Biden: Americans Need To ‘Forgo’ Holiday Traditions This Year Tyler Durden

Thu, 11/26/2020 – 11:40

As Democrat leaders across the country arrogantly ignore their own COVID-19 restrictions (over and over and over), their leader – Joe Biden – has asked Americans to “forgo” holiday traditions this year.

In a monotone Thanksgiving eve address against a yellow “Office of the President Elect” backdrop (an office which doesn’t actually exist), the presumptive president-elect said that every American has “a responsibility” to take coronavirus seriously and ‘redouble our efforts’ to fight the disease.

“This year we are asking Americans to forgo so many of the traditions that have long made this holiday,” said Biden, before urging people to limit travel and practice social distancing to reduce the risk of exposure – noting that he and wife Jill Biden will be spending Thanksgiving with their daughter and son-in-law, while their other children will be doing their own thing “in small groups” (which may include hookers and crack).

“I know how hard it is to forgo family traditions, but it’s so very important.”

Pres.-elect Joe Biden on skipping family’s holiday traditions amid COVID-19 surge: “Because we care so much for each other, we’re going to be having a separate Thanksgiving.” https://t.co/pjEkZJtJGSpic.twitter.com/Z6WzgS1yJA

“I know how hard it is to forgo family traditions,” Biden added. “But it is so very important. Our country’s in the middle of a dramatic spike in cases. We are now averaging 160,000 new cases a day.”

via ZeroHedge News https://ift.tt/39gMrYa Tyler Durden

Disney’s Thanksgiving Present: Another 4,000 Layoffs Tyler Durden

Thu, 11/26/2020 – 11:15

Some four thousands workers woke up this morning thankful for unemployment benefit claims after they received notice they will no longer work at Wall Disney, which quietly continued its massive layoff spree the night before Thanksgiving.

Walt Disney said late on Wednesday it would lay off about 32,000 workers, primarily at its theme parks, an increase of 4,000 from the 28,000 it announced in September, as the company struggles with limited customers due to the coronavirus pandemic. The layoffs will be in the first half of 2021, the company said in a filing with the Securities and Exchange Commission.

Earlier this month, Disney said it was furloughing additional workers from its theme park in Southern California due to uncertainty over when the state would allow parks to reopen.

When the company reported its Q3 results earlier this month, it revealed how the coronavirus pandemic has hammered Disney’s traditional businesses like studios, parks and cruises while accelerating a pivot to streaming. The theme parks showed a loss of $1.1 billion in quarterly results this month, made up for by surging growth in its on-demand video platform Disney+, which smashed subscriber number estimates. Unfortunately, the high margin streaming business employs only a handful of people compared to the hordes of park workers who remain indefinitely redundant.

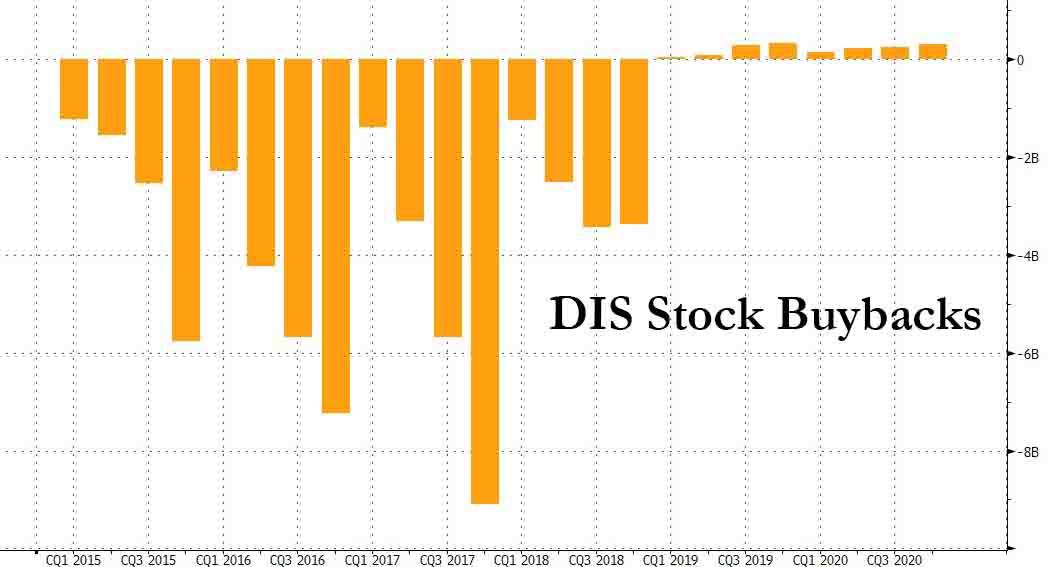

It’s gotten so bad, the company still can’t go back to its stock repurchasing days, when between 2015 and 2018 it would regularly buyback billions in Disney shares (money which it could have saved up and used to, you know, pay its workers during a crisis like now).

Disney’s theme parks in Florida and those outside the United States reopened earlier this year without seeing new major coronavirus outbreaks but with strict social distancing, testing and mask use. However, Disneyland Paris was forced to close again late last month when France imposed a new lockdown to fight a second wave of the coronavirus cases. The company’s theme parks in Shanghai, Hong Kong and Tokyo remain open.

via ZeroHedge News https://ift.tt/3q3lwVH Tyler Durden

“I Humbly Ask For Your Forgiveness” – Yet Another Democrat Leader Busted Breaking His Own COVID Rules Tyler Durden

Thu, 11/26/2020 – 10:50

Update (1330ET): In standard Democrat crisis management mode, the mayor drafted a virtue-signaling statement asking for the peasantry of Denver to forgive him: (emphasis ours)

I fully acknowledge that I have urged everyone to stay home and avoid unnecessary travel. I have shared how my family cancelled our plans for our traditional multi-household Thanksgiving celebration.

What I did not share, but should have, is that my wife and my daughter have been in Mississippi, where my daughter recently took a job. As the holiday approached, I decided it would be safer for me to travel to see them than to have two family members travel back to Denver.

I recognize that my decision has disappointed many who believe it would have been better to spend Thanksgiving alone. As a public official, whose conduct is rightly scrutinized for the message it sends to others…

…I apologize to the residents of Denver who see my decision as conflicting with the guidance to stay at home for all but essential travel.

I made my decision as a husband and father, and for those who are angry and disappointed, I humbly ask you to forgive decisions that are borne of my heart and not my head.

The damage was done, however…

“I decided it would be safer for me to travel to see them than to have two family members travel back to Denver”

How can you be a leader & not get how wrong this is? This is the selfishness that keeps us in this mess & it’s an insult to everyone sacrificing for the greater good. https://t.co/oUk7Eknpwd

I don’t usually jump in when people are apologizing to say “not good enough” but this is a typical “I’m sorry you feel that way.” He’s not sorry he did it, he’s sorry he got caught. https://t.co/oEcIygCVi8

This has got to be one of the lamest, worst, poor excuses of a statement any politician caught with his hand in the cookie jar has ever issued. https://t.co/oUoYcDrDu8

Every small business in Denver that’s been closed should fully reopen right now and say their decision to was made of their heart, not their head. https://t.co/zsMyFnYQzQ

Sorry, no forgiveness here @MayorHancock. No amount of rationalization on your part excuses you’re hypocrisy. If you were truly sorry you’d rent a car and come home. But I doubt you have the cojones to do that. Your apology rings hollow. https://t.co/2xwLC2r2qt

The mayor of Denver is traveling to Mississippi to visit his daughter after urging everyone not to travel for Thanksgiving. This thread boils down to, “I said we all need to sacrifice, but by ‘we’ I meant ‘you’.” https://t.co/9NAls2rY1p

So, as a reminder of the dissonant hypocrisy demanded of the left, we should forgive him his sins “borne of his heart” (‘do as I say, not as I do’) while we ‘cancel’ anyone immediately and forever who thinks white lives matter as much as black lives, anyone who questions the ‘fact’ that boys can be girls if they just think that way, anyone who dares to argue with the efficacy of mask-wearing, oh, and anyone who voted for President Trump.

