OECD Slashes 2021 Global Forecast, Warns Gov’ts Must Continue Fiscal Support Tyler Durden

Tue, 12/01/2020 – 09:10

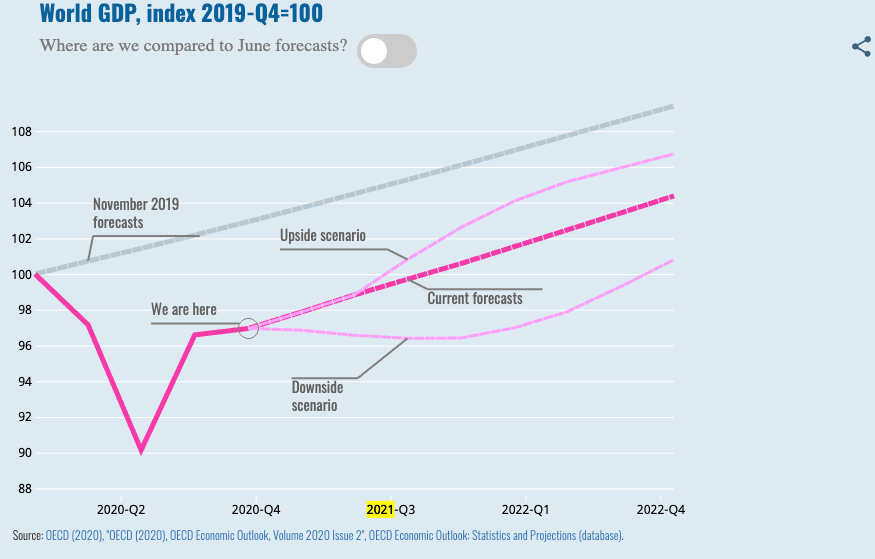

The Organization for Economic Cooperation and Development (OECD) warned Tuesday that the virus pandemic’s resurgence across the Western world has weakened the global recovery and could worsen as governments withdraw or do not provide enough fiscal support.

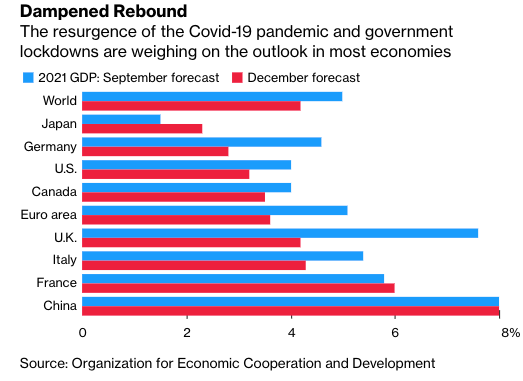

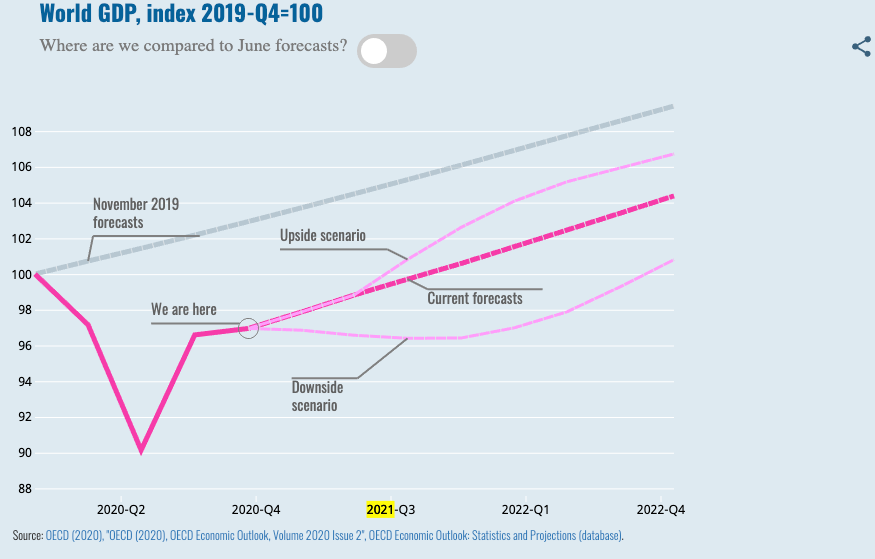

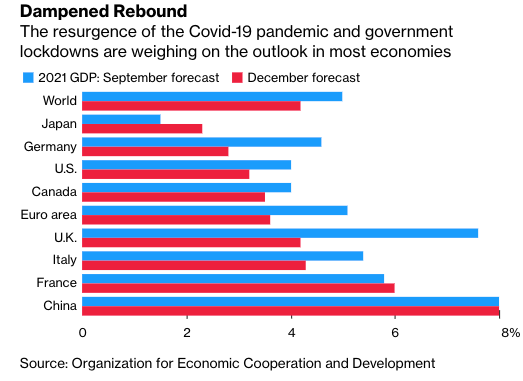

OECD’s latest Economic Outlook slashed its 2021 global growth forecast to 4.2% from 5% in September. The Paris-based organization said, “activity will continue to be restricted with social distancing and partly-closed borders most likely remaining through the first half of 2021.”

It said, “the recovery will be uneven across countries and sectors and could lead to lasting changes in the world economy. Countries with effective testing, tracking and isolation programs and where effective vaccinations can be distributed rapidly should perform relatively well, but a high degree of uncertainty persists.”

Some of the largest downgrades in growth for 2021 were in Europe and the UK, with a forecast slashed to 4.2% from 7.6%. The US also had its growth projection cut to 3.2% from 4%.

OECD Chief Economist Laurence Boone warned, “if public health or fiscal policy falters, then we would see a loss of confidence and a much more depressing outlook.”

“The toll on the economy could be severe, in turn raising the risk of financial turmoil from fragile sovereigns and corporates, with global spillovers,” Boone continued.

The OECD said in its report that Europe and North America will be smaller contributors to global GDP next year as their recoveries flounder, while China will account for over one-third of the global expansion.

The report made clear that governments need to continue supporting robust fiscal programs to avoid “fiscal cliffs.” Despite soaring public debt, the OECD was not concerned about mounting debt loads because borrowing costs are low.

The deployment of COVID-19 vaccines could be one of the significant factors in determining the global recovery trajectory next year. A successful deployment of the vaccine would allow governments to ease strict lockdowns and fully reopen economies.

With so much hope pinned on a successful vaccine deployment, any delays could produce significant setbacks.

“Despite the huge policy band-aid, and even in an upside scenario, the pandemic will have damaged the socio-economic fabric of countries worldwide,” Boone warned.

via ZeroHedge News https://ift.tt/33xtWv0 Tyler Durden

2 Killed, Several Injured After Car Hits Crowd Of Pedestrians In Germany Tyler Durden

Tue, 12/01/2020 – 09:02

German police say 2 killed, several injured in Trier when car hits pedestrians; the driver has been arrested.

Whether or not this is another terror attack is uncertain, but local media reports claim that 10 or more people might have been injured,. The attack recalls the 2016 Nice truck attack, which killed more than 80 people on a crowded promenade on Bastille Day.

BREAKING – Car plows through pedestrians in the German city of Trier, at least 2 dead, 10 injured. The police rammed the car and arrested the driver.pic.twitter.com/oQHM83arwv

Welcome to Reason‘s annual webathon week, where we ask you to support the work we do here at the magazine of free minds and free markets.

Listen, we know this has been a helluva year for everyone. Together we weathered a bruising pandemic, an election, street protests, policy fights, and confirmation battles. Reason has been no exception to the tumult of 2020. This year has actually been a monster traffic year for us, with a huge spike in readership, viewership, and listenership. People came to Reason for the broadsides of Nick Gillespie and J.D. Tuccille, the epidemiological insights of Jacob Sullum and Ronald Bailey, the wonkery of Christian Britschgi and Eric Boehm, the investigative criminal justice reporting of C.J. Ciaramella and Elizabeth Nolan Brown, the sober legal analysis of Damon Root and the folks at The Volokh Conspiracy, the comedy stylings of Remy and the Braggbrothers, the visual storytelling of Zach Weissmueller and Jim Epstein, and much, much more from the rest of the Reason crew.

But thanks to the shenanigans of the 2020 economy, more people consuming our stuff doesn’t necessarily translate into more money to make that stuff. That’s where you come in. Kicking in whatever cash you can spare—truly, anything helps—means Reason can keep making the stuff you love, whether it’s is our award-winning print magazine, our online stories, our many email newsletters, our array of podcasts, our videos, or our presence in your Twitter, Facebook, and Instagram feeds.

Our goal is $200,000 this year, and we hope you’ll contribute. Besides the satisfaction of supporting a worthy cause (plus the extra satisfaction of knowing you are sticking it to the taxman with your deductible donation), there’s some pretty good swag, including a bookmark designed by Reason contributor editor and cartoonist Peter Bagge, a 2021 calendar filled with weird and important dates in the history of freedom from the fevered brains of Meredith and Austin Bragg, autographed books, an (optional) shoutout on Facebook or Twitter, tickets to Reason events, or even lunch with an editor (pick me!) if your pants are especially fancy.

If you need an extra nudge to donate right now, on this Giving Tuesday: Donating this very moment will make your popups go away for the duration of the webathon, so you get more bang for your buck if you give ASAP.

