China Braces For “Nightmare Scenario” As Evergrande Offers Broke Investors Discounted Apartments

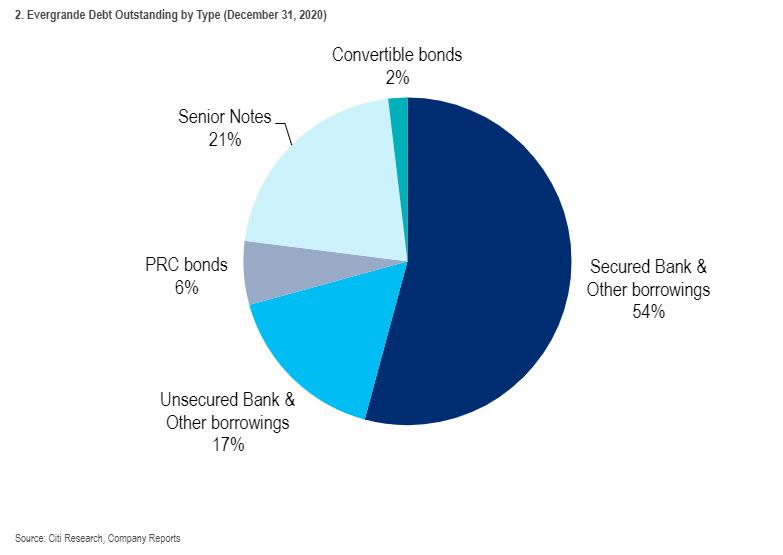

Up until now the collapse of China’s Evergrande was very much a slow motion affair, captured perhaps best by Forte Securities trader Keith Temperton who said that “the Asian banks will get hit hard if there’s a default, but then there will be a 10-year recovery process. The market’s getting a hang of it. The way they’ve managed the news flow seems quite clever. They haven’t let a swathe of bad news at once.” But while Beijing was indeed successful in extending the period of collapse as long as possible, now that Evergrande is effectively insolvent and having suspended its bonds from trading we have finally gotten to the endgame and the realization that hundreds of billions in capital (Evergrande’s total debt was just over $300 billion) is gone for ever.

This realization has already prompted angry protesters at China Evergrande Group offices across the country as the developer has fallen further behind on promises to more than 70,000 investors. Construction of unfinished properties with enough floor space to cover three-fourths of Manhattan grinds to a halt, leaving more than a million homebuyers in limbo.

In an effort to appease its angry (and very soon, poor) stakeholders, Evergrande plans to let consumers and staff bid on discounted properties this month to repay them for billions in overdue investment products as the embattled developer seeks to preserve cash, according to people familiar with the matter.

According to Bloomberg, the company will organize an online property event by Sept. 30 for investors who opt for discounted real estate in lieu of cash, said two employees who were briefed on an internal call Thursday and asked not to be identified. The world’s most-indebted property developer is pushing the discounted real estate as the preferred of three options for angry investors seeking repayments.

The high-yield “shadow bank” products paying as much as 13% a year have become a lightning rod for cash-strapped Evergrande, with investors and staff protesting losses and delayed payments from investments that were marketed as safe. Indeed, demonstrations that are breaking out across China could sway any bailout decisions by the government, which places a high priority on social stability, although it’s likely too late for that.

More than 70,000 people bought the products, including many Evergrande employees, Bloomberg reported earlier, citing an executive of Evergrande’s wealth division. And with about 40 billion yuan ($6.2 billion) of them are now due according to Caixin, there is about to be a whole lot of angry investors, who will not be swayed by the company’s hail mary plan to offer steep discounts on property assets. Investors can invest in residential housing units at a 28% discount, offices at a 46% discount and stores and parking units at 52%. Discounted rates can’t be lower than price floors designated by local governments. The property discounts are a voluntary repayment option, according to the briefing.

And while we wait to see what the acceptance rate on this bizarre debt-for-apartments exchange offer will be, the reality of the absurd situation is finally seeping in and is pummeling China’s already shaky real estate market, where new land sales just crashed by 90% in August…

… in the process squeezing other developers and rippling through a supply chain that accounts for more than a quarter of Chinese economic output. And as fear of contagion and exposure to Evergrande has finally emerged, credit-market stress spreads from lower-rated property companies to stronger peers and banks as global investors who bought $527 billion of Chinese stocks and bonds in the 15 months through June begin to sell.