As Summit News’ Steve Watson detailed earlier, the Democratic Mayor of Denver was caught violating his own COVID travel ordinance, getting on a plane to see family just 30 minutes after decreeing that people should not travel to visit their own relatives.

Pass the potatoes, not COVID.

🏘️Stay home as much as you can, especially if you’re sick.

💻Host virtual gatherings instead of in-person dinners.

❌Avoid travel, if you can.

🍲Order your holiday meal from a local eatery.

🎁Shop online with a small business for #BlackFriday. pic.twitter.com/acQpWs2Ism

“Pass the potatoes, not COVID,” Denver Mayor Michael Hancock tweeted Wednesday, adding “Stay home as much as you can, especially if you’re sick. Host virtual gatherings instead of in-person dinners.”

“Avoid travel, if you can,” the tweet also stated, continuing “Order your holiday meal from a local eatery. Shop online with a small business for Black Friday.”

Denver Mayor Michael Hancock gave you the bird for Thanksgiving. If he doesn’t want to lead, then he shouldn’t. A @nexton9news commentary: pic.twitter.com/kWo0sFngem

The incident adds to the growing list of Democrats who have been caught breaking their own decrees on covid:

And Newsom, Pelosi, Cuomo … hypocrisy from politicians who claim to trust the science isn’t helping to strengthen dire public health messages /pleas from medical professionals and frontline workers.

Just infuriating. https://t.co/haNs3QVnU7

Gavin Newsom wants us suicidal in our bedroom praying to have a familial thanksgiving meal, while the California Governor is caught openly and overtly ignoring his own rules.

For all these petty tyrants, there is only one rule: “obey!”

via ZeroHedge News https://ift.tt/3fCDZDI Tyler Durden

Sweden Unexpectedly Expands QE By 40% Tyler Durden

Thu, 11/26/2020 – 10:25

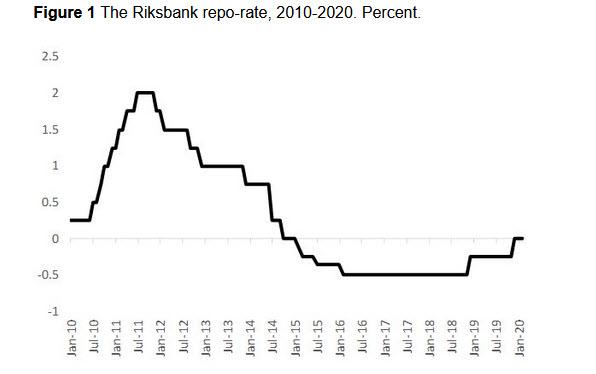

Back in 2017, Sweden made a mistake: the Governor of the Swedish Riksbank, Stefan Ingves, described the use of negative interest rates an “experiment” never tried before, and with inflation in the Scandinavian country surging, he said that the experiment was officially over, with the Riksbank beginning a hiking cycle in late 2018 which pushed the Swedish repo rate back to 0 last December, and making another trip into negative rates virtually impossible without the Riksbank’s reputation suffering a terminal hit.

While the impact of the negative rates on the domestic inflation rate was small (and in fact probably contributed to wholesale deflation as we have shown previously), the effects of negative rates on the housing market – where prices exploded amid the ultra-loose conditions making housing unaffordable, and on household debt levels are large. As a result, imbalances which had already begun to materialize before the Global Crisis have worsened. Real estate prices rose rapidly, contributing to rising wealth inequality (and yes, a central bank was explicitly at fault), while household debt reached record levels. Ironically, even though the exchange rate of the Swedish krona has depreciated by more than 10%, with no major impact on the domestic rate of inflation.

In short, as Professors Fredrik Andersson and Lars Jonung wrote in May, Sweden’s negative rates “created an economy with signs of ‘overheating’. However, this is likely a short-run gain. The Riksbank will face a major challenge to calibrate its policy during the next downturn.”

Their conclusion on Sweden’s negative rates experience was simple: “Don’t do it again!”

There is just one problem: when the Riksbank resumed tightening and pushed rates back to 0%, both its and Europe’s economy were recovering, and it seemed there was limited risk from another contraction. And then the covid pandemic hit, crippling both Europe – which is facing a double dip recession following the latest round of lockdowns – and Sweden’s economy.

And since the world’s oldest central bank could not cut rates again without risking a huge reputational and credibility blow after it triumphantly ended its “negative rates experiment” several years ago, eager to halt the dramatic appreciation in the Swedish Krone which is up more than 6% YTD, the central bank had just one option: expand QE even more.

Which is precisely what the Sweden’s central bank did this morning when it surprised markets with a bigger-than-expected expansion of its asset purchase program, and said there’s room to deliver more stimulus between scheduled meetings. Specifically, the Riksbank announced that it was expanding its quantitative easing program to 700 billion kronor ($82 billion), which is 200 billion kronor more than its earlier target. With economists at SEB predicting a 100 billion-krona QE expansion, while most others expected no change in policy, the krona immediately sank up to 0.5% against the euro although it remains dramatically higher YTD.

Meanwhile, the key interest rate was kept at zero, as expected, and will probably stay there in “the coming years,” the bank said, clearly not willing to risk reversing on its promises to not go back to NIRP.

And since it no longer has the capacity to cut rates “for years” absent a complete economic crash, the Riksbank not only expanded its QE target, but also said it will step up the pace of asset purchases next quarter, as the Executive Board also decided to step up the quarter-on-quarter pace of its purchases during the first quarter of 2021, committing to buy SEK120bn over that quarter, which means QE will only keep rising as long as negative rates remain off the table.

The surprising decision to expand the asset purchase program prompted “reservations” from two Executive Board members advocating for later action: Breman advocated that the program should instead be expanded by SEK100 billion during the second half of 2021; Floden thought that the Riksbank should pledge that monetary policy will remain expansionary as long as necessary without deciding now on purchase sums for the second half of 2021. Their opposition to the QE expansion was duly noted… and ignored.

At the press briefing, Governor Stefan Ingves said the extra 200 billion kronor in QE won’t be put toward reinvestments, but also assured markets that the Riksbank will continue to reinvest in bonds affected by its program.

“If the world changes, if there’s turbulence for various reasons and if we conclude that we need to do something between meetings, we will do so,” Ingves said during a virtual press briefing in Stockholm on Thursday.

As Bloomberg notes, and confirming the above, “Ingves has repeatedly underscored his preference for asset purchases over rate cuts to support the economy. The Riksbank ended half a decade of negative rates almost a year ago, and Ingves has shown a reluctance to delve below zero again, amid financial stability concerns.”

