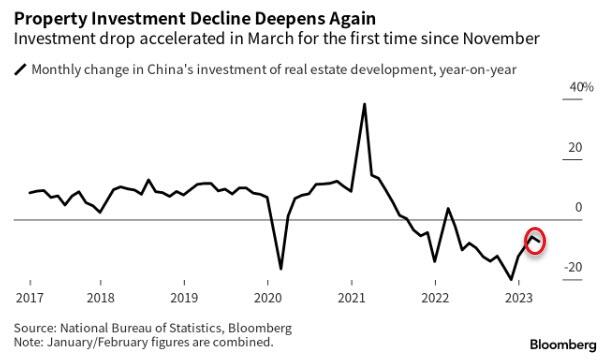

US Futures extended yesterday’s rally after the Senate passed a bill late on Thursday to raise the debt ceiling and prevent a US default, with risk-on sentiment getting a boost following the sharpest rally in Chinese stocks for three months amid Bloomberg reports that China is mulling a new stimulus package to support the property market after existing policies failed to sustain a rebound in the ailing sector.

At 7:45am, S&P futures rose 0.5% to 4249, while the Nasdaq rose by 0.6% and was set for a sixth straight weekly advance. Europe’s Stoxx Europe 600 index followed Asian benchmarks higher, with luxury-goods makers LVMH and Richemont among the leading gainers after the China stimulus report. Treasury yields were little changed, diverging from higher rates in Europe and the UK. Oil and bitcoin both gained more than 1%, while gold was little changed after three days of gains.

In premarket trading, US-listed Chinese stocks extended a rally after Bloomberg News reported that regulators are considering a new basket of measures to boost the property market. Broadcom shares fell as the chipmaker remains mired in a broader slowdown. While the company talked up the potential boost from artificial intelligence, it wasn’t enough to sustain recent gains for the stock, which jumped nearly 30% last month. Dell Technologies also fell after the personal-computer maker gave a lukewarm sales outlook indicating that a recovery may take a bit longer than expected as it continues to struggle to sell PCs, particularly to consumers. Here are some other notable premarket movers:

- Lululemon shares surged after the athletic- apparel brand reported first-quarter net revenue that beat estimates. Analysts say the results were better than feared, highlighting the brand’s strong guest metrics as well as growth in China.

- MongoDB shares soared, with analysts positive on the database software company after it reported first-quarter results that beat expectations and raised its full-year forecast. Citi says the outlook “could signal a faster recovery in the consumption trends of the business, potentially driven by GenAI tailwinds.”

- SentinelOne shares slumped after the software company cut its year revenue guidance. “Macroeconomic pressures continue to impact deal sizes, sales cycles, and pipeline conversion rates,” the company wrote in a letter to shareholders.

Tech giants are still driving most of the stock market’s advance, with Apple nearing a record and Nvidia. climbing more than 5% Thursday; both were set for more gains today. The sector attracted record inflows last week, Bank of America said. Aside from the obsession for anything AI-related that drove megacaps up 17% in May, the industry also got a boost from wagers the Fed will stop raising interest rates.

Late on Thursday, the Senate voted 63-36 to pass the US debt ceiling bill, which sends it to President Biden’s desk. Biden said he wants to thank Senate leaders Schumer and McConnell for quickly passing the debt ceiling bill and noted that the bipartisan agreement is a big win for the economy, while he looks forward to signing the bill ASAP and directly addressing Americans on Friday. The White House announced that President Biden is to deliver an address on averting a default and the bipartisan budget agreement according to Reuters.

