“Picking Quarrels & Provoking Trouble” – China Slams Journalist With 4 Years In Jail Over COVID Reporting

At the beginning of the pandemic, the Communist Party filled the airwaves with positive headlines about how well it was mitigating the virus’ spread. The Chinese government also went on a censoring spree, removing online content posted by journalists or citizen-journalist who reported firsthand accounts of the public health crisis unfolding in Wuhan, China, the epicenter of COVID-19. The government even went to the extent of detaining people who reported on the crisis, alleging they were spreading lies.

Citizen journalist Zhang Zhan is the first known person to be handed a four-year jail term for her reporting in Wuhan.

Zhan provided firsthand accounts of overcrowded hospitals and empty streets that challenged the government’s official narrative.

She was convicted on Monday at the Shanghai Pudong New Area People’s Court for “picking quarrels and provoking trouble,” according to Reuters.

The verdict is a warning to all journalists in the country that the communist government is coming after those who exposed their shortcomings during the initial months of the virus outbreak. More importantly, Zhan’s case shows the government has a zero-tolerance policy for critics.

“I don’t understand. All she did was say a few true words, and for that she got four years,” said Shao Wenxia, Zhan’s mother, who attended the trial.

Zhan’s lawyer Ren Quanniu was quoted by Reuters:

“We will probably appeal,” adding that the trial at a court in Pudong, a district of the business hub of Shanghai, ended at 12.30 p.m.

Before the trial, he said, “Zhan believes she is being persecuted for exercising her freedom of speech.”

Kenneth Roth, the Geneva-based executive director of Human Rights Watch, tweeted that China intentionally planned for Zhan’s trial to be held over the Western holiday to minimize attention.

“Beijing’s selection of the sleepy period between Christmas and New Year’s suggests even it is embarrassed to sentence citizen-journalist Zhang Zhan to four years in prison for having chronicled the uncensored version of the coronavirus outbreak in Wuhan,” tweeted Roth.

Zhang is among a handful of journalists who covered the outbreak in Wuhan. Others like her have been detained and are awaiting sentencing or ordered by the government to stop reporting.

For its part, Jonathan Turley writes that the Chinese government has denied any failures in its policies towards COVID despite overwhelming evidence of a cover-up that denied the world critical time to contain and fight the spread of the virus.

Notably, the Chinese continue to scrub any discussion of its role in social media. It is a chilling example of the censorship that is now being embraced by many in the United States. The Atlantic published an article by Harvard Law School professor Jack Goldsmith and University of Arizona law professor Andrew Keane Woods calling for Chinese style censorship of the internet. They declared that “in the great debate of the past two decades about freedom versus control of the network, China was largely right and the United States was largely wrong” and “significant monitoring and speech control are inevitable components of a mature and flourishing internet, and governments must play a large role in these practices to ensure that the internet is compatible with society norms and values.”

At the same time, Democrats have embraced censorship and speech controls. We have have been discussing how writers, editors, commentators, and academics have embraced rising calls for censorship and speech controls, including President-elect Joe Biden and his key advisers. The erosion of free speech has been radically accelerated by the Big Tech and social media companies. The level of censorship and viewpoint regulation has raised questions of a new type of state media where companies advance an ideological agenda with political allies.

From Laguerre v. Maurice, decided Wednesday by the New York Appellate Division (Justice Sheri S. Roman, joined by Justices Cheryl E. Chambers, Sylvia O. Hinds–Radix, and Colleen D. Duffy):

[P]laintiff alleges that he was defamed by the pastor of the defendant church when the pastor told members of the congregation that the plaintiff was a homosexual who viewed gay pornography on the church’s computer…. The plaintiff is a former elder in the Gethsemane SDA Church …. The defendant Pastor Jean Renald Maurice is the pastor in charge of the church, which allegedly is operated by the defendant The Greater New York Corporation of Seventh Day Adventist….

As set forth in the complaint, Pastor Maurice stated before approximately 300 members of the church that “the [p]laintiff was a homosexual,” and that “the [p]laintiff disrespected the church by viewing gay pornography on the church’s computer.” The complaint alleged that these statements constituted defamation per se, inasmuch as they falsely portrayed the plaintiff “as a homosexual man with no self-control who uses the church’s computer to view gay porn.” The complaint further alleged that Pastor Maurice used these statements to influence the church to vote to relieve the plaintiff of his responsibilities at the church and to terminate his membership….

Some defamation cases within religious organizations can’t be resolved by secular courts, because they require determination of religious doctrine (e.g., if the allegations are that someone has departed from orthodox teachings, or is a Satanic influence). But here the court said that the matter could be resolved “by application of neutral principles of law,” so the Religion Clauses would be no obstacle:

The allegedly defamatory remarks at issue, i.e., that the plaintiff is a homosexual who viewed gay pornography on the church’s computer, may be evaluated without reference to religious principles. The defendants point out that the church manual provides that “[f]ornication,” which includes “homosexual activity,” and the use of “pornographic material” are reasons for which members may be subject to discipline. However, the plaintiff does not challenge his expulsion from the church, or request reinstatement as a church elder. Thus, under the circumstances of this case, resolution of the issues raised would not involve an impermissible inquiry into religious doctrine or practice.

Other defamation cases within organizations are dismissed because of a privilege for “a communication made by one person to another upon a subject in which both have an interest.” But this is a “qualified” privilege, which could be defeated by a showing of “either common-law malice, i.e., spite or ill will, or … actual malice, i.e., knowledge of falsehood of the statement or reckless disregard for the truth,” and here the plaintiff had alleged that the defendant was motivated by both kinds of malice:

[Plaintiff had] alleged … that the plaintiff had a disagreement with Pastor Maurice which initially centered around church-related issues, and that Pastor Maurice stated that, if the plaintiff “[did] not submit to him,” Pastor Maurice would “crumble” the plaintiff.

As further set forth in the complaint, Pastor Maurice allegedly stated that he would make false statements against the plaintiff, and have the church membership vote to relieve the plaintiff of his responsibilities at the church. Accepting the facts as alleged in the complaint to be true, and according the plaintiff the benefit of every possible favorable inference, it sufficiently alleged that Pastor Maurice made false statements of fact with malice so as to overcome the common-interest qualified privilege.