Alas, Sweden shows just what happens when a central bank is virtually out of ammo, and worse – it main policy tool, interest rates, is now limited to the zero lower bound. Meanwhile, the country is now bracing for a dark winter as the pandemic spreads, intensive-care beds fill up and curbs on movement increase. The government has already warned that the next few months will be tougher on the economy than first feared.

Fearing that much worse is yet to come, the Riksbank tried to pretend as if it never said all those bad things about “experimental” negative rates, knowing full well it will have no choice but to go NIRP again, sooner or later. As a result, the Riksbank said the repo rate “can be cut if this is assessed to be an effective measure, particularly if confidence in the inflation target were to be threatened.” The irony, of course, is that years of negative rates did nothing to boost inflation to hit the target; instead what NIRP did is create a massive housing and debt bubble, which the Riksbank scrambled to shortcircuit before everything came crashing down.

And now it faces a dismal dilemma: reflate the biggest asset and credit bubble ever (which even the Riksbank has admitted is it own doing), ensuring that the next crash – when it comes – will be truly devastating, or step back and allow the economy to crumble. Meanwhile, inflation remains well below the Riksbank’s 2% target, coming in at just 0.3% in October.

The Riksbank’s surprise decision to expand its stimulus program came just two weeks before the European Central Bank is expected to unveil more support measures.

“We are neighbors with an elephant and when the elephant moves it affects us,’ Ingves said. “I can’t comment on what they’ll do and in what way, but basically everything the ECB does to keep the euro zone economy running and to bring up inflation is good for Sweden as well.“

“But what they’ll do and how, we’ll have to see further ahead, because we are not party to that decision-making process,” Ingves said.

Well, Stefan, we can tell you: the ECB will almost certainly expand its emergency pandemic QE by hundreds of billions in December, as today’s ECB minutes hinted.

Meanwhile, In Thursday’s statement, the Riksbank cut its forecast for gross domestic product this year and now sees a contraction of 4%, compared with 3.6% previously. The rebound in 2021 will also be smaller than earlier thought, with growth seen at 2.6%, compared with the 3.7% seen earlier.

* * *

But going back to the problem at hand, the Riksbank revised down its growth forecasts to -4.0% (compared to the -3.6% forecast in September) for 2020 and 2.6% (3.7%) for 2021. At the same time, inflation will remain below the bank’s 2% target throughout the forecast period, which extends into 2023. The Riksbank expects unemployment to peak at 9.4% in 2021—a 0.2pp upward revision from the September MPR—before falling back subsequently.

Looking ahead, the MPR reiterated that the “possibility of a repo rate cut cannot be ruled out” although to do that and to crush what little credibility it has left, would require a true economic shock. The Riksbank cited the exchange rate, how fast the supply side of the economy recovers, and the pass-through of the repo rate to interest rates in the broader economy as factors it will consider when assessing the usefulness of an interest rate cut, clearly forgetting its admission as recently as 2018 that NIRP was an “experimental” mistake.

via ZeroHedge News https://ift.tt/3l3Drbe Tyler Durden

US Army Fires Rockets Capable Of Striking Crimea Into Black Sea Tyler Durden

Thu, 11/26/2020 – 10:00

A US Army rocket test in Eastern Europe connected to NATO exercises in Romania has ratcheted tensions with Russia given the close proximity to its border.

The US this week conducted rocket-launch tests of M142 High Mobility Artillery Rocket (HIMARS) vehicles, which had been transferred from Germany.

The rocket test was close enough to Russia for its Defense Ministry to deploy what Russian media described as “advanced hardware” on the Crimean peninsula should it be needed to neutralize any “surprise missile attack.”

M142 High Mobility Artillery Rocket (HIMARS) launchers previously in exercises in Poland, via US Army.

It was also provocative enough for Forbes to introduce the maneuvers in the following way:

The U.S. Army sneaked a pair of long-range rocket launchers near Russia’s Black Sea outpost on Thursday, fired off a few rockets then hurried the launchers back to the safety of their base in Germany. All within a few hours.

The one-day mission by the Army’s new Europe-based artillery brigade was practice for high-tech warfare. It clearly also was a message for Moscow. The U.S. Army in Europe has restored its long-range firepower. And it wants the Russians to know.

According to Russian media reports over 130 NATO soldiers and 30 units of military equipment were involved. The missile salvos were reportedly fired into the Black Sea.

And further according to Forbes, “The [US] brigade’s rapid deployment to Romania last week could prove even more provocative. Especially considering the new munitions the Army is developing for the HIMARS and MLRS. These include an anti-ship missile and a replacement for ATACMS that can travel as far as 310 miles.”

Via NPR

“It’s just 250 miles across the Black Sea from the Romanian coast to Crimea. Army HIMARS flying in and out of Romania pose a serious, and unpredictable, threat to Russian forces in the region,” the report underscores further.

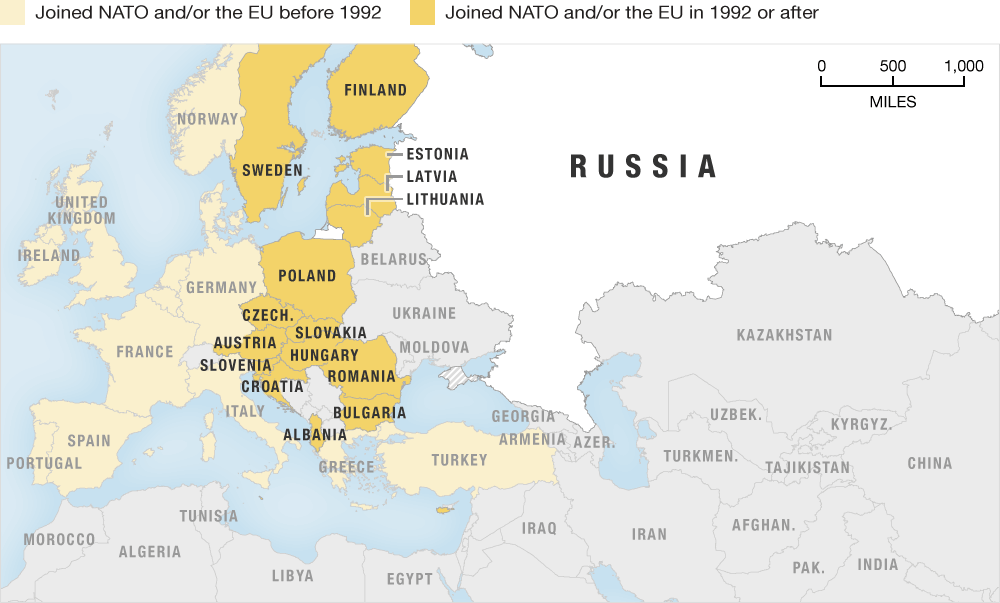

All of this suggests the standoff over both Ukraine and Russia’s 2014 annexation of Crimea (which was done after a popular referendum) is far from over. Further, Russia has long slammed NATO for encroaching right up to its border, violating key agreements from the 1990s after the Soviet Union collapsed.

via ZeroHedge News https://ift.tt/3pXmqmG Tyler Durden

A UK travel agency has announced it will be boycotting Australian airline Qantas over its ‘no vaccine, no flight’ policy, saying travelers should have freedom of choice.

