US Manufacturing Slumps To Weakest Since 2020 As Cost Inflation Hits Record High

October and November have seen US macro-economic data surprise to the upside (admittedly from a depressingly low level overshoot), and flash PMI signaled an uptick in Manufacturing earlier in the month, but that was the end of the good news.

Markit US Manufacturing was a big disappointment, tumbling from 59.1 earlier in the month to 58.3 final for November, which is below October’s final 58.4 – the weakest print since Dec 2020.

ISM US Manufacturing also disappointed, though only modestly, printing 61.1 vs 61.2 exp, but up from October’s 60.8.

So Markit worst since 2020, and ISM best since March…

Source: Bloomberg

Markit warns that longer lead times, supplier shortages and higher energy prices meanwhile pushed the rate of cost inflation to a fresh series high.

“Broad swathes of US manufacturing remain hamstrung by supply chain bottlenecks and difficulties filling staff vacancies. Although November brought some signs of supply chain problems easing slightly to the lowest recorded for six months, widespread shortages of inputs meant production growth was again severely constrained to the extent that the survey is so far consistent with manufacturing acting as a drag on the economy during the fourth quarter.

“While demand remains firm, November brought signs of new orders growth cooling to the lowest so far this year, linked to shortages limiting scope to boost sales and signs of push-back from customers as prices continued to rise sharply during the month.

“While average selling price inflation eased as firms sought to win customers, the rate of input cost inflation hit a new high, hinting at a squeeze on margins.”

So, is it any wonder that the yield curve is collapsing in fear of an imminent policy error by The Fed – tightening into a slowdown.

Powell’s comments during the Q&A overshadowed virtually every other aspect of yesterday’s CARES Act testimony before the Senate Banking Committee, where Powell was joined by Treasury Secretary Janet Yellen. Today, the Treasury head and Fed chief will join the House Financial Services Committee for the second part of the testimony mandated by the COVID bailout law signed by President Trump during the spring of 2020.

Just like yesterday’s testimony, the hearing is set to begin at 1000ET.

The committee is led by Chairwoman Maxine Waters, the prickly House Dem from LA who made headlines for clashing with Trump Treasury Secretary Steve Mnuchin during his routine appearances before her committee.

As the world waits to hear more from President Biden about the US’s new strategy for curbing omicron, readers can hear more about the Fed’s and the Treasury’s plans for handling omicron, as well as the Treasury’s hopes for raising the debt ceiling before it runs out of dollars, below:

Chairman Brown, Ranking Member Toomey, members of the Committee: It is a pleasure to testify today. November has been a very significant month for our economy, and Congress is a large part of the reason why. Our economy has needed updated roads, ports, and broadband networks for many years now, and I am very grateful that on the night of November 5, members of both parties came together to pass the largest infrastructure package in American history.

November 5th, it turned out, was a particularly consequential day because earlier that morning we received a very favorable jobs report– 531,000 jobs added. It’s never wise to make too much of one piece of economic data, but in this case, it was an addition to a mounting body of evidence that points to a clear conclusion: Our economic recovery is on track. We’re averaging half a million new jobs per month since January.

GDP now exceeds its pre-pandemic levels. Our unemployment rate is at its lowest level since the start of the pandemic, and our economy is on pace to reach full employment two years faster than the Congressional Budget Office had estimated. Of course, the progress of our economic recovery can’t be separated from our progress against the pandemic, and I know that we’re all following the news about the Omicron variant.

As the President said yesterday, we’re still waiting for more data, but what remains true is that our best protection against the virus is the vaccine. People should get vaccinated and boosted. At this point, I am confident that our recovery remains strong and is even quite remarkable when put it in context. We should not forget that last winter, there was a risk that our economy was going to slip into a prolonged recession, and there is an alternate reality where, right now, millions more people cannot find a job or are losing the roofs over their heads.

It’s clear that what has separated us from that counterfactual are the bold relief measures Congress has enacted during the crisis: the CARES Act, the Consolidated Appropriations Act, and the American Rescue Plan Act. And it is not just the passage of these laws that has made the difference, but their effective implementation. Treasury, as you know, was tasked with administering a large portion of the relief funds provided by Congress under those bills. During our last quarterly hearing, I spoke extensively about the state and local relief program, but I wanted to update you on some other measures. First, the American Rescue Plan’s expanded Child Tax Credit has been sent out every month since July, putting about $77 billion in the pockets of families of more than 61 million children.

Families are using these funds for essential needs like food, and in fact, according to the Census Bureau, food insecurity among families with children dropped 24 percent after the July payments, which is a profound economic and moral victory for the country. Meanwhile, the Emergency Rental Assistance Program has significantly expanded, providing muchneeded assistance to over 2 million households. This assistance has helped keep eviction rates below prepandemic levels.

This month, we also released guidelines for the $10 billion State Small Business Credit Initiative program, which will provide targeted lending and investments that will help small businesses grow and create well-paying jobs. As consequential as November was, December promises to be more so. There are two decisions facing Congress that could send our economy in very different directions. The first is the debt limit. I cannot overstate how critical it is that Congress address this issue. America must pay its bills on time and in full. If we do not, we will eviscerate our current recovery. In a matter of days, the majority of Americans would suffer financial pain as critical payments, like Social Security checks and military paychecks, would not reach their bank accounts, and that would likely be followed by a deep recession. The second action involves the Build Back Better legislation.

I applaud the House for passing the bill and am hopeful that the Senate will soon follow. Build Back Better is the right economic decision for many reasons. It will, for example, end the childcare crisis in this country, letting parents return to work. These investments, we expect, will lead to a GDP increase over the long-term without increasing the national debt or deficit by a dollar. In fact, the offsets in these bills mean they actually reduce annual deficits over time. Thanks to your work, we’ve ensured that America will recover from this pandemic. Now, with this bill, we have the chance to ensure America thrives in a post-pandemic world. With that, I’m happy to take your questions.

Chairman Brown, Ranking Member Toomey, and other members of the Committee, thank you for the opportunity to testify today.

The economy has continued to strengthen. The rise in Delta variant cases temporarily slowed progress this past summer, restraining previously rapid growth in household and business spending, intensifying supply chain disruptions, and, in some cases, keeping people from returning to work or looking for a job. Fiscal and monetary policy and the healthy financial positions of households and businesses continue to support aggregate demand. Recent data suggest that the post-September decline in cases corresponded to a pickup in economic growth. Gross domestic product appears on track to grow about 5 percent in 2021, the fastest pace in many years.

As with overall economic activity, conditions in the labor market have continued to improve. The Delta variant contributed to slower job growth this summer, as factors related to the pandemic, such as caregiving needs and fears of the virus, kept some people out of the labor force despite strong demand for workers.

Nonetheless, October saw job growth of 531,000, and the unemployment rate fell to 4.6 percent, indicating a rebound in the pace of labor market improvement.

There is still ground to cover to reach maximum employment for both employment and labor force participation, and we expect progress to continue.

The economic downturn has not fallen equally, and those least able to shoulder the burden have been the hardest hit. In particular, despite progress, joblessness continues to fall disproportionately on African Americans and Hispanics.

Pandemic-related supply and demand imbalances have contributed to notable price increases in some areas. Supply chain problems have made it difficult for producers to meet strong demand, particularly for goods. Increases in energy prices and rents are also pushing inflation upward. As a result, overall inflation is running well above our 2 percent longer-run goal, with the price index for personal consumption expenditures up 5 percent over the 12 months ending in October.

