Submitted by David Stockman via Contra Corner blog,

There is nothing like the release of secret tape recordings to clarify an inconclusive debate. I recall that happening with Nixon back in the day. Even as a Washington apprentice I could see that he was a ruthless, power hungry abuser of his office, but much of official Washington just denied it. Then came the tapes. Soon there was no doubt. In short order Nixon was gone.

So now comes the Goldman tapes – 46 hours of recordings by an embedded New York Fed regulator at Goldman Sachs who got fired for attempting to, well, regulate. Would that the Carmen Segarra affair generates a Nixonian result – that is, exposure that “regulatory capture” is an endemic, potent and inextricable evil that can’t be remediated in situ.

Never mind that what Ms. Segarra was attempting to regulate–whether Goldman had a conflict of interest policy with respect to its M&A clients—-was actually none of the state’s business in the first place. If in the instant case GS was giving squinty eyed advise to its client, El Paso Corporation, because it owned a $4 billion position in the other party to the transaction, Kinder Morgan, so be it. Either the conflict was harmless or eventually Goldman’s M&A business would have been punished by the marketplace—–even stupid executives and boards wouldn’t pay huge fees to be taken to the cleaners for long.

Actually, what the tapes really show is that the Fed’s latest policy contraption – macro-prudential regulation through a financial stability committee – is just a useless exercise in CYA. Apparently, even the colony of the bubble blind which inhabits the Eccles Building has started to get nervous about financial bubbles and instability in recent months. What with junk bond yields sporting a 5 handle, the Russell 2000 trading at 80X reported profits and the IPO market having gone full-tilt manic with last week’s pricing at 27X sales of a Chinese e-commerce mass merchant that is a pure proxy for the greatest credit fueled house of cards in human history—-it needed to show some gesture of concern.

Now, it might have gone straight to the horse’s mouth. It might have asked about 70 consecutive months of zero money market rates, for instance, and the manner in which that has enabled speculators to mount massive momentum trades everywhere in the financial markets by funding any “risk asset” that generates a yield or a short-run gain with nearly zero cost options or repo. Or it might have inquired about the destruction of the market’s natural internal mechanisms of stability and financial restraint—-that is, short sellers and two way trading—that has resulted from the Greenspan/Bernanke/Yellen Put; or it might have wondered whether its bald-faced doctrine of “wealth effects” and ever rising stock prices does not in itself create a massive bias toward speculative risking taking and a blind buy-the-dips herd mentality in the casino.

But that would have been inconvenient because it would meant an abrupt end to its labor market focused policy of “accommodation” and a violent hissy fit in the casino. So Yellen and here Keynesian compatriots have invented out of whole cloth a method to drive the wildly vibrating Wall Street financial jalopy with both feet to the floor. That is, on the monetary “policy” side they intend to perpetuate ZIRP for at least another 9 months and near-ZIRP as far as the eye can see , while at the same time interposing in today’s frothy financial markets a Stanley Fischer led posse of regulators to keep speculator exuberance within safe boundaries.

At this point it is not clear which part of the Fed’s “macro-pru” initiative is the more preposterous. Why would you think that a system which required only 9 months to fire Carmen Segarra for comparatively trivial meddling in Goldman’s M&A department is capable of bubble prevention when we are talking about trillions of inflated value in the stock, bond, derivatives and real estate markets? Or that putting a proven serial bubble generator—-that’s essentially what Fischer accomplished during his stint as head of Israel’s central bank—at the head of the financial stability committee would produce, well, financial stability?

It should be evident by now that regulatory capture and the inherent capacity of the marketplace to evade bureaucratic rules, edicts and embedded supervisors mean that “macro-pru” is a crock—an excuse to prolong a dangerous monetary experiment that is inexorably fueling a giant financial bubble and the crash which must inevitably follow.

Take the soaring issuance of sub-prime auto credit, for example, which now accounts for a record 30% of car loans and is putting people in cars at 130% loan-to-value ratios—-borrowers that have no hope of avoiding the repo man a few months down the road. On the margin, nearly all of this explosive growth is being funded in the non-bank market. That is, by freshly minted sub-prime auto lenders who have been given a sliver of equity by LBO houses and a ton of debt by the high yield market. Who is Stanley Fischer going to crack down upon—–the LBO houses creating these fly-by-night lenders, the Wall Street underwriters lead by Goldman who are distributing the junk or Bill Gross’s yield-parched successors at PIMCO and its mutual fund competitors who are buying the stuff?

OK, Stanley Fischer being from MIT, the IMF, Citibank, the Bank of Israel—and to say nothing of his long ago supervision of Ben Bernanke’s PhD thesis which merely Xeroxed Milton Friedman’s false claim that the Fed’s failure to engage in massive QE during 1930-1932 caused the Great Depression—-is too sophisticated to say “no auto junk, period”. What his committee will likely do is issue guidance about keeping debt-to-EBITDA ratios “prudent” at some notional leverage of say 6-8X when these newly minted auto junk yards are issuing the same.

But that’s before the underwriters parade in with a host of complications embedded in “adjusted EBITDA” to account for the fact that two fly-by-night subprime lenders, for example, just merged and therefore need a pro forma adjustment for down-the-road synergy savings; or that a newly minted lender is still scaling up its volume and that on a last month’s run-rate basis, its adjusted EBITDA ratio is 7.8X, not the 16X ratio embedded in its actual GAAP results.