This, in turn, brings us to China’s nightmare scenario: an uncontrolled bankruptcy which escalates into an all out economic crash.

As Bloomberg notes, it’s impossible to know for sure what would happen if Beijing allows Evergrande’s downward spiral to continue unabated, but China watchers are already mapping out worst-case scenarios as they contemplate how much pain the Communist Party is willing to tolerate. Pressure to intervene is growing as signs of financial contagion increase and as more and more popular anger builds.

“As a systemically important developer, an Evergrande bankruptcy would cause problems for the entire property sector,” said Shen Meng, director at Beijing investment bank Chanson & Co. “Debt recovery efforts by creditors would lead to fire sales of assets and hit housing prices. Profit margins across the supply chain would be squeezed. It would also lead to panic selling in capital markets.”

Evergrande had 1.3 trillion yuan ($202 billion) in presale liabilities at the end of June, equivalent to about 1.4 million individual properties that it has committed to complete, according to a Capital Economics report last week. “If Evergrande had to dump its inventory onto the market” it would “drag down property prices substantially,” said Hao Hong, chief strategist at Bocom International.

Such an outcome would be catastrophic for China’s economy, where real estate represents 70% of household net worth, but absent a full-blown bailout by Beijing which would appear as glaring weakness coming so late into the process, it is unclear what other alternatives are viable even if Shen, and virtually all other analysts and investors discussing Evergrande say Beijing is in no mood for a Lehman moment. Instead, rather than allow a chaotic collapse into bankruptcy, they predict regulators will engineer a restructuring of Evergrande’s $300 billion pile of liabilities that keeps systemic risk to a minimum.

While markets seem to agree with the Shanghai Composite Index less than 3% from a six-year high and the yuan is near the strongest level in three months against the dollar, it is unclear just how Beijing – which did not allow corporate debt restructurings until a few years ago – will oversee a bankruptcy process that would be substantially bigger and more complicated than that of Lehman brothers.

Even Bloomberg agrees that “a benign outcome is far from assured” and reminds us of Beijing’s bungled stock-market rescue in 2015 which showed how difficult it can be for central planning policymakers to control financial outcomes, even in a system where the government runs most of the banks and can exert outsized pressure on creditors, suppliers and other counterparties.

