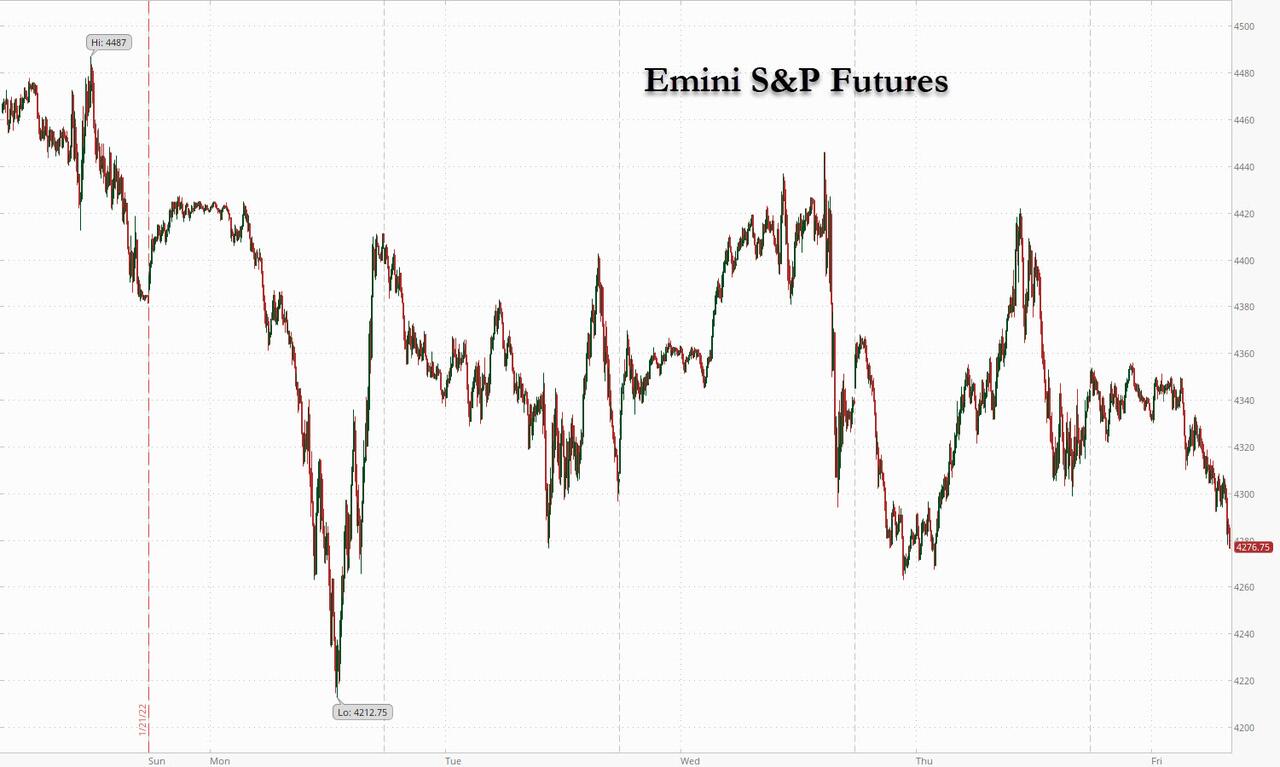

If you thought that yesterday’s blowout, record earnings from Apple would be enough to put in at least a brief bottom to stocks and stop the ongoing collapse in risk assets, we have some bad news for you: after staging a feeble bounce overnight, S&P futures erased earlier gains as traders ignored the solid results from Apple and instead focused on the risk of higher interest rates hurting economic growth. Contracts in S&P 500 dropped as negative sentiment continued to prevail, while Nasdaq 100 futures erased earlier gains after strong Apple earnings. As of 730am, Emini futures were down 48 points or 1.12% to 4,269, Dow futures were down 335 points or 0.99% and Nasdaq futs were down 77 or 0.6%. The dollar was set for a fifth straight day of gains, the longest streak since November, 19Y TSY yields were up 3bps to 1.83%, gold and bitcoin both dropped.

