Portland Police Declare “Riot,” Use Smoke Grenades, Pepper Balls As Violence Flares Up Tyler Durden

Tue, 09/01/2020 – 09:20

Police in Portland declared a “riot” Monday night as protests flared up outside Portland Mayor Ted Wheeler’s residence at a condominium complex in the downtown area, complete with fireworks and other loud, disruptive activities.

The Oregonian reported at least 200 demonstrators “marched to the Pearl District condominium tower where Portland Mayor Ted Wheeler lives to demand his resignation.”

The local newspaper said, “demonstration quickly turned destructive as some in the crowd lit a fire in the street, then placed a picnic table from a nearby business on top of the fire to feed the blaze. People shattered windows and broke into a ground-floor dental office, including a chair, and added to the fire and office supplies.”

Allison Mechanic, a reporter for KATU News, posted a series of videos on Twitter showing police tackling demonstrators and other scenes of generalized chaos.

— Portland Independent Documentarians (@PDocumentarians) September 1, 2020

Earlier in the night in Portland, antifa rioters calmly smashed up a random business to protest police & @tedwheeler. They stole furniture from inside to use as tinder for their fire. They then set the office’s lobby on fire. #PortlandsRiotspic.twitter.com/b7rNvAEqNn

“This was the arson fire that prompted a riot declaration tonight,” the Portland Police said on Twitter while quoting a video from The New York Times reporter. “It was critical to secure the area to allow firefighters to respond to this dangerous situation.”

This was the arson fire that prompted a riot declaration tonight. It was critical to secure the area to allow firefighters to respond to this dangerous situation. https://t.co/k33vcLD4BY

Wheeler has been targeted by several civil rights groups demanding his resignation. The mayor has come out in the last couple of days and said he has no plans to do so, placing blame on the Trump administration for the violence.

Trump has deployed federal forces to the imploding Democratically-controlled city. The president has criticized leaders of these cities and towns, such as ones in Portland, Chicago, and New York City, as unrest continues into late summer and violent crime surges.

Trump has surged in the polls following the Republican National Convention, while enthusiasm for Joe Biden and Democrats slips.

Trump has made it a focal point of his presidential campaign, ahead of the Nov. 3 elections, to bash Democrats for inciting violence across major metro areas. This has given the president a boost in the polls.

via ZeroHedge News https://ift.tt/31N4cdC Tyler Durden

“A Classic Feedback Loop”: Why Everyone Is Chasing The “Gamma Crash Up” Tyler Durden

Tue, 09/01/2020 – 08:54

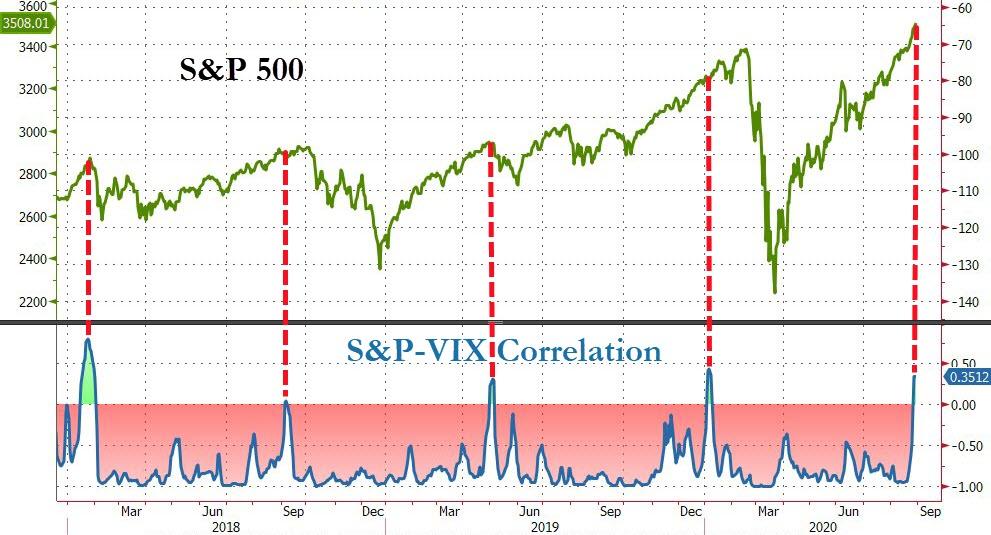

On Saturday, when we published our lengthy compendium of bizarro market charts showing the paradoxical melt up in both risk assets and the VIX, leading to the most positive correlation between the S&P and the VIX since the Feb 2018 Volmageddon event…

… we said that “one reason why no conventional indicator seem to matter is because it now appears that gamma has become a primary driver in the market’s latest meltup.”

One day later, when we showed that the VIX is now at the highest level at a a new all time high in the S&P since March 2000, i.e., the day the do com bubble burst…

… it was the world’s most important “market maker” (or taker as some may joke), Citadel that laid out its own take on this unprecedented “gamma grab”. For those who missed it, this is what Citadel said:

Over the past few weeks, there has been a massive buyer in the market of Technology upside calls and call spreads across a basket of names including ADBE, AMZN, FB, CRM, MSFT, GOOGL, and NFLX. Over $1 billion of premium was spent and upwards of $20 billion in notional through strike – this is arguably some of the largest single stock-flow we’ve seen in years. “The average daily options contracts traded in NDX stocks to rise from ~4mm/day average in April to ~5.5mm/day average in August (a 38% jump in volume).

Given this group of 7 stocks accounts for a ~40% weighting in the NDX, the outsized volatility buying in the single names is having an impact at the Index level. So why are Vols moving Wednesday and Thursday when this call buying has been taking place for weeks? Yesterday CRM, one of the names we have seen outsized flow, rallied 26% on earnings – a less than ideal outcome for those short volatility from all the call buying.

As the street got trapped being short vol, other names in the basket saw 3-4 standard deviation moves higher as well – on Wednesday FB rallied 8% (a 3 standard deviation move), NFLX rallied 11% (a 4 standard deviation move), and ADBE rallied 9% (a 3 standard deviation move).

The most natural place to hedge being short single name Tech volatility is through buying NDX volatility. As such, there has been a flood of NDX volatility buyers with NDX vols up about 4 vol points in 2 trading days. And if NDX volatility is going up, SPX volatility/VIX will eventually go up too.”

Of course, if gamma is discussed Charlie McElligott can’t be far behind, and in a note this morning, the Nomura cross-asset strategist echoes what we said about this underlying reflexive beast that is propelling the market higher, saying that Gamma hedging has become “the most important flow in the market, with the convexity of said short-dated “lottery ticket” options creating an ‘all-or-nothing’ binary-options market behavior into weekly expiries, seen in these increasingly exponential ramps in names like TSLA.”

In his explanation of the “spot up, vol up” moves seen across major indices, McElligott repeats what we explained over the weekend, saying “it’s as simple as this: Street-wide, Dealers are short Gamma / short Calls off the back of the MASSIVE upside premium buyer (as in BILLIONS spent) who has been in the market over the past month or so in a number of mega-cap single-name Tech cos.”

This, according to McElligott (and Citadel), “is why CRM had its freakish +26% post-EPS single-day move last week (lolwut), and dragged-up a number of other high-profile big name Tech which have also been part of the upside buying program (AMZN, ADBE, NFLX, FB, MSFT) all enormously “over-shooting” thereafter, as generically, the Street was short 1m 20d Calls which turned 25d real quick, forcing Dealers to grab Delta to stay hedged, in classic “tail wags the dog” feedback loop.”

Another way to describe the feedback loop of course is what we said on Sunday: calls spiking higher amid this gamma squeeze, leading to more buying of the underlying stock, leading to even higher call prices, even more call squeezing, even more delta-hedging and buying the underlying, which eventually spills over into more and more of the market, and so on until there is one massive marketwide meltup.

Then there was the added matter that this flow was simply larger than an August illiquid single-name market could take, with McElligott noting that “the hedging of single-names becomes forced lookalike buying in NQ- and likely ES- as well (because it looks relatively “cheap”)—spot up, vol up, as this “upside-crash” has to be hedged.”

As a result, we are now also seeing the VVIX exploding higher (+9vols yday!) “as market makers are forced into grabbing upside tails, while too, this dynamic is also evidenced by the spread btwn UX1 (front VIX future) as implied vol vs SPX 30d realized vol (so heavily weighted in US Tech) currently stands at 17.5, the most in 10 years.“

* * *

It’s not just the “self-fulfilling” gamma grab flow of course, and at a time when retail traders have become the most improtant marginal price setter (as we explained in May), the larger multi-month theme of “Robinhood-esque” speculative buying in short-dated deep OTM Calls continues to iterate McElligott’s refrain that “Gamma” hedging “is the most important flow in the market, with the convexity of said short-dated “lottery ticket” options creating an “all-or-nothing” binary-options market behavior into weekly expiries, seen in these increasingly exponential ramps in names like TSLA.”

