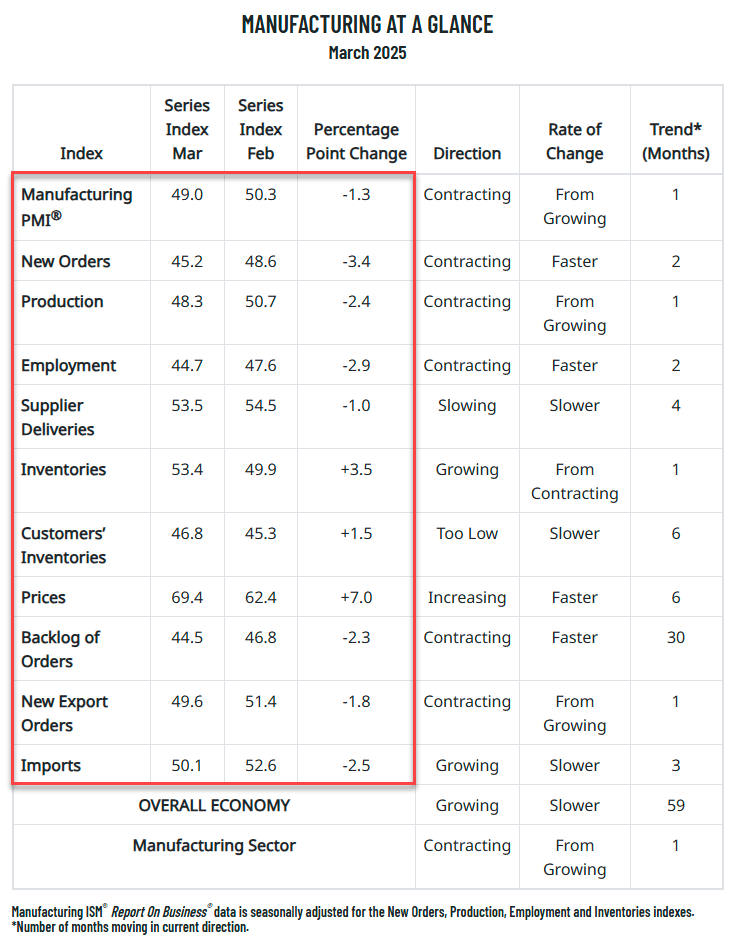

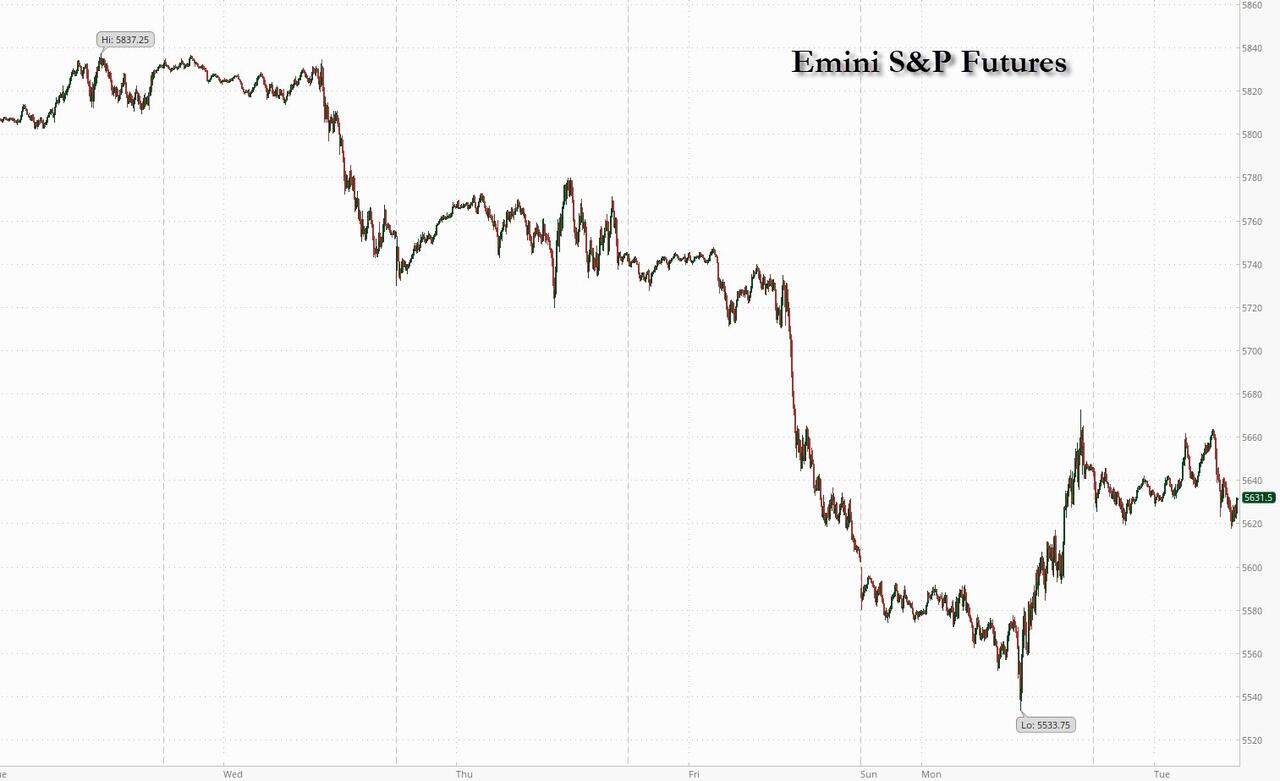

US equity futures fell abruptly just around 6am ET, reversing earlier gains and unable to benefit from the positive risk tone in European trade, hinting at another very volatile session on Wall Street, as tomorrow’s tariffs “liberation day” loomed over markets. Gold extended its winning streak, rising to another record high. As of 8:00am ET, S&P futures were down 0.5%, reversing an earlier gain of 0.2%, after the Washington Post reported a White House proposal to impose tariffs of around 20% on most imports. Nasdaq futures slid 0.6% as Tesla rose modestly but other Mag 7 stocks were in the red. European and Asian markets both rose. Bond yields slid 4bps, pushing the 10Y yield to 4.16% while the USD traded higher on the back of Euro weakness. Commodities are mostly flat this morning with base metals declining (copper -0.9%). Overnight, headlines were largely light, with geopolitical tension and trade policy remaining uncertain. Trump seems to dial back his criticism on Putin, per BBG article (here). We will get the Final March ISM-Mfg this morning: consensus expects the Index to print 49.5 survey vs. 50.3 prior; we also get the latest JOLTS report.

In US premarket trading, Tesla rose while fellow Magnificent Seven stocks edge lower (Tesla +3.1%, Nvidia +0.6%, Alphabet +0.5%, Meta +0.2%, Amazon +0.3%, Microsoft +0.2%, Apple -1%). Johnson & Johnson slid 3.5% in premarket trading after a judge rejected its third attempt to use bankruptcy of one of its units to end baby powder cancer claims. Delta Airlines Inc. and Southwest Airlines Co. fell after Jefferies analysts cut their ratings on concern about consumer spending. Here are some other notable premarket movers:

- Newsmax shares jump 11%, putting the conservative media outlet’s stock on track to extend gains after it jumped 735% in its debut Monday.

- Live Nation slip 1.5% after President Donald Trump said he will sign an executive order aimed at tackling ticket scalping, saying that it is a “big step” in dealing with an issue that “bothers” a lot of artists

- Microvast shares surge 26% after the lithium-ion battery maker reported 2024 revenue that beat its guidance thanks to growing demand for its technology.

- Gorilla Technology shares drop 6.4% after the analytics technology firm reported full-year results and reiterated its revenue forecast for 2025.

- Intel slid after new CEO Lip-Bu Tan said the chipmaker will spin off assets that aren’t central to its mission and create new products including custom semiconductors to try to better align itself with customers

President Donald Trump will announce his reciprocal tariff plan at 3 p.m. on Wednesday at an event in the White House Rose Garden, but the extent of his levies remain unclear. There’s also confusion around whether the US president will take a lenient or harder tack, making investors wary of risky stock bets.

