Imagine fathers at the little league baseball fence. The first brags, “My son is batting 200!” You should be thinking, “That’s not very good.” The second intones, “Oh yea, well my son is batting 175!” “Hold it,” you’re thinking, “this is going backwards.” And your suspicions are confirmed when the third yells out, even louder, “Here comes my son, batting 150!”

As all three dads high-five each other, you look at the name on the uniforms and it reads “Bidenomics.” You think – like Alice – you’ve fallen down a rabbit hole into Wonderland, but soon you realize, this is the economic world the progressives intended. Losers are applauded, the winners chided, and covetousness is the over-arching narrative.

The new Biden plan to reduce student loan payments will be based on income with some payments being zero.

It’s called SAVE for “Saving on a Valuable Education.”

Who saves? Well, like most socialist plans, this one puts the motivations in all the wrong places by encouraging lower incomes, just as the little league ads were encouraging lower batting averages.

Atlas Shrugged

In Atlas Shrugged, Ayn Rand explains how rich folks “shrugged” when taxes got too high. It’s actually an effective explanation of the Laffer Curve, by Arthur Laffer, which shows that at higher levels of taxation, people reduce their contribution. We all “shrug” at some level of taxation. The Biden SAVE plan encourages college graduates to “shrug” as soon as they graduate. Don’t go for a higher paying job, go for the lower one.

Just a few months ago Dallas Mavericks owner Mark Cuban was fined $750,000 by the NBA for purposely losing games. He was encouraged to “shrug” so his team could get a higher draft pick at the end of the season. The Biden SAVE plan does the same thing: It encourages students to lose, by taking lower-paying jobs.

I’ve been told that the poverty mindset goes something like this: “I’m never going to get ahead, so why try?” They think they will always be poor. The Biden plan appeals to those emotions.

The Government has no money!

The money paid for student loans was taken from a productive source and given to an unproductive source. Think about it: If the unproductive source was productive, it would have been supported by the market, and wouldn’t need government help in the first place. This is what government always does. The government only taxes productive sectors of the economy. And it only gives to unproductive sectors. The Biden student loan scheme is simply another example.

Julia and Joe

The Obama administration famously produced an animated video titled The Life of Julia. It explained how she went through life, moving from one government support program to another. My prediction is that the recent Biden student repayment scheme will produce “Julias and Joes.”

You think people won’t “game” the system? I can hear it now, a conversation taking place in the bowels of a university, where they are calculating the highest loan amounts, relative to the lowest repayment schedules, which creates the biggest government payment for tuition. I would think that the university folks making the calculations are calling these students “Julias” and “Joes,” (Biden). When you simply insert this chapter into the Julia video and determine how long the person must work before they can start claiming unemployment, or disability insurance, or social security, or some other government program, you begin to see how the SAVE plan fits into the broader socialist scheme.

Pay=Worth

The Biden plan is called “The SAVE plan” for “Saving on a Valuable Education.” However, if the education were valuable, it would reflect higher, not lower income after graduation. So, the program is mis-titled in the first place. But we should be accustomed to this administration’s use of what George Orwell called “Newspeak” in the dystopian totalitarian state that he described in 1984.

In economic terms, what a person is paid reflects the value they create in a supply and demand market. Construction workers are paid more than elementary teachers because they create more value, according to the market. Burisma pay Hunter Biden $83,000 a month, because he created $83,000 a month in value for access to his father. Simple as that.

However, via the new student-debt plan, President Biden wants US workers to deliver less value to the workplace. I don’t have to explain what that does to GDP and the general wealth of the nation. We all get poorer.

Bring back manufacturing?

Oh, now it’s making sense to me. President Biden wants to bring manufacturing back to the US. He intends to do it by lowering Americans wages below those of the Chinese workers. Brilliant!

When my colleagues hear the phrase, When Helping Hurts, they know it’s from the very good book by Brian Fikkert and Steve Corbett by that name. There also is a series of videos from the Acton Institute titled Poverty Cure, which explains how simply giving money does not cure poverty. Acton’s latest video on this topic is titled Poverty Inc. It explains how resources that were intended to alleviate poverty have created an industry that supports poverty. President Biden’s SAVE scheme is part of that industry.

Oh, it’s a damn shame what the world’s come to They want us back in the office on Mondays too Wish I could just wake up and it not be true But it is, oh it is

Not living in the real world is a lot harder than you would know Sure I got dental, but it’s bad, I go mental ‘cuz I had to fill out both of these forms I also see price hikes on necessities I had to purchase my rental in Ocean City Please don’t tell anyone, it’s so embarrassing The plight of rich men north of Richmond

I just sit here a-wasting my whole life away ‘Cuz this verification code is taking all day How do you expect me to check my 401(k)? Plus, my Fudge Rounds supplier no longer takes Apple Pay

Oh, it’s a damn shame what the world’s come to It takes one person to do my job, so we have two Wish I could just wake up and it not be true But it is, oh it is

Not living in the real world is a lot harder than you would know Sure I got health care, but I get an in-depth scare, only weeks left to open enroll

The new guy plays with his pen, he just sits there and snaps How am I to get in all my 2 p.m. naps? They want us back now on Tuesdays, I just might collapse The plight of rich men north of Richmond

UMich Inflation Expectations Jumped In August, Sentiment Slipped

The final print for August’s University of Michigan sentiment survey was expected to confirm the preliminary data’s rise in confidence driven by a decline in inflation expectations.

However, instead the final print saw inflation expectations increasing intra-month and sentiment declining.

Year-ahead inflation expectations edged up from 3.4% last month to 3.5% this month (up signifcantly from the 3.3% preliminary print). Long-run inflation expectations came in at 3.0% for the third consecutive month, but up from the 2.9% preliminary print.

Source: Bloomberg

After rising sharply for the past several months, the final print for August’s UMich headline sentiment data declined…

Source: Bloomberg

While buying conditions for durables and expectations over living conditions both improved, the long-run economic outlook fell back about 12% this month but remains higher than just two months ago.

Finally, UMich notes that consumers perceive that the rapid improvements in the economy from the past three months have moderated, particularly with inflation, and they are tentative about the outlook ahead.

Watch Live: “A Long Way To Go” – Fed Chair Powell Delivers Hawkish J-Hole Speech

Update: Powell’s full speech is below but to summarize – “we ain’t done yet.”

Chair Powell said The Fed is prepared to raise interest rates further if needed and intends to keep borrowing costs high until inflation is on a convincing path toward the Fed’s 2% target.

“Although inflation has moved down from its peak – a welcome development – it remains too high,” Powell said in the text of a speech Friday at the US central bank’s annual conference in Jackson Hole, Wyoming.

“We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.”

Powell further cautioned that the process “still has a long way to go, even with the more favorable recent readings.”

The Fed Chair explicitly noted the economy may not be cooling as fast as expected, saying recent readings on economic output and consumer spending have been strong.

“Additional evidence of persistently above-trend growth could put further progress on inflation at risk and could warrant further tightening of monetary policy,” Powell said.

Finally, Powell pushed back on speculation that the central bank could raise its inflation target, an idea that has been hotly debated mostly by academics in recent months.

“Two percent is and will remain our inflation target,” he said.

A hawkish address – but admittedly not as hawkish as last year.

* * *

After last year’s brief (8 minutes) uber-hawkish speech, all eyes and ears are on Jackson Hole this morning as Fed Chair Powell delivers his between-FOMC-meetings speech.

Goldman sees a 55-70% chance that he is ‘hawkish’ – the Volcker scenario – reiterate a “job not done” message, indicating the need for an extended period of tighter monetary policy to achieve a decisive win against inflation, whatever it takes.

And a 30-45% chance of a dovish delivery – with Powell questioning the necessity of maintaining a 4% front-end real interest rate at the present time, and whether there is room to align with market expectations for 2024 by reducing front-end real rates by half.

One thing is for sure, markets will react one way or the other.

Watch Powell’s speech below (due to start at 10am ET)…

Read Powell’s full address below:

Good morning. At last year’s Jackson Hole symposium, I delivered a brief, direct message. My remarks this year will be a bit longer, but the message is the same: It is the Fed’s job to bring inflation down to our 2 percent goal, and we will do so. We have tightened policy significantly over the past year. Although inflation has moved down from its peak—a welcome development—it remains too high. We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.

Today I will review our progress so far and discuss the outlook and the uncertainties we face as we pursue our dual mandate goals. I will conclude with a summary of what this means for policy. Given how far we have come, at upcoming meetings we are in a position to proceed carefully as we assess the incoming data and the evolving outlook and risks.

The Decline in Inflation So Far

The ongoing episode of high inflation initially emerged from a collision between very strong demand and pandemic-constrained supply. By the time the Federal Open Market Committee raised the policy rate in March 2022, it was clear that bringing down inflation would depend on both the unwinding of the unprecedented pandemic-related demand and supply distortions and on our tightening of monetary policy, which would slow the growth of aggregate demand, allowing supply time to catch up. While these two forces are now working together to bring down inflation, the process still has a long way to go, even with the more favorable recent readings.