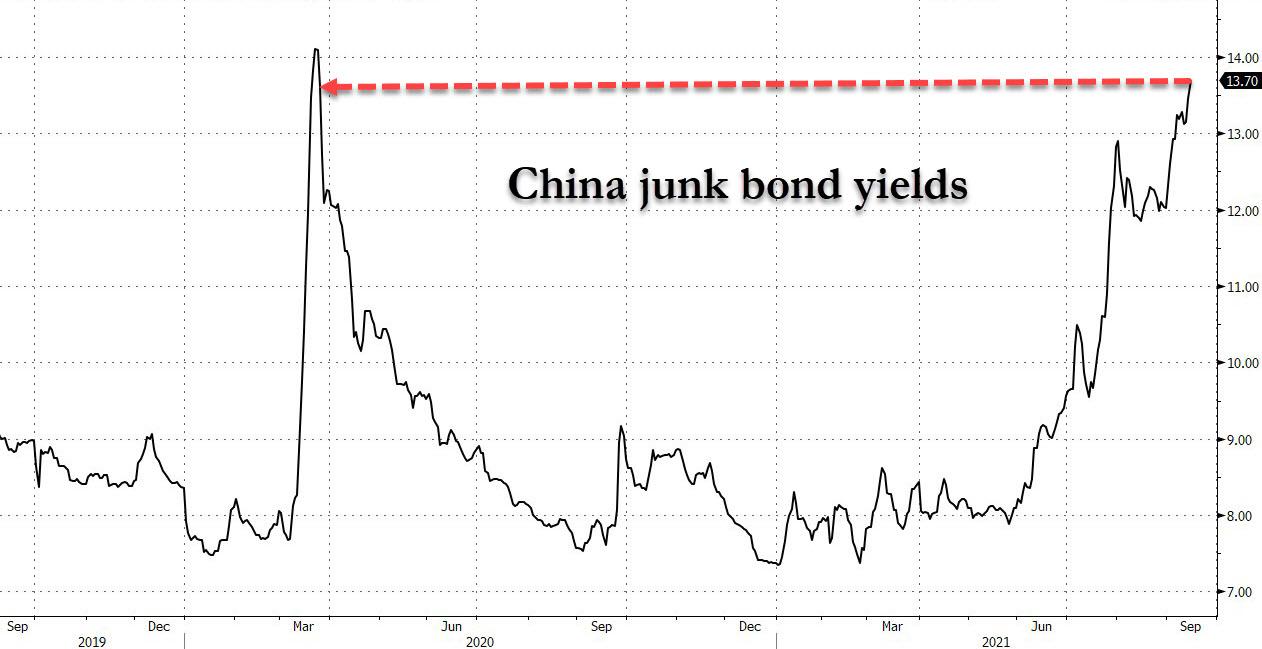

And while equities continue to exist in a world of their own where nothing can go wrong, some parts of the market are starting to crask amid the surge in contagion risk: as noted in recent days, Chinese junk-bond yields jumped to an 18-month high and shares of real estate companies plunged after Evergrande had its credit rating downgraded and requested a trading halt in its onshore bonds. Furthermore, ahead of what many fear could become a cascading liquidity crisis, banks in China are hoarding yuan at the highest cost in almost four years, a sign they may be preparing for what a Mizuho Financial Group Inc. strategist called a “liquidity squeeze in crisis mode.”

With so much unclear, where Xi will ultimately draw the line to contain the fallout remains a mystery. While China’s top financial regulator has urged billionaire Evergrande founder Hui Ka Yan to solve his company’s debt problems, authorities have yet to spell out how they envision him backstopping hundreds of billions in liabilities, and even whether the government would allow a major debt restructuring or bankruptcy. Adding to the China’s recent deleveraging campaign would lose credibility

Even senior officials at state-owned banks have told Bloomberg that they’re confused and still waiting for guidance on a long-term solution from top leaders in Beijing. Evergrande’s main banks were told by China’s housing ministry this week that the developer won’t be able to make interest payments due Sept. 20.

To be sure, China’s government isn’t averse to nationalizing failed private companies: in 2019, Beijing seized Baoshang Bank and assumed control of HNA Group, the once-sprawling conglomerate in early 2020 after the coronavirus pandemic decimated the company’s main travel business. Court-led restructurings have also become more common in recent years, with more than 700 being completed in 2020.

Ultimately, rhe Evergrande endgame will depend largely on how Xi balances his goals of maintaining social and financial stability against his multi-year campaign to reduce moral hazard (spoiler alert: in a country of 1.4 billion people preventing social unrest will always win over moral hazard). Then again, the timing is particularly tricky as China juggles an economic slowdown, a sweeping crackdown on the private sector and rising tensions with Washington – all in the runup to a once-in-five-year leadership reshuffle in 2022 at which Xi is set to extend his indefinite rule.

So while some sort of rescue is likely, “the government has to be very, very careful in balancing support for Evergrande,” said Yu Yong, a former China Banking and Insurance Regulatory Commission regulator and now chief risk officer at China Agriculture Reinsurance Fund.

“Property is the biggest bubble that everyone has been talking about in China,” Yu told Everbright Sun Hung Kai analyst Jonas Short in a recent podcast. “So if anything happens, this could clearly cause systematic risk to the whole China economy.”

Courtesy of Bloomberg, here are some of the factors that may sway Chinese leaders:

Social Unrest – Maintaining social order has always been a key priority for the Communist Party, which has no tolerance for protests of any kind. In Guangzhou, homebuyers surrounded a local housing bureau last week to demand Evergrande restart stalled construction. Disgruntled retail investors have gathered at the company’s Shenzhen headquarters for at least three straight days this week, and videos of protests against the developer in other parts of China have been shared widely online (see video above). Without a social safety net and with limited places to put their money, Chinese savers have for years been encouraged to buy homes whose prices were only ever supposed to go up (similar to the US before 2007 when even idiots like Ben Bernanke said that the US housing market never goes down). Today, buying a house (or two) is a cultural touchstone. While housing affordability has become a hot topic in the West, many Chinese are more likely to protest falling home prices than spiking ones.

