There were many things that contributed—ample land, a wide ocean, and more. But so much, I think, comes from this one foundation:

They were fortunate enough to have been born Englishmen.

from Latest – Reason.com https://ift.tt/3zzORvj

via IFTTT

another site

There were many things that contributed—ample land, a wide ocean, and more. But so much, I think, comes from this one foundation:

They were fortunate enough to have been born Englishmen.

from Latest – Reason.com https://ift.tt/3zzORvj

via IFTTT

Immediately after the publication of the original Yale Book of Quotations, readers—some of them scholars, but more of them ordinary quotation-lovers—sent excellent new information to the editor. These discoveries are now incorporated into The New Yale Book of Quotations. The preeminent contributor was Garson O’Toole, who was inspired to create the magnificent quoteinvestigator.com website. The help furnished by the crowd-sourcing resulted in a new volume that not only traces famous quotes to their true origins, but also captures the many famous quotations omitted by other reference works. Below is the third part of the NYBQ’s introduction.

The publication of the first edition of The Yale Book of Quotations triggered a remarkable “crowd-sourcing” response by quotation-lovers and researchers spanning the globe. Employing printed books, online searching, and their own memories, many readers emailed, or communicated by other avenues, outstanding contributions of quotations for inclusion or of improvements in information about quotes in the YBQ. The names of the more active such contributors are given in the Acknowledgments above, but special credit needs to be elaborated here for Garson O’Toole.

In 2007 O’Toole became curious about the genesis of the supposed Chinese curse “May you live in interesting times,” which Wikipedia had traced back to 1950. He then was able to find the curse in a 1944 book and posted his discovery on a blog. This posting was noticed by the Yale Book of Quotations editor, who added a comment pointing out that the YBQ had a 1939 citation. O’Toole later wrote that he “purchased a copy of The Yale Book of Quotations and began purposefully scanning its entries.” The rest is history, as he was inspired by the Yale volume to create, three years later, a website he titled Quote Investigator (quoteinvestigator.com). Quote Investigator has grown to include well over a million words of authoritative quote-sleuthing. O’Toole’s brilliant researches have greatly aided The New Yale Book of Quotations, which has many dozens of entries reflecting Quote Investigator findings.

The compilation of the present book has also benefited from extensive use of the electronic mailing list of the American Dialect Society and the Project Wombat network of reference librarians and researchers, both of which bring together very skilled people dedicated to answering sophisticated questions. Specific contributors are listed in the Acknowledgments. Finally, traditional methods of library research, utilizing the resources of the Yale University Library and Yale Law Library as well as interlibrary borrowing from other institutions, were pursued to verify quotations and to find their origins.

The research efforts outlined above were devoted not only to tracing and verifying quotation origins, but also to ensuring that all of the most famous quotations were included in this book. As a result, many important quotations not found in prior quotation dictionaries appear here, such as Willard Motley’s 1947 suggestion to “Live fast, die young, and leave a good-looking corpse”; the famous sentence from Lou Gehrig’s farewell speech at Yankee Stadium in 1939: “Today I consider myself the luckiest man on the face of the earth”; and Friedrich Nietzsche’s 1888 epigram, “Whatever does not kill me makes me stronger.” More than a thousand previous quotation collections and other types of anthologies were canvassed; many Internet resources were perused; and experts on specific authors and types of literature were consulted.

As a result of the unique approaches and methods employed, The New Yale Book of Quotations has a Janus-like duality. As noted above, the NYBQ serves a very traditional function of gathering the monuments of literary expression and other forms of enduring culture. It also, however, captures the most celebrated items of contemporary discourse and public life. Thus William Shakespeare and Donald Trump coexist in these pages. One of them is far less eloquent than the other, but, for better or worse, both are now part of our verbal heritage, with Mr. Trump’s most remarkable utterances and Tweets carefully recorded here. Other recent individuals whose quotes have been introduced or supplemented in this edition include, among many others, Warren Buffett, Hillary Clinton, Pope Francis, Jonathan Franzen, Alan Greenspan, Steven Jobs, Cormac McCarthy, Lin-Manuel Miranda, Toni Morrison, Barack Obama, Sarah Palin, David Foster Wallace, and Warren Zevon.