But ultimately the court threw out the lawsuit because mere allegations of homosexuality were no longer so socially or professionally harmful as to warrant a presumption of damages, even the absence of proof of damages:

The elements of a cause of action to recover damages for defamation are (1) a false statement that tends to expose a person to public contempt, hatred, ridicule, aversion, or disgrace, (2) published without privilege or authorization to a third party, (3) amounting to fault as judged by, at a minimum, a negligence standard, and (4) either causing special harm or constituting defamation per se. “Special damages [under New York law] contemplate the loss of something having economic or pecuniary value.” A statement is defamatory per se if it (1) charges the plaintiff with a serious crime; (2) tends to injure the plaintiff in her or his trade, business, or profession; (3) imputes that the plaintiff has a loathsome disease; or (4) imputes unchastity to a woman. “When statements fall within one of these categories, the law presumes that damages will result, and they need not be alleged or proven.” …

In 1984, this Court decided Matherson v. Marchello. In Matherson, the plaintiffs, husband and wife, commenced an action to recover damages for defamation based upon certain statements made during a radio interview by the defendants, members of a singing group [The Good Rats, it turns out -EV]. The plaintiffs alleged, in pertinent part, that the statement directed at the plaintiff husband—”I think it was when somebody started messing around with his boyfriend that he really freaked out”—constituted an imputation of homosexuality which should be recognized as defamatory.

This Court noted that “[i]t cannot be said that social opprobrium of homosexuality does not remain with us today,” and that “[r]ightly or wrongly, many individuals still view homosexuality as immoral.” Additionally, we observed that “[l]egal sanctions imposed upon homosexuals in areas ranging from immigration to military service [had] recently been reaffirmed.” Thus, we concluded that “the potential and probable harm of a false charge of homosexuality, in terms of social and economic impact, cannot be ignored,” and “that the imputation of homosexuality is reasonably susceptible of a defamatory connotation … and is actionable without proof of special damages.” …

[But this and other similar past precedents are] “inconsistent with current public policy and should no longer be followed.” … “[T]he prior cases categorizing statements that falsely impute homosexuality as defamatory per se [were] based upon the flawed premise that it is shameful and disgraceful to be described as lesbian, gay or bisexual,” and that “such a rule necessarily equates individuals who are lesbian, gay or bisexual with those who have committed a ‘serious crime’—one of the four established per se categories.” …

“[I]n light of the tremendous evolution in social attitudes regarding homosexuality, the elimination of … legal sanctions …[,] and the considerable legal protection and respect that the law of this state now accords lesbians, gays and bisexuals, it cannot be said that current public opinion supports a rule that would equate statements imputing homosexuality with accusations of serious criminal conduct or insinuations that an individual has a loathsome disease.” … [T]he decades since Matherson “have seen a veritable sea change in social attitudes about homosexuality,” including [the Supreme Court’s decisions protecting same-sex sexual conduct and same-sex marriage and New York statutes barring sexual orientation discrimination] ….

Based on the foregoing, we conclude that the false imputation of homosexuality does not constitute defamation per se. Matherson’s holding to the contrary should no longer be followed. Furthermore, the additional allegation that the plaintiff viewed gay pornography on the church’s computer likewise does not fit within any of the categories of defamation per se.

Therefore, the plaintiff was required to allege special damages. He failed to do so, and, consequently, his cause of action alleging defamation per se must be dismissed.

Sounds right to me.

from Latest – Reason.com https://ift.tt/37Rfgti

via IFTTT

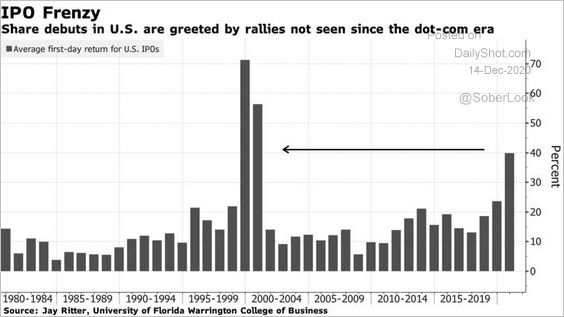

“Maybe this time is different. Those words, supposedly the most dangerous to utter in the investing realm, came to mind amid the frenzied pops in the highly anticipated initial public offerings recently.” That quote was from Randall Forsyth discussing why the current market mania reminds him of the “Shades of 1999.”

There are certainly many similarities between today and 1999. From exceedingly high valuations to a rush by private equity investors to IPO overly priced companies as quickly as possible, prices are high. Of course, such is not possible without an underlying “Fear Of Missing Out, or F.O.M.O.” by retail investors.

As discussed previously, “valuations” are a representation of market excesses.In other words, psychology is key to the formation, and inflation, of a financial bubble. However, it requires a supportive underlying narrative, a “siren’s song” to lure “sailors onto the rocks.”

Price measures the current “psychology” of the “herd” and is the clearest representation of the behavioral dynamics of the living organism we call “the market.”

The Bull Case

My colleague, and always a good read, Greg Feirman at Top Gun Financial Planning, recently had a great post.

In the past cycle, the Fed has become very sensitive to a sudden tightening in financial conditions, especially when equities start to fall aggressively

Another $5 trillion USD is expected to resume in the coming months.

Such would send US equities to new all-time highs

Any bear retracement in the near term is a good opportunity to “buy the dip.”

It is not a good time to try to short equities

One crucial thing that we have learned over the past 12 years is that the Fed has become very sensitive to a sudden tightening in financial conditions, especially when equities start to fall aggressively.”

“When all the experts and forecasts agree – something else is going to happen.”

