Two topics this morning. The Outlook for Q4 and The Pandemic.

Let’s start with Q4.

Starts today.. Get set, ready, go! As we enter the final quarter of this incredible year, stock markets are wobbly but remain close to record levels, bond markets have staged record issuance, and yields have never been so low. Yet London’s City is empty, activity is crashing once more, millions face unemployment as second lockdowns bite across the land!

The good news is there will be no Christmas to distract us from the vitally important business of flustering and flaffing about markets. Bah Humbug rules will apply this year. There will be no New Year either – which means we shall be trapped in perpetuity in the misery that was 2020… Argg….

October is always a fascinating month. It’s not just leaves falling off trees, but the occasional banker jumping out of high windows as the seasonal autumn market crash comes around. Can the gains seen since March be maintained? Or will it all come crashing down on a Manic Monday, Black Tuesday, Woeful Wednesday, Terror Thursday or any normal Friday?

I suspect markets remain flat for the time being. Probably. Maybe. Central banks have little choice but to continue juicing markets through zero rates and QE Infinity. When returns are so low, investors have little choice but to keep taking risk – meaning equity markets are likely to benefit. But it’s getting increasingly selective out there. Even a broadly positive fundamental-led market doesn’t mean bubbles aren’t ripe for popping.

The shape of the global economy remains troubling – China would like us to think their domestic economy is resurgent, but oil and commodities remain weak, while job losses across Occidental economies are rising. Few folk are talking about synchronous recovery in 2021. Markets are rightly nervous.

The key influence this month will be the US election and stimulus hiatus. At present we’re waiting to see if and when the US government gets around to pumping in some fresh stimulus to boost markets higher. Although there is much talk and stimulus posturing – but it’s unlikely in the current fervid US environment. Fears about how good or bad a Democrat or Republican leader will or won’t be for the economy are not as forceful short-term factors as a new dose of stimulus could provide – but in a market desperately seeking direction and nudge, any Political noise is likely to trigger volatility ructions – especially if the market takes a tantrum on the lack of stimulus package.

The other big issue remains the Pandemic. Markets are being driven by the implications of lockdowns on recession and consideration of the K-shaped recovery – whereby the rich with access to capital get richer and the rest of sink further into penury. That’s not an entirely encouraging perspective for the long-term future of QE interventions and social cohesion as Europe enters its next election cycle.

What will markets do? Has the rally run of out steam? Are we in a flat market till a new US administration sets the narrative in Jan?

Its flat markets that can be most dangerous – that’s when suddenly confidence snaps and we get the big tumbles. Will it happen? Watch this space.

Meanwhile… What’s the real story about the Virus?

I am always amused by ridiculous conspiracy theories telling us the world is in the grip of a small number of billionaires with hidden agendas and designs to reset a new world order.. You can understand why weak and feeble minds are drawn to them… But I am increasingly wondering what we aren’t being told about the virus.

Y’day Boris warned us of further restrictions to come – the virus is “not-under-control” wail his scientists. He went all Churchillian and said he is “not afraid” to put measures “more costly than the ones in effect now” to stem the virus. He tells us that we (the great British public) don’t want to “throw in the sponge” when it comes to fighting the virus.

Actually.. many of us do want to stop. We want back to normal. Government, and the Media (which is luxuriating in 24 hour wall-to-wall horror coverage of the pandemic) are just too invested in the crisis to let it take its course.

What is it Boris thinks we are fighting? The virus is not the Black Death, and it isn’t even the much feared Epidemic we’ve been fearing for decades. Nor is it a simple flu – it’s clearly more complex in the way it attacks the body. But it does exactly what the regular yearly flu does – predates the elderly and sick in our population. Sad but that’s life (actually, death..)

What has been achieved locking down commerce and taking massive, potentially terminal, risks with the economic health of the nation? There is a simple cost-benefit to lockdown vs saving lives. At the moment, based on the data, it makes little sense.

Let’s consider the facts about Coronavirus here in the UK.

The following numbers are all from official statistics taken the NHS website collating all data on English deaths due to Covid.

NHS England official data shows the following:

21 people under 20 have died. 4 of them did not have an indentified pre-condition.

217 people aged between 20 and 40 have died of Covid. 35 of them had no pre-existing conditions.

2312 people between 40-60 have died. 270 had no pre-existing conditions.

11343 people under 80 have died. 577 had no pre-existing conditions.

15431 people over 80 have died. 514 had no pre-existing conditions.

Patients with Chromic Pulmonary Disease, Respitory, and Heart Disease figure in 48% of Covid deaths. Dementia is listed in 26% of Covid deaths.

Obesity is not recorded as a pre-existing conditions, but it is known to increase the risk to people with Covid. Earlier in the pandemic it was suggested ethnic minorities were also more at risk, but the numbers show 15% of deaths are from minorities which is close to their 14% representation in the population.

There is data on hospitals – but it is only updated monthly. The last snapshot from the beginning of September shows there are over 110,000 hospital beds in England. 468 were occupied by Covid Patients. Its been largely that way since June. Things have changed since then though.

Over the last 20 years deaths in the UK have ranged between 550k to 620K. Flu accounts for around 30k deaths in a normal year, dwarfed by Cancers, Dementia and Heart Disease.

All the above are facts. If the facts change as we learn more then we can reassess new facts as they emerge.

Now for some opinion:

As I observed a few weeks ago the UK ran a successful campaign to reduce heart-attacks from 2000 only to see dementia deaths rise by roughly the same amount. The reality is we are all going to die. (Having suffered a massive sudden heart-attack after a botched operation I know they are painful, scary and nasty, but, for choice, I’d rather go quick than slowly losing it.)

Flu deaths thru 2020-21 are likely to be lower because of Covid has already removed a large part of its target cohort. The me is true for all other major causes of death.

We know who the vulnerable are. Protect them – shielding if necessary. We know who is less vulnerable – let them get on with life and chose their risk.

We don’t yet know how deaths from foregone medical treatments, increased mental illness, loneliness, despair and suicide will rise. We know the impact of lost jobs and income is going to be felt most heavily among lower paid workers likely to cause long-term social deprivation issues. The young will suffer most to save the elderly.

Having looked at the data above, the obvious conclusion is the risks are not dissimilar to a bad flu year. My question is what Facts and “Science” has Boris used to determine he is justified in wrecking the nation’s economy? Continued lockdown flies in the face of the data or cost/benefit.

