1/31/2006: Justice Samuel Alito takes oath.

The post Today in Supreme Court History: January 31, 2006 appeared first on Reason.com.

from Latest – Reason.com https://ift.tt/ryXTq9FsB

via IFTTT

another site

1/31/2006: Justice Samuel Alito takes oath.

The post Today in Supreme Court History: January 31, 2006 appeared first on Reason.com.

from Latest – Reason.com https://ift.tt/ryXTq9FsB

via IFTTT

Deputizing private parties to restrict liberty has become popular among politicians constrained by constitutional protections for individual rights. They get to target personal freedom without explicitly restricting anything, like a bratty kid waving his hands around a sibling’s face while chanting “I’m not touching you!” The latest such example is the San Jose, California, city government, which insists that it is “constitutionally compliant” in requiring gun owners to purchase liability insurance and to pay an “annual gun harm reduction fee” to exercise a right specifically protected by the Second Amendment.

“Tonight San José became the first city in the United States to enact an ordinance to require gun owners to purchase liability insurance, and to invest funds generated from fees paid by gun owners into evidence-based initiatives to reduce gun violence and gun harm,” San Jose Mayor Sam Liccardo boasted in a January 25 statement. “Thank you to my council colleagues who continue to show their commitment to reducing gun violence and its devastation in our community. I am deeply grateful also to our advocacy and legal partners with Cotchett, Pitre & McCarthy, LLP, EveryTown, Moms Demand Action, SAFE, the Gifford Law Alliance and many others who work tirelessly to help us craft a constitutionally compliant path to mitigate the unnecessary suffering from gun harm in our community. I look forward to supporting the efforts of others to replicate these initiatives across the nation.”

There’s a lot to unravel in that smug statement, including the assumption that firearms ownership imposes costs and not benefits, as well as the assertion that requiring people to carry liability insurance and pay fees to the government in order to exercise a right specifically enumerated in the Second Amendment is somehow constitutionally compliant. None of what Liccardo says is well-grounded in reality. But he’s especially sensitive to the idea that imposing costs on gun owners is an example of government overreach.

“This isn’t actually governmental regulation,” Liccardo insisted to NPR last week. “This is private sector regulation. This is insurance companies. Insurance companies have been regulating safety of automobiles for five decades, and as a result, we all have seen per mile deaths drop dramatically over the last five decades because we have air bags and anti-lock brakes and so forth that insurance companies incentivize drivers to go buy.”

That’s a common comparison for gun prohibitionists and it doesn’t improve with repetition. For starters “the right to bear arms” enjoys specific constitutional protections, unlike car ownership. Then there’s the fact that, like many places, California doesn’t require insurance and registration for vehicles used only on private property or transported by trailer. If the Second Amendment didn’t protect gun ownership, that might make car insurance and fee requirements comparable to burdens on people carrying concealed weapons, but not to those placed on people keeping guns in their homes and taking them to a range.

Even worse is that automobile regulation is an unfortunate example of how burdensome restrictions can become on activities that don’t enjoy specific protection. From tags and taxes we’ve moved on to inspections and fuel-economy requirements, and now politicians propose mandating interlock technology that prevents vehicles from starting if built-in sensors detect alcohol in our bodies. This isn’t a path to follow, it’s a warning of what might be in store.

That’s especially true when politicians coyly deputize private parties to impose restrictions that they are prevented from putting into law. The San Jose city government’s restrictionist agenda is obvious from the list of gun control organizations Liccardo thanks in his press release. The clear assumption is that imposing fees and insurance requirements will create new barriers to owning firearms. Insurance companies may be on-board with that mission, or the heavily regulated industry may just succumb to government pressure to cooperate. This wouldn’t be the first time the private sector has been put in that role.

“I am directing the Department of Financial Services to urge insurers and bankers statewide to determine whether any relationship they may have with the NRA or similar organizations sends the wrong message to their clients and their communities who often look to them for guidance and support,” then-New York Gov. Andrew Cuomo urged in a 2018 statement.

“The NRA alleges that Cuomo and top members of his administration abused their regulatory authority over financial institutions to threaten New York banks and insurers that associate with the NRA or other ‘gun promotion’ groups, and that those threats have jeopardized the NRA’s access to basic insurance and banking services in New York,” the ACLU responded. “In the ACLU’s view, targeting a nonprofit advocacy group and seeking to deny it financial services because it promotes a lawful activity (the use of guns) violates the First Amendment.”

Leaning on the private sector to lean on people you don’t like because politicians aren’t allowed to lean on them directly is “constitutionally compliant” only in a brat’s “I’m not touching you” sense. It’s an end-run around legal protections for the exercise of individual rights.

