By Michael Every of Rabobank

I’ve said it before recently, but there are decades where nothing happens and weeks where decades happen: this is not one of those decades, but this is possibly one of those weeks.

First, Ukraine. The follow-on from Friday’s public White House meltdown between President Trump, Vice-President Vance, and President Zelenskyy — which is how diplomacy often works when the cameras are off — was another emergency European summit in London attended by all those whom the US and Russia have already cut out of negotiations, plus Canada, and at which Zelenskyy was literally embraced.

The easy work there was Zelenskyy again saying he’ll sign the US minerals agreement deal, as Trump and others make clear he has no other choice. The unresolved hard work is still what blew up Friday’s meeting: Zelenskyy’s demands for security guarantees and a reported desire to fight on rather than offer big concessions for a peace deal without them.

Europe is saying that it will step up to make Ukraine an “indigestible steel porcupine.” Their unfolding proposal is a one month pause in air, sea, and energy attacks, followed by a “Coalition of the willing” sending troops to Ukraine to enforce a ceasefire. Yet that proposal unfolds when Europe admits it still requires a US backstop, with the implication being NATO Article 5 protection.

As Elon Musk agreed with a call for the US to leave NATO and the UN, that may not fly as it would directly link America to a war they are trying to step away from to focus on Asia; the US is offering the presence of its businesses on the ground alone to deter Russian attacks. Moreover, Russia has previously said foreign troops in Ukraine is a casus bello: even the term “Coalition of the willing” was last used during the 2003 Iraq war which Russia opposed as illegal. That means that Europe would be embracing a strategy that risks direction confrontation with Russia unless the latter was utterly convinced that this could not work due to Europe’s ability to project overwhelming force. Even there we see huge risks: France and the UK could already extend their nuclear umbrellas to Ukraine, for example, but obviously won’t for fear of escalation, even as France considers doing so for Europe: so, what will Europe be prepared to do on the conventional front?

As Professor Helen Thompson puts it: “The veil often placed over US power to sooth European pride is being removed, but the core European demand in the horror at this exposure is for the US to maintain overstretch and exercise power it does not have.”

Vice-President Vance was more direct: “The bitter irony of America’s present predicament is that the very people who cheer for permanent arms shipments to Ukraine also supported the de-industrialization of America. The very things you want us to send are things we don’t make enough of.”

President Trump was, of course, far more provocative: “We should spend less time worrying about Putin, and more time worrying about migrant rape gangs, drug lords, murderers, and people from mental institutions entering our Country – So that we don’t end up like Europe!”

To be clear, Europe can support Ukraine and itself: it’s just going to be very expensive – and the Americans won’t be paying for Europe anymore.

Indeed, if in 1938 British PM Chamberlain claimed, “Peace for our time”, in 2025 PM Starmer is admitting, “Peace for our dime.” Bloomberg has estimated Europe might have to spend €300bn extra annually in defence spending ahead, but Jakub Janda from the Centre for Security Policy in Prague states: “It is possible to have strong European military to defend Europe. Even without the US. It costs at least 7-10% of GDP annually in initial years and then at least 5% of GDP. When the hell are we starting?” Is Europe serious about doing this? We will hear more on that this week, with a Bundesbank proposal on debt brake reform today, and another European summit on Thursday. Just recall there is a huge price tag for European inaction as well.

Yet even in crazy times, beware crazy press stories. For example, that the US is looking to reopen Nord Stream 2, with a former Stasi member driving the deal forwards. Given the US would then lose its LNG exports to Europe to cheaper Russian gas, and Europe would lose strategic autonomy vs. Russia, the only geopolitical worlds in which that deal could happen are one where either: 1) the US offers Russia a sphere of influence over all of Europe as quid pro quo for an inverse-Nixon strategy of Russia stepping away from its relationship with China; or 2) Europe walks away from Ukraine and the US and accepts the same de facto deal. To say that these scenarios come with large macro and market side effects is an understatement that those going cross-eyed at the idea of cheaper European energy prices will probably fail to see.

Second, tariffs. Tuesday sees 25% US tariffs on Mexico and Canada kick in, unless changes are made at the last minute, and an additional 10% on China, which seems a given. Notably, Mexico is offering to match the US external tariff against China, as well as buying more US goods, to avoid its own US tariff. US Treasury Secretary Bessent favours this “Fortress America” approach and has asked Canada to join (even as the US is also considering putting tariffs on lumber, which would hit Canada hardest). I flagged exactly this approach as logical economic statecraft from the start.