The Beatings Will Continue

As noted, the “psychology” of a “mania” requires a narrative. In this case, it is the “Fed Put.” As Greg noted:

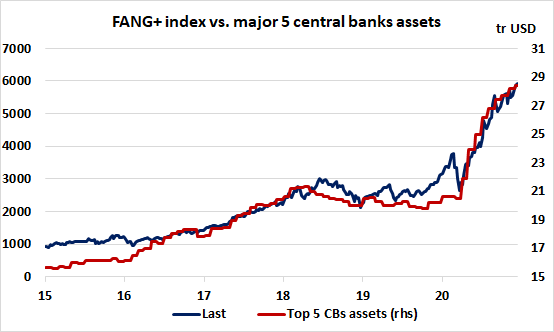

“Why did investors underestimate the force of monetary liquidity after 10 years of sample data? We mentioned previously that stocks could diverge quite significantly from fundamentals amid the massive Fed intervention and the strength of the FANG stocks in the COVID-19 environment. We can notice the titanic rise in central bank assets has ‘perfectly’ matched the strong rebound in the mega-cap growth stocks in the past 8 months.”

In other words, the Fed’s primary goal has been to allow the “beatings to continue until morale improves.”

The repeated rounds of liquidity, interventions, and accommodative policies have trained investors to take on more “risk.” Such was the point we recently discussed in “Moral Hazard.”

“What exactly is the definition of ‘moral hazard.’ It is the lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.”

Moral Hazard

Where do we see evidence of “moral hazard” currently?

You don’t have to look too hard to find it.

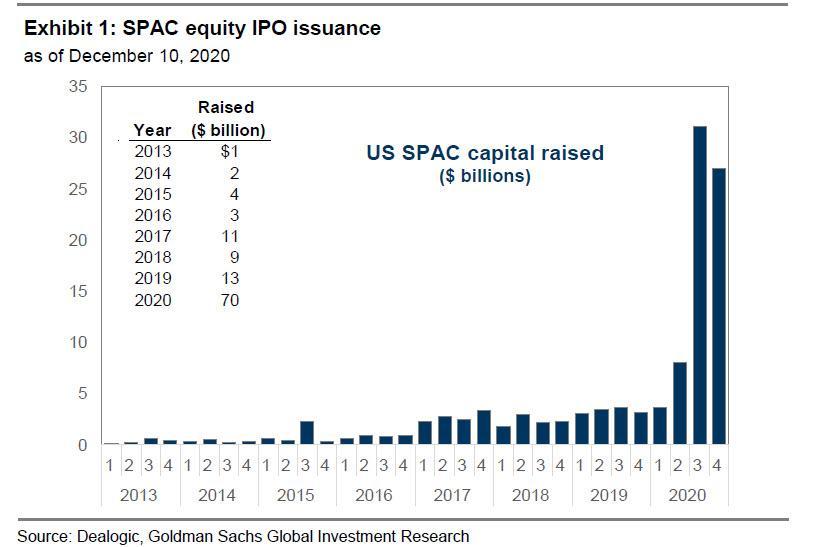

Wall Street is rushing IPO’s to market to fill “speculative demand” from retail investors.

Retail investors are piling into trading equities.

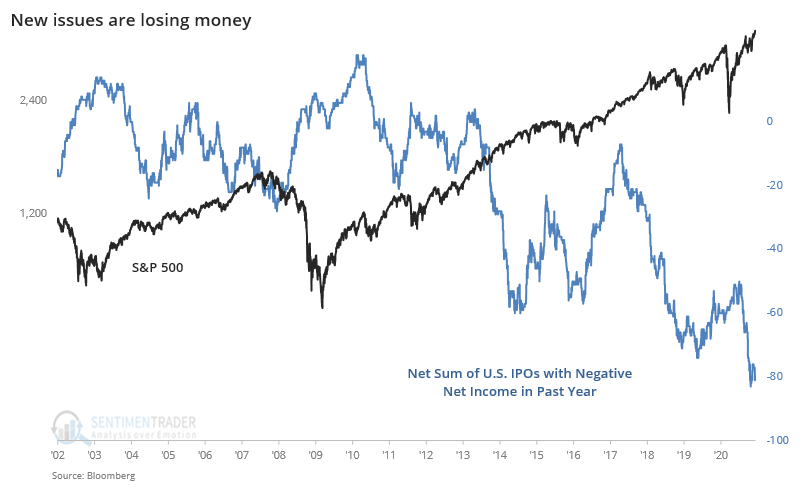

Speculators are paying astronomical multiples for IPO’s of companies with negative incomes.

The rush to invest billions into S.P.A.C.”s, shell companies with no business, in hopes they can find the next “big deal.”

Speculators in the options market increase their bets to leverage returns on risky stocks.

You get the idea.

Speaking of “SPAC exuberance,”Bespoke Investment Group recently published one statistic showing the market’s feeding frenzy. Of the 287 SPACs that have come to market over the last two years, just six are down 10% or more from their IPO price. In contrast, 15 SPACs have more than doubled from their IPO price.

“In other words, more than twice as many SPACs are up 100% as down 10%. If that isn’t a sign of exuberance, we don’t know what is!” – Bespoke

Such activities will not end well. However, the “psychology” is that since the Federal Reserve will not let the markets fall in price, there is “no risk.”

Seen This Picture Before

We have written extensively about the extreme extension we see in the markets. Such is due to the Fed’s ongoing “repo” operations in 2019, and current QE directly fueling a sharp rise in asset prices. The problem is prices are surging at a time when both corporate profits and earnings growth remain weak.

Notably, the ongoing Fed policies have lured investors into an extreme sense of complacency, as witnessed by the sharp drop in “short-interest” in the S&P 500. This belief the markets can no longer have a correction is fueling an equity chase in companies with the most inferior underlying fundamentals.