Most forecasters, including at the Fed, continue to expect that inflation will move down significantly over the next year as supply and demand imbalances abate. It is difficult to predict the persistence and effects of supply constraints, but it now appears that factors pushing inflation upward will linger well into next year. In addition, with the rapid improvement in the labor market, slack is diminishing, and wages are rising at a brisk pace.

We understand that high inflation imposes significant burdens, especially on those less able to meet the higher costs of essentials like food, housing, and transportation. We are committed to our price-stability goal. We will use our tools both to support the economy and a strong labor market and to prevent higher inflation from becoming entrenched.

The recent rise in COVID-19 cases and the emergence of the Omicron variant pose downside risks to employment and economic activity and increased uncertainty for inflation. Greater concerns about the virus could reduce people’s willingness to work in person, which would slow progress in the labor market and intensify supply-chain disruptions.

To conclude, we understand that our actions affect communities, families, and businesses across the country. Everything we do is in service to our public mission.

We at the Fed will do everything we can to support a full recovery in employment and achieve our price-stability goal.

Thank you. I look forward to your questions.

The big question now: will Powell sound dovish, or hawkish, under questioning? What’s more, investors should be on the lookout for Yellen’s comments on the debt ceiling – particularly anything she says about the timing for when the Treasury might run out of funds.

Fed watchers will be on the lookout for any more clues about the Fed’s thinking on the pace of tightening monetary policy by shrinking its balance sheet and raising interest rates

Boston politicians are fighting to retain one of the country’s last remaining eviction bans in the face of a waning pandemic and an adverse court ruling. Newly elected Boston Mayor Michelle Wu has vowed to contest a state judge’s ruling, which found that the city’s moratorium was an abuse of its emergency powers.

“We need more protections for renters in Boston,” declared Wu in a statement. “Our focus remains on protecting tenants from displacement during the COVID emergency, and connecting our residents to City and State rental relief programs.”

In August, the Boston Public Health Commission (BPHC) issued a sweeping ban on evicting almost any Boston resident for non-payment of rent. Only tenants who had been found by a judge to have violated their lease terms in a way that impaired the health and safety of other building tenants and neighbors could be removed under the order.

The city’s moratorium was issued just a few days after the U.S. Supreme Court struck down a federal eviction ban that had been issued by the Centers for Disease Control and Prevention (CDC). A Massachusetts ban on evictions, imposed by Republican Gov. Charlie Baker, was allowed to expire in October.

Boston’s moratorium immediately proved controversial. Landlord groups argued it was a usurpation of the state’s powers to regulate housing and landlord-tenant matters. Even some housing activists, while supportive of the policy, worried that it would be vulnerable to legal challenges.

A landlord and a constable eventually sued.

BPHC argued in response to their lawsuit that its own eviction moratorium was necessary to prevent the spread of COVID-19, and was therefore justified by state public health laws that gave it the power to craft “reasonable public health regulations” to combat communicable diseases.

In a Monday decision, Housing Court Judge Irene Bagdoian firmly rejected this argument, saying that nothing in the statutes cited by BPHC would suggest that an eviction moratorium that overrides state landlord-tenant law was “reasonable.”

“This court perceives great mischief in allowing a municipality or one of its agencies to exceed its powers,” wrote Bagdoian. She notes that the same logic employed by Boston to defend its moratorium would allow another city to use COVID-19 as a justification for opting out of state laws that force cities to allow for denser housing.

Almost every state and many localities imposed some kind of moratorium on evictions during the pandemic. Most of these have since been repealed, allowed to expire, or significantly weakened as the pandemic has waned, and billions of dollars in federal rental assistance have been made available to tenants in arrears.

Boston’s sweeping ban was one of the last of its kind.

It’s also one of the few local moratoriums to be successfully challenged in court. Judges have generally given local and state governments wide latitude to impose whatever limits on evictions they see fit during the pandemic.

These moratoriums have been justified as necessary to prevent a “wave” of evictions during the pandemic. That fear was always overblown, and wave has failed to materialize almost anywhere eviction bans have been allowed to lapse.

The policies have, however, put an incredible amount of hardship on a limited number of landlords, who have effectively been forced to provide free housing for unscrupulous, and in a few cases dangerous, tenants.

It is well past time to lift these extraordinary limits on property rights.

COVID-19

The Biden administration is reportedly following up on the limited travel restrictions it imposed on Monday with a plan to require all people entering the U.S. to be tested for COVID-19 and to self-quarantine. TheWashington Post reports:

As part of an enhanced winter covid strategy Biden is expected to announce Thursday, U.S. officials would require everyone entering the country to be tested one day before boarding flights, regardless of their vaccination status or country of departure. Administration officials are also considering a requirement that all travelers get retested within three to five days of arrival.

In addition, they are debating a controversial proposal to require all travelers, including U.S. citizens, to self-quarantine for seven days, even if their test results are negative. Those who flout the requirements might be subject to fines and penalties, the first time such penalties would be linked to testing and quarantine measures for travelers in the United States.

The initial travel restrictions announced by the Biden administration in response to the new omicron variant prohibited people who were neither American citizens nor permanent residents from traveling to the U.S. from several African nations.

FREE MARKETS

Federal Reserve Chairman Jerome Powell says it’s probably time to stop describing the ongoing inflation as “transitory.” Asked by Sen. Pat Toomey (R–Penn.) at a Senate hearing how long the current 6 percent inflation rate would persist, and whether it was right to continue calling it transitory, Powell said the term was confusing people who thought the word meant something closer to its dictionary definition.

Powell explained that while the word has “different meanings to different people,” the Federal Reserve “tend to use it to mean that it won’t leave a permanent mark in the form of higher inflation.

“I think it’s—it’s probably a good time to retire that word and try to explain more clearly what we mean,” Powell added.

The Wall Street Journal editorial board said in response that “the current annual rate of 6% is already permanent in the sense that the inflation of the last year is built in and prices won’t fall to erase it. Transitory or permanent, we’d prefer that Mr. Powell act to stop it.”

QUICK HITS

It’s Reason‘s annual webathon this week! Please consider supporting all the free content we provide in support of free minds and free markets.

BioTech CEO Ugur Sahin told Reuters the COVID-19 vaccine his company developed with Pfizer should still offer robust protection against severe disease. Moderna CEO Stéphane Bancel had said yesterday that there would be a “material drop” in the effectiveness of his company’s COVID-19 vaccine.

A D.C. assistant principal was apparently moonlighting as a full-time principal at a school in Rhode Island, reportsDCist. What a commute!

Sloths are having trouble adjusting to the face-paced hustle and bustle of urban life. CityLab reports on a Costa Rica nonprofit that’s trying to help them adapt.

GOP lawmakers are plotting a federal government shutdown over President Joe Biden’s vaccine mandate for private employers, according to Politico.

A new lead emerges in the investigation into how live ammunition got onto the set of the movie Rust, where actor Alec Baldwin accidentally shot two crew members, one fatally.

Belarusian President Lukashenko Threatens To Halt Transit Of Energy Products From Russia

As if the energy sector needed any more volatility than it’s already experiencing, Belarusian President Alexander Lukashenko has thrown his hat in the ring by commenting this week that he could shut down transit of energy products if Poland closes its border with his country.