“Investors are grappling with what could be announced this week,” said Laura Cooper, global investment strategist at Nuveen. “The range of outcomes is so wide that traders are struggling with how to price in that potential outcome.”

Futures were hit shortly after 6am after the WaPo reported that White House aides have drafted a proposal to impose tariffs of around 20% on most imports to the United States. In a hitpiece that appears intended to spark panic and restart the selloff, the authors write that “if implemented, the plan is likely to send shock waves through the stock market and global economy. Assuming that permanent tariffs took effect in the current quarter and triggered robust retaliation by U.S. trading partners, the economy would almost immediately tumble into a recession that would last for more than a year, sending the jobless rate above 7 percent, according to Mark Zandi, chief economist for Moody’s, who described the results as a worst-case scenario.”

Trump has touted his April 2 announcement as a “Liberation Day,” heralding the start of a more protectionist policy meant as retribution against trading partners he has long accused of “ripping off” the US. He has already placed levies on Canada, Mexico and China — the US’s three largest trading partners — as well as automobiles, steel and aluminum. Import taxes on copper could come within several weeks. He has also threatened duties on pharmaceutical, semiconductor and lumber imports.

Many fear Trump’s announcement will mark the start of lengthy and fractious negotiations with trade partners, pressuring the economy and keeping market volatility elevated. On Tuesday, European Commission President Ursula von der Leyen said the bloc is prepared to retaliate if reciprocal tariffs are imposed.

“We could get another period of potential negotiations which is just going to prolong this uncertainty and underpin further choppy price action,” Nuveen’s Cooper said.

As tariffs loom, US carmakers are lobbying the administration to exclude certain low-cost car components, Bloomberg reported. The EU said it will use a broad range of options to retaliate. An analysis by Bloomberg Economics found that a maximalist approach could add up to 28 percentage points to the average US tariff rate — resulting in a hit of 4% to US GDP.

Strategists at Citigroup said that a surge in short flows pushed net positioning for the Nasdaq back to neutral ahead of tariff announcements. Barclays strategists, meanwhile, said that hedge funds and CTAs turned short US equities and long Treasuries last month, likely improving the risk-reward outlook into April 2.

Chip stocks could be in focus after Commerce chief Lutnick signaled he could withhold promised Chips Act grants as he pushes companies in line for subsidies to expand their US projects.