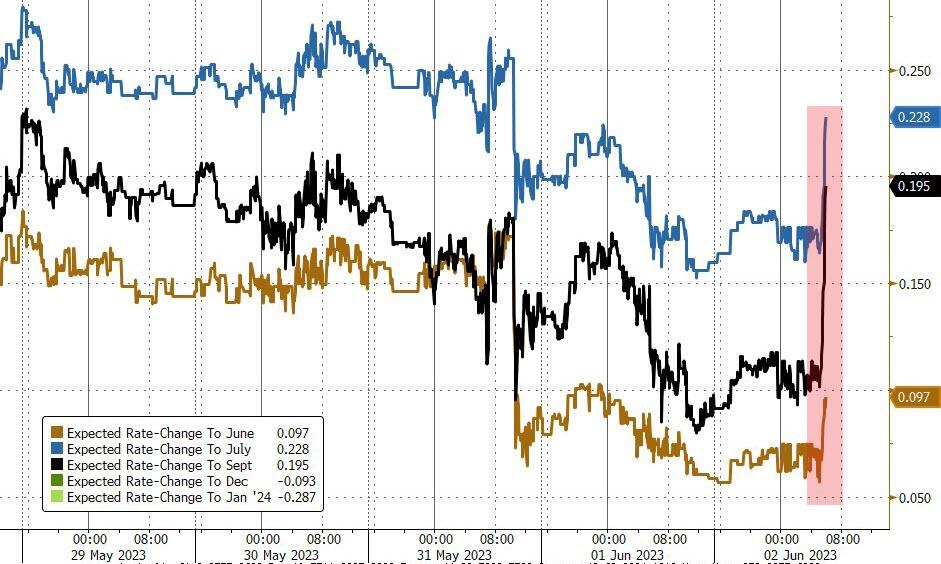

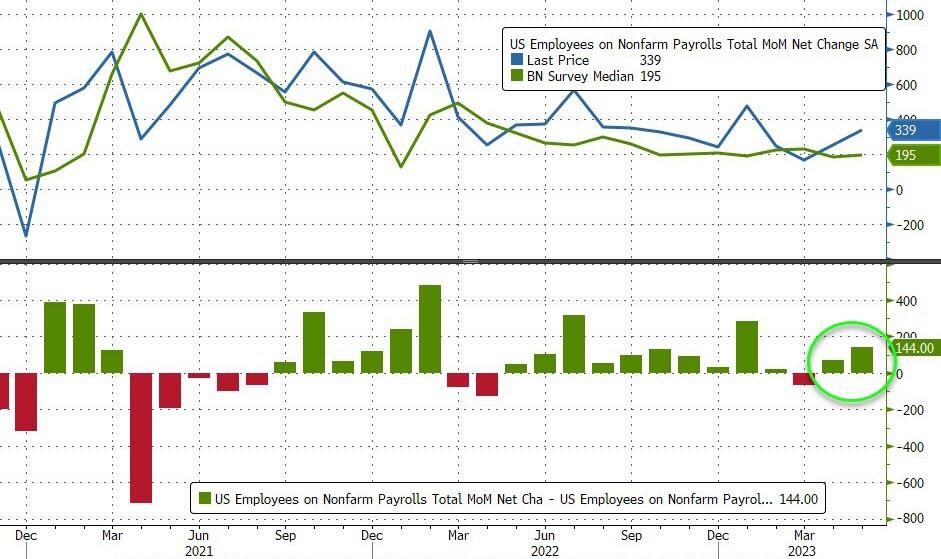

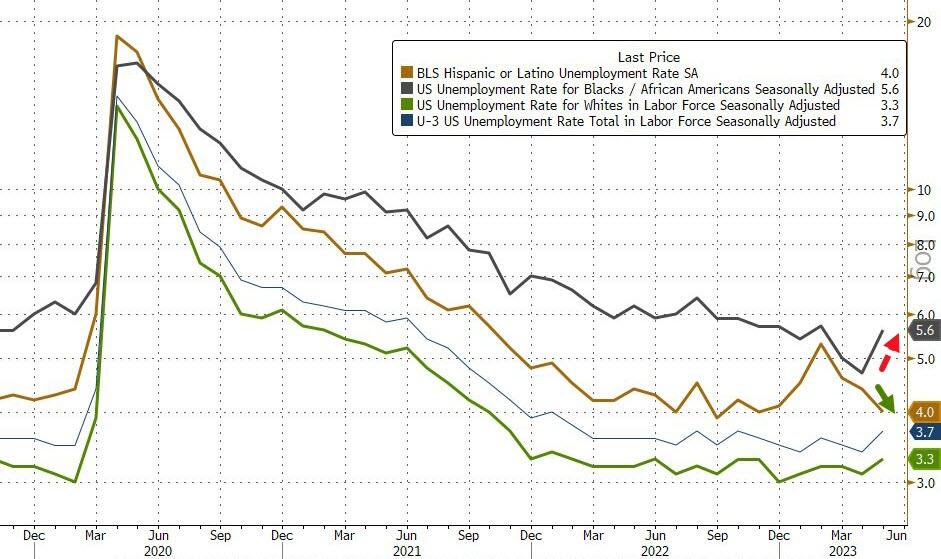

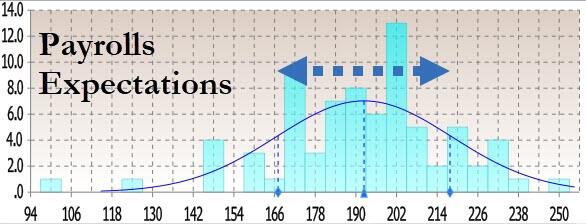

Today, all eyes will be on the NFP print at 8:30am (see our preview here). Consensus expects NFP to print 195k with the whisper number higher at 225k (vs. 253k prior) and the Unemp rate to rise to 3.5%, vs. 3.4% prior; focus also on average hourly earnings data which is expected to rise 0.3% MoM. Traders are betting that the jobs report will show enough moderation in the pace of hiring to allow the Fed to pause its tightening cycle, helping sustain the rally. Dovish comments from Fed officials supported this view: Fed Bank of Philadelphia President Patrick Harker said “we should at least skip this meeting in terms of an increase,” and his St. Louis counterpart James Bullard said interest rates may already be sufficiently restrictive to bring down inflation.