Life is about compromise. You try to get the best out of it – despite the hurdles it throws our way in terms of health, wealth and petty bureaucracy. It’s a constant process of weighing up risks and making choices accordingly.

On balance locking down our economy to protect the elderly sounds like a courageous decision. But it’s not a good decision under any form of analysis. It does not make any economic sense. It’s not callous to suggest we have to acknowledge Covid-19 is a bad break? I am pretty sure my Dad would be furious if he’d lived to see his grand-kids’ futures compromised to give him a few extra months/years. He’d be livid.

My conclusion is Government is now so lost, stumbling and trapped in its own narrative because it committed and went all-on on lockdown/shutdown and “saving the NHS” by scaring the pants off the population so comprehensively that now it can’t face the consequences of what its already done… Boris will no doubt tell us he destroyed the economy to save us all. The only hope for the Tories will be to dump him. With prejudice.

Compare and contrast Sweden and UK.

via ZeroHedge News https://ift.tt/2GncTmP Tyler Durden

Futures Surge After Stimulus Pessimism Turns To Stimulus Optimism Tyler Durden

Thu, 10/01/2020 – 08:09

Narratives used to explain market moves have become so simple enough even 16-year-old Robinhood traders can understand them: if markets are down, it’s due to stimulus pessimism, rising covid cases and/or a fading economic recovery; if markets are up, it’s due to stimulus optimism, covid vaccine hopes and/or a stronger economic recovery.

Case in point, yesterday we for the former, when late in the session news out of McConnell and Mnuchin hit market sentiment late in the session. However, all that reversed overnight, when Roll Call reported that Mnuchin had proposed a $1.62 trillion compromise proposal including more state and local aid and $400 a week in unemployment insurance. Talks continue today after the House delayed a vote on its $2.2 trillion plan to give Mnuchin and Nancy Pelosi more time to try to thrash out a deal

That was enough to boost market sentiment, while allowing traders to ignore the latest flood of mass layoff announcements as American Air and United said they’ll start laying off a combined 32,000 workers (but said they would reverse the move if the government agrees to additional support in the coming days, adding more pressure on policy makers to reach an eleventh-hour stimulus deal, according to Bloomberg). Also overnight, President Trump signed a stopgap spending legislation early Thursday to avert a government shutdown weeks before the presidential election.

As a result futures S&P 500 E-mini futures breached Wednesday’s highs, gaining as much as 1%, and the dollar weakened as investors “remained hopeful” – as Reuters put it – of a new coronavirus fiscal aid package ahead of a clutch of economic data including consumer spending and weekly jobless claims. European stocks advanced, led by technology firms.

Shares of American Airlines Group, Delta Air Lines, United Airlines and JetBlue rose all between 1.3% and 3.6% in thin premarket tradin, after the White House proposed a new stimulus bill to House Democrats worth more than $1.5 trillion that includes a $20 billion extension in aid for the battered airline industry. U.S. airlines have been pleading for more payroll support to protect jobs after the current package expired at midnight on Thursday.

Boeing rose 2.7% a day after Federal Aviation Administration Chief Steve Dickson conducted a 737 MAX test flight, a milestone for the jet to win approval to resume flying after two fatal crashes. PepsiCo gained 2.2% after it forecast full-year profit above estimates as consumers bought more of its snacks such as Doritos and Cheetos, while staying indoors due to the COVID-19 pandemic. Nasdaq futures also rose as tech giga-caps including Apple, Nvidia, Microsoft and Alphabet all rose between 1.3% and 2.4%.

Europe’s Stoxx 600 pared its advance to 0.1%, with FTSE 100 also relinquishing some gains on Brexit concern as the EU started the first step of legal action against the U.K. for breaching the terms of the Withdrawal Agreement. Travel and leisure shares fare worst on Stoxx 600, while chip stocks rallied after STMicroelectronics N.V. raised its revenue guidance. The French-Italian chipmaker jumped 6.4% after it saw a sharp rise in automotive and microcontrollers demand in the third quarter, setting it on course to top its 2020 forecast. Bayer AG shares fell as much as 13% in Frankfurt after the agriculture and pharma giant issued a profit warning. Engine maker Rolls-Royce Holdings Plc dropped after announcing a share sale. The UK’s FTSE 100 trims advance even as GBP falls; midcap FTSE 250 almost wipes gains of as much as 0.6%.