The border is currently turning into a point of contention between the European Union and Lukashenko. Thousands of migrants are stuck in the middle of the border and at least 11 have died, according to the Wall Street Journal. The migrants are seeking refuge and to move further into Europe. The EU has blamed Lukashenko for using the migrants as “pawns”, while Lukashenko attests that something should be done about the humanitarian crisis.

Lukashenko has now escalated tensions over the crisis by indicating he is “serious” about halting energy products from Russia.

“You should think about how you will buy fuels from Russia,” he said in an interview this week, according to Bloomberg.

“Listen, when I’m being strangled by the Poles or whoever, will I look at some contracts? Come on, what are you talking about?” he continued.

Belarus and Poland are on the front lines of a geopolitical standoff between Russia, Belarus’s closest ally, and the West. Poland says Belarus is using thousands of migrants camped on its border in a new type of war aimed at provoking clashes and sowing division among EU member states. The Belarusian military has tried to tear down the spools of barbed wire that Poland has used to fence off the border, according to the Polish Border Guard, which has also accused Belarus of equipping migrants with tear gas.

Wedged between EU nations and Russia, Belarus has long been known as “Europe’s last dictatorship,” whose leader for the last quarter century, Mr. Lukashenko, held a firm grip on social and political life. Mass protests broke out in 2020, prompting security forces to crack down and leading Europe to respond with sanctions.

Now the tensions between Europe and Belarus are exploding as thousands of people from Iraq, Syria and other poor and war-torn countries try to cross from Belarus into Poland, their first step into the EU.

As we noted earlier this morning, Lukashenko has also (again) announced his country stands ready to host nuclear weapons provided by Russia on its territory. “We are ready for this on the territory of Belarus,” Lukashenko told Russia’s RIA news agency in an interview published Tuesday.

Lukashenko held it out as the necessary response in the scenario where NATO would deploy nuclear systems to neighboring Poland. The Belarusian president said he will soon propose this plan to Putin.

In the interview he had been asked to respond to recent comments of NATO Secretary General Jens Stoltenberg, who provoked anger out of Moscow by suggesting the Western military alliance could eventually see its nukes deployed to Eastern European partners.

Boston politicians are fighting to retain one of the country’s last remaining eviction bans in the face of a waning pandemic and an adverse court ruling. Newly elected Boston Mayor Michelle Wu has vowed to contest a state judge’s ruling, which found that the city’s moratorium was an abuse of its emergency powers.

“We need more protections for renters in Boston,” declared Wu in a statement. “Our focus remains on protecting tenants from displacement during the COVID emergency, and connecting our residents to City and State rental relief programs.”

In August, the Boston Public Health Commission (BPHC) issued a sweeping ban on evicting almost any Boston resident for non-payment of rent. Only tenants who had been found by a judge to have violated their lease terms in a way that impaired the health and safety of other building tenants and neighbors could be removed under the order.

The city’s moratorium was issued just a few days after the U.S. Supreme Court struck down a federal eviction ban that had been issued by the Centers for Disease Control and Prevention (CDC). A Massachusetts ban on evictions, imposed by Republican Gov. Charlie Baker, was allowed to expire in October.

Boston’s moratorium immediately proved controversial. Landlord groups argued it was a usurpation of the state’s powers to regulate housing and landlord-tenant matters. Even some housing activists, while supportive of the policy, worried that it would be vulnerable to legal challenges.

A landlord and a constable eventually sued.

BPHC argued in response to their lawsuit that its own eviction moratorium was necessary to prevent the spread of COVID-19, and was therefore justified by state public health laws that gave it the power to craft “reasonable public health regulations” to combat communicable diseases.

In a Monday decision, Housing Court Judge Irene Bagdoian firmly rejected this argument, saying that nothing in the statutes cited by BPHC would suggest that an eviction moratorium that overrides state landlord-tenant law was “reasonable.”

“This court perceives great mischief in allowing a municipality or one of its agencies to exceed its powers,” wrote Bagdoian. She notes that the same logic employed by Boston to defend its moratorium would allow another city to use COVID-19 as a justification for opting out of state laws that force cities to allow for denser housing.

Almost every state and many localities imposed some kind of moratorium on evictions during the pandemic. Most of these have since been repealed, allowed to expire, or significantly weakened as the pandemic has waned, and billions of dollars in federal rental assistance have been made available to tenants in arrears.

Boston’s sweeping ban was one of the last of its kind.

It’s also one of the few local moratoriums to be successfully challenged in court. Judges have generally given local and state governments wide latitude to impose whatever limits on evictions they see fit during the pandemic.

These moratoriums have been justified as necessary to prevent a “wave” of evictions during the pandemic. That fear was always overblown, and wave has failed to materialize almost anywhere eviction bans have been allowed to lapse.

The policies have, however, put an incredible amount of hardship on a limited number of landlords, who have effectively been forced to provide free housing for unscrupulous, and in a few cases dangerous, tenants.

It is well past time to lift these extraordinary limits on property rights.

COVID-19

The Biden administration is reportedly following up on the limited travel restrictions it imposed on Monday with a plan to require all people entering the U.S. to be tested for COVID-19 and to self-quarantine. TheWashington Post reports:

As part of an enhanced winter covid strategy Biden is expected to announce Thursday, U.S. officials would require everyone entering the country to be tested one day before boarding flights, regardless of their vaccination status or country of departure. Administration officials are also considering a requirement that all travelers get retested within three to five days of arrival.

In addition, they are debating a controversial proposal to require all travelers, including U.S. citizens, to self-quarantine for seven days, even if their test results are negative. Those who flout the requirements might be subject to fines and penalties, the first time such penalties would be linked to testing and quarantine measures for travelers in the United States.

The initial travel restrictions announced by the Biden administration in response to the new omicron variant prohibited people who were neither American citizens nor permanent residents from traveling to the U.S. from several African nations.

FREE MARKETS

Federal Reserve Chairman Jerome Powell says it’s probably time to stop describing the ongoing inflation as “transitory.” Asked by Sen. Pat Toomey (R–Penn.) at a Senate hearing how long the current 6 percent inflation rate would persist, and whether it was right to continue calling it transitory, Powell said the term was confusing people who thought the word meant something closer to its dictionary definition.

Powell explained that while the word has “different meanings to different people,” the Federal Reserve “tend to use it to mean that it won’t leave a permanent mark in the form of higher inflation.

“I think it’s—it’s probably a good time to retire that word and try to explain more clearly what we mean,” Powell added.

The Wall Street Journal editorial board said in response that “the current annual rate of 6% is already permanent in the sense that the inflation of the last year is built in and prices won’t fall to erase it. Transitory or permanent, we’d prefer that Mr. Powell act to stop it.”

QUICK HITS

It’s Reason‘s annual webathon this week! Please consider supporting all the free content we provide in support of free minds and free markets.

BioTech CEO Ugur Sahin told Reuters the COVID-19 vaccine his company developed with Pfizer should still offer robust protection against severe disease. Moderna CEO Stéphane Bancel had said yesterday that there would be a “material drop” in the effectiveness of his company’s COVID-19 vaccine.

A D.C. assistant principal was apparently moonlighting as a full-time principal at a school in Rhode Island, reportsDCist. What a commute!

Sloths are having trouble adjusting to the face-paced hustle and bustle of urban life. CityLab reports on a Costa Rica nonprofit that’s trying to help them adapt.

GOP lawmakers are plotting a federal government shutdown over President Joe Biden’s vaccine mandate for private employers, according to Politico.

A new lead emerges in the investigation into how live ammunition got onto the set of the movie Rust, where actor Alec Baldwin accidentally shot two crew members, one fatally.