“The more pertinent Fed speakers have suggested a June pause is more likely and I don’t think non-farms payrolls should change that view meaningfully,” said James Athey, investment director at Abrdn. “Therefore I think the risks are skewed to a dovish disappointment this afternoon.”

According to Goldman trading desk, a print sub 100k likely hits the tape by ~100bps and a print north of 375k hits the tape by 25 – 50bps.

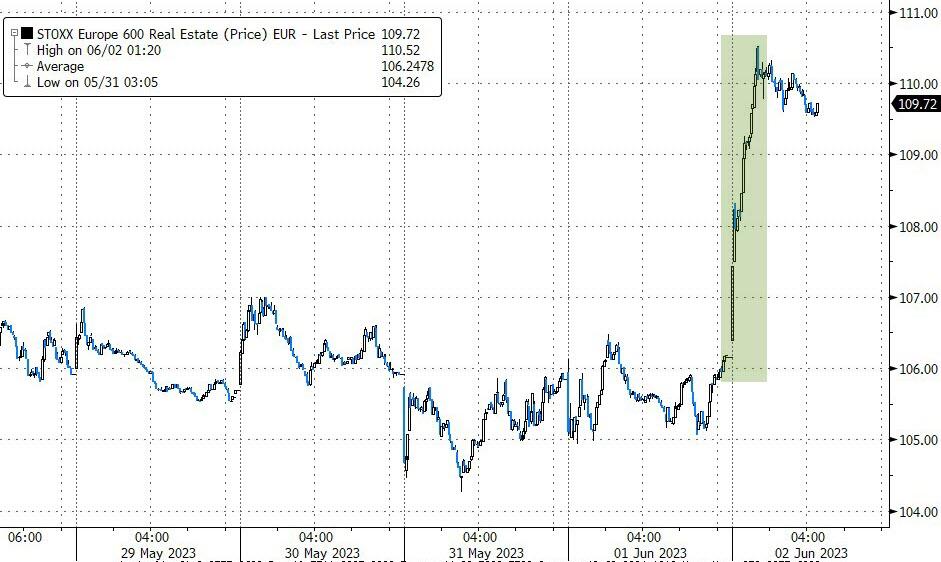

In Europe, the Stoxx Europe 600 index was up 1% and on course for back-to-back gains for the first time in two weeks, following Asian benchmarks higher, with luxury-goods makers LVMH and Richemont among the leading gainers after Bloomberg reported that China is considering new stimulus measures. Miners and energy companies climbed as crude oil and industrial metals rebounded. Among individual movers in Europe, sportswear makers Puma SE and Adidas AG rose more than 4% each after Lululemon Athletica Inc.’s robust results. Dechra Pharmaceuticals Plc jumped after EQT AB made a firm offer for the UK veterinary drugmaker. Embattled Swedish landlord SBB soared as it attracted interest from investors including Brookfield Asset Management. Here are some other notable movers.

- Addnode shares gain as much as 11% after the Swedish IT services group announced it would acquire US firm Team D3 for up to $59m. Handelsbanken says the price tag looks “almost worryingly attractive”

- Diageo shares underperformed its peers Friday, with analysts seeing the UK alcoholic beverage maker’s capital markets day as failing to dispel uncertainty about its outlook, with Citi noting a lack of clarity