This webathon week, you’ll also have a chance to ask Reason editors anything! We’ll be recording a special edition of The Reason Roundtable where we’ll do our best to answer listener questions of all kinds. Send your queries about life, the universe, and everything to podcasts@reason.com by the end of the day for a chance to be included. Ask Nick Gillespie for hair tips. Ask Matt Welch for…hair tips! Ask Peter Suderman for hair tips? Ask me for, well, you know.

On a more serious note: Your donations make the work we do at Reason possible. If you already support Reason, thank you. If you’re thinking about becoming a donor for the first time, thank you. This year has been absolutely wild. We hope that we played a small part in helping you get through it, and that you might consider returning the favor now.

from Latest – Reason.com https://ift.tt/33Ais9Y

via IFTTT

Rabobank: Yellen Is Offering To Recover The “American Dream”: What Does That Mean? Tyler Durden

Tue, 12/01/2020 – 08:51

By Michael Every of Rabobank

Dream a little dream for me

She’s ba-aaack.

Janet Yellen, now officially named as Biden’s nominee for Treasury Secretary, joined Twitter yesterday. (She was hardly going to turn up on Parler.) “We face great challenges as a country right now,” she tweeted. “To recover, we must restore the American dream – a society where each person can rise to their potential and dream even bigger for their children. As Treasury Secretary, I will work every day towards rebuilding that dream for all.” Pass the motherhood and apple pie, please.

What is the American Dream, exactly? Like America, it has changed over the years. Once, it was all Puritans dreaming of being able to live their own religious truth far from the controls of Europe; the “pursuit of happiness” was written into the Declaration of Independence along with life and liberty; in the 19th century, the Dream for European immigrants was political freedom and the absence of stifling aristocracy; then the opportunities of the Frontier; then chasing free money in the form of Californian gold; by 1931, in the teeth of the Great Depression, it was that “life should be better and richer and fuller for everyone, with opportunity for each according to ability or achievement” regardless of social class or circumstances of birth”; and to Martin Luther King, Jr. in the 1960s, it was spreading those opportunities to *all* US citizens. In 2020 some now argue: “If anyone can be said to embody the American Dream, it’s Kim Kardashian West.”

What part of the American Dream is Yellen offering to recover? Presumably not the gold rush, or Bitcoin, but one could see that as a possible side-effect if you are in that camp: will she ever say “There will never be a fiscal crisis in my lifetime”?

What about the Pursuit of Happiness? But from the Treasury? Unlikely. Or religious or political liberty? Wrong portfolio. More seriously, how about socioeconomic mobility, which has been withering in the US? Or good middle-class jobs, which have also been withering? If so, it would be useful to get some details soon of exactly how this will be done, and against the backdrop of the current Congress, not a dream one.

Perhaps owning one’s own home? That is often seen as a key part of the American Dream. Yet didn’t we try that in the early 2000s – and how did that end up? Wouldn’t that today require much lower house prices, or much higher wages, neither of which Yellen did much to cheerlead while at the Fed? (Not that anyone else has either, to be fair.) Lower rates have surely done all they can for their part on housing affordability, and yet rates have trended in the same direction as the American Dream for many people.

A true return of the American Dream would be bearish for bonds and bullish for the USD – unless everyone else globally is also living that Dream of middle-class jobs and wage inflation and higher rates. They aren’t – which is everyone looks to America in the first place. Even the new RCEP, for example, is a mainly a collection of net exporters who mainly net export to the US (or Europe). Let’s also recall the last Fed tightening cycle and the 2013 Taper Tantrum: they were more of a global nightmare, weren’t they? The rest of the world is keen on keeping up with Keeping up with Kardashians, but not on Keeping up with the Keynesians when they raise rates. As J. G. Ballard said decades ago,

“The American Dream has run out of gas. The car has stopped. It no longer supplies the world with its images, its dreams, its fantasies. No more. It’s over. It supplies the world with its nightmares now: the Kennedy assassination, Watergate, Vietnam.”

One might say the same about Fed tightening cycles: they may be over (and they are a US nightmare).

Of course, one of the reasons people still talk about the American Dream is because there aren’t many global alternatives. True, Canada and Australia and New Zealand all offer their own versions, but on a small scale with exclusive entry requirements too sometimes. But is there a British Dream other than “Brexit means Brexit”, or a good cup of tea, or pubs reopening? And is there an official European Dream other than ‘more Europe’? What about the Chinese Dream talked of since 2013? This seems to have many interpretations, but one is “a collectivist dream, for which everybody, with hard work, determination, and bravery, cooperate to make China (not the individual) a great nation.” Not really the same kind of global message as in the US – though of global significance.

Indeed, Australia just experienced a very “determined” message from the Global Times via an editorial titled ‘China’s goodwill futile with evil Australia’, which following a spat over China’s use of what was seen as offensive imagery of an Australian soldier, states: “Australia’s evil acts toward China have made Chinese society not only surprised, but also disgusted. Many Chinese people feel as if they have swallowed a fly when hearing about Australia….How arrogant and shameless the Morrison government is!…Australia treats China’s goodwill with evil. It is not worthy to argue with it. If it does not want to do business with China, so be it. Its politics, military and culture should stay far away from China – let’s assume the two countries are not on the same planet. As a warhound of the US, Australia should restrain its arrogance. Particularly, its warships must not come to China’s coastal areas to flex muscles, or else it will swallow the bitter pills.”)

The RBA also failed to mention any of this backdrop at its on-hold meeting today, focusing instead on vaccine and recovery hopes. That said, it added: “For its part, the Board will not increase the cash rate until actual inflation is sustainably within the 2-3% target range. For this to occur, wages growth will have to be materially higher than it is currently. This will require significant gains in employment and a return to a tight labour market. Given the outlook, the Board is not expecting to increase the cash rate for at least 3 years.” So how are we going to recover that Aussie dream of a tight labour market and wage growth and good middle-class jobs, to say nothing of affordable homes (as CoreLogic house prices jumped 0.7% m/m in November)?

Markets continue to stay in their own little dream-world through all of this; or they are living the dream. Are they right to do so? For now, perhaps. Longer term, dream on!

That’s the thing about dreams. Eventually you wake up. And sometimes in a cold sweat.

via ZeroHedge News https://ift.tt/37mqODn Tyler Durden

NASDAQ To Require One Woman And One Minority Or LGBTQ On Company Boards Tyler Durden

Tue, 12/01/2020 – 08:28

Today in “affirmative action for public company boards” news…

In a move that does little to help either diversity or equality, NASDAQ is now pushing for SEC approval of a rule that would require public companies on its exchange to have at least one woman director and one “diverse” director – meaning a director that self-identifies as an underrepresented minority or LGBTQ. You know, like how Elizabeth Warren “self-identified” as Native American.

Oddly enough, there’s still no requirement that Board Members need to know how to read financial statements. But, we digress.

The exchange is also pushing for its more than 3,000 companies to be forced to report “data on board diversity” or “face consequences”, including having to publicly explain why they haven’t done so. Also known as public shaming.

“Under the proposal, all Nasdaq-listed companies will be required to publicly disclose board-level diversity statistics through Nasdaq’s proposed disclosure framework within one year of the SEC’s approval of the listing rule,” a NASDAQ PR reads.

“To give companies time to comply, they will need to publicly disclose their board diversity data within a year of S.E.C. approval, and have at least one woman or diverse director within two years. Bigger companies will be expected to have one of each type of director within four years,” DealBook reported this morning.

Even more frightening is the fact that NASDAQ wants to impose these rules on private companies as well. Adena Friedman, Nasdaq’s CEO, said: “The ideal outcome would be for the S.E.C. to take a role here. They could actually apply it to public and private companies because they oversee the private equity industry as well.”

“Our goal with this proposal is to provide a transparent framework for Nasdaq-listed companies to present their board composition and diversity philosophy effectively to all stakeholders; we believe this listing rule is one step in a broader journey to achieve inclusive representation across corporate America,” she continued.

It was not immediately clear how anyone can uniformly impose such gratuitous virtue signalling across the millions of private mom and pop companies across America, but whatever.

And what would any good diversity initiative be without introducing a corporate partnership to implement it, where someone gets paid for enabling this latest virtue signaling lunacy. “Nasdaq will also introduce a partnership with Equilar, the leading provider of corporate leadership data solutions, to aid Nasdaq-listed companies with board composition planning challenges,” its PR says.

Zero Hedge looked up Equilar’s Board of Directors and found that out of its 5 members, there doesn’t appear to be a person of color or openly LGBTQ member. We wonder if they will use their own “corporate leadership solutions” to diversify their own board further.

Not at all surprising, currently 75% of NASDAQ companies do not meet the new requirements. Which means that instead of making life easier for businesses, the regulations will unleash countless amounts of red tape, new meetings and diversity seminars that will slow down business and infringe upon efficiency at each organization they “save”.

The irony of the new rule is, of course, that it limits a company’s ability to select qualified/interested candidates to the pre-determined race and sex of NASDAQ’s choosing.

The good news is that Elizabeth Warren’s 1/2000th Native American heritage may find her a post-Congress job on the board of Goldman Sachs a little bit quicker.

The bad news is we now have super-duper-useful indexes like the “LGBT-350”, a market-cap weighted basket of LGBT-inclusive companies. Because everyone knows investing is all about diversity and ESG, and no longer about generating alpha.

INBOX: Credit Suisse introduces the “LGBT-350”, a market-cap weighted basket of LGBT-inclusive companies.