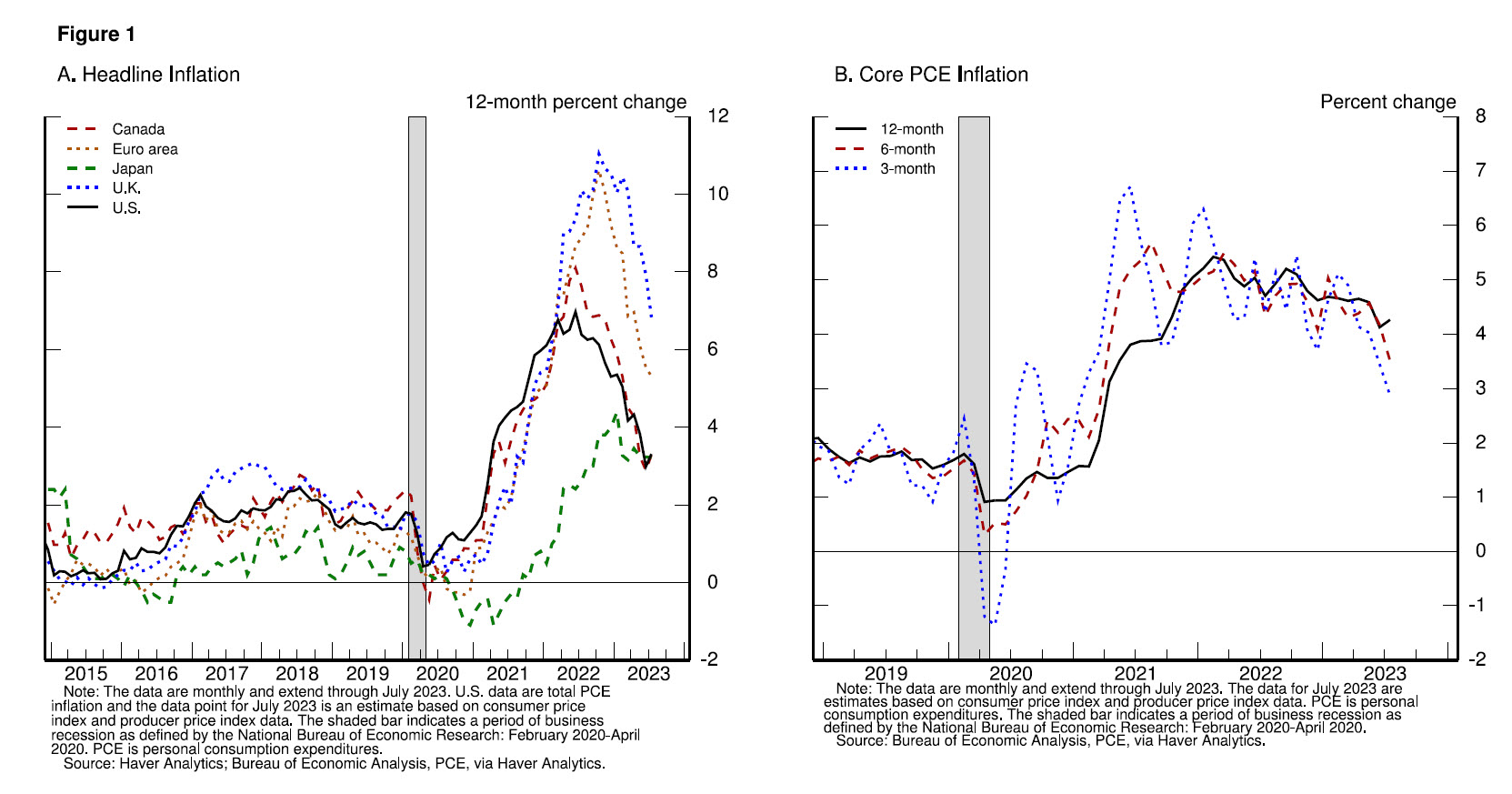

On a 12-month basis, U.S. total, or “headline,” PCE (personal consumption expenditures) inflation peaked at 7 percent in June 2022 and declined to 3.3 percent as of July, following a trajectory roughly in line with global trends (figure 1, panel A).1 The effects of Russia’s war against Ukraine have been a primary driver of the changes in headline inflation around the world since early 2022. Headline inflation is what households and businesses experience most directly, so this decline is very good news. But food and energy prices are influenced by global factors that remain volatile, and can provide a misleading signal of where inflation is headed. In my remaining comments, I will focus on core PCE inflation, which omits the food and energy components.

On a 12-month basis, core PCE inflation peaked at 5.4 percent in February 2022 and declined gradually to 4.3 percent in July (figure 1, panel B). The lower monthly readings for core inflation in June and July were welcome, but two months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal. We can’t yet know the extent to which these lower readings will continue or where underlying inflation will settle over coming quarters. Twelve-month core inflation is still elevated, and there is substantial further ground to cover to get back to price stability.

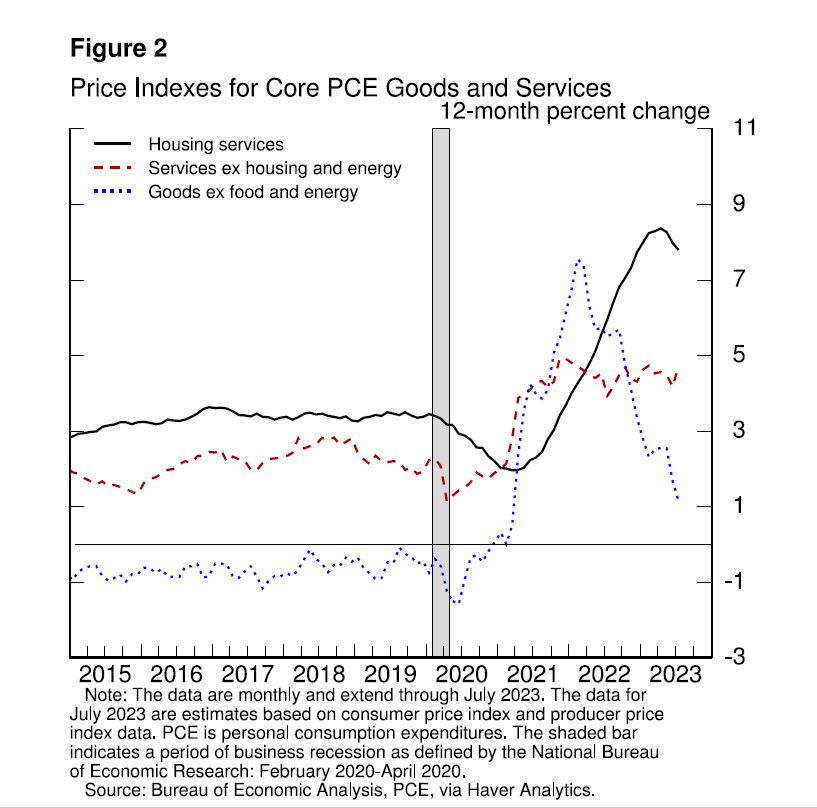

To understand the factors that will likely drive further progress, it is useful to separately examine the three broad components of core PCE inflation—inflation for goods, for housing services, and for all other services, sometimes referred to as nonhousing services (figure 2).

Core goods inflation has fallen sharply, particularly for durable goods, as both tighter monetary policy and the slow unwinding of supply and demand dislocations are bringing it down. The motor vehicle sector provides a good illustration. Earlier in the pandemic, demand for vehicles rose sharply, supported by low interest rates, fiscal transfers, curtailed spending on in-person services, and shifts in preference away from using public transportation and from living in cities. But because of a shortage of semiconductors, vehicle supply actually fell. Vehicle prices spiked, and a large pool of pent-up demand emerged. As the pandemic and its effects have waned, production and inventories have grown, and supply has improved. At the same time, higher interest rates have weighed on demand. Interest rates on auto loans have nearly doubled since early last year, and customers report feeling the effect of higher rates on affordability.2 On net, motor vehicle inflation has declined sharply because of the combined effects of these supply and demand factors.

Similar dynamics are playing out for core goods inflation overall. As they do, the effects of monetary restraint should show through more fully over time. Core goods prices fell the past two months, but on a 12-month basis, core goods inflation remains well above its pre-pandemic level. Sustained progress is needed, and restrictive monetary policy is called for to achieve that progress.

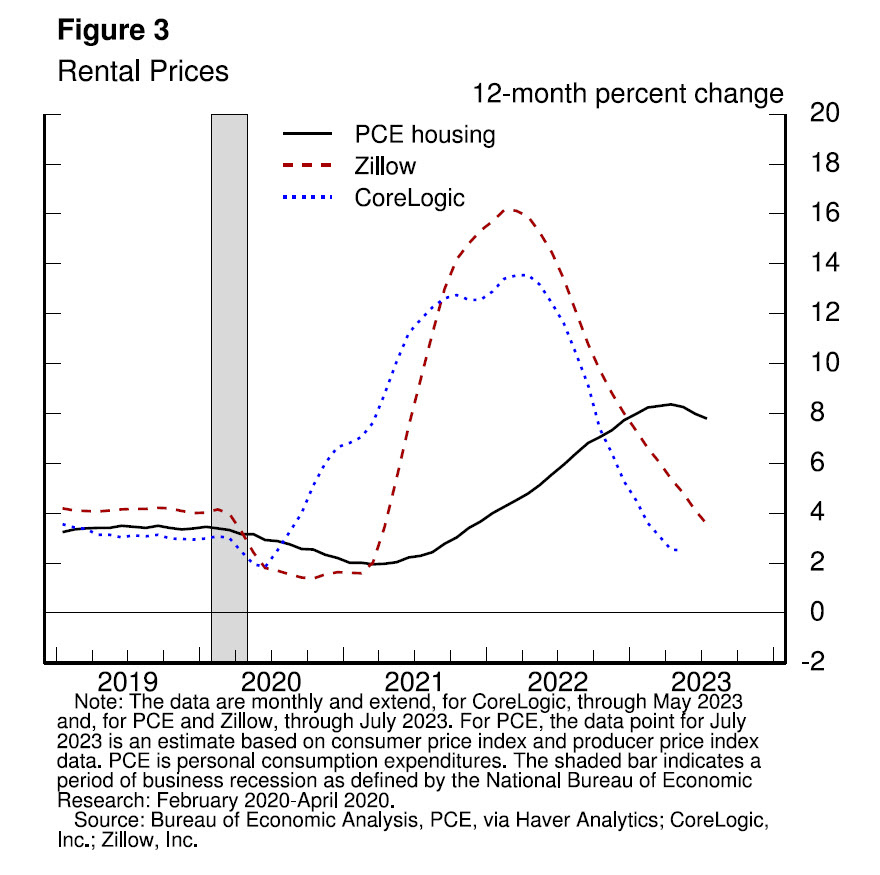

In the highly interest-sensitive housing sector, the effects of monetary policy became apparent soon after liftoff. Mortgage rates doubled over the course of 2022, causing housing starts and sales to fall and house price growth to plummet. Growth in market rents soon peaked and then steadily declined (figure 3).3

Measured housing services inflation lagged these changes, as is typical, but has recently begun to fall. This inflation metric reflects rents paid by all tenants, as well as estimates of the equivalent rents that could be earned from homes that are owner occupied.4 Because leases turn over slowly, it takes time for a decline in market rent growth to work its way into the overall inflation measure. The market rent slowdown has only recently begun to show through to that measure. The slowing growth in rents for new leases over roughly the past year can be thought of as “in the pipeline” and will affect measured housing services inflation over the coming year. Going forward, if market rent growth settles near pre-pandemic levels, housing services inflation should decline toward its pre-pandemic level as well. We will continue to watch the market rent data closely for a signal of the upside and downside risks to housing services inflation.

The final category, nonhousing services, accounts for over half of the core PCE index and includes a broad range of services, such as health care, food services, transportation, and accommodations. Twelve-month inflation in this sector has moved sideways since liftoff. Inflation measured over the past three and six months has declined, however, which is encouraging. Part of the reason for the modest decline of nonhousing services inflation so far is that many of these services were less affected by global supply chain bottlenecks and are generally thought to be less interest sensitive than other sectors such as housing or durable goods. Production of these services is also relatively labor intensive, and the labor market remains tight. Given the size of this sector, some further progress here will be essential to restoring price stability. Over time, restrictive monetary policy will help bring aggregate supply and demand back into better balance, reducing inflationary pressures in this key sector.

The Outlook

Turning to the outlook, although further unwinding of pandemic-related distortions should continue to put some downward pressure on inflation, restrictive monetary policy will likely play an increasingly important role. Getting inflation sustainably back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.

