Authored by Lance Roberts via RealInvestmentAdvice.com,

Decades of data across global markets reach the same verdict: the more frequently retail traders trade, the worse they perform. The infrastructure has never been more inviting. The losses have never been more documented. Here are some key statistics we will dive into further.

Retail traders have never had it so easy. Zero commission platforms, options on your phone, social media feeds full of “10 bagger” tips, and a Reddit thread for every stock in the S&P 500. The infrastructure for frequent trading has never been more frictionless, more democratized, or more psychologically seductive.

And the evidence is overwhelming that it is destroying investor wealth at scale.

The data is not subtle. It is not marginal underperformance that can be dismissed as noise. Across decades of academic research, multiple global markets, and every asset class retail traders favor, from stocks to complex options, the conclusion is remarkably consistent: the more frequently retail traders trade, the worse they perform. Not slightly worse. Dramatically, often catastrophically, worse.

The Behavioral Gap Is Growing

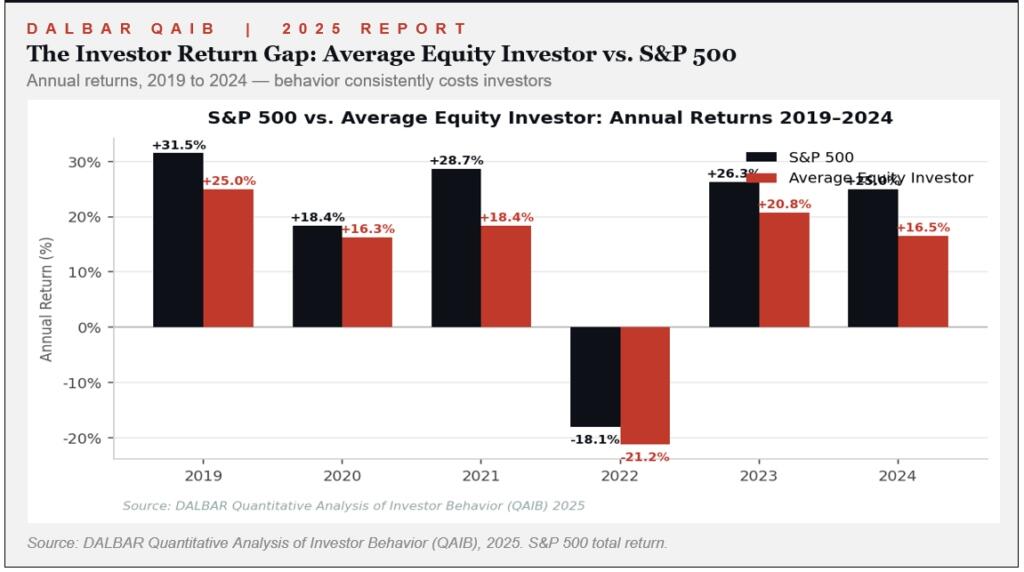

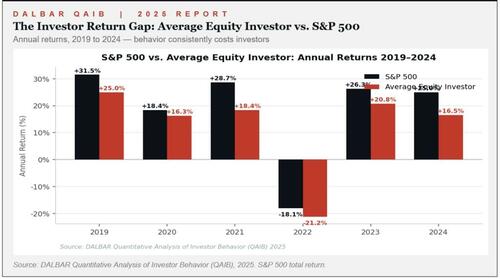

Every year, DALBAR publishes its Quantitative Analysis of Investor Behavior, the most comprehensive long-term study of how retail investors actually perform versus the benchmarks they chase. The 2025 report covering 2024 returns delivered yet another indictment.

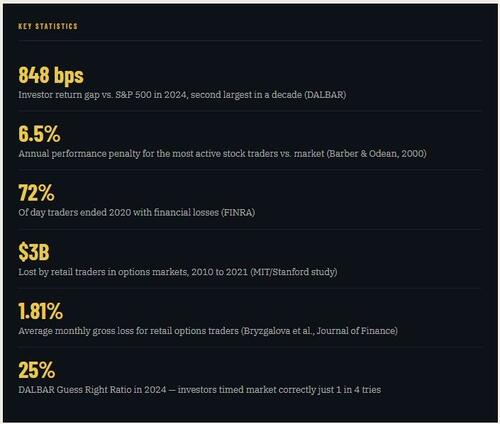

The average equity investor earned 16.54% in 2024. The S&P 500 returned 25.02%. That 848-basis-point shortfall was the second-largest investor performance gap of the past decade. In one of the strongest bull markets in recent memory, retail traders left nearly a third of available returns on the table. And 2024 was not an anomaly. Retail traders have now underperformed the S&P 500 for 15 consecutive years.