from Latest – Reason.com https://ift.tt/3mSmJAk

via IFTTT

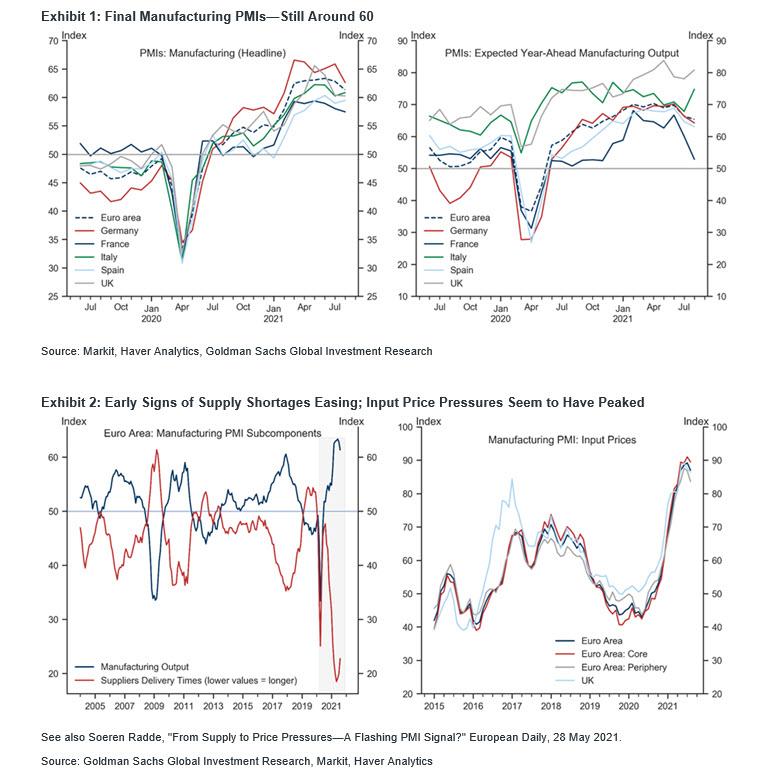

Futures Rise Toward Fresh Record High As PMIs Confirm Global Economy Slowing

After a somewhat soggy end to the otherwise spectacular month of August which saw 12 new all time highs in the S&P500, global stocks and US futures are solidly green to start the month of September despite another round of dismal global PMIs confirming the global economy is slowing, and especially China where the Caixin China manufacturing PMI came in at 49.2, missing expectations of 50.3, and the first contraction since April 2020. Of course, the coming global slowdown is great news for stocks as it means more stimmies in China, and a potential taper delay in the West (where hyperinflation is “transitory” after all) meanwhile the Fed’s QE cannon continues to blast billions in daily liquidity and naturally futures were solidly in the green, higher by 15 points to 0.34% to 4,536, Dow e-minis were up 106 points, while Nasdaq 100 e-minis were up 33.75 points, or 0.22%.ahead of U.S. ISM manufacturing data and ADP employment change.

Energy stocks led Wednesday’s gains, with oil majors Chevron Corp, Exxon Mobil and Schlumberger NV rising between 0.5% and 1.1% in premarket trading as crude prices rose ahead of today’s OPEC+ meeting. Rate-sensitive banks also rose with J.P.Morgan, Goldman Sachs and Citigroup up about 0.6% on support from higher bond yields. U.S-listed shares of the world’s biggest miner BHP Group dropped 1.7%, while those in China-focused mining giant Rio Tinto fell 1.2% after tepid China factory data dented copper and iron ore prices. Shares of Calvin Klein and Tommy Hilfiger owner PVH Corp surged 7.8% after it raised its full-year earnings forecast. Here are some other notable movers:

Still, while corporate results are strong, concerns about the delta variant, inflation spikes, supply bottlenecks and stimulus tapering could easily trigger a 10%-20% drop in stock prices, said Ipek Ozkardeskaya, senior analyst at Swissquote. “The markets are on path for more gains,” she wrote in a report. “Nobody can tell how healthy the trend is, where it will end, or how it will end.”

The ADP report, published ahead of the government’s more comprehensive and closely watched employment report on Friday, is expected to show private payrolls rose by 613,000 in August after 330,000 gain in July. The number is due at 8:15 a.m. ET. Separately, the Institute for Supply Management’s gauge of manufacturing sector activity is expected to have moderated to 58.6 in August from 59.5 in the previous month.

Earlier, surveys showed Asian and European factory activity lost momentum in August as the ongoing coronavirus pandemic-disrupted supply chains. Many firms reported logistical troubles, product shortages and a labor crunch which have made it a sellers’ market of the goods factories need, driving up prices. Here is a snapshot of the overnight PMIs:

While factory activity remained strong in the euro zone, IHS Markit’s final manufacturing Purchasing Managers’ Index (PMI) fell to 61.4 in August from July’s 62.8, below an initial 61.5 “flash” estimate. “Despite the strong PMI figures, we think that lingering supply-side issues and related producer price pressures might take longer to resolve than previously expected, increasing the downside risk to our forecast,” said Mateusz Urban at Oxford Economics. In Britain, where factories also faced disruptions, manufacturing output grew in August at the weakest rate for six months. The United States likely suffered a similar slowdown, data is expected to show later on Wednesday.

“We’re moving past the point of peak growth. The strongest period of the recovery now looks to be behind us, we’re seeing that in the economic data,” said Hugh Gimber, global market strategist at JP Morgan Asset Management. “The recovery is slowing, but it remains on track. And so that I think is what’s underpinning markets.”

Nothing like new all time highs to celebrate the slowdown.