Economic growth

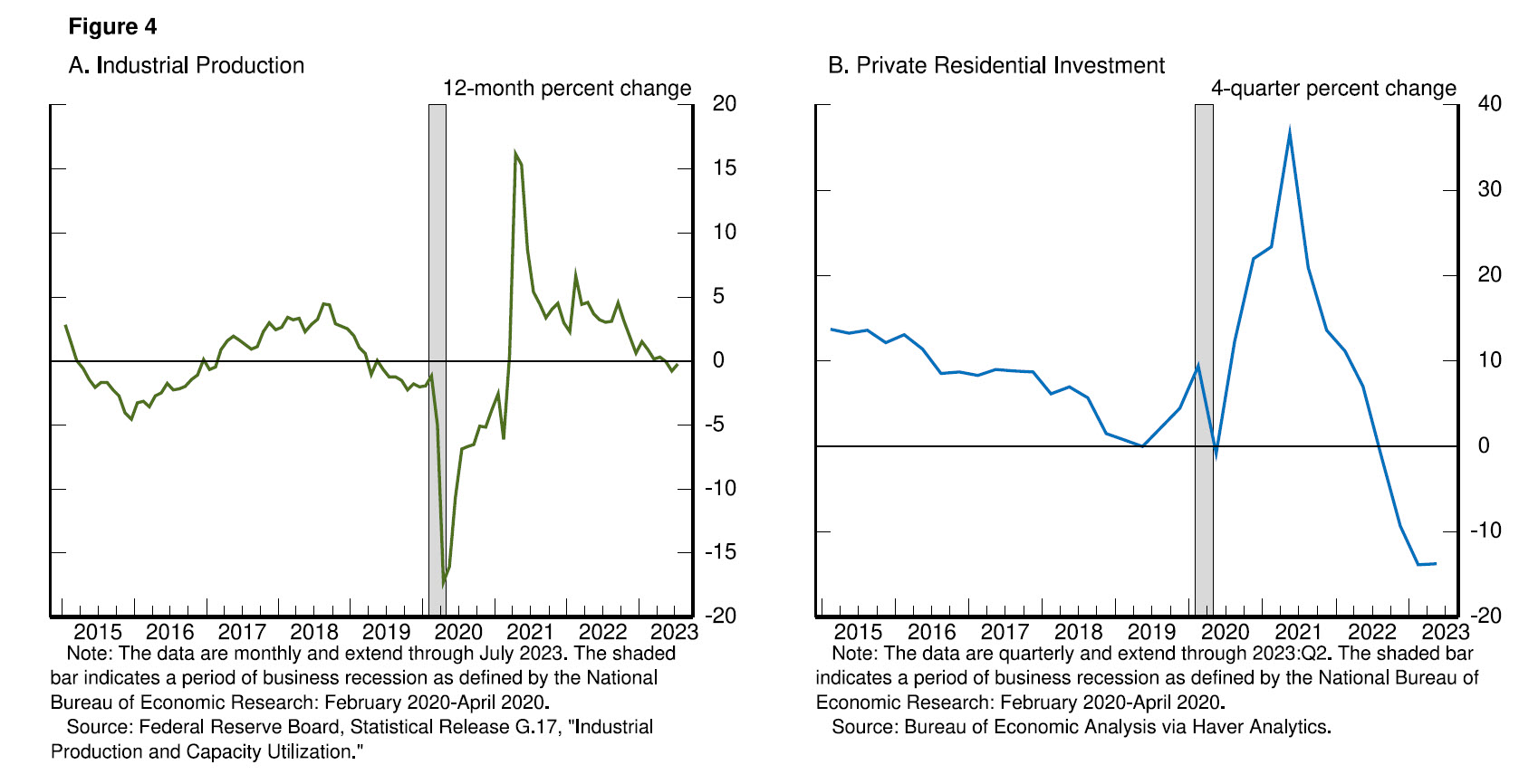

Restrictive monetary policy has tightened financial conditions, supporting the expectation of below-trend growth.5 Since last year’s symposium, the two-year real yield is up about 250 basis points, and longer-term real yields are higher as well—by nearly 150 basis points.6 Beyond changes in interest rates, bank lending standards have tightened, and loan growth has slowed sharply.7 Such a tightening of broad financial conditions typically contributes to a slowing in the growth of economic activity, and there is evidence of that in this cycle as well. For example, growth in industrial production has slowed, and the amount spent on residential investment has declined in each of the past five quarters (figure 4).

But we are attentive to signs that the economy may not be cooling as expected. So far this year, GDP (gross domestic product) growth has come in above expectations and above its longer-run trend, and recent readings on consumer spending have been especially robust. In addition, after decelerating sharply over the past 18 months, the housing sector is showing signs of picking back up. Additional evidence of persistently above-trend growth could put further progress on inflation at risk and could warrant further tightening of monetary policy.

The labor market

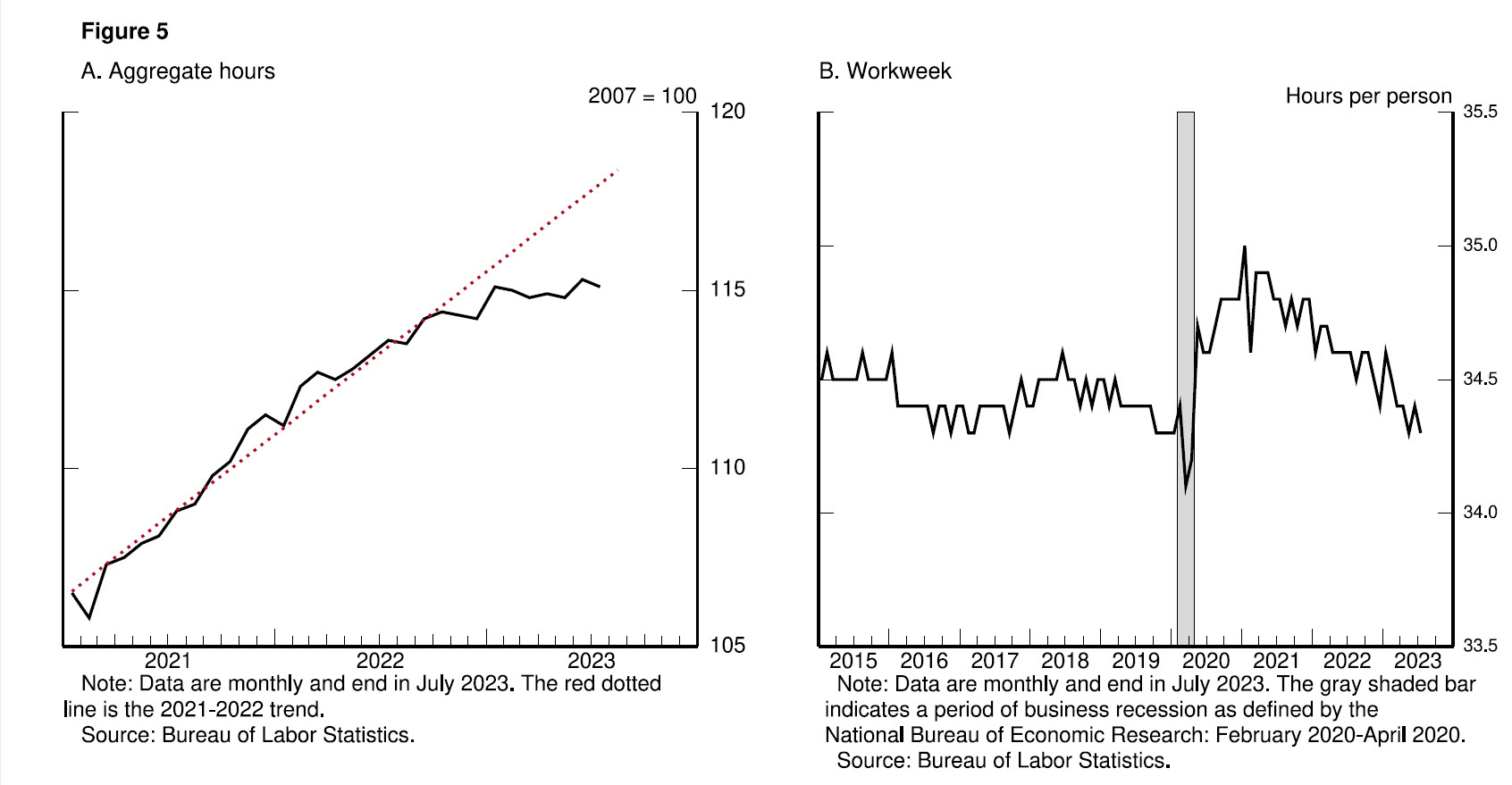

The rebalancing of the labor market has continued over the past year but remains incomplete. Labor supply has improved, driven by stronger participation among workers aged 25 to 54 and by an increase in immigration back toward pre-pandemic levels. Indeed, the labor force participation rate of women in their prime working years reached an all-time high in June. Demand for labor has moderated as well. Job openings remain high but are trending lower. Payroll job growth has slowed significantly. Total hours worked has been flat over the past six months, and the average workweek has declined to the lower end of its pre-pandemic range, reflecting a gradual normalization in labor market conditions (figure 5).

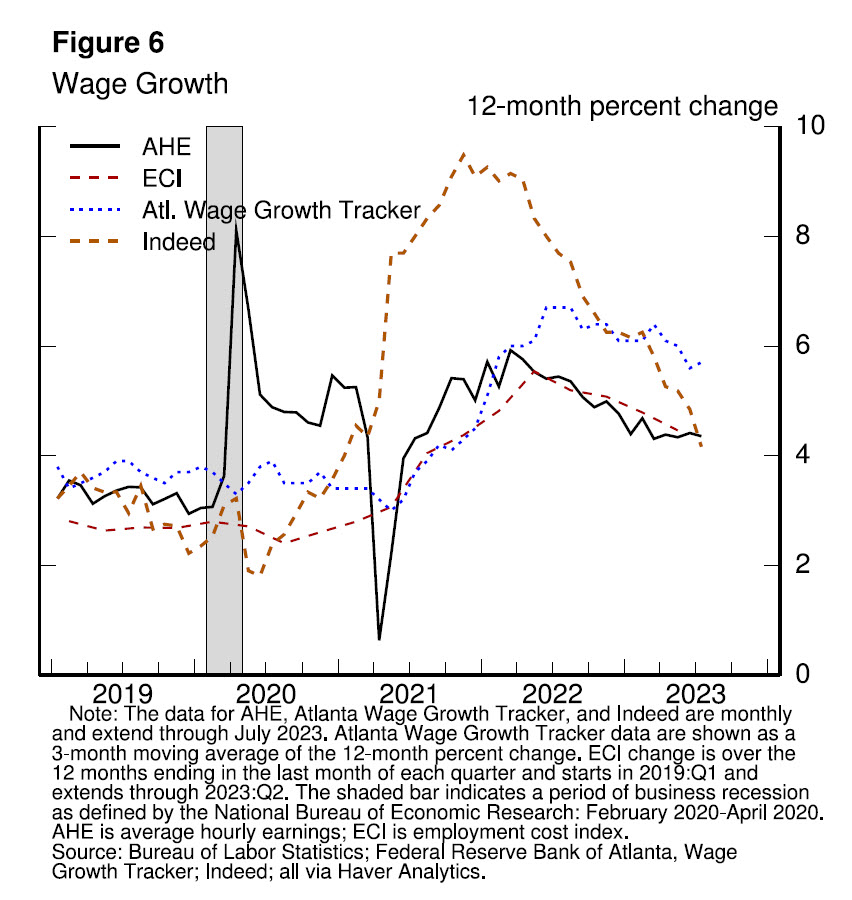

This rebalancing has eased wage pressures. Wage growth across a range of measures continues to slow, albeit gradually (figure 6). While nominal wage growth must ultimately slow to a rate that is consistent with 2 percent inflation, what matters for households is real wage growth. Even as nominal wage growth has slowed, real wage growth has been increasing as inflation has fallen.

We expect this labor market rebalancing to continue. Evidence that the tightness in the labor market is no longer easing could also call for a monetary policy response.

Uncertainty and Risk Management along the Path Forward

Two percent is and will remain our inflation target. We are committed to achieving and sustaining a stance of monetary policy that is sufficiently restrictive to bring inflation down to that level over time. It is challenging, of course, to know in real time when such a stance has been achieved. There are some challenges that are common to all tightening cycles. For example, real interest rates are now positive and well above mainstream estimates of the neutral policy rate. We see the current stance of policy as restrictive, putting downward pressure on economic activity, hiring, and inflation. But we cannot identify with certainty the neutral rate of interest, and thus there is always uncertainty about the precise level of monetary policy restraint.

That assessment is further complicated by uncertainty about the duration of the lags with which monetary tightening affects economic activity and especially inflation. Since the symposium a year ago, the Committee has raised the policy rate by 300 basis points, including 100 basis points over the past seven months. And we have substantially reduced the size of our securities holdings. The wide range of estimates of these lags suggests that there may be significant further drag in the pipeline.