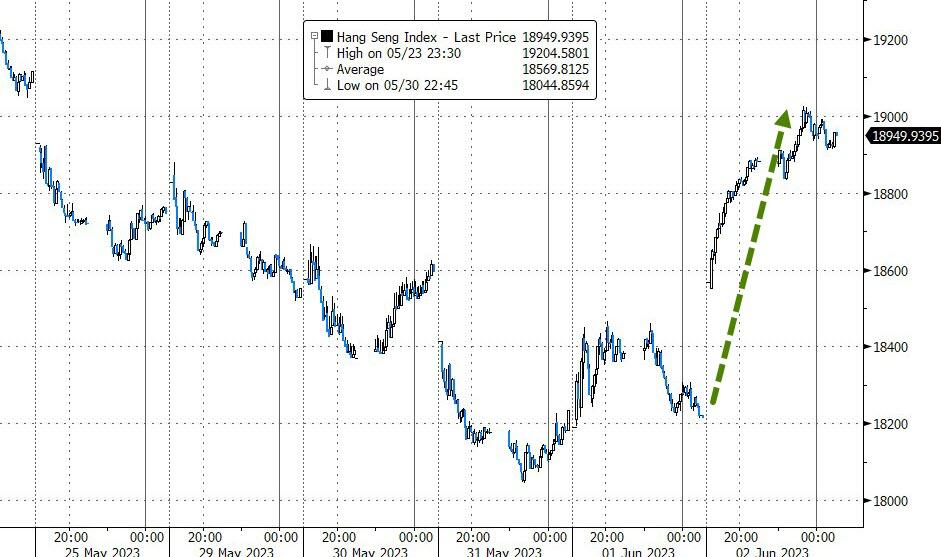

The MSCI Asia-Pacific Index jumped as much as 2.1% Friday, poised for its biggest weekly advance since late January as Chinese tech stocks fuel big gains in Hong Kong benchmarks. Biggest contributors to gauge’s climb are Tencent and Alibaba, which jump more than 5% each. Hang Seng Tech Index spikes as much as 5.7%; other Hang Seng benchmarks rally at least 4% Shares in Japan, Australia, China advanced while South Korea’s Kospi index was headed for bull market territory following a gain of more than 20% from a low in September. Hong Kong’s Hang Seng index rose more than 3%, pulling the benchmark back from the brink of a bear market following concerns about Chinese growth.

The bullish sentiment emerged amid reports that China is working on a new basket of measures to support the property market after existing policies failed to sustain a rebound in the ailing sector, Bloomberg reported Friday. The yuan extended gains and crude oil rose along with industrial metals. An index of emerging-market stocks soared the most since January.

In FX, the Bloomberg Dollar Spot Index eased for a second day as traders are betting that the monthly US jobs report will show enough moderation in the pace of hiring to allow the Fed to pause its tightening cycle. Money markets now assign a three-in- four chance of a 25 basis-point hike next month. Supporting that view, Fed Bank of Philadelphia President Patrick Harker said “we should at least skip this meeting in terms of an increase,” and his St. Louis counterpart James Bullard said interest rates may already be sufficiently restrictive to bring down inflation. Dollar weakness also gained traction after a report that China is working on a new basket of measures to support its property market.

- TheAussie rose as much as 1% against the dollar after industrial relations umpire boosted the national minimum wage by 5.75%, a decision that increased the chances of an interest-rate increase as soon as next week

- Short-covering against the yen topped out around 139.00 option strikes, according to traders

- The pound was up 0.1% to $1.2533, set for a sixth day of gains for the first time since December; currency is up 1.5% this week, the biggest advance this year

In rates, treasuries were slightly cheaper across the curve as S&P 500 futures gain; Treasury yields cheaper by 0.5bp to 2bp across the curve with 2s10s, 5s30s spreads steeper by 1bp and 0.5bp as front-end slightly outperforms; 10-year yields around 3.61% with bunds, gilts cheaper by 3bp and 1bp in the sector. US session focus switches to data, with the May jobs report scheduled for 8:30am New York.

In commodities, crude futures advance with WTI rising 1.9% to trade near $71.45. Spot gold is little changed around $1,980. Bitcoin rises 1%

Looking to the day ahead now, and the main highlight will be the US jobs report for May. Otherwise, data releases include French industrial production for April. And from central banks, we’ll hear from the ECB’s Vasle.

Market Snapshot

- S&P 500 futures up 0.4% to 4,244.25

- MXAP up 2.0% to 162.70

- MXAPJ up 2.2% to 513.59

- Nikkei up 1.2% to 31,524.22

- Topix up 1.6% to 2,182.70

- Hang Seng Index up 4.0% to 18,949.94

- Shanghai Composite up 0.8% to 3,230.07

- Sensex up 0.4% to 62,663.00

- Australia S&P/ASX 200 up 0.5% to 7,145.14

- Kospi up 1.3% to 2,601.36

- STOXX Europe 600 up 0.7% to 458.52

- German 10Y yield little changed at 2.28%

- Euro little changed at $1.0771

- Brent Futures up 0.7% to $74.80/bbl

- Gold spot down 0.0% to $1,977.49

- U.S. Dollar Index down 0.10% to 103.46

Top Overnight News

- China is working on a new basket of measures to support the property market after existing policies failed to sustain a rebound in the ailing sector, according to people familiar with the matter. BBG

- South Korea’s CPI cools to 19-month low, coming in at +3.3% Y/Y in May (down from +3.7% in April and below the Street’s +3.4% forecast). RTRS

- Australia’s industrial relations umpire raised the national minimum wage by 5.75% in an effort to support low-paid workers, a decision that boosted the chances of an interest-rate increase as soon as next week. BBG

- The UN food price index for May fell 2.6% M/M and is now off 22.1% from the all-time high hit in March of 2022. UN

- The Senate passed wide-ranging legislation Thursday that suspends the $31.4 trillion debt ceiling while cutting federal spending, backing a bipartisan deal struck by President Biden and House Speaker Kevin McCarthy to avert an unprecedented U.S. default. WSJ