This is critical not just in terms of macro strategy but regarding ‘grand macro strategy’. If the US presses ahead with 25% tariffs, the White House is aiming at going solo. That means global chaos, and the market impact would be enormous. However, if the US builds a “Fortress America” vs. China, the same umbrella could extend to the UK, Europe, and others, if they agree the same terms. That means global bifurcation, and the market impact would again be huge. Indeed, as trade and defence policy become fused, even South Korea and Japan, despite their historic frictions, say they need to increase their cooperation rapidly: a long-standing US foreign policy goal is perhaps being achieved on that front.

Third, China. This week sees the “Two sessions” of the National People’s Congress and the Chinese People’s Political Consultative Conference. The policies announced are likely to focus on how to steer the economy through the turbulence of US tariffs and a changing world order. Markets will be most focused on how much stimulus is announced, and in what form. Given we already have an ongoing uptick in inflation in some places, and US tariffs are clearly adding to that momentum, large Chinese fiscal stimulus, if seen, could easily exacerbate market concerns.

Fourth, crypto. Prices of some of these assets have already soared from recent lows after they were included in an announcement on a planned US strategic crypto reserve. Friday will see a formal US Crypto Summit that may flesh out exactly how, and how much, crypto will be bought by the US, and to what end. There are potentially major implications here for the global financial architecture alongside “Buy all the things!” memetastic trading opportunities.

Fifth, the Middle East. The Israel-Hamas ceasefire is wobbling as Egypt’s plans for Gaza progress.