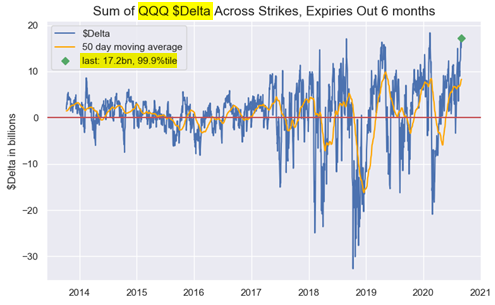

As a result, broad index and ETF options-wise “are as extreme as it gets (QQQ $Delta 99.9%ile, SPX / SPY $Delta 96.9%ile)…

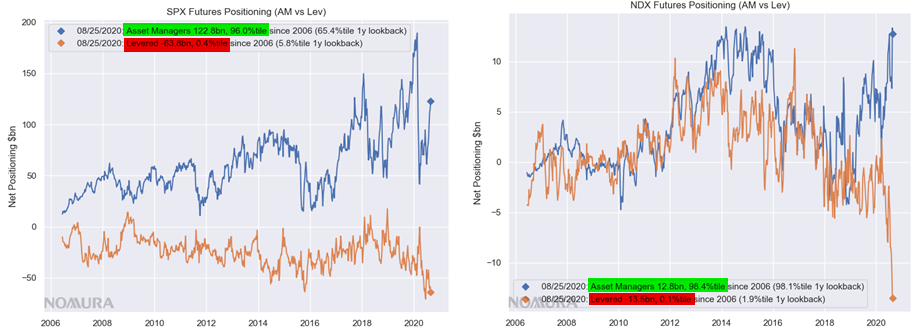

… while too CFTC TFF futures positioning data shows the “Asset Manager” extreme net $long at 98%ile in NQ and 96%ile in ES, while the “Leveraged Fund” net $position is at extreme SHORT (hedging underlying “longs,” of course) with 0.1%ile in NQ and 0.4%ile in ES net positions since 2006.”

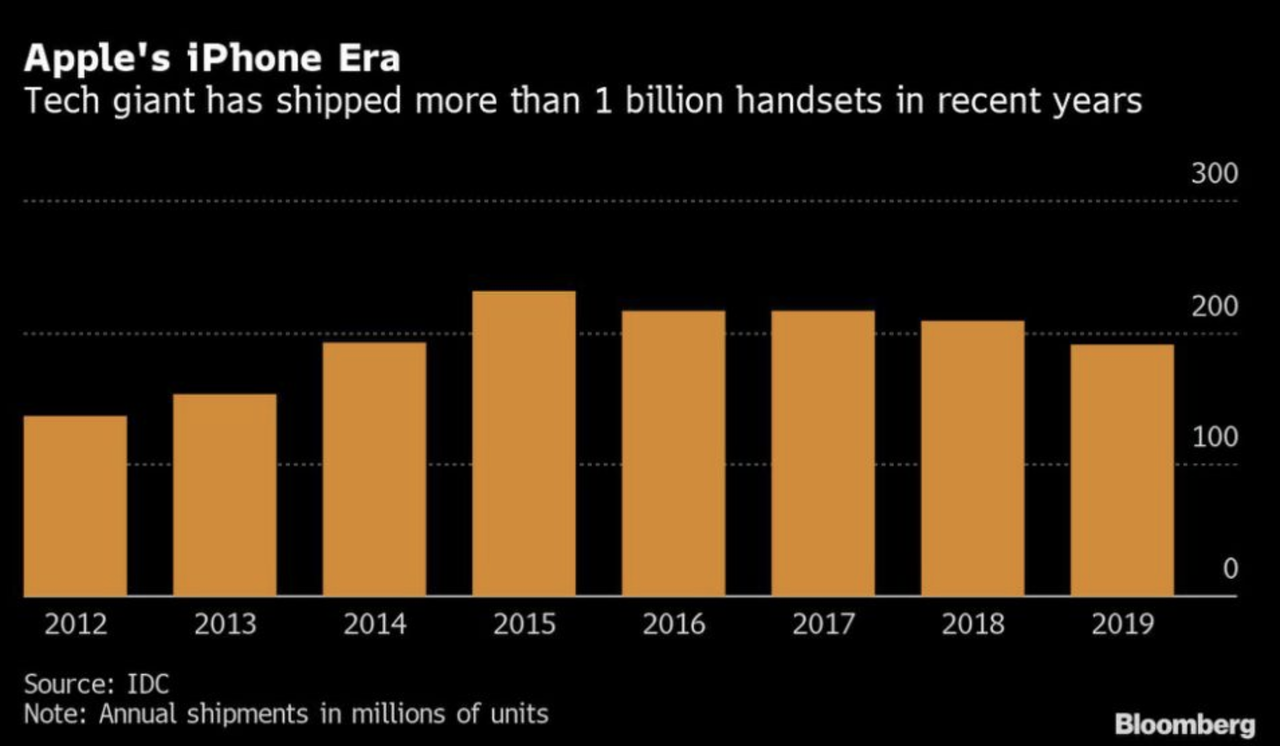

Apple Hopes To Sell 80 Million New ‘5G-Enabled’ iPhones Despite Pandemic Production Delays Tyler Durden

Tue, 09/01/2020 – 08:30

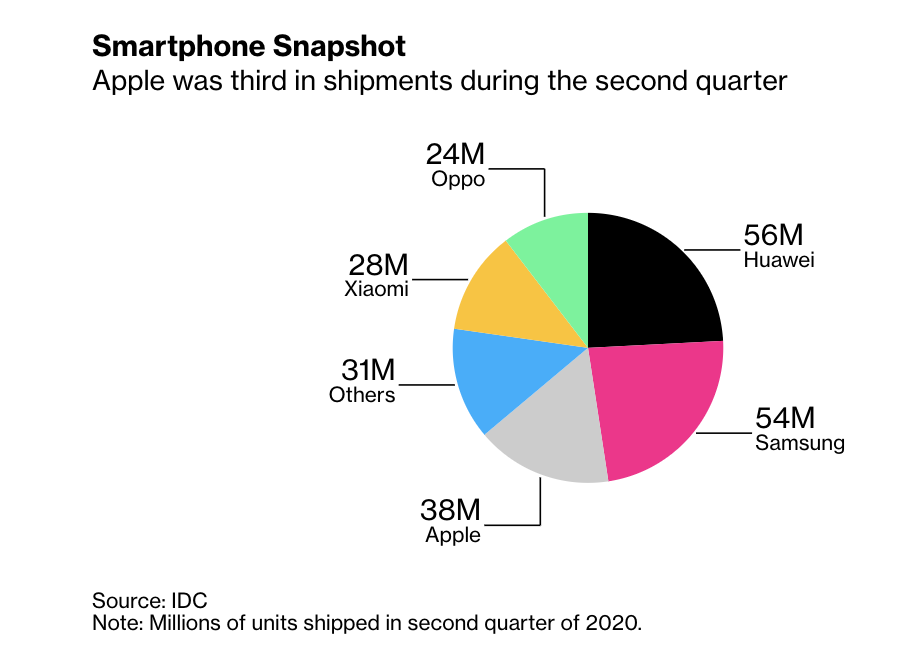

Social media users were quick to lampoon the first leaked images of Apple’s new iPhone 12 series, with some complaining that the new camera array “looks like my stove”. But despite all of the logistical disruptions caused by the SARS-CoV-2 pandemic, Apple is apparently still planning to roll out its first batch of 5G-compatible phones and devices.

One day after Apple’s shares powered higher on Monday following a 4-for-1 stock split, the company’s comms department has strategically leaked details about its upcoming product slate to Bloomberg. And just like that, all those jokes about “trypophobia” have been immediately forgotten, as consumers focus on several key product offerings, including a new generation of air pods, and a new set of lower-end Apple Watches – a surprise smash hit in the company’s product line – intended to compete with FitBit.

While Wall Street analysts question the notion that the rollout of 5G will create a new smartphone-sales ‘supercycle’, Apple is going all-in, reportedly ordering 75 million 5G iPhones to be shipped during the 2020 holiday shopping system. Apple insiders told BBG that the company expects as many as 80 million units, more than they sold during 2019, the year the post-GFC boom peaked – and a year when sales already started to show some weakness, which Apple – to its credit – telegraphed months in advance.

The cheaper iPhone 12 models will launch at an unspecified date in October, followed by the iPhone 12 Pro phones in November. Thanks to production delays caused by COVID-19, the iPhone 12 Pro models will hit stores even later in the season than the iPhone X did in 2017 (the company’s pioneering ‘premium’ phone hit stores on Nov. 3, 2017).

In another bullish indicator, during preparation for the annual production ramp, Foxconn published several notices on WeChat over the past month recruiting workers for its main iPhone campus in the central Chinese city of Zhengzhou.

That’s one reason why Apple CEO Tim Cook has been so determined to promote the company’s services revenue as a key driver for future growth.

