” about the rising caseload in a number of states. Arizona saw cases rise 6.3% over a two-day period (they had data issues yesterday on lab results) but with the average of those two days below the 5.0% average seen in the week prior. Notably, the Arizona Governor has closed bars, gyms, movie theaters, and water parks for the next month, citing the need to “relieve stress on our health care system and give time for new transmissions to slow.” Also yesterday, the United Auto Workers union in Texas asked GM to temporarily close its large-SUV plant in the Arlington after the daily average of new cases recently passed 5000 per day, further highlighting how the uncontained spread is having economic effects.

In a sign that this concern about the US is gaining traction internationally, the EU extended its travel ban for US residents. Puerto Rico, a U.S. commonwealth and heavily reliant on tourism, is also now requiring travellers to show evidence of a negative Covid-19 test or submit to a two-week quarantine.

We would again stress that there is still no sign of fatalities gathering much momentum in these troubled US states though. Arizona is the worst on this measure but still well behind the trends seen elsewhere in the first wave. A crucial few days awaits though but one that could start to change the way we collectively think about the virus.

Back to markets and tech stocks led the advance in equities yesterday, with the NASDAQ up +1.87% (+12.67% YTD and +30.95% in Q2 alone). Energy stocks were the best performing S&P sector on the day as Saudi crude exports for June fell to 5.7mln barrels a day, the lowest since Bloomberg began tracking the data at the start of 2017. Even still, oil prices moved marginally lower on the day, with WTI down -1.08% and Brent down -1.34%. As with US equities it was a particularly strong quarter for crude prices, with Brent rallying +80.96%, the most since Q3 1990.

Over in Europe, indices closed lower for the most part missing the late US rally, with the FTSE 100 (-0.90%) and the CAC (-0.19%) both losing ground. However a strong performance from German stocks, where the DAX rose +0.64%, helped the Stoxx 600 to eke out a +0.13% gain. In particular it was technology stocks outperforming in both the Stoxx 600 (+1.24%) and DAX (+1.79) that caused the indices to remain above water.

In response to the US rally, Treasury yields climbed +3.3bps to 0.656. In Europe there was a divergent performance between core and periphery, with 10yr bund yields +1.6bps, whereas peripheral yields including those on Italian (-4.0bps) and Greek (-4.9bps) debt fell. Finally in commodity markets gold set new records as it closed up +0.46% at a fresh 7-year high, and copper similarly continued to climb, rising +1.27% to a fresh 5-month high. As you’ll see in our performance review Gold is the leading asset class YTD and is up around 17.38%.

The majority of Asian markets have started Q3 on the front foot with the Shanghai Comp (+0.91%), Kospi (+0.88%) and ASX (+0.59%) all up. The exception is the Nikkei (-0.20%) while Hong Kong is closed for a holiday. In FX, the Japanese yen is up +0.27%. Meanwhile, yields on 10y USTs are up +2.4bps and futures on the S&P 500 are down -0.19% as we type. In commodities, oil prices are up c.1% and spot gold prices are up +0.19%.

Overnight, China’s Caixin June manufacturing PMI showed steady improvement, printing at 51.2 (vs. 50.5 expected and 50.7 last month). Japan’s final manufacturing PMI reading also got revised up to 40.1 from 37.8 in the flash. Other manufacturing PMI readings in the region also improved with Australia printing at 51.2 (vs. 49.8 in flash), Vietnam at 51.1 (vs. 42.7 last month), Taiwan at 46.2 (vs. 41.9 last month) and South Korea at 43.4 (vs. 41.3 last month). It’s worth noting however that while the trend is positive, the majority of PMIs are still below their pre-Covid levels.

In other news, Hong Kong’s new security law came has come into force and City’s Chief Executive Carrie Lam reiterated that the law wouldn’t impact Hong Kong’s high degree of autonomy or judicial independence. Yesterday UK PM Johnson said that he was “deeply concerned” about the law, and Australia said it was “troubled”, while the Trump administration has vowed “strong actions”.

In other news, Fed Chair Powell and Treasury Secretary Mnuchin appeared before the House Financial Services Committee yesterday. Chair Powell stressed the need to keep the virus at bay for the US recovery to take hold, while also noting that the bounce back in economic activity is “sooner than expected.” The Fed chair indicated that, a “full recovery is unlikely until people are confident that it is safe to re-engage in a broad range of activities.” The question remains if that is before a vaccine is delivered. Secretary Mnuchin said that it was the administration’s goal to get another round of fiscal stimulus done by the end of July, while not indicating if it would be based off the $3.5trn bill that was passed by the House in May. Senate Majority Leader McConnell called that bill a non-starter and that his caucus would draft a bill, with Bloomberg reporting that Republicans want to keep the overall cost under one trillion.