Markets have been whiplashed by volatility this week as the Federal Reserve signaled aggressive tightening, adding to investor concerns about geopolitical tensions and an uneven earnings season. Also sapping sentiment on Friday were weak data on the German economy and euro-area confidence. Meanwhile, geopolitical tensions were still on the agenda with a potential conflict in Ukraine not yet defused.

“Market expectations for four to five rate hikes this year will not derail growth or the equity rally,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “We expect an eventual relaxation of tensions between Russia and Ukraine,” he added. Expected data on Friday include personal income and spending data, as well as University of Michigan Sentiment, while Caterpillar, Chevron, Colgate-Palmolive, VF Corp and Weyerhaeuser are among companies reporting earnings.

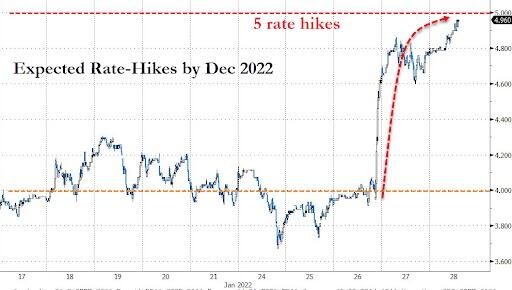

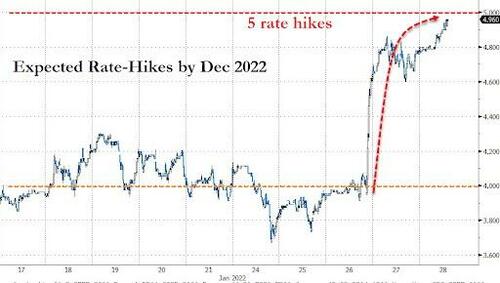

Money markets are now pricing in nearly five Fed hikes this year after a hawkish stance from Chair Jerome Powell. That’s up from three expected as recently as December.

“Tighter liquidity and weaker growth mean higher volatility,” Barclays Plc strategists led by Emmanuel Cau wrote in a note. The “current growth scare looks like a classic mid-cycle phase to us, while a lot of hawkishness is priced in.”

In premarket trading, Apple shares rose 4.5% as analysts rose their targets to some of the most bullish on the Street, after the iPhone maker reported EPS and revenue for the fiscal first quarter that beat the average analyst estimates. Watch Apple’s U.S. suppliers after the iPhone maker posted record quarterly sales that beat analyst estimates, a sign it was able to work through the supply-chain crunch. Peers in Asia rose, while European suppliers are active in early trading. Tesla shares also rise as much as 2% in premarket, set to rebound from yesterday’s 12% slump following a disappointing set of earnings and outlook. Other notable premarket movers:

- Visa (V US) shares gain 5% premarket after company reported adjusted earnings per share for the first quarter that beat the average analyst estimate.

- Cryptocurrency-exposed stocks gain as Bitcoin and other digital tokens rise. Riot Blockchain (RIOT US) +3.7%, Marathon Digital (MARA US) +3.3%, Bit Digital (BTBT US) +1.6%, Coinbase (COIN US) +0.5%.