In the early days of television, Sheila Kuehl had a role in a now forgotten show, The Many Loves of Dobie Gillis, which ended in 1963. She then became a leftist, a lawyer, and a politician. Despite the long interval between her Hollywood years and today, Kuehl still clings to that lampooned Hollywood notion about stars versus “the little people.” How else can one explain that, after railing against restaurants and voting to shut them down, Kuehl promptly went to a nice restaurant for dinner?

During the lockdown, politicians continued to draw their taxpayer-funded paychecks and telecommute from the comfort of their homes. Meanwhile, they targeted small businesses that depend on dealings with the public. More than any other business, restaurants were in Democrat politicians’ crosshairs.

As of mid-September, more than 100,000 restaurants had closed across America. In the two months since then, it’s certain that several thousand more have closed. The San Francisco Chronicle, for example, runs a regular column identifying restaurants that are gone.

Every closed restaurant represents several people’s lives going down the drain. The owner who sank all of his money in the restaurant, the employees who worked there, the suppliers who were dependent on its custom, and the surrounding stores who counted on the foot traffic it brought — all of it’s gone. And I might add, there’s no reason to believe that these horrific losses made a damned bit of difference to the course of a virus that is relentlessly working its way through the population.

While the people have suffered, the politicians imposing this suffering, like European royalty of old, have flaunted their special status.

Denver’s mayor, Michael Hancock, flew to his family within 30 minutes of telling Denver citizens to stay home for Thanksgiving.

Andrew Cuomo, having reinstated the lockdown across New York, boasted about his family coming home for Thanksgiving.

Illinois’s Governor J.B. Pritzker, another Democrat millionaire, was happy to see his family travel during the height of the spring lockdown.

Pennsylvania’s health secretary, “Rachel” Levine, who leftists pretend is not a mentally ill man telling people he’s a woman, forced sick people into nursing homes in May, even as he secretly removed his own mother. Levine, incidentally, is being floated as a possible surgeon general. That’s just what America needs: a hypocritical, self-entitled, mentally ill surgeon general.

And in California, Governor Gavin Newsom started by making headlines for imposing ridiculously stringent lockdown rules on people’s Thanksgiving celebrations, including requiring outdoor dining only, suggesting masks throughout the meal, giving people limited permission to use the bathroom, and cracking down on singing.

Then, just before Thanksgiving, photos emerged of Newsom and his wife having an indoor dinner with a large crowd of lobbyists at the über-expensive French Laundry in Napa Valley. None of the guests was masked. Afterward, Newsom gave a fake apology because Democrats are so certain that they’ve achieved perpetual power that they don’t even bother anymore to go through the motions of political humility.

The latest politician who can’t be bothered with the rules she imposes on little people is former Hollywood actress Sheila Kuehl: the Los Angeles County Supervisor, a Democrat, ate outdoors at Il Forno Trattoria in Santa Monica, just hours after casting the deciding vote to ban all outdoor dining in the county last week.

You can watch my 7pm live report on this in the link above. Tonight at 10pm I’ll have a full story about this, including reaction from local restaurant owners, and fellow L.A. County Supervisor Janice Hahn, who did not support the decision to ban outdoor dining. @FOXLA

Kuehl said during a recent Board of Supervisors meeting that outdoor dining is “a most dangerous situation,” saying she felt there was a risk of transmission of the virus from unmasked customers to their masked waiters and waitresses.

“This is a serious health emergency and we must take it seriously,” Kuehl said.

“The servers are not protected from us, and they’re not protected from their other tables that they’re serving at that particular time, plus all the hours in which they’re working.”

According to Kuehl, she ate there one last time before she destroyed it. Okay, I made up the part about destroying it, but her spokesperson said the meal was a fond farewell.

“She did dine al fresco at Il Forno on the very last day it was permissible,” a spokesperson for Kuehl told Fox 11 after the broadcaster received tips about what happened.

“She loves Il Forno, has been saddened to see it, like so many restaurants, suffer from a decline in revenue. She ate there, taking appropriate precautions, and sadly will not dine there again until our Public Health Orders permit.”

But what about Kuehl’s claim that such dining was “a most dangerous situation”? Apparently, it’s dangerous only for the little people.

These people are disgusting. I used to think voters were fools who kept voting them in. I now suspect that voters were naïve and credulous for believing that elections are fair. In California, at least, a lot of people probably got into office “the Dominion way.” We need to clean up elections and throw these people to the curb.

via ZeroHedge News https://ift.tt/3mxNl6I Tyler Durden

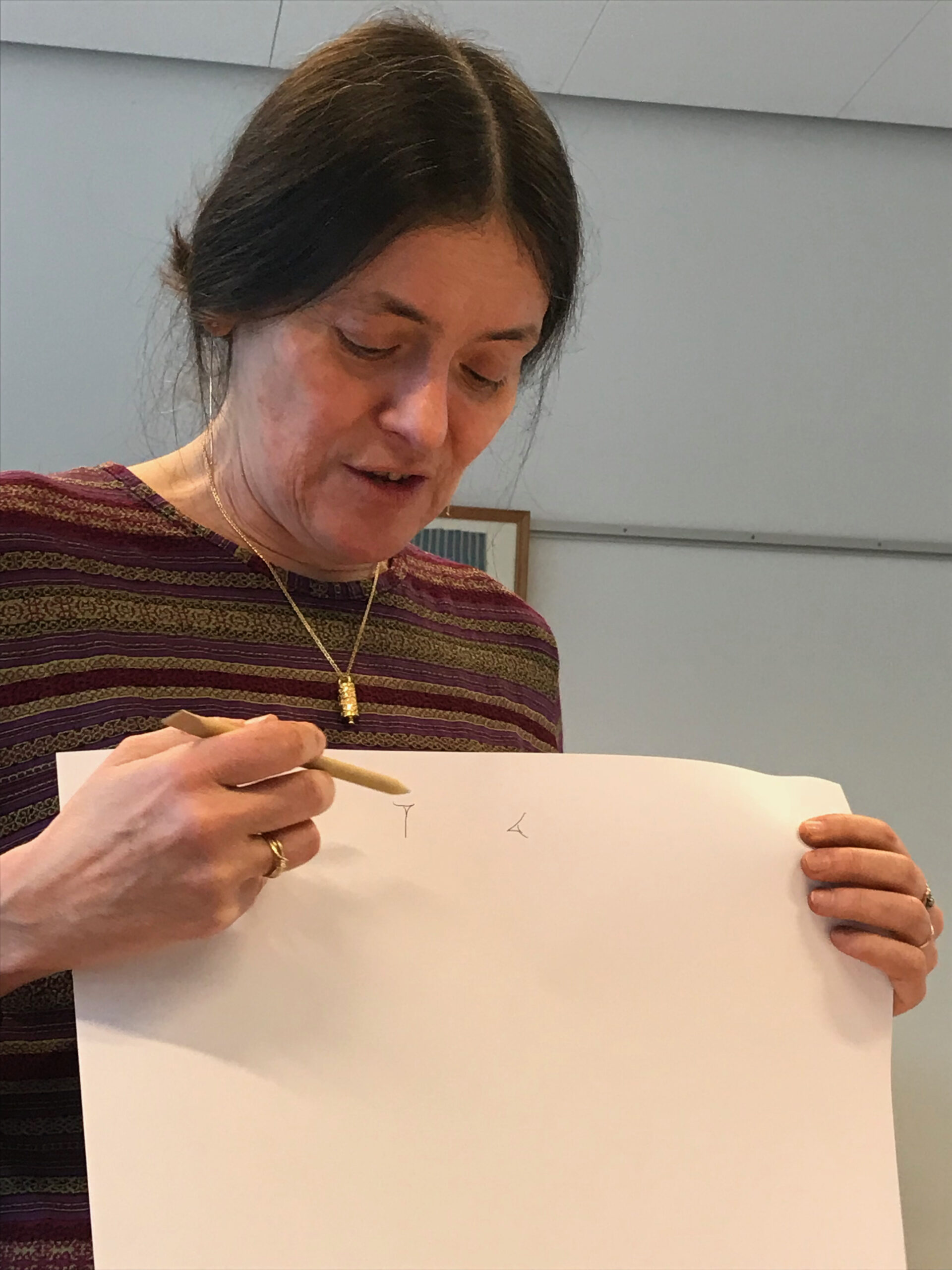

One of the many interesting scholars I met while researching The Fabric of Civilization was Cécile Michele, a French Assyriologist who has translated many of the 23,000 cuneiform tablets excavated from a site in Turkey. Here she is teaching us the basics of how to write in cuneiform.