Europe’s Stoxx 600 rose 1.2% and is on course to snap a four-day losing streak as concerns regarding imminent US trade tariffs appear to have subsided. All 20 sectors are in the green, with auto, industrial and technology names leading gains. Goldman Sachs strategists cited a weaker growth outlook as a reason to cut their forecast for Europe’s Stoxx 600, following a similar move from the US team. The team led by Sharon Bell trimmed the 12-month target on the index to 570 points from 580. Here are the biggest movers Tuesday:

- Europe’s biggest pharmaceutical companies advance, making healthcare the best performing Stoxx 600 subgroup, after JPMorgan analysts say potential US tariffs are expected to have a “manageable impact” on the sector

- Gubra shares jump as much as 19% after the Danish drugmaker said interim phase 1 results for its obesity treatment candidate GUBamy were “positive.” Shares trim some gains to rise 12% at 10.27am CET

- Greencore Group shares rise as much as 11% after the food producer said better-than-expected profit conversion means its FY25 adjusted operating profit will be ahead of current consensus. Analysts at Jefferies said the positive update

- Enav shares jump after results met estimates and the air navigation services firm said it sees an annual revenue growth of 4.3% by 2029; Banca Akros’ Francesco Sala says the results were in line with estimates

- UK supermarket stocks fall as a Kantar report adds to concern over increasing competitive pressures across the industry. Separately, BNPP Exane cuts earnings estimates for Tesco and Sainsbury, while downgrading the latter

- Genmab falls as much as 5.4% after Bernstein cut its rating on the biotechnology company to underperform, saying the share price is far from fully discounting the loss of exclusivity for its Darzalex blood cancer treatment

- Zealand Pharma shares drop as much as 6.3%, worst performer in the Stoxx 600 Health Care Index, after smaller Danish drug developer Gubra said interim early-stage results for its experimental obesity treatment were positive

- Travis Perkins shares fall as much as 13% to their lowest since June 2009 after the wholesaler said there was uncertainty regarding recovery in UK construction activity and challenging market conditions have continued

- Interroll shares drop as much as 2.6% after Kepler Cheuvreux cut the recommendation on the Swiss industrial equipment firm to reduce from hold, citing limited near-term catalysts and high valuation

Earlier in the session, Asian equities also rose, poised to snap a three-day selloff as traders reassessed positions ahead of the planned imposition of more US tariffs. The MSCI Asia Pacific Index advanced as much as 1.1%, led by gains in Taiwan, South Korea and Hong Kong. TSMC, Tencent and Samsung Electronics were among the biggest boosts. Traders remained on edge, however, with 30-day volatility on the gauge trading around the highest level since October. Most key Asian benchmarks were in the green on Tuesday. India was an exception, with tech heavyweights sliding on concern that slower growth in the US may hurt spending by their clients. Markets in Indonesia, Malaysia and the Philippines were shut for holidays.

The rebound doesn’t signal “much about the overall market’s direction in next 6 to 12 months,” said Homin Lee, senior macro strategist at Lombard Odier Singapore. “It will still be important to get the details of Trump’s announcements tomorrow given the significant – and potentially market-negative – complexities implied in the tariff framework Trump appears to be considering.”

In FX, the Bloomberg Dollar Spot Index is little changed. The Aussie dollar pared gains seen after the RBA stood pat on rates with a slight hawkish tinge to the statement. The Swedish krona takes top spot with a 0.5% gain.

In rates, treasuries continue to benefit from haven demand, with futures reaching session highs after the Washington Post reported a White House proposal to impose tariffs of around 20% on most imports. Additional support comes from steeper gains for bunds after euro-area inflation eased further toward the European Central Bank’s 2% target, and declines for S&P 500 futures. US yields are 2bp-4bp richer across maturities with gains led by intermediates, flattening 2s10s spread by around 2bp; 10-year is on session lows around 4.165% with bunds and gilts outperforming by 3bp and 2.5bp in the sector. European government bonds are broadly higher with UK and German 10-year borrowing costs falling 6 bps each. Traders have added to their ECB and BOE interest-rate cut bets, although there was little reaction to euro-area CPI data – the headline matched forecasts while the core rate slowed slightly more than expected. US session includes March US manufacturing PMIs from S&P Global and ISM.

In commodities, spot gold adds $10 to $3,133 having notched another record high earlier near $3,150. WTI is steady near $71.50 a barrel. Bitcoin rises over 2% to above $84,000.

Today’s US economic calendar includes March final S&P Global US manufacturing PMI (9:45am), February construction spending, JOLTS job openings and March ISM manufacturing (10am) and Dallas Fed services activity (10:30am). ed speaker slate includes Richmond Fed’s Barkin discussing monetary policy and the economic outlook (9am).

Market Snapshot

- S&P 500 mini -0.5%

- Nasdaq 100 mini -0.4%

- Russell 2000 mini +0.1%

- Stoxx Europe 600 +1.2%, DAX +1.5%, CAC 40 +0.9%

- 10-year Treasury yield -3 basis points at 4.18%

- VIX +0.1 points at 22.39

- Bloomberg Dollar Index little changed at 1274.63

- euro little changed at $1.0806

- WTI crude -0.3% at $71.23/barrel

Top Overnight News

- The US plans to extend the 2017 tax cuts, making them permanent and adding Trump’s campaign promises like eliminating taxes on tips, overtime pay and Social Security, Treasury Secretary Scott Bessent told Fox News. BBG

- Howard Lutnick may withhold Chips Act grants to push companies to expand their US projects, people familiar said. Lutnick aims to generate tens of billions of dollars in additional investment commitments without increasing the size of federal grants. Donald Trump created a new office to manage the Chips Act’s funds and speed up some investments in the US. BBG

- President Trump signed an executive order establishing the United States Investment Accelerator which establishes an office within the Department of Commerce meant to facilitate and accelerate investments above USD 1bln in the US, while the White House said the Investment Accelerator is to administer the CHIPS program office.