Here’s a breakdown of all the new products featured in the latest piece from Bloomberg’s Mark Gurman and Debbie Wu.

Apple plans to mark the official rollout of 5G with four new models of iPhone featuring a heavily updated design and a wider choice of screen sizes. For the first time, the four new phones will be split into two basic and two high-end models: all will feature OLED displays with improved color and clarity. The two regular handsets will come in new 5.4-inch and a 6.1-inch options. The “Pro”-banded phones will offer a choice of 6.1-inch or an enlarged 6.7-inch display, which will be the largest ever on an iPhone. All the new phones will have updated designs featuring squared edges similar to the iPad Pro. The high-end phones will continue to use stainless steel edges versus, while the cheaper phones will feature aluminum sides. The company is also planning a new dark blue color option for the Pro models, which will replace the Midnight Green of 2019’s iPhone 11 Pro line.

As virtual reality becomes more popular, the larger of the new “Pro” phones will feature the same LIDAR camera as on the latest iPad Pro. The new camera will allow augmented-reality apps to have a greater understanding of their surrounding environment. They will also feature an A14 processor, which will improve speed and power efficiency.

As we mentioned earlier, Apple plans to ship the lower-end phones sooner than the Pro devices, which will ship “a few weeks” later than last year’s models, which started shipping Sept. 20.

A smaller, more affordable HomePad model is also being introduced.

A new Apple TV box will feature a faster processor for improved gaming.

Apple is also preparing a new iPad Air with a “Pro-like” screen that will run “edge to edge” on the tablet. According to BGR, a recent leak showed the unreleased table will feature a Touch ID button embedded in the home button.

The company is launching two new Apple Watch models. The new lineup will include a successor to the popular Apple Watch Series 5, and a new model to replace the Series 3 which will compete with FitBit and other budget-friendly devices.

Apple will introduce its first over-the-ear model of headphones outside the “Beats” brand.

Finally, Apple is expected to unveil its “AirTags” trackers, which will come with a leather carrying case.

It’s one of the boldest slates of new product offerings we’ve seen from Apple in years. Washington’s decision to crimp Huawei’s access to microchips and processors needed for its popular handsets has effectively knee-capped one of Apple’s biggest international rivals.

But will that be enough to bolster the Cupertino tech giant’s sales at such a delicate time? We’ll need to wait and see.

via ZeroHedge News https://ift.tt/2Dhm9Yg Tyler Durden

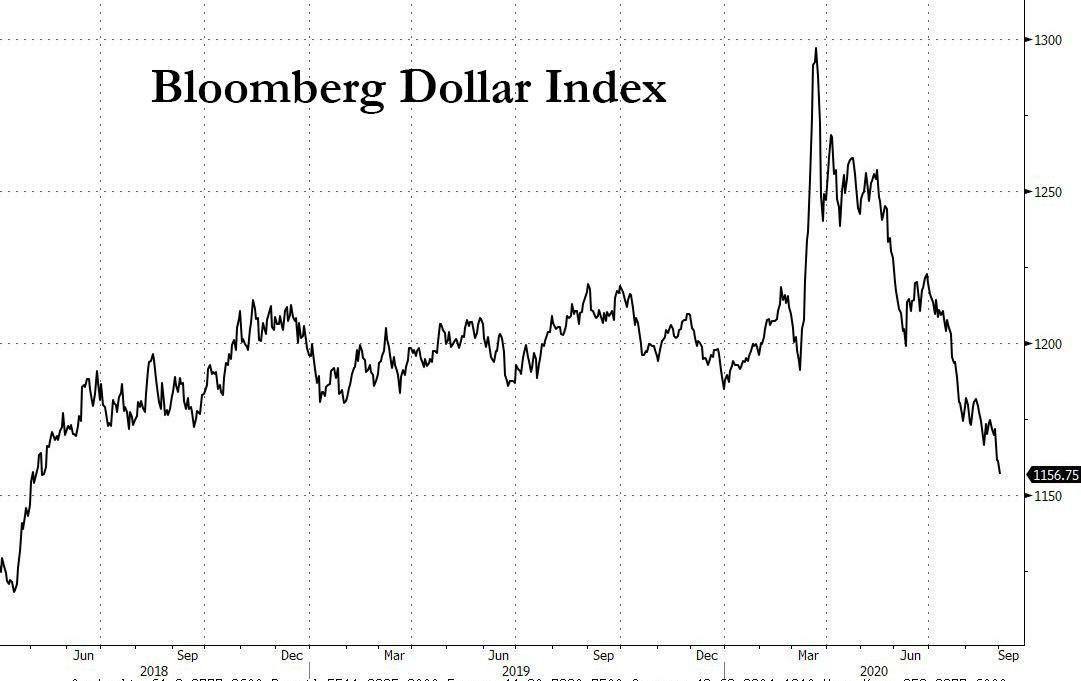

Futures Coiled Near All Time High As Dollar Tumbles To Fresh Two Year Low Tyler Durden

Tue, 09/01/2020 – 08:12

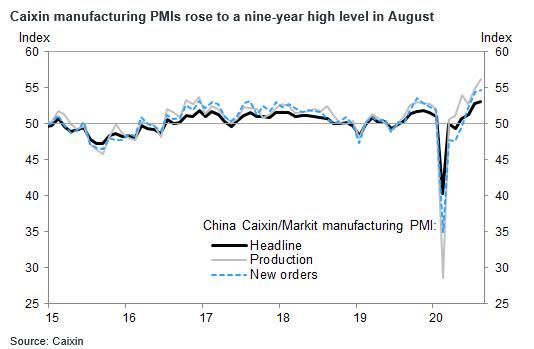

Stocks started September on a positive note on Tuesday, with S&P futures flat after fading earlier gains alongside shares in Europe as global indexes close to all-time highs as data in China and Europe showed manufacturing demand rebounding from coronavirus-induced lows. The dollar tumbled to a two-year low and the Yuan jumped after Chinese manufacturing data indicated that exports are underpinning a recovery.

The MSCI world equity index, which tracks shares in 49 countries, was close to recent highs, while the pan-European Stoxx 600 rose 0.3% in early trading with technology and basic resources climbing the most among sectors. France’s Cac 40 was up 0.2% and Germany’s Dax was up 0.7%. Britain’s FTSE 100 lagged, down 1.4%, hurt by a rising pound. Euro zone manufacturing activity grew last month, though factory managers remained wary about investing and hiring more workers. The French Mfg PMI beat expectations coming at 49.8, above the 49.0 consensus if down from 52.4, while Germany output grew at its fastest pace since February 2018, while in France it contracted.

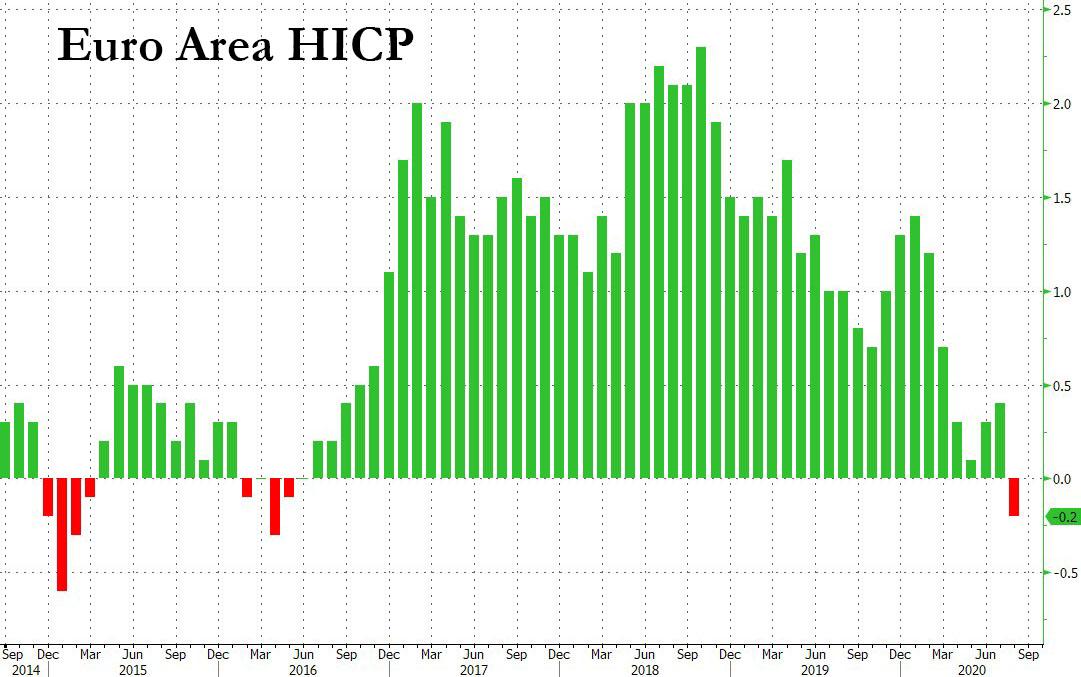

European stocks had opened even higher but pared gains after Germany cut its GDP forecast for 2021. Both shares and the euro, which rose to a two-year high of $1.19975 overnight in New York, were little changed after data showed annual euro zone inflation fell well below expectations in August, turning negative for the first time since May 2016, and a far cry from the European Central Bank’s inflation target of just under 2% (some have mused if the ECB will follow the Fed in announcing AIT as well).