Here in the UK, Prime Minister Johnson confirmed yesterday that there would be no return to the type of austerity we saw in 2010 as the UK seeks to recover from the economic effects of the pandemic. Nevertheless, our UK economist Sanjay Raja writes (link here) that while austerity in its previous form is not an option, there won’t be any blank cheques either, with Chancellor Sunak already having noted that the bar for state bailouts is “very high”. Finally on the UK, it’s worth noting some comments from the BoE’s chief economist Haldane (who was the only one of the MPC not to vote for further QE at the last meeting), who said that since the May meeting, “positive news on demand has, in my opinion, more than counterbalanced the rise in downside risks to employment.”

Looking at yesterday’s data, the main highlight was the flash estimate of Euro Area CPI, which rose to +0.3% in June (vs. +0.2% expected). Core CPI fell by a tenth to 0.8% however, it’s lowest in over a year. With the higher-than-expected inflation, market expectations also rose, with five-year forward five-year inflation swaps for the Euro Area at 1.12%, their highest level since early March.

In terms of other data, the contraction in the UK’s Q1 GDP was revised to show a larger -2.2% fall (vs. 2.0% previously). Meanwhile French inflation in June fell to a 4-year low of +0.1% (vs. +0.5% expected), while the Italian reading sunk into deflationary territory with a -0.4% reading that also marked a 4-year low. On the other side of the Atlantic, Canadian GDP fell by -11.6% month-on-month in April. And in the US, we got the MNI Chicago PMI for June, which rose by less than expected to 36.6. However the Conference Board’s consumer confidence indicator from the US rose to a stronger-than-expected 98.1 (vs. 91.5 expected), and the expectations reading was also up to a 4-month high of 106.0.

To the day ahead now, and the highlight will likely be the manufacturing PMIs for June, along with the ISM manufacturing index from the US. Otherwise, from Germany there’ll be May’s retail sales as well as the unemployment report for June, while in the US there’ll also be June’s ADP employment report and May’s construction spending. From central banks, we’ll get the FOMC minutes from their June meeting, along with remarks from the Fed’s Evans, the ECB’s Panetta and the BoE’s Haskel. Finally, Germany will today take over the rotating presidency of the EU, while the USMCA trade agreement will come into effect.

via ZeroHedge News https://ift.tt/31AtHPE Tyler Durden

European Stock Markets Suffer 3 Hour Outage Due To “Technical Issue” Tyler Durden