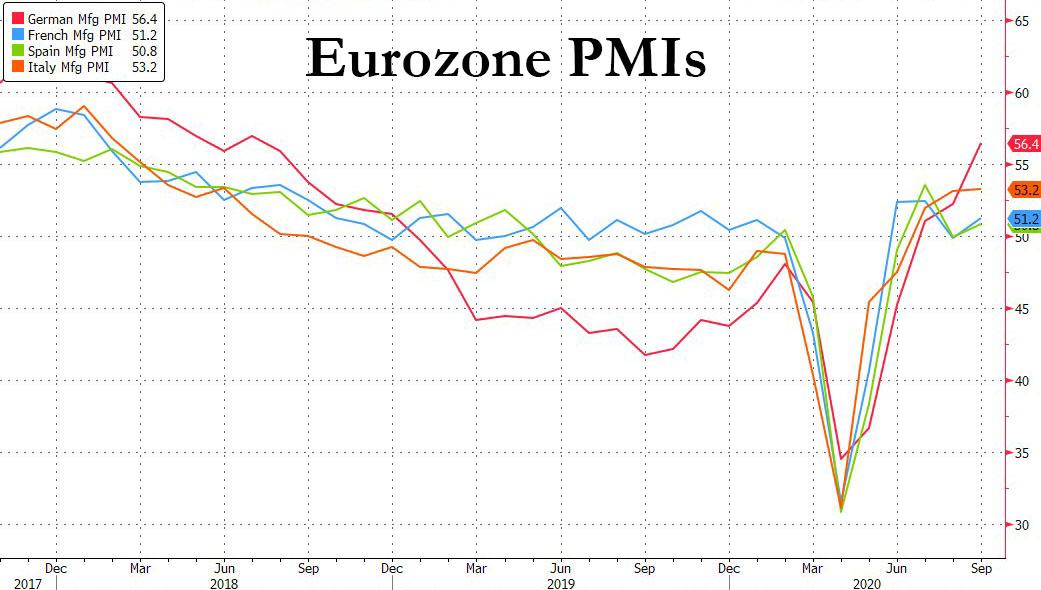

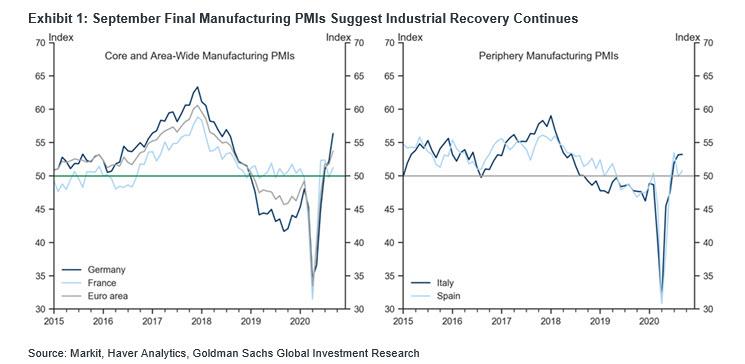

The recovery in euro zone manufacturing activity gathered pace last month but it was largely driven by strength in powerhouse Germany, and rising coronavirus cases across the region may yet reverse the upturn, a survey showed. The Euro area manufacturing PMI for September was unrevised from its flash estimate of 53.7, primarily reflecting partially offsetting revisions to the German (-0.2pt) and French (+0.3pt) counterparts, and somewhat stronger PMIs elsewhere than initially implied. The Italian manufacturing PMI rose only modestly further (below expectations), whereas the Spanish counterpart rose more notably (above expectations). The composition of both the Italian and Spanish readings was mixed, with some commonalities such as (i) weaker domestic but stronger foreign demand, and (ii) relative weakness in consumer goods and strength in investment goods.

Commenting on the data, Goldman said that “the September manufacturing PMI readings across the Euro area suggest the recovery in the industrial sector has continued, reflecting a net positive impulse despite (primarily domestic) headwinds amid a recovery in global industrial activity.”

Earlier in the session, the Tokyo Stock Exchange halted trading for the entire day Thursday. Japan Exchange Group, the operator of the TSE, said the problem occurred due to a failed switchover to backups following a hardware breakdown. The exchange will replace hardware and restart its system, aiming to resume trading as normal on Friday. Elsewhere, Asian stocks gained, led by materials and finance, after falling in the last session. The Topix was little changed, with Kyokuyo rising and Kyokuyo falling the most.

In rates, US Treasuries have been under modest selling pressure after S&P 500 E-mini futures breached Wednesday’s highs, gaining as much as 1%. The long-end yields are cheaper by ~2bp, steepening 2s10s, 5s30s by ~1bp each; 10-year, higher by 1.7bp at 0.70%, trails bunds and gilts by ~1bp. 30-year rose as much as 2.7bp to 1.482% in European trading.

In FX, the dollar slipped against most of its G-10 peers even though trading was muted in Asian session with Hong Kong and China shut for a holiday. The weakness continue what was the worst quarter for the dollar in more than three years.

The Bloomberg Dollar Spot Index slipped, yet came off a an early London session low as a rally in equities lost steam. The pound sank versus the euro after the European Union started legal proceedings against the U.K. over Prime Minister Boris Johnson’s plan to breach terms of its Brexit divorce deal. However, pound options traders are in no rush to hedge the risk of a sharp decline in the U.K. currency due to Brexit risks, according to Bloomberg. The Australian and New Zealand dollars rose to a one-week high as gains in U.S. stock futures and China’s yuan lift sentiment.

In commodities, crude futures continued to decline in tandem with sentiment in Europe as Brexit remains in the doldrums while crude-specific news-flow for the complex remains light; as participants look towards the day’s European Council gathering & key US data. WTI Nov trades on either side of USD 40/bbl (vs. high 40.47/bbl) whilst Brent Dec oscillates around the USD 42/bbl mark (vs. high 42.55/bbl). Elsewhere, spot gold remains capped by the USD 1900/oz mark as the yellow metal failed another jab at the psychosocial levels, whilst spot silver retraces some of yesterday’s losses and sees itself north of 23.50/oz.

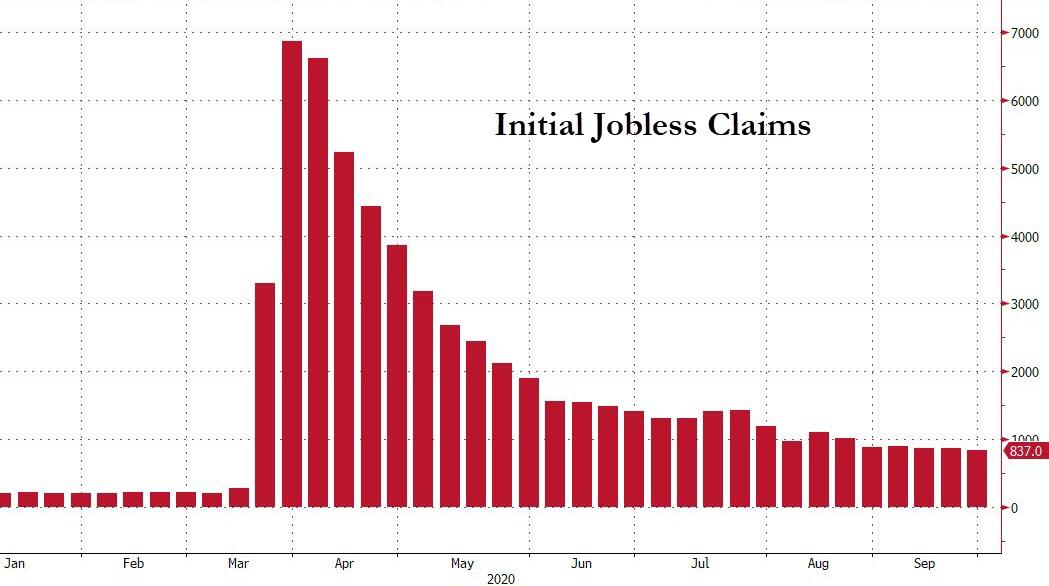

With a clutch of better-than-expected data also boosting sentiment in the previous session, investors will turn to consumer spending figures for August and the latest batch of weekly jobless claims on Thursday to gauge the pace of the domestic economic recovery. Initial jobless claims are not expected to show much improvement from last week’s 870,000 total when the data is released at 8:30 a.m. Eastern Time. The number comes as more companies announce they are going to move ahead with layoffs with American Airlines Group and United Airlines Holdings cutting a combined 32,000 positions. Goldman Sachs Group is also swinging the ax. Increasingly, signs are pointing to the rapid rebound in activity in the third quarter grinding to a near halt, according to Bloomberg. September data on the manufacturing sector is also due at 10 a.m. ET, while the Labor Department’s jobs report is scheduled for release on Friday.