- Trump signed an executive order aimed at protecting fans from ‘exploitative ticket scalping’ and reforming the US live entertainment ticketing industry, according to Reuters.

- Republicans could be poised to deal a symbolic blow to President Donald Trump’s trade policy, with several GOP senators indicating they planned to join Democrats in a Tuesday vote to block blanket tariffs on Canada (although the bill will probably never become law). Politico

- President Trump said that he had settled on a plan for his latest batch of tariffs expected this week but didn’t reveal what he had decided, after his economic team struggled to coalesce around a remade U.S. trade strategy. He wants to both raise revenue with tariffs and use them as leverage to get other nations to lower their own duties, or make other policy changes.

- Boeing (BA) slows the production of 737 Max to 31 craft per month (current 38) to keep from derailing the assembly line, via Air Current; further slowing wing production.

- Eurozone CPI for Mar comes in a bit cooler than anticipated on a core basis (+2.4% vs. the Street +2.4% and down from +2.6% in Feb) while headline was inline at +2.2% (down from +2.3% in Feb). BBG

- The European Union said it will use a broad range of options to retaliate against the US if President Donald Trump follows through on his threat to impose so-called reciprocal tariffs on the bloc this week. “We do not necessarily want to retaliate,” European Commission President Ursula von der Leyen said on Tuesday. “If necessary we have a strong plan to retaliate and will use it.” BBG

- China’s factory activity expanded at its fastest pace in four months in March, buoyed by stronger demand and robust export orders, a private-sector survey showed on Tuesday. The Caixin/S&P Global manufacturing PMI climbed to 51.2 in March from 50.8 in the previous month, surpassing analyst expectations of 51.1. The 50-mark separates growth from contraction. RTRS

- China has kicked off large-scale military and coastguard exercises around Taiwan, the latest round in Beijing’s escalating campaign to assert its claims of sovereignty and suppress the island nation’s efforts to preserve its de facto independence. The drills on Tuesday came as Taiwan’s President Lai Ching-te seeks to improve military and civilian preparedness for a potential Chinese attach and strengthen society to defend against espionage and other infiltration from China, which last month he called a “hostile foreign force.” FT

- China, Japan and South Korea agreed to jointly respond to U.S. tariffs, a social media account affiliated with Chinese state media said on Monday, an assertion Seoul called “somewhat exaggerated”, while Tokyo said there was no such discussion. The state media comments came after the three countries held their first economic dialogue in five years on Sunday, seeking to facilitate regional trade as the Asian export powers brace against U.S. President Donald Trump’s tariffs. RTRS

Tariffs/Trade

- US President Trump said we will see tariff details maybe Tuesday night or on Wednesday which are going to be nice in comparison to other countries and in some cases, they may be substantially lower. Trump also stated that many countries have been looting the US and they will stop that on April 2nd, as well as noted there will be investments worth USD 5tln in the US. Furthermore, he stated that TikTok is not tied to a larger tariff deal but could be.

- US Treasury Secretary Bessent said President Trump will announce reciprocal tariffs at 15:00EDT/20:00BST on Wednesday.

- US automakers seek to exclude low-value car parts from tariffs, according to Bloomberg.

- US State Department said Secretary of State Rubio spoke to his Mexican counterpart regarding the US automobile industry, while Rubio thanked Mexico for efforts to reduce illegal immigration and continuing to accept deportation flights.

- China’s Foreign Minister Wang Yi said higher US tariffs on Chinese goods are unreasonable and harm global markets.

- UK Trade Secretary Reynolds says, “we are hopeful that Trump’s tariffs will be reversed within weeks, or months”; adds, “It appears tomorrow there’ll be no country in the world exempt from the initial announcements”, via BBC Breakfast.

- EU Commission President von der Leyen says the bloc has the power to push back against US tariffs; all instruments are on the table for countermeasures; EU is open to negotiations on trade. Says EU needs to take down the remaining barriers in the single market. Adds, EU has a strong plan to retaliate if necessary and will use it.

- UK PM Starmer says discussions on an economic deal with the US are “well advanced”.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly higher as markets recovered from the recent sell-off and with sentiment helped by data releases although gains were capped as tariff uncertainty persists heading into April 2nd ‘Liberation Day’ reciprocal tariffs. ASX 200 advanced with broad gains seen across sectors, while there was a muted reaction to the RBA rate decision in which the central bank maintained the Cash Rate at 4.10% as unanimously forecast and provided little clues for future policy. Nikkei 225 rallied at the open after data showed a decline in the Unemployment Rate and a mostly better-than-expected Tankan survey although the index then pulled back and gradually reversed the gains after failing to sustain a brief reclaim of the 36,000 level. Hang Seng and Shanghai Comp were underpinned after stronger-than-expected Chinese Caixin Manufacturing PMI data.