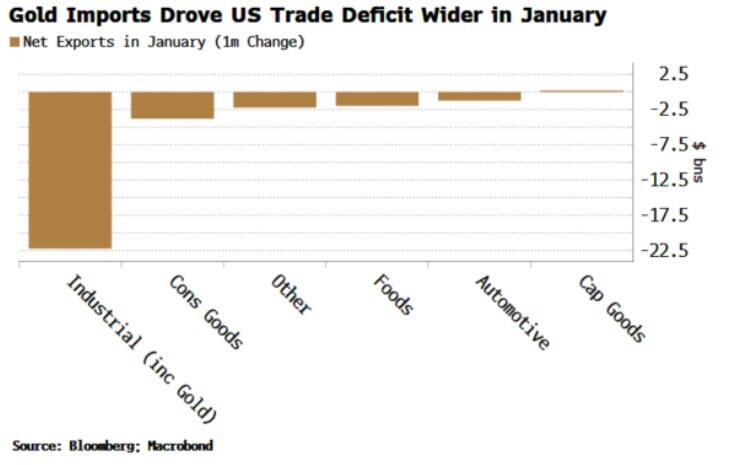

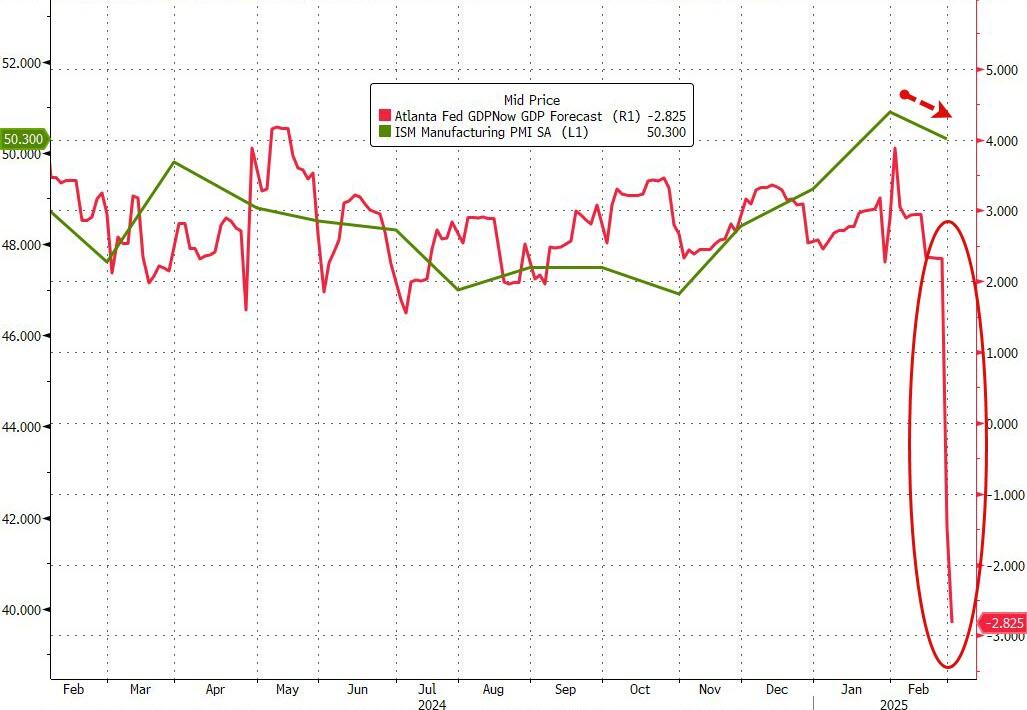

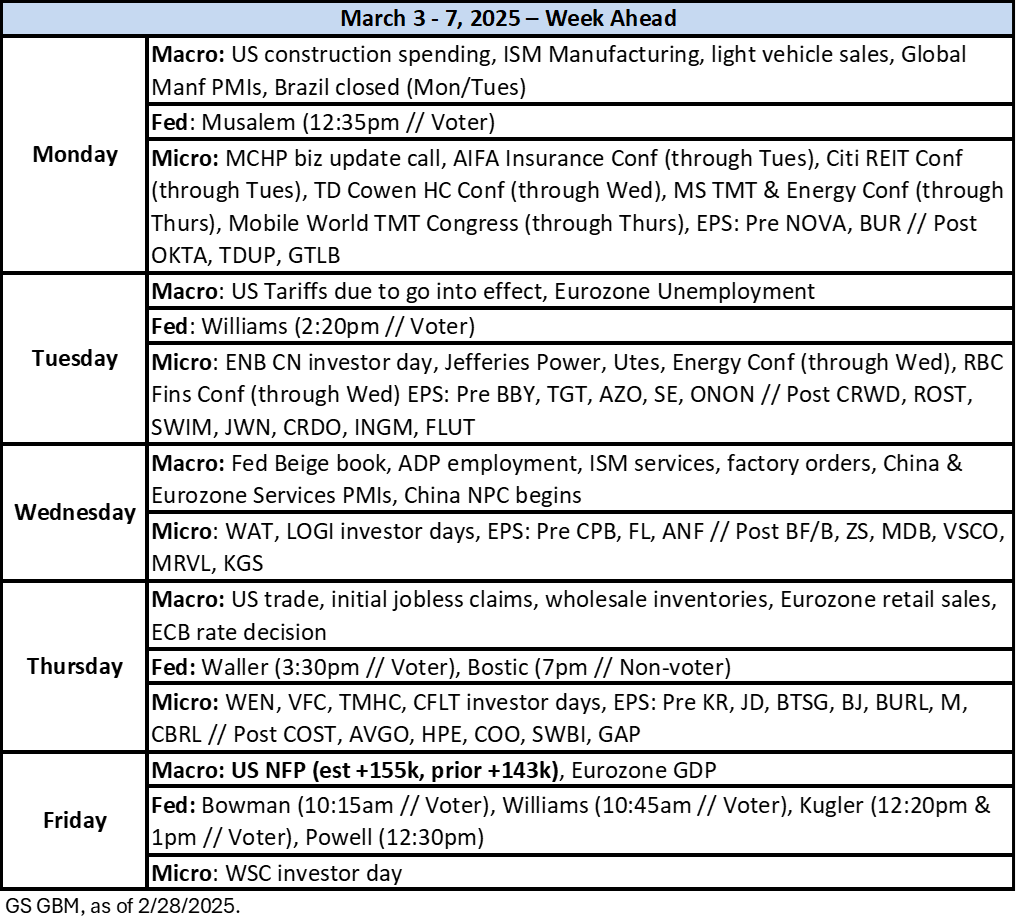

Sixth, traditional macro. Friday saw the Atlanta Fed GDPNow print plunge from 2.3% to -1.5%, driven by the DOGE cost-cutting on a US economy propped up by a 6-7% fiscal deficit. Markets will start thinking about a recession if that continues. That’s before we get the ECB meeting on Thursday (see our preview), and US payrolls on Friday, as federal workers fear for their jobs.