- Consensus for payrolls this AM is +195k headline print (vs +253k prior, GIR +175k), AHE MoM .3% (vs .5% prior, GIR +.25%) & U/E 3.5% (vs 3.4% prior, GIR 3.4%). We are finally back in a good employment data is good for stocks set up with goldilocks zone for headline print at +175k to +250k (anything in here should keep today’s rally going). A print sub 100k likely hits the tape by ~100bps and a print north of 375k hits the tape by 25 – 50bps. GS GBM

- The buzz around AI has investors pouring a record amount of money into tech stocks, with the Nasdaq 100 Index now at an all-time high relative to the Russell 2000 small-cap index. A “baby bubble” in AI was the dominant market theme in May, with tech funds attracting a high of $8.5 billion in the week through May 31, he said, citing EPFR Global data. BBG

- Brookfield is said to be among investors in early stage talks to evaluate SBB’s real estate portfolio (European real estate rallying sharply in sympathy). RTRS

- Broadcom said sales tied to AI will double this year but will be overshadowed by a wider slowdown. Chip revenue from companies building out their AI capabilities may grow to $1 billion per quarter. Broadcom’s total revenue is expected to rise less than 5% this quarter, its slowest in years. The shares dipped. BBG

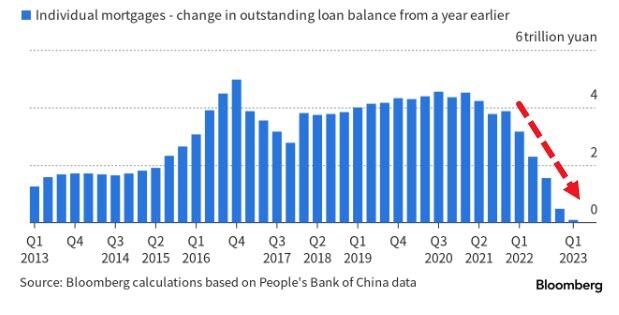

- The average rate on the standard 30-year fixed mortgage rose to 6.79%, according to a survey of lenders released Thursday by mortgage-finance giant Freddie Mac. That is the highest level since this past fall, when mortgage rates briefly topped 7% for the first time in two decades. The near-quarter percentage point increase from a week ago was the largest jump since October. Mortgage rates remain sharply above their roughly 5% level a year ago. That and elevated home prices have kept many potential home buyers on the sidelines. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher as the region took impetus from Wall St where the S&P 500 and Nasdaq climbed to 9-month highs amid debt ceiling optimism, falling labour costs and dovish Fed commentary. ASX 200 was positive with the index led higher by the mining sector and after the Australian Fair Work Commission raised the minimum wage by 5.75%, although gains were capped by weakness in financials and after recent upward revisions to banks’ forecasts on the RBA’s peak rate. Nikkei 225 was underpinned amid comments from BoJ Governor Ueda who stuck to the dovish script, with SoftBank among the biggest gainers following a buy rating from Jefferies and as the Co. benefits from the recent AI tech bid in the build-up to the ARM IPO. Hang Seng and Shanghai Comp. conformed to the broad upbeat mood with Hong Kong significantly outperforming amid a rally in property and tech.

Top Asian News

- China is reportedly mulling a property-market support package to bolster the economy, according to Bloomberg sources. Regulators are said to be considering reducing the down payment in some non-core neighbourhoods of major cities, alongside lowering agent commissions on transactions, and further relaxing restrictions for residential purchases under the guidance of the State Council, according to sources. China is working on a new basket of measures to support the property market after existing policies failed to sustain a rebound.

- US President Biden said the US does not seek conflict in competition with China and the countries should work together where they can.

- BoJ Governor Ueda said premature tightening could hurt companies even in good health and may weaken the economy’s potential, while he said patiently maintaining easy policy would heighten Japan’s potential growth in the long run. Ueda also stated it is not time yet to debate a specific exit strategy including the possible sale of the BoJ’s holdings of J-REITs and the BoJ will maintain massive monetary easing as it will take more time to achieve the price target, according to Reuters.

Top European News

- European equities trade on the front foot following the Senate passage of the debt ceiling bill. Despite the positivity during today’s session, the negativity earlier in the week means that the Stoxx 600 is on track to close the week out with losses of around 0.8%.

- Equity sectors in Europe are higher across the board (ex-healthcare) with Real Estate names top of the leaderboard followed by Basic Resources and Consumer Products & Services. Luxury names also benefit from gains in the sector overnight.

- US equity futures see gains but to a lesser magnitude compared to European peers ahead of the US jobs report.

Debt Ceiling news

- US Senate voted 63-36 to pass the US debt ceiling bill, which sends it to President Biden’s desk.