Top Asian News

- Some Chinese banks have reportedly started raising interest rates amid growing bad consumer loans, weeks after cutting rates, according to Reuters sources; the move is expected to weigh on Beijing’s efforts to stimulate the economy

- RBA kept the Cash Rate unchanged at 4.10%, as expected, while it stated the outlook remains uncertain, underlying inflation is moderating and sustainably returning inflation to target is the priority. RBA noted that monetary policy is well placed to respond to international developments if they were to have material implications for Australian activity and inflation, and noted that the board’s assessment is that monetary policy remains restrictive. Furthermore, it stated the continued decline in underlying inflation is welcome, but there are nevertheless risks on both sides and the board is cautious about the outlook, while the board needs to be confident that this progress will continue so that inflation returns to the midpoint of the target band on a sustainable basis.

- RBA Governor Bullock said in the post-meeting press conference there is a chance of more strength in the economy than seems and the board will continue to look at the data, while she said the board did not discuss a rate cut and holding rates was a consensus decision. Bullock also stated they have to be careful not to get ahead of themselves on policy and that the board has not made up its mind on a May move, while she said they are not endorsing the market path on future rate cuts. Furthermore, she said the board did not open the door to a May rate cut and there is more economic data to come, as well as updated forecasts for the May meeting.

- RBNZ said the Board is in the process of preparing a recommendation for the appointment of a Governor for six months and will be sending it to the minister soon, while it continues business as usual with Deputy Governor Christian Hawkesby as acting Governor and CEO until such time the minister makes an appointment.

European bourses (STOXX 600 +0.9%) are entirely in the green, as the region recovers from the prior day’s hefty losses. Indices have gradually climbed higher as the morning progressed. European sectors hold a strong positive bias, but with no clear outperformer and with gains fairly broad based given the risk tone. Healthcare leads the pack today, lifted by strength in AstraZeneca (+1.5%) after it reported positive trial results for its cholesterol drug, which has boosted hopes of another blockbuster drug. Consumer Products is a little higher today, with clothing brands benefiting in tandem with post-earning strength in PVH (+15.8% pre-market) which beat Q4 analyst expectations.

Top European News

- BoE’s Greene says slack is opening up in the UK labour market, happy with central forecast for inflation, disinflation continues to be underway. There is a risk that productivity growth recovery does not happen as the BoE assumes. Rising UK public inflation expectations are concerning, “I think they remain anchored”. Dollar’s role as a reserve currency could be undermined by the current uncertainty.

- ECB’s Rehn says if the data verifies the baseline, the right reaction in monetary policy should be to cut in April, via Politico

- ECB’s Cipollone says “Digitalisation is driving economic progress and transforming the way we make retail payments”.

FX

- DXY is currently slightly softer but with FX markets broadly in a holding pattern in the run up to Wednesday’s “Liberation Day”. Ahead of which, US President Trump is said to be still deciding which plan he will take for reciprocal tariffs and has been presented with “multiple” tariff plans, according to administration sources cited by FBN’s Lawrence. Today’s US data docket includes JOLTS and ISM Manufacturing.

- EUR is trivially firmer vs. the USD following an indecisive session yesterday whereby markets digested softer-than-expected German inflation data and ECB sources. On the latter, Bloomberg reported that several ECB officials are still wavering on whether to cut interest rates next month.

- USD/JPY has failed to sustain a move above the 150 mark as markets digested mostly better-than-expected data via the latest unemployment and Tankan metrics. USD/JPY has delved as low as 149.51 but is some way off Monday’s trough at 148.69.

- GBP is flat vs. the USD with fresh macro drivers for the UK on the light side aside from non-incremental comments from BoE’s Greene that slack is opening up in the UK labour market and disinflation is continuing. Elsewhere, UK PM Starmer noted that discussions on an economic deal with the US are “well advanced”. Cable is currently holding above the 1.29 mark and within yesterday’s 1.2885-1.2972 bounds.

- Antipodeans are steady vs. the USD with little sustained follow-through from the RBA rate decision. As expected, the RBA held the Cash Rate at 4.1% as unanimously forecast and provided little clues for future policy. In the follow-up press conference, Governor Bullock noted the board did not discuss a rate cut – which did help to lift the Aussie slightly.

- PBoC set USD/CNY mid-point at 7.1775 vs exp. 7.2606 (Prev. 7.1782).

Fixed Income

- USTs are firmer, and while the move is significant on the session, USTs are yet to surpass the top-end of yesterday’s 111-04 to 111-22+ band. Overall, the narrative remains much the same as markets countdown to “Liberation Day” and await any possible announcements/details on the eve of it. Ahead of that, traders will await US ISM Manufacturing PMI and JOLTS data.

- A similar narrative to USTs with Bunds firmer and at a 129.42 peak but shy of Monday’s 129.59 best. If that is surpassed, resistance features at 130.00 before 130.93 from mid-January. The bid this morning in EGBs, and fixed generally, comes as the market is seemingly, for now at least, more concerned with the growth implications than the inflation implications of the looming US measures. Tariffs/trade aside, the morning has seen modest downward revisions to March’s Manufacturing PMIs – though this move was not sustained. And on the inflation front, EZ HICP printed in-line on the headline and cooler than expected for the core and super-core Y/Y. Additionally, the Services Y/Y figure moderated to 3.4% (prev. 3.7%) – despite the cooler figures, a hawkish move was seen.