DALBAR’s “Guess Right Ratio,” meaning how frequently investors correctly time their entries and exits, fell to just 25% in 2024, tying a record low. Retail traders got market direction right just once out of every four times. And yet, the urge to act, reposition, and trade around every headline only intensified.

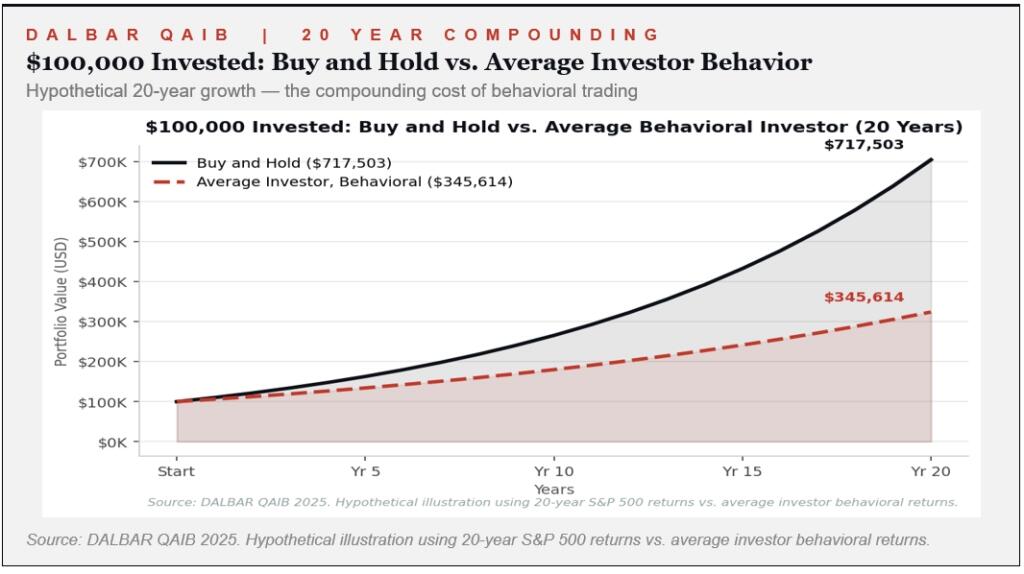

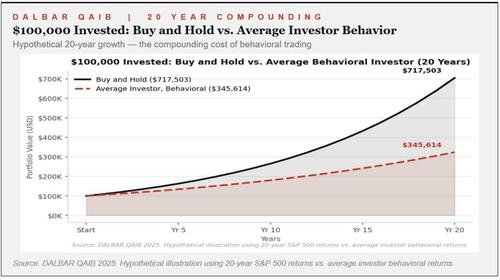

The compounding consequences are brutal. A hypothetical buy and hold investor who started 2024 with $100,000 in the S&P 500 finished the year with $125,020. The “average” investor, mimicking the behavioral cash flows DALBAR tracks, ended with $112,774, over $12,000 less in a single calendar year, simply from repositioning at the wrong times. Extended over twenty years, that same $100,000 left untouched in the S&P would have grown to $717,503. The average behavioral investor ended up with $345,614, forfeiting more than half their potential wealth, not to the market, but to their own decisions.