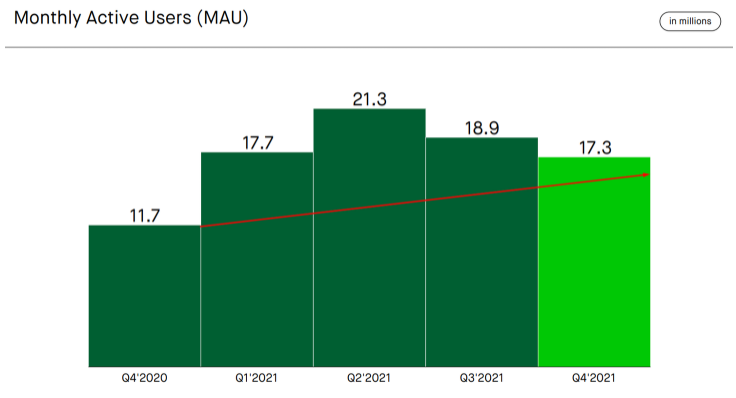

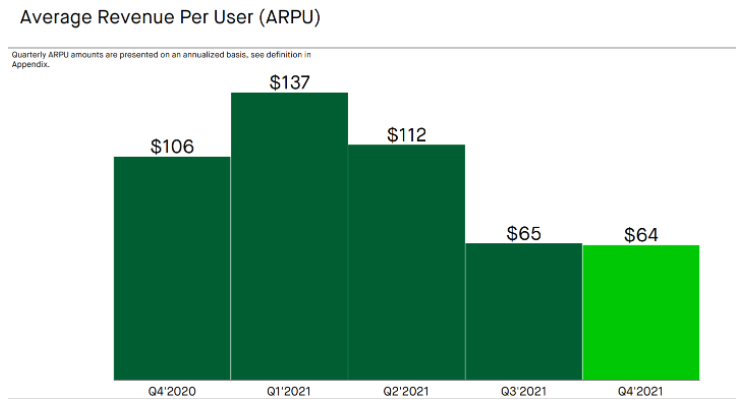

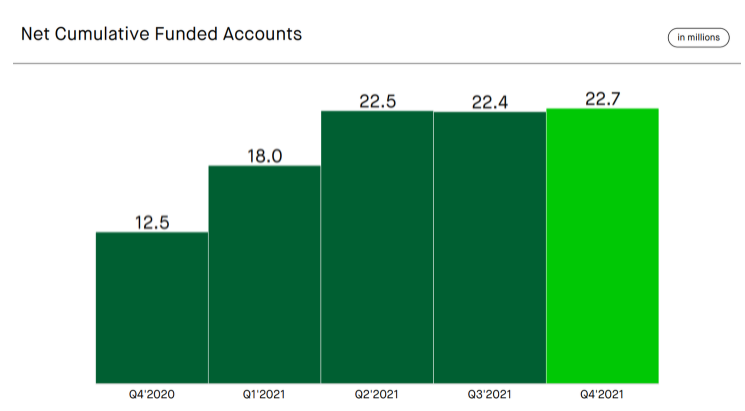

- Robinhood (HOOD US) shares tumbled 14% in premarket after the online brokerage’s fourth-quarter revenue and first-quarter outlook missed estimates. Some analysts cut their price targets.

- Atlassian (TEAM US) shares jump 10% in extended trading on Thursday, after the software company reported second-quarter results that beat expectations and gave a third-quarter revenue forecast that was ahead of the analyst consensus.

- U.S. Steel (X US) shares fall as much as 2.4% aftermarket following the steelmaker’s earnings release, which showed adjusted earnings per share results missed the average analyst estimate.

The U.S. stock market is priced “quite aggressively” versus other developed nations as well as emerging markets, and valuations in the latter can be a tailwind rather than a headwind as in the U.S., Feifei Li, partner and CIO of equity strategies at Research Affiliates, said on Bloomberg Television.

European equity indexes are again under pressure, rounding off a miserable week, and set for the worst monthly decline since October 2020 as corporate earnings failed to lift the mood except in the retail sector. The Euro Stoxx 50 dropped over 1.5%, DAX underperforming at the margin. Autos, tech and banks are the weakest Stoxx 600 sectors; only retailers are in the green. Hennes & Mauritz shares climbed on a profit beat, while technology stocks continued to underperform. Here are some of the biggest European movers today:

- LVMH shares rise as much as 5.8% after analysts praised the French conglomerate’s full-year results, with several noting improved performance at even minor brands such as Celine.

- Signify gains as much as 15% after saying it expects to grow in 2022 even as the supply chain problems that caused its “worst ever” quarter continue.

- H&M climbs as much as 7.4% after posting a strong margin in 4Q which impressed analysts. Analysts also lauded the Swedish retailer’s buyback announcement and target to double sales by 2030.

- Stora Enso rises as much as 6.2% on 4Q earnings with the CEO noting paper capacity closures have helped boost its pricing power, contributing to a turnaround in the unprofitable business.

- SCA gains as much as 5.5% in Stockholm, the most since May 2020, after reporting better-than-expected Ebitda earnings and announcing a SEK3.25/share dividend — higher than analysts had estimated.

- AutoStore rises as much as 18% after a German court halts Ocado’s case against the company. Ocado drops as much as 8.1%.