- US President Biden said he wants to thank Senate leaders Schumer and McConnell for quickly passing the debt ceiling bill and noted that the bipartisan agreement is a big win for the economy, while he looks forward to signing the bill ASAP and directly addressing Americans on Friday. Furthermore, the White House announced that President Biden is to deliver an address on averting a default and the bipartisan budget agreement at 19:00EDT/00:00BST, according to Reuters.

FX

- DXY oscillates in a tight range on either side of 103.50 ahead of the US jobs report, whilst the debt ceiling bill makes its way to President Biden after passing through the Senate.

- Yuan is firmer on reports China is reportedly mulling a property-market support package to bolster the economy as existing policies failed to sustain a rebound.

- Yen saw its revival thwarted by firmer US Treasury yields whilst also taking on board more dovish comments from the BoJ governor,

- Euro and Sterling are flat against the Dollar around 1.0770 and 1.2530 respectively in a quiet morning.

- Aussie outperforms amid a rebound in base metal prices ahead of the RBA policy announcement next week.

- PBoC set USD/CNY mid-point at 7.0939 vs exp. 7.0958 (prev. 7.0965)

Fixed Income

- Debt futures are observing caution in the run-up to NFP that crowns a holiday-shortened week.

- Bunds are losing further traction from 136.00 following an opening 136.36 Eurex print.

- Gilts trades around 97.00 and T-note is closer to 114-19+ overnight trough than 114-24+ peak

Commodities

- WTI and Brent front-month futures are on a firmer footing as the complex holds onto yesterday’s data-driven upside with further tailwinds seen following reports China is looking to further boost its property sector.

- Spot gold is flat around the USD 1,975/oz mark after meeting resistance at its 21 DMA (1,983.77/oz) overnight, with eyes on the US jobs report.

- Base metals are firmer across the board, bolstered by the risk appetite coupled with stimulus hopes from China.

Geopolitics

- South Korea and the US issued a joint cybersecurity advisory against North Korean hacking group Kimsuky and stated that North Korea is engineering cyberattack campaigns targeting think tanks, academia and news outlets, while South Korea issued new independent sanctions on the North Korean hacking group, according to the South Korean Foreign Ministry cited by Reuters.

- North Korea denounced the US Secretary-General over condemning its satellite launch and said it will continue to exercise its sovereign rights including the military spy satellite launch, according to KCNA.

- UN spokesman is concerned about the continuous slowdown in implementing the Black Sea grain initiative and noted that a slowdown was observed particularly in April and May.

- White House National Security Adviser Sullivan hosted Israel’s National Security Advisor and Minister of Strategic Affairs, while the officials continued discussions on enhanced coordination to prevent Iran from acquiring a nuclear weapon, according to Reuters.

- Chinese Eurasian Affairs Envoy said ‘fruitful’ talks on Ukraine may be difficult, according to Reuters.

US Event Calendar

- 08:30: May Change in Nonfarm Payrolls, est. 195,000, prior 253,000

- 08:30: May Change in Private Payrolls, est. 165,000, prior 230,000

- 08:30: May Change in Manufact. Payrolls, est. 5,000, prior 11,000

- 08:30: May Unemployment Rate, est. 3.5%, prior 3.4%

- 08:30: May Labor Force Participation Rate, est. 62.6%, prior 62.6%

- 08:30: May Average Weekly Hours All Emplo, est. 34.4, prior 34.4

- 08:30: May Average Hourly Earnings YoY, est. 4.4%, prior 4.4%

- 08:30: May Average Hourly Earnings MoM, est. 0.3%, prior 0.5%

DB’s Jim Reid concludes the overnight wrap

Markets recovered their poise over the last 24 hours, with the S&P 500 (+0.99%) closing at a 9-month high. That’s been driven by several factors, including the passage of the debt ceiling deal through Congress, the prospect that the Fed might finally pause their rate hikes at the next meeting, along with further signs that inflation is still falling. All this meant that June kicked off with a decent cross-asset rally, and sovereign bonds and commodities also moved higher after a fairly rough performance back in May.