Looking at today’s session, U.S. economic data includes initial jobless claims and August personal income and spending (includes PCE deflator) at 8:30am, final September Markit manufacturing PMI (9:45am), August construction spending and September ISM manufacturing (10am); jobs report is ahead Friday.

Market Snapshot

S&P 500 futures up 0.6% to 3,372.75

STOXX Europe 600 up 0.3% to 362.31

MXAP up 0.4% to 170.66

MXAPJ up 0.6% to 560.29

Nikkei unchanged at 23,185.12

Topix unchanged at 1,625.49

Hang Seng Index up 0.8% to 23,459.05

Shanghai Composite down 0.2% to 3,218.05

Sensex up 1.6% to 38,668.04

Australia S&P/ASX 200 up 1% to 5,872.93

Kospi up 0.9% to 2,327.89

German 10Y yield rose 0.3 bps to -0.519%

Euro up 0.03% to $1.1725

Brent Futures down 0.8% to $41.98/bbl

Italian 10Y yield rose 1.4 bps to 0.662%

Spanish 10Y yield rose 0.3 bps to 0.251%

Brent Futures down 0.8% to $41.98/bbl

Gold spot up 0.5% to $1,894.65

U.S. Dollar Index down 0.02% to 93.86

Top Overnight News from Bloomberg

President Donald Trump signed stopgap spending legislation early Thursday to avert a government shutdown weeks before the presidential election, the White House said

U.S. Treasury Secretary Steven Mnuchin and House Speaker Nancy Pelosi plan to resume discussions Thursday on a new pandemic relief package, racing against the clock to resolve their differences on another round of coronavirus stimulus

The European Commission will on Thursday send a “letter of formal notice” to the U.K. for breaching the terms of the Withdrawal Agreement, a person familiar with the matter says

The ECB’s emergency stimulus has propelled excess cash sloshing around the euro area’s economy past 3 trillion euros ($3.5 trillion) for the first time

The Tokyo Stock Exchange halted trading for the entire day Thursday, freezing buying and selling in thousands of companies in the worst-ever outage for the world’s third-largest bourse

Sweden’s Riksbank said in the minutes of its latest monetary policy meeting that if there is a need for more monetary policy stimulus, further expansion of the balance sheet remains an important tool

A quick look at global markets courtesy of NewsSquawk

European cash indices trade with modest gains (Eurostoxx 50 +0.3%), albeit off best levels as Q4 gets underway. Direction is potentially in part due to gains in US equity index futures, which remain elevated near yesterday’s best levels as policymakers in Capitol Hill continue to attempt to broker some form of agreement on COVID-19 stimulus. Focus ahead, will likely be on whether the administration and Democrats can bridge the gap between their respective USD 1.62trl and USD 2.2trl offers respectively and then ultimately whether any agreed deal can make its way through Congress; failure to do so at this juncture will likely mean that the US will not receive a fiscal boost until after the November election. From a European perspective, the DAX (+0.2%) has been a modest laggard throughout the session amid losses in index-heavyweight Bayer (-10.5%) after the Co. announced it is intending to cut around EUR 1.5bln in annual costs whilst citing weakness in the agricultural sector, which desks suggest further undermines the efficacy of the Co.s’ purchase of Monsanto. From a sector standpoint, retail names have been underpinned by upside in H&M (+6.6%) after its Q3 update posted a beat on expectations and revealed plans to lower its store count by 250 in 2021. IT names are also firmer this morning after prelim Q3 earnings from STMicroelectronics (+5.8%) saw the Co. raise its net revenue outlook for the quarter to USD 2.67bln from USD 2.45bln whilst nothing that Q3 was fuelled by “significantly better than expected market conditions throughout the quarter”; peers such as Infineon (+5.7%) and Dialog Semiconductor (+4.1%) have been seen higher in sympathy. Elsewhere, travel & leisure names are the clear laggard in the region with losses in airline names such as IAG (-3.9%), easyJet (-2.3%) and Ryanair (-2%). Finally, Rolls-Royce (-9.5%) have faced heavy selling pressure throughout the session after the Co. announced a GBP 2bln rights issue alongside the intention to begin a bond offering raising at a minimum of GBP 1bln.

Top European News

Brexit Prompts 7,500 City Jobs, $1.6 Trillion to Leave U.K.

H&M German Unit Fined $41.4 Million for Snooping on Staff

ECB’s Overnight Funding Rate Falls to Record Low Amid Cash Glut

UniCredit CEO Says M&A Isn’t a ‘Panacea’ for His Bank

Asia-Pac markets were quiet, owing to the closures in key bourses across the region with China, Hong Kong, Taiwan and South Korea all observing holidays, while trade in Japan was also mired by system issues for the Tokyo Stock Exchange which forced JPX to announce a halt of trade for the entire day. The lack of participants resulted in an uneventful overnight session; however, the mood was still positive as US equity futures extended on gains which had been attributed to month-end flows, strong data and increased stimulus hopes. This was after attempts by US Treasury Secretary Mnuchin and House Speaker Pelosi to reach an agreement on COVID relief and although progress was said to have been made, an actual deal remained elusive and House Democrats were forced to postpone the vote on their USD 2.2tln bill to Thursday to allow more time for talks with the White House. ASX 200 (+1.0%) traded with firm gains and surged above the 5,900 level with the index underpinned as miners led the broad strength in all its sectors, while Nikkei 225 remained suspended alongside Tokyo trade but Osaka futures were higher by 0.2% with a mild lift provided by the tailwinds from US and amid reports Japan is to consider further stimulus to address the pandemic. There was also mixed Tankan data which despite mostly missing expectations including on the headline Large Manufacturers Index, it still showed an improvement of the index for the first time in 11 quarters and Large All Industry Capex also topped estimates. Finally, 10yr JGBs futures were steady just above the 152.00 psychological level with price action contained as firmer results in the 10yr JGB auction was nullified by the system issues in Tokyo.