Wed, 07/01/2020 – 07:34

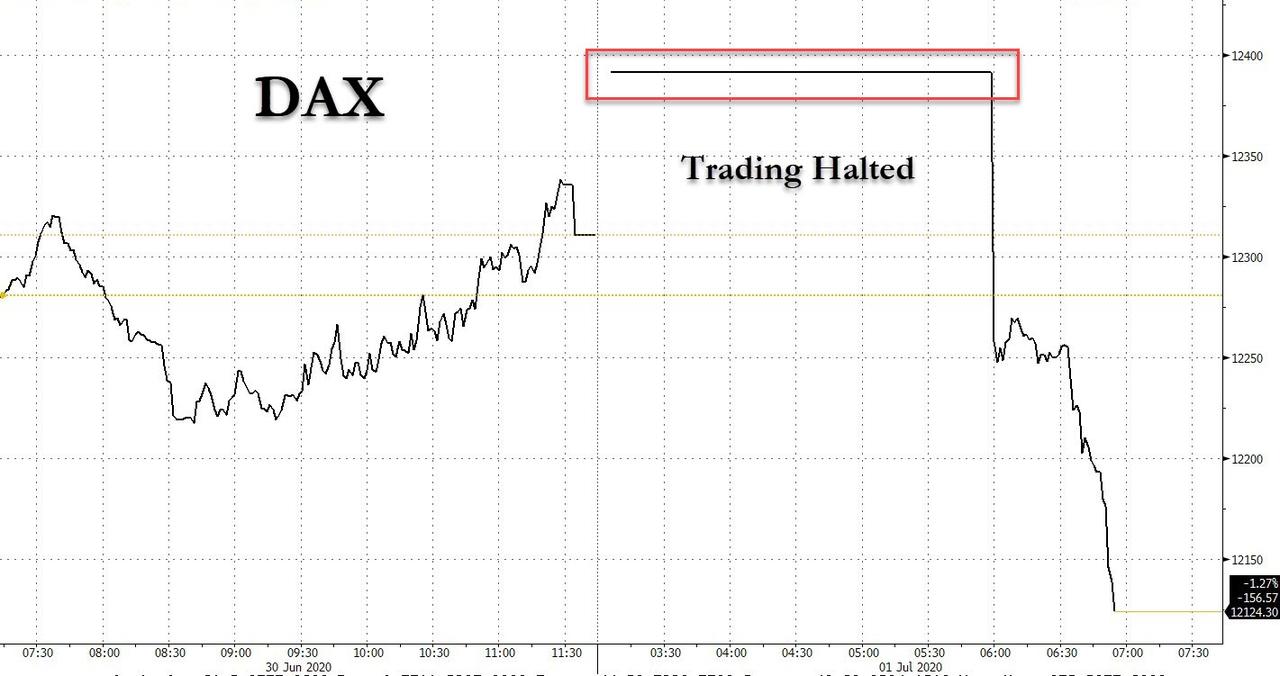

Trading in Germany’s main index DAX and various other European cash and futures exchanges was halted for nearly three hours on Wednesday due to a “technical issue” at German electronic trading platform Xetra. The interruption in the fully-electronic cash market trading system affected stock exchanges in Frankfurt, Vienna, Ljubljana, Prague, Budapest, Zagreb, Malta and Sofia as they use the Xetra T7 system, exchange operator Deutsche Boerse said.

Xetra’s T7 system for cash stock trading was unavailable starting around 847am CET, the exchange operator says on its website. Trading of derivatives on Deutsche Boerse’s Eurex also faced technical difficulties, and only about 30 of 99 stocks on Germany’s HDAX large and mid-cap index were showing trades as of open of trading in Frankfurt.

“Due to technical problems, the Eurex T7 system is not available at the moment. We are investigating and will keep you informed,” Eurex noted on its website. However, alternative exchanges like the Tradegate Exchange in Berlin were functioning properly.

The chart below show the nearly 3 hour long trading halte in the cash DAX, which tumbled as soon as trading resumed.

The technical snag was a further blow to Deutsche Boerse, which saw one of its longest outages in April when the Frankfurt stock exchange was halted for more than four hours.

As Reuters reports, Deutsche Boerse CEO Theodor Weimer said after the April blackout that the stock exchange had taken precautions to avoid such a breakdown in the future. Just two months later, it was followed by another 3-hour-long halt.

Exchanges slowly came back online around 0930 GMT, but the cause of the disruption in Xetra on Wednesday was not immediately clear. The DAX eventually reopened just around 1145am CEST.

The German stock exchange’s cash markets generated a turnover of 159.8 billion euros ($179.5 billion) in May. Some European bond and stocks futures affected by the Xetra issue also resumed trading.

via ZeroHedge News https://ift.tt/3gcNA3p Tyler Durden

Munich Prosecutors Raid Wirecard Offices As Probe Into $2BN Accounting Fraud Heats Up Tyler Durden

Wed, 07/01/2020 – 07:16

The German leadership has already scapegoated an industry group, the Financial Reporting Enforcement Panel, over the Wirecard disaster in the hope that the appearance of reform might be enough to placate Brussels and ESMA after Germany’s most powerful financial regulator, BaFin, was exposed as virtually complicit in the biggest corporate accounting fraud in the country’s post-war history.

But as prosecutors continue to build their case and demonstrate to the German public (and the world, and most importantly Brussels) that they’re taking the Wirecard investigation extremely seriously, officers stormed several offices belonging to Wirecard, including the company’s headquarters.

Munich prosecutors and police searched Wirecard’s headquarters and four further properties as part of a fraud probe following the arrest of the payments firm’s former chief executive, Markus Braun, prosecutors said on Wednesday.

Twelve prosecutors and 33 police officers were involved in the raids to investigate suspected fraud, including market manipulation, prosecutors said.

A spokeswoman told Reuters that prosecutors were investigating board members Alexander von Knoop and Susanne Steidl, as well as Braun and former director Jan Marsalek. Those people could not be immediately reached for comment.