- Gilts are bid but, unlike its peers above, has managed to eclipse Monday’s 92.10 high to a 92.45 peak for the week. A level which encounters resistance from earlier in the month at 92.46, 92.48 and 92.56. Newsflow has unsurprisingly been focused on tariffs, with reports indicating that the UK-US trade deal has broad agreement and is ready to be signed once a few details are ironed out. Commentary from BoE’s Greene has had little impact on UK-paper.

- Germany sells EUR 3.418bln vs exp. EUR 4.5bln 2.20% 2027 Schatz: b/c 3.5x (prev. 2.4x), average yield 2.01% (prev. 2.22%), retention 24.04% (prev. 22.29%)

Commodities

- A choppy session for the crude complex this morning. Price action was initially downward, giving back some of the prior day’s upside, but recent CPC pipeline related newsflow has sparked a paring of this pressure and lifted the benchmarks marginally into the green . Reuters reported that Kazakhstan will have to start reducing oil production within days as CPC pipeline reduces intake. WTI May resides in a USD 71.27-71.75/bbl range while Brent June sits in a current USD 74.58-75.02/bbl parameter.

- Mixed trade across precious metals with spot gold continuing to hold near record highs, whilst spot silver is subdued and spot palladium coat-tails the gains across the Auto sector this morning. Spot gold currently resides in a USD 3,120.12-3,149.09/oz range.

- Mostly firmer trade across base metals, with the complex buoyed by the better-than-expected Chinese Caixin Manufacturing PMI data overnight which bodes well for the demand side of the equation. 3M LME copper currently trades in a narrow USD 9,712.40-9,794.00/t range.

- Kazakhstan will have to start reducing oil production within days as CPC pipeline reduces intake, according to Reuters citing multiple sources; CPC repairs will take more than a month, according to a singular source.

- Russian oil product exports from Black Sea Port of Tuapse planned at 0.864mln tons in April (prev. scheduled 0.798mln tons in March).

- Norway’s Gassco sees higher gas deliveries Y/Y this summer due to less maintenance.

Geopolitics: Middle East

- Israeli military said it attacked a Hezbollah target in Beirut’s southern suburbs.

- Iran complained to the UN about reckless and belligerent remarks by US President Trump and said the remarks are a flagrant violation of international law and core principles of the UN Charter, according to a letter seen by Reuters. Iran said it is deeply regrettable and concerning that the US wields military power as its primary tool of coercion to advance political and geopolitical objectives, while it warned it will respond swiftly and decisively to any act of aggression or attack by the US or Israel against its sovereignty, territorial integrity or national interests.

Geopolitics: Ukraine

- Ukraine’s Foreign Minister says one round of consultations with the US has taken place on the new draft of the minerals deal, the process continues, the text entails strong presence of American business in Ukraine, which contributes to security.

- US President Trump said he wants to see Russian President Putin make a deal and wants to make sure Putin follows through, while Trump added he doesn’t want to do secondary tariffs but noted secondary tariffs are something that he would do if Putin doesn’t do the job.

- Russia Defence Ministry says Ukraine continues its attacks on Russia’s energy infrastructure, via Interfax; Ukraine attacked Russia’s energy infrastructure twice in the last 24hrs.

Geopolitics: China

- Chinese military conducted joint army, navy and rocket force exercises around Taiwan, while it stated that sinister moves of Taiwan separatists will cause disaster for themselves and called Taiwan President Lai a parasite in a video related to the drill.

- Taiwan senior officials noted that more than 10 Chinese military ships approached close to Taiwan’s 24 nautical mile contiguous zone on Tuesday morning and Taiwan dispatched its own warships to respond, while Taiwan’s presidential official strongly condemned China’s military drills and said China is widely recognised by the international community as a troublemaker.

- De facto US embassy in Taiwan said it is closely monitoring China’s military activity near Taiwan and that China has shown that it is not a responsible actor and has no problem putting the region’s security and prosperity at risk. It also stated the US will continue to support Taiwan in the face of China’s military, economic, informational, and diplomatic pressure campaign.

Geopolitics: Other

- US President Trump responded that there is communication when asked about North Korea and commented that he will probably do something on North Korea.

- US Secretary of State Rubio said the US is taking steps to impose visa restrictions on Chinese officials substantially involved in policies related to access for foreigners to Tibetan areas.