Top Asian News

Rare Ouster of Indian Bank CEOs to Spur Drive to Find Suitors

Top India Carmaker’s Sales Soar to 2-Year High After Lockdown

Global Investors Sell Record Japanese Debt as FX Swaps Sour

Korea Exports Rise in September for First Time Since Pandemic

In FX, sterling stands as the marked underperformer with initial downside sparked by source reports that the UK and EU have failed to narrow differences on State Aid in trade talks, whilst notably, a senior diplomat said the final agreement will be contingent on the UK withdrawing the Internal Market Bill – a move the UK PM previously rejected, citing UK safeguards. Thereafter, the European Commission President announced that Brussels will begin infringement proceedings against the UK for the breach of the Withdrawal Agreement, again in relation to the IMB. As such, Cable slid from an overnight high of 1.2950 to print a base at 1.2820 before stabilising, whilst EUR/GBP was propelled from 0.9070 to a high just shy of 0.9150. EUR/USD meanwhile has been under some pressure, potentially on Dollar-follow-through from the Sterling weakness as final manufacturing PMIs and an in-line EZ unemployment rate were brushed aside, with the pair briefly dipping below 1.1725 (vs. high 1.1758), whilst today’s NY cut sees a raft of large EUR/USD opex including some EUR 1.175bln rolling off between 1.1700-50 and EUR 2bln between 1.1680-85.

DXY – The broader Dollar and index remain within a tight range but off worst levels with the aid of the aforementioned Sterling weakness, with overnight losses a function of the then upbeat sentiment across markets, with talks on State-side stimulus still in limbo but the two sides seemingly in tense negotiations for an agreement. DXY resides around the middle of its current 93.614-876 intraday band, with downside levels including the 50 DMA at the 93.50 psychological level. The Buck now eyes US PCE Price Index and ISM Manufacturing PMI, alongside another wave of Fed speakers, relief bill talks and the fallout from the Special European Council Summit.

AUD, NZD, CAD – The non-US Dollars stand as the G10 gainers and hold onto APAC upside which was fuelled by overnight sentiment coupled with a firm CNH performance in the absence of the PBoC, and amidst a lack of pertinent data. AUD/USD trades just below 0.7200 having had tested the level to the upside overnight. A breach to the upside would open the door to the 50 and 21 DMAs at 0.7206 and 0.7211 respectively. The Kiwi similarly remains buoyed with a 0.6600+ status but just shy of the 0.6650 psychological level vs. the USD which lines up with the 21DMA. The Loonie’s gains meanwhile are to a lesser extent as the decline in oil prices weigh on the currency, but nonetheless USD/CAD meanders around 1.3300 having printed a current range of 1.3280-3327.

JPY – Shallow losses for the JPY but seemingly on Dollar-dynamics after the technical glitch in Tokyo stock markets. USD/JPY sees itself a touch above 105.50 as it eyes Tuesday’s high at 105.73 and the 50 DMA at 105.75. Note: today’s notable option expiries see USD 1.6bln at 105, USD 1.1bln between 105.30-35 and USD 1.4bln between 105.70-80.

In Commodities, WTI and Brent futures continue to decline in tandem with sentiment in Europe as Brexit remains in the doldrums with the EU readying legal actions against the UK on breaches of “good faith”, whilst crude-specific news-flow for the complex remains light; as participants look towards the day’s European Council gathering & key US data. WTI Nov trades on either side of USD 40/bbl (vs. high 40.47/bbl) whilst Brent Dec oscillates around the USD 42/bbl mark (vs. high 42.55/bbl). Elsewhere, spot gold remains capped by the USD 1900/oz mark as the yellow metal failed another jab at the psychosocial levels, whilst spot silver retraces some of yesterday’s losses and sees itself north of 23.50/oz. Finally, LME copper prices have retreated from earlier highs as the red metal tracks losses in stock markets, Dollar dynamics and overall sentiment.

US Event Calendar

8:30am: Initial Jobless Claims, est. 850,000, prior 870,000; Continuing Claims, est. 12.2m, prior 12.6m

8:30am: Personal Income, est. -2.5%, prior 0.4%; Personal Spending, est. 0.8%, prior 1.9%

9:45am: Markit US Manufacturing PMI, est. 53.5, prior 53.5;

10am: Construction Spending MoM, est. 0.7%, prior 0.1%

10am: ISM Manufacturing, est. 56.4, prior 56; New Orders, est. 65.2, prior 67.6; Prices Paid, est. 58.8, prior 59.5

Wards Total Vehicle Sales, est. 15.7m, prior 15.2m

DB’s Jim Reid concludes the overnight wrap

Welcome to October and the last quarter of what has been a decidedly strange year. Markets rounded off a fairly solid Q3 yesterday, even if September was more difficult. The quarter ended on a decent note though, as hopes rose among investors that a US stimulus deal might finally be reached between Republicans and Democrats, even if we were off the highs for the session as nothing materialised from talks. Henry is publishing the latest monthly, quarterly and YTD performance numbers in the next hour so watch out for that. As a spoiler the worst performer in September was the best in Q3. I’ll let you guess what that was before the note hits your inbox.

In terms of yesterday’s developments, the day started with higher expectations on the US fiscal front as Treasury Secretary Mnuchin said on CNBC that he hoped to have an “understanding” worked out with Speaker Pelosi by today. However after having met Pelosi for around 90 minutes yesterday, Mnuchin said that there was no agreement on an additional stimulus package. He tried to keep the mood upbeat, saying “we’ve made progress in a lot of areas.” Pelosi agreed in her own statement, “we found areas where we are seeking further clarification. Our conversations will continue.” The House was supposed to vote on the most recent Democratic proposal for a $2.2 trillion package overnight but it seems that’s now today’s business. That bill will likely be dead on arrival in the Republican Senate, where Senate Majority Leader McConnell called it “outlandish”. McConnell has tempered expectations quite a bit, saying the two sides were “very, very far apart on a deal.” Overnight, the Roll Call has reported that Mnuchin has offered a $1.62t relief proposal to Pelosi which includes more state and local assistance than Republican negotiators had previously offered and $400 per week in unemployment insurance.

The earlier initial hopes that a stimulus deal might soon be reached were a boon for risk assets, as the S&P 500 was up +1.74% intra-day. However after Mnuchin and McConnell’s comments the broad index retraced over 1.5% before a slight rally into the close saw the S&P finish +0.83%. Elsewhere the NASDAQ followed a similar pattern, finishing well off its highs, but closing up +0.74%. In Europe, the STOXX 600 fell -0.11% as fiscal stimulus was an issue as well, with Germany warning that delays to the European Union’s Recovery Fund were inevitable given disputes between member countries.