Last week, Qantas CEO Alan Joyce announced the airline would implement a policy barring anyone who has not had the COVID-19 vaccine from using their service.

“We are looking at changing our terms and conditions to say, for international travelers, that we will ask people to have a vaccination before they can get on the aircraft,” he said.

#BREAKING: QANTAS CEO confirms that proof that you’ve been vaccinated for COVID-19 will be compulsory for international air travel onboard his aircraft. #9ACApic.twitter.com/dhk3Hsnxn9

This policy has since been backed up by Australian Prime Minister Scott Morrison, who said passengers who didn’t take the vaccine before entering Australia would be subject to two weeks quarantine.

Other airlines such as Korean Air have also signaled they will require vaccination, while the industry in general appears to be moving towards a digital ‘Common Pass’ that will carry details of vaccination status.

However, the backlash has already begun, with one travel agent in the UK announcing a blanket boycott of Qantas over its vaccine policy.

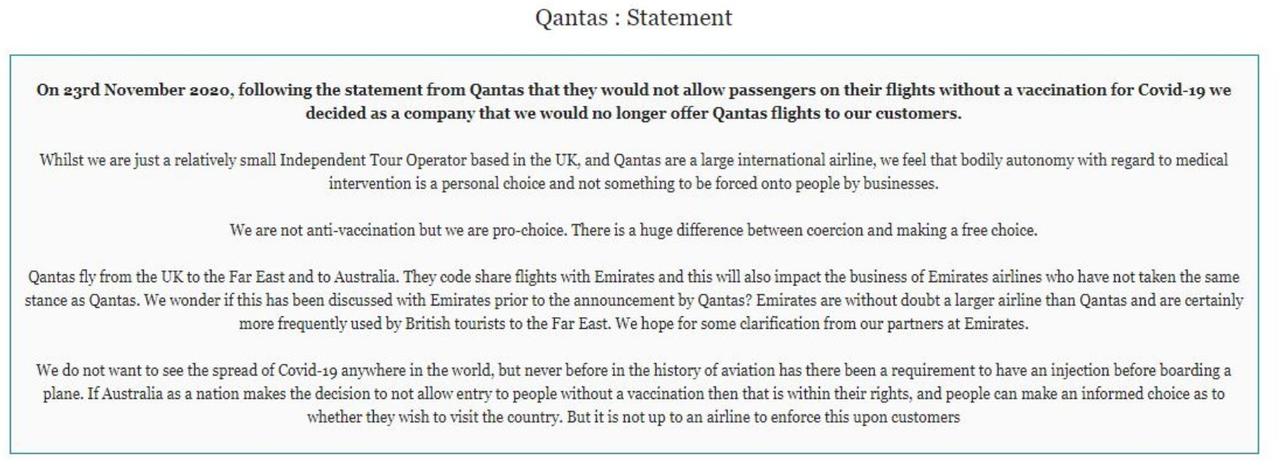

Tradewinds Travel posted a statement on their website asserting that “bodily autonomy with regard to medical intervention is a personal choice and not something to be forced onto people by businesses.”

“We are not anti-vaccination but we are pro-choice. There is a huge difference between coercion and making a free choice,” says the statement.

The company also noted how Qantas “code share(s) flights with Emirates” to the far east and that Emirates has not announced it will follow the same policy, prompting the question, “We wonder if this has been discussed with Emirates prior to the announcement by Qantas?”

“Never before in the history of aviation has there been a requirement to have an injection before boarding a plane,” the statement adds.

“If Australia as a nation makes the decision to not allow entry to people without a vaccination then that is within their rights, and people can make an informed choice as to whether they wish to visit the country. But it is not up to an airline to enforce this upon customers.”

The company said it had received “much support” over its stance.

In a related development, European airliner Ryanair has signaled that it will not require fliers to take a coronavirus shot before allowing them to travel.

Chief executive Eddie Wilson pointed out that mandating a vaccine would be pointless since people can travel between different European countries by car or train.

“With short haul and freedom of movement of people in Europe… I think we’ll see an entirely different landscape come spring and early summer, not really relevant for short haul and European travel,” said Wilson.

“In Paris, if you were to choose no vaccination… you’d just get a train instead,” he added.

* * *

New limited edition merch now available! Click here. In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown. Also, I urgently need your financial support here.

via ZeroHedge News https://ift.tt/37ag7n9 Tyler Durden

Apple Orders Foxconn To Shift Some MacBook and iPad Production From China To Vietnam Tyler Durden

Thu, 11/26/2020 – 09:15

According to sources cited by Reuters, Foxconn, formally known as Hon Hai Precision Industry, has been ordered by Apple to shift some iPad and MacBook production lines to Vietnam from China.

Foxconn is building assembly lines for Apple’s iPad tablet and MacBook laptop at its plant in Vietnam’s northeastern Bac Giang province, to come online in the first half of 2021, the person said, declining to be identified as the plan was private.

The lines will also take some production from China, the person said, without elaborating how much production would shift.

“The move was requested by Apple,” the person said. “It wants to diversify production following the trade war.” -Reuters

Foxconn was not at liberty to discuss “company policy and for reasons of commercial sensitivity” behind the shift in production lines.

The Nikkei recently learned that Foxconn is set to invest $270 million into new production facilities in Vietnam.

Amid President Trump raising tariffs and hurling Twitter threats at China – Apple has taken steps to add geographic diversity to its supply chain in China. Apple suppliers in Vietnam already manufacture the company’s AirPods and AirPods Pro.

Other Apple suppliers, such as Pegatron and Compal Electronics, “are also considering building plants in Mexico,” the source continued. Companies continue to reduce reliance on China as they diversify supply chains.

In August, Foxconn Chairman Liu Young-way told investors that Trump’s trade war had fractured the world into two – indicating his firm had to develop “two sets of supply chains.”

Even with Trump upending decades of American trade policy in four years – the lasting effects are starting to be realized.

Despite that rhetoric of a Biden presidency would mean China would “own America” – and in some respects they already do – messaging from the Biden camp suggests they would continue the tough approach on Beijing.

via ZeroHedge News https://ift.tt/3fE5pcy Tyler Durden

An opinion columnist at the University of Virginia’s student newspaper encouraged her readers to “stand up” to “ racist family” at Thanksgiving.

Emma Camp, who writes a regular opinion column for the Cavalier Daily, asserted that “white progressives must privilege their principles over personal comfort” in conversations with family during the holiday season. In order to fulfill this mandate, they “need to stand up to their racist loved ones.”

Though Trump, who Camp defines as a “proto-fascist,” who has “been defeated,” she argues that “the hateful rhetoric, conspiratorial thinking and virulent racism, xenophobia and sexism he espoused during his tenure remain deeply entrenched in American political discourse.”

“When we sit silent over our uncle’s QAnon rants or our high school friends’ xenophobic comments,” she continues, “it shows that we value our own comfort over what we know to be our ethical duty.”

She again admonishes readers to prove that their “moral principles” are more important than their “relationship with racists.”

“No matter the outcome, standing up for your principles disrupts the presumption of agreement so often assumed by bigots,” concludes Camp.

“Hateful beliefs may continue — but at the very least you can make it clear that they are not welcome to at least one person at the dinner table.”