“These numbers are clearly inconsistent with the ECB’s target,” said George Buckley, chief European economist at Nomura, who said the low reading will raise questions about whether the ECB should, like the Fed, adopt average inflation targeting. There were however credibility issues with such an approach, if the bank was unable to raise inflation to balance out the periods of lower inflation.

In Asia, China’s yuan touched the highest since 2019 and equities benchmarks in Hong Kong, Shanghai, Taipei and Seoul climbed. The Caixin PMI survey of China’s factory activity rose at the fastest pace in August since January 2011, helped by improving exports and continued domestic recovery, and boosted market sentiment overnight and into the European market open.

In rates, 10Y yields rose to 0.72% , up 2bps on the day with treasuries trading heavy led by the long end as month-end bid unwound. Yields were cheaper by up to 3bp at long end of the curve, steepening 2s10s, 5s30s by 1.6bp and 2.7bp; 10-year yields around 0.725%, cheaper by 1.8bp vs Monday’s close while gilts lag by ~1.5bp across the sector. Gilts underperformed, weighing on Treasuries along with a sharp selloff in Aussie bonds during Asia session. Core euro zone bond yields were up around 1 to 2 basis points, with the benchmark German 10-year yield at -0.387%.

In FX, the dollar continued to drop to a fresh two-year low and was down 0.4% at 91.826, dropping below 92 for the first time since May 2018 after a purchasing managers index for China beat estimates to raise optimism over Asia’s economic recovery.

“The weakness in the dollar is likely to continue and I suspect it will be substantially weaker from where it is against the euro by the end of the year,” said Savvas Savouri, chief economist at Toscafund Asset Management. “We’ve got the Fed chairman clearly telling us he wants inflation to ratchet upwards, and the only reliable way to achieve this is through the channel of a weaker currency.”

The euro climbed after German unemployment eased for a second month, though gains fell short of reaching $1.20 following the abovementioned deflationary print. At 1025 GMT, the single currency traded at $1.19835, up 0.4% since New York’s close as a dollar sell-off continued. Sterling rose to eight-month highs against the dollar, strengthening to as much as $1.3465 at 1028 GMT, and was up around 0.3% versus the euro.

In commodities, oil prices gained, reversing overnight losses. Brent climbed 56 cents to $45.84 a barrel while WTI futures rose 47 cents to $43.08 a barrel. Gold prices also rose, to their highest in two weeks.

Market Snapshot

S&P 500 futures up 0.3% to 3,510.75

STOXX Europe 600 up 0.2% to 367.28

MXAP up 0.4% to 173.35

MXAPJ up 0.5% to 574.03

Nikkei down 0.01% to 23,138.07

Topix down 0.2% to 1,615.81

Hang Seng Index up 0.03% to 25,184.85

Shanghai Composite up 0.4% to 3,410.61

Sensex up 0.8% to 38,948.09

Australia S&P/ASX 200 down 1.8% to 5,953.41

Kospi up 1% to 2,349.55

German 10Y yield rose 0.9 bps to -0.388%

Euro up 0.3% to $1.1971

Italian 10Y yield rose 5.0 bps to 0.968%

Spanish 10Y yield rose 0.8 bps to 0.417%

Brent futures up 1.2% to $45.82/bbl

Gold spot up 1.1% to $1,989.57

U.S. Dollar Index down 0.3% to 91.91

Top Overnight News from Bloomberg

A private gauge of China’s factory activity grew at the fastest rate in August since January 2011, helped by exports and domestic recovery

Global trade is expected to rebound faster than after the 2008 financial crisis, according to Germany’s Kiel Institute for the World Economy. The number of coronavirus cases approaches 25.5 million worldwide, while deaths surpass 850,000

The euro zone’s inflation rate went negative for the first time since 2016. Meanwhile Germany’s hit from the coronavirus will be less severe than feared, as the government’s efforts to kick start Europe’s largest economy show signs of bearing fruit

A closely-watched euro-area interbank borrowing rate fell to a record, dragged down by all the money sloshing around the economy

A quick look at global markets courtesy of NewsSquawk:

Asian equities traded cautiously as the region took its cue from the losses seen across most global counterparts despite Wall St. notching its biggest monthly gain since April and its best August performance in more than 3 decades, while participants also digested encouraging Chinese Caixin Manufacturing PMI data. ASX 200 (-1.8%) underperformed and briefly wiped out all of the prior month’s gains on a collapse below the 6,000 level with the downturn led by hefty losses in tech and energy, while the detention of a Chinese-Australian television anchor further highlighted the souring bilateral relations with China. Nikkei 225 (-0.1%) was indecisive but with downside stemmed by recent currency weakness and political continuity hopes with Chief Cabinet Secretary Suga said to be supported by the largest faction of the ruling LDP and is set to announce an intention to continue with Abenomics and the pandemic response when declaring his candidacy on Wednesday. Elsewhere, Hang Seng (U/C) and Shanghai Comp. (+0.4%) swung between gains and losses as mild support was seen following the strongest Caixin Manufacturing PMI reading since January 2011, but with upside also capped after the PBoC drained CNY 230bln from the interbank market and due to lingering US-China tensions after White House trade adviser Navarro stated the US will go after others not just TikTok and WeChat. Finally, 10yr JGBs were higher following the recent gains in T-notes and indecisive risk tone in the region, although some of the gains were reversed after all metrics pointed showed weaker results at the 10yr JGB auction.

Top Asian News

Total Enters Giant Korean Floating Wind Projects in Green Push

Samsung’s Heir Jay Y. Lee Indicted in Succession Probe

Supreme Court Approves 10-Year Rescue Plan for Indian Telcos

SoftBank Corp. Is ‘Surprise’ Addition to Japan’s Nikkei 225

Earlier gains across European equities have somewhat faded (Euro Stoxx 50 +0.4%) despite a lack of fresh macro catalysts, with the region now ultimately mixed, whilst losses in UK’s FTSE 100 (-1.3%) persist amid a catch-up play from its long weekend Bank holiday. Sectors performance is also varied with no clear risk profile to be derived: the IT sector outperforms as chip-makers cheer reports that Apple is aiming to launch four new iPhone models next month, with volumes in the 75mln region. Thus, the likes of STMicroelectronics (+1.1%), Dialog Semiconductor (+3.3%), Infineon (+1.2%) remain propped up. On the other side of the spectrum resides Travel & Leisure, alongside Banks and Oil & Gas. In terms of individual movers, Novartis (+3.0%) keeps the healthcare sector afloat on the back of a broker upgrade at Morgan Stanley coupled with an announcement that it has developed new ESG targets in order to ramp up access to medicines and achieve full carbon neutrality. Sticking with the healthcare sector, Sanofi (+0.6%) has largely brushed off its COVID-19 Kevzara vaccine failing to meet primary and key secondary endpoints in its Phase III trials. Meanwhile, AstraZeneca (-0.5%) succumbs to the weakness in the post-bank holiday UK markets but with downside somewhat cushioned by a positive update for its Farxiga, Imfinzi and COVID-19 vaccine deal with Canada. Elsewhere, Shell (-2.0%) and BP (-2.1%) are subdued despite higher oil prices, and with losses more pronounced that its cross-border counterparts amid catch-up play alongside reports UK Chancellor Sunak could increase fuel duty by 5p to help pay for the coronavirus in the Autumn budget.

Top European News

U.K. Manufacturing Output Expands at Fastest Pace in Six Years

European Factories Brace for Economic Rebound to Falter

Russia Passes 1 Million Covid-19 Cases as Epidemic Simmers

German Joblessness Falls Again Amid Revival of Economic Activity

In FX, the Dollar is suffering from a post-month end hangover as the DXY slips to a new 2020 low of 91.741 amidst broad losses vs G10 peers and most EM currencies. Confirmation of a firm US manufacturing PMI via the final release and ISM matching expectations for a pick-up in headline activity could conceivably provide the Greenback some respite, but the index remains toppy on rebounds over 92.000 as buoyant risk sentiment counters renewed bear-steepening along the Treasury curve.