The net positive sentiment in the US was further supported by some positive data surprises. To start with, the ADP’s report of private payrolls in September showed a +749k increase (vs. +649k expected), while the previous month’s figure was revised up by +53k. Furthermore, pending home sales in August saw an +8.8% increase (vs. +3.1% expected), and the MNI Chicago PMI rose to 62.4 in September (vs. 52.0 expected), which was its highest level since December 2018.

Overnight in Asia, the markets which are open are mostly trading up including the Asx (+1.58%) and India’s Nifty (+1.14%). Futures on the S&P 500 are also up +0.51%. Japanese bourses have halted trading for the whole session following a serious hardware breakdown at the Tokyo Stock Exchange. This is the worst breakdown that the world’s third-largest bourse has ever suffered. Currently, there is no guidance on if trading will resume tomorrow. Meanwhile markets in China, Hong Kong and South Korea are closed for a holiday. Chinese markets will remain closed for a week. In Fx, the US dollar index is trading down -0.21%. Elsewhere, spot gold and silver prices are up +0.36% and +1.33% respectively.

In overnight news, President Donald Trump signed an executive order aimed at expanding domestic production of rare-earth minerals vital to most manufacturing sectors and reducing dependence on China. Meanwhile, the Fed has extended through the rest of the year its constraints on dividend payments and share buybacks for the biggest US banks citing “economic uncertainty from the coronavirus response” and the need for the banking industry to preserve capital. Elsewhere, Bloomberg has reported the White House is planning to announce an investigation into Vietnam’s currency practices, under section 301 of the 1974 Trade Act, after the Departments of Commerce and Treasury in August determined that Vietnam had manipulated its currency in a specific trade case involving tires.

The main data highlight of the day ahead will be the manufacturing PMIs from major economies. We have already seen the Jibun Bank Japan PMI come in at 47.7 (vs flash 47.3). In the West, the flash readings generally showed global manufacturing PMIs in expansion territory and roughly in line with expectations, whereas the services readings disappointed. In the Euro Area, the flash manufacturing PMI rose to 53.7, the highest reading since August 2018. While Germany’s flash manufacturing PMI rose to 56.6, not every region saw robust momentum with France (50.9) closer to the 50pt line that divides expansion and contraction. The US ISM manufacturing reading was quite strong last month at 56.0 and the market is expecting 56.4 today. It will be key to see if a recent pickup of covid-19 cases in the Midwest (particularly towards the latter end of the month) affect any momentum. Similarly if the rising coronavirus cases and reintroduction of some restrictions in Europe have affected data there.

In terms of the coronavirus itself, Spain became the most recent country to order restrictions on movement and social gatherings. Spanish Health Minister Illa indicated that a majority of the 17 regions of Spain agreed to the new rules which will limit public services and retail to 50% capacity and install a 10pm closing hour. The measures are meant to target regions with more than 50 infections per 10,000 people or where ICU capacity is strained, currently including Madrid. In the UK, the government reached a compromise with rebel Conservative MPs, as the Health Secretary announced that MPs would be able to have a vote on national regulations before they come into force “wherever possible”. It came as a further 7,121 cases were reported yesterday, pushing the 7-day average up to 6,220. Elsewhere in New York City, the positivity rate fell back to 0.94%, a day after it had been above the 3% threshold which if maintained over a 7-day rolling average could trigger school closures. At the moment, the 7-day rolling average is at 1.46%. See our table below for all the latest Covid cases numbers. The rolling 7-day number remains our focus. Also as we showed in our CoTD link here yesterday, covid has moved up to 20th in the list of the worst pandemics in history. Find out in the note how far it could end up going by looking at other pandemics through history.

Overnight we also saw some vaccine related news, with the CEO of Moderna saying that the company would not be ready to seek emergency use authorisation from the US FDA before November 25 at the earliest. He also added that the company doesn’t expect to have full approval to distribute the drug to all sections of the population until next spring. On the positive side, Bloomberg reported that the European Medicines Agency is expected to announce an accelerated “rolling review” for the University of Oxford and AstraZeneca Plc vaccine candidate as soon as this week to grant it an emergency approval. Such reviews allow regulators to see trial data while the development is ongoing to speed up approvals of drugs and vaccines. The move comes even as the US FDA widened its investigation of a serious illness in AstraZeneca’s vaccine study by asking for data from earlier trials of similar vaccines developed by the same scientists.

As investors moved away from safe havens, the dollar index (-0.01%) fell for a 3rd consecutive session, which concluded a quarter in which the greenback had weakened -3.51% in its worst performance since Q2 2017. And sovereign bonds also sold off on both sides of the Atlantic, with 10yr Treasury yields climbing +2.79bps to reach 0.684%, while in Europe 10yr bunds (+2.3bps), OATs (+2.4bps) and BTPs (+1.5bps) all saw yields rise.

Staying on Europe, following the weak German inflation print on Tuesday, both the French and Italian readings similarly showed readings that were below expectations. In Italy, inflation fell to -0.9% (vs. -0.4% expected), while over in France, inflation came in at 0.0% (vs. +0.2% expected), which was the lowest since April 2016. We’ll get the flash reading for the whole Euro Area on Friday, but given the Euro’s +4.34% appreciation against the US dollar over Q3, the figures will represent yet more unwelcome news for ECB policymakers.

On the US election, there wasn’t a lot of news yesterday following the raucous presidential debate we covered yesterday, and we won’t find out if there’s been any impact on the polls for a few days yet. Nevertheless, the betting/prediction markets have shifted somewhat in Biden’s favour in the last 24 hours, probably because there is little that’s likely to jolt the race out of the current dynamic with a persistent Biden lead in the mid-to-high single digits. The next set-piece event is on Wednesday, with the Vice-Presidential Debate between incumbent VP Mike Pence and California Senator Kamala Harris.

To the day ahead now, and as mentioned earlier the manufacturing PMIs from around the world will be the main data highlight. Otherwise, there’s also the Euro Area unemployment rate for August, the weekly initial jobless claims from the US, as well as US data on personal income, personal spending and construction spending for August. From central banks, we’ll hear from the ECB’s Lane and Hernandez de Cos, the BoE’s Haldane, and the Fed’s Williams and Bowman. Finally, EU leaders will gather in Brussels for a Special European Council summit.

via ZeroHedge News https://ift.tt/33iqMLL Tyler Durden

Florida localities are in rebellion following an order from Gov. Ron DeSantis (R) forbidding them from collecting fines and penalties “associated with COVID-19 enforced upon individuals.”