“Frosty wind made moan, Earth stood hard as iron, Water like a stone.”

Did you feel markets judder when Powell spoke? The mood has changed as markets wake up to the danger Central Banks might just start doing their jobs. As Winter begins, Europe faces a bleak energy crisis of its own making. My solution? Buy a generator!

Today marks the first day of meteorological winter, and the first day of Advent – which means its ok to quietly hum Christmas songs in the office, although the Lapland convention on Christmas dictates loud Xmas jumpers remain verboten till after the ides of the month. As your December First advent surprise from the virtual Blain’s Morning Porridge Advent Calendar, enjoy this virtual Tunnocks Caramel Wafer – Scotland’s National Biscuit.. Mmmmm, they’re delicious…

Lots to talk about this morning as Powell shifts the rules, bond markets get the heebie-jeebies, transitory inflation is consigned to junkpile, and markets wake up to the threat Central Banks might just start doing their jobs… A deep judder just ran down the spine of the market….

But first…

It’s the first day of winter, and surprisingly in this year of climate noise, extreme events and erratic weather patterns, its 0.4 degrees colder than the average of the last decade. That, of course is terrible news for the whole of Europe. The outlook from the UK Met Office is for a wet and windy early December with possible wintery spells, before it becomes more settled around Christmas with fog and frost. Again, terrible news.. (We pay attention to the Met Office because grousing about the weather is about the UK’s only definable social skill, and the Met Office has got the biggest computers…)

Why such bad news?

Cold winter days mean increased energy demand… Gas prices have never been so high, supply has never been so limited, and the sources of power are looking strained. I’ve been checking out the prices of generators – they are not cheap (even more so if you want them to cut in automatically), but they are distinctly preferable to the prospect of freezing to death through the festive jollities..

The big problem for Europe this year has been Wind. Governments have bet the shop on Wind as the simple, reliable, dependable, cheap source of renewable power over the last decade. We’ve seen our mountains sprout forests of turbines, and our oceans are now jagged with wind generators. Problem is… Europe has had a very unwindy year. Some estimates are 60% less wind than normal.

I’ve experienced that personally sailing this year – half a dozen regatta days where racing has been abandoned due to zero wind. Boats trying to race across the Atlantic in the “Transat” race have found little or no wind. And if it has not been “light and sh*te” as sailors say, it’s been blowing “Half-Pelicans” (apparently a Danish expression), or “dogs off chains”. Storm Arwen last week caused spectacular damage across the UK, but produced limited power – wind generators can’t cope with storms.

It means Europe is going to suffer a serious energy crisis this winter.

We’ve nobody to blame but ourselves. The politicians will blame Putin for using Europe’s energy crisis to threaten us, but who allowed Europe’s energy sovereignty to get to this perilous stage? The UK once held a massive Gas stockpile – but the largest facility at Rough in the North Sea was allowed to run down and close on the basis it would be cheaper not to repair it, and secure spot supplies on the global gas market.

Do you feel an “doh” moment coming on?

UK Govt minister Kwasi Kwarteng recently said he has no concerns about blackouts this winter – 50% of our needs come from domestic production, and 30% from Norway. When a minister says our energy supplies are secure.. well that’s why I’m buying a generator and a week’s supply of Diesel to run it. Basically, the UK has a strategic gas reserve on hand of a couple of days. If things get dicey this winter.. that generator will look a really smart idea.

Across Europe Gas reserves are around 70% of normal levels. Spot demand will depend entirely how Russia plays. Putin doesn’t need Europe to buy – he’s got a ready market in China (where state industries and power companies have been specifically instructed to secure energy supplies of gas and oil at “any cost”.)

Of course… if governments had woken up and smelt the coffee a few decades ago.. we’d now have modern Nuclear power stations on line – taking our base energy level up into the 60% non-fossil range. We’d have the luxury of unreliable renewables like Wind and Solar providing maybe 10% base load, and be reaping the rewards of years of development into reliable renewables like efficient heat pumps, tidal and hydro power and geothermal.

We’d have a vibrant coal mining sector, producing the best metallurgical coal on the planet to make the premium steels that would be used to re-infrastucture our energy rich economy, and to build the next generation of fusion reactors.. We’d have invested in a diverse range of non-fossil, renewable power to ensure the resilience of the economy. Gas and oil power would be a memory…

STOP.. NO MORE DREAMING.

The die is cast. It’s going to be a cold, miserable winter…

Meanwhile.. back in the USA

Jay Powell has dumped “transitory”. Inflation is expect to linger into “next year”. I am sending him one of my coveted “No Sh*t Sherlock” awards. His response will be a Hawkish early taper/reduction of the asset-purchase programme, which will be announced at the Dec 14-15 Fed Meeting.

Surging inflation, the new Omicron variant threat, higher rates and central banks waking up to reality – no wonder markets cratered yesterday.

Reality sucks and it bites. Witness carnage in bonds yesterday and illiquidity as markets went offered only. Its only just beginning – bond traders will be weighing up increased credit risks stemming from higher debt costs, the prospects of a renewed economic shut down on the Omicron variant, sustained supply chain dislocation, and falling corporate earnings as taxes and rates rise.. When bonds crash… in Bonds there is Truth..

“Perfect storm” is a massively overused metaphor, but this might be it coming. Watch this space.

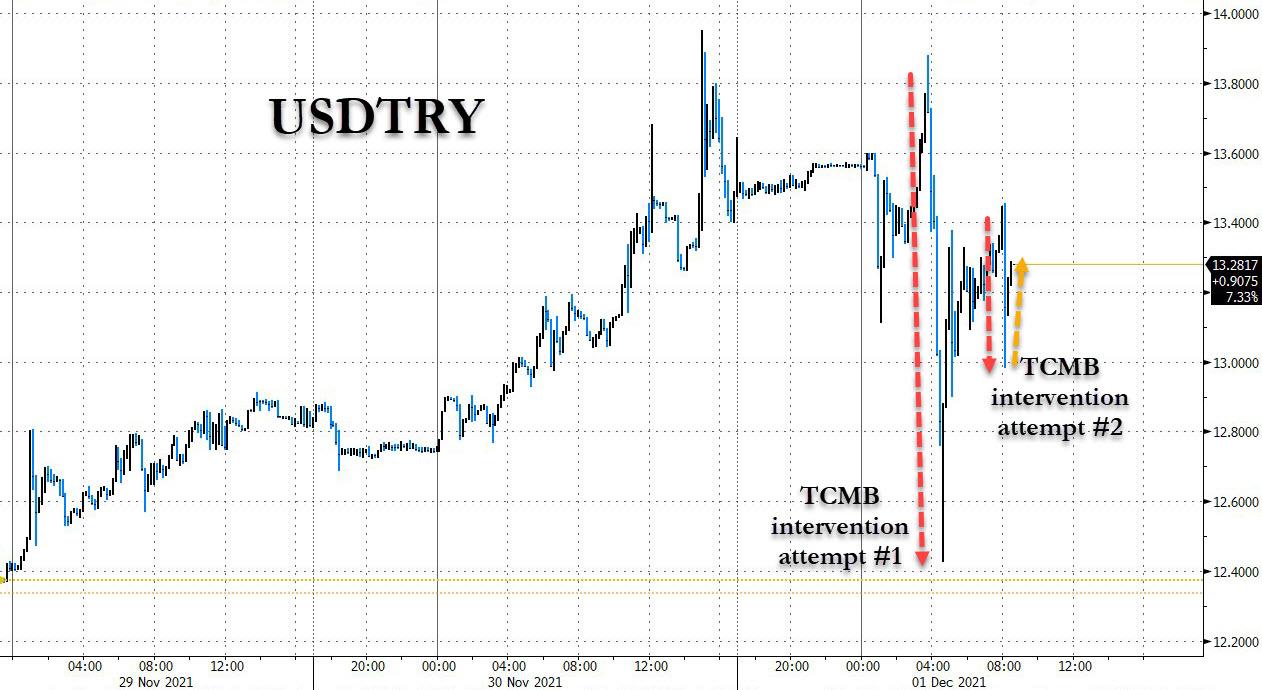

In Act Of Sheer Panic, Turkey Central Bank Intervenes To Prop Up Lira, Fails

With the lira having lost 40% of its value in just the past 3 weeks (and down almost 50% YTD), now that the market finally realizes just how insane Erdogan has been all along with his intention to keep cutting rates until the mid-2023 Turkish elections…