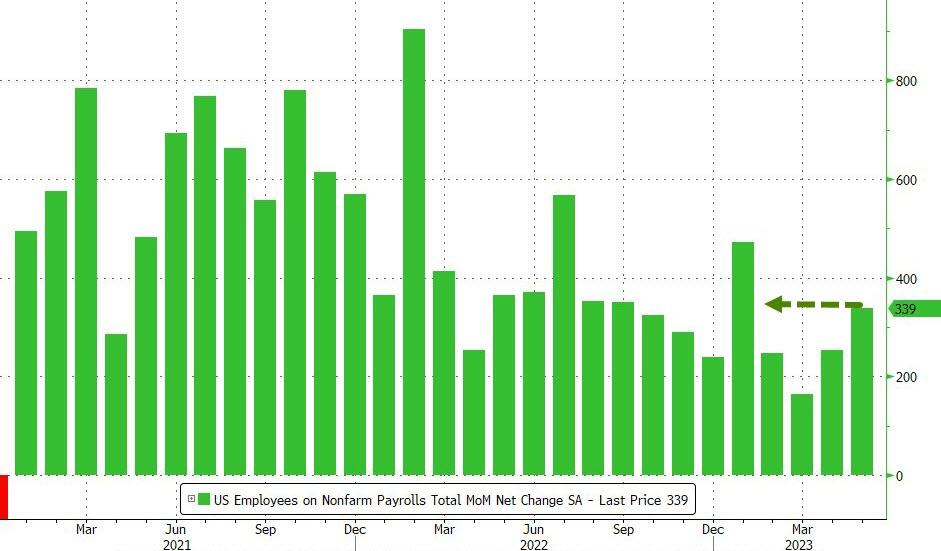

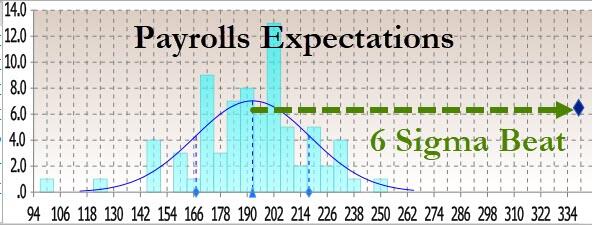

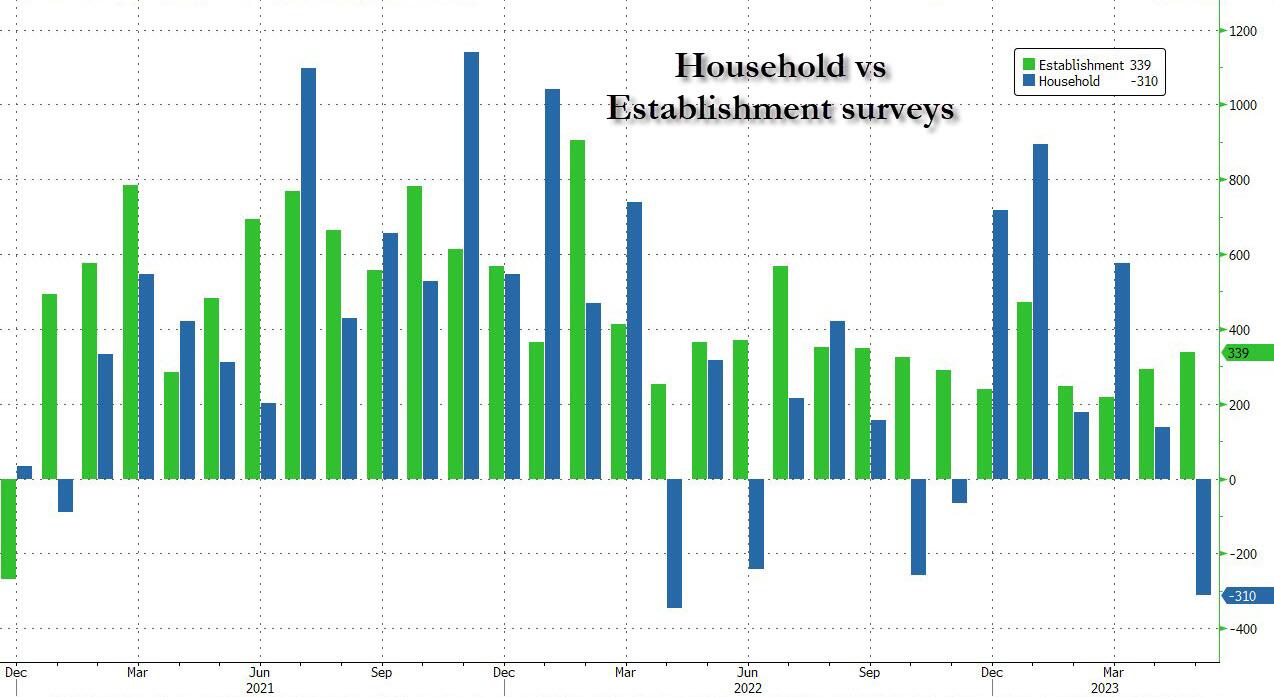

The next test for markets will come with today’s US jobs report, which is one of the last big data releases ahead of the Fed’s next decision on June 14. For what it’s worth, markets have been consistently taken by surprise by the jobs report over recent months, and the last 13 in a row have all seen the initial release for nonfarm payrolls beat the Bloomberg consensus forecast on the day. In terms of what to expect, our US economists are looking for a +200k increase in payrolls (vs. +195k consensus), so slightly above consensus once again. In turn, that would see the unemployment rate tick up a tenth to 3.5%, having come in at a 53-year low of 3.39% last month if you look to two decimal places. See more from our US economists here.