That prohibition on collecting fines came as part of a larger executive order DeSantis issued this past Friday allowing restaurants and bars that serve food to open at 100 percent capacity statewide.

Mask-mandating municipalities across the state say that they will continue to enforce their local COVID-19 restrictions, regardless of the governor’s order

“We will continue to issue citations for those not wearing masks. It is a public safety measure,” said Miami-Dade County Mayor Carlos Gimenez, in a Tuesday press conference. “We cannot collect fines, but we can issue fines. The county will collect once the governor’s order expires.”

Miami-Dade police and code enforcement officers are empowered to issue fines of up to $100 to individuals who are out of compliance with the county’s New Normal guidelines, which require a mask be worn in public at all times.

The city of Miami has even stiffer penalties on the books. Those not wearing masks are subject to $100 fines on the first and second offense and arrest for a third violation. The city has also dedicated 39 police officers to enforcing its mask mandate.

Many of the states and localities that have imposed mask mandates have not proactively enforced them, effectively making them non-binding guidelines.

That’s not been the case in the Miami area. Miami-Dade police issued 162 citations within the first two weeks of having its mask mandate on the books, according to the Miami Herald. Police reportedly ticketed people for taking their mask off outside, and for not having it cover one’s nose. As of mid-August, the Herald reports that Miami Dade police have issued 225 citations.

The city of Miami Beach has been even more proactive. Between late July and mid-August, officials there have issued fines to 288 people worth a collective $14,440.

The Herald again has documented how many of these fines were issued to people not wearing masks outside.

Other local governments in Florida have instead focused their enforcement against businesses, who can be fined for not enforcing mask-wearing and social distancing protocols for patrons and employees. The ability to fine businesses is presumably unaffected by DeSantis’ order, which restricts itself to suspending fines for individuals.

The Naples Daily News reports that businesses and local governments are seeking clarification on the extent of the governor’s order.

There’s an argument for mask mandates on libertarian grounds, namely that they correct for the negative externality of people walking around infecting others. By mitigating the spread of COVID-19, these mandates make the need for other, more onerous COVID-19 restrictions obsolete.

This theoretical case has to be weighed against how mask mandates, and the enforcement of them, works in the real world.

“With masks, the question is how mandates work when compared to the next best alternative,” wrote economists Steve Horwitz and Donald J. Boudreaux in an op-ed for The Detroit News.

“How many more people would use masks if they are mandated versus simply relying on strong social pressure and private sector no-mask, no-service rules? It might not be many,” the two write, adding that “by creating more opportunities for encounters between law enforcement and the citizenry, mask mandates create yet one more way for authorities to harass the relatively powerless.”

Studies showing the effectiveness of mask mandates often do not measure the level of enforcement or rates of compliance with those mandates, nor do they distinguish the effect of government mask mandates versus societal norms encouraging mask-wearing.

The way Miami is enforcing mask requirements vindicates the case against these mandates. Police are setting up mask traps and randomly fining people not wearing masks outside, where the risks of transmission are much lower.

DeSantis was right to try to put a stop to these abuses with his executive order. Hopefully, more will be done to prevent those municipalities from trying to issue fines.

from Latest – Reason.com https://ift.tt/30qpY5I

via IFTTT

Florida localities are in rebellion following an order from Gov. Ron DeSantis (R) forbidding them from collecting fines and penalties “associated with COVID-19 enforced upon individuals.”

That prohibition on collecting fines came as part of a larger executive order DeSantis issued this past Friday allowing restaurants and bars that serve food to open at 100 percent capacity statewide.

Mask-mandating municipalities across the state say that they will continue to enforce their local COVID-19 restrictions, regardless of the governor’s order

“We will continue to issue citations for those not wearing masks. It is a public safety measure,” said Miami-Dade County Mayor Carlos Gimenez, in a Tuesday press conference. “We cannot collect fines, but we can issue fines. The county will collect once the governor’s order expires.”

Miami-Dade police and code enforcement officers are empowered to issue fines of up to $100 to individuals who are out of compliance with the county’s New Normal guidelines, which require a mask be worn in public at all times.

The city of Miami has even stiffer penalties on the books. Those not wearing masks are subject to $100 fines on the first and second offense and arrest for a third violation. The city has also dedicated 39 police officers to enforcing its mask mandate.

Many of the states and localities that have imposed mask mandates have not proactively enforced them, effectively making them non-binding guidelines.

That’s not been the case in the Miami area. Miami-Dade police issued 162 citations within the first two weeks of having its mask mandate on the books, according to the Miami Herald. Police reportedly ticketed people for taking their mask off outside, and for not having it cover one’s nose. As of mid-August, the Herald reports that Miami Dade police have issued 225 citations.

The city of Miami Beach has been even more proactive. Between late July and mid-August, officials there have issued fines to 288 people worth a collective $14,440.

The Herald again has documented how many of these fines were issued to people not wearing masks outside.

Other local governments in Florida have instead focused their enforcement against businesses, who can be fined for not enforcing mask-wearing and social distancing protocols for patrons and employees. The ability to fine businesses is presumably unaffected by DeSantis’ order, which restricts itself to suspending fines for individuals.

The Naples Daily News reports that businesses and local governments are seeking clarification on the extent of the governor’s order.

There’s an argument for mask mandates on libertarian grounds, namely that they correct for the negative externality of people walking around infecting others. By mitigating the spread of COVID-19, these mandates make the need for other, more onerous COVID-19 restrictions obsolete.

This theoretical case has to be weighed against how mask mandates, and the enforcement of them, works in the real world.

“With masks, the question is how mandates work when compared to the next best alternative,” wrote economists Steve Horwitz and Donald J. Boudreaux in an op-ed for The Detroit News.

“How many more people would use masks if they are mandated versus simply relying on strong social pressure and private sector no-mask, no-service rules? It might not be many,” the two write, adding that “by creating more opportunities for encounters between law enforcement and the citizenry, mask mandates create yet one more way for authorities to harass the relatively powerless.”

Studies showing the effectiveness of mask mandates often do not measure the level of enforcement or rates of compliance with those mandates, nor do they distinguish the effect of government mask mandates versus societal norms encouraging mask-wearing.