… and foreign investors pulling their capital from Turkey in a show of defiance to the Erdogan regime – they may return if and when a new, more sensible ruler emerges – overnight the Turkish central bank intervened in the foreign exchange market for the first time in seven years, and in an act of sheer desperation, fought to shore up the plunging lira.

The Turkish Central Bank (TCMB) said in a statement that it took action due to “unhealthy price formations” in the lira, which has been in freefall since President Recep Tayyip Erdogan renewed his push for lower interest rates.

Needless to say, the price formation is “unhealthy” only to the Erdogan regime, the entrenched Turkish state, and Erdogan’s puppet central bank, and quite healthy to short sellers who have long been warning that Turkey is doomed to collapse under the Erdogan dictatorship, and only a currency collapse and hyperinflation has any hope of dislodging Turkey’s batshit insane ruler.

Indeed, in recent days we have seen sporadic protests against the currency collapse and soaring prices, and Erdogan is scrambling to intercept these before they spread to the rest of the population.

Unfortunately for Erdogan, as Japan, the UK and so many other central banks have demonstrated with their failed intervention attempts, all the TCMB is achieving is blowing through its dollar reserves and ensuring that the currency collapse will come even faster and will be even more acute when it hits.

Sure enough, while the lira initially surged against the dollar after the announcement, climbing as much as 8.5%, it later pared gains. A subsequent intervention by the central bank had a far smaller impact and was quickly faded by the market.

Bottom line: after spending hundreds of millions or even billions, the lira is almost back where it was and every incremental attempt to punish lira shorts and send the lira higher will lead to an even faster collapse in the doomed currency which will not rebound as long as i) Erdogan is president or ii) until Erodgan capitulates and admits that his bizarre economy experiment has been a failure (which won’t happen).

Meanwhile, perhaps unaware of the endgame, Erdogan said that the central bank “can make the necessary intervention if that’s needed,” speaking to a group of reporters on Wednesday after addressing his party’s lawmakers in parliament.

The intervention which took place in both spot and futures markets marks a new episode in Erdogan’s latest policy pivot according to Bloomberg. It follows after his latest pledge on Tuesday to keep lowering interest rates until elections in 2023. The Turkish leader also effectively doomed the currency saying that the country will no longer try to attract “hot money” by offering high interest rates and a strong lira. In Erdogan’s base scenario, cheaper money will boost manufacturing and create jobs while inflation eventually stabilizes.

That said, the central bank’s surprise – and desperate – decision to sell more from its dwindling foreign assets shows policymakers are turning less comfortable with the lira’s rising volatility than the Turkish president.

It “reflects how serious the situation is,” said Piotr Matys, an analyst at InTouch Capital. “But it’s likely to prove insufficient. Turkey doesn’t have sufficient FX reserves to sell substantial amount of dollars on a regular basis.”

As Bloomberg reminds us, the last intervention took place in January 2014, when the central bank sold $3.1 billion in spot markets. The move failed to stabilize the lira and less than a week later, Turkey was forced to more than double its benchmark interest rate to 10% in an emergency meeting.

Expect a similar outcome, only this time Erdogan won’t concede defeat and won’t hike rates, which is why we repeat that our fair value for the USDTRY is 20, and potentially much more once local banks start defaulting on foreign-denominated debt.

Bloomberg also admits that the country faces a very different set of circumstances now. Governor Sahap Kavcioglu is the fourth central bank chief since Erdogan was sworn in with expanded executive powers in 2018, which included being able to fire and replace bank governors. Kavcioglu has repeatedly changed his forward guidance in recent months to make room for rate cuts while inflation kept climbing. Since September, the central bank slashed the one-week repo rate by 4 percentage points to 15%.

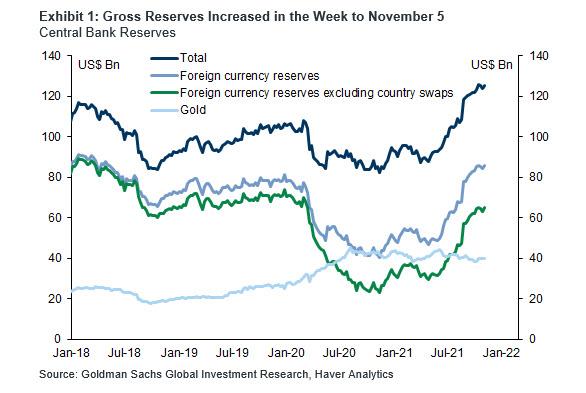

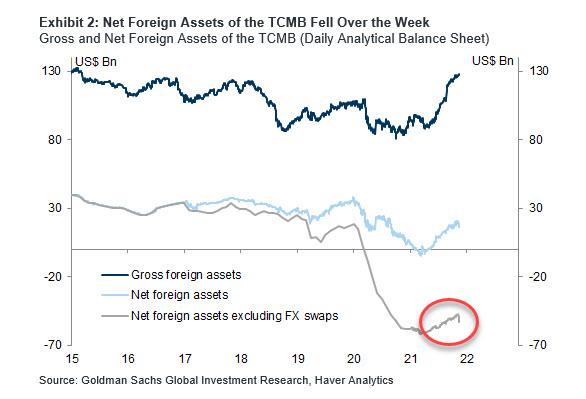

Looking ahead, the question traders should ask is how long can Turkey buy the currency some respite from the relentless selling. The answer, as BBG’s Ven Ram notes, comes down to the size of the war chest and how willing the central bank is to run down those assets. While the Turkish central bank’s gross reserves add up to $128.5 billion, with $60.5 billion coming from the bank’s swap deals. with some $40 billion in gold (at least in theory; we have a strong suspicion Erdogan and his cronies have long ago sold or syphoned off Turkey’s gold and all that number represents is an empty placeholder).

However, when swaps and other liabilities such as required reserves are stripped, Turkey’s net reserves stand at -$35 billion! Yes, negative.

While the bank has predictably said on many occasions that its gross reserves – the total amount at its disposal at the time – are more important than net reserves, the FX swaps will promptly collapse once counterparties realize they are on the hook for billions in losses as the Turkish economy implodes and unwind the swaps. As such, expect attention to turn to the massive negative number of true net foreign assets.

Separately, Ram also notes that the central bank’s intervention this morning is significant if only for the signaling it sends.