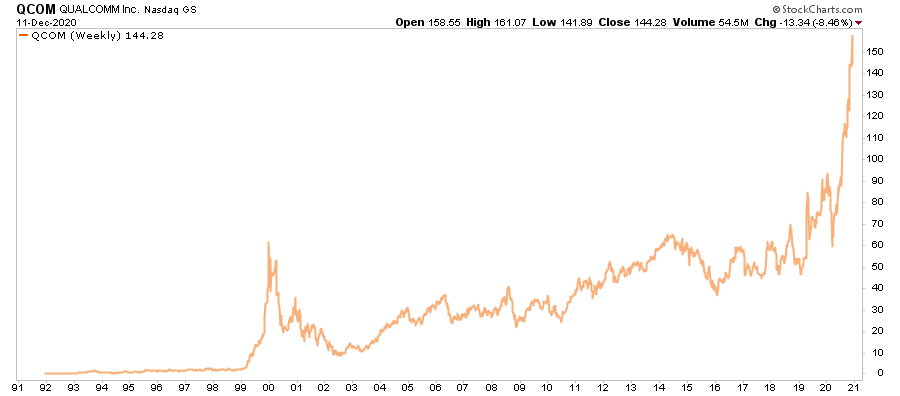

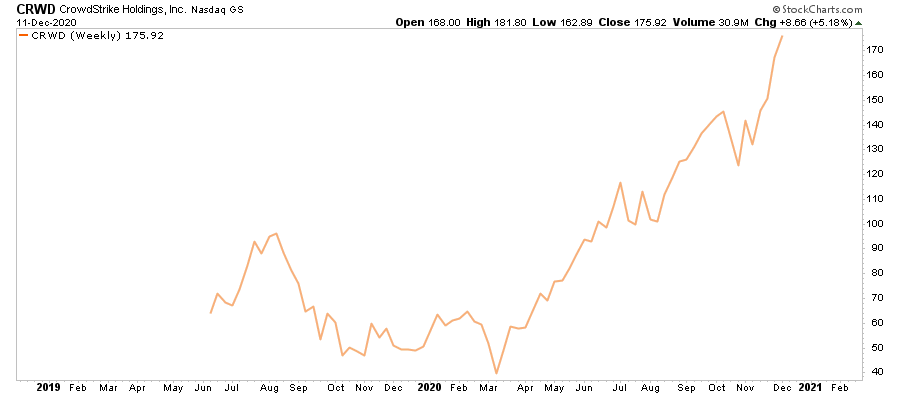

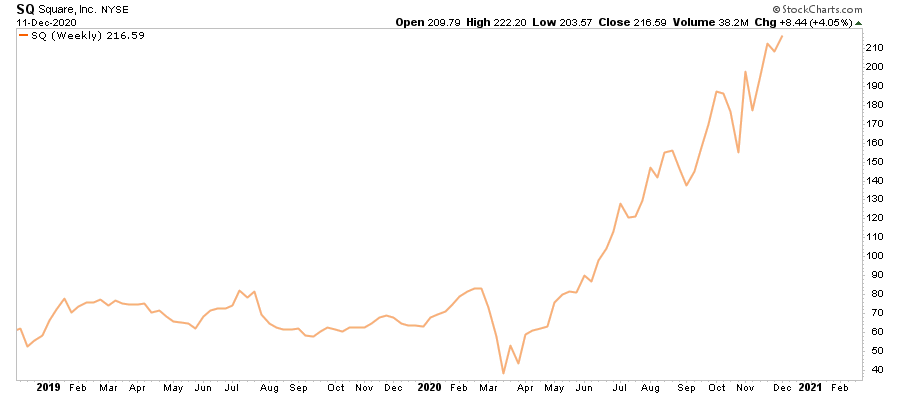

The last time we saw asset prices surge by 20%, or more, in a month, particularly in companies with no revenue, unfavorable valuations, and poor business models, was in 1999. The chart of Qualcomm (QCOM) in late 1999 is a good example.

Unfortunately, for investors in QCOM, by the end of 2000, that 95% gain turned into a 10% loss. But QCOM was not alone. The only difference is that the vast majority of the other companies like Global Crossing, Enron, Worldcom, Lucent Technologies, Sun Micro, and many others no longer exist in the original forms today, if at all.

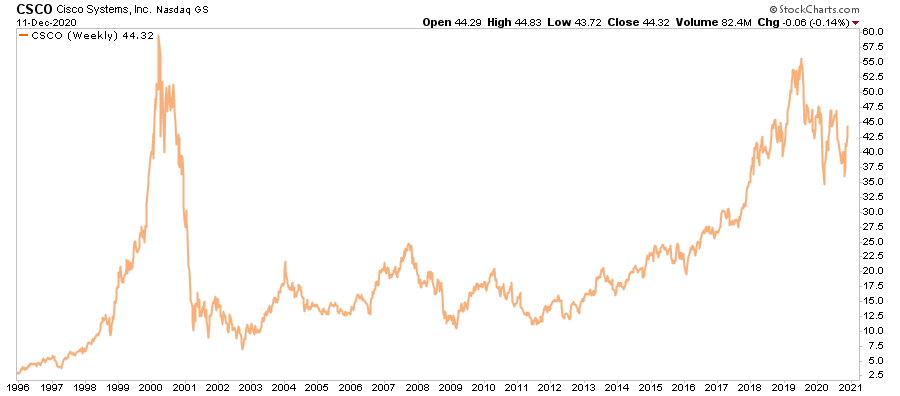

Here is another excellent example, if you had bought CSCO at the turn of the century, you would still be down by 10% on your position 20-years later.