The way Miami is enforcing mask requirements vindicates the case against these mandates. Police are setting up mask traps and randomly fining people not wearing masks outside, where the risks of transmission are much lower.

DeSantis was right to try to put a stop to these abuses with his executive order. Hopefully, more will be done to prevent those municipalities from trying to issue fines.

from Latest – Reason.com https://ift.tt/30qpY5I

via IFTTT

WHO Begs For Billions To Support Global COVID-19 Vaccinations, Israel Sees Another Daily Record: Live Updates Tyler Durden

Thu, 10/01/2020 – 07:43

Summary:

CDC extends ‘no sail’ order until end of Oct. amid controversy

WHO begs for more money for global vaccine effort

New restrictions imposed in Spain, UK

Germany sees another jump in cases

Europe supports expedited review for AZ-Oxford vaccine

Texas virus hospitalizations jump

* * *

Last week, the CDC quietly published its latest calculations on the ‘Infection-Fatality’ Ratio, which found that Americans under the age of 70 have a 99%+ chance of surviving a bout of COVID-19. But as President Trump’s political opponents continued to castigate the CDC for the appearance of political interference, the agency last night ordered an extension of its “no sail” order until the end of October, following a New York Times report claiming that the administration had “blocked” a longer extension until February at the behest of the tourism industry.

To be sure, in Europe, national governments in Spain and France have undertaken many more consequential decisions to try and revive their flagging tourism industries. Last night, the CDC announced the extension until Oct. 31. The previous “no sail” order expired at midnight on Wednesday.

Just in: “@CDCgov announced the extension of a No Sail Order for cruise ships through October 31. This order continues to suspend passenger operations on cruise ships with the capacity to carry at least 250 passengers in waters subject to U.S. jurisdiction.

And then per @axios

“Robert Redfield, the director of the @CDCgov was overruled when he pushed to extend a ‘no-sail order’ on passenger cruises into next year, according to two sources with direct knowledge of the conversation today in the White House Situation Room.”

The White House denied the NYT’s claims that the decision was politically motivated.

Brian Morgenstern, the White House deputy press secretary, said that the administration’s cruise ship plans were not politically motivated. “The president, the vice president and the task force follow the science and data to implement policies that protect the public health and also facilitate the safe reopening of our country,” he said.

At any rate, the administration could simply extend the order again later this month when the new deadline approaches. Still, the report represents the latest embarrassment for the CDC, which last month elicited an outpouring of criticism after publishing guidance on airborne transmission, only to revoke it a few days later. The agency also angered epidemiologists when it declared that asymptomatic people who were recently in contact with a COVID-19 positive individual didn’t need to be tested.

Meanwhile, as Bill Gates urges developed nations to pour more money into vaccination efforts for low-income developing nations, the UN Secretary General Antonio Guterres declared Thursday that the world needs a “quantum leap in support” for the global vaccination plan to contain the pandemic. The UK, Canada, Germany and Sweden have already pledged nearly $1 billion to secure developing nations’ access to vaccines. But COVAX, the WHO-led organization that’s leading the charge, says it needs another $35 billion, on top of the $3 billion it has already received, of which $15 billion will be needed before the end of the year. Some 168 countries are already signed up.

Global cases of the virus are approaching 34 million, with 33,832,124 as of Thursday morning at 0630ET, while the worldwide death toll has hit 1,012,341.

In Europe, the Spanish government ordered even more restrictions on movement in Madrid to try and slow the latest wave of infections. The new curbs will limit shops and public services to 50% capacity, while limiting operating hours to 10pm local time, with few exceptions. Local officials in Madrid agreed to implement the new measures, but said they might push back against them. In the UK, Health Secretary Matt Hancock announced new restrictions for areas in northern England to try and prevent the spread of the virus, warning that cases are “still rising”, even after a coterie of local officials wrote to Hancock asking him to ease up on the economy crushing restrictions in place in several cities in Northern England. The new measures require residents in the Liverpool region, as well as Warrington, Hartlepool and Middlesbrough, to be barred from meeting other households in all settings except outdoor public spaces. Residents are also advised to avoid sporting events while only visiting care homes in “exceptional circumstances.”

Across the Mediterranean, Israel posted yet another daily record, with 8,919 new cases reported in a single day, following a dip in confirmed cases over the holiday weekend. The new cases brought Israel’s total to over 248,000, including more than 1,500 deaths. PM Benjamin Netanyahu has promised to lift the restrictions only slowly, saying they could be in place for as long as six months.

Here’s more COVID-19 news from overnight and Thursday morning.

Indonesia’s Kalbe Farma begins distributing the antiviral drug remdesivir to hospitals (Source: Nikkei) .

India reports 86,821 new cases over the last 24 hours, vs. 80,472 the prior day, lifting the country total above 6.3 million (Source: JHU).

China reports 12 new COVID-19 cases for Wednesday, vs 19 a day earlier (Source: Xinhua).

Germany sees the most new cases since late April, while its infection rate fell below a key benchmark of 1.0 for the first time in five days. There were 2,442 new cases in the 24 hours through Thursday morning, according to data from JHU. That’s still far short of almost 7,000 cases recorded at the peak of the pandemic in the spring. Nevertheless, officials are still worried about a new wave of the disease stretching the health-care system and are urging citizens to respect distancing and hygiene rules (Source: Bloomberg).

As the FDA expands its probe into the AstraZeneca-Oxford vaccine, European regulators are getting ready to begin an accelerated review of the partnership’s vaccine, which would restore the group’s status as the fastest moving project in the West, despite some setbacks from Washington (Source: Bloomberg).

Just days after deaths fell to the lowest level in months, Texas virus hospitalizations just saw their biggest daily increase in more than three weeks, with a 3% jump (93) to 3,344, an 8.5% increase since the caseload bottomed out 10 days ago.

via ZeroHedge News https://ift.tt/3cQCwsm Tyler Durden

Please feel free to write comments on this post on whatever topic you like! (As usual, please avoid personal insults of each other, vulgarities aimed at each other or at third parties, or other things that are likely to poison the discussion.)

from Latest – Reason.com https://ift.tt/36omowS

via IFTTT

Please feel free to write comments on this post on whatever topic you like! (As usual, please avoid personal insults of each other, vulgarities aimed at each other or at third parties, or other things that are likely to poison the discussion.)

from Latest – Reason.com https://ift.tt/36omowS

via IFTTT