During a previous episode of similar stress in the lira back in 2018, there was no reported intervention. In other words, the policy makers may be telling the markets that their strategy to ward off any speculation on the currency will take a different tack this time.

And while, in 2018, the central bank took the benchmark rate to 24% from 8% in a short span to arrest the decline in the lira, this time rate hikes are off the table and instead the central bank will burn through its remaining reserves instead before the TRY truly collapses.

Erdogan said on Tuesday that old policies based on “false” premises would result in higher inequalities, while leaving Turkey at the mercy of foreign money barons.

“The high interest-rate policy imposed on us is not a new phenomenon,” he said. “It is a model that destroys domestic production and makes structural inflation permanent by increasing production costs. We are ending this spiral.”

We very much doubt Erdogan is ending “this spiral” but we are absolutely certain that he is now starting Turkey’s “hyperinflation spiral.”

“Say say two thousand zero zero party over, oops, out of time

So tonight I’m gonna party like it’s nineteen ninety-nine” -Prince 1999

Prince wrote the song “1999” in 1982, 18 years before the clock ran out on the 20th century and possibly the greatest stock market run in American history.

In 1999, equity valuations stood at unprecedented peaks, even dwarfing those of 1929. At the time, investors were euphoric as if the rally were eternal. Newbies were killing it, and veterans were cleaning up like never before. Some stocks were rising 10, 20, and even 30% or more in a day. Companies adding dot com to their name or discussing new internet technology saw huge pops in their share prices. Investors bought the narrative with little to no due diligence.

Sound familiar? Not only is today’s speculative environment eerily similar to the late 90s, but valuations, in many cases, are frothier than that period.

Comparing valuations from separate periods is inaccurate as economic and earnings environments can be different. This article contrasts the valuations and environments to consider if it’s time to leave the party or stay and rock on. To help you decide we provide a statistical analysis showing the potential downside risk facing the S&P 500.

First, however, let’s look at a few valuation measures to provide context between today and 1999.

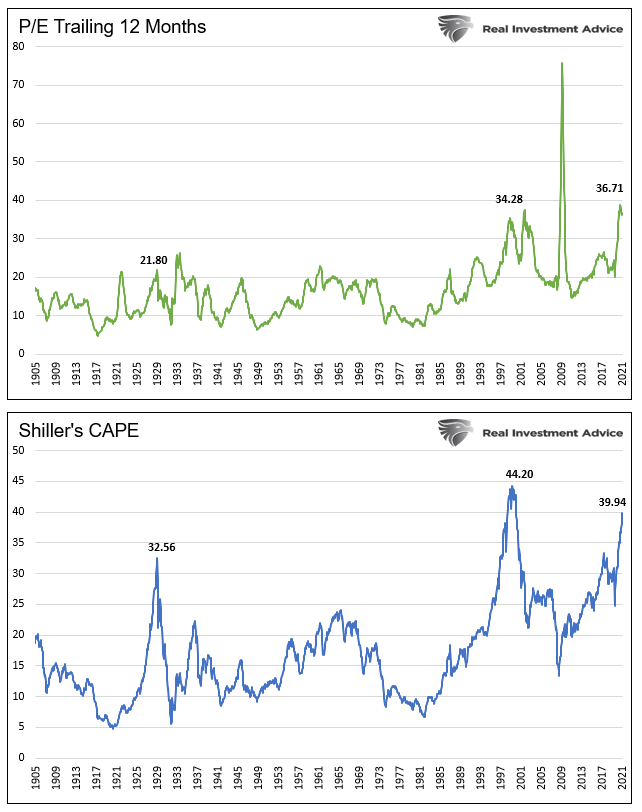

S&P 500 Price to Earnings

Price to earnings (P/E) is the most often used method to value stocks. It’s common for investors to use the trailing 12 months (ttm) of earnings in the P/E denominator, as shown in the first graph.

Some investors, including ourselves, prefer using the CAPE P/E. Robert Shiller’s CAPE method uses the last ten years of earnings to better factor in secular earnings trends and avoids one-off events that distort valuations.

P/E valuations are grossly extended, and in both calculations nearing or surpassing levels in 1999. The graphs also show valuations are well above those of 1929.

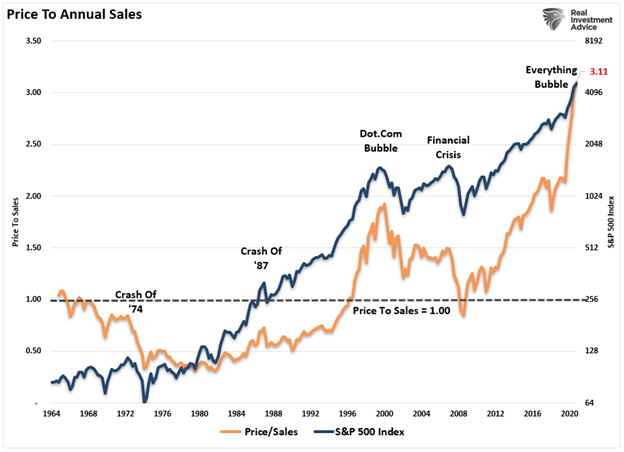

Price To Sales

The benefit of using the ratio price to sales (P/S) versus P/E is that sales, or revenue, are not easy to manipulate by executives.

The graph below shows the price to sales ratio (P/S) is now 50% above where it was in 1999.

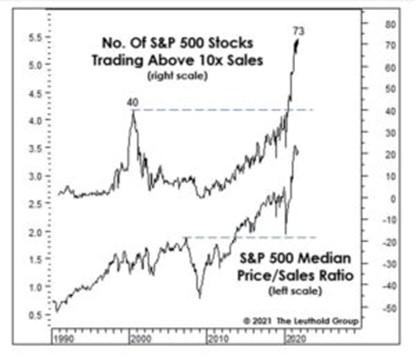

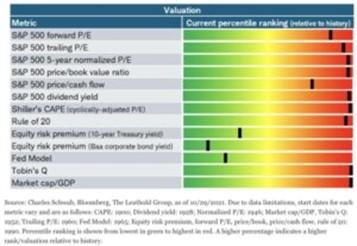

The charts below, courtesy of the Leuthold Group, provide further context. The top chart shows 15% of the S&P 500 stocks have a P/S ratio greater than ten. That compares to 8% in 1999. The bottom graph shows the median P/S ratio is nearly double the 1999 level.

To highlight what a P/S ratio of ten entails, we quote Scott McNeely, the CEO of Sun Microsystems, from 1999.

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. It assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are?”

More Valuation Metrics

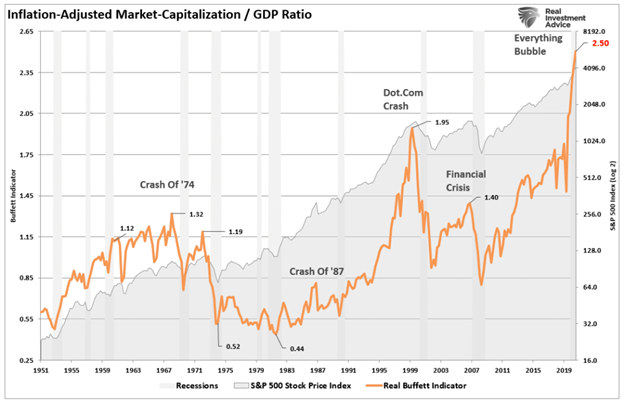

The following graph is purportedly Warren Buffet’s favorite valuation technique. The measure compares the inflation-adjusted market cap of the S&P 500 as a ratio to the economy. Given that earnings and economic growth correlate well over time, the ratio effectively points out valuation extremes. Currently, the ratio is at 2.50, well above the 1.95 from 1999 and 1.40 leading into the Financial Crisis.