Beyond these traditional sources of policy uncertainty, the supply and demand dislocations unique to this cycle raise further complications through their effects on inflation and labor market dynamics. For example, so far, job openings have declined substantially without increasing unemployment—a highly welcome but historically unusual result that appears to reflect large excess demand for labor. In addition, there is evidence that inflation has become more responsive to labor market tightness than was the case in recent decades.8 These changing dynamics may or may not persist, and this uncertainty underscores the need for agile policymaking.

These uncertainties, both old and new, complicate our task of balancing the risk of tightening monetary policy too much against the risk of tightening too little. Doing too little could allow above-target inflation to become entrenched and ultimately require monetary policy to wring more persistent inflation from the economy at a high cost to employment. Doing too much could also do unnecessary harm to the economy.

Conclusion

As is often the case, we are navigating by the stars under cloudy skies. In such circumstances, risk-management considerations are critical. At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks. Based on this assessment, we will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data. Restoring price stability is essential to achieving both sides of our dual mandate. We will need price stability to achieve a sustained period of strong labor market conditions that benefit all.

By Maartje Wijffelaars, Senior Economist at Rabobank

Stock and bond markets have had quite a busy week in the run up to central bankers’ speeches later today at the Fed’s annual symposium. They’ve both moved up and down, weighing incoming economic data and monetary policy makers’ statements. Currently, the S&P500 is almost back at last week’s close, after it gained 1.5% by the midst of this week. Meanwhile, 10-year treasury yields are almost back at last week’s close of 4.25%, after having reached a 16-year high earlier in the week and dipping upon weak incoming PMI data.

This afternoon, markets and analyst will be searching for any hints regarding the future monetary policy path when Fed chair Jerome Powell takes the stage at 10:05 ET/ 16:05 CET – to be streamed at the Kansas City Fed’s YouTube channel. Later in the day/ evening, at 15:00 ET/ 21:00 CET, ECB president Christine Lagarde will take the floor. Yet don’t hold your breath, as both might well be unwilling to give much guidance into their respective September meetings.

This far into the hiking cycle and with the sticky core inflation still high, it becomes ever more difficult to balance the risk of doing too much or doing too little. Given the rather mixed signals provided by recent data coming in, it seems likely both the Fed and ECB will prefer to gather as much data as possible to make a decision on the best way forward.

Indeed, while recent data quite convincingly suggest economic growth is slowing in Europe, core inflation gave no sign of retreat in July as it stayed put at June’s 5.5% y/y. Next week we will get the first figures for August and it could help the ECB a lot they down as expected by analysts (core is expected to drop to 5.2% y/y and headline to 5.1% y/y).

With respect to the economic data, German GDP figures this morning confirmed the eurozone’s largest economy stagnated in the second quarter of the year. And this morning’s IFO survey for August confirmed the ongoing weakness that was already laid bare by last Wednesday’s PMI data. The IFO Business Climate came in below consensus at 85.7, down from July’s 87.3. In fact, all sectors saw their diffusion index declining, which is further proof that weakness is spreading more broadly into the economy. Remember, that the composite PMI dived deeper into negative territory as well, as activity in the services sector is weakening. At 44.7, Germany’s composite PMI convincingly showed that the tide is worsening rather than improving.

Germany is not alone, however, as the composite PMI for the Eurozone came in at a 33-month low in August, falling starkly into contractionary territory. It dropped from 48.6 in July to 47 in August, also convincingly below the consensus of 48.5. Most worrying is the fact that weakness is more visibly spreading to services. If anything, the risk of a near-term recession has clearly increased. All in all, these figures have let us to revise down our growth projections for the euro area from stagnation in the second half of this years to a minor contraction in the current and final quarter of the year. Minor because, for one, we don’t expect major labour shedding as companies will try to hold on to their workforce in the currently very tight labour market. That being said, risks are clearly tilted to the downside. We will explore our projections in more detail in forthcoming publications.

At the other side of the Atlantic, yesterday’s durable goods orders joined the recent PMI figures in suggesting that the US economy is slowing down. The former came in at -5.2% m/m in July compared to -4% m/m consensus and after 4.6% in June. Remember, the composite PMI fell from 52 in July to 50.4 in August. Yet whilst slowing down, the PMI figure for the US still points to growing rather than contracting activity, driven by the services sector.

This is underscored by the Nowcast forecast by the Atlanta Fed. Its updated figure on 24 August, shows the US economy grew by a still staggering 5.9% annualised rate in the third quarter. Clearly, only so much data has come in for the third quarter so far, yet at least it suggests the US is not as close to entering a recession as the EU – although the US still has a recession approaching further down the road, according to our US watcher Philip Marey. Meanwhile, albeit on a downward trend, core CPI still stood at 4.4% in July, down from its peak of 5.6% in March.

Importantly, while board members of both the ECB and Fed publicly disagree – or at least express doubts – about whether another rate hike is warranted in September, none of them hints at a pivot coming soon. On the contrary, all reiterate yields will need to stay higher for longer. And the latter thinking seems to have been gaining ground in the markets, especially in the US where a pivot was already priced in earlier than in Europe. That said, the weak data in the euro area so far has left a bigger mark on 10-year bond yields than in the US. And, we would also argue that the ‘China factor’ may have had a bigger impact than on the other side of the Atlantic.

US outperformance with respect to the Eurozone and a growing belief that yields will stay higher for longer have supported the dollar recently. The EURUSD cross has dropped from 1.12 last week to 1.08 yesterday, and the euro’s decline is continuing this morning. Our FX strategist Jane Foley believes the dollar is up for some more gains in the coming months, reaching 1.06 on a three-to six-month horizon, before it loses some strength as the gap in economic performance tightens and Fed rate cuts move into view.

As mentioned, bond yields in the euro area have come down from last week’s peak. While non-negligible, they will give governments little respite, however, in terms of rising interest costs. Indeed, while debt ratios, are set to fall in the short term, helped by high nominal GDP growth, in a recent publication we show that projected interest costs are to rise substantially over the coming few years, especially in high-debt countries.

While interest payments will require a larger portion of all countries’ revenues, Italy and Spain are expected to face the greatest debt affordability challenges. In the former, interest-to-revenue ratios are expected to exceed the threshold above which countries tend to enter speculative grade rating territory. On the bright side, there is still time to avoid such a situation and we don’t forecast a new eurozone debt crisis – not the least because of all the EU safety nets set up over the past few years -, but we do point out several vulnerability risks and argue there is no time for complacency in a number of countries. For more insights please read the report or reach out.

Day ahead

The most interesting event of the day will certainly be the Fed’s symposium titled “Structural Shifts in the Global Economy”. Apart from Jerome Powell’s view towards the economic outlook and any possible hints with regards to monetary policy going forward, it will also be interesting if and what he has to say about de-risking, decoupling, and de-dollarization. Will he reiterate parts of Lagarde’s speech earlier this year on the structural impact on consumer price indices of decoupling? Will he share his views on the BRICS extension announced yesterday?

Yesterday the BRICS asked six out of twenty-two applicants to join the bloc: Saudi Arabia, Iran, Egypt, Argentina, Ethiopia and the UAE. Looking at all the vowels it does not seem to make for a nice new acronym. Yet given its increased heft and the inclusion of several heavy weights in commodities (and hence with extensive financial powers), it certainly warrants attention. Will the group be able to agree on a future economic and political course? Will it lead to faster de-dollarization – towards perhaps yuanization? – and a stronger front against Western hegemony in global institutions? As we have already covered in several Dailies this week, in spite of all the heft, it remains to be seen if and how the enlarged group will be able to move forward, given the many different voices, aspirations, dependencies and economic sizes and structures of the countries within the group. Yet it certainly is not a development to neglect by analysts and policy makers.

This afternoon the University of Michigan will also publish its consumer survey outcome for August and the Kansas City Fed will present its services survey activity index for August.

Genital squeezing at jail is “not related to a legitimate penological purpose” and not protected by qualified immunity. Sometimes it seems like the doctrine of qualified immunity—under which police officers and other agents of the state are protected from legal liability for some abuses and mistakes—has no limit. So it’s nice to see courts at least occasionally reject ridiculous qualified immunity claims, like the idea that squeezing a detainee’s genitals during a strip-search is proper and standard procedure.

Indeed, “squeezing a detainee’s penis hard is not a ‘proper part of a search,'” a federal appeals court has held.

The case, before the U.S. Court of Appeals for the 8th Circuit, was brought by Wilbert Glover against Minnesota corrections officer Richard Paul. Paul strip-searched Glover while Glover was jailed at the Ramsey County Adult Detention Center in St. Paul in 2015.

Paul “made me take off my jumpsuit strip search me took his hand and grasp my penis squeeze it hard and gestures,” Glover alleged. After the incident, Glover sought medical care and filed a complaint against Paul, alleging that the corrections officer had violated his constitutional rights.

Paul responded by claiming that he “never touched [Glover’s] genitals or otherwise touched him inappropriately” and that even if he had, he was protected by qualified immunity.

The U.S. District Court for the District of Minnesota rejected Paul’s argument, concluding “that Paul’s alleged actions violated Glover’s clearly established constitutional right to be free from excessive force in the form of sexual assault or abuse,” as the appeals court describes it. In an August 24 ruling, the court affirmed the district court’s ruling.

“On appeal, Paul maintains that he is entitled to qualified immunity,” noted the 8th Circuit judges in their decision:

Qualified immunity protects governmental officials from suit under 42 U.S.C. § 1983 unless a plaintiff shows that the official’s alleged conduct violated a clearly established right of the plaintiff.…Because Glover was a detainee at the time of the incident, his relevant constitutional rights arise under the Due Process Clause of the Fourteenth Amendment….A detainee alleging an excessive use of force must show that the force used against him was objectively unreasonable….

Paul argues that he did not violate Glover’s clearly established right under the Fourteenth Amendment. He maintains that no constitutional violation occurred because “manual contact with a detainee’s genitals may be necessary as part of a search.” And he says that there is no evidence that the strip search or his actions during the search were performed for an improper purpose.

In determining whether Paul is entitled to qualified immunity, we must accept facts that the district court assumed were supported by sufficient evidence….In the order denying qualified immunity, the district court stated that squeezing a detainee’s penis hard is not a “proper part of a search,” and that the “action does not seem inadvertent nor does Paul assert it was.” The court explained that a “jury could find that squeezing a prisoner’s penis hard during a strip search is not penologically necessary.” We infer from these statements that the court assumed that a jury could find that Paul intentionally squeezed Glover’s penis hard in a manner that was not related to a legitimate penological purpose….

Viewing the facts in the light most favorable to Glover, a jury could find that the alleged conduct constituted sexual abuse or assault. We accept that some contact with a detainee’s genitals may be necessary and proper during a legitimate strip search, but Paul’s alleged conduct was intentional and gratuitous, and thus exceeded the legitimate purpose of a search….A reasonable official would have understood that the conduct alleged in Glover’s verified complaint constituted an unreasonable use of force that violated a detainee’s right under the Fourteenth Amendment.

The Foundation for Individual Rights and Expression (FIRE) is fighting a West Virginia University policy requiring faculty to “accept and encourage change that is for the greater good.”

Last month, FIRE wrote @WestVirginiaU expressing concern about a new policy requiring faculty members to “accept and encourage change that is for the greater good.”