And that doesn’t even account for the fact that the loan books of these start-up auto sub-primes are inherently unseasoned. It does take some time for an assistant night shift manager at a McDonald’s to become the subject of a “restructuring” initiative by the local franchisee and to subsequently default on his car loan. Indeed, the Fischer committee would even be up against the inherently vexing math of a rapidly ramping loan book. That is, while the denominator of loans issued is soaring, the numerator of delinquencies is still lagging. So loan loss reserves are invariably understated during the final blow-off stage of a financial bubble, meaning that earnings and EBITDA are over-stated and hidden leverage risk is rampant. The evidence is there in s

pades in the wreckage of the LBO and high yield markets during 20009-2010.

In short, even assuming that the obsequious culture of accommodation at the New York Fed so evident in the Goldman tapes could be uprooted, macro-pru is inherently impotent because of information asymmetry. What the Austrian thinkers 100 years ago said about socialism in general is true in spades with respect to the gambling casinos created by the Keynesian money printers. Without honest market prices in the trading pits and at loan desks and underwriting syndicates, financial booms and busts are inevitable, and the state’s regulators and supervisors are hopelessly at sea because they cannot hope to gather and process enough information to stymie the army of speculators chasing false prices with cheap credit.

Or to take another example, what is the Fischer committee going to do about leveraged stock buybacks? Not only is this fueling the speculative rise in the stock averages and the illusion that earnings are growing, when in fact it is only the share count which is shrinking, but it is also adding to the dangerous build-up of corporate debt that will become hugely problematic when interest rates are finally allowed to normalize.

But imagine the utter hissy fit that would instantly arise on Wall Street if the Fischer committee was even rumored to be addressing the issue of leveraged stock buybacks. It would generate a violent sell-off of the likes not seen since the House Republicans voted down TARP the first time around.

And then would come the information miasma. Wall Street would trot out the cash on the sidelines canard, arguing there is no problem here because not withstanding the current $700 billion annualized run-rate of buybacks for the S&P 500 alone, there is plenty of cash cushion available to corporate chieftains who wish to invest in their own company’s future— albeit with shareholder money, not theirs.

In truth, of course, the business sector did not delever one wit after the financial crisis. Since the fourth quarter of 2007, business debt in the US has risen from $11 to $14 trillion. That $3 trillion gain dwarfs the $500 billion pick up in business cash balances. In fact, the rise in cash was never a sign of returning financial health in the fist place: it was only a telltale sign that by causing debt to be drastically mis-priced, the Fed was encouraging companies to artificially balloon both sides of their balance sheets.

Yet it would take the Fischer committee months to sort-out the truth and refute the sell-side propaganda—even if it had the will. Meanwhile, the bubble would continue to expand.

So here’s the thing. Our monetary politburo has its ass backwards. Macro-pru is an impossible delusion that should not be taken seriously be sensible adults. It is not, as Janet Yellen insists, a supplementary tool to contain and remediate the unintended consequence – that is, excessive financial speculation – of the Fed’s primary drive to achieve full employment and fill the GDP bathtub to the very brim of its potential.

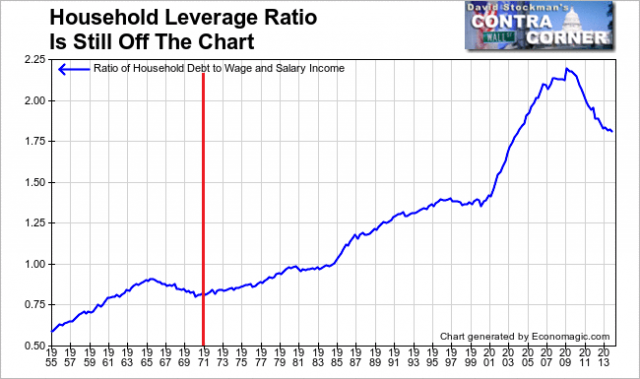

Instead, rampant speculation, excessive leverage, phony liquidity and massive financial instability are the only real result of current Fed policy. We are at peak debt in the household and business sectors of the private economy. Accordingly, the credit channel of monetary transmission is broken and done. Indeed, the modest pick-up in leverage in the household sector has been exclusively among utterly marginal borrowers. That is, among students who are just treading water until the eventual day of default and sub-prime auto borrowers who are actually underwater they day they take out their loans.

No, the central bankers’ one time parlor trick has been played and leverage was ratcheted-up until it reached a peak in 2007-2008. Now the central bankers are pushing on a string.

But even as their liquidity tsunami never escapes the canyons of Wall Street, and, as an empirical matter, circulates right back to excess reserves at the New York Fed, it does have an immense untoward effect during its circular journey. Namely, it causes the most important price in all of capitalism—that is, the cost of overnight money and the speculators’ “carry” on his asset positions—to be drastically mispriced. It turns the central bank into a serial bubble machine.

Not 10,000 Carmen Segarra’s could stop the boom and bust cycle thus manufactured by the money printers ensconced in the Eccles Building. Stanley Fischer’s financial stability committee, therefore, is not merely a pointless farce. Its evidence that the next financial crash is nigh.

via Zero Hedge http://ift.tt/YIfsnz Tyler Durden