NZD/CAD/GBP/EUR – The major beneficiaries of ongoing Buck weakness as the Kiwi pivots either side of 0.6750 awaiting NZ terms of trade for Q2 and the Loonie extends through the psychological 1.3000 level with some assistance from firm crude oil. Meanwhile, the Pound has scaled another big figure and briefly breached a mid-December 2019 peak (1.3422), as Eur/Gbp unwinds modest RHS demand for the August/September turn from circa 0.8950 towards 0.8900 irrespective of more negative sounding Brexit news (EU chief negotiator Barnier reportedly unwilling to discuss new UK fishing proposals unless Britain compromises on other contentious issues). Elsewhere, the Euro has tested round number resistance at 1.2000 vs the Dollar, but market contacts note heavy offers related to option expiries and on that note 1.1 bn rolling off between 1.1895-1.1900 at today’s NY cut may keep the headline pair supported given little net reaction to mixed Eurozone manufacturing PMIs and even weak, deflationary inflation.

JPY/AUD/CHF – Also firmer against the Greenback, albeit mildly as the Yen hovers midway within a 106.03-105.60 range, the Aussie fades after another 0.7400+ foray and Franc fails to breach 0.9000. For the record, the RBA stuck to the script overnight, though did extend and expand its Term Funding Facility, while July building approvals smashed estimates and the Q2 current account surplus was wider than forecast. However, relations with China are going from bad to worse as barley imports from Australia’s CBH Grain company are suspended.

SCANDI/EM – Not much response to rises in Swedish and Norwegian manufacturing PMIs, but China’s stronger than expected Caixin reading has helped the Yuan appreciate further vs the Dollar in contrast to a decline in the Turkish headline index that is weighing on the already lagging Try.

In commodities, WTI and Brent front month futures continue to ebb higher in early European trade, in what is a continuation of price action seen overnight as a function of the weakening Dollar, whilst the complex also remains underpinned by overall risk sentiment. Aside from that, pertinent news flow has been on the light side, although sources reported that UAE’s ADNOC pumped some 2.693mln BPD of crude in August in order to meet domestic demand – above its quota under the OPEC+ pact. That being said, sources added that the country will compensate for the undercompliance in the months ahead, whilst Iraq submitted a plan to OPEC that proposes additional cuts of 400k BPD in August and September and Kazakhstan plans additional cuts of 95k BPD over the same two-month period, according to sources. Further, Goldman Sachs raised 2020 Brent crude price forecast to USD 43.63/bbl from USD 40.51/bbl and raised 2021 forecast to USD 59.38/bbl from USD 55.63/bbl. WTI October holds its head above USD 43.00/bbl having found an overnight base around USD 42.75/bbl, whilst its Brent counterpart inches higher towards 46/bbl from a low of 45.47/bbl. Elsewhere, the weaker Buck keeps precious metals afloat with spot gold inching higher towards the USD 2000/oz mark (vs. low 1965/oz) whilst spot silver extends gains above USD 28.75/oz (vs. low 28.04/oz). Meanwhile, LME copper prices climbed to levels last seen over two years ago – bolstered by the Chinese Caixin Manufacturing beat coupled with the softer Dollar, whilst Dalian iron ore saw mild gains due to the same factors.

US Event Calendar

9:45am: Markit US Manufacturing PMI, est. 53.6, prior 53.6

10am: ISM Manufacturing, est. 54.8, prior 54.2

10am: Construction Spending MoM, est. 1.0%, prior -0.7%

Wards Total Vehicle Sales, est. 15m, prior 14.5m

DB’s Jim Reid concludes the overnight wrap

Never has the restrictions of social distancing felt so liberating. As of today I can break the shackles of two weeks in quarantine. It’s been tedious, tiresome and ponderous. As least during full lockdown we went out for a nice walk once a day and I had heaps of work to occupy me. Of these past 14 days, 10 were spent on holiday at home (or weekends) and 4 at work in my home office. The latter were infinitely more enjoyable and less stressful for me. Much less for my wife. Every morning the twins repeatedly say “Go Mummy car”. They can’t work out why we don’t go out and are very confused. Hopefully they’ll squeal with delight when they realise their wish is finally going to come true.

So with a dull second half of August behind me we welcome in September today. To mark this we are launching our monthly survey this morning as a back to school special. This month’s includes plenty of questions about life around the virus including some questions on whether you will be first up volunteering to take any vaccine, whether you think they should be compulsory and how your understanding is on the effectiveness of vaccines generally. Also a number of other questions. It only takes 3 mins to fill in and results will come in the days ahead. Here is the link. All help filling in the survey very much appreciated.

This morning Henry is publishing the monthly performance review. It was another good month for risk especially for Silver (+15.39%) and the Nasdaq (+9.59%). It was also the best August for the S&P (+7.01%) since 1986 and the best individual month since April – just after the pandemic lows. See the full review in your inboxes soon for more.

Even with the good month, August ended with the S&P 500 slipping slightly, falling -0.16%, as even large gains in tech stocks were unable to keep the index in the green. Roughly 70% of the index was lower on the day after stocks dipped mid-session on reports of China blocking US companies from buying social media company TikTok. In a story that speaks to the power of retail investing in the current market, Apple and Tesla powered the Nasdaq +0.68% higher to another record after their pre-announced stock splits were enacted. The two stocks added +3.39% and +12.57% of value respectively by just lowering the sticker price.

In Europe with the UK markets closed, the Stoxx 600 fell -0.62% during the last session of August, reversing a gain of as much as +0.7% early in the session. This left the index up +2.86% on the month for its best August performance since 2009. Core sovereign bonds diverged much like equities with US 10yr Treasury yields down -1.6bps to finish at 0.705%, while 10yr Bund yields rose +1.2bps to -0.40%. The dollar resumed its slide as well (-0.25%), falling for the fifth session in a row.

Overnight Asian markets are a little directionless with the Nikkei (-0.07%) and Hang Seng (-0.02%) trading flat while the CSI (+0.12%) and Shanghai Comp (+0.04%) are posting modest advances. The Kospi (+1.06%) is leading the way on news that the government is preparing to boost its 2021 budget by 8.5%. In FX, all G-10 currencies are up (0.2-0.6%) against the greenback with the Euro trading closer to the 1.20 handle at 1.1992. Meanwhile the onshore Chinese yuan is up +0.42% to 6.8202, the highest level in over a year. Futures on the S&P 500 are up +0.11% while those on the Nasdaq are up +0.40%. Elsewhere, crude oil prices are trading up c.1% this morning while gold and silver are up +0.91% and +1.81% respectively.

It’s another round of global PMIs today and we’ve already kicked things off in Asia with China’s Caixin manufacturing PMI printing at 53.1 (vs. 52.5 expected and 52.8 last month), the highest reading since Jan 2011 and further emphasising the China recovery story. Yesterday, we saw China’s official August PMIs with manufacturing printing 0.2pts lower than expectations at 51.0 while services were at 55.2 (vs. 54.2 expected). Back to today and Japan’s final manufacturing PMI reading was confirmed at 47.2 (vs. 46.6 in flash). South Korea also showed an improvement at 48.5 (vs. 46.9 last month) while for Taiwan it was at 52.2 (vs. 50.6 last month), the highest reading in 2 years. However, readings for Vietnam (at 45.7 vs. 47.6 last month) and Australia (at 53.6 vs. 53.9 in flash and 54.0 last month) retreated on account of renewed lockdowns during the past month.

Following the policy framework changes laid out by Fed Chair Powell last week, yesterday Federal Reserve Vice Chair Clarida spoke to the possibility of using Treasury yield caps at some point, but suggested that it is not currently in the plans. He also noted that it is appropriate in many circumstances for inflation to overshoot the 2% goal. Markets also heard from the Fed’s Bostic, who said that he was ‘very worried’ about the drop in fiscal support for economy. Given that several participants argued for more accommodation in July, a lack of fiscal response and further gridlock may cause more committee members to opt for additional easing. With the next FOMC in two weeks this meeting will slowly come into the market’s view.

On the coronavirus, yesterday news came that Paris will now offer free testing at various locations throughout the city in order to identify and contain the spread of infections within the French capital. Cases in the country grew by 35,000 in the last week which is almost as many as seen at the country’s April peak, but there has not yet been a significant change in hospitalisations. The pace of new cases in the US continues to slow even as confirmed cases passed 6 million. Earlier this month New York City mayor said that indoor dining would be closed until June 2021, and then yesterday added that any resumption of indoor dining may hinge on a “huge step forward” such as a vaccine. With no guarantee of an effective or widely administered vaccine and colder months coming, this could lead to lower mobility and business output from the largest US city. Across the other side of world, India is now undoubtedly the global epicenter of the virus with the rise in new cases topping 70k on a daily basis. It also has the third highest fatalities now at 64,469. A reminder that we still publish our daily tables in the full pdf if you click on “view report”.