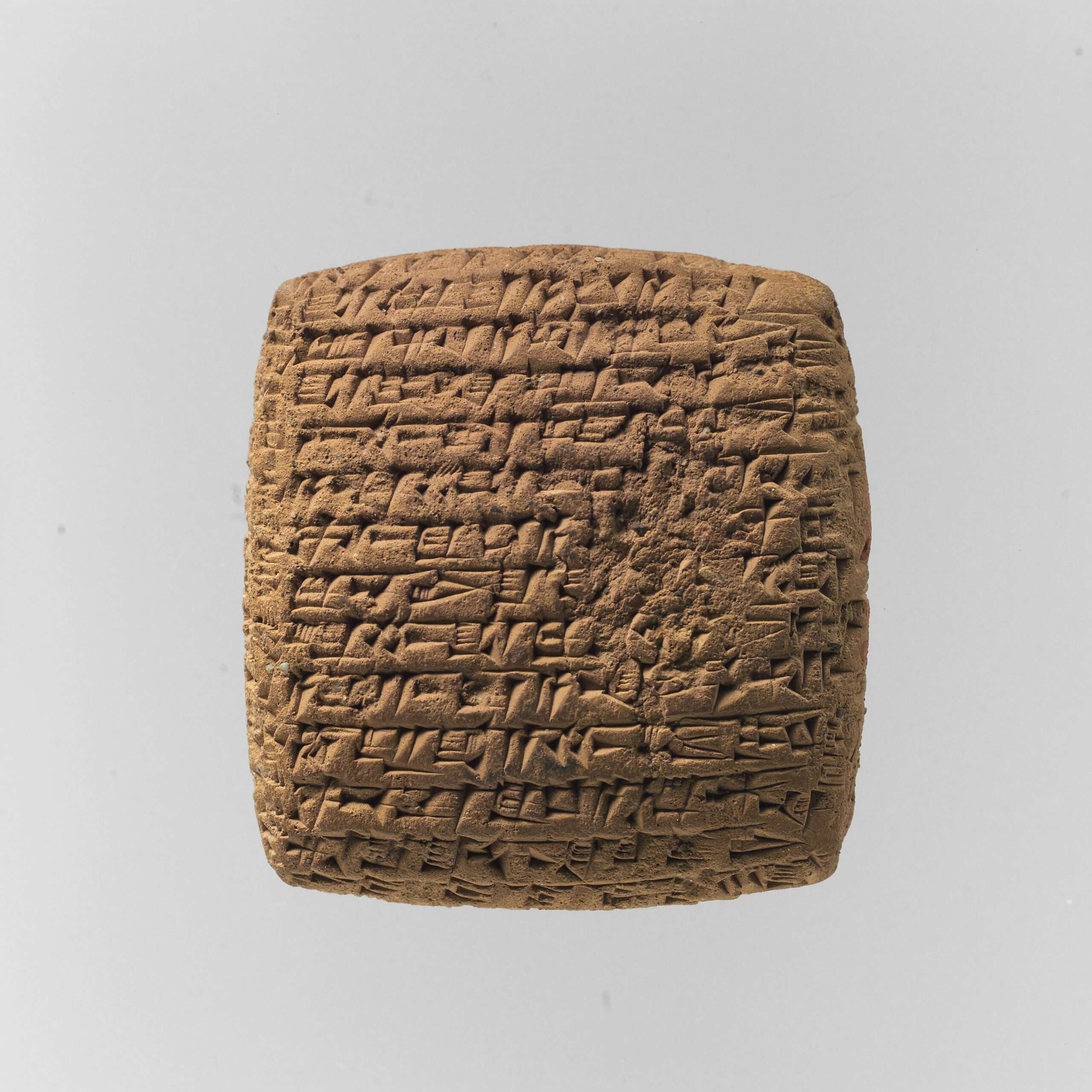

The tablets, known as the Old Assyrian private archives, are about 4,000 years old. They were found in the homes of expatriate merchants in the city of Kanesh, now the archaeological site called Kültepe. These letters and legal documents preserve the practices and personalities of a thriving commercial culture. They are our oldest records of long-distance trade.

Capturing dilemmas and decisions still faced by commercial businesses, these ancient records testify to the central role of textiles in the innovations that enable economic exchange. Here, the inventions aren’t material artifacts or physical processes but “social technologies”: the records, agreements, laws, practices, and standards that foster trust, ameliorate risks, and allow transactions across time and distance. Four millennia later, we can still hear the voices they record.

Lamassī was doing her best to keep up with the demand for her fine woolen cloth, fickle though the requirements seemed to be. First her husband asked for less wool in the fabric, and then he asked for more. Why couldn’t he make up his mind? Maybe it was his customers in that distant country. Maybe they didn’t know what they wanted. At any rate, her latest batch of cloth, or most of it, would soon be on its way. She wanted Pūsu-kēn to know it was coming. She wanted him to know she was doing her job. She wanted a little appreciation.

Lamassī rolled a small ball of damp clay between her hands, then flattened and smoothed it into a neat, pillow-shaped tablet, which she cupped in her left palm. She picked up her stylus and began to write, pressing wedge-like characters into the wet clay.

Say to Pūsu-kēn, thus says Lamassī

Kulumāya is bringing you nine textiles. Iddin-Sîn is bringing you three textiles. Ela refused to take any textiles and Iddin-Sîn refused to take another five textiles.

Why do you always write to me, “The textiles that you send me each time aren’t good!” Who is this person living in your house and denigrating the cloth that I send to you? For my part, I do my best to make and send you textiles so that for every trip at least ten shekels of silver can reach your house.

Her message completed, Lamassī dried the tablet in the sun. She then wrapped it in a gauzy fabric, which she coated with a thin layer of clay. She ran a cylindrical seal along the clay envelope to mark the letter as hers. A messenger would take it to her husband, 750 miles away in the Anatolian city of Kanesh.

Lamassī lived in Aššur, on the Tigris river near Mosul in modern-day Iraq. It was a city of middlemen who purchased tin and textiles and exported them, along with their women’s weaving, to Kanesh. Twice a year, caravans of donkeys made the six-week journey. A single caravan might include wares from eight different merchants, with thirty-five donkeys carrying more than a hundred pieces of cloth and two tons of tin. Some of the wares went for taxes in the two cities and in kingdoms along the way that guaranteed safe passage. The rest were traded for silver and gold.

By the time Lamassī picked up her stylus, cuneiform script was a thousand years old. For most of that time, however, writing had been the monopoly of a small class of specially trained scribes, probably a mere one percent of the population. Throughout most of human history, in fact, literacy belonged to the few, mostly men working for state or religious institutions.

Not so in Aššur.

For its people, letters were a critical technology. They needed to send instructions between Aššur and Kanesh and between Kanesh and the surrounding towns, where their agents sold textiles and tin. They needed to record orders, sales, loans, and other contracts. They needed the flexibility and control that come with literacy.

Over time, these pragmatic merchants simplified the cuneiform script, making it easier to learn and write. They invented new punctuation that let them skim documents quickly. Some wrote well, others poorly. But in this society of long-distance traders, most men and many women were literate.

Trade requires clear communication, particularly if the business owner doesn’t conduct every negotiation personally. Consider Pūsu-kēn. He first went to Kanesh as the agent of an older merchant in Aššur and, even as his own ventures grew, he continued to work on behalf of various traders back home. When their textiles and tin arrived in Kanesh, he needed to know what to do with the goods. Should he sell them in the city’s marketplace, sacrificing profits for immediate cash? Or should he seek a higher price by selling them on credit to an agent who worked the outlying towns? Letters came with the goods, telling him what to do.

Letters are such an old technology that we take them for granted. But they were crucial to long-distance trade. When commerce stretched over time and distance, written correspondence—and the literacy it required—came with it.

from Latest – Reason.com https://ift.tt/2KLEAYr

via IFTTT

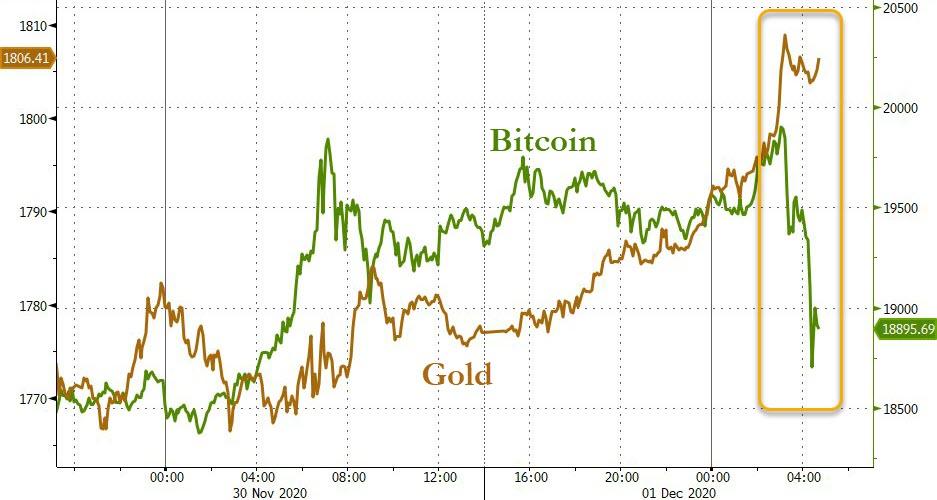

Gold Jumps Back Above $1800 As Bitcoin Drops $2000 From Record High Tyler Durden

Tue, 12/01/2020 – 08:02

After testing new record highs overnight, just shy of $20,000, Bitcoin has tumbled $2000 this morning…

Source: Bloomberg

The entire crypto space is also getting whacked…

Source: Bloomberg

And at the same time, gold has surged back above $1800, erasing last week’s sudden plunge…

Is the gold-to-bitcoin rotation unwinding?

Source: Bloomberg

Interestingly, Ethereum also took a big hit…

Source: Bloomberg

As Ethereum 2.0 Beacon Chain goes live. As CoinDesk notes, today’s launch concludes the opening act, or “Phase 0,” of Ethereum’s consensus mechanism transition, which will see the network – whose native cryptocurrency, ether, is worth $70 billion by market cap – fundamentally change how it settles payments while in motion.