- Henkel slides as much as 10% after the company’s forecast for organic revenue growth of 2% to 4% in 2022 was seen as cautious.

- Wartsila falls as much as 9% after posting 4Q earnings that analysts say showed strong order intake overshadowed by lagging margins.

- Alstom drops as much as 7.3% after Exane BNP Paribas downgrades to neutral, citing risk that the company might resort to raising equity financing to forestall a possible credit-rating cut.

Earlier in the session, Asian stocks rose after slumping to their lowest since November 2020, with Japan and Australia leading the rebound as turbulence over the highly anticipated U.S. monetary tightening eased. The MSCI Asia Pacific Index climbed as much as 1% on Friday following a 2.7% slide the day before. Industrials and consumer-discretionary names provided the biggest boosts to the measure. Japan’s Nikkei 225 Stock Average was among the best performers in the region after enduring its worst daily drop in seven months. “It’s undeniable that stock markets last year — as well as the real economy — were supported by continued monetary easing, considering which, more share-price correction could be anticipated,” said Tetsuo Seshimo, a portfolio manager at Saison Asset Management in Tokyo. Even so, “stocks fell too much yesterday.” The Asian benchmark is down almost 5% this week, and set to cap its biggest such drop since February last year. Federal Reserve Chair Jerome Powell said the central bank was ready to raise interest rates in March and didn’t rule out moving at every meeting to tackle inflation, triggering a broad selloff in global equities Thursday. Japan’s Topix and Australia’s S&P/ASX 200 gained after slipping into technical correction earlier this week. South Korea’s Kospi also added almost 2% after sliding into a bear market Thursday. Meanwhile, Chinese shares extended a rout of nearly $1.2 trillion this month.

Japanese equities rose, trimming their worst weekly loss in two months, as some observers saw the selloff on concerns over higher U.S. interest rates as having gone too far. Electronics and auto makers were the biggest boosts to the Topix, which rose 1.9%, paring its weekly decline to 2.6%. Fast Retailing and Shin-Etsu Chemical were the largest contributors to a 2.1% rise in the Nikkei 225. The yen was little changed after weakening 1.3% against the dollar over the previous two sessions. “Looking at the technical indicators like RSI, you can see that Japanese equities have been oversold,” said Nobuhiko Kuramochi, a market strategist at Mizuho Securities. “Shares have fallen too much considering the not-bad corporate earnings and also when compared with U.S. equities.” U.S. futures rallied in Asian trading hours, after a volatile cash session that ended in losses as investors continued to reprice assets on the Fed’s pivot to tighter policy. Apple provided a post-market lift with record quarterly sales that sailed past Wall Street estimates.

In Australia, the S&P/ASX 200 index rose 2.2% to 6,988.10 at the close in Sydney, bouncing back after slipping into a technical correction on Thursday. The benchmark gained for its first session in five as miners and banks rallied, trimming its weekly slide to 2.6%. Champion Iron was a top performer after its 3Q results. Newcrest was one of the worst performers after its 2Q production report, and as gold extended declines. In New Zealand, the S&P/NZX 50 index fell 1.6% to 11,852.15.

India’s benchmark index edged lower on Friday to extend its decline to a second consecutive week as investors grapple with volatility created by the U.S. Federal Reserve’s rate-hike plan. The S&P BSE Sensex fell 0.1% to 57,200.23 in Mumbai on Friday, erasing gains of as much as 1.4% earlier in the session. The NSE Nifty 50 Index ended flat. For the week, the key gauges ended with declines of 3.1% and 2.9%, respectively. All but five of the 19 sector sub-indexes compiled by BSE Ltd. climbed on Friday, led by a measure of health-care companies. BSE’s mid- and small-sized companies’ indexes outperformed the benchmark by rising 1% and 1.1%. “Selling pressure has now cooled off, markets will now focus on local triggers such as expectations from the budget,” said Prashant Tapse, an analyst with Mumbai-based Mehta Equities. Investors will also monitor corporate-earnings reports for the December quarter to gauge demand and inflation outlook. Of the 21 Nifty 50 companies that have announced results so far, 12 either met or exceeded expectations, eight missed, while one can’t be compared. Kotak Mahindra Bank continued the strong earnings run by lenders, reporting fiscal third-quarter profit ahead of the consensus view, while Dr. Reddy’s Laboratories missed the consensus estimate. ICICI Bank contributed the most to the Sensex’s decline, falling 1.6%. Out of 30 shares in the Sensex index, 14 rose and 16 fell.