The problems with requiring people to pay fees and carry insurance to exercise their rights might be more obvious if the San Jose city government had imposed its rules on journalists and bloggers. Liability insurance and annual fees would be obvious infringements of First Amendment rights if smugly imposed as an effort to offset the supposed harms caused by alleged disinformation and misinformation. Then again, Liccardo and company might consider that a clever idea after all.

“In a new trend, many governments have sought to shift the burden of censorship to private companies and individuals by pressing them to remove content, often resorting to direct blocking only when those measures fail,” Freedom House warned in 2015. “Local companies are especially vulnerable to the whims of law enforcement agencies and a recent proliferation of repressive laws. But large, international companies like Google, Facebook, and Twitter have faced similar demands due to their significant popularity and reach.”

Since then, privatized authoritarianism has only proliferated. We now commonly see demands that companies boot disfavored speakers coming from sources as highly placed as the White House. Politicians who think it’s fine to conscript private businesses into muzzling their opponents were never going to balk at drafting those same firms into helping them to disarm the public. Rather than submit, people who care about liberty need to exercise it in defiance of out-sourced efforts at control.

The post San Jose's Insurance Requirement Is Privatized Gun Control appeared first on Reason.com.

from Latest – Reason.com https://ift.tt/SWz5nFUAt

via IFTTT

“Thank You To The Haters”: Joe Rogan Breaks Silence On Spotify Controversy, Rejects “Disinformation” Label

Hours after Spotify said in a statement that it would modify its content policies – which Joe Rogan did not violate, the company clarified – and adopt a “content advisory” for certain podcast episodes in an effort to placate the snowflakes, Joe Rogan finally broke his silence on the uproar over his podcast in a 10-minute video shared to Instagram.

In the video, a kind of frank confessional apparently shot by Rogan himself using his own phone, Rogan apologized to those he had unwittingly offended, before launching into a poignant, carefully crafted explanation that gently nudged and reminded objectors about why Rogan’s show is a must-listen, and a leader in the modern-day podcast gold rush.

But first, Rogan asked listeners to ignore certain “disparaging” headlines that he said misrepresent what he’s doing.

“I wanted to make this video first of all because I think there are a lot of people who have a distorted misconception about what I do maybe based on soundbites or headlines of articles that are disparaging. The podcast has been accused of spreading ‘dangerous misinformation’…specifically about two episodes, one with Dr. Peter McCollough and one with Dr. Robert Malone.”

Both doctors are highly credentialed, while also harboring views on SARS-CoV-2 and how to combat it that are “different” from the mainstream narrative.

“Both of these people are very highly credentialed very intelligent highly accomplished people and they have an opinion that’s different from the mainstream narrative. I wanted to hear what their opinion is.”

Unfortunately, there are others who are fearful of what these two doctors have to say, and believe that they are somehow personally responsible for the ongoing COVID pandemic (despite the fact that “the science” shows it’s quite obvious that there’s nothing humans can do to stop the pandemic, although they can take steps to limit fatalities).

This is the problem: since the start of the pandemic, public health authorities have seen their guidance proven wrong again and again, as comedian Adam Carolla put it: “what have you guys been right about?”

Rogan says something similar, claiming that practically every piece of “misinformation” has later been proven correct – everything from whether the vaccinated can still spread the virus, to whether COVID may have been created in a Wuhan laboratory, a view that once saw Zero Hedge banned from Twitter for months.

“The problem I have with the term disinformation, especially today, is that 8 months ago, many of the things that were considered ‘disinformation’ are now accepted as fact. For example, 8 months ago, if you said ‘if you get vaccinated you can still catch COVID and you can still spread COVID, you would be removed from social media, they would ban you from certain platforms.”

He continued: 8 months or a year ago, “…if you said ‘I don’t think cloth masks work’ you would be banned from social media, now that’s openly and repeatedly stated on CNN. If you said ‘I think it’s possible COVID may have come from a lab’ you would be banned from many social media platforms – now it’s on the cover of Newsweek.”

Again, Rogan insisted that he isn’t endorsing the views of his guests, nor proclaiming them to be somehow correct or immutable: he’s simply exploring a range of viewpoints to help his audience arrive at their own conclusions, instead of being indoctrinated with viewpoints favorable to the masters of whatever corporate-owned media they consume.

“I don’t know if they’re right? No…I’m not a doctor, I’m not a scientist…I’m just a person who sits down with people and have conversations with them. Do I get things wrong? Absolutely…but when I get things wrong I try to correct them…because I’m interested in finding out what the truth is, and I’m interested in having conversations with people who have different opinions. I’m not interested in talking with people…who have only one perspective.”