Wirecard CEO/mastermind Markus Braun, meanwhile, remains out on bail.

via ZeroHedge News https://ift.tt/3f19ciM Tyler Durden

First Arrests Made Under New Hong Kong “National Security” Law As Thousands Flood The Streets In Protest Tyler Durden

Wed, 07/01/2020 – 06:50

At least two people were arrested Wednesday as Hong Kong protesters, undaunted by the new penalties they might face, clashed with police, with some proudly carrying the flag of Hong Kong independence despite the tremendous personal risks: Under the new security law, brandishing pro-independence material could lead to arrest and prosecution with stiff prison sentences.

One day after President Xi signed the new National Security law, officially overriding part of the Hong Kong Basic Law via a loophole in the quasi-constitution left behind by the British, Hong Kongers are on the edge of open revolt, as the drop in COVID-19 cases has emboldened more to return to the streets, despite the legal risks.

Police used intense crowd-control methods like water cannons, cordons and pepper spray to keep marchers off the main local road between the shopping district of Causeway Bay and central Hong Kong. Instead, tens of thousands of marchers took to secondary streets. Unlike past protests, few carried signs or banners or coordinated their outfits in black. Though at least one of those arrested was booked for carrying the flag, a serious offense as we mentioned above.

Chanting was mostly limited, although the forbidden call of “Revolution of our times” echoed from the open plaza crossing under the Times Square shopping mall as more young people poured out from a subway exit to join the protest, according to a report from Nikkei Asian Review.

Hong Kong police, who have been more than willing to kowtow to Beijing’s every demand tied to the law, have already formed a special unit to enforce “national security” offenses, according to a statement from the police chief. That’s bad news for the two people arrested during the march, one of whom was touting the independence flag, as we noted above (according to Nikkei).

One of the more terrifying features of the new law is the possibility that ‘national security’ offenders might be prosecuted by mainland courts, where any semblance of the civil liberties enjoyed in Hong Kong would vanish. Chinese leaders have insisted that these types of cases would be extremely rare.

Despite the government of HK citing the pandemic as an excuse to ban the protest, pro-democracy lawmakers urged people to take to the streets in protest despite the police interference.

Citing coronavirus restrictions, city authorities prohibited the annual protest that was arranged by the Civil Human Rights Front, the organizer of last year’s massive rallies. But pro-democracy lawmakers and activists have urged people to defy the ban and take to the streets.

During the protest, journalists were attacked by police in the chaos.

HK Chief Executive Carrie Lam, who was installed by Beijing, spoke at a flag-raising ceremony on Wednesday morning where she proclaimed that the new law is “the most important milestone to strengthen the ‘one country, two systems’ framework.”

“The legislation will protect the majority of people who abide by the laws,” Lam said. “It’s a turning point for Hong Kong to restore stability.”

Pro-democracy lawmakers, along with Secretary of State Mike Pompeo and British Foreign Secretary Dominic Raab, have slammed the law as bringing about the death of “one country, two systems”. Raab vowed to take action to protect the people of Hong Kong, to whom Britain made a commitment to protect when it agreed to return the territory to Chinese control.

Even the leaders of the pro-democracy opposition in Hong Kong say they weren’t allowed to see the text of the law until after it had been enacted. Many in Hong Kong still aren’t 100% aware of the laws exact strictures, which is the very definition of China’s system of “rule by law” instead of “rule of law”.

Say what you want about Hong Kong, for decades, it has been one of the few reliable jurisdictions in Asia where individuals could sue the government and stand a chance of winning. That westernized commitment to fairness (which, as we’ve learned via the trails and travails of Carlos Ghosn, doesn’t exist even in Japan) was what helped transform HK into China’s “gateway” to the west.

But now, Beijing clearly sees Hong Kong’s restiveness as too big of a risk; and so the former golden goose is being slaughtered.

And while the protests rage, ordinary Hong Kongers are scrambling to remove protest signs from businesses and scrub social media profiles, and even text messages.

i was walking around mong kok and came across a depressing scene of this Hong Kong diner removing protest art and signs stuck to the outside just hours after the national security law passed, HK’s freedoms are dying in real time pic.twitter.com/hoBpEmGo1S

That fear, a sense of foreboding that even innocent actions might elicit disastrous consequences, has become an unsettling new feature of life in Hong Kong.

via ZeroHedge News https://ift.tt/2Zl016o Tyler Durden