In rates, bonds trade poorly again with gilts and USTs bear steepening, cheapening 3-3.5bps across the back end. Treasuries are weaker, same as most European bond markets, with stock markets under pressure globally and S&P 500 futures lower but inside weekly range. Treasury yields are cheaper by 4bp-5bp from intermediate to long-end sectors, 10-year around 1.84%, inside weekly range; though front-end outperforms, 2-year yield reaches YTD high 1.22%, steepening 2s10s by ~1bp. Gilts underperformed as traders price in a more aggressive path of rate hikes from the BOE. Treasury curve is steeper for first day in four, lifting spreads from multimonth lows. Globally in 10-year sector, gilts lag Treasuries by 0.5bp while bunds outperform slightly. Bunds bear flatten with 5s30s near 52bps after two block trades but subsequently recover above 54bps. IG dollar issuance slate empty so far; Procter & Gamble priced a $1.85b two-tranche offering Thursday, the first since Wednesday’s Fed meeting.

In FX, Bloomberg Dollar Spot pushes to best levels for the week. Scandies and commodity currencies suffer the most. The Bloomberg Dollar Spot Index was set for a fifth straight day of gains, the longest streak since November, and near its strongest level in 17 months as the greenback was steady or higher against all of its Group-of-10 peers. The euro steadied near a European session low of $1.1121 while risk-sensitive Australian and Scandinavian currencies led the decline. Sweden’s krona sank, despite data showing the Nordic nation’s economy grew more than expected in the final quarter of 2021, fueling speculation that the central bank could soon start to take its foot off the stimulus pedal. Australia’s dollar dropped to the lowest level in 18 months as the Reserve Bank of Australia lags behind many of its peers in signaling monetary tightening. Treasuries sold off, led by the belly; Bunds also traded lower, yet outperformed Treasuries, and Germany’s 5s30s curve flattened to 52bps after two futures blocks traded. Italian government bonds underperformed with the nation’s parliament voting twice on Friday to elect a new president, as the lack of progress after four days of inconclusive ballots adds to pressure to end a process that’s left the country in limbo.

In commodities, Crude futures hold a narrow range, just shy of Asia’s best levels. WTI trades either side of $87, Brent just shy of a $90-handle. Spot gold drops near Thursday’s lows, close to $1,791/oz. Base metals are under pressure; LME copper underperforms peers, dropping over 1.5%.

Crypto markets were rangebound in which Bitcoin traded both sides of the 37,000 level. Russia’s government drafted a roadmap for cryptocurrency regulation, according to RBC.

To the day ahead now, and data releases include Germany’s Q4 GDP, US personal income and personal spending for December, as well as the Q4 employment cost index and the University of Michigan’s final consumer sentiment index for January. Earnings releases include Chevron and Caterpillar.

Market Snapshot

- S&P 500 futures up 0.1% to 4,323.75

- STOXX Europe 600 down 1.0% to 465.51

- MXAP up 0.5% to 182.48

- MXAPJ little changed at 597.31

- Nikkei up 2.1% to 26,717.34

- Topix up 1.9% to 1,876.89

- Hang Seng Index down 1.1% to 23,550.08

- Shanghai Composite down 1.0% to 3,361.44

- Sensex down 0.1% to 57,197.94

- Australia S&P/ASX 200 up 2.2% to 6,988.14

- Kospi up 1.9% to 2,663.34

- Brent Futures up 0.4% to $89.71/bbl

- Gold spot down 0.3% to $1,792.52

- U.S. Dollar Index up 0.13% to 97.38

- German 10Y yield little changed at -0.05%

- Euro down 0.1% to $1.1132

Top Overnight News from Bloomberg

- The euro-area economy kicked off 2022 on a weak footing, with pandemic restrictions taking a toll on confidence and growing fears that Germany may be on the brink of a recession for the second time since the crisis began. A sentiment gauge by the European Commission fell to 112.7 in January, the lowest in nine months, driven by declines in most sectors and among consumers. Employment expectations dropped for a second month

- Germany’s economy shrank 0.7% in the fourth quarter with consumers spooked by another wave of Covid-19 infections and factories reeling from supply-chain problems.