“Given that the bulk of people’s wealth is already in property, even a 10% correction would be a serious knock to many people,” said Fraser Howie, an independent analyst and co-author of books on Chinese finance who has been following the country’s corporate sector for decades. “It would certainly knock their hopes and dreams and expectations about what property is.”

Shadow banks: Another potential flashpoint is whether Evergrande can repay high-yield wealth management products that it sold to thousands of retail investors, including many of its own employees. About 40 billion yuan of the WMPs are due to be repaid, according to Caixin, a Chinese financial news service. Evergrande is trying to free up cash by selling assets, including stakes in its electric-car and property-management businesses, but has so far made little progress.

Capital Markets: Evergrande is the largest high-yield dollar bond issuer in China, accounting for 16% of outstanding notes, according to Bank of America. Should the company collapse, that alone would push the default rate on the country’s junk dollar bond market to 14% from 3%. While Beijing has become more comfortable with allowing weaker businesses to fail, an uncontrolled spike in offshore funding costs would risk derailing a key source of financing. It could also undermine global confidence in the country’s issuers at a time when Beijing is pushing for larger foreign investor ownership. Yields on China’s junk dollar bonds are nearing 14%, up from about 7.4% in February, according to a Bloomberg index, largely due to the crash in Evergrande debt.

The stakes are even higher on the mainland, where the yuan-denominated credit market is about 15 times the size at $12 trillion. While Evergrande is less of a whale onshore, a collapse could force banks to cut their holdings of corporate notes and even freeze money markets, the plumbing of China’s financial system. In such a credit crunch, the government or central bank would be forced to act. Banks involved in property lending may come under pressure, leading to an increase in soured loans. Smaller banks exposed to Evergrande or other weaker developers may face “significant” increases in non-performing loans in the event of a default, according to Fitch Ratings.

Economic Impact: Concern over Evergrande comes at a time when China’s economy is slowing sharply. Aggressive controls to curb outbreaks of Covid-19 are hurting retail spending and travel, while measures to cool property prices are taking a toll. Data this week showed home sales by value slumped 20% in August from a year earlier, the biggest drop since the onset of the coronavirus early last year. Responding to a question on Evergrande’s potential impact on the economy, National Bureau of Statistics spokesman Fu Linghui said some large property enterprises are running into difficulties and the fallout “remains to be seen.”

China’s current priorities of promoting “common prosperity” and deterring excessive risk-taking mean there’s unlikely to be any easing of property curbs this year, according to Macquarie Group Ltd. The sector will be a “main growth headwind” for next year, although policy makers may loosen restrictions to defend growth goals, Macquarie analysts wrote in a Wednesday note.

A crash in China’s property market would not only slow the domestic economy but have global consequences too.

“A significant slowdown in property construction over the next few years appears probable already, and would become even more likely in the event of an Evergrande failure or bankruptcy,” said Logan Wright, a Hong Kong-based director at research firm Rhodium Group LLC. “A long-term slowdown in property construction, an industry that represents around a fifth or a quarter of China’s economy by most estimates, would cause a significant decline in GDP growth, commodity demand, and would likely have disinflationary effects globally.”

* * *

The bottom line is that while stocks stubbornly refuse to reflect the huge risks faced by China in the coming days when Evergrande’s fate will be revealed, the reality is that a nightmare scenario – one which is all but assured absent a full-scale bailout by Beijing – would lead not only to a Chinese financial crisis and economic crisis, but to a global stagflationary depression because unlike the global financial crisis when it was China that dragged the world out of the depth of the crisis, this time it will be China responsible for the collapse and as much as they may try, developed nations simply do not have the horsepower to pull the world out of the coming chasm.

d

dd

Tyler Durden

Thu, 09/16/2021 – 18:30

via ZeroHedge News https://ift.tt/3tQLr5l Tyler Durden