Rogan then name-checked several more mainstream COVID experts – from Dr. Sanjay Gupta and Dr. Michael Osterholm, a member of President Biden’s COVID advisory board), to others – as evidence that he is truly interested in hearing a diverse range of opinions and views, not just those who parrot the government-endorsed “official” narrative.

As for the situation with Neil Young, Rogan gamely noted that he’s “sure there are other things going on behind the scenes.” For example, might Young be doing this to try and fetch a higher price for his lifetime music catalogue ahead of a sale (like Bob Dylan did).

But still, Rogan insisted that he has always been a huge Neil Young fan, even recounting an amusing story about a Neil Young show he attended while working concert security in his youth.

As for the “interviews” he conducts with his guests, “…they are just conversations…often times I have no idea what I’m going to talk about until I sit down…that’s also the appeal of the show, it’s one of the things that makes it interesting.”

Toward the end of the video, Rogan said this to sum up:

“I’m not trying to promote misinformation, I’m not trying to do anything controversial, I’m just trying to have regular conversations with these people.”

“My pledge to you is that I will do my best to balance out these more controversial viewpoints with other people’s perspectives so that we can maybe find a better view. I don’t just want to just show the contrary opinion to what the prevailing narrative is. I want to show all kinds of opinions so that we can figure out what’s going on – and not just about COVID, about health, about fitness, wellness, the state of the world itself.

And finally, he even thanked “the haters” for helping to keep him sharp.

“Even thank you to the haters, it’s good to have some haters because it makes you reassess what you’re doing…and I think that’s good, too.”

Readers can watch the clip below:

Tyler Durden

Mon, 01/31/2022 – 07:04

via ZeroHedge News https://ift.tt/hz8KEiw4I Tyler Durden

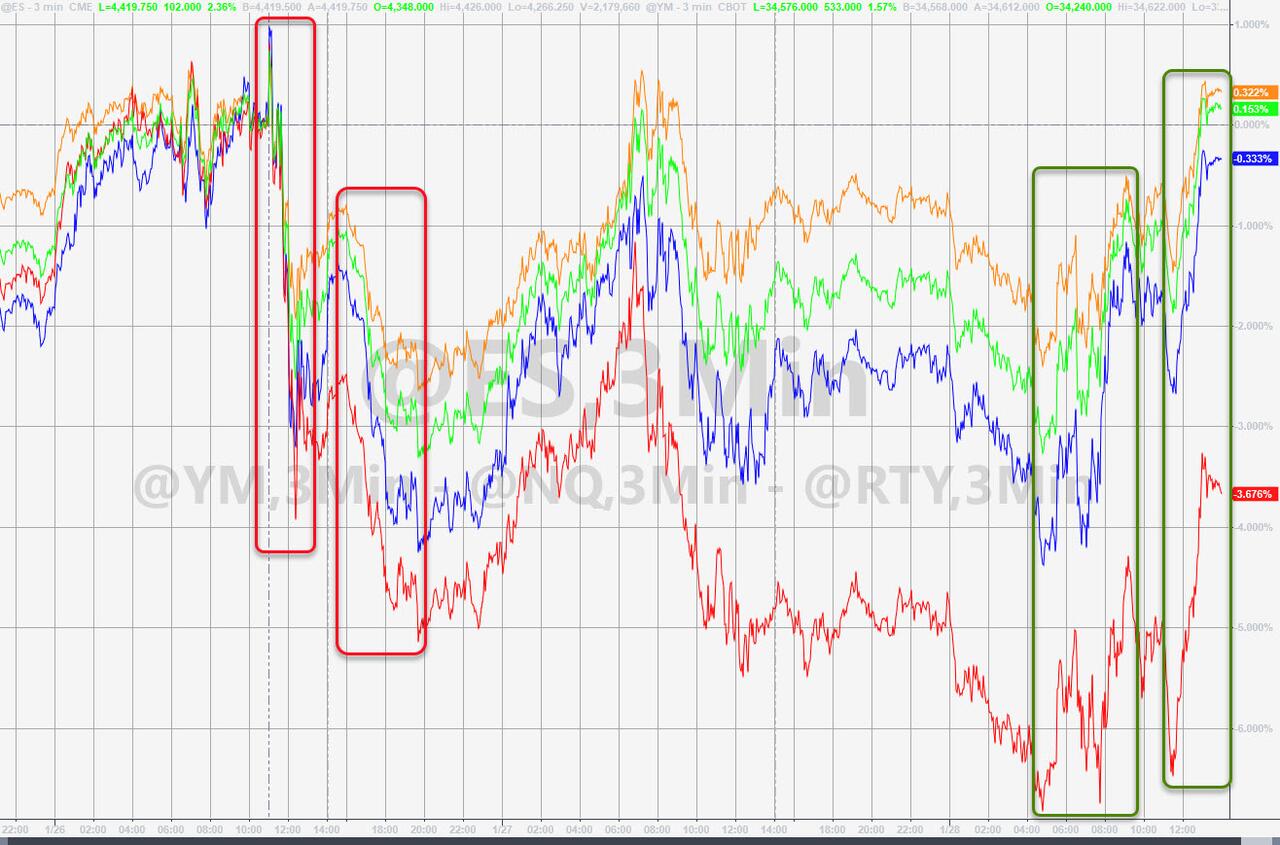

Markets Have Seen This Movie Before (Spoiler Alert: The Ending Is Horrible)

Authored by James Rickards via The Daily Reckoning,

As I expected, the Fed didn’t raise rates this week at its January FOMC meeting.

If you were thinking the Fed would have to begin raising rates to counteract inflation, you’re probably going to have to wait until March, when the Fed’s Open Market Committee meets again.

The Fed says it “will soon be appropriate” to raise rates. It also says it will end asset purchases in March, so all signs point to a March rate hike.

How did the stock market react to this week’s messaging from the Fed?

[ZH: The initial reaction was a puke across all major US equity markets… followed by the ubiquitous overnight ramp to erase the loss. Thursday saw more selling at the open which extended into the US cash open on Friday.]

{ZH: At which point, a buying panic ensued, lifting The Dow and S&P back into the green post-FOMC, Nasdaq down modestly, but Small Caps crushed.]

Yields on the all-important 10-year Treasury note spiked to 1.876% on Wednesday – a 10bps surge. That’s an earthquake in bond land. [ZH: But, by the end of the week, amid fears of policy errors, the 10=year yield had tumbled back to unchanged post-FOMC.]

Ten-year yields opened the year under 1.6%, and the increase has spooked the stock market.

The 10-year note yield is a good proxy for long-term investment in mortgages, construction and infrastructure projects and therefore reflects expectations about the real economy.

Until recently, the interim high yield on the 10-year note had been 1.745% on March 31, 2021. Rates fell through the summer of 2021 and then began rising again, but the rate spikes fell short of that 1.745% level and then fell back.

That pattern prevailed until Jan. 14, 2022, when rates broke through and hit 1.794%. That was the highest level since Jan. 13, 2020, almost exactly two years ago, and before the pandemic became widespread in the U.S.

At that time, rates had declined from their pre-pandemic interim high of 2.761% on Jan. 23, 2019, almost exactly three years ago. Again, today’s yield is 1.848%.

But if rates are not fundamentally higher than they were two years ago and are significantly lower than they were three years ago, what does that say?

If a wave of inflation is about to smash into us, why aren’t rates at 3.0% or higher? A yield of 1.876% is pretty puny if the inflation narrative is correct.

People throw the word “stimulus” around, even those who should know better, and say, “The Fed’s cut rates to zero. That’s stimulus. The Fed’s printing money. That’s stimulus.”

They then say, “If you’re going to print that much money, you’re going to get inflation.”

But none of that is true. It’s far too simplistic. Reality is much more complicated than the simple money printing equals inflation narrative. Yes, the money printing is true. But it’s not inflationary unless the money gets put to use in the economy.

If the money gets put to use in the form of widespread lending and spending, that’s a setup where you have to think hard about inflation. But that’s not what we’re seeing.

What happens then to the money the Fed creates?

The big banks have accounts at the Fed. They take the money and they leave it at the Fed in the form of excess reserves, meaning basically more reserves than the law requires them to have.

So the money doesn’t go anywhere. It’s not being invested. It’s not being loaned out. It’s not being borrowed. It’s not being spent. So it doesn’t matter how much there is if the money doesn’t go anywhere, and that’s exactly the situation we’re facing.

I often refer to the velocity of money. Quite simply, velocity is the turnover of money, the rate at which money changes hands.

The Fed can create money just by buying bonds with money it creates out of thin air. But velocity is a psychological phenomenon.

It all depends how consumers feel. If they feel prosperous, if they feel that their job is secure, if they feel that their businesses are doing well, they might be more willing to borrow money to expand the business or spend money on personal consumption.

But we’re not seeing that. We’re seeing velocity drop. Some people are getting money, whether it’s in the form of government handouts or slightly higher wages, but they’re saving it. They’re not spending it. That doesn’t add up to rampant inflation.

I realize I may be in the minority, but the bond market is telling us that inflation will be much tamer than expected (I expect inflation to return with a vengeance eventually, but not yet).

In other words, the U.S. may be seeing peak inflation and peak interest rates for this cycle.