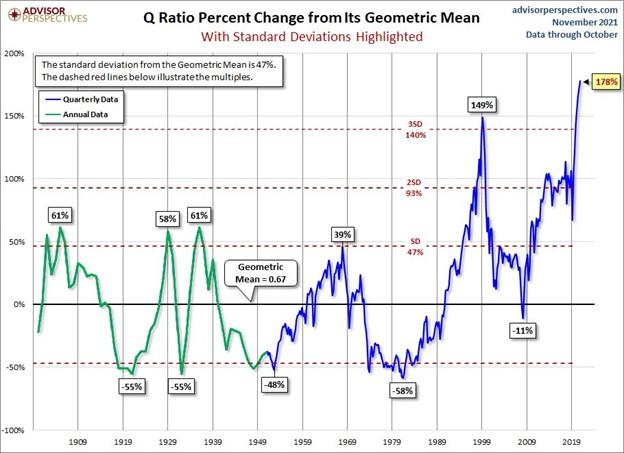

The Q-ratio takes the S&P 500 market cap and divides it by the aggregate replacement costs of the assets held by the companies in the index. It effectively quantifies how much an investor is paying for the underlying corporate assets. As shown below, courtesy of Advisor Perspectives, the ratio is now over 3.5 standard deviations above its norm. It is also higher than it was in 1999 and multiples of any other prior peak.

Compared to What?

Conservatively speaking, current valuations are on par or greater than those in 1999 and any other period. Such a statement is statistically factual, but it ignores the economic environments of both periods. For instance, if you think the economy and corporate earnings will grow at double-digit rates for years, we can make the case valuations are fair today.

The table below compares economic environments from both periods.

Economic and earnings growth rates today are weaker than 20 years ago. Further, debt levels, measured as a ratio to GDP, are much higher today. Productivity growth and demographics, two significant factors determining economic growth, are weighing on economic growth today. In the 90s, they were strong economic tailwinds.

The last three indicators show the amount of monetary stimulus via low-interest rates, and the Fed’s enlarged balance sheet is much more accommodative than in 1999.

Fundamentals and the economic/earnings outlook are weaker today than in 1999. As a result, investors were better off paying higher valuations in 1999 than today.

However, the Fed is, directly and indirectly, bolstering asset prices and, therefore, valuations via their excessive actions. Low-interest rates promote the use of leverage and encourage buybacks which fuel stock prices. Additionally, investors shun low-yielding bonds to chase stocks to pick up needed returns. For more, please read The Fed is Juicing Stocks.

The Fed is the Fundamentals

The bottom line is investors are paying more and getting less compared to 1999. The graph below shows numerous measures of valuations are at extremes except three. Those three in green shading use comparisons of stock prices to interest rates. They are “fairly valued.”

Whether they know it or not, investors are betting the Fed continues to levitate the market. Can stocks remain at extremely lofty valuations while lacking fundamental backing if the Fed continues to reduce QE purchases and ultimately raises interest rates?

Essentially the real gamble investors are taking is that inflation will be transitory. If high inflation is persistent and not transitory, the Fed will find it increasingly challenging to continue current policy.

Without the Fed’s enormous liquidity, valuation gravity will reassert itself.

Statistics Warn of 2650

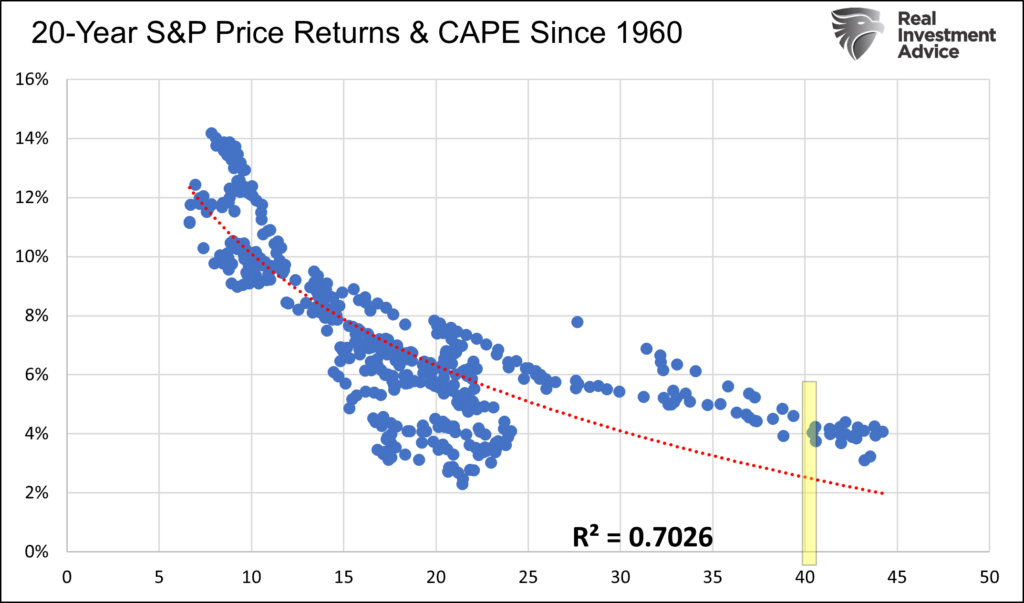

The graph below shows the strong correlation between CAPE valuations and future 20-year returns. At current levels, highlighted in yellow, we should expect annualized returns ranging from 2-4% for the next 20 years.

You may be thinking 2-4% doesn’t sound too bad considering how high valuations are. The problem, however, with such a long-range forecast is there may be periods with negative growth and others with double-digit growth within the twenty years.

While the regression allows us to form 20-year expectations, it also gives us the ability to forecast shorter periods.

Eighteen years ago, in October 2003, the S&P stood at 1019.50. Based on the regression above, investors could expect 4.90% annualized returns at that time. At such a growth rate, the S&P would rise to 2655 in October 2023. Currently, the S&P 500 is around 4700. Assuming the regression holds and history has favorable odds of that occurring, we should expect the S&P 500 to fall to 2650 in the next two years. A 43% decline is harsh, but it will only leave the index at fair value based on the last 40 years of CAPE levels. Quite often, markets revert below their means.

Before you dismiss our statistical analysis, let’s look back to 1999.

Prince wrote “1999” in 1982. When he wrote it, the S&P was at 111. Using the same math, investors could have expected 12% annualized returns, putting the S&P 500 at 1068 on New Year’s Eve 1999. The S&P, at the end of 1999, was 1450, offering investors a two-year expected return of -26%. Statistics delivered right on cue, and just two years later, the S&P hit 1068. The index ultimately fell to the low 800s before the stock market crash ended.

Summary

Every era of speculation brings forth a crop of theories designed to justify the speculation, and the speculative slogans are easily seized upon. The term “new era” was the slogan for the 1927-1929 period. We were in a new era in which old economic laws were suspended.” -Dr. Benjamin Anderson – Economics and the Public Welfare

Investors are making a big bet on the Fed and a “new era.”

On the eve of the stock market crash in 1929, Irving Fisher erroneously declared that stocks hit “what looks like a permanently high plateau.” Fisher could not have been more wrong. Same with investors in the “new era” of the internet of the late 90s.