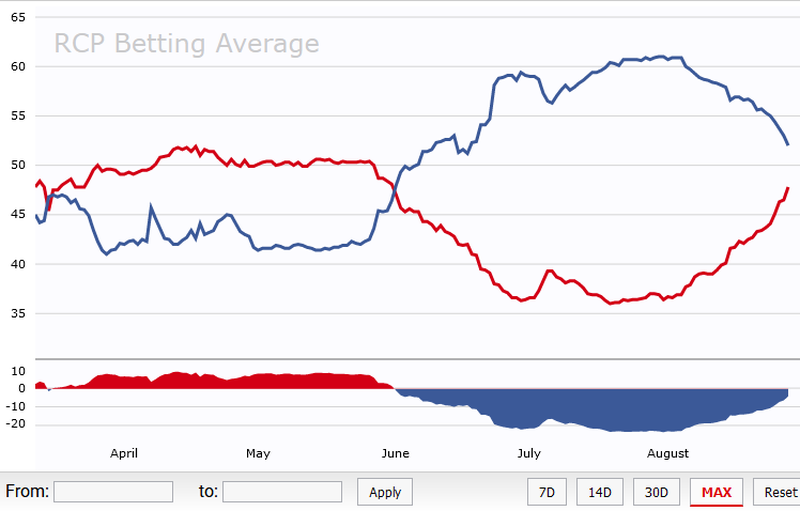

There was a good deal of attention on the US Presidential race this weekend after the conclusion of the Republican National Convention last Thursday night. We will see what kind of polling bounce President Trump receives, if any, by the end of the week as very few polls currently include the final, higher profile nights of the convention. In 2016, President Trump saw a nearly 5pt improvement in head-to-head polls against Secretary Clinton after the RNC. He even led her in polling averages for a small amount of time before seeing the bounce decline within a month. That said, Mr. Trump has seen his poll numbers vs Mr. Biden improve by nearly 2.8ps over the past 6 weeks. The RealClearPolitics polling average measures his nadir at 40pts in mid-summer. Mr. Trump is now back to the head-to-head polling range of 42-44pts he was sitting at following the first wave of outbreaks in the US. Overall RCP measures a +6.9pt spread for Mr. Biden (49.7%) over Mr. Trump (42.8%) but check in later this week to see how the RNC may change that.

Today we get final August manufacturing PMI’s from around the world, along with the ISM readings from the US, which will give us an indication of how the global economy has fared through the month as some economies opened up further and some became more restricted as viral patterns differed around the world. Note that the flash readings for the Euro Area saw a loss of momentum in the early part of August as its composite PMI fell from 54.9 to 51.6. Outside of the PMI’s, we will get July unemployment data out of the Euro Area, Italy and Japan, while seeing August unemployment change from Germany.

Back to this week’s calendar and later in the week the main highlights are the corresponding services and composite PMIs (Thursday) as well as the US jobs report on Friday. On payrolls, consensus on Bloomberg is currently expecting a further +1.518m increase in nonfarm payrolls last month, which would bring the total growth in nonfarm payrolls to 10.797m since April trough. However that would still be less than half of the 22.16m jobs lost in March and April. We have the day by day highlights for the rest of the week at the end.

To quickly recap last week for those on holiday yesterday, global equity markets continued to rise as the Federal Reserve’s new inflation targeting approach percolated through the financial system late in the week. The S&P 500 finished up +3.26% (+0.67% Friday) over the course of the week, having closed at record highs for 6 sessions in a row. The index has now risen 8 of the last 9 weeks since coronavirus cases rose quickly throughout the Southern and Western United States in June. The tech-focused Nasdaq rose +3.39% (+0.60% Friday) finishing at fresh highs as well and is now up over 30% YTD. In Europe, equities lagged behind their US counterparts, but the Stoxx 600 ended the week +1.02% (-0.52% Friday) higher.

Core sovereign bonds fell significantly on the week, before gaining on Friday with yields near their highest levels since June. The US yield curve steepened significantly following Fed Chair Powell’s statement on Thursday around the policy review and average inflation targeting. US 10yr Treasury yields rose +9.3bps (-3.1bps Friday) to finish at 0.721%, the highest weekly close since late March. Meanwhile 10yr Bund yields rose a similar +9.8bps (-0.2bps Friday) to -0.41% and 10yr Gilts rose +10.5bps (-2.5bps Friday) to 0.31%. The US 2y10y yield curve steepened +10.9bps to the highest levels since early June. In other markets, the dollar fell -0.94% on the week and is set to finish August lower for a fifth straight month.

via ZeroHedge News https://ift.tt/31OVgEJ Tyler Durden

Tesla Announces $5 Billion “At The Market” Stock Offering Tyler Durden

Tue, 09/01/2020 – 07:37

Just two days ago we reported that according to at least one CIO, Tesla is the only stock that matters: “Tesla is the key to this market, all are in Elon’s world, I am ignoring everything else, rates, dollar, etc.. for now. They are truly minor in comparison until Tesla breaks.” More importantly, the CIO made an important observation: “My gut tells me Elon does a massive secondary into SPX add, like $30B. Tesla would come out with the world’s best auto-balance sheet, on par with Toyota.“

It took exactly 2 days for this prediction to come partially true because moments ago, Tesla disclosed in an 8K that it had entered into an equity distribution agreement – read an “At-the-market” offering – with banks including Goldman Sachs, BofA Securities, Barclays Capital, Citigroup Global Markets, Deutsche Bank, Morgan Stanley, Credit Suisse, SG Americas, Wells Fargo and BNP Paribas (pretty much every possible bank) to sell up to $5 billion in shares from time to time based on Tesla’s instructions.

Here are the details from the 8-K:

On September 1, 2020, Tesla, Inc. (“Tesla”) entered into an equity distribution agreement (the “Equity Distribution Agreement”) with Goldman Sachs & Co. LLC, BofA Securities, Inc., Barclays Capital Inc., Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Morgan Stanley & Co. LLC, Credit Suisse Securities (USA) LLC, SG Americas Securities, LLC, Wells Fargo Securities, LLC and BNP Paribas Securities Corp., as sales agents (each, a “Sales Agent” and collectively, the “Sales Agents”), to sell shares of common stock, par value $0.001 per share, of Tesla (the “Common Stock”) having aggregate sales proceeds of up to $5.0 billion (the “Shares”), from time to time, through an “at-the-market” offering program (the “Offering”).

Upon delivery of a placement notice and subject to the terms and conditions of the Equity Distribution Agreement, the Sales Agents will use reasonable efforts consistent with their normal trading and sales practices, applicable state and federal laws, rules and regulations, and the rules of the Nasdaq Global Select Market to sell the Shares from time to time based upon Tesla’s instructions for the sales, including any price, time or size limits specified by Tesla. Under the Equity Distribution Agreement, the Sales Agents may sell the Shares by any method permitted by law, including in ordinary brokers’ transactions, in negotiated transactions, in block trades, and in transactions that are deemed to be an “at-the-market offering” as defined in Rule 415(a)(4) under the Securities Act of 1933, as amended (the “Securities Act”). The Sales Agents’ obligations to sell the Shares under the Equity Distribution Agreement are subject to satisfaction of certain conditions, including customary closing conditions.

The Equity Distribution Agreement provides that the Sales Agents will be entitled to compensation for their services in the form of a commission of up to 0.50% of the aggregate gross proceeds from each sale of the Shares, and Tesla has agreed to reimburse the Sales Agents for certain specified expenses. Tesla has also agreed to provide the Sales Agents with customary indemnification and contribution rights. Tesla is not obligated to sell any Shares under the Equity Distribution Agreement and may at any time suspend solicitation and offers under the Equity Distribution Agreement. The Equity Distribution Agreement may be terminated by Tesla at any time by giving written notice to the Sales Agents for any reason or by each Sales Agent at any time, with respect to such Sales Agent only, by giving written notice to Tesla for any reason or immediately under certain circumstances, including but not limited to the occurrence of a material adverse change in the company. The Offering of the Shares pursuant to the Equity Distribution Agreement will terminate upon the termination of the Equity Distribution Agreement by Tesla or the Sales Agents.

As noted at the top, one of the recurring questions during Tesla’s tremendous meltup is why the company never announced an official follow-on or secondary offering, and now we know: because it couldn’t, and instead it has to resort to such gimmicks as ATM offerings. As a reminder, the last notable attempt to sell stock At The Market came from bankrtup Hertz, which hoped to sell up to $1 billion in stock in lieu of a DIP loan, to Robinhood investors, and was barred in the last moment by the bankruptcy judge.

But why an ATM? As the WSJ’s Charlie Grant explained in June, “at-the-market deals are often deployed by smaller public companies, like biotech firms that don’t generate product sales or profits. Lately, however, bigger names have taken advantage as well. In addition to Hertz, Red Robin Gourmet Burgers unveiled a $40 million offering on Tuesday. Shake Shack announced a $75 million deal back in April. So far in the U.S. this year, there have been more than 200 at-the-market financings for slightly more than $31 billion in expected proceeds, according to Dealogic data. That is on pace to break last year’s record volume of $56.7 billion.”