University of Virginia undergraduate Deven Upadhyay told Campus Reform that “calling white progressives to action at Thanksgiving turns social activism into a game, eliciting frivolous accusations and burning bridges with loved ones.”

“Today’s progressives have developed a savior complex that has become so sensitive, diluting the severity of real instances of xenophobia, sexism, and racism,” he added.

“As this piece pins this task on white people, it seems that people of color need to be ‘saved’ by our white friends.”

Upadhyay, who is Indian-American, says that he does not “need to be saved or pandered to. By playing along with the policing of white progressives, we grant them a position of superiority and false sense of accomplishment.”

“If the purpose of activism is to make change, telling your uncle Steve he’s a white supremacist surely won’t win you a Nobel prize,” he added.

Campus Reform reached out to Camp for comment and will update this article accordingly.

via ZeroHedge News https://ift.tt/3mmVaMt Tyler Durden

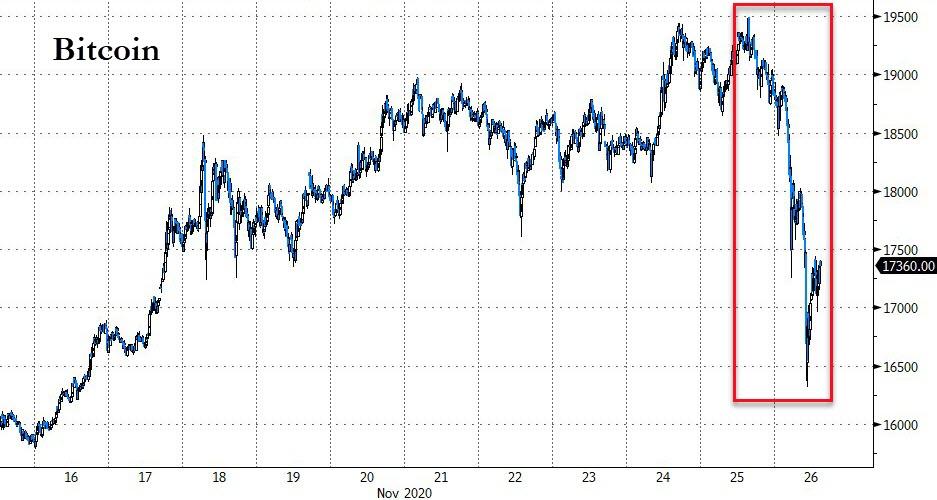

Crypto Crashes Overnight As Whales Move Bitcoin To Exchanges Tyler Durden

Thu, 11/26/2020 – 08:25

In the biggest crash since March, Bitcoin prices collapsed by over $3000 overnight (from just shy of $19500 to $16300 at the morning’s lows)…

Source: Bloomberg

Many analysts had already warned that the recent gains were due for a pullback, among them CNBC host Brian Kelly and trader Tone Vays, who forecast a dip to $14,000 on Thursday; but while the rest of the crypto space is also under pressure, November remains a big month with Bitcoin up 25%…

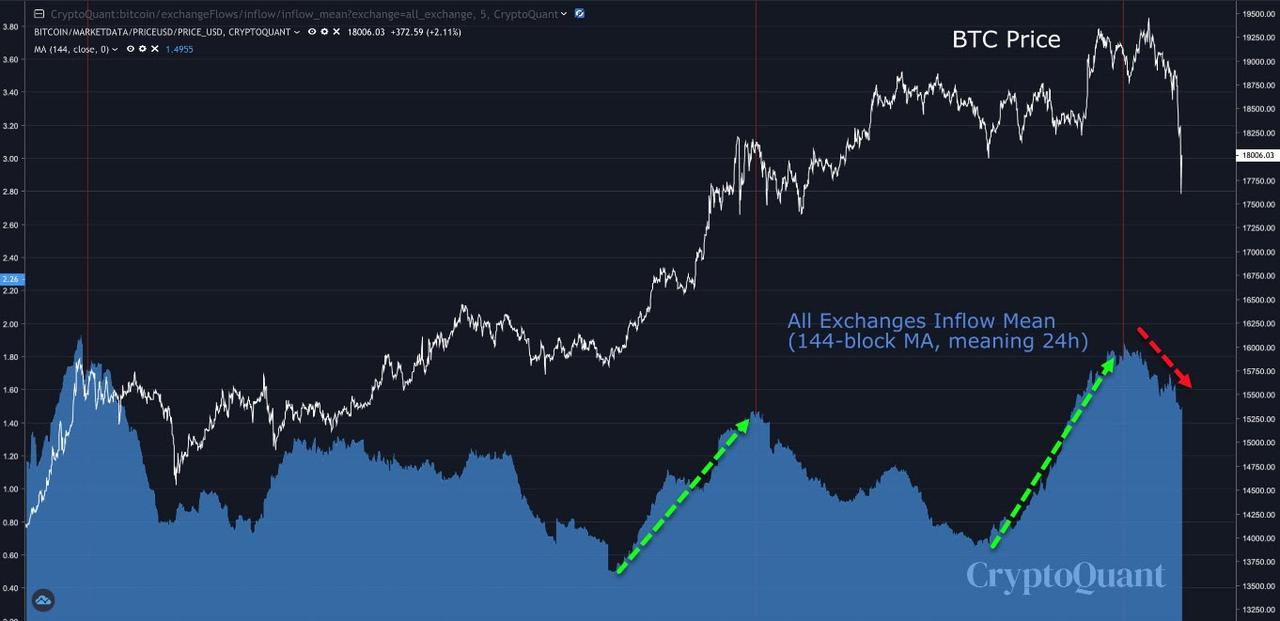

“All Exchanges Inflow Mean increased a few hours ago. It indicates that whales, relatively speaking, deposited $BTC to exchanges,” Ki Young Ju, creator of on-chain analytics resource CryptoQuant, summarized to Twitter followers.

“But long-term on-chain indicators say the buying pressure prevails. I still think we can break 20k in a few days.”

Exchange inflows in November. Source: CryptoQuant/ Twitter

At the same time, major exchange OKEx announced that it had reinstated withdrawals. Ki Young Ju, founder of on-chain analytics service CryptoQuant, highlighted increased outflow activity from OKEx to both wallets and other exchanges.

“BTC flows from OKEx to all other exchanges hit 493 BTC at that time,” he wrote in his latest Twitter update.

“83% of total outflows went to non-exchange wallets like custody. It could be a bullish signal in the long-term.”

image courtesy of CoinTelegraph

Finally, additional bearish fuel came from Brian Armstrong, CEO of Coinbase, who commented on recent rumors that the United States plans to introduce new regulation governing self-hosted cryptocurrency wallets.

“If this crypto regulation comes out, it would be a terrible legacy and have long standing negative impacts for the U.S. In the early days of the internet there were people who called for it to be regulated like the phone companies. Thank goodness they didn’t,” he warned.

At time of writing we note that Bitcoin is around $1000 off its intraday lows as Bitcoin’s fundamental indicators support the bullish theory going forward with the mining difficulty set for a 7.3% uptick in three days’ time and hash rate continuing to grow.

via ZeroHedge News https://ift.tt/3nVKg0k Tyler Durden

Futures Flat, Global Stocks Mixed In Thin Thankgsgiving Trade Tyler Durden

Thu, 11/26/2020 – 08:12

Global stocks held near record highs on Thursday, with US equity futures flat due to the Thanksgiving holiday while the rally in European stocks paused, as recent vaccine progress and hopes for further stimulus – whether monetary or fiscal – kept markets bullish.