- Russian Foreign Minister Sergei Lavrov said on Friday that the American proposal to defuse tensions with Ukraine contained “rational elements,” even though some key points were ignored

- A U.K. government probe into alleged rule-breaking parties in Boris Johnson’s office during the pandemic could be stripped of key details at the request of police, potentially handing the prime minister a boost as he tries to persuade his Conservatives not to mount a leadership challenge

- Governor Haruhiko Kuroda said the Bank of Japan won’t be switching its bond yield target until inflation rises high enough to warrant exit talks

- Seven straight jumps in the so- called “fear gauge” for the S&P 500 is a signal that it may be time to wager against volatility, if history is any guide. Only 10 times in the past two decades has the Cboe Volatility Index – – better known as the VIX — risen for that many trading sessions in a row

A more detailed look at global markets courtesy of Newsquawk

Asian stocks eventually traded mixed although China lagged ahead of holiday closures next week. ASX 200 (+2.2%) was lifted back up from correction territory. Nikkei 225 (+2.1%) gained on a weaker currency and with corporate results driving the biggest movers. KOSPI (+1.9%) was boosted by earnings including from the world’s second-largest memory chipmaker SK Hynix. Hang Seng (-1.1%%) and Shanghai Comp. (-0.9%) lagged with a non-committal tone in the mainland ahead of the Lunar New Year holiday closures and with Hong Kong pressured by losses in blue chip tech and health care

Top Asian News

- Asia Stocks Rise, Still Head for Worst Week Since February

- Kuroda Hints No Chance of Switching Yield Target Until Exit

- China Fintech PingPong Said to Mull $1 Billion Hong Kong IPO

- Biogen Sells Bioepis Stake for $2.3 Billion to Samsung Biologics

European bourses have conformed to the downbeat APAC handover with losses in the region extending following the cash open, Euro Stoxx 50 -1.7%. Sectors were mixed with Tech and Banking names the laggards while Personal/Household Goods and Retail outperformer following LVMH and H&M respectively; since then, performance has deteriorated though the above skew remains intact. US futures are moving in tandem with European-peers; however, magnitudes are more contained as the ES is only modestly negative and NQ continues to cling onto positive territory following Apple earnings. Apple Inc (AAPL) Q1 2022 (USD): EPS 2.10 (exp. 1.89), Revenue 123.95bln (exp. 118.66bln), iPhone: 71.63 bln (exp. 68.34bln), iPad: 7.25bln (exp. 8.18bln), Mac: 10.85bln (exp. 9.51bln), Services: 19.52bln (exp. 18.61 bln), according to Businesswire. +3.5% in the pre-market, trimming from gains in excess of 5.0% earlier

Top European News

- German Economy Contracted Amid Tighter Virus Curbs, Supply Snags

- H&M CEO Sets Target to Double Retailer’s Sales by 2030

- Telia Sells Tower Stake for $582 Million, Cuts Costs

- U.K. ‘Partygate’ Probe May Be Watered Down at Police Request

In FX, buck bull run continues as DXY takes out another July 2020 high to leave just 97.500 in front of key Fib resistance. Aussie feels the heat of Greenback strength more than others amidst risk-off positioning and caution ahead of next week’s RBA policy meeting. Kiwi also lagging and Loonie losing crude support after the BoC’s hawkish hold midweek. Euro and Yen reliant on some hefty option expiry interest to provide protection from Dollar domination. BoJ Governor Kurdoa if times come to debate the exit of policy, then targeting shorter maturity JGBs could become an option; at this stage its premature to raise yield target or take steps to steepen yield curve.

In commodities, WTI and Brent are consolidating somewhat after yesterday’s choppy price action, but remain towards the lowend

of a circa. USD 1.00/bbl range. Focus remains firmly on geopols as Russia is set to speak with French and German officials on Friday, though rhetoric, remains relatively familiar. Spot gold and silver are pressured as the yellow metal loses the 100-DMA, and drops to circa. USD 1780/oz as the USD rallies, and ahead of inflation data while LME copper follows the equity downside.