Ahead of that jobs report, yesterday brought a collection of robust data releases on the US labour market. First, the ADP’s report of private payrolls rose by +278k in May (vs. +170k expected), which was above every economist’s forecast on Bloomberg. Second, the weekly initial jobless claims came in at 232k over the week ending May 27 (vs. 235k expected), which took the 4-week moving average down to an 11-week low of 229.5k. And third, although the latest ISM manufacturing reading remained in contractionary territory at 46.9 (vs. 47.0 expected), the employment component ticked up to a 9-month high of 51.4. This good news wasn’t just confined to the US either, since the Euro Area unemployment rate fell to its lowest since the formation of the single currency in April, at 6.5%.

Alongside those positive signals on the labour market, markets also received some good news on inflation too. In the Euro Area, the flash CPI estimate for May fell to a 15-month low of +6.1% (vs. +6.3% expected), and core inflation was down for a second month running to +5.3% (vs. +5.5% expected). And in the US, the prices paid component of the manufacturing ISM was far beneath expectations at 44.2 (vs. 52.3 expected).

Markets then got some further momentum by fresh support for the Fed pausing their cycle of rate hikes at the next meeting. That came from Philadelphia Fed President Harker, who said that “we should at least skip this (June) meeting in terms of an increase” and that “we are close to the point where we can hold rates in place”. As a result, investors further dialled back the chances of a June rate hike, which were down to 23% by yesterday’s close, having been as high as 69% at the close last Friday. We did hear from St Louis Fed President Bullard as well, one of the hawks on the committee, who published an updated analysis suggesting that policy rates are “now at the low end of what is arguably sufficiently restrictive”.

Those various good news stories lay the foundation for a decent rally, with US Treasuries rallying as investors became less concerned that the Fed would continue to hike aggressively. Yields on 10yr Treasuries were down -4.8bps to 3.595%, and the movement was driven by real yields which fell -4.9bps on the day. For Europe there was also a decline in yields, with those on 10yr bunds (-3.3bps), OATs (-3.8bps) and BTPs (-7.0bps) all moving lower. But that was driven by inflation expectations, particularly since natural gas prices hit a 2-year low yesterday at just €23.10/MWh, which builds on their astonishing run of declines since the turn of the year.

This backdrop proved very positive for equities too, and the S&P 500 (+0.99%) hit a 9-month high. Indeed, the index is just shy of being up +10% on a YTD basis, which is remarkable when you consider that the equal-weighted S&P is still down -0.68% since the start of the year, so this is still an incredibly narrow rally. Once again, tech stocks were a big driver, and the NASDAQ advanced +1.28% to now be up more than +25% YTD, whilst the FANG+ Index (+2.03%) is now up more than +64% YTD. And over in Europe, the STOXX 600 (+0.78%) recovered from its 2-month low the previous day, with larger gains for the DAX (+1.21%) and the FTSE MIB (+2.01%).

The optimistic mood has continued overnight, partly thanks to the news that the US Senate had passed the debt ceiling deal in a 63-36 vote, which follows the vote in the House of Representatives the previous day. The bill will now be sent for President Biden’s signature, who said in a statement that “I look forward to signing this bill into law as soon as possible”. So that takes the threat of a near-term default off the table again, and Biden is expected to speak from the Oval Office at 7pm Eastern Time.

In light of the various good news stories, Asian equities have seen strong gains overnight, with advances for the Hang Seng (+3.66%), the Nikkei (+1.39%), the CSI 300 (+1.29%), the KOSPI (+1.03%), and the Shanghai Comp (+0.76%). The advance is also evident among US equity futures, with those on the S&P 500 up +0.18% overnight, following the index reaching a 9-month high the previous day. The risk-on moves have also seen Treasuries pare back their gains, with the 10yr yield up +1.9bps overnight to 3.61%, whilst Brent Crude oil prices (+0.58%) are up to $74.41/bbl.

In other news yesterday, we got the accounts of the ECB’s May meeting, which highlighted the ECB’s hawkish bias. On core inflation “the latest developments were broadly seen as worrisome”, and “members concurred that further tightening was needed”. See more from our European economists here. The accounts came as President Lagarde herself said in a speech that “There is no clear evidence that underlying inflation has peaked”. Against this backdrop, investors are still expecting a further 25bp hike as the most likely outcome at the next ECB meeting on June 15, which if realised would take the deposit rate up to 3.5%.

When it came to yesterday’s other data, UK mortgage approvals fell to 48.7k in April (vs. 53.5k expected). Otherwise, the final manufacturing PMIs for May showed a similar picture to the flash readings. The Euro Area print was revised up two-tenths to 44.8, the UK print was revised up two-tenths to 47.1, and the US was revised down a tenth to 48.4.

To the day ahead now, and the main highlight will be the US jobs report for May. Otherwise, data releases include French industrial production for April. And from central banks, we’ll hear from the ECB’s Vasle.