The Hazardous Truth About Stock Trading Frequency

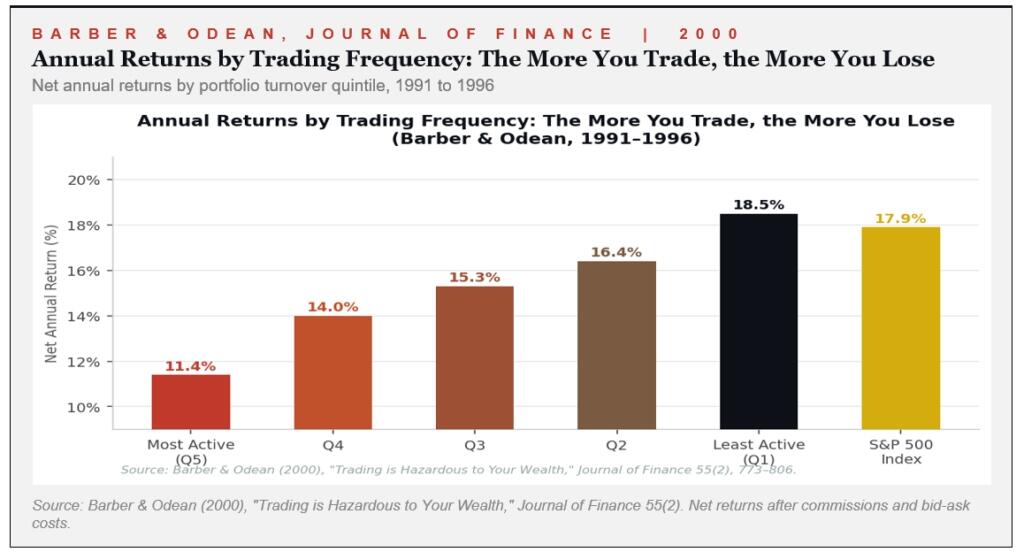

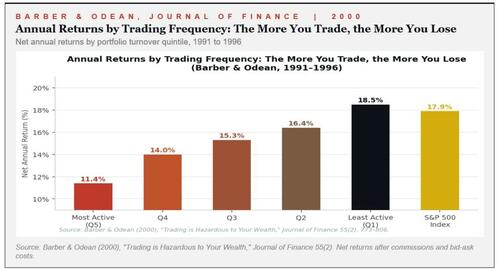

The academic literature on trading frequency and performance is unambiguous, and it dates back decades. The landmark 2000 study by Professors Brad Barber and Terrance Odean, “Trading is Hazardous to Your Wealth” (Journal of Finance), analyzed 66,465 household brokerage accounts from 1991 to 1996. Its central finding was stark: retail traders who traded most aggressively earned an annual return of just 11.4%, while the market returned 17.9%. That is a 6.5 percentage point annual performance drag attributable entirely to excessive trading.

Even the average household in the study, turning over 75% of its portfolio every year, still earned 1.5 percentage points less than a simple buy-and-hold strategy. The gross returns were nearly identical across groups. All the destruction happened after transaction costs and the accumulated impact of poorly timed decisions. Overconfidence was the root cause Barber and Odean identified. Retail traders consistently overestimated their informational edge, leading them to trade when sitting still would have served them far better.

Subsequent research confirmed the finding globally. A study of the Colombian Stock Exchange covering 5.38 million trades by over 42,000 individual investors from 2006 to 2016 found that retail investors generated negative abnormal returns of 4% to 4.4% per year, before transaction costs. The most active traders performed the worst, even on a gross basis. The problem is not just the cost of trading. It is the trading itself.

Day Trading: Where Retail Traders Go to Lose Everything

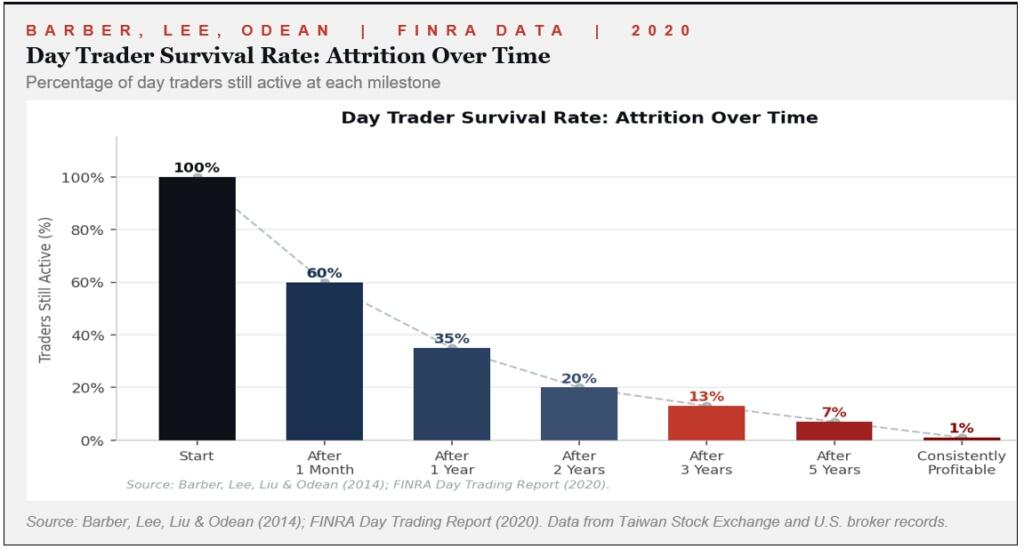

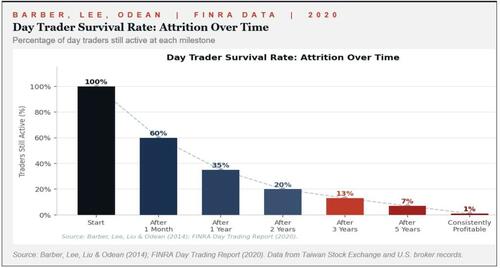

If frequent stock trading is hazardous, day trading is in a category of its own. FINRA data from 2020 showed that 72% of day traders ended the year with financial losses. Among proprietary traders, those treating it as a professional business, only 16% were profitable. A mere 3% earned more than $50,000 for the year.