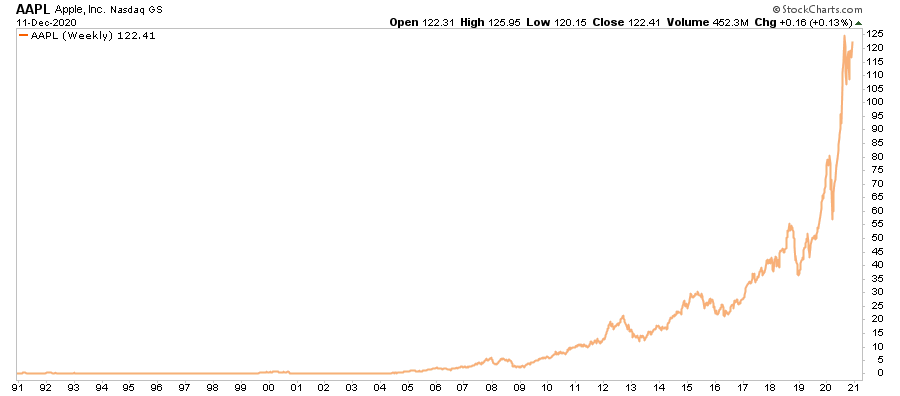

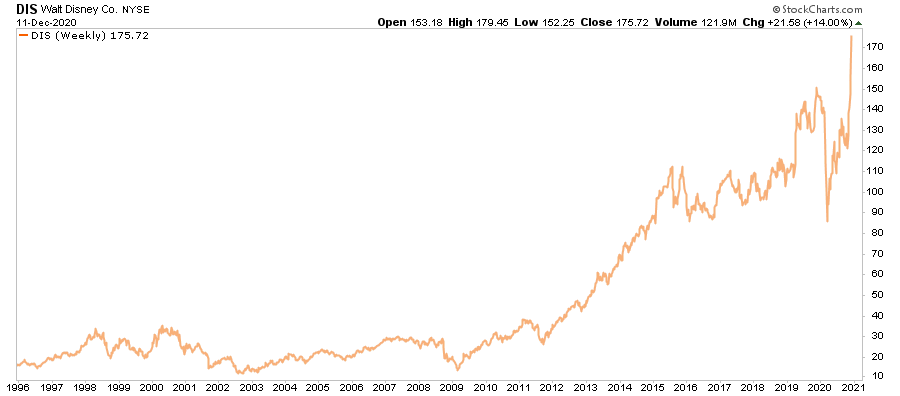

Over the last 5-years, AAPL has barely grown revenue, yet its stock price has gone parabolic. I love the company, but they will never grow revenue to justify the current price.

The same for DIS.

Many suggest stocks are rising in anticipation of growth; such was also the “rationalization” for the last 5-years.

In other words, there is an essential difference between “hoping for growth” and getting it.

The New Breed

Today, we see the same chase in companies that exhibit similar characteristics to what we saw in 1999:

Flawed business models with little, or no, “protective moat.”

Little or no earnings

Excessively high or negative valuations

Prices are rising on “hope” these companies will mature into their valuations in the future.

Sure, companies from Tesla (TSLA) to Zoom Video (ZM) might be the next Amazon (AMZN) of the “dot.com” mania to survive and prosper. However, the odds are highly stacked against that being the case.

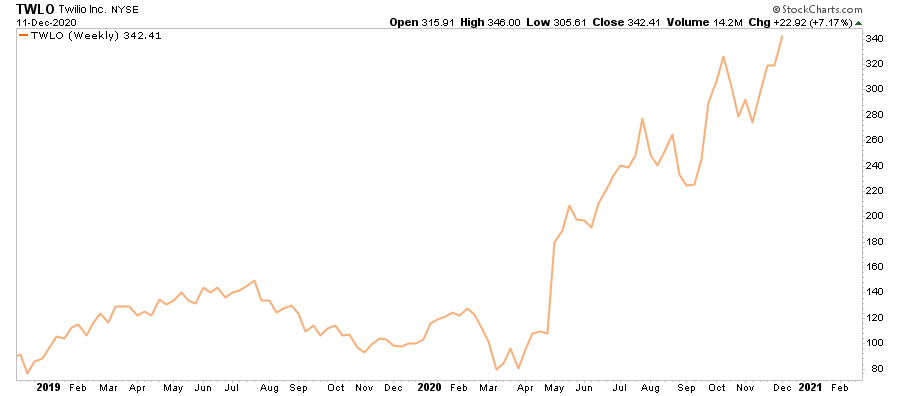

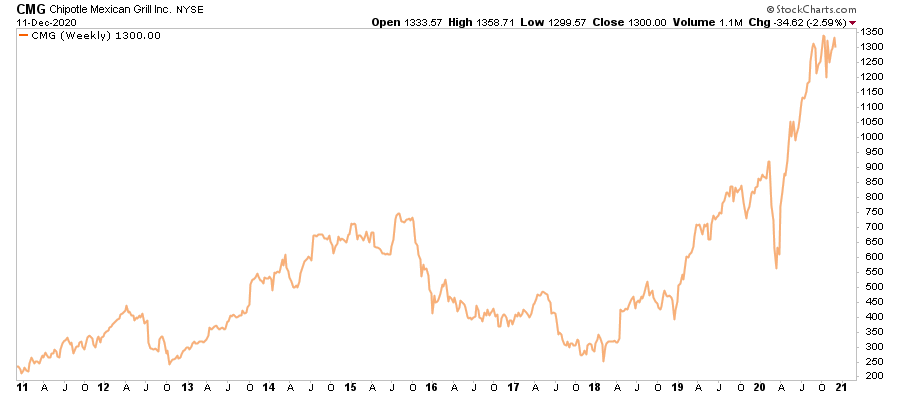

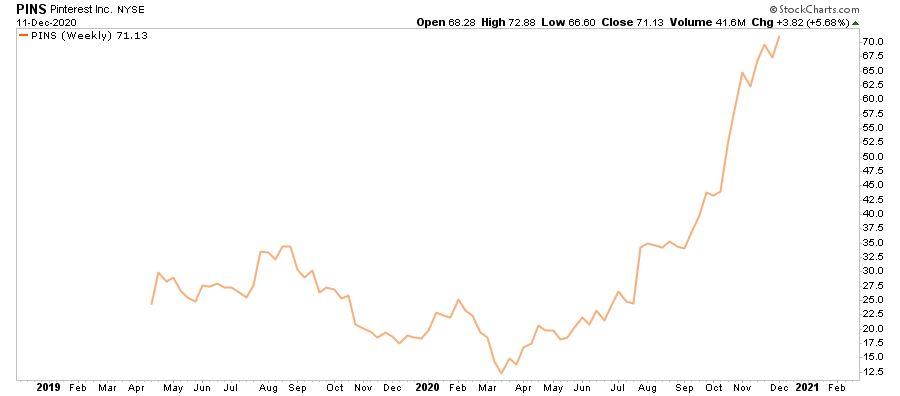

Here are a few examples of why it looks like investors are once again “Partying Like It’s 1999.”

These are but just a few examples. The market is replete with many companies whose price far exceeds any rational grasp of the underlying fundamentals.

But such is always the case when individuals throw out “fundamentals” to chase “price.”

Retail “Investor” Or “Speculator?”

In today’s market, the majority of investors are simply chasing performance.

But, this isn’t “investing,” it’s “speculation.”

Think about it this way.

If you were playing a hand of poker and dealt a “pair of deuces,” would you go “all-in.”