US Event Calendar

- 9:45 am: Mar F S&P Global U.S. Manufacturing PMI, est. 49.85, prior 49.8

- 10:00 am: Feb Construction Spending MoM, est. 0.3%, prior -0.16%

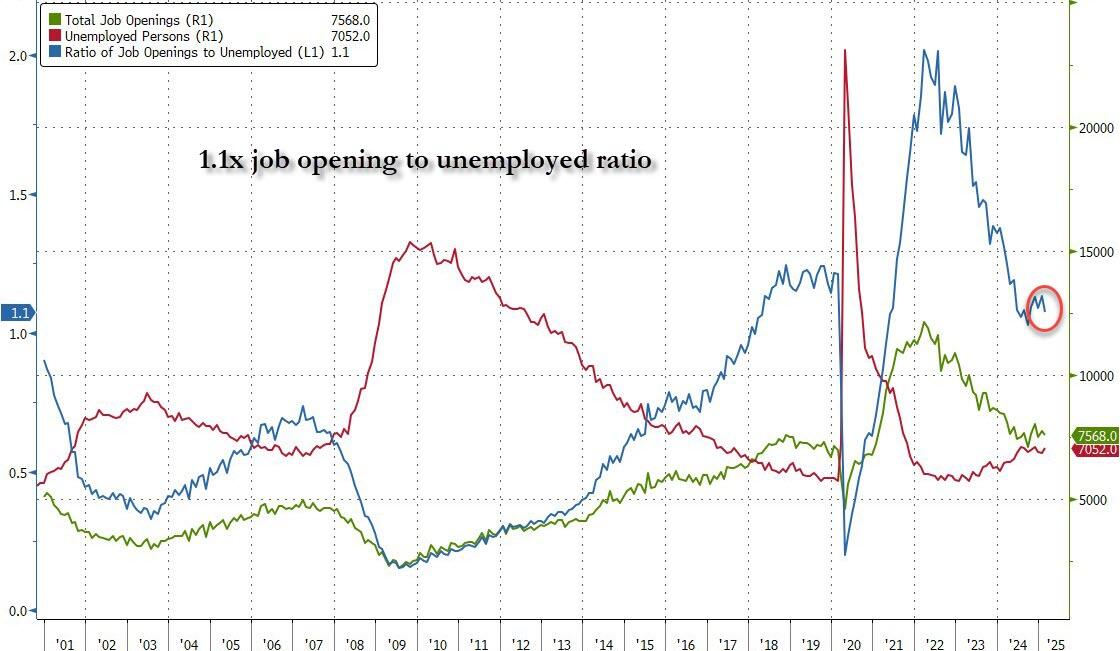

- 10:00 am: Feb JOLTS Job Openings, est. 7655k, prior 7740k

- 10:00 am: Mar ISM Manufacturing, est. 49.5, prior 50.3

- 10:00 am: Mar ISM Prices Paid, est. 64.6, prior 62.4

DB’s Jim Reid concludes the overnight wrap

Happy April Fools’ Day. I could make up a wild story here but it might be boring relative to realities these days. Having said that, 15 years ago today I went on a first date with my wife. I think she now thinks that there has been a decade and a half long April Fools’ joke at her expense. So thoughts are with her this morning.

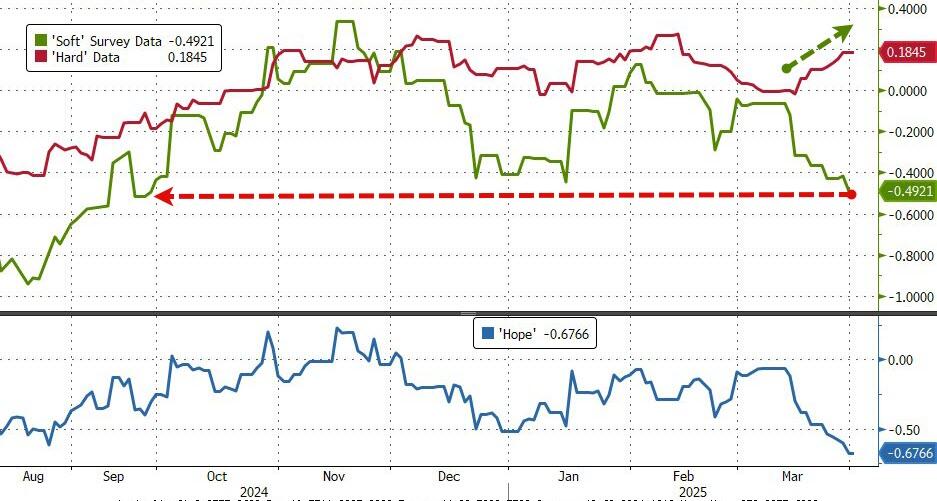

For US markets Q1 seemed like a bad joke as the rest of the world left it behind in equity terms. Henry will soon be releasing our regular performance review, running through how different assets fared over the quarter just gone. It’s fair to say it was a historic period for markets, as the combination of US tariffs, the European fiscal shift, and DeepSeek’s AI model led to a huge reappraisal about the near-term outlook. Indeed, the S&P 500 has just posted its worst month in two years. However, European equities did very well by comparison, with the DAX up +11.32% YTD thanks to the fiscal impulse. And given the general risk-off tone and stagflationary fears, gold put in its best quarterly performance since 1986. See the full review in your inboxes shortly.

Some of those Q1 trends did reverse yesterday amid a jittery quarter-end session as investors await the US reciprocal tariffs announcement tomorrow. The S&P 500 recovered from -1.65% down shortly after the open, when it was briefly back in correction territory, to close +0.55% higher, while the STOXX 600 (-1.51%) fell to a two-month low. On the US side there must have been some quarter end flows that made a difference, especially as US equity futures are back down nearly half a percent this morning.

The losses for the STOXX 600 means that it has now unwound over half of its YTD gains, having risen +5.18% since the start of the year, though it is still way ahead of the S&P 500’s -4.59% decline. And even as US equities outperformed, the gains for the S&P were led by defensive sectors with consumer staples (+1.63%) leading the way. By contrast, the Magnificent 7 (-0.41%) moved lower, while the VIX (+0.62pts) rose for a fourth consecutive session, reaching a two-week high of 22.28. And over in Japan, yesterday saw the Nikkei fall -4.05%, marking its biggest daily decline since September. This morning it’s given up most of its attempts to rally back and is only just above flat.