I expect the U.S. economy will slow from here (for many reasons including the pandemic, supply chain disruptions and excess debt), rates will level off and then decline and the dollar will weaken.

Of course, the Fed is preparing to tighten monetary policy at a time when the economy shows weakening. It’s tightening into weakness. But that’s no surprise.

Looking at the entire history of the Fed since 1913, it’s proven that it’s really good at wrecking the economy by doing the wrong thing at the wrong time. And it’s in the process of doing that again.

I feel like we’re watching the same movie that we’ve already seen. We’re seeing this movie again because the Fed did this before. From 2008–2013, the Fed did what they did the last couple of years.

They bought bonds, created money supply, blew up the balance sheet and cut rates to zero. The zero interest rate policy, the money printing, they did that from 2008–2013. They took the Fed’s balance sheet from about $800 billion to about $4 trillion (today it’s dramatically higher because of its response to the pandemic).

Then they tried to “normalize.” They began raising rates aggressively. They got the fed funds rate up to 2.25%, with nine 25-basis-point increases between December 2015 and December 2018.

They trimmed the balance sheet down. Not greatly, but they brought it down from about $4.5 trillion to about $3.7 trillion. That’s not an insignificant reduction.

In other words, the Fed was trying to raise rates and reduce the balance sheet, and they were succeeding. But it all culminated on Dec. 24, 2018, in what I call the Christmas Eve Massacre.

The Fed sank the stock market. It fell 20% in 2½ months.

And that was after a long bull market from 2009–2018, when stocks tripled over that time period.

The lesson is that when the Fed tries to normalize, they can’t do it. They’re caught in a trap of their own creation, with no way out, or at least no easy way out without causing a lot of pain.

They’re about to make things worse with tightening into weakness, with tapering and with rate increases. The market already sees this coming because they’ve seen the movie before. They know how it ends.

And it ends poorly.

Tyler Durden

Mon, 01/31/2022 – 06:30

via ZeroHedge News https://ift.tt/7QJTnhPbz Tyler Durden

Three JP Morgan Formers Fired For Communicating On Personal Devices Have All Found New Jobs On Wall Street

Three executives that were ousted from J.P. Morgan for using their personal phones to communicate work information have landed new jobs in the industry. The news serves as a positive beacon for the rest of Wall Street, who were collectively nervous about an ongoing U.S. regulator probe into the practice.

Bloomberg called the phone rule “a rule that just about everyone seemed to be breaking”.

Despite J.P. Morgan paying $200 million in fines for the practice, Ben Sykes, an executive director who left last year wound up finding a new job at Jefferies. Earl Dowling, a former managing director landed at PJT Partners and Ed Koo, another JP Morgan executive that was ousted, is now a portfolio manager at Brean Asset Management, according to Bloomberg.

Sykes FINRA BrokerCheck record reads that he was “terminated for violating the firm’s communication policy by moving several internal business communications from a surveilled approved electronic communication channel to an unapproved electronic communication channel, and for the inappropriate content of certain communications.”

Koo’s says he “used a third-party social media application for internal business communications.”

Meanwhile, the Federal probe into the rule breaking has expanded “to examine whether more firms broke recordkeeping requirements designed to protect investors”, the report says. The investigation has already yielded managers who were supposed to help preventing texting outside of official channels, but instead engaged in the practice themselves.

Adam Pritchard, a law professor at the University of Michigan, commented: “These people were able to find alternative employment because presumably they have skills and are good at what they’re able to do.”

He continued: “JPMorgan probably had to fire some people to show that they were serious. So you can see how a subsequent employer would say, ‘Yeah, that’s a regulatory violation, but you weren’t stealing from your customers.’”

The SEC has also recently accused JP Morgan of failing to meet its obligation to archive written communications, which has been required since the 1930’s. It did not, however, accuse the investment bank of using unauthorized platforms to cheat clients or engage in wrongdoing.

The bank has since settled with the SEC and the Commodity Futures Trading Commission.

Tyler Durden

Mon, 01/31/2022 – 05:45

via ZeroHedge News https://ift.tt/dU7FHIAxa Tyler Durden

Farming Insider Warns The Coming Food Shortages Are Going To Be Far Worse Than We’re Being Told

Authored by Michael Snyder via TheMostImportantNews.com,

The information that I am about to share with you is extremely alarming, but I have always endeavored to never sugarcoat things for my readers. Right now, there are shortages of certain items in grocery stores across the United States, and food supplies have gotten very tight all over the globe. I have repeatedly warned that this is just the beginning, but I didn’t realize how dire things have already gotten until I received an email from a farming insider that I have corresponded with over the years. I asked him if I could publicly share some of the information that he was sharing with me, and he said that would be okay as long as I kept his name out of it.