“The launch of the beacon chain is a huge accomplishment and lays the foundation for Ethereum’s more scalable, secure, and sustainable home,” Ethereum Foundation researcher Danny Ryan told CoinDesk in an email. “There is still much work to do, but today we celebrate.”

The Beacon Chain will be the backbone of a new Ethereum blockchain, a network intended to keep pace with PayPal and Visa in terms of processing speed, while rivaling them in terms of transparency and payment finality.

As CoinTelegraph points out, the transition to PoS paves the way for future planned upgrades to be implemented, such as sharding to improve scalability.

Currently staked ETH are likely to be locked up until Phase 1.5 of the Ethereum 2.0 rollout, currently planned for late 2021 or early 2022. This will see the current Ethereum mainnet merge with the new beacon chain and sharding system.

Anticipation for the Eth2 launch has been building throughout 2020, and has been reflected in the price of Ether, which started the year at just $130 but is currently riding high at over $600.

The launch will be especially welcomed by those in the decentralized finance community. The explosion of DeFi during 2020 saw a huge increase in traffic and gas fees on the Ethereum network.

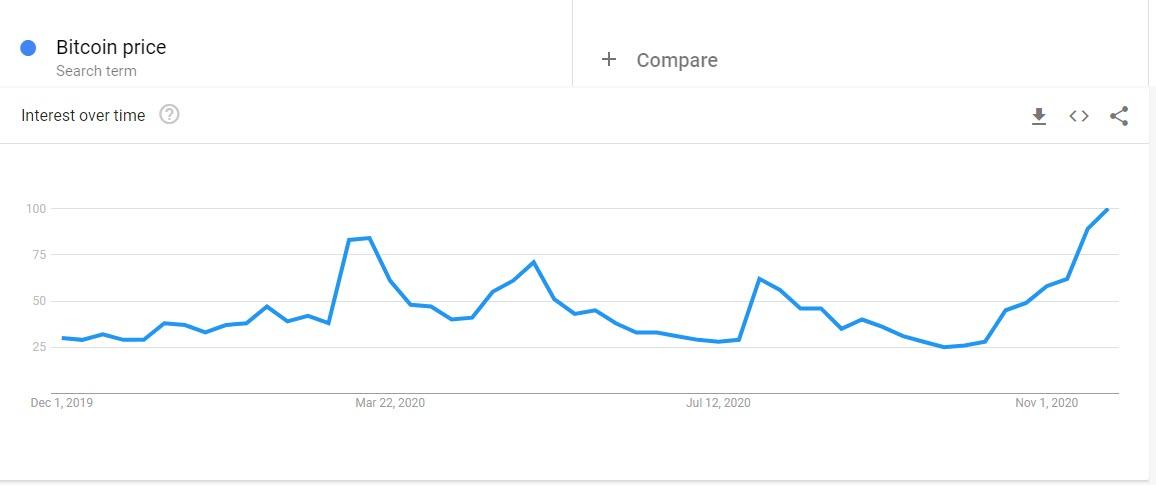

And it appears retail is starting to show interest again as Google searches for Bitcoin Price are at two year highs…

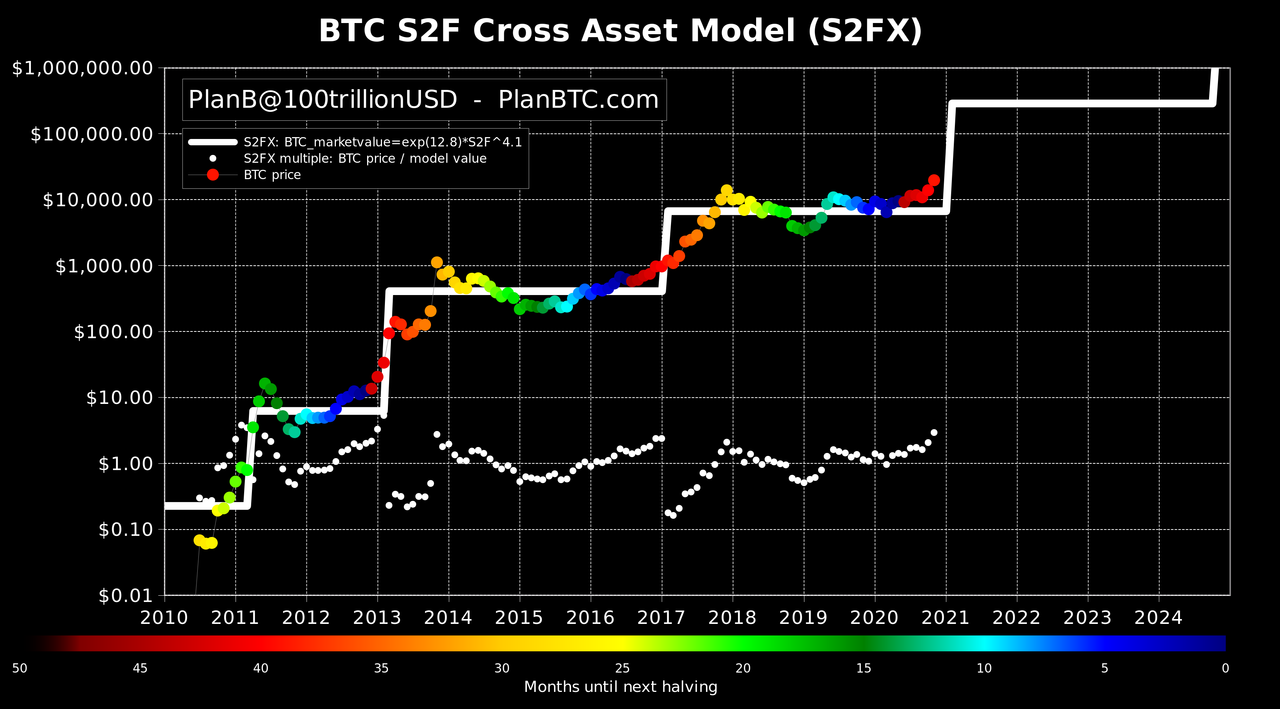

And as institutional interest also picks up, CoinTelegraph notes that “PlanB,” the pseudonymous creator of the stock-to-flow-based family of Bitcoin price models, said on Dec. 1 that all was still going to plan after the most recent halving event in May.

“My fellow Bitcoiners, the bull market is upon us,” he declared, producing the latest version of his Stock-to-Flow Cross-Asset (S2FX) chart showing BTC/USD posting its highest-ever monthly close.

PlanB believes that recent gains mark just the start of Bitcoin’s next phase, a theory which would see Bitcoin simply follow its historical behavior.

“Like clockwork November red dot closed above all other red dots .. at $19,700 .. a new Bitcoin ATH. This is just the beginning. We will see volatility (e.g. -35%), but also new ATHs. Enjoy the ride!” he added.

via ZeroHedge News https://ift.tt/3o4Ja2u Tyler Durden

One of the many interesting scholars I met while researching The Fabric of Civilization was Cécile Michele, a French Assyriologist who has translated many of the 23,000 cuneiform tablets excavated from a site in Turkey. Here she is teaching us the basics of how to write in cuneiform.

The tablets, known as the Old Assyrian private archives, are about 4,000 years old. They were found in the homes of expatriate merchants in the city of Kanesh, now the archaeological site called Kültepe. These letters and legal documents preserve the practices and personalities of a thriving commercial culture. They are our oldest records of long-distance trade.

Capturing dilemmas and decisions still faced by commercial businesses, these ancient records testify to the central role of textiles in the innovations that enable economic exchange. Here, the inventions aren’t material artifacts or physical processes but “social technologies”: the records, agreements, laws, practices, and standards that foster trust, ameliorate risks, and allow transactions across time and distance. Four millennia later, we can still hear the voices they record.

Lamassī was doing her best to keep up with the demand for her fine woolen cloth, fickle though the requirements seemed to be. First her husband asked for less wool in the fabric, and then he asked for more. Why couldn’t he make up his mind? Maybe it was his customers in that distant country. Maybe they didn’t know what they wanted. At any rate, her latest batch of cloth, or most of it, would soon be on its way. She wanted Pūsu-kēn to know it was coming. She wanted him to know she was doing her job. She wanted a little appreciation.

Lamassī rolled a small ball of damp clay between her hands, then flattened and smoothed it into a neat, pillow-shaped tablet, which she cupped in her left palm. She picked up her stylus and began to write, pressing wedge-like characters into the wet clay.

Say to Pūsu-kēn, thus says Lamassī

Kulumāya is bringing you nine textiles. Iddin-Sîn is bringing you three textiles. Ela refused to take any textiles and Iddin-Sîn refused to take another five textiles.

Why do you always write to me, “The textiles that you send me each time aren’t good!” Who is this person living in your house and denigrating the cloth that I send to you? For my part, I do my best to make and send you textiles so that for every trip at least ten shekels of silver can reach your house.

Her message completed, Lamassī dried the tablet in the sun. She then wrapped it in a gauzy fabric, which she coated with a thin layer of clay. She ran a cylindrical seal along the clay envelope to mark the letter as hers. A messenger would take it to her husband, 750 miles away in the Anatolian city of Kanesh.