In Geopolitics:

- US President Biden reaffirmed in call with Ukraine’s President the readiness of US to respond decisively if Russia further invades Ukraine, according to Reuters.

- Russian Foreign Minister Lavrov says Russia is analysing NATO and US proposals and will decide on how to respond to them, via Reuters; additionally, Lavrov will speaking with German Foreign Minister Baerbock on Friday, via Ifx.

- Russia’s Kremlin says President Putin’s talks with Chinese President Xi will give attention to security in Europe and Russia-US dialoged, according to Reuters; Kremlin does not rule out that Putin will provide some assessments on response to Russian proposals.

- US requested a public UN Security Council meeting for Monday to discuss the build up of Russian forces on Ukraine border, according to Reuters citing diplomats.

- US bipartisan group of Senators have reportedly been meeting to create legislation that would dramatically increase presence of US military aid for Ukraine, according to Reuters sources.

- Lithuania and Germany are in discussions to increase the presence of the German military, given current events, according to Reuters

US Event Calendar

- 8:30am: 4Q Employment Cost Index, est. 1.2%, prior 1.3%

- 8:30am: Dec. Personal Income, est. 0.5%, prior 0.4%

- Dec. PCE Core Deflator YoY, est. 4.8%, prior 4.7%; PCE Core Deflator MoM, est. 0.5%, prior 0.5%

- Dec. PCE Deflator YoY, est. 5.8%, prior 5.7%; PCE Deflator MoM, est. 0.4%, prior 0.6%

- 8:30am: Dec. Personal Spending, est. -0.6%, prior 0.6%; Real Personal Spending, est. -1.1%, prior 0%

- 10am: Jan. U. of Mich. Sentiment, est. 68.8, prior 68.8

- Current Conditions, est. 73.2, prior 73.2; Expectations, est. 65.9, prior 65.9

- 1 Yr Inflation, est. 4.9%, prior 4.9%; U. of Mich. 5-10 Yr Inflation, prior 3.1%

DB’s Jim Reid concludes the overnight wrap

What a week we’ve had. Yesterday saw another market whipsaw as markets continued to try to digest the aftermath of Chair Powell’s press conference. In particular, there was growing speculation that the Fed would embark on back-to-back hikes in order to get inflation under control, with Fed funds futures now pricing 2 full hikes over the next two meetings in March and May, in line with our US econ team’s updated call. Assuming this is realised, then this would be a much faster pace of hikes than anything seen over the last cycle, when the initial hike in December 2015 wasn’t followed by another for an entire year, and the fastest things got was a consistent quarterly pace when the Fed hiked 4 times in 2018. This time, we almost have 4 hikes priced between March and September alone. Of course however, it’s worth noting that today they face a very different set of circumstances, since the last hiking cycle actually began with inflation beneath the Fed’s target, and was a pre-emptive one given their belief that inflation would rise from that point. By contrast, this cycle of rate hikes is set to begin with inflation at levels not seen since the early 1980s, with the Fed seeking to regain credibility after consistently underestimating inflation over the last year. As we’ve highlighted in our work over the last 6-9 months this is a very, very, very different cycle to the last one and we should therefore expect different inflation and Fed outcomes. We repeat a few slides on this in the chart book so feel free to dip in.

These growing expectations of near-term hikes supported the more policy-sensitive 2yr Treasury yield, which rose a further +3.8bps to a fresh post-pandemic high after the previous day’s massive +13.3bps advance. And the number of hikes priced for 2022 as a whole actually rose to a new high of its own at 4.8 hikes. However, a -6.4bps decline in the 10yr yield to 1.80% meant that there was a further flattening of the yield curve, with the 2s10s down to its flattest level in over a year, at just 60.9bps. This is only adding to the late-cycle signals we’ve been discussing of late, particularly when you consider that the yield curve historically tends to flatten in the year after the Fed begins hiking rates, so an inversion over the next 12 months would be no surprise on a historic basis followed perhaps by a 2024 recession? See the chart book for more on this. Indeed, some parts of the curve are even closer to inverting than the 2s10s, with the 5s10s slope at just 14.1bps yesterday, which is the flattest it’s been since the initial market panic about Covid back in March 2020.