According to this farming insider, dramatically increased costs for fertilizer will make it impossible for many farmers to profitably plant corn this year. The following is an excerpt from an email that he recently sent me…

“Things for 2022 are interesting (and scary). Input costs for things like fertilizer, liquid nitrogen and seeds are like triple and quadruple the old prices. It will not be profitable to plant this year. Let me repeat, the economics will NOT work. Our plan, is to drop about 700 acres of corn off and convert to soybeans (they use less fertilizer, and we also have chicken manure from that operation). Guess what? We are not the only ones with those plans. Already there is a shortage of soybean seeds, so we will see how that will work out. The way I see it, there will be a major grain shortage later in the year, especially with corn. I mean, we are small with that. What about these people in the midwest who have like 10,000 acres of corn? This will not be good.”

Once I received that message, I wrote him back with some questions that I had.

In response, he expanded on his comments in a subsequent email…

As for the farming, I see it getting bad. Things like fertilizer and liquid nitrogen have tripled and quadrupled in price. Yes commodity prices are up, but that certainly wont cover the new increased input costs. We are in NC, so while certainly not like the midwest, we still grow grain. The midwest of course will have these same higher input costs as well.

Corn for example, typically takes about 600 pounds of fertilizer per acre, plus 50 gallons of liquid nitrogen. Times that by many acres and thats a lot of money. Soybeans take much less. The plan for us, and most others around here, is to drastically cut corn acres and switch to soybeans. Problem is, there is apparently a soybean seed shortage because others have this plan as well. We were lucky enough to pre buy enough to do it. However, most people, especially younger farmers, or farmers where that is all they do, probably don’t have the money to front like that.

The way I see it, a corn shortage will come. I guess there could possibly be a glut of soybeans, but remember that could depend on the seed being available. I guess there are other alternatives, maybe milo, oats, or barley. Of course the corn market is much larger. Think animal feed and ethanol. I mean for animals, soybeans are used too, but its a mix. What happens to the animal producers who depend on reasonably priced corn? I just don’t see how it can end well. I mean, even if we end up with plenty of soybeans, even a glut, then you have a busted market for that. I don’t know. There just isnt much history to base any of this on. I just see it hurting both grain farmers, and animal farmers, and also translating to more shortages and price increases for consumers who buy the end products.

I was stunned when I first read that.

Corn is one of the foundational pillars of our food supply.

If you go to the grocery store and start reading through the ingredients of various products, you will quickly discover that corn is in just about everything in one form or another.

So what is our country going to look like if a severe corn shortage actually happens?

I don’t even want to think about that.

Of course fertilizer prices are not just going through the roof here in the United States.

In South America, high fertilizer prices are going to dramatically affect coffee production…

Christina Ribeiro do Valle, who comes from a long line of coffee growers in Brazil, is this year paying three times what she paid last year for the fertilizer she needs. Coupled with a recent drought that hit her crop hard, it means Ms. do Valle, 75, will produce a fraction of her Ribeiro do Valle brand of coffee, some of which is exported.

There is also a shortage of fertilizer. “This year, you pay, then put your name on a waiting list, and the supplier delivers it when he has it,” she said.

If you love to drink coffee in the morning, you will soon be paying much more for that privilege.

Over in Africa, fertilizer prices could result in “30 million metric tons less food produced”…

Fertilizer demand in sub-Saharan Africa could fall 30% in 2022, according to the International Fertilizer Development Center, a global nonprofit organization. That would translate to 30 million metric tons less food produced, which the center says is equivalent to the food needs of 100 million people.

“Lower fertilizer use will inevitably weigh on food production and quality, affecting food availability, rural incomes and the livelihoods of the poor,” said Josef Schmidhuber, deputy director of the United Nations Food and Agriculture Organization’s trade and markets division.

Where in the world are we going to get enough food to replace “the food needs of 100 million people”?

This is beyond serious.

Basically, the stage is being set for the sort of historic global crisis that I have been relentlessly warning about.

Many Americans had assumed that even if the rest of the world was suffering that we would be immune.

But now there are widespread shortages all over the nation, and the Wall Street Journal just published a major article entitled “U.S. Food Supply Is Under Pressure, From Plants To Store Shelves”.

This is really happening.

In Washington D.C., residents are being instructed to “just buy what you need and leave some for others”…

“If you’re hitting the grocery store to prepare for winter weather, please just buy what you need and leave some for others! You may have noticed empty shelves in some stores due to national supply chain issues, but there is no need to buy more than you normally would.”

What would have been unimaginable just a few years ago is now making headlines on a daily basis.