Biden administration pushes double talk on tariffs:

The White House says—correctly—that tariffs are taxes that raise prices on American families. Yet, they continue to defend Trump’s near-universal tariffs on steel + alum and $335B of goods from China. Biden could repeal these taxes today with the stroke of a pen. pic.twitter.com/7kf3TJXWf7

• Donald Trump’s mug shot from Fulton County, Georgia, was released yesterday. The former president is using it as a campaign promotion, posting it to Twitter—the first time he’s posted since CEO Elon Musk reinstated his account:

• Paper and bamboo straws were supposed to be better for the environment, but they’re full of potentially toxic per- and polyfluoroalkyl substances (PFAS), a new study finds. “PFAS were more frequently detected in plant-based materials, such as paper and bamboo,” than in plastic straws, note the study authors. “The presence of PFAS in plant-based straws shows that they are not necessarily biodegradable.”

• Three men who say they were coerced into confessing to a murder they didn’t commit had their convictions thrown out on Thursday. The men—Earl Walters, Armond McCloud, and Reginald Cameron—were between the ages of 17 and 20 at the time of their initial interrogations. Each spent between nine and 29 years in prison.

• A federal court has partially dismissed pharmaceutical company GenBioPro’s lawsuit against the state of West Virginia over its restrictions on abortion pills, rejecting GenBioPro’s claim that the state’s ban on abortion pills is preempted by federal law. The court said “GenBioPro could challenge West Virginia’s prohibition on telehealth access to the drug because it’s still up to the FDA to decide how a drug can be provided to patients,” reports ABC News.

• Coming soon to porn in Texas:

The Texas anti-porn law will force all adult websites to post nonsense "HEALTH WARNINGS" about supposed "brain harms" from watching porn, and orders ALL consensual sex content among adults to have "child trafficking" warnings.

• A ballot initiative that “would limit the size of pot farms and severely restrict any modifications to existing ones” has qualified for California’s March 2024 election, notes SFGATE. “The local farmers are warning that passing the initiative would destroy the local commercial cannabis industry.”

• “The principal and a teacher at a Florida Elementary school have been placed on paid administrative leave after staff singled out Black fourth- and fifth-graders and pulled them into assemblies about low test scores,” reportsUSA Today.

Fitch’s recent downgrade of the U.S. debt rating alarmed investors as the deficit and debt steadily increased. The downgrade sent 10-year Treasury bond yields above 4%, causing concern about America’s deteriorating financial condition. The problem is that if radical steps aren’t taken to curb spending, such will cause interest rates to rise. To wit:

“The U.S. borrows in its own currency and will never actually default involuntarily as long as it has a printing press. As rising rates push that financing need higher, though, the ability of the U.S. government to change the fiscal path without politically disastrous measures like cutting entitlements or by overtly printing money is becoming more limited.

If no such radical steps are taken then it almost certainly means paying more to borrow. That rising risk-free-rate will crowd out private investment and dent the value of stocks, all else being equal.”– WSJ

Such certainly seems like a logical conclusion. However, the key to the statement is in the last sentence. Many “bond bears” suggest that rates must rise as deficits increase and more debt is issued. The theory is that at some point, buyers will require a higher yield to buy more debt from the U.S. Such is perfectly logical in a normally functioning bond market where the only players are the individual and institutional bond market players.

In other words, as long as “all else is equal,” rates should rise in such an environment.

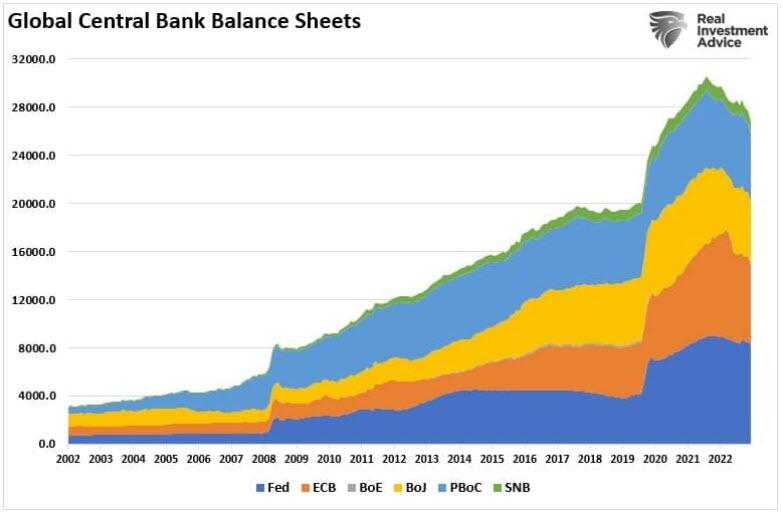

However, all else is not equal in a global economy where government debt yields are controlled by Central Banks colluding with Governments to maintain economic growth, control inflation, and avoid financial crises. Such is evident in the chart below. Since 2008, Central Banks globally have been buyers of global debt.

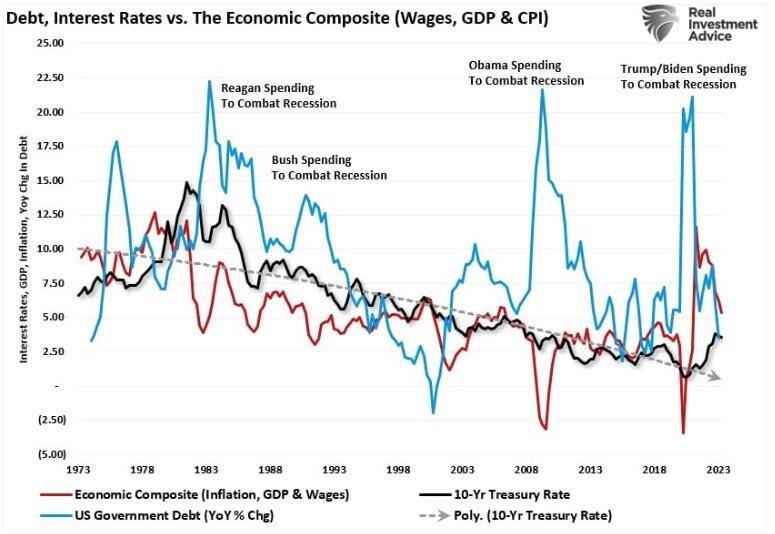

Why have Central Banks engaged in such a massive bond-buying program? To provide liquidity to combat the deflationary forces of debt and keep global economies out of recession. As shown, since 1980, each time the economy was dealt a recessionary blow, the Government responded by increasing debt. However, more debt resulted in a continued decline in inflation, wages, economic growth, and interest rates.

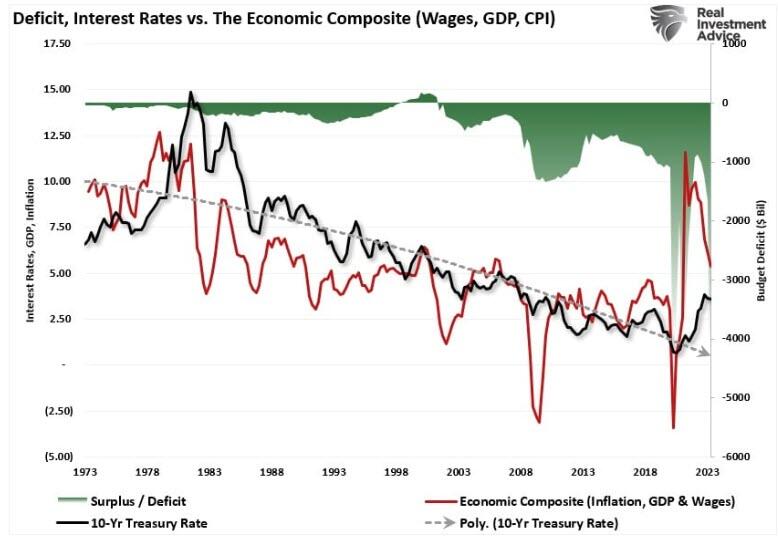

The analysis becomes clearer when viewing the economic composite against the deficit.

The expectation is that “this time is different.” More debt and more significant deficits will lead to higher interest rates. However, since 1980, such has not been the case. (The exception was in 2020, when sending checks to households and shuttering the economy, creating an inflation spike.) More importantly, the Federal Reserve and the global Central Banks remain trapped.

The Fed Remains Trapped

Before 2020, the Federal Reserve wanted higher inflation. However, after the failed experiment of shuttering the economy and sending checks to households, the Fed now wants lower inflation. Ultimately, the Federal Reserve will get its wish as rising debt levels foster slower economic growth rates and disinflation.

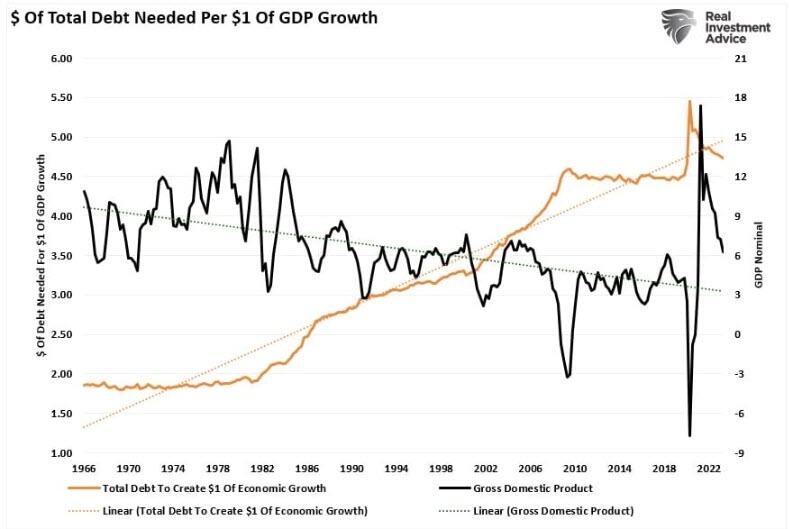

Since 1980, increasing debt levels have been required to create $1 of economic activity. At nearly $5 of debt to create $1 of economic activity, the ability to foster more robust economic growth and inflation is unlikely.

Even if the “bond bears” are correct, and increasing debt levels and deficits do cause higher rates, Central Banks will take actions to push rates artificially lower.

At 4% on 10-year Treasury bonds, borrowing costs remain relatively low from a historical perspective. However, we still see signs of economic deterioration and negative consumer impacts even at that rate. When the leverage ratio is nearly 5:1 in the economy, 5% to 6% rates are an entirely different matter.

Interest payments on the Government debt increase, requiring further deficit spending.

The housing market will decline. People buy payments, not houses, and rising rates mean higher payments.

Higher interest rates will increase borrowing costs, which leads to lower profit margins for corporations.

There is a negative impact on the massive derivatives market, leading to another potential credit crisis as interest rate spread derivatives go bust.

As rates increase, so do the variable interest payments on credit cards. Such will lead to a contraction in disposable income and rising defaults.

There is a negative impact on banks as rising defaults on large debt levels erode capitalization.

Rising interest rates will negatively impact already underfunded pension plans, leading to insecurity about meeting future obligations.

I could go on, but you get the idea.