The implications of this hawkish push could also be seen in FX markets, where the dollar index strengthened +0.81% to levels not seen in over 18 months. Conversely though, the Fed’s more aggressive posture on inflation significantly hurt precious metals, with gold (-1.22%) falling by more than -1% for a second consecutive session.

Transatlantic equity performance was a mixed bag yesterday. The STOXX 600 fell -1.47% immediately after the European open, just as US futures were pointing to additional losses on top of the previous day’s. However, sentiment turned into the European afternoon, with the major indices on both sides of the Atlantic moving into positive territory, leaving the STOXX 600 +0.65% higher. True to recent form though, the S&P 500 reversed course after the European optimists called it a day, drifting lower to end the day at -0.54%. Sector performance was fairly split, with five sectors in the red: discretionary (-2.27%) and real estate (-1.75%), industrials (-0.93%), financials (-0.92%), and tech (-0.69%). Energy (+1.24%) was again the outperformer, but didn’t do enough to drag the entire index into the green. Tesla was a big driver of the discretionary drawdown. After bouncing around following its earnings release the evening before, Tesla declined -11.55% yesterday on the back of potential supply chain issues, and to a 3-month low. The NASDAQ underperformed the S&P, declining -1.40%, bringing it -16.84% below its all-time high. The Russell 2000 of small caps (-2.29%) fell into “bear market” territory and is now down -20.94% from its highs in early November. The Vix index of volatility closed modestly lower (-1.37ppts) for the first time in almost two weeks, but remained elevated at 30.59.

Apple reported fourth quarter earnings after the close. Like other goods manufactures, they continued to be besot by supply chain issues, but that did not stop them from beating sales and earnings estimates, posting their best quarter of revenues ever. The stock was more than +5% higher in after-hours trading following the release. Prior to this they were down around -10% YTD. This has helped the S&P 500 (+0.7%) and Nasdaq (+1.1%) futures rebound as we hit the last day of a tough and very volatile week.

Overnight in Asia, equity markets are also recovering some of their recent losses with the Nikkei rebounding (+2.17%), after falling nearly -3% in the previous session, followed by the Kospi (+1.44%). Meanwhile, the Shanghai Composite (+0.05%) and CSI (0.08%) are trading flattish as we type. On the other hand, the Hang Seng (-0.94%) is extending its recent losses this morning ahead of the release of Hong Kong’s Q4 GDP report scheduled in a few hours.

Early morning data showed consumer prices in Tokyo fell to +0.5% y/y in January from +0.8% in December while the core CPI inflation (+0.2% y/y) in January failed to exceed market expectations (+0.3%) after increasing +0.5% last month. Elsewhere, South Korea’s industrial output surprisingly advanced +4.3% m/m in December against economist expectations of -0.3%. It follows November’s upwardly revised +5.3% increase.

Back in Europe, sovereign bond yields rose for the most part, having been closed at the time of Chair Powell’s press conference the previous day. Those on 10yr bunds (+1.6bps), OATs (+0.7bps) and gilts (+3.1bps) all moved higher, and that rise in gilt yields comes ahead of next week’s Bank of England decision, where overnight index swaps are now pricing in a 94% chance of another rate hike, which is also our UK economist’s expectation.

One factor supporting sentiment yesterday was a decent set of economic data, with the US economy growing by an annualised rate of +6.9% in Q4 2021 (vs. +5.5% expected). That’s the fastest quarterly pace since Q3 2020 when the economy rebounded sharply from the various lockdowns, and left growth for the full year 2021 at +5.7%, the fastest since 1984. Meanwhile, the weekly initial jobless claims for the week through January 22 subsided to 260k (vs. 265k expected), ending a run of 3 consecutive weekly increases.

To the day ahead now, and data releases include Germany’s Q4 GDP, US personal income and personal spending for December, as well as the Q4 employment cost index and the University of Michigan’s final consumer sentiment index for January. Earnings releases include Chevron and Caterpillar.