Of course, not.

The reason is you intuitively understand the other factors “at play.” Even a cursory understanding of the game of poker suggests other players at the table are probably holding better hands, which will lead to a rapid reduction of your wealth.

Ultimately, investing is about managing the risks that will substantially reduce your ability to “stay in the game long enough” to “win.”

“Philip Carret, who wrote The Art of Speculation (1930), believed “motive” was the test for determining the difference between investment and speculation. Carret connected the investor to the economics of the business and the speculator to price. ‘Speculation,’ wrote Carret, ‘may be defined as the purchase or sale of securities or commodities in expectation of profiting by fluctuations in their prices.’”

Chasing markets is the purest form of speculation. It is just a bet on prices going higher than determining if the price paid for those assets is a discount to fair value.

Graham & Dodd

Along with David Dodd, Benjamin Graham attempted a precise definition of investing and speculation in their seminal work Security Analysis (1934).

“An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

There is also an essential passage in Graham’s The Intelligent Investor:

“The distinction between investment and speculation in common stocks has always been a useful one and its disappearance is a cause for concern. We have often said that Wall Street as an institution would be well advised to reinstate this distinction and to emphasize it in all its dealings with the public. Otherwise the stock exchanges may some day be blamed for heavy speculative losses, which those who suffered them had not been properly warned against.”

Surviving The Game

Regardless of whether you believe fundamentals will ever matter again is irrelevant. What is essential is that periods of excess speculation always end the same way.

For now, Dave Portnoy has garnered a legion of followers. However, Dave’s financial future is entirely secure after selling his company to Penn National for $450 million. So, when things go wrong in the market, he will be just fine financially. However, for the host of inexperienced, over-confident millennials who follow him, many have the financial livelihoods on the line.

I get it.

If you are one of our younger readers, who have never been through an actual “bear market,” I wouldn’t believe what I am telling you either.

However, after living through the Crash of ’87, managing money through 2000 and 2008, and navigating the “Great Crash of 2020,” I can tell you the signs are all there.

A real bear market will happen. When? I don’t have a clue.

But it will be an unexpected, exogenous event that triggers the selling.

It always appears easiest at the top, and at the bottom retail investors will not want to buy.

Historically, the environment we are living in currently has not worked out well for investors. However, in the short-term, the “irrationality” will last long enough to convince you “this time is different.”

“History doesn’t always repeat itself, but it often rhymes.” – Samuel Clemens

From Laguerre v. Maurice, decided Wednesday by the New York Appellate Division (Justice Sheri S. Roman, joined by Justices Cheryl E. Chambers, Sylvia O. Hinds–Radix, and Colleen D. Duffy):

[P]laintiff alleges that he was defamed by the pastor of the defendant church when the pastor told members of the congregation that the plaintiff was a homosexual who viewed gay pornography on the church’s computer…. The plaintiff is a former elder in the Gethsemane SDA Church …. The defendant Pastor Jean Renald Maurice is the pastor in charge of the church, which allegedly is operated by the defendant The Greater New York Corporation of Seventh Day Adventist….

As set forth in the complaint, Pastor Maurice stated before approximately 300 members of the church that “the [p]laintiff was a homosexual,” and that “the [p]laintiff disrespected the church by viewing gay pornography on the church’s computer.” The complaint alleged that these statements constituted defamation per se, inasmuch as they falsely portrayed the plaintiff “as a homosexual man with no self-control who uses the church’s computer to view gay porn.” The complaint further alleged that Pastor Maurice used these statements to influence the church to vote to relieve the plaintiff of his responsibilities at the church and to terminate his membership….

Some defamation cases within religious organizations can’t be resolved by secular courts, because they require determination of religious doctrine (e.g., if the allegations are that someone has departed from orthodox teachings, or is a Satanic influence). But here the court said that the matter could be resolved “by application of neutral principles of law,” so the Religion Clauses would be no obstacle:

The allegedly defamatory remarks at issue, i.e., that the plaintiff is a homosexual who viewed gay pornography on the church’s computer, may be evaluated without reference to religious principles. The defendants point out that the church manual provides that “[f]ornication,” which includes “homosexual activity,” and the use of “pornographic material” are reasons for which members may be subject to discipline. However, the plaintiff does not challenge his expulsion from the church, or request reinstatement as a church elder. Thus, under the circumstances of this case, resolution of the issues raised would not involve an impermissible inquiry into religious doctrine or practice.

Other defamation cases within organizations are dismissed because of a privilege for “a communication made by one person to another upon a subject in which both have an interest.” But this is a “qualified” privilege, which could be defeated by a showing of “either common-law malice, i.e., spite or ill will, or … actual malice, i.e., knowledge of falsehood of the statement or reckless disregard for the truth,” and here the plaintiff had alleged that the defendant was motivated by both kinds of malice:

[Plaintiff had] alleged … that the plaintiff had a disagreement with Pastor Maurice which initially centered around church-related issues, and that Pastor Maurice stated that, if the plaintiff “[did] not submit to him,” Pastor Maurice would “crumble” the plaintiff.

As further set forth in the complaint, Pastor Maurice allegedly stated that he would make false statements against the plaintiff, and have the church membership vote to relieve the plaintiff of his responsibilities at the church. Accepting the facts as alleged in the complaint to be true, and according the plaintiff the benefit of every possible favorable inference, it sufficiently alleged that Pastor Maurice made false statements of fact with malice so as to overcome the common-interest qualified privilege.

But ultimately the court threw out the lawsuit because mere allegations of homosexuality were no longer so socially or professionally harmful as to warrant a presumption of damages, even the absence of proof of damages:

The elements of a cause of action to recover damages for defamation are (1) a false statement that tends to expose a person to public contempt, hatred, ridicule, aversion, or disgrace, (2) published without privilege or authorization to a third party, (3) amounting to fault as judged by, at a minimum, a negligence standard, and (4) either causing special harm or constituting defamation per se. “Special damages [under New York law] contemplate the loss of something having economic or pecuniary value.” A statement is defamatory per se if it (1) charges the plaintiff with a serious crime; (2) tends to injure the plaintiff in her or his trade, business, or profession; (3) imputes that the plaintiff has a loathsome disease; or (4) imputes unchastity to a woman. “When statements fall within one of these categories, the law presumes that damages will result, and they need not be alleged or proven.” …

In 1984, this Court decided Matherson v. Marchello. In Matherson, the plaintiffs, husband and wife, commenced an action to recover damages for defamation based upon certain statements made during a radio interview by the defendants, members of a singing group [The Good Rats, it turns out -EV]. The plaintiffs alleged, in pertinent part, that the statement directed at the plaintiff husband—”I think it was when somebody started messing around with his boyfriend that he really freaked out”—constituted an imputation of homosexuality which should be recognized as defamatory.