Lamassī lived in Aššur, on the Tigris river near Mosul in modern-day Iraq. It was a city of middlemen who purchased tin and textiles and exported them, along with their women’s weaving, to Kanesh. Twice a year, caravans of donkeys made the six-week journey. A single caravan might include wares from eight different merchants, with thirty-five donkeys carrying more than a hundred pieces of cloth and two tons of tin. Some of the wares went for taxes in the two cities and in kingdoms along the way that guaranteed safe passage. The rest were traded for silver and gold.

By the time Lamassī picked up her stylus, cuneiform script was a thousand years old. For most of that time, however, writing had been the monopoly of a small class of specially trained scribes, probably a mere one percent of the population. Throughout most of human history, in fact, literacy belonged to the few, mostly men working for state or religious institutions.

Not so in Aššur.

For its people, letters were a critical technology. They needed to send instructions between Aššur and Kanesh and between Kanesh and the surrounding towns, where their agents sold textiles and tin. They needed to record orders, sales, loans, and other contracts. They needed the flexibility and control that come with literacy.

Over time, these pragmatic merchants simplified the cuneiform script, making it easier to learn and write. They invented new punctuation that let them skim documents quickly. Some wrote well, others poorly. But in this society of long-distance traders, most men and many women were literate.

Trade requires clear communication, particularly if the business owner doesn’t conduct every negotiation personally. Consider Pūsu-kēn. He first went to Kanesh as the agent of an older merchant in Aššur and, even as his own ventures grew, he continued to work on behalf of various traders back home. When their textiles and tin arrived in Kanesh, he needed to know what to do with the goods. Should he sell them in the city’s marketplace, sacrificing profits for immediate cash? Or should he seek a higher price by selling them on credit to an agent who worked the outlying towns? Letters came with the goods, telling him what to do.

Letters are such an old technology that we take them for granted. But they were crucial to long-distance trade. When commerce stretched over time and distance, written correspondence—and the literacy it required—came with it.

from Latest – Reason.com https://ift.tt/2KLEAYr

via IFTTT

Futures Soar Just Shy Of Record Highs As Meltup Returns Ahead Of Powell Hearing Tyler Durden

Tue, 12/01/2020 – 07:54

S&P futures and global stocks started the last month of the year on a euphoric note, rallying to just below all time highs following a freak one-day selloff (perhaps on pension-rebalance selling) to close November after robust China data boosted expectations of a recovery from the COVID-19 downturn and as drugmakers seek fast approval for their vaccines and authorities look set to keep stimulus support.

E-mini futures jumped 1%, more than reversing all of Monday’s losses while the MSCI world equity index was up 0.4%. News that Tesla would be added to the S&P500 all in one move on Dec 21 propelled the stock to new record highs above $600 and boosted the broader Nasdaq. Meanwhile work from Home darling Zoom dropped despite reporting stellar results and guiding higher than forecast.

The risk-on mood carried across other markets. Bitcoin was on the verge of $20,000 before it was hit with a sharp selloff, while futures on the Russell 2000 Index outperformed the tech-heavy Nasdaq 100 Index. Breakthroughs in vaccine developments from Pfizer, Moderna and AstraZeneca last month along with news that Janet Yellen would head the Treasury helped the world equity index surge the most on record, up 12% to new all-time peaks.

On Monday, Moderna applied for U.S. emergency authorization for its COVID-19 vaccine after full results from a late-stage study showed it was 94.1% effective with no serious safety concerns, while in the latest vaccine news, this morning Pfizer and partner BioNTech sought regulatory clearance for their Covid-19 vaccine in the European Union, putting the shot on track for potential approval there before the end of the year.

“We believe the rally can continue, with the current pipeline of expected vaccine rollouts in line with our central scenario of widespread availability in the second quarter of 2021,” said Mark Haefele, Chief Investment Officer at UBS Global Wealth Management in Zurich. “We also believe that a divided U.S. government – which looks the most likely outcome – is no impediment to a rising market.”

Europe’s Stoxx 600 Index was 0.7% higher lifted by banks, miners and energy firms. U.K. stocks were up almost 2% after Goldman Sachs Group strategists called them a buy ahead of a Brexit trade deal. Stocks ignored the latest disappointing PMI data which found that Euro zone factory growth cooled last month as renewed coronavirus lockdown measures hurt demand, leaving the bloc lagging many Asian peers who recovered further from the COVID-19 crisis, surveys showed on Tuesday.

The euro zone is on track for its first double-dip recession in nearly a decade, according to a recent Reuters poll of economists, and IHS Markit’s final manufacturing Purchasing Managers’ Index fell to 53.8 in November from October’s 54.8. The Euro area manufacturing PMI for November was revised up by 0.2pt from its flash estimate of 53.6, reflecting upward revisions in both France (+0.5pt) and the periphery (+0.4pt), with a modest downward revision in Germany (-0.1pt). In the UK, the manufacturing PMI rose by more than was initially reported. However, both the Italian and Spanish manufacturing PMIs declined, surprising expectations to the downside, showing a sequential weakening across most subcomponents.

“Manufacturing is not that bad considering the pressure on the economy, but it’s all about services which have lost a lot of momentum,” said Peter Dixon at Commerzbank. While the region’s manufacturing sector continued to expand, an earlier flash reading of the overall survey showed growth in the dominant service industry contracted last month as COVID-19 restrictions were imposed to quell a second wave of infections.

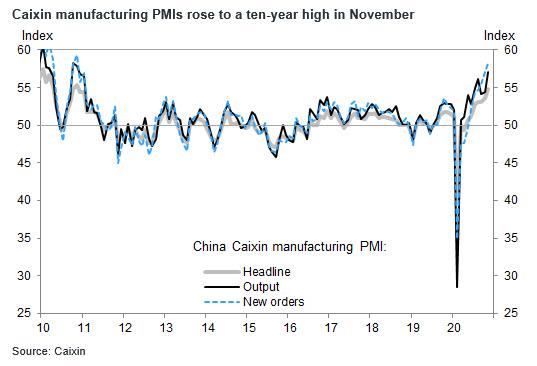

Earlier the MSCI’s broadest index of Asia-Pacific shares outside Japan added 1.3%, while China’s Shanghai Composite Index rose 1.8%, driven by China Merchants Bank and ICBC after the latest Markit (or is that S&P) survey showed on Tuesday activity in China’s factory sector accelerated at the fastest pace in a decade in November.

Trading volume for MSCI Asia Pacific Index members was 22% above the monthly average for this time of the day. The Topix added 0.8%, with Daikin and Shin-Etsu Chemical contributing the most to the move. Japan’s Nikkei rose 1.3% while Australia’s S&P/ASX 200 gained 1.1% after Australia’s central bank said the country’s economy would need fiscal and monetary support “for some time”.

“What we are seeing today is that upward trend reasserting itself, given the positive news on the vaccine front, China’s growth picking up, and the tremendous faith in the ability of central banks to keep the markets afloat,” said Stephen Miller, market strategist for GSFM Funds Management.

It’s not all good news though. Fed Chair Jerome Powell is expected to caution lawmakers that the U.S. economy remains in a damaged and uncertain state. In testimony released ahead of a Tuesday hearing before the Senate Banking Committee, Powell gave no indication how the central bank may respond to those worries when it conducts its next policy meeting even as he warned that a slowing recovery and a surging pandemic meant the U.S. was entering a “challenging” few months, with the potential deployment of a vaccine still facing hurdles.

In foreign exchange markets, the dollar was under pressure after closing out its worst month since July with a little bounce and as investors reckon on even more U.S. monetary easing. The Bloomberg Dollar Spot Index dropped 0.3%, near a fresh two-year low, as the pound rose to the highest level since early September as officials sounded an optimistic tone on negotiations over a U.K. trade deal with the European Union. Sweden’s krona led gains after posting its biggest drop in a month versus the dollar on Monday. Australia’s dollar gained as the central bank pledged to continue supporting the recovery. The yen was little changed as gains in stocks dented demand for haven assets. The ZAR lead gains in EM FX, while TRY faded losses after a short-lived move above 7.90/USD.

As the dollar slide continued, China’s yuan surged the most in two weeks in offshore trading, bolstered by surging risk appetite globally, equity inflows from overseas, and signs that exporters were selling dollars to start the month. The offshore yuan rose as much as 0.49% to 6.5519 versus the dollar, the biggest gain since Nov. 16. The rebound came after the currency weakened a total of 0.32% in the last three trading days of November, its longest losing streak in a month.

The U.S. bond market was steady, as the U.S. Congress began a two-week sprint to secure government funding and avoid a possible shutdown amid the coronavirus pandemic. U.S. 10-year Treasury yields were up slightly at 0.8438%. Germany’s benchmark 10-year bond yield hovered near three-week lows, a touch lower in early trade at -0.574%, close to Monday’s three-week low of -0.60% while peripheral European bonds were briefly rattled by words of caution from ECB’s Schnabel, who warned against hopes for blockbuster stimulus although traders later dismissed his warning saying the it does not signal a game-changer.

In other markets, and reflecting the upbeat mood, copper prices rose with Shanghai prices hitting a more than eight-year high, helped by the robust Chinese data. Oil prices however were slightly lower after leading producers delayed talks on 2021 output policy, while the coronavirus pandemic continued to sap fuel demand. OPEC+ delayed talks on output policy for next year until Thursday as key players still disagreed on how much oil they should pump amid weak demand; gold advanced back over $1800.