While US cash equities are closed for the Thanksgiving holiday, S&P futures were flat after fading modest overnight gains, however Nasdaq futures were well in the green, as cyclical companies including banks and energy firms which have benefited the most from the post-vaccine surge retreated while more defensive tech shares gained.

Markets also took a boost from minutes from the latest Fed minutes which showed that officials discussed how the central bank’s asset purchases could be adjusted to provide additional support to the economy. The minutes said policymakers may give new guidance about its bond-buying “fairly soon”.

“2021 is going to be a year of economic catch-up,” said Samy Chaar, chief economist at Lombard Odier. “When you keep the pandemic contained and under control, economic activity catches up very quick.”

Recovery sentiment turned cautious Thursday, however, as the virus toll continued to rise in Europe and the U.S., leading German Chancellor Angela Merkel to call on Europe’s ski resorts to close this winter. The task of a global vaccination comes with logistical problems, all while the virus gains ground and economic recoveries wobble.

“Question marks still surround the speed of a global roll-out and the proportion of populations willing to be vaccinated,” Geir Lode, head of global equities at the international business of Federated Hermes, wrote in a note to clients. “These factors, combined with a second consecutive week of rising jobless claims in the U.S,, appear to have brought the rotation into value and back-to-work stocks grinding to a halt for now.”

“The market’s very much looking forward to 2021 and the time when vaccines will be rolled out and economic activity can get back to normal,” said Kiran Ganesh, a multi-asset strategist at UBS, adding that the equities rally is “particularly driven by the rotation trade away from large caps and towards small caps, away from the U.S. and towards Europe, and away from technology and towards some of the cyclicals.”

The MSCI world equity index rose to a record high on Wednesday and held close to it on Thursday, up 0.1% on the day as markets shrugged off the latest rise in U.S. jobless claims. Global stocks are having their best month on record in November, boosted by a slew of positive vaccine announcements and hopes that Biden’s administration will deliver more economic stimulus and political stability.

Europe’s STOXX 600, which is also having its best month on record, up 14.4% in November, was down 0.1% on the day. European equities traded a narrow range in a quiet morning, with a few central bank speakers and minutes from the ECB’s October meeting the only scheduled events of interest. Gains in tech, travel and healthcare stocks were offset by losses in banks, oil & gas and autos. The UK’s FTSE 100 and Spain’s IBEX laged European peers. In France and Germany, consumer confidence plunged in November under new lockdown restrictions, challenging the idea of a quick return to normal in the euro zone’s two biggest economies. German Chancellor Angela Merkel told parliament that lockdown measures will be in place until at least the end of December and possibly longer.

Earlier in the session, Asian stocks gained, led by the communications and IT sectors, after falling in the last session. Most markets in the region were up, with Indonesia’s Jakarta Composite advancing 1.4% and Thailand’s SET rising 0.9%, while Australia’s S&P/ASX 200 slid 0.7%. The Topix added 0.6%, with SoftBank and Nintendo contributing the most to the move. The Shanghai Composite Index rose 0.2%, driven by Ping An Insurance and Yangtze Power.

Emerging-market stocks resumed gains after a one-day drop, suggesting the remains intact even as trading slows due to the U.S. Thanksgiving holiday. The MSCI Inc. measure of developing-nation equities moved to within 50 points of its 2018 high, a level that was only surpassed before the global financial crisis. Foreign-exchange markets were mixed, with Asian currencies and the Turkish lira rising, while eastern European currencies and the South African rand fell

In rates, Treasury futures edged higher with the cash market closed, with traders off for Thanksgiving holiday in the U.S. A deluge of data on Wednesday brought the first back-to-back rise in weekly U.S. jobless claims since July and a widening trade deficit. In Europe, bunds and gilts bull-flattened gently while peripheral and semi-core spreads widened slightly to core, with Italy underperforming.

In FX, Bloomberg dollar index drifts higher, back into the green. NOK and SEK are the worst G-10 performers. EUR/USD fades an early push up to 1.1941, cable trades at the lows.

In crypto, Bitcoin plunged over 10% on the session amid a sudden bout of overnight selling.

In commodities, crude futures slumped with WTI dropping ~1.5% having failed to breach $46 overnight, Brent drops back on a $47-handle after running into resistance near $49 during Asian trade. Spot gold grinds higher near $1,814/oz. Base metals trade well, with LME copper outperforming

There is nothing on today’s calendar with the US closed for holiday.

Top Overnight News from Bloomberg

Sweden’s central bank surprised markets with a bigger-than- expected expansion of its asset purchase program, amid signs the Covid crisis will do more damage to the largest Nordic economy than previously feared

Trillions of euros in spare cash sloshing through the euro zone have made it cheaper for investors to access funding for one week as opposed to one day for the first time

The U.K. Debt Management Office will continue selling inflation-linked debt tied to the flawed Retail Price Index even after plans were announced to move away from the benchmark, according to Chief Executive Officer Robert Stheeman

The European Central Bank should consider wiping out or holding forever the government debt it buys during the current crisis to help nations recover and restructure, a top Italian government official said

Chancellor Angela Merkel urged Germans to do more to rein in the coronavirus to avoid the “worst-case scenario” of an overburdened health care system

China’s imports of U.S. goods under the phase-one trade deal slowed last month after hitting a high in September, leaving the full-year target well out of reach

China will maintain normal monetary policy for as long as possible and keep macro leverage ratio basically stable, PBOC says in its quarterly policy implementation report

A more detailed look at Global Markets courtesy of NewsSquawk

Major European bourses see a mixed session thus far (Euro Stoxx 50 Unch) as the non-committal tone and holiday-thinned trade from Asia-Pac reverberates into Europe on US Thanksgiving. Sectoral performance have more of a defensive bias, with Healthcare, Utilities and Staples among the top gainer, whilst cyclicals reside at the bottom of the pile but IT bucks the trend. The oil and gas sector is the laggard as the crude complex pulls back following its recent rally ahead of next week’s key energy meetings, whilst Financial names also sees losses on account of lower yields. Thus, UK’s FTSE 100 (-0.6%) narrowly underperforms regional peers with its heavy-weight banking and energy names hampering performance. Travel & Leisure names continues to be underpinned on vaccine hopes, with easyJet (+2%) and Air France-KLM (+1.4%) trading firmer. In terms of individual movers, Volkswagen (-1.8%) sees more pronounced losses than some peers amid reports that the Co. and Audi are to face prosecution in India under charges of cheating & conspiracy.