This Court noted that “[i]t cannot be said that social opprobrium of homosexuality does not remain with us today,” and that “[r]ightly or wrongly, many individuals still view homosexuality as immoral.” Additionally, we observed that “[l]egal sanctions imposed upon homosexuals in areas ranging from immigration to military service [had] recently been reaffirmed.” Thus, we concluded that “the potential and probable harm of a false charge of homosexuality, in terms of social and economic impact, cannot be ignored,” and “that the imputation of homosexuality is reasonably susceptible of a defamatory connotation … and is actionable without proof of special damages.” …

[But this and other similar past precedents are] “inconsistent with current public policy and should no longer be followed.” … “[T]he prior cases categorizing statements that falsely impute homosexuality as defamatory per se [were] based upon the flawed premise that it is shameful and disgraceful to be described as lesbian, gay or bisexual,” and that “such a rule necessarily equates individuals who are lesbian, gay or bisexual with those who have committed a ‘serious crime’—one of the four established per se categories.” …

“[I]n light of the tremendous evolution in social attitudes regarding homosexuality, the elimination of … legal sanctions …[,] and the considerable legal protection and respect that the law of this state now accords lesbians, gays and bisexuals, it cannot be said that current public opinion supports a rule that would equate statements imputing homosexuality with accusations of serious criminal conduct or insinuations that an individual has a loathsome disease.” … [T]he decades since Matherson “have seen a veritable sea change in social attitudes about homosexuality,” including [the Supreme Court’s decisions protecting same-sex sexual conduct and same-sex marriage and New York statutes barring sexual orientation discrimination] ….

Based on the foregoing, we conclude that the false imputation of homosexuality does not constitute defamation per se. Matherson’s holding to the contrary should no longer be followed. Furthermore, the additional allegation that the plaintiff viewed gay pornography on the church’s computer likewise does not fit within any of the categories of defamation per se.

Therefore, the plaintiff was required to allege special damages. He failed to do so, and, consequently, his cause of action alleging defamation per se must be dismissed.

Sounds right to me.

from Latest – Reason.com https://ift.tt/37Rfgti

via IFTTT

Futures, Global Stocks Jump After Trump Signs Coronavirus Stimulus Package

Global stocks jumped and US equity futures spiked in light overnight trading, after President Trump unexpectedly signed the $2.3 trillion spending package on Sunday evening and as investors continued to celebrate a last-minute trade deal clinched between Britain and the European Union.

By backing down from his previous threat to block the bipartisan bill, Trump allowed millions of Americans to continue receiving unemployment benefits and averted a federal government shutdown.

“As the coronavirus pandemic has shown little sign of abating, the emergency aid was needed to avoid a sharp slowdown in the economy during the first quarter,” said Nobuhiko Kuramochi, market strategist at Mizuho Securities. “It would have been unsettling if we hadn’t had it by the end of year,” he added.

The rollouts of COVID-19 vaccines were also bolstering hopes of more economic normalisation next year, with Europe launching a mass vaccination drive on Sunday, which however has been met with rising skepticism.

That for now has offset alarm over a new, highly infectious variant of the virus that has been raging in England and was confirmed in many other countries, including Japan, France and Canada, over the weekend.

The MSCI world index rose 0.3% boosted by strong opening gains in Europe and a positive session in Asia overnight, although trading was thinner due to the holiday season.

The euro STOXX index rose 0.9% in the first trading session after London and Brussels signed an eleventh hour deal on Thursday evening that preserves zero tariff access to each other’s markets. Germany’s DAX Index climbed to a record while British markets were closed for the Boxing Day holiday.

“We can finally move on from the Brexit drama,” said Win Thin, global head of currency strategy at Brown Brothers Harriman. “After the last-minute deal was struck last week, the UK parliament will vote on the deal Wednesday. With (opposition party) Labour promising its support, it should pass handily,” he added.

Earlier in the session, Asian stocks rose after capping their first weekly drop in two months Friday. Stock markets in Indonesia, Taiwan and India led a broad regional advance as the MSCI Asia Pacific Index climbed 0.4% with Japan’s Nikkei advancing 0.7% and China also rising, helped by strong industrial profit data. Gains in Samsung Electronics and Taiwan Semiconductor Manufacturing helped a gauge of regional technology names rally more than 1%. IT was the best-performing sector even as Alibaba tumbled, leading a selloff in Chinese tech giants, triggered by fears antitrust scrutiny will spread beyond Jack Ma’s Internet empire.

An index of Asian communication services stocks was the sole loser among industry groups. Tencent Holdings slid more than 6% to be the biggest drag on the measure. Meanwhile, utilities and finance were the other top-performing industry groups in Asia Monday. Stocks in the Philippines and Thailand bucked the region’s rising trend amid concerns over virus outbreaks and related restrictions in those countries. Philippine President Rodrigo Duterte said he’s open to reinstating tighter movement curbs if coronavirus infections spike. Markets in Australia and New Zealand remained closed for holiday.

In FX, the dollar fell 0.2% to 90.028; analysts believe the dollar will stay under pressure as investors bet on a prolonged period of loose U.S. monetary policy. The euro was up 0.1% at $1.2206, a tad below its 2-1/2-year high of $1.22735, while the yen changed hands at 103.41 per dollar. The British pound slumped in anticipation of the EU-UK trade deal, as traders sold the news pushing cable to 1.3487, down 100 pips on the session.