Looking at the day ahead there are a number of highlights including the release of the November manufacturing PMIs from around the world, Fed Chair Powell testifying with Treasury Secretary Mnuchin before the Senate banking Committee, and ECB President Lagarde speaking at an Atlantic Council event. Otherwise, data releases include the ISM manufacturing reading in the US, the flash estimate of the Euro Area’s CPI for November and Canada’s GDP for September. Other central bank speakers include the Fed’s Brainard, Daly and Evans.

Market Snapshot

S&P 500 futures up 1% to 3,657.75

STOXX Europe 600 up 0.8% to 392.40

German 10Y yield rose 0.8 bps to -0.563%

Euro up 0.4% to $1.1975

Italian 10Y yield rose 3.2 bps to 0.515%

Spanish 10Y yield rose 2.0 bps to 0.101%

MXAP up 1.1% to 191.28

MXAPJ up 1.3% to 629.67

Nikkei up 1.3% to 26,787.54

Topix up 0.8% to 1,768.38

Hang Seng Index up 0.9% to 26,567.68

Shanghai Composite up 1.8% to 3,451.94

Sensex up 1.3% to 44,710.59

Australia S&P/ASX 200 up 1.1% to 6,588.54

Kospi up 1.7% to 2,634.25

Brent futures up 0.6% to $48.18/bbl

Gold spot up 0.9% to $1,792.98

U.S. Dollar Index down 0.2% to 91.69

Top Overnight News from Bloomberg

President-elect Joe Biden is setting up his first confirmation fight with Senate Republicans by choosing Neera Tanden — a sometimes-acerbic Democratic policy wonk with an often-partisan Twitter feed — to serve as his White House budget chief

Bitcoin has shot to a record just as billions of institutional dollars have fled gold. The the debate is now heating up on whether the world’s largest digital currency can one day rival bullion as an inflation hedge and portfolio diversifier

German manufacturing recorded solid growth in November. Factories are benefiting from a rebound in global trade after a slump earlier in the year. Respondents to IHS Markit’s monthly survey pointed to export demand across Europe and from China

U.K. house prices rose 6.5% last month from a year earlier, the fastest pace in almost six years, as the property market defied a wider economic slump

U.K. Prime Minister Boris Johnson battled to win support for his coronavirus strategy from lawmakers in his Conservative Party after they threatened to undermine his authority in a vote in the House of Commons scheduled for Tuesday

Asian equity markets traded positively as strong data releases helped the region shrug-off the weak handover from US where stocks were pressured by month-end flows in which cyclicals underperformed and most major indices finished in negative territory, although the DJIA still notched its best monthly performance in more than 3 decades with a monthly gain of almost 12%. ASX 200 (+1.1%) advanced from the open with broad optimism across its sectors aside from energy following similar underperformance stateside and with the OPEC+ meeting postponed to Thursday to provide additional time for talks amid disagreements regarding extension of current production levels. Nikkei 225 (+1.3%) benefitted from more favourable currency flows which provided reprieve for Japanese exporters, while the KOSPI (+1.7%) was boosted after the upward revision to South Korean GDP for Q3 which was increased to 2.1% Q/Q from the preliminary 1.9% growth. Hang Seng (+0.9%) and Shanghai Comp. (+1.8%) conformed to the upbeat mood following the blockbuster Caixin Manufacturing PMI data which printed at a decade high of 54.9 vs. Exp. 53.5 and spurred Chinese markets to pick up from the slow start after the PBoC drained liquidity and with China’s new export control laws taking effect today, while Hong Kong had also announced further COVID-19 restrictions to curb the latest wave of the virus. Finally, 10yr JGBs saw mild gains despite the positive risk tone and mixed results at the 10yr JGB auction, as prices extended on the rebound from support through the key 152.00 level.

Top Asian News

RBA Keeps Key Rate, Yield Unchanged, as Seen by All Economists

Armenia Withdraws From Key Azerbaijani Region Under Truce Deal

China’s Top Watchdog Vows ‘Special’ Oversight of Fintech Giants

Hong Kong Virus Surge Scuttles Travel Bubble, Sends Bankers Home

Major European bourses see gains across the board (Euro Stoxx 50 +1.1%) as the region added to the modest upside seen at the cash open after taking its cue from positive APAC session. State-side, US equity futures hold onto gains seen overnight in a retracement of yesterday’s month-end induced losses – with ES +0.8%, NQ +0.7% and YM +1.1%, RTY +1.5%. On the COVID-19 front, distribution of a vaccine is seemingly unlikely this year as the European Medicine Agency (EMA) is to express an opinion on the Pfizer/BioNTech vaccine on December 29th, according to sources cited by FT whilst Moderna’s shot discussion will take place on January 12th and AstraZeneca’s vaccine will not be scrutinised before January. Back to Europe, the region experiences broad-based upside with sectors also higher across the board and with a pro-cyclical bias vs. the mixed performance seen at the open. As such, Basic Resources, Banks, Oil & Gas and Autos top the charts whilst Healthcare, Staples and Utilities reside on the other end of the spectrum. As such, the SMI’s (+0.1%) gains are hampered given its heavy exposure to the pharma sector. The energy sector meanwhile rose from the ashes amid the price action in the energy complex. In terms of individual movers, UniCredit (-6.2%) share remain pressured after following CEO Mustier is to step down following clashes with the board over strategy. Mustier will remain in his post until either the end of his term of until a successor has been appointed. Elsewhere, Munich Re (+1.7%) shares saw a leg higher after setting FY20 targets whilst noting the pandemic impact on next year’s financials will be considerably lower.

Top European News

Swiss Economy Grew Most in Four Decades After Curbs Lifted

Bayer Raises $1.6 Billion by Selling Most of Stake in Elanco

VW Puts Audi at Center of Taking on Tesla With EVs, Software

Macron U- Turn Leaves French Police Chief to Take Heat Over Abuse

In FX, and looking at the USD, that didn’t last long in terms of a recovery for the Greenback and price action suggests a classic short squeeze once the bulk of or residual month end rebalancing was out of the way. Indeed, the DXY only managed a fleeting appearance back above 92.000 late Monday before receding again and is back below the round number within a 91.964-603 range having rebounded from 91.504 to 92.051 amidst another upturn in risk sentiment at the start of December awaiting the final US Markit manufacturing PMI, ISM, construction spending and the first testimony from Fed chair Powell that has been somewhat pre-empted by the release of his text.

GBP/EUR – The Pound has picked up the baton from the Euro in terms of testing psychological resistance vs the Buck, at 1.3400, but like the single currency it has failed to sustain momentum as Brexit trade talks remain stymied on the 3 key issues and UK Cabinet Minister Gove concedes that there may be no negotiated outcome. However, Eur/Gbp is holding around 0.8960 after touching 0.9000 yesterday following an upward revision to the final manufacturing PMI that marginally eclipsed the Eurozone upgrade after mixed individual member state readings. Hence, Eur/Usd remains capped below 1.2000 and 1 bn option expiry interest from the big figure up to 1.2010, albeit recouping losses after its reversal to sub-1.1930.

NZD/CHF/CAD/AUD – All firmer against their US counterpart, but to varying degrees as the Kiwi consolidates off 0.7050 peaks in the run up to NZ trade data and Franc pivots 0.9070 in wake of stronger than forecast Swiss GDP and manufacturing PMI. Elsewhere, the Loonie is holding 1.3000+ status and eyeing crude prices in advance of OPEC for further direction and the Aussie is straddling 0.7350 post-RBA (unchanged policy settings in line with consensus so soon after aggressive easing last time) and conflicting leads via building approvals, current account and net export releases overnight. Next up, Q3 GDP before a speech from RBA Governor Lowe later on Wednesday.

JPY – The Yen is still caught between stalls as it tracks Dollar moves in response to the overall market tone and its own standing as a safe haven, but has retreated through 104.00 to test support into 104.50 after several failed attempts to breach recent highs. Nevertheless, Usd/Jpy appears unlikely to threaten decent option expiries between 104.85-105.00 (1 bn) at this stage.

SCANDI/EM – Contrasting fortunes for the Sek and Nok in keeping with the respective Swedish and Norwegian manufacturing PMIs, while the latter also looks apprehensive given the delay in scheduling for OPEC+ due to the lack of agreement within the cartel on extending output curbs. Meanwhile, the Cnh continues bounce with assistance from another strong Chinese PMI (Caixin manufacturing) and irrespective of the PBoC setting a softer Cny midpoint fix, in contrast to the Try after a slowdown in Turkey’s manufacturing PMI.

In commodities, WTI and Brent futures see a choppy session whereby the benchmarks nursed earlier losses seen in wake of the OPEC+ meeting postponement to Dec 3rd which was due to ministers being unable to reach concensus on potential tweaks to the Declaration of Cooperation (Doc), although ministers are set to meet today at 13:00GMT/08:00EST for further negotiations, and thus source reports throughout the day are expected (Note: the Newsquawk OPEC Twitter Dashboard is available via the website). Meanwhile, markets are yet to see the implications of Saudi Arabia resining from its role as chairman of the OPEC-plus alliance and co-chairman of the JMMC, with some speculation doing the rounds of increased risks of a price war. Eyes are also on UAE who seemingly has not commmitted itself to a particularly course of action, and with recent reports resurfacing that the Kingdom is may drop out of the OPEC alliance. In terms of recent commentary from members, the Algerian Energy Ministry struck an optimistic tone with regards to reaching an accord whilst Kremlin stated that President Putin will not consult with Russian oil companies ahead of the OPEC+ meeting. WTI Jan has reclaimed a USD 45/bbl handle (vs. low 44.81/bbl) whilst Brent Feb 21 sees itself on either side of USD 48/bbl (vs. low 47.40/bbl). Elsewhere, spot gold and silver prices are underpinned by the softer Buck as the former breached 1800/oz to the upside alongside its 200DMA ~1801/oz, whilst the latter re-gained a footing above USD 23/bbl. Finally, LME copper prices are bolstered by the softer Dollar and stock market gains as the contracts mimic price action seen in Shanghai futures.