The survival statistics are equally grim. 80% of day traders quit within the first two years. Nearly 40% abandon it within one month. After three years, only 13% remain active. Only 1% of day traders maintain consistent profitability over a five-year horizon.

The most comprehensive single market study, a 2020 examination of Brazilian equity index futures traders who persisted for more than 300 trading days, found that 97% lost money. Only 1.1% earned more than Brazil’s minimum wage, and all of them experienced substantial volatility. No survivorship bias. Every trader who tried was measured over an extended period.

Retail traders, undeterred by the data, have gotten more aggressive since COVID. Post-pandemic research found that poor market timing, which cost investors roughly 0.53% per year before 2020, nearly doubled to 1.01% per year since. The explosion in retail participation, fueled by social media and zero-commission apps, has not produced better outcomes. It has produced worse ones.

Options: A Wealth Destruction Engine

If day trading is a casino, retail options trading is the casino where the house advantage is structural, invisible, and relentless. The research here is particularly damning.

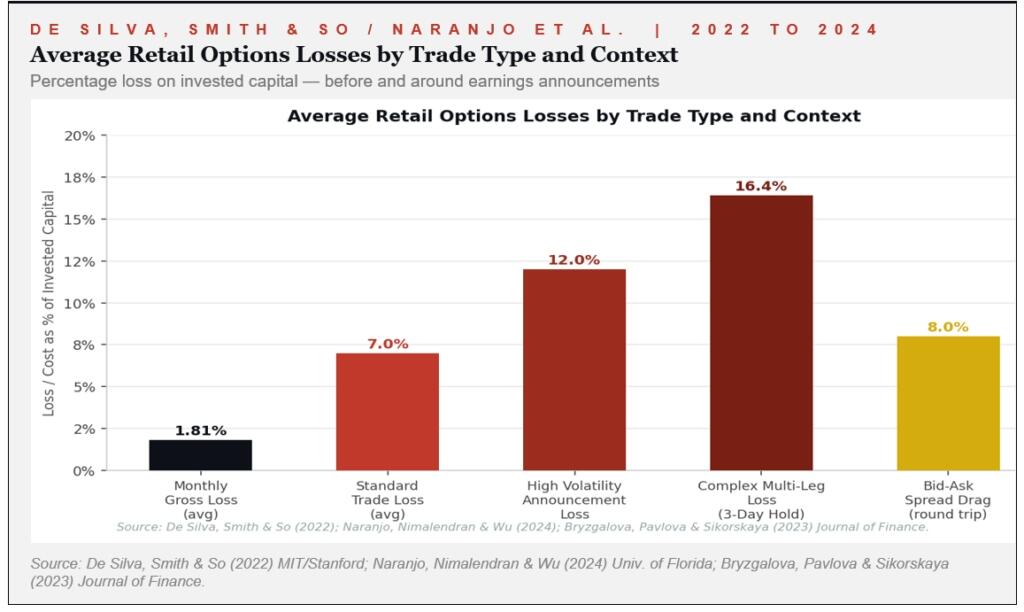

A landmark study by de Silva, Smith, and So (“Losing is Optional,” MIT Sloan and Stanford, 2022) found that retail traders lost approximately $3 billion in options trades over the period from January 2010 through February 2021. Market makers were the primary beneficiaries.

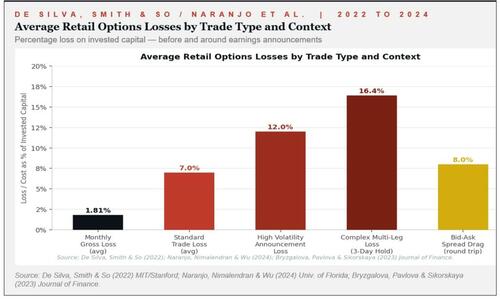

Bryzgalova, Pavlova, and Sikorskaya (Journal of Finance, 2023) calculated that the aggregate retail options portfolio lost $2.1 billion from November 2019 through June 2021 alone, with the bulk of those losses coming not from bad directional calls, but from the cost of trading itself. Retail traders in options incur average gross monthly losses of 1.81%, described by researchers as “economically large and statistically significant.”