Of course it isn’t just our food supply that is under threat. As Victor Davis Hansen has aptly noted, our country is now in the process of undergoing a “systems collapse”…

In modern times, as in ancient Rome, several nations have suffered a “systems collapse.” The term describes the sudden inability of once-prosperous populations to continue with what had ensured the good life as they knew it.

Abruptly, the population cannot buy, or even find, once plentiful necessities. They feel their streets are unsafe. Laws go unenforced or are enforced inequitably. Every day things stop working. The government turns from reliable to capricious if not hostile.

A lot of people are going to be caught off guard by the pace of change.

Things are shifting so rapidly that it really is hard to keep up with it all unless you are paying very close attention.

Now that you have been exposed to the information in this article, please don’t go back to sleep.

This is not a drill.

We really are heading into a nightmare scenario, and I strongly urge you to act accordingly.

* * *

It is finally here! Michael’s new book entitled “7 Year Apocalypse” is now available in paperback and for the Kindle on Amazon.

Tyler Durden

Mon, 01/31/2022 – 05:00

via ZeroHedge News https://ift.tt/Ib8vesu4f Tyler Durden

Shane Lee Brown, then 23, spent six days in a Las Vegas jail in 2020 after cops arrested him on a warrant for Shane Neal Brown, then 49. In addition to the age difference, Shane Neal Brown is white and is taller than Shane Lee Brown, who is black. Shane Lee Brown is now suing the Las Vegas Metropolitan Police Department and the Henderson, Nevada, police department, which made his initial arrest, for civil rights violations, false imprisonment, negligence and other wrongful conduct.

The post Brickbat: A Mistake Anyone Could Make appeared first on Reason.com.

from Latest – Reason.com https://ift.tt/Nt9TXS12e

via IFTTT

Credit Suisse Hikes Cash Bonuses For Top Bankers After Disastrous 2021

For the last few weeks, the financial press has been replete with headlines about bankers getting generous raises. From JPM CEO Jamie Dimon – who was paid a new record annual sum close to $35 million – on down to the rest of the front office.

Well, just weeks after firing its chairman of just 8 months for daring to attend Wimbledon in defiance of the bank’s COVID rules (among other misgivings), the bankers at Credit Suisse are learning that they, too, will be treated to an even larger bonus than they might have anticipated, despite 2021 being one of the bank’s most disastrous years in recent memory.

According to Reuters, Credit Suisse is lifting cash payouts for senior bankers (MDs and up, it looks like). The bank reportedly broke the news to employees on Friday.

But after the year Credit Suisse just had, management is arguing that the bonuses are necessary to retain top earners. Otherwise, the bank would be in even bigger trouble.

For bankers who accept the increased pay, there’s a catch: they can only keep it if they stay with the firm for three years.

“For Managing Directors and Directors, this change is intended to rebalance the amount of immediate cash that is paid compared to prior years,” executive managers told employees in the internal memo confirmed by the company.

Shares of the bank lost more than 25% of their value last year. As a result, bankers will be getting an even larger cash helping and a smaller potion of their comp in short-term equity incentives that vest after a year.

Banker pay rose across the industry in 2021 amid a boom in M&A activity thanks in large part to the SPAC bonanaza.

Starting early in the year, Credit Suisse brooked billions in losses in 2021 from its prime brokerage business thanks to the collapse of Archegos, as well as its asset management business, where the collapse of Australian “supply chain finance” firm Greensill led CS to freeze $10 billion in client funds which essentially became worthless.

Given all this, it’s hardly surprising that Credit Suisse chose to emphasize “accountability and responsibility” in a statement about the bonuses.

With its new incentives scheme, Credit Suisse told employees it aimed to reinforce a culture “based on personal accountability and responsibility” that would better align compensation with “positive behaviors”.

“With regards to executive compensation, Credit Suisse aims to strike an appropriate balance with the interests of shareholders and wider stakeholders,” the bank said in a statement. “We have also said that we will further align remuneration with our new strategic objectives, including our renewed focus on risk management.”

Meanwhile, the bank warned shareholders on Tuesday to expect a loss in Q4 dues to mounting legal costs and lower revenues in its trading and wealth management businesses.

Tyler Durden

Mon, 01/31/2022 – 04:15

via ZeroHedge News https://ift.tt/p0lrCcDIT Tyler Durden

Shane Lee Brown, then 23, spent six days in a Las Vegas jail in 2020 after cops arrested him on a warrant for Shane Neal Brown, then 49. In addition to the age difference, Shane Neal Brown is white and is taller than Shane Lee Brown, who is black. Shane Lee Brown is now suing the Las Vegas Metropolitan Police Department and the Henderson, Nevada, police department, which made his initial arrest, for civil rights violations, false imprisonment, negligence and other wrongful conduct.