The Fed Will Intervene

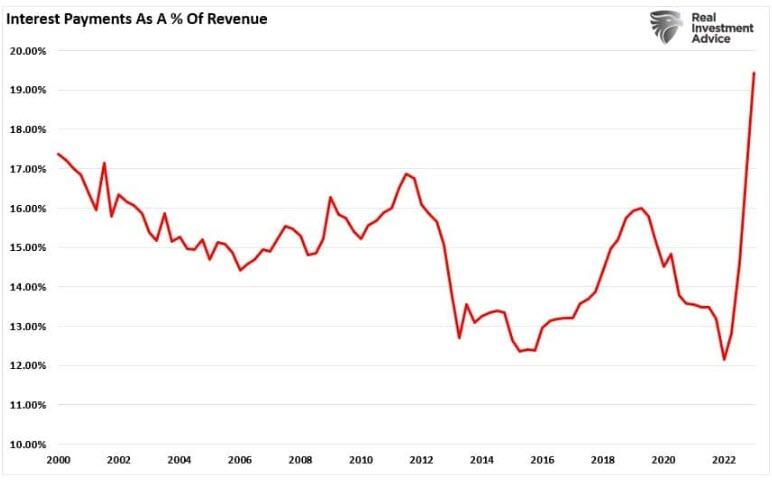

The issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. Such is why the Federal Reserve and the Government will force rates lower through both monetary and fiscal policies. Such is particularly true when the interest on the existing debt absorbs nearly 1/5th of your collected tax revenues.

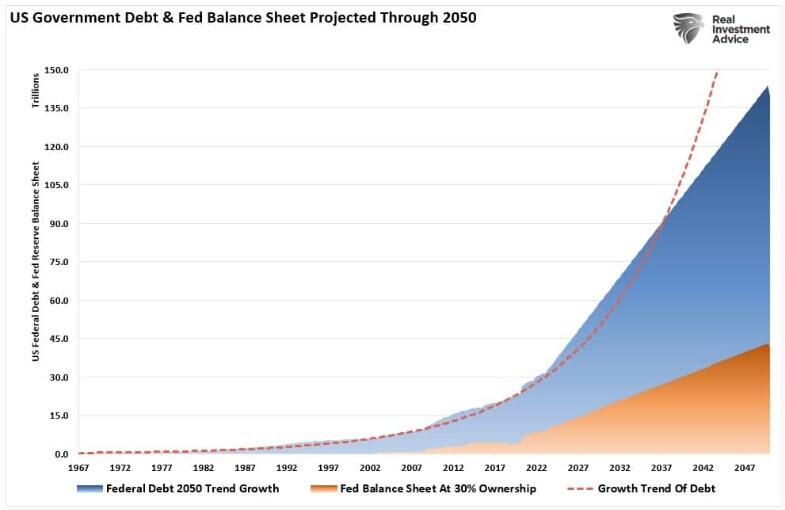

The biggest problem with the “rates must go higher” thesis is the inability of the economy to sustain higher rates due to mounting debt issuance and rising deficits. The Congressional Budget Office recently updated its debt trajectory over the next 30 years. The chart below models that analysis using the growth trend of debt but also factors in the need for the Federal Reserve to monetize nearly 30% of that issuance.

At the current growth rate, the Federal debt load will climb from $32 trillion to roughly $140 trillion by 2050. Concurrently, assuming the Fed continues monetizing 30% of debt issuance, its balance sheet will swell to more than $40 trillion.

Let that sink in for a minute.

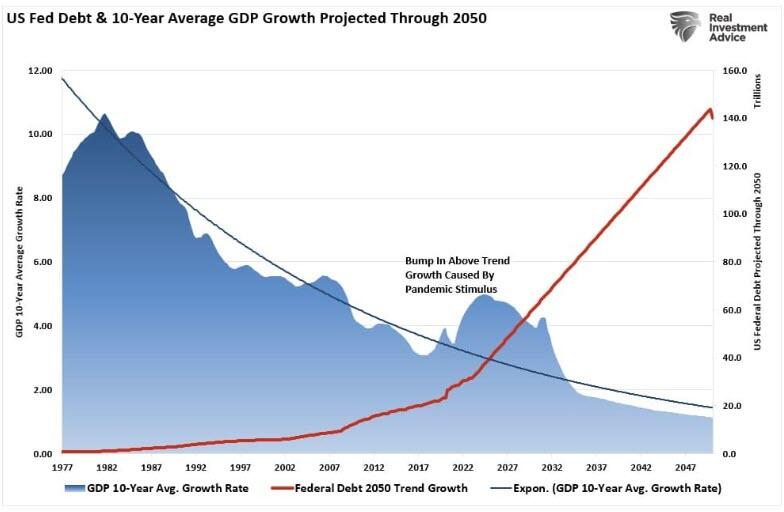

What should not surprise you is that non-productive debt does not create economic growth. Since 1977, the 10-year average GDP growth rate has steadily declined as debt increased. Thus, using the historical growth trend of GDP, the increase in debt will lead to slower economic growth rates in the future.

Conclusion

Therefore, as debt and deficits increase, Central Banks will be forced to suppress interest rates to keep borrowing costs down to sustain weak economic growth rates. The problem with the assumption that rates MUST go higher is three-fold:

All interest rates are relative. The assumption that rates in the U.S. are about to spike higher is likely wrong. Higher yields in U.S. debt attract flows of capital from countries with low to negative yields, which pushes rates lower in the U.S. Given the current push by Central Banks globally to suppress interest rates to keep nascent economic growth going, an eventual zero-yield on U.S. debt is not unrealistic.

The coming budget deficit balloon. Given Washington’s lack of fiscal policy controls and promises of continued largesse, the budget deficit is set to swell above $2 Trillion in coming years. This will require more government bond issuance to fund future expenditures, which will be magnified during the next recessionary spat as tax revenue falls.

Central Banks will continue to buy bonds to maintain the current status quo but will become more aggressive buyers during the next recession. The next QE program by the Fed to offset the next economic downturn will likely be $4 Trillion or more, pushing the 10-year yield toward zero.

If you need a road map of how this ends with lower rates, look at Japan.

Policy analyst Michele Wucker described this sort of problem in her 2016 book “The Gray Rhino,” which was an English-language bestseller in China. Unlike an out-of-the-blue crisis dubbed a “black swan,”a gray rhino is a probable event with plenty of warnings and evidence that is ignored until it is too late.

Zillow Extends Lifeline: New Down Payment Aid Targets Struggling Homebuyers

On Thursday, Freddie Mac’s average rate on a 30-year fixed mortgage topped 7.09%, the highest since 2002, in yet another blow to homebuyers and a sign the housing affordability crisis worsens. On the same day, Zillow Home Loans published a press release about its new “1% Down Payment program to allow eligible home buyers to pay as little as 1% down on their next home purchase.”

“This program can reduce the time needed to save for a down payment and provide another option for those who are otherwise ready to take on a mortgage payment,” Zillow said, adding the new program will first be available for Arizona properties, with nationwide expansions sooner after:

With the 1% Down Payment program, borrowers who qualify can now save just 1% to cover their portion of the down payment and Zillow Home Loans will contribute an additional 2% at closing. The 1% Down Payment program can reduce the time eligible home buyers need to save and open homeownership to those who are otherwise ready to take on a mortgage.

Zillow aims to lower the downpayment barrier and increase activity in the frozen housing market. The highest 30-year fixed mortgage rate since 2002 has sent mortgage applications to the lowest levels since 1995

“For those who can afford higher rent payments but have been held back by the upfront costs associated with homeownership, down payment assistance can help to lower the barrier to entry and make the dream of owning a home a reality,” said Zillow Home Loans’ senior macroeconomist Orphe Divounguy.

Divounguy continued, “The rapid rise in rents and home values means many renters who are already paying high monthly housing costs may not have enough saved up for a large down payment, and these types of programs are welcome innovations in lowering the potential barriers to homeownership for those who qualify.”

If mortgage rates increase, more buyers will be sidelined — and Zillow appears to be getting ahead of this by offering the new program. The inventory issue has yet to abate and is a structural problem that has kept home prices at lofty levels — making this moment in time the least affordable since 1984.

Chief economist at Moody’s Analytics, Mark Zandi, told Bloomberg, “When you get to 7% plus, the market goes dark. Affordability is too far out of reach.”

Perhaps this Zillow venture will fare better than its home flipping several years ago that led to steep losses.

Authored by Simon White, Bloomberg macro strategist,

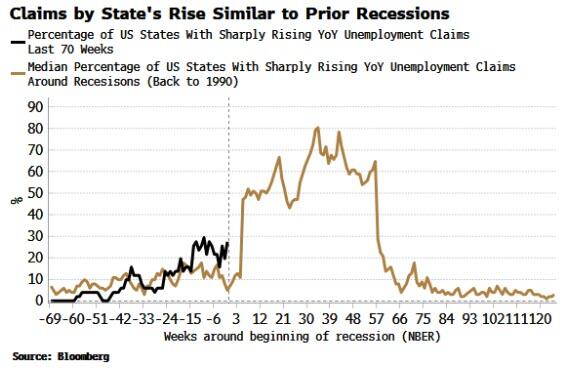

With soft-landing talk rife, it’s a good time to focus on the data still pointing to a recession beginning very soon. Stocks and bonds are not pricing an imminent or near-term recession.

One of these data points is the percentage of states whose unemployment claims are rising sharply on an annual basis. The chart below shows this percentage for this year (black line), and the median of this percentage over recessions back to 1990 (brown line).

As can be seen, the current path is consistent with a recession in the near future.

(We get a similar message if we exclude the extreme 2020 recession.)

The standard caveat applies that this is just one indicator, but its extra utility is that it measures what is going on at sub-national level, and captures the pervasive nature of recessions, in that they are widespread both by sector and geographically.

The indicator also captures the regime-shift nature of recessions, with economies moving abruptly from non-recessionary to recessionary states (everything looks fine … until it doesn’t).

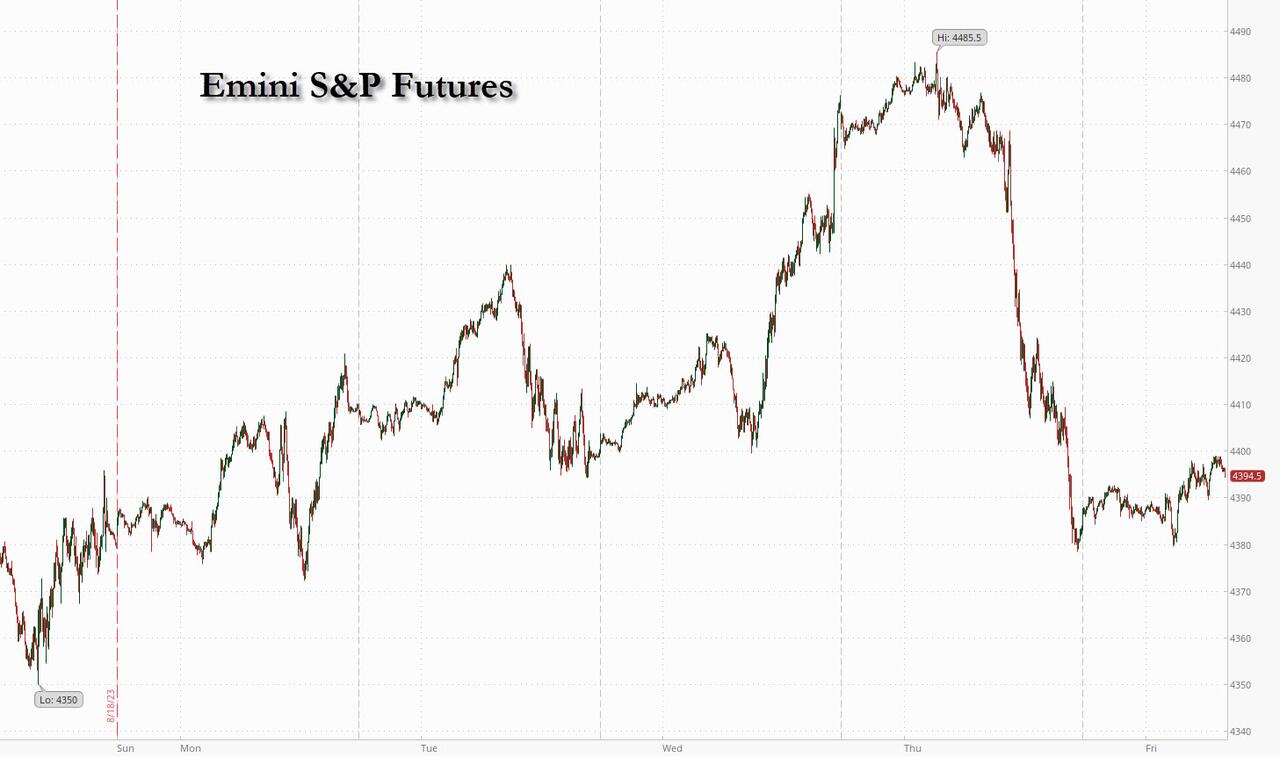

Futures Climb Tentatively Ahead Of Powell’s J-Hole Speech

Futures are slightly higher ahead of today’s Jackson Hole main event, with tech flat following yesterday’s violent Nvidia “sell the news” dump even as yields ticked modestly higher again. At 8:00 am, S&P futures were higher by 0.3% on the day, trading just around 4,400 and paring a portion of Thursday’s session losses while Nasdaq 100 futures are flat after the index sank more than 2% yesterday. Europe’s Stoxx 50 rises 0.6%, extending its first weekly advance in four as commodity shares led gains as oil and iron ore prices climbed; Asian equities slumped Friday, paring their first weekly gain since July, as Chinese stocks slid and technology shares were sold off. Quality is leading, Growth is lagging; Cyclicals flat vs. Defensives.