In terms of the upcoming tariff announcement, we still don’t know which countries they’ll be imposed on and what rate. It’s fair to say that the administration might not have the final plan ready as yet. Yesterday, White House Press Secretary Leavitt said a planned Rose Garden announcement would feature “country-based” tariffs, with further sectoral duties to come later, while last night Treasury Secretary Bessent said on Fox News that Trump will announce the reciprocal tariffs at 3pm EST on Wednesday. Bessent also said that he was working with Republicans in Congress to deliver Trump’s fiscal campaign promises, including “No tax on tips, no tax on Social Security, no tax on overtime”.

A big concern for investors is that the US tariffs will be met by retaliatory moves, which in turn could lead to a further round of escalation as the US seek to respond. So that’s meant inflation expectations have continued to rise, with the 1yr US inflation swap (+13.3bps) yesterday hitting another two-year high of 3.25%. Other traditional inflation hedges have done well on the back of that, with gold prices (+1.24%) moving up to another record high of $3,124/oz. And matters weren’t helped yesterday by a fresh rise in oil prices, with Brent crude (+1.51%) moving up to a one-month high of $74.74/bbl. So collectively, that’s served to exacerbate existing concerns about inflationary pressures.

Those losses cascaded across global markets, and mounting fears of a US downturn led to a fresh decline in Treasury yields. For instance, the 2yr yield (-2.8bps) fell back to 3.89%, whilst the 10yr yield (-4.3bps) fell to 4.21% with a further -1.15bps fall in Asia so far. That came as investors dialled up the likelihood of Fed rate cuts over the rest of the year, with the amount priced in by the December meeting up +2.7bps on the day to 76bps. Those declines in yields would have been even greater were it not for the move up in inflation expectations, as the 2yr real yield (-4.5bps) hit a two-and-a-half year low of 0.60%.

Over in Europe, sovereign bonds had initially rallied as well, but those moves were pared back after Bloomberg reported that ECB officials were questioning whether they should cut rates again at the next meeting. They’ve already delivered 150bps of easing since last June, but inflation is still lingering slightly above target, and the article said that policymakers were thinking about a pause given the uncertainty over tariffs and higher military spending. There was no sourcing in the article so its not clear it was anything other than observing the facts as they stand. Regardless of this, yields on 10yr bunds (+1.0bps), OATs (+2.1bps) and BTPs (+1.9bps) had all moved slightly higher. An April cut by the ECB was 73% priced by the close, having been at nearly 90% early in the session but falling as low as 65% after the Bloomberg story broke.

Earlier in the day, we also had the latest inflation data from Germany, where the EU-harmonised print surprised on the downside at +2.3% (vs. +2.4% expected). That followed last week’s releases showing downside surprises in France and Spain, so those collectively pointed on the downside. However, the Italian reading yesterday was stronger than expected, moving up to +2.1% (vs. +1.8% expected), so that pointed in the other direction. We’ll get the Euro Area-wide numbers today, so that’ll be an important input for the ECB’s next decision in just over two weeks’ time.

Staying on Europe, there was significant political news out of France, as the National Rally’s Marine Le Pen was given a five-year election ban after being convicted of embezzling EU funds. That means she wouldn’t be able to run in the next presidential election in 2027, but Le Pen’s lawyer said that she’ll appeal the verdict. Later in the evening, Le Pen criticised the ruling as a “political decision”, saying she would fight for the right to run for President.

Asian equities are recovering this morning after Wall Street’s overnight gains but performance is mixed. Across the region, the KOSPI (+1.89%) is leading gains with the Hang Seng (+1.06%) also trading notably higher. Elsewhere, the Nikkei’s (+0.20%) recovery is disappointing after yesterdays -4.05% rout where it hit a six-month low. The S&P/ASX 200 (+0.92%) is also trading higher after the RBA decided to leave rates unchanged while Chinese equities are edging higher with the CSI (+0.29%) and the Shanghai Composite (+0.59%) both trading in the green as China’s factory activity beat forecasts (more below). S&P 500 (-0.40%) and NASDAQ 100 (-0.45%) futures are moving back lower.

As was widely expected, the RBA left the Official Cash Rate (OCR) unchanged at 4.1% at the conclusion of the April monetary policy meeting this morning. In an accompanying statement the central bank sounded cautious about the outlook and reiterated that returning inflation sustainably to target remains the highest priority, thus failing to give clarity on when the next rate cut might arrive. Attention now turns to the next two-day meeting on 19-20 May, where markets expect a second cut after February’s 25bps cut, which was the first reduction since late 2020.

Coming back to China, manufacturing activity grew more than expected to a four-month high as the Caixin manufacturing PMI hit 51.2 in March (v/s 50.6 expected) due to a sustained rise in new orders. It follows the prior month’s reading of 50.8. The Caixin data comes after the official PMI over the weekend, which showed the manufacturing sector grew a bit more than expected in March.

To the day ahead now, and US data releases include the ISM manufacturing for March, and the JOLTS report for February. Elsewhere, we’ll get the global manufacturing PMIs for April, the Euro Area flash CPI print for March, and the Euro Area unemployment rate for February. Central bank speakers include ECB President Lagarde, and the ECB’s Vujcic, Cipollone and Lane, along with the Fed’s Barkin and the BoE’s Greene. And in the political sphere, there are two special elections taking place for the US House of Representatives in Florida.