In rates, 10-year yields rose to 0.9581% and 10-year German bund yields inched lower to -0.550%. Treasuries opened lower with the curve steeper after Trump relented on the stimulus deal, with a compressed Treasury auction cycle (2- and 5-year notes Monday, 7-year notes Tuesday) totaling $176 billion is an additional headwind. Yields are higher by nearly 4bp at long end, leaving 2s10s and 5s30s spreads wider by 2bp-3bp; 10-year ~0.955%, 3bp cheaper vs. Dec. 24 close

In commodities, oil prices rose, with Brent crude futures up 0.7% at $51.67 per barrel and U.S. crude futures up 0.8%. Precious metals were flat despite gold rising 1.3% at one point to a one week high as investors welcomed Trump’s signing of the pandemic aid bill, with a weaker dollar lending further support. However, they have since given up all gains. One can’t say the same thing for cryptos however, with the entire sector continuing its relentless surge higher. Bitcoin, which hit a new record high over the weekend, was up 2.2% at $26,876, bringing the total value of the cryptocurrency in circulation to over $500 billion.

No major economic data releases or U.S. company earnings are expected.

Market Snapshot

S&P 500 futures up 0.6% to 3,716.75

STOXX Europe 600 up 0.6% to 398.31

German 10Y yield unchanged at -0.547%

Euro up 0.4% to $1.2239

Brent Futures up 1.1% to $51.83/bbl

Italian 10Y yield unchanged at 0.474%

Spanish 10Y yield fell 0.5 bps to 0.068%

MXAP up 0.4% to 195.53

MXAPJ up 0.08% to 644.47

Nikkei up 0.7% to 26,854.03

Topix up 0.5% to 1,788.04

Hang Seng Index down 0.3% to 26,314.63

Shanghai Composite up 0.02% to 3,397.29

Sensex up 0.8% to 47,353.04

Australia S&P/ASX 200 up 0.3% to 6,664.77

Kospi up 0.06% to 2,808.60

Brent Futures up 1.1% to $51.83/bbl

Gold spot down 0.01% to $1,883.24

U.S. Dollar Index down 0.2% to 90.03

Top overnight news from Bloomberg

Prime Minister Boris Johnson said major changes are coming in the U.K. as the result of the trade deal his government negotiated with the European Union, completing the country’s separation from the bloc, the Telegraph reported. Major Issues the Brexit Deal Leaves Unresolved

A coordinated vaccination campaign is under way in Europe, just days after the European Union cleared a shot developed by Pfizer Inc. and BioNTech SE. The U.K. could clear AstraZeneca Plc’s vaccine as early as this week

Japan’s industrial production failed to eke out an overall gain in November, slowing more than expected from previous advances amid a resurgence in the coronavirus at home and abroad

Oil fell in Asian trading as pessimism over a new strain of Covid-19 that’s threatening more travel restrictions outweighed the passage of a U.S. stimulus bill into law

US Event Calendar

10:30am: Dallas Fed Manf. Activity, est. 10.2, prior 12

Please feel free to write comments on this post on whatever topic you like! (As usual, please avoid personal insults of each other, vulgarities aimed at each other or at third parties, or other things that are likely to poison the discussion.)

from Latest – Reason.com https://ift.tt/3mNM3Uk

via IFTTT

12/28/1856: President Woodrow Wilson’s birthday. His administration would initiate the prosecutions under the Sedition Act that gave rise to Schenck v. U.S., Debs v. U.S., and Abrams v. U.S.

from Latest – Reason.com https://ift.tt/3mRNiSw

via IFTTT

Please feel free to write comments on this post on whatever topic you like! (As usual, please avoid personal insults of each other, vulgarities aimed at each other or at third parties, or other things that are likely to poison the discussion.)

from Latest – Reason.com https://ift.tt/3mNM3Uk

via IFTTT

12/28/1856: President Woodrow Wilson’s birthday. His administration would initiate the prosecutions under the Sedition Act that gave rise to Schenck v. U.S., Debs v. U.S., and Abrams v. U.S.

from Latest – Reason.com https://ift.tt/3mRNiSw

via IFTTT

EU Nations Unanimously Approve Brexit Deal As UK Warns Businesses To “Prepare For A Bumpy Ride”

It has been two days since Brussels and London finally released the text of the draft trade deal struck between UK and the EU negotiators last week, and on Monday morning, EU leaders officially signed off on the deal, clearing one of the last major hurdles for what is expected to be a historic trade deal.

Germany, which presently holds the EU presidency, announced the decision came during a meeting of EU ambassadors on Monday, which was called to assess the 1,200+ page deal.

According to the AP, Germany’s spokesman Sebastian Fischer confirmed the “Green light” to the press, proclaiming that the EU Ambassadors had “unanimously approved the provisional application of the EU-UK Trade and Cooperation Agreement as of January 1, 2021.”

Now the deal goes to a last-minute vote. Given the timing, there will be almost no room for error, as the new rules outlined in the last-minute agreement will take effect on Thursday.

The full text of the agreement can be found here, along with a Q&A to try and help businesses and private citizens better understand the coming changes.

However, four days after finally striking a deal, the UK’s Michael Gove has warned businesses to get ready for disruptions and “bumpy moments” when the new rules take effect on Thursday night.

Gove told BBC‘s morning program that “I’m sure there will be bumpy moments but we are there in order to try to do everything we can to smooth the path.” He added that time was “very short” to make the final preparations before the transition period ends.

“The nature of our new relationship with the EU – outside the Single Market and Customs Union – means that there are practical and procedural changes that businesses and citizens need to get ready for,” Gove continued.

“We know that there will be some disruption as we adjust to new ways of doing business with the EU, so it is vital that we all take the necessary action now.”

In other Brexit-related commentary, UK Chancellor Rishi Sunak said in an interview Monday morning that financial services firms in the UK shouldn’t take the 1,246-page agreement as the final word on EU market access, offering up hope for services-based business like finance that the lack of provision in the trade deal for services – which comprise 80% of the UK economy – won’t cause too much economic disruption, after PM Boris Johnson admitted that the deal’s provisions for market access fell short of his hopes.

Votes on the text of the deal in Parliament and the EU Parliament, which will represent the final obstacles to the deal being officially ratified, are scheduled for Wednesday.