US Event Calendar

9:45am: Markit US Manufacturing PMI, est. 56.7, prior 56.7

10am: ISM Manufacturing, est. 58, prior 59.3; New Orders, prior 67.9; Prices Paid, est. 65, prior 65.5; Employment, prior 53.2

10am: Construction Spending MoM, est. 0.8%, prior 0.3%

Wards Total Vehicle Sales, est. 16.1m, prior 16.2m

DB’s Jim Reid concludes the overnight wrap

I’ve hated Christmas for many more years of my life than I’ve enjoyed it but I’m going through a good relationship with the event at the moment. I’ve now heard Last Xmas, two Xmas trees are up at home, the advent calendars are awaiting the children this morning, and the twins are now old enough to get excited about Xmas and Santa. Oh and I’ve just bought myself an early Xmas present heavily discounted and second hand on eBay. Yes it’s is a golf trolley that follows you round the course via Bluetooth without you having to touch anything on it. This is my example of “revenge shopping” as after not playing for a month due to lockdown 2 I will be playing again on Saturday and wanted to treat myself. I’ll let you know on Monday whether the Bluetooth fails (it is second hand) and it runs off and rips up the green and gets me chucked out of my club.

So as advent calendars get popped around the world, we can reflect on the best month for some equities markets on record which is an astonishing statistic. We will publish our monthly performance review around 30 minutes after this goes out and you can view the sea of positivity that November brought. As a highlight the STOXX 600 in Europe capped off its strongest monthly performance in price terms (+13.73%) since the index was created, as did the small-cap Russell 2000 index (+18.29%) in the US. Meanwhile Bitcoin soared to an all-time record yesterday of $19,379, bringing its gains for the month to +42.08%, which itself follows a +27.39% rise in October. Haven assets were the place to avoid in November however, even as the dollar index rose slightly yesterday (+0.09%) just off a 2-year low, as gold shed a further -0.61% on the last day of the month to cap off the precious metal’s worst month (-5.42%) for 4 years.

Even though it was a record month, the last day was a little bit of a dampener on what went on before as investors paused for breath following the unprecedented rally. However futures are back up this morning wiping out yesterday losses at the moment. Before that yesterday saw a move back into some of the defensive large cap tech names, with Apple (+2.11%) for example, having a good day and helping US equities recover from the lows yesterday. By the close, the S&P 500 had fallen -0.46% from its Friday record, with a broad-based decline that saw 71% of the index moving lower, as the Dow Jones (-0.91%) moved even lower. The NASDAQ (-0.06%) nearly ended in positive territory though due to strong performance from Semiconductors (+1.66%), Tech hardware (+1.61%) and Biotech (+0.53%) to a lesser degree. In Europe most of the continent’s major indices including the STOXX 600 (-0.98%) moved lower. 18 of the 20 STOXX 600 sectors dipped as only Retail (+0.56%) and Health care (+0.07%) pulled out gains. Energy was the worst performer on both sides of the Atlantic, -3.43% in Europe and -5.37% in the US as the reflation trades lost ground in addition to the OPEC meeting not going as expected.

The OPEC+ meeting that was planned for today has been rescheduled until Thursday as the member nations needed “further consultations”. Yesterday’s meeting of the countries’ ministers appeared to reach a consensus on rolling the existing production cuts for a further three months though. However, some countries want that extension made contingent on all nations meeting their targets. OPEC+ is expected to continue discussions in the next two days to hammer out details ahead of the new meeting on Thursday. Oil prices whipsawed around the news of the extension, with WTI and Brent crude seeing multiple 2% moves in either direction all session long before WTI ended the day down -0.42% and Brent crude fell -1.22%, but the latter future had closed before the meeting extension news.

As discussed above markets are back to their recent winning ways overnight with the Nikkei (+1.41%), Hang Seng (+0.98%), Shanghai Comp (+1.31%), Kospi (+1.60%) and Asx (+1.09%) all up. Futures on the S&P are up +0.81%. In terms of overnight data releases, China’s November Caixin manufacturing PMI affirmed yesterday message from the official release as it printed at 54.9 (vs. 53.5 expected), the highest reading in 10 years. Japan’s final manufacturing PMI also came in 0.7pts above the flash at 49.0. Manufacturing PMIs for other countries in the region were also mostly strong with South Korea (at 52.9 vs. 51.2 last month), Taiwan (56.9 vs. 55.1) Indonesia (50.6 vs. 47.8) and India (56.3 vs. 58.9) all reporting robust prints. Vietnam was an exception with the PMI declining to 49.9 from 51.8 last month. We’ll see the European and US data later so all eyes on that.

In other news, Fed chair Powell said in testimony released ahead of today’s hearing before the Senate Banking Committee that the US economy remains in a damaged and uncertain state, though recent news on the vaccine front “is very positive for the medium term.” More this afternoon but there were no real surprises.

On the virus, the main news yesterday came from Moderna, which announced that it would be requesting an Emergency Use Authorization from the FDA in the US, as well as a conditional marketing authorisation with the European Medicines Agency. Their vaccine is 94.1% effective and all of the severe Covid cases occurred in the placebo group. In response, the company’s share price rose by a further +20.24% yesterday. In other vaccine news, Novavax’s announced that the company’s study in the U.K. reached full enrollment and would have results soon. The news caused the shares to rise +10.99% on the day after being down -9.60% premarket after worries about delays in reporting elsewhere. Sticking with vaccines, Axios has reported overnight that the White House has summoned the US FDA chief Stephen Hahn to justify why he hasn’t moved faster to approve the Pfizer vaccine.

In terms of the other developments yesterday, the UK saw its 7-day average of confirmed cases fall below 15k for the first time since mid-October. It comes ahead of the regional tier system coming back in England tomorrow, with today being the last day of the England-wide lockdown. Elsewhere France saw positive news as well with the lowest daily rise in cases since August, as ICU and general hospitalisations stats continued to trend lower as well. Meanwhile, Turkey has announced a nationwide weekday curfew starting at 9 pm and ending at 5 am as the country copes with about 30,000 new cases per day. Similarly, the US news was not so positive even as daily counts are currently clouded by lower testing capacity around the Thanksgiving holiday weekend. New York City, at one point the epicenter of the virus in the US, saw their weekly average positivity rate rise over 4%. Meanwhile New York state overall is seeing elective surgery halted in northern counties as the Governor anticipates possible stress to the hospital system during the winter. In fact the number of Americans hospitalised with Covid-19 is at the highest at any point of the pandemic. California is considering a return to stay-at-home orders as hospitalisations soar, with projections showing that intensive-care demand will exceed capacity.

Back to yesterday and there was a reasonable selloff in sovereign bond markets especially in Europe. Yields on 10yr bunds (+1.7bp) and BTPs (+1.4bps) rose. The one exception was Greek debt, where the country’s spread over 10yr bunds fell -3.0bps to 1.21%, its tightest since 2009 before the sovereign debt crisis kicked off.

On Brexit, we’ve now reached the final month of the transition period, which is set to conclude at 11pm London time on December 31. Yesterday didn’t see anything concrete from the negotiations, though an EU source told Reuters that talks in London over the weekend had been “quite difficult” and there were “massive divergences” on the long-standing sticking points. In separate remarks, German Chancellor Merkel said that it would be a bad example for the rest of the world if the UK and the EU didn’t manage to reach an agreement.

In terms of yesterday’s data, UK mortgage approvals soared to 97.5k in October, which was their highest level since September 2007. It comes amidst a temporary cut in the tax on home purchases, which is set to last until the end of March and is seeing a number of buyers bring forward transactions so as to avoid it. Otherwise, preliminary inflation data for Germany in November showed an accelerating decline in consumer prices, having fallen by -0.7% year-on-year on the EU-harmonised measure, matching the post-GFC low set in July 2009. Italy saw more moderate deflation of -0.3% over the same period, up from the previous month’s -0.6% reading. Finally in the US, the data slightly underwhelmed expectations, with pending home sales falling -1.1% in October (vs. +1.0% expected), while the Dallas Fed’s manufacturing index fell to 12.0 (vs. 14.3 expected).

To the day ahead now, and there are a number of highlights including the release of the November manufacturing PMIs from around the world, Fed Chair Powell testifying with Treasury Secretary Mnuchin before the Senate banking Committee, and ECB President Lagarde speaking at an Atlantic Council event. Otherwise, data releases include the ISM manufacturing reading in the US, the flash estimate of the Euro Area’s CPI for November and Canada’s GDP for September. Other central bank speakers include the Fed’s Brainard, Daly and Evans.

via ZeroHedge News https://ift.tt/2KXzpVx Tyler Durden

Our goal is $200,000 this year, and we hope you’ll

Our goal is $200,000 this year, and we hope you’ll

{kind=link}

{kind=link}

{kind=link}