A non-committal tone was evident for most of Asia-Pac trade following the indecisive lead from the US where stocks were rangebound heading into the Thanksgiving holiday and after a deluge of mixed data releases. ASX 200 (-0.7%) was led lower by an unwinding of yesterday’s outperformance in cyclicals and with sentiment clouded by frictions with Australia’s largest trading partner after China alleged there were environmental quality issues concerning Australian coal in which AUD 700mln worth is stuck on ships being delayed from entering and unloading at Chinese ports. Nikkei 225 (+0.9%) shook off the initial caution to outperform its regional peers on supportive measures with the Japanese government to extend its employment subsidy program until end-February and the virus loan application period to end-March, while KOSPI (+0.6%) was kept afloat after the BoK maintained its Base Rate at 0.50% as expected and upgraded its GDP growth forecasts for 2020 and 2021 as it anticipates an export-driven recovery. Hang Seng (+0.1%) and Shanghai Comp. (+0.2%) lacked firm direction with the mainland tentative amid ongoing trade uncertainty after the Trump administration granted ByteDance a new 7-day extension of the divestiture order directing it to sell to TikTok by December 4th, while the Peterson Institute for International Economics also noted that China total purchases of US goods during the first 10 months of the year, were less than half of the annual commitment under the Phase 1 deal.

In FX, hot on the heels of dovish FOMC minutes and ahead of the ECB account that is tipped to follow a similar path, the Riksbank has exceeded or confounded expectations by expanding and extending its QE remit by Sek 200 bn for an extra 6 months through the end of 2021. Two Board members entered reservations, but the accompanying statement and updated (downgraded) economic forecasts supported the policy action – see 8.30GMT post on the headline feed for full details and our snap analysis. Predictably, Eur/Sek rebounded in response from a low around 10.1200 to circa 10.1770 before paring back, albeit no more so in percentage terms than Eur/Nok between 10.5130-5740 parameters, as the Norwegian Krona tracks a retreat in crude prices.

DXY – The Dollar remains on the back foot in wake of, if not directly due to the aforementioned Fed release, as the Committee committed to provide further guidance on bond buying and could enhance stimulus via increasing the pace, moving down the curve or maintaining the size and current maturity profile, but continue purchases for a longer period. However, the index has survived another attempt to test y-t-d lows (91.740 from September 1st) and is trying to regain a foothold above the 92.000 handle within a 92.091-91.844 range in thin US Thanksgiving holiday trade.

JPY – Contrary to month end rebalancing models signalling a strong Greenback sell vs G10 counterparts, bar the Yen, Usd/Jpy is capped below 104.50 and a key Fib retracement level at 104.67, but the headline pair faces even bigger option expiry interest at the 104.00 strike (1.7 bn) ahead of the NY cut and more Japanese inflation data in the form of Tokyo CPI.

AUD/EUR/CAD/NZD/GBP/CHF – All narrowly mixed against the Buck and holding in fairly familiar ranges, with the Aussie reclaiming 0.7350+ status following mixed Capex data and Euro consolidating above 1.1900 having reached another new November pinnacle, but not able to breach 1.1950 in advance of the latest ECB minutes and remarks from chief economist Lane before Schnabel. Elsewhere, the Loonie pivoting 1.3000 without further impetus from oil awaiting rather stale Canadian average weekly earnings and the Kiwi is straddling 0.7000 after in line NZ trade data and reflecting on potential changes to the RBNZ mandate to incorporate house prices that are running hot. Meanwhile, Sterling is still eagerly and anxiously looking for Brexit updates, as Cable continues to hit a brick wall into 1.3400 where latest heavy offers are said to have been layered from 1.3390 through 1.3385 to 1.3380, and the Franc is hovering above 0.9100.

In commodities, WTI and Brent front month futures see a session of losses in what seems to be a retracement from the recent rally, which was fueled by optimism OPEC+ will extend current cuts despite the recent vaccine news lifting the outlook for the complex. News flow for the complex has remained light throughout early European hours, but source reports later on in the day cannot be dismissed given the preparatory OPEC meetings in the run-up to the main even at month-end. Market expectations (as things stand) are widely skewed towards the second tranche (7.7mln BPD cuts) being extended through Q1 2021, a view also backed by Goldman Sachs, ING and UBS, despite positive vaccine noise and amid rising production in Libya. Recent sources also noted OPEC+ are still leaning towards a rollover of the current tranche notwithstanding the recent oil price rally, with Russia likely to agree to this if necessary, however, enthusiasm for cuts is not universal. WTI briefly dipped below USD 45/bbl (vs. high 46.09/bbl), whilst Brent Feb hovers around USD 48/bbl after hitting resistance at USD 49/bbl. Elsewhere, spot gold and silver saw a bout of upside, albeit modest, heading into the European cash open amid thinned conditions and a distinct lack of newsflow. The precious metals have since waned off best levels with spot gold ~1815/oz (vs. low 1806/oz) whilst spot silver hit highs just shy of USD 23.50/oz (vs. low 23.19/oz)

DB’s Jim Reid concludes the overnight wrap

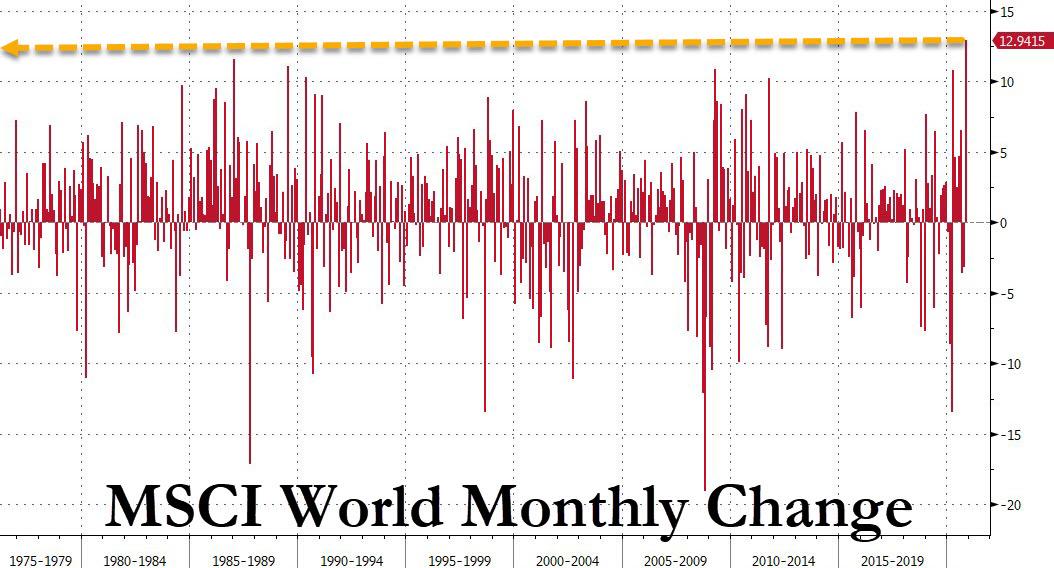

Happy Thanksgiving to our US readers. Let’s hope you have better things to do than read this though. Ahead of the holiday, US equities fell back from their record highs on Tuesday as a deteriorating situation on the coronavirus and weak economic data served as a reality check to the surge in risk assets we’ve seen in recent days. By the close, the S&P 500 had fallen -0.16% and the Dow Jones was down a larger -0.58%, as the latest data showed weekly initial jobless claims in the US rose more than expected for a second week running, up to 778k for the week through November 21. Furthermore, data on personal income for October showed an unexpectedly large -0.7% fall (vs. -0.1% expected), which will add to fears that the US economy is losing momentum as the number of Covid-19 cases continues to rise throughout the country heading into the winter. Even as the equity rally took a pause, the VIX volatility index fell -0.4 pts to its lowest closing levels (21.3) since February 21. That was the initial Friday sell-off before the S&P 500 fell a further -33% over the next 21 trading sessions.