The post Brickbat: A Mistake Anyone Could Make appeared first on Reason.com.

from Latest – Reason.com https://ift.tt/Nt9TXS12e

via IFTTT

The Battle For Europe Integration Has Failed And Russia Provides Proof

Authored by Mike Shedlock via MishTalk.com,

It’s time to concede European integration failed. What are the consequences?

Eurointelligence founder Wolfgang Münchau is a strong pro-Europe advocate. He has been that way for the entire decade I followed him.

Earlier this month he commented: “The battle for European integration has failed. It is time to recognise defeat, and to think through the consequences.“

Please consider Münchau’s thought-provoking article When Did We Lose the Fight? Emphasis below is mine.

When you fight for a cause that does not materialise, at what point do you recognise, and admit, defeat? There are some causes you may want to keep fighting for no matter what, like human rights or climate change. Is European integration in that category? For me, it is not. My biggest area of disagreement with my fellow European federalists is not in what we think is desirable. What we disagree on is where the dividing line between realpolitik and wishful thinking lies.

A good example occurred this weekend. The fool whose committed the crime of saying what everybody in the SPD is thinking was Kay-Achim Schönbach. He was forced to resign as head of the German Navy for revealing to the world that Germany’s natural ally is Russia.

Germany also plays a non-cooperative game in the EU’s monetary union, through an economic model that is reliant on large savings surpluses. Whether the issue is economic or foreign policy, other member states have been reluctant to challenge Germany.

The euro area’s sovereign debt crisis deprived me of my last great European illusion, the notion that crises make us stronger. That particular crisis made us weaker. So has the pandemic. I see no trajectory whatsoever for Italy to generate the degree of productivity growth needed to render its foreign debt sustainable. The only way to avoid disaster is for the ECB to support Italian debt forever. It might do so. But that would set the ECB on a toxic path, leading to a wide selection of other horrible destinations. Then again, the euro area would probably not survive an Italian debt default intact either. Pick your poison.

My scepticism is not impatience, but concern that opportunities have been lost forever. Take ECB asset purchases. There was a short window for a genuine eurobond between 2008 and 2015, when the ECB’s programme of quantitative easing started. Afterwards, the ECB bought national sovereign debt in the trillions, and turned them into euros. This is what QE does: it swaps debt for money. Money is a liability similar to bonds, except that the maturity is shorter.

The idea behind a real eurobond could not be more different. It would not have been about the monetisation of national debt. A real eurobond would have been a debt instrument of a federal fiscal union with limited tax raising powers.

If only. I have come to the conclusion that this ship has sailed. Once you realise this, the consequences are far-reaching. If a proper economic union constitutes the first-best option, it is does not follow logically that a dysfunctional economic union is the second best.

But if you don’t, you have to ask yourself some rather troubling questions. This is where I am at. One of the questions is this: even if the European solution is optimal, is it possible that the national alternative is superior to a malfunctioning hybrid?

I disagree with Münchau that there ever was a chance for a united Europe.

The euro itself is fatally flawed. There is no way for a single interest rate to work for Italy, Germany, France, Spain and Greece with monstrously different work ethics, hours pension plans, productivity, etc.

There is no way to change the rules.

When the Eurozone was formed, Germany insisted on rules that could not be changed without unanimous consent of all countries and without consent of the German constitution.

Over the years Germany bent in minor ways, but did not break on some constitutional debt rules.

But point two still remains. It take unanimous consent to do nearly anything in the EU or Eurozone that was not explicitly spelled out in the Maastricht Treaty that created the EU.

This is why it took a nearly a decade for the EU to work out a simple trade agreement with Canada.

Germany will never give up on debt brakes and France will never give up on Agricultural policy. The latter has stymied every global global trade agreement for at least two decades.

Russia is and has been Germany’s natural ally. Note that Germany even blocked sending military aid to Lithuania and Ukraine.

Former Chancellor Angela Merkel, bowed to the Greens and dismantled German nuclear reactors.

Now Germany is in desperate need of Russian natural gas.

Germany will not stand up to China, once again over trade issues.

The US has still not figured out Germany is a weak ally at best. The EU has not figured out that Germany has no intention of ever changing its trade stance.

But everyone does understand that France will never change its agricultural policy.

The UK did good to exit the EU mess via Brexit even if they have so far mishandled many steps along the way.

Münchau asks the right question: “Even if the European solution is optimal, is it possible that the national alternative is superior to a malfunctioning hybrid?“

* * *

Tyler Durden

Mon, 01/31/2022 – 03:30

via ZeroHedge News https://ift.tt/ty5hoYiZ4 Tyler Durden