As Grant went on to note, there were several important advantages for issuers: “There is wide latitude to sell stock as desired, which allows companies to raise money at relatively favorable prices. Perhaps even more important, bankers can sell stock to the general public without having to organize a roadshow with institutional buyers.“

That means higher takeup by individual investors, and many of these offerings might well be of shares that institutions don’t want…. Should the euphoria of the current market ever subside, individual investors could find themselves holding shares in businesses that are poorly equipped to handle a downturn. Even, or perhaps especially, in frothy markets, investors should remember that it is always a good idea to know what you own.

In short, for those asking with TSLA picked an ATM, it was to avoid an institutional roadshow where buyers can perform diligence or simply ask questions.

* * *

What is remarkable is that despite the coming dilution and the company’s own admission that this is the top, the stock dipped as one would expect, but it is still trading some 4% above Monday’s close, and was last seen at $515 pre-market (the equivalent of $2,575 pre-split) after hitting a new all time high of $538.75 earlier in the session.

via ZeroHedge News https://ift.tt/2QJFu7O Tyler Durden

WHO’s Tedros Warns “No Country Can Just Pretend The Pandemic Is Over” As Trump Embraces ‘Herd Immunity’ Tyler Durden

Tue, 09/01/2020 – 07:15

WHO Director-General Tedros Adhanom Ghebreyesus on Monday said during the organization’s latest Monday virtual news conference from its Geneva headquarters that “no country can just pretend the pandemic is over” as governments around the world ease social distancing restrictions and start to send children back to the classroom.

It’s just the latest example of Dr. Tedros implicitly criticizing President Trump and his handling of the US outbreak, after Trump recently insisted that the virus is “under control” despite flare-ups in Sun Belt states.

“The more control countries have over the virus, the more they can open up. Opening up without having control is a recipe for disaster. It’s not one size fits all, it’s not all or nothing,” Tedros said.

Dr. Tedros described “four essential things that all countries, communities, and individuals must focus on to take control” of the virus before they start to unwind their emergency measures.

First, prevent amplifying events. COVID-19 spreads very efficiently among clusters of people.

Second, reduce deaths by protecting vulnerable groups, including older people, those with underlying conditions, and essential workers.

Third, individuals must play their part by taking the measures we know work to protect themselves and others – stay at least one meter away from others, clean your hands regularly, practice respiratory etiquette, and wear a mask.

And fourth, governments must take tailored actions to find, isolate, test, and care for cases, and trace and quarantine contacts. Widespread stay-at-home orders can be avoided if countries take temporary and geographically-targeted interventions.

Individuals can minimize their chances of infection by avoiding the “three Cs”, Dr. Tedros said: closed spaces, crowded places, and close-contact environments.

Tedros also said countries should protect the most vulnerable people, including the elderly, those with underlying conditions, and essential workers to help save lives.

“If countries are serious about opening up, they must be serious about suppressing transmission and saving lives,” he said. “This may seem like an impossible balance, but it’s not. It can be done and it has been done.”

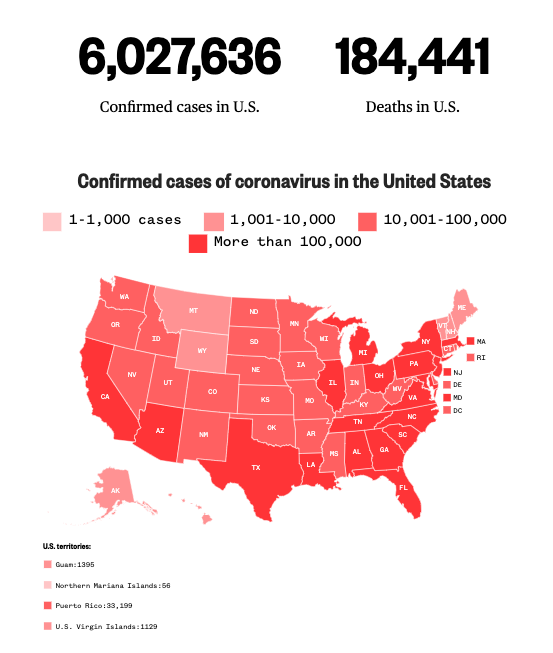

The latest data compiled by Johns Hopkins University shows more than 25 million people have been infected by COVID-19 and 848,000 have been killed globally. The US has been the epicenter of cases, reporting 6 million, along with most deaths, at 184,441.

Trump, who has a presidential election to win on Nov. 3, has continued to push headlines about ‘breakthrough‘ treatments – example: convalescent plasma – and a stream of optimistic vaccine headlines as a way to pump markets and boost optimism among increasingly exasperated consumers as the president struggles to revitalize the American economy after one of the most brutal crashes in recent memory.

Dr. Tedros’s remarks come as more public health ‘experts’ – including former FDA head Dr. Scott Gottlieb – slam President Trump for flirting with a new strategy of “herd immunity“. Such a strategy would, in theory, avert any future lockdowns or rollbacks of virus-inspired restrictions in favor of pushing ahead with reopening the economy while protecting the most vulnerable patients. While the White House has denied claims that it is shifting its strategy, a new advisor named Dr. Scott Atlas is purportedly pushing the US to mimic the approach embraced by Sweden.

via ZeroHedge News https://ift.tt/3jwVQNi Tyler Durden

“They Left His Body Face Down In The Dirt” – Protesters Surround LA Sheriff’s Office After Latest Police Killing Of ‘Armed’ Black Man Tyler Durden

Tue, 09/01/2020 – 06:52

Following deadly shootings in Kenosha and Portland over the past week during demonstrations allegedly inspired by the latest police shooting to rock the nation, a black man was shot and killed by a sherrif’s deputy in LA Monday night after the man allegedly punched the deputy before whipping out a handgun, prompting two deputies to fire their weapons.

Now, hundreds have gathered in peaceful protests in LA last night, laying siege to an LA sheriff’s office in the latest tense situation to emerge during the nationwide protest movement which has dragged on for 100 days.

Protesters lay siege to #LA sheriff’s office as riot police declare unlawful assembly #LAProtests

As has become distressingly common in recent weeks, this latest police shooting involving a black man inspired hundreds of people to gather – just like they did after Jacob Blake was shot by police – across south LA to protest this latest “senseless” police killing of a black man before any facts and information have been collected.

The man, identified by family members online as Dijon Kizzee, was observed by deputies riding a bike down along 110th Street and Budlong Avenue in violation of an unspecified vehicle code. The officers made a U-turn in their vehicle to approach him. A police public information office said he was “unable” to specify which vehicle codes Kizzee had been accused of violating before police approaching, apparently not realizing how protesters might seize on this as evidence of police skulduggery.

Kizzee

As officers approached, the suspect fled, but officers later caught up with him. As officers moved in, Dijon allegedly sprinted away, dumping a bundle of clothes he had been carrying. What comes next is a little hazy, but both deputies said they saw a semiautomatic handgun in Kizzee’s possession, which is when both deputies fired their weapons.

“Give us time to conduct our investigation,” Dean said. “We will get all the facts of the case out and eventually present them.”

Kizzee was pronounced dead at the scene, and no deputies were injured.

In the early hours of Tuesday morning, a crowd of around hundreds of ‘people from the neighborhood’, mixed with full-time activists, gathered at the scene of the fatal shooting in Westmont in the latest “demonstration” against lethal use of force by police.

A post on the Black Lives Matter LA Twitter account reportedly galvanized the protesters to gather at the scene before they moved to the sheriff’s office.

Los Angeles County Sheriffs killed a Black man…Dijon…on 109th and Budlong and left his body facedown in the dirt.

We need all hands on deck.

Please get here ASAP!

Unlike LAPD, sheriff’s deputies don’t carry body cameras.

Video from the protest showed a man addressing the crowd through a megaphone, urging them to ‘Say his name’, to which the crowd responded in chorus, ‘Dijon Kizzee.’

About 75 to 100 demonstrators are gathered near West 109th Place and Budlong Avenue in South L.A. where deputies with the Los Angeles County Sheriff’s Department shot and killed a Black man earlier today https://t.co/xCnRQq1v6rpic.twitter.com/XQXpwWpR16

Protesters who pull down statues are usually not content with removing the inanimate metal or stone object from its pedestal. They berate it, ridicule it, hammer it; they try to set it on fire; when that doesn’t work, they’re liable to behead it or dump it in a river to drown. Then the authorities retrieve it, as though fishing a corpse out of the lake. They crate it up so it can do no further harm, ship it to a statue internment facility, and forget about it forever.

Sympathetic accounts of the process make it sound quite rational. A statue of a Confederate general or a slave-owning president or Christopher Columbus, looming at you above the public square, might, especially if you are black or Indigenous, make you realize that the people who run and adorn your city aren’t like you. In fact, they make heroes out of the sort of people who oppress people like you, and they create a built environment where you might have to make your way through your oppressors’ distorted, self-serving interpretations of history every day on your way to the bus stop.