Powell kicks off 10:05 am ET and this year’s theme “structural changes in the global economy” appears to have roiled bond markets with some thinking >5% Fed Funds is the new normal or perhaps a higher inflation target. The bond market reaction may result in lower yields as we turn the page to Sept as JPM does not think Powell tips his hand on future policy at this event. Treasury yields ticked higher, with two-year notes holding above 5%. The dollar was little changed; commodities are mixed with Energy leading and metals lagging.

In premarket trading, Digital World Acquisition Corp. the special-purpose acquisition company that’s seeking to take Donald Trump’s media company public, falls 4.4% after the former President posted his own mug shot in a return to Elon Musk’s X. Affirm Holdings jumped 7.5% after fourth-quarter revenue at the financial technology company beat expectations, helped by an increase in transactions on its platforms. Here are some other notable premarket movers:

Ardelyx rises 2.8% after the biotech was upgraded to overweight from neutral at Cantor Fitzgerald, saying that the Street is underappreciating the peak sales potential of Xphozah, Ardelyx’s flagship drug.

Clarivate Plc dips 1.8% after RBC Capital Markets downgraded the information services company to sector perform from outperform.

Domo (DOMO) tumbles 33% after the application software company cut its full-year forecast. Cowen cut its rating on the firm in the wake of the report, citing the significantly lower guidance.

Hawaiian Electric (HE) sinks 21% as the utility’s woes deepened following the wildfires in Maui, suspending its dividend while S&P cut its credit rating.

Marvell Technology (MRVL) falls 3.1% after the semiconductor company gave a forecast for the current quarter that was largely line with Wall Street estimates. Analysts noted that its AI business was continuing to grow while KeyBanc said its networking and consumer segments were still weak.

Olaplex (OLPX) drops 5.0% as Piper Sandler cuts its recommendation on the hair-care company to underweight from neutral, citing margin pressures.

Equities have struggled for direction this week, gaining strongly one day only to wipe out the advance the next, as the focus swung from Nvidia earnings to the trajectory of interest rates. As previewed yesterday, Powell, who is scheduled to deliver a speech at 10:05 a.m. Washington time, will likely outline how officials will assess whether rates should go higher and determine when it’s time to start cutting them.

“There could be another phase of uncertainty and a broad-based selloff is possible depending on the magnitude of the hawkishness” at Jackson Hole, said Carlos von Hardenberg, portfolio manager at Mobius Capital Partners. “But the market is differentiating relatively radically between companies that are in the pole position to show very strong earnings growth in the near and medium term.”

The effects of higher-for-longer interest rates will overshadow the buzz around artificial intelligence, spelling trouble for tech stocks, according to Bank of America Corp. strategists. On Thursday, even a blowout sales forecast from Nvidia wasn’t enough to stem the Nasdaq 100’s slump amid a rise in bond yields.

Elsewhere, China eased its mortgage policies further in a push to support its economy, although the boost to stocks on the mainland from the news proved to last just a few minutes.

Europe’s Stoxx 600 is up 0.3% and set to log its first weekly rise in four. Mining, retail and energy stocks are leading gains while health care creates a drag. Here are the biggest European movers:

Tesco shares gain as much as 1.9%, among the top performers in the FTSE 100 Index, after Barclays lifted its price target on the UK grocer and said there’s scope for a guidance boost.

JCDecaux shares gain as much as 4.5%, the most since May, after Deutsche Bank raises the advertising company to buy from hold, saying risks related to the firm’s China exposure may have been priced in.

Aston Martin shares rise as much as 5.7% after Jefferies raised its recommendation on the luxury sports carmaker to buy from hold, saying it sees scope for the company to build on the re-positioning begun by Chairman Lawrence Stroll.

European tech stocks miss out on any artificial intelligence buzz generated by Nvidia’s blowout sales forecasts, as they languish on the fringes of the global AI race.

Watches of Switzerland plunges as much as 29%, the most on record, after Rolex said it plans to buy luxury retailer Bucherer.

CMC Markets shares drop as much as 20% at the open to their lowest level in nearly four years after the online trading platform said in a trading update that its annual net operating income would be lower than last year due to “subdued” market conditions.

Earlier in the session, Asian equities slumped paring their first weekly gain since July, as Chinese stocks slid and technology shares were sold off on risk aversion ahead of a speech from Federal Reserve Chair Jerome Powell. The MSCI Asia Pacific Index declined as much as 1.2%, trimming its advance for the week to 0.6%, with chipmakers TSMC and Samsung among the biggest drags. A gauge off Chinese technology stocks in Hong Kong slumped more than 2% after Meituan warned of slower orders, while NetEase dropped on a revenue miss as the widespread tech selling clouded over their earnings results, while losses in the mainland were limited following a firm liquidity injection by the PBoC and after the securities regulator met with financial industry firms and urged longer-term funds to help steady the stock market.

Japan’s Nikkei 225 fell by as much as 2% after it gapped below 32,000 with tech stocks hit by the broad sector recoil.

ASX 200 was pressured by heavy losses in tech and the commodity sectors, while consumer stocks showed some resilience after stronger earnings from Wesfarmers.

Indian markets closed at their lowest level since June 30 on Friday, marking their fifth straight week of losses, on broad risk aversion ahead of Federal Reserve Chair Jerome Powell’s speech. The S&P BSE Sensex fell 0.6% to 64,886.51 in Mumbai, while the NSE Nifty 50 Index declined by the same magnitude.

Risk appetite in Asia remains fragile amid concerns on China’s economy and expectations of higher-for-longer US interest rates. After a tech-led rally Thursday on Nvidia’s strong results, investor attention has shifted to the Jackson Hole Symposium where Powell’s speech may provide clues on the Fed’s policy path.

In FX, the greenback is supported with the Dollar Index rising 0.2% to its highest since the start of June.

The euro extends recent losses and heads for its sixth weekly decline. EUR/USD drops as much as 0.4% to 1.0766, breaches 200-DMA support on an intraday basis; technically, there is little support until 1.0635, the May lows

USD/JPY pares a 0.3% advance to trade 0.1% higher on the day at 146.04; the pair heads for its fourth weekly advance for the first time since Feb.

GBP/USD down 0.3% to 1.2560, lowest since June 13; the pound was sold for dollars by momentum funds as concerns of a hawkish Powell spurred broad greenback strength, according to traders

In rates, treasuries were slightly cheaper across the curve, following losses seen in core European rates over the early London session. 10-year TSY yields are around 4.245%, cheaper by 1bp on the day with bunds and gilts lagging by additional 3bp and 1.5bp in the sector; belly slightly lags on the Treasuries curve, flattening 5s30s spread by 1.2bp vs. Thursday close. Treasury futures are near lows of the day, adding to losses seen Thursday although price action broadly remains within Wednesday’s session range. US session focus is on Jackson Hole economic policy symposium, where Fed Chair Powell is expected to speak at 10:05am New York. Investors will be focused on Fed speakers at Jackson Hole and the FOMC’s view on the long-term neutral interest rate, which has been in focus extensively this week

In commodities, iron ore was set for its biggest weekly gain since June ahead of China’s traditional peak season for construction activity from next month. Oil trimmed a weekly loss.

Bitcoin is contained in narrow parameters with specific catalysts light as we await Central Bank impetus from the ECB and Fed. JPM sees limited downside for crypto markets in the near term, via CoinDesk.

To the day ahead now, and there are several central bank speakers today, including Fed Chair Powell, the Fed’s Harker, Mester and Goolsbee, along with ECB President Lagarde. Data releases include the Germany’s Ifo business climate indicator for August, and in the US we’ll get the University of Michigan’s final consumer sentiment index for August.

Market Snapshot

S&P 500 futures up 0.2% to 4,396.25

STOXX Europe 600 up 0.3% to 452.93

German 10Y yield little changed at 2.55%

Euro down 0.3% to $1.0782

MXAP down 1.3% to 158.38

MXAPJ down 1.2% to 498.03

Nikkei down 2.1% to 31,624.28

Topix down 0.9% to 2,266.40

Hang Seng Index down 1.4% to 17,956.38

Shanghai Composite down 0.6% to 3,064.08

Sensex down 0.4% to 64,978.04

Australia S&P/ASX 200 down 0.9% to 7,115.18

Kospi down 0.7% to 2,519.14

Brent Futures up 1.1% to $84.27/bbl

Gold spot down 0.2% to $1,913.99

U.S. Dollar Index up 0.20% to 104.20

Top Overnight News from Bloomberg

An abstract interest-rate metric is dominating discussions across trading desks ahead of the Jackson Hole symposium, with investors wondering if Federal Reserve Chair Jerome Powell will weigh in, and bracing for further declines in US Treasuries if he does.

European Central Bank Governing Council member Joachim Nagel said that he’s not convinced inflation is under control enough for a halt in interest rate hikes, with his decision hinging on additional data in the coming weeks.

Business confidence in Germany took another hit in August, despite the economy just exiting a recession in the second quarter.

The yen has eclipsed bond market liquidity as a potential catalyst for a further adjustment to the Bank of Japan’s monetary policy.

American politicians are keener than ever to juice the economy with government cash, a shift that’s already helping to drive up borrowing costs and looks likely to keep them high long after the inflation emergency is over.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded lower following the weak handover from global counterparts after the Nvidia-related euphoria wore off and with markets bracing for Fed Chair Powell’s speech at Jackson Hole. ASX 200 was pressured by heavy losses in tech and the commodity sectors, while consumer stocks showed some resilience after stronger earnings from Wesfarmers. Nikkei 225 fell by as much as 2% after it gapped below 32,000 with tech stocks hit by the broad sector recoil. Hang Seng and Shanghai Comp declined with NetEase and Meituan among the worst performers in Hong Kong as the widespread tech selling clouded over their earnings results, while losses in the mainland were limited following a firm liquidity injection by the PBoC and after the securities regulator met with financial industry firms and urged longer-term funds to help steady the stock market.