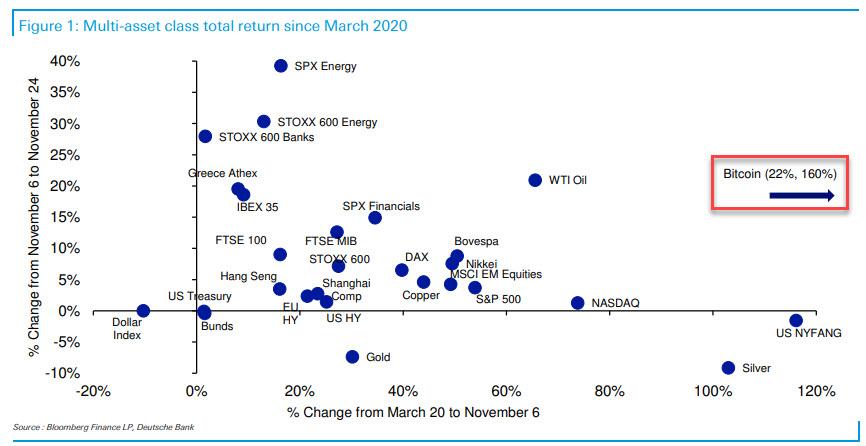

With the economic picture showing signs of weakness, big tech got a renewed bid again with the NASDAQ Composite +0.48% to reach its highest-ever closing level thanks to decent performances from Amazon (+2.15%), Apple (+0.75%) and Tesla (+3.35%). Even as tech outperformed yesterday, they still have massively lagged cyclicals over the past 2.5 weeks as our CoTD yesterday (link here) shows. The chart looks at a scatter of asset class and sector returns from after the Pfizer/BioNTech vaccine news against their returns from March 20th to November 6th. Energy and bank stocks of the top level sectors have led the charge post the vaccine news, even as they paused for breath yesterday.

Other safe havens showed signs of strength too, with core sovereign bonds in Europe rising as yields on bunds (-0.5bps) and gilts (-1.2bps) fell back, whereas their counterparts in southern Europe such as 10yr Italian (+0.3bps) and Greek (+1.7bps) debt rose. In equities, however, southern Europe outperformed the rest of the continent, with Italy’s FTSE MIB (+0.72%) and Spain’s IBEX 35 (+0.26%) both outperforming the STOXX 600 (-0.08%). On the other hand, yields on 10yr Treasuries (+0.2bps) rose slightly to 0.882%.

Asian markets are trading mostly higher this morning with a few indices at multi-year highs. The Nikkei (+0.88%), Hang Seng (+0.23%) and Kospi (+0.70%) are up while the Shanghai Comp (-0.01%) is flat and the ASX (-0.70%) is down. Futures on the S&P 500 are up +0.19% ahead of the holiday. Meanwhile, the BoK at its monetary policy decision today kept the interest rates unchanged while revising GDP forecasts upwards by 0.2pp for both this year and next. Elsewhere, Bitcoin is down -5.38% this morning following its spectacular run so far this year.

The minutes from the Federal Open Market Committee’s November 4-5th meeting were released last night. The committee viewed current asset valuations as “moderate” when taking low interest rates into account. The participants noted that “immediate adjustments to the pace and composition of asset purchases were not necessary” but, “they recognized that circumstances could shift to warrant such adjustments.” There was a more pertinent discussion of updating forward guidance on their bond-buying strategy “fairly soon”, ensuring that any additions in the Central Banks’ securities holdings would taper and end before the federal funds rate was raised. There was some discussion on the facilities that the Treasury department has since shut with officials at the meeting “emphasizing the important roles” the lending programs played “in restoring financial market confidence and supporting financial stability”. With these programs closed, the central bank could act more aggressively if financial conditions do worsen going forward.

In terms of the latest on the virus, it feels a little like summer again with case count news easing in Europe and worsening in the US. Yesterday, France’s 7-day running tally of infections fell to its lowest levels since October 9, while general hospitalisations and ICU usage continue to fall. Geneva and other Swiss cities are said to be reopening restaurants from December 10 onwards, while non-essential shops will reopen from this weekend. On the other hand, Germany has decided to extend its partial lockdown for at least 3 weeks to December 20 and has tightened restrictions on private gatherings. The German government has also indicated that they expect wide-ranging restrictions to stay in place until early January, particularly for restaurants and hotels. Meanwhile, New York saw its daily case numbers rise above 6,000 for the first time since April and California reported over 18,000 new cases, well over the 15,400 daily record from this past weekend. While mass gatherings have been largely discouraged by local governments, there still seems to be quite a bit of mobility ahead of today’s holiday and we will learn the impact of this in the first couple of weeks of December, just ahead of Christmas travel. Across the other side of world, South Korea reported 583 infections in the past 24 hours, the highest since March.

Here in the UK, the main headlines yesterday surrounded the government’s latest spending review, where the OBR forecast that the budget deficit in 2020-21 would climb to a peacetime record of 19% of GDP, while public sector net debt would reach 105.2% of GDP. Though the government was eager to advertise the funds being spent on infrastructure and tackling Covid-19, one of the key takeaways was the likely fiscal consolidation in the years ahead, with the announcements including a public sector pay freeze in 2021-22 and major cuts to the overseas aid budget. The UK is seemingly looking to fiscally consolidate, which is brave at this point but with no election for 4 years one can understand the political motivation. On Brexit, the OBR’s forecasts assumed that there would be a trade deal reached with a smooth transition to the new arrangements, but if there were a no-deal outcome, that could reduce real GDP next year by an extra 2% relative to their central forecast.

Speaking of Brexit, with just 5 weeks today until the transition period comes to an end, there’s still no sign of progress on the key issues in the trade negotiations. In a speech to the European Parliament yesterday, Commission President Ursula von der Leyen said that “I cannot tell you today, if in the end there will be a deal”, and although she said that there’d been “genuine progress” on a number of issues, the three usual stumbling blocks of the level-playing field, fisheries and governance remained. It’s still not obvious from where or from whom the compromises will come, and the BBC’s Europe Editor Katya Adler tweeted yesterday that EU sources had said that the talks weren’t going well. There is a story on Bloomberg this morning where the French foreign minister is accusing the UK of dragging its feet with Barnier apparently also suggesting there is little point in him coming to London unless the UK is prepared to give ground. So tension are mounting.

Wrapping up with yesterday’s other data, the second estimate of US GDP growth in Q3 was maintained at an annualised growth rate of +33.1%. Meanwhile, the preliminary October reading for durable goods orders showed a stronger-than-expected +1.3% rise (vs. +0.8% expected). US home sales rose to an annualised rate of 999k in October, which was actually slightly lower than the upwardly revised 1002k the previous month. And the University of Michigan’s final consumer sentiment index for November fell a tenth from the preliminary reading to 76.9, having been 81.8 the previous month.

To the day ahead now, and it’ll likely be a quieter one because of the Thanksgiving holiday in the US. Otherwise, we’ll get the minutes of the ECB’s October meeting, remarks from the ECB’s Lane and Schnabel, as well as the Euro Area’s M3 money supply data for October. There’ll also be a decision on interest rates from the Riksbank.

via ZeroHedge News https://ift.tt/2J1HwzT Tyler Durden

{kind=link}

{kind=link}