That would be a reason to go to the city council and urge members to hold some hearings on removals and replacements. Screaming at a statue, slapping it around, and then beheading it suggest another level of rage—and another level of interpretation. The statue has come to be identified with the person it represents. Ridiculing the hunk of bronze is ridiculing the represented person and attacking everything that, in turn, that person seems to mean. Traditionally (in the French Revolution, for example), pulling a statue off its pedestal is symbolically overthrowing or expunging the leader or ruler it depicts. One of the first things American soldiers did when they got to Baghdad was pull down the colossal Saddam Hussein. Reporters and television crews covered the toppling of the statue obsessively; it may be the best-remembered image of the Iraq invasion. Overthrowing Hussein and pulling down his statue didn’t seem to be clearly distinguished in anyone’s mind.

Monuments are often fated to become effigies, their destruction a premonition of the fall of the leader and the transformation of his symbolic order. In other cases, the destruction of the monument is a reenactment of the death or dismemberment of the leader that has already taken place, a way of killing him over and over even if he died in his sleep, as in the fate of thousands of statues of Stalin after the fall of the Soviet Union. Robert E. Lee is dead, but that doesn’t mean we shouldn’t kill him again (and again) in his images. What was “he” doing still hovering over the city of Richmond in 2020, anyway?

President Donald Trump’s response to this has also been traditional, indeed ancient. Appearing on Independence Day in front of one of the world’s largest sculptures, he said: “Today, we pay tribute to the exceptional lives and extraordinary legacies of George Washington, Thomas Jefferson, Abraham Lincoln, and Teddy Roosevelt. I am here as your president to proclaim before the country and before the world: This monument will never be desecrated, these heroes will never be defaced, their legacy will never, ever be destroyed, their achievements will never be forgotten, and Mount Rushmore will stand forever as an eternal tribute to our forefathers and to our freedom.” Then he announced that the “ringleader” of the “attack” on a statue of Andrew Jackson in D.C. had been arrested.

Trump further declared that he was issuing executive orders to make assaults on statuary punishable by 10 years in prison and to establish a “National Garden of American Heroes,” featuring a hundred or more sculptures depicting the likes of Davy Crockett, Amelia Earhart, Billy Graham, Douglas MacArthur, Dolley Madison, Audie Murphy, George S. Patton Jr., Ronald Reagan, Betsy Ross, and both Booker T. and George Washington. Sounds like the world’s least dynamic amusement park, but perhaps they’ll add some animatronics.

Trump’s claim that Rushmore “will never be desecrated” makes clear that he, and we, still understand the mentality of the idolater: Damaging a statue of Andrew Jackson is contaminating a sacred object, which makes the act outrageous. But the fact that the act of desecrating a statue outrages the idolaters is precisely what drives the iconoclasts; it’s the veneration of the person embodied in the inanimate object and in its placement and presentation that makes damaging or destroying it a symbolically powerful act. That’s how you get these idol wars.

The conflict between worshipping and destroying images, between idolatry and iconoclasm, is found in some form in almost every human culture. One classical depiction is in the Hebrew Bible. Moses returned from a mountaintop talk with Yahweh to find the Israelites worshipping a golden calf. “He took the calf the people had made and burned it in the fire; then he ground it to powder, scattered it on the water and made the Israelites drink it.” Then he set them to slaughtering each other. Ever since, there have been restrictions on images: The Jewish God can definitely not be sculpted, and similar, sometimes harsher, restrictions have run through Islam. The Protestant Reformation of the 16th century was to a remarkable extent a conflict about the use of images in worship, with the Protestants accusing the Catholics of worshipping paintings and sculptures, and hence of being pagans and polytheists. The Protestants destroyed images all over Europe.

Now, if you ask me squarely whether I’d rather be an idolater or an iconoclast, I’m likely to answer “an iconoclast,” because that sounds unconventional and interesting; I’d rather be an overthrower of shibboleths than an enforcer of them. Also, idolatry still sounds wildly irrational, as though we were worshipping the Great God Yottle, the omnipresent hunk of bronze.

But the image breakers seem rather irrational too, venting their rage on inanimate objects as though that would be a substantive blow against racism or whatever else they take themselves to oppose. It’s a bit like trying to suspend time by taking a hammer to your clock radio.

Irrational though it may be, the idolatry that leads to colossal Lincolns and Jeffersons in D.C. is routine for us all. On July 4, Trump described America as “uplifted by the Titans of Rushmore,” the event as taking place “before the eyes of our forefathers,” just as though the presidents were alive still and inhabiting their giant rock faces. He spoke of the woke iconoclasts as “ripping down Washington and Jefferson” (the men, not their images, mind) and as literally destroying American history; it appears that the level of symbols and the level of reality have been entirely confounded. But any child might point at an equestrian statue and ask, “Who’s that?” To which the answer is “Robert E. Lee” or “Napoleon,” not “that’s not a person—it’s a hunk of bronze.” I regularly say things like “I saw Trump on television” rather than declaring that I saw a very small, flat image of Trump. We all slide between representation and reality with great ease. Perhaps too great, because it leaves us vulnerable to elementary and sometimes bizarre confusions.

In other words, I’m more interested in what idolaters and iconoclasts have in common than the millennia-long conflict raging between them. Both sides evidently are working from a belief in what anthropologists once termed “sympathetic magic”: the idea that a person or a god inhabits, is actually present within, the representation. One worships the god in and as the statue, or one attacks the emperor by defacing his image. Harming an image of your enemy has the power to harm your enemy; gazing at a prospective lover’s or even a celebrity’s picture puts you under their spell, “enchants” you. Images are often reported to weep, or heal, or speak. Or they seduce and corrupt, and must be defaced, hidden, or destroyed. The idol of today—the colossal Stalin, and perhaps even the mountain-size president-gods of Rushmore—is fated for desecration tomorrow. Idolaters and iconoclasts need each other.

They share a belief in—really, a vivid, immediate experience of—what the art historian David Freedberg, in his 1989 book The Power of Images, called “fusion”: the presence in the image of the person or thing or god of which it is an image. In fusion, Freedberg writes, “the body in the image loses its status as representation”; it becomes, in the mind of the idolater or the iconoclast, what it depicts. “Arousal ensues,” says Freedberg (he’s got the response to pornography in mind, as well as patriotic or religious fervor): positive arousal to adoration in the case of the idolater, negative arousal to loathing, disgust, or rage in the case of the iconoclast.

“The iconoclast,” Freedberg continues, “sees the image before him. It represents a body to which, for whatever reason, he is hostile. Either he sees it as living, or he treats it as living.” Either way, “he feels he can somehow diminish the power of the represented by destroying the representation or mutilating it.”

Freedberg argues that things have changed little, that we still experience just as vividly as ancient cultures the presence of the thing in the image. It’s a hard feeling to escape, really. If you think you are immune to it, consider how you might feel if I stood in front of you and slowly ripped a picture of your mother in two. I doubt that ancient Byzantium or Reformation Europe can boast any clearer cases of the conflict between idolaters and iconoclasts than the scenes from Philadelphia in May and June, in which some people attacked while others tried to defend statues of Christopher Columbus and former Mayor Frank Rizzo (both of whom have “iconic” status in certain neighborhoods of South Philly). Certainly, it is hard to imagine such a conflict breaking out over an unshaped hunk of metal. Freedberg argues that it’s the resemblance of the statue to the person that lends it power: the power to make that person, even if he’s been dead a long time, manifest in the physical reality of the present.

But the “magical” identification of an image with its human inspiration goes only so far to explain widespread paroxysms of iconoclasm of the sort that occurred in eighth century Byzantium, in the Netherlands during the Reformation, during the French Revolution, or on the streets of America in 2020. Who controls public space, and hence who gets honored in public space, is a relatively raw vector of power. When the municipal or federal government is erecting and protecting images, tearing images down can become a generalized expression of anti-authoritarianism.

That’s the turn of mind that turns iconoclasm from occasional vandalism, or even a focused demand to reinterpret history, into a widespread outbreak of symbolic violence indiscriminately directed at publicly venerated images in general. We reach the point at which there is a loathing not only for specific historical symbols but for the whole authoritative symbolic order, right down to its approved artistic styles and the ways it orders public space. Pretty soon you’re tearing down anything that looks like a realist sculpture. Historical outbreaks of iconoclasm have often followed that pattern, progressing from criticism of specific sorts of images to what almost amounted to an attempt to erase or replace all images. Notoriously, the current wave of iconoclasm has not always distinguished between (images of) Robert E. Lee and (images of) Ulysses S. Grant, between images of slaveholders and images of abolitionists.

Even if we admit that we are all somewhat susceptible to sympathetic magic, we need to maintain some distance and distinctions if we intend to stop short of sheer superstition. Nothing you can do to his statues will alter history so that Robert E. Lee never existed. And as many totalitarian regimes have shown, it’s a lot easier to change all the pictures and sculptures than it is to change people’s minds or the concrete conditions in which they live.

from Latest – Reason.com https://ift.tt/2YVSL1n

via IFTTT