Top Asian News

PBoC was said to ask some banks to limit southbound bond connect investments with the guidance said to be aimed at outflows and limiting yuan offshore supply, according to Reuters sources.

China reportedly plans to cut stamp duty on domestic stock trading by up to 50%, via Reuters citing sources; could be announced as soon as Friday.

China is issuing nationwide guidance on the easing of mortgage rules; issuing detailed rules for conditions to qualify for first-home mortgage rates.

Reuters polls shows 55% of economists say the BoJ will not start unwinding ultra-easy policy until at least July 2024, while 73% of economists think BoJ will end YCC control in 2024 (prev. 50%) and 41% expect BoJ to end NIRP in 2024 (prev. 54%)

European bourses are modestly firmer, Euro Stoxx 50 +0.4%, with the overall tone a tentative one ahead of Jackson Hole. Limited equity reaction was seen to German Ifo, GDP revisions or an ECB sources piece that had a dovish headline message. Sectors are primarily in the green with outperformance in Energy and Basic Resources while Health Care languishes in the red. Stateside, futures are more contained than their above peers but retain a similar positive skew, ES +0.2% as attention turns to Chair Powell.

Top European News

ECB’s Nagel it is much too early to think about a rate-hike pause, while he stated they have to be stubborn on policy and more stubborn than inflation, according to an interview with Bloomberg TV.

ECB’s Vujcic said the Eurozone economy is basically stagnating and inflation has most likely peaked, while he added that it is to be seen whether rates are restrictive enough, according to an interview on Bloomberg TV.

Momentum is growing for a pause in ECB rate hikes as recession fears increase, debate still open, via Reuters citing sources; Policymakers agree that any decision to pause would need to make clear the job is not done and future hikes could still be needed. Several of the sources said they saw chances evenly split between hike/pause, smaller number saw a pause as more likely. Re. August Flash PMIs, several policymakers cautioned against reading too much into such surveys as there is a growing gap between hard data and sentiment readings. All sources agreed that even in the scenario of a pause, ECB would need to make clear its job was not done and more policy tightening could still be needed. Those arguing for tightening want solid evidence that inflation is heading back to target without the risk of getting stuck above 2%, say a meaningful decline in underlying inflation would be needed for a pause.

UK Ofgem Energy Price Cap (GBP): 1923 (prev. 2074), -7.3% for dual-fuel households, for the October-December. The first time the average energy bill has gone below 2k since April 2022.

FX

Greenback elevated before Fed Chair Powell emerges from Jackson Hole with the DXY holding above 104.000.

Euro lags after losing 200 DMA and 1.0800+ status vs Dollar even before dovish-leaning ECB sources and downbeat German Ifo survey.

Yen back below 146.00 as yields remain lofty and Tokyo CPI metrics come in mostly softer than expected.

Kiwi faces stronger AUD/NZD headwinds as Aussie derives support from base metals.

NZD/USD towards the bottom of the 0.5928-0.5895 range and AUD/USD vice-versa between 0.6427-03 parameters.

Pound flounders sub-1.2600 against Buck irrespective of improvement in UK consumer confidence per GfK.

PBoC set USD/CNY mid-point at 7.1883 vs exp. 7.2923 (prev. 7.1886)

Fixed Income

Deeper retreat in debt before Fed Chair Powell and ECB President Lagarde deliver remarks at the JH symposium.

Bunds back down towards 132.20 low from 132.57 peak set post-ECB sources and Ifo survey.

Gilts and T-note both depressed within 94.48-24 and 109-20/12+ respective ranges.

BTPs remain under par and sub-115.00 in the wake of a mixed 2-year Italian auction.

Commodities

Crude benchmarks are trending higher despite the modest USD upside and tentative tone overall, action which comes in relatively limited specific fundamentals as we await developments around Australian LNG.

Currently, the benchmarks are towards session highs with WTI Oct’23 above USD 80.00/bbl and Brent Oct’23 around USD 84.50/bbl.

Spot gold is little changed given the incrementally firmer USD and tentative tone overall while spot silver has resumed its advance with technicals assisting.

Base metals benefit from the latest support measures out of China, targeting the property sector.

Offshore Alliance members at Woodside Energy (WDS AT) endorsed the in-principle agreement.

Chevron (CVX) says it has not received any notice of intent to strike from Australian LNG unions.

China’s Industry Ministry said it aims to increase the output of 10 non-ferrous metals by 5% in 2023-2024 and will promote companies cooperating in overseas iron ore exploration, especially in neighbouring countries.

Trader sources cited by Reuters suggest rising prices of a popular Russian crude sold in China are set to peak soon as independent refiners are likely to switch to cheaper Iranian crude as Iran boosts exports to four-and-a-half-year highs.

Geopolitics

White House said US President Biden and Ukrainian President Zelensky discussed the start of training Ukrainian fighter pilots and the expedited approval of other nations to transfer their F-16s, according to Reuters.

Russian military said it intercepted a Ukrainian S-200 missile over Russian territory, while the Russian Defence Ministry said a Ukrainian attack on Crimea involving 42 drones was thwarted, according to Reuters and AFP.

Taiwan Defence Ministry said 13 Chinese military aircraft entered Taiwan’s ‘response zone’ and 5 Chinese naval ships engaged in combat readiness patrols on Friday morning, according to Reuters.

US Event Calendar

10:00: Aug. U. of Mich. Sentiment, est. 71.2, prior 71.2

Current Conditions, prior 77.4

Expectations, prior 67.3

1 Yr Inflation, est. 3.3%, prior 3.3%

5-10 Yr Inflation, est. 2.9%, prior 2.9%

11:00: Aug. Kansas City Fed Services Activ, prior -1

Central Banks

10:05: Fed’s Powell Speaks at Jackson Hole Economic Policy Symposium

11:00: Fed’s Harker Interview With Bloomberg TV

11:30: Fed’s Mester Speaks on CNBC

11:30: Fed’s Harker Interview With Yahoo Finance Live

12:30: Fed’s Goolsbee Speaks on CNBC

14:00: Fed’s Goolsbee Speaks on Bloomberg TV

14:30: Fed’s Mester Speaks on Bloomberg TV

DB’s Henry Allen concludes the overnight wrap

Markets lost significant ground over the last 24 hours, with equities and bonds paring back Wednesday’s gains after strong data and comments from central bankers saw investors price in more rate hikes. That left the S&P 500 down -1.35%, whilst the NASDAQ fell by an even-larger -1.87%, despite the positive earnings release from Nvidia after the previous day’s close. One of the main catalysts for this were the US weekly jobless claims, which fell to 230k (vs. 240k expected) in the week ending August 19. That was beneath every economist’s expectation on Bloomberg, and the fact it hit a 3-week low created some optimism that the economy might not be as weak as the flash PMIs had suggested earlier in the week.

With the data still pointing in different directions, all attention today will now be on the gathering of central bankers at Jackson Hole for the annual economic symposium. This year’s theme is focusing on “Structural Shifts in the Global Economy”, and the big highlight today will be Fed Chair Powell’s speech at 15:05 London time, where we simply have the title “Economic Outlook”.

Recent years have seen Chair Powell use the conference to address important themes. Last year we had a fairly short and direct message on the importance of price stability, which left little doubt about the Fed’s resolve to get inflation back down. And back in 2021, there was a much more dovish message that leaned into the view that above-target inflation would prove temporary. According to our US economists, they don’t expect Powell to send strong signals this year about the near-term policy path. Their view is that the data dependence message at the last FOMC meeting was clear, and it’s too early to abandon that approach. But it’ll be interesting to see if we get any more insight into Powell’s inflation views, and whether he sticks to the view that getting inflation back to target will require economic weakness, including via a higher unemployment rate.

Ahead of Powell’s speech, there were some interesting developments in market pricing yesterday. In particular, futures now suggest that another Fed rate hike to the 5.5-5.75% range is more likely than not for the first time since SVB’s collapse, with the chance of another hike by the November meeting at 53% by the close, and up again to 55% this morning. Clearly we’ve got another jobs report and CPI print ahead of the next meeting, but the moves suggest that markets are coming round to the Fed’s most recent dot plot from June, which suggested there’d still be one more rate hike from here.

The prospect of another hike meant that Treasuries sold off again, and the 3m T-bill yield (+2.8bps) hit a fresh post-2001 high of 5.464%. There was also an increase in yields further out the curve, with the 2yr yield up +5.6bps to 5.02%, and the 10yr yield up +4.5bps to 4.24%. Not all officials seemed to agree with that, with Philadelphia Fed President Harker (a voter this year) saying that “I think that we’ve probably done enough”, and that “I’m in the camp of, let the restrictive stance work for a while, let’s just let this play out for a while, and that should bring inflation down”. On other hand, Boston Fed President Collins sounded more open to further hikes, commenting that “We may need additional increments, and we may be very near a place where we can hold for a substantial amount of time”.

That fresh rise in bond yields meant that the initial equity rally quickly petered out yesterday, and the S&P 500 was down -1.35% by the close, marking its worst day in over 3 weeks. Tech stocks led the moves lower, as the FANG+ Index fell by -3.04%. Nvidia had traded as much as +6.7% higher at the open after reporting very strong results after the previous day’s close, but gave up these gains to close up by a mere +0.10%. Earlier in the day, European equities saw more moderate losses, and the STOXX 600 (-0.41%) fell back after a run of 3 successive gains.

Speaking of Europe, market attention will also be on Jackson Hole this evening, since ECB President Lagarde is due to give a speech there at 20:00 London time. Since the flash PMIs on Wednesday, investors have become more sceptical that the ECB will keep hiking rates, with just a 32.5% chance of a September hike currently priced. The PMIs pointed to growing economic weakness, with the composite PMI for the Euro Area at its lowest level since November 2020, but Euro Area inflation still remains at more than double the ECB’s target, so there’s lots of points for all sides of the debate.

Similar to Powell in the US, our European economists do not expect Lagarde to give any strong near term signal, but are watchful of hints on how the ECB’s reaction function may evolve as it finds itself at or close to the terminal rate but seeks to avoid an easing in financial conditions. Ahead of Lagarde’s speech today, we heard from Centeno, one of the ECB doves, who said that “we have to be cautious (at the September meeting) because downside risks… have materialized”. This is one of the most dovish ECB comments of the summer though he added that “it was probably too soon to call it a done deal” when it comes to a September pause. On the other hand, Bundesbank President Nagel said that for him it was “much too early to think about a pause” European sovereign bonds were mostly steady yesterday, with yields on 10yr bunds (-0.5bps), OATs (-0.3bps) and BTPs (+0.7bps) seeing little movement in either direction.

Overnight in Asia, the equity declines have continued across the entire region. The Nikkei (-1.84%) is leading the moves, bringing an end to its run of 4 consecutive gains, while the Hang Seng (-1.03%), the KOSPI (-0.72%), the CSI (-0.49%) and Shanghai Composite (-0.45%) have also lost ground. Looking forward, US equity futures have stabilised overnight, with those on the S&P 500 (+0.06%) marginally higher after the previous day’s losses. Otherwise, the US Dollar has continued to strengthen ahead of Chair Powell’s speech, and the dollar index is now on track to close at its highest level since May 31, having risen for 6 consecutive weeks now.

To the day ahead now, and there are several central bank speakers today, including Fed Chair Powell, the Fed’s Harker, Mester and Goolsbee, along with ECB President Lagarde. Data releases include the Germany’s Ifo business climate indicator for August, and in the US we’ll get the University of Michigan’s final consumer sentiment index for August.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}