The mechanics of the losses fall into three repeating behavioral traps. First, retail traders systematically overpay for options relative to the realized volatility the underlying actually delivers, especially around earnings announcements. Second, they incur bid-ask spreads averaging roughly 8% of the option’s value on a round trip, an immediate structural headwind equivalent to a 9 to 10% drag on invested capital before any directional bet pays off. Third, they hold losing positions well past the point where price decay accelerates after a catalyst passes, sitting on deteriorating contracts as volatility collapses around them.

Since the introduction of zero-commission complex options trading, retail volumes surged by more than 75%. More access did not produce better results. It produced more frequent losing trades.

The Common Thread: Overconfidence

Across every study, every market, and every asset class, the behavioral driver is the same: overconfidence. Retail traders overestimate their ability to predict short-term price movements. Unsurprisingly, they trade more after a strong recent performance, buy into momentum precisely when the easy money has already been made, and sell winners 50% faster than they sell losers. In other words, they confuse activity with skill.

Short-term trading is largely a zero-sum game. For every retail trader who profits, a more sophisticated, better capitalized, algorithmically equipped counterparty sits on the other side. The house advantage embedded in options markets alone, via bid-ask spreads and market maker flow, is the financial equivalent of playing blackjack at a table where the dealer wins on ties.

The antidote is not complicated, even if it is psychologically difficult. Discipline, lower turnover, longer time horizons, and a ruthless focus on what can actually be controlled, including cost, diversification, and behavior, remain the only reliable defenses against the retail trading trap.

Five Tactics to Navigate Risk Without Overreacting

None of the evidence above argues for passivity in the face of market risk. Risk is real, volatility is real, and periods of genuine portfolio danger require thoughtful responses. The problem is not that retail traders care about risk. The problem is that their responses to it, frequent repositioning, speculative options bets, and tactical timing, reliably make outcomes worse rather than better. The following five tactics are designed to keep investors engaged and protected without triggering the behavioral traps revealed by the data.

-

Write a Personal Investment Policy Statement. A written Investment Policy Statement (IPS) is the single most underused tool in retail investing. Furthermore, it forces the investor to commit, before any market stress arrives, to their asset allocation targets, acceptable drawdown thresholds, rebalancing triggers, and the conditions under which they will and will not make changes. When markets fall 15%, and every instinct screams to act, a pre-committed IPS replaces emotion with a predetermined framework. Writing an IPS does not eliminate risk. It eliminates the most dangerous variable in the portfolio, which is the investor’s own unguided reaction to it.

-

Rebalance on a Schedule, Not a Sentiment. Rules-based rebalancing, triggered by calendar dates or percentage drift thresholds rather than market headlines, captures one of the few mechanical edges available to individual investors: it systematically forces buying of what is cheap and trimming of what is expensive. Research from Vanguard and Morningstar consistently shows that disciplined annual or threshold-based rebalancing adds 10 to 50 basis points of return per year over time while materially reducing drawdown severity.

-

Replace Speculative Options with Defined-Risk Structures. For investors who use options, the research is clear about where losses concentrate: in naked or leveraged directional bets, especially around earnings announcements, when bid-ask spreads widen and volatility collapses after the event destroys premium value. Instead, use defined-risk structures, including covered calls on existing long equity positions, protective puts sized to hedge a specific portfolio drawdown threshold, and vertical spreads that cap both gain and loss, to generate a fundamentally different statistical profile.

-

Require a Three-Day Waiting Period Before Any Non-Scheduled Trade. Before executing any trade that is not part of a pre-scheduled rebalance, the investor imposes a mandatory 72-hour waiting period and writes down, in plain language, why they are making the trade, what the exit criteria are, and what price action would tell them they are wrong. Most trades that feel urgent on Monday look considerably less urgent on Thursday. The behavioral literature consistently finds that the speed of a trading decision is inversely correlated with its quality. Slowing the process forces the investor to engage their deliberate reasoning rather than their reactive instincts.

-

Calculate Your Own Behavioral Return Gap Every Year. The exercise is straightforward: take the time-weighted return of each position as if it had been held without any transactions, then compare it to the account’s actual dollar-weighted return, including every buy, sell, and repositioning decision made during the year. The difference is the personal behavioral gap, the exact cost in dollars of every trade made. For most active retail traders, this number is negative and larger than they expect. For some, it represents tens of thousands of dollars in self-imposed performance drag per year. Seeing that number concretely, attached to actual dollars rather than abstract percentages, is the most powerful behavioral intervention available.

The market will always be there tomorrow. The question is whether your capital will be, and whether the decisions you make today will compound in your favor or against you.