Do you have faith the “new era” of Fed-managed markets can levitate stocks well above historical norms and prevent a stock market crash? Or will this “new era” resolve itself like prior “new eras” with a stock market crash?

Established in 1968, Reason has a long history of discovering, inventing, and championing the future. We were the first serious magazine to champion outlandish, seemingly insane policies such as drug legalization and equal rights for gays and lesbians half a century ago when more conventional rags like National Review and The New Republic were locked in twilight struggles over threats posed by long hair and rock music. We were early adopters to the web (circa 1995) and we published the first-ever mass-individualized magazine that sent unique covers and content to 40,000-plus subscribers. In 2007, we launched our award-winning video platform that has gone on to pull 234 million views at YouTube alone (and millions more at Facebook, Twitter, and Instagram). If some aspects of Termination Shock, the wonderful new Neal Stephenson novel about geoengineering, sound familiar, you may have read about them here in 1997.

At Reason, we don’t fear the future, we celebrate it—and want to help guide its development by exploring what policies, technologies, mindsets, and temperaments are best suited to prosper in the creative destruction that is an essential part of a vibrant, innovative, and forward-facing world.

And that brings me to a fun new thing we’re doing as part of our annual webathon, the one week a year where we ask our kind, gentle, generous, and so-goddamn-beautiful-it-hurts-my-eyes readers of this website to help cover the costs of producing great articles, videos, and podcasts. If you make a tax-deductible donation of $50, you get a temporary Reason tattoo and to see your name in the banner ad celebrating our supporters. At $100, you get that, plus a digital subscription (with access to 50-plus years of archives) and optional Twitter, Facebook, and Instagram shout-outs. At $500, you get all that, plus a 2021 Reason calendar and a signed copy of Robby Soave’s Tech Panic. For $1,000, you get even more, including lunch in D.C. with an editor. Go here to see all the different giving levels.

And click on the image here to check out what is surely the first non-fungible token (NFT) that is being auctioned off to support a “think magazine.”

Ted Barnett, one of the tech-savvy trustees of the nonprofit Reason Foundation that publishes Reason, is auctioning off this NFT of the regulars on The Reason Roundtable podcast (Katherine Mangu-Ward, Peter Suderman, Matt Welch, and me), with all of the proceeds going to fund our journalism.

If you’re new to the weird, wild, and wonderful world of NFTs, read this explainer from Reason‘s Liz Wolfe. Suffice it to say that NFTs represent a form of art and property whose provenance is perfectly unique even as it is also perfectly duplicable (suck it, Walter Benjamin!). NFTs are hot now and they may indeed turn out to be a passing fad in the art world, even as they hold promise for all sorts of other uses and stores of value.

If you win the auction for the Reason NFT #1, you get to do with it what you want, though the “smart contract” governing the object stipulates that Reason Foundation will receive 10 percent of any future purchases (pretty cool, eh?). Whatever you pay for it will go to Reason‘s coffers (though because of complicated tax laws, you will not be able to claim the cost as a tax deduction).

The auction is hosted at Open Sea, the largest NFT site, and it requires a basic understanding of the cryptocurrency Ether and the Ethereum blockchain, how crypto wallets work, and some time to work through the kinks of connecting your crypto funds, your wallet, and Open Sea. But if I—a left-handed, near-sighted, 58-year-old English major—can figure all that out, so can you. Nobody said the future would be frictionless, and Open Sea has a rich FAQs section that should help. The auction ends when the webathon does, at 6 p.m. on Tuesday, December 7.

So become the first owner of the first Reason NFT and do with it what you will! Or support Reason‘s journalism—and a future of libertarian “free minds and free markets”—by more conventional, fully tax-deductible means using credit cards, PayPal, or crypto (of course). The swag is pretty great (for $5,000, you get too much stuff to list in a parenthetical!) and it’s all right here.

Established in 1968, Reason has a long history of discovering, inventing, and championing the future. We were the first serious magazine to champion outlandish, seemingly insane policies such as drug legalization and equal rights for gays and lesbians half a century ago when more conventional rags like National Review and The New Republic were locked in twilight struggles over threats posed by long hair and rock music. We were early adopters to the web (circa 1995) and we published the first-ever mass-individualized magazine that sent unique covers and content to 40,000-plus subscribers. In 2007, we launched our award-winning video platform that has gone on to pull 234 million views at YouTube alone (and millions more at Facebook, Twitter, and Instagram). If some aspects of Termination Shock, the wonderful new Neal Stephenson novel about geoengineering, sound familiar, you may have read about them here in 1997.

At Reason, we don’t fear the future, we celebrate it—and want to help guide its development by exploring what policies, technologies, mindsets, and temperaments are best suited to prosper in the creative destruction that is an essential part of a vibrant, innovative, and forward-facing world.

And that brings me to a fun new thing we’re doing as part of our annual webathon, the one week a year where we ask our kind, gentle, generous, and so-goddamn-beautiful-it-hurts-my-eyes readers of this website to help cover the costs of producing great articles, videos, and podcasts. If you make a tax-deductible donation of $50, you get a temporary Reason tattoo and to see your name in the banner ad celebrating our supporters. At $100, you get that, plus a digital subscription (with access to 50-plus years of archives) and optional Twitter, Facebook, and Instagram shout-outs. At $500, you get all that, plus a 2021 Reason calendar and a signed copy of Robby Soave’s Tech Panic. For $1,000, you get even more, including lunch in D.C. with an editor. Go here to see all the different giving levels.

And click on the image here to check out what is surely the first non-fungible token (NFT) that is being auctioned off to support a “think magazine.”

Ted Barnett, one of the tech-savvy trustees of the nonprofit Reason Foundation that publishes Reason, is auctioning off this NFT of the regulars on The Reason Roundtable podcast (Katherine Mangu-Ward, Peter Suderman, Matt Welch, and me), with all of the proceeds going to fund our journalism.

If you’re new to the weird, wild, and wonderful world of NFTs, read this explainer from Reason‘s Liz Wolfe. Suffice it to say that NFTs represent a form of art and property whose provenance is perfectly unique even as it is also perfectly duplicable (suck it, Walter Benjamin!). NFTs are hot now and they may indeed turn out to be a passing fad in the art world, even as they hold promise for all sorts of other uses and stores of value.

If you win the auction for the Reason NFT #1, you get to do with it what you want, though the “smart contract” governing the object stipulates that Reason Foundation will receive 10 percent of any future purchases (pretty cool, eh?). Whatever you pay for it will go to Reason‘s coffers (though because of complicated tax laws, you will not be able to claim the cost as a tax deduction).

The auction is hosted at Open Sea, the largest NFT site, and it requires a basic understanding of the cryptocurrency Ether and the Ethereum blockchain, how crypto wallets work, and some time to work through the kinks of connecting your crypto funds, your wallet, and Open Sea. But if I—a left-handed, near-sighted, 58-year-old English major—can figure all that out, so can you. Nobody said the future would be frictionless, and Open Sea has a rich FAQs section that should help. The auction ends when the webathon does, at 6 p.m. on Tuesday, December 7.

So become the first owner of the first Reason NFT and do with it what you will! Or support Reason‘s journalism—and a future of libertarian “free minds and free markets”—by more conventional, fully tax-deductible means using credit cards, PayPal, or crypto (of course). The swag is pretty great (for $5,000, you get too much stuff to list in a parenthetical!) and it’s all right here.

{kind=link}