European stocks also rose in the first trading session of September (because like the Fed, the ECB will be injecting billions in liquidity for a long, long time) after seven straight months of gains. The Stoxx 600 is up ~0.5%, led higher by travel, retail and banking industries. DAX took back some earlier gains, but was still up 0.1% on the day, while the FTSE 100 is up 0.6%. French spirits maker Pernod Ricard gained 3.3% after reporting better-than-expected results. Carrefour slumped 4.4% in Paris as billionaire Bernard Arnault sold his remaining holding in the supermarket chain. European luxury shares rose after Bernstein says stock market movements in August have priced in the risk of potentially higher taxation in China, “at least in its milder form.” Among the gainers were Richemont +2.2%, LVMH +2.2%, Kering +2%, Burberry +1.8%, Hermes +1.3%, and Swatch +0.9%. While new taxation would prompt rich consumers to momentarily rein in their discretionary spending, it’s unlikely that there will be “highly disruptive action” from the Chinese authorities, analyst Luca Solca writes in a note. Here are some of the biggest European movers today:

Earlier in the session, Asian stocks climbed for a fourth straight day as Chinese technology heavyweights extended their rebound from the massive rout seen earlier this year. The MSCI Asia Pacific Index rose as much as 0.5%, with Tencent and Meituan the biggest individual contributors to the gauge’s advance. The financials sector gave the biggest boost, helped by Ping An Insurance’s bounce back from Tuesday’s losses. Equity benchmarks in China, Singapore and Japan were among the region’s biggest gainers. The Hang Seng Tech Index rallied for a third day as more investors grow confident that a bottom may have been reached following the selloff sparked by Beijing’s regulatory crackdown on private industry. A gauge of Asia’s software technology firms including Tencent also rose after capping its first monthly advance since April. Asia’s stock benchmark is extending gains after rising 2.3% in August in what was its best monthly performance since December. Still, the rout in China and Hong Kong has meant that regional shares continue to underperform peers in the U.S. and Europe so far this year. “Many are starting to realize that the regulatory crackdown on large Internet platforms is becoming quite targeted in nature and isn’t creating existential threats to their business,” said Bloomberg Intelligence analyst Matthew Kanterman. “Coupled with relatively strong sector results the last few weeks and what appears to be a slowing cadence of bad regulatory developments vs July, sentiment may be starting to turn the corner for the sector.” Japan’s Topix closed at its highest level since April, while China’s CSI 300 Index climbed more than 1%.

Australian stocks pared declines after GDP beat expectations; the country’s S&P/ASX 200 index fell 0.1% to close at 7,527.10, trimming a loss of as much as 1% after Australia’s GDP report. The economy grew faster than expected last quarter as household’s tapped their savings to boost spending, underscoring the central bank’s view that the nation entered a renewed lockdown with solid momentum. Mesoblast was among the worst performers after Jefferies lowered its rating on the stock to “hold.” Alumina was among the top performers, extending its winning streak to a fourth day. In New Zealand, the S&P/NZX 50 index rose 0.2% to 13,243.49

In FX, the Euro trades around session high after the ECB’s Yannis Stournaras said inflation jump is temporary and the central bank should be cautious. Dollar was little changed for a third day. Commodity-linked currencies led gains while havens slipped; the euro and the pound were steady. The Aussie rallied amid short covering of AUD/USD and AUD/JPY positions after a strong close in Japanese stocks; bond yields in Australia and New Zealand jumped after hawkish comments from ECB officials spurred losses in global debt markets. The yen weakened a third day amid risk-positive sentiment and higher Treasury yields as traders positioned before the U.S. data.

In rates, 10-year Treasury yields are little changed at 1.31%. Treasuries were steady, off session lows, after facing slight pressure following block sale in Ultra 10-year note futures shortly after 6am ET. In Europe, bunds continue to underperform amid heavy debt sales in Germany. U.S. stock futures advance, still inside Tuesday’s range. Yields were cheaper across belly, remain broadly within a basis point of Tuesday’s close; in 10-year sector bunds lag by 1bp vs Treasuries while gilts trade broadly in line.

Government bond yields across the euro area touched their highest levels in around six weeks, pushed up by unease over the future pace of European Central Bank bond purchase after two ECB officials said the central bank needs to begin tapering soon. Germany’s 10-year Bund yield touched its highest level in just over six weeks, briefly rising above -0.36%.

In commodities, crude maintained a zigzag-trading pattern ahead of the upcoming OPEC ministers and allies meeting later Wednesday. Brent and WTI are little changed, with the global crude benchmark holding above $71/bbl. LME copper extends decline, down 2% after China released its third batch of metals from state reserves, vowing to sell more based on the market. The rest of the base metals complex is in red. In fixed income, bund yields gives back some gains, trading at the -0.38-handle, while peripheral spreads move wider to the core, the steepest at the longest end of the curve.

Market Snapshot

Top Overnight News from Bloomberg

A more detailed look at global markets courtesy of Newsquawk

Asian stocks traded somewhat cautiously after further disappointing Chinese PMI data and following a soft handover from the US where sentiment was mired by disappointing Chicago PMI and US Consumer Confidence data, although the losses on Wall Street were only marginal and all major indices registered a seventh consecutive monthly gain for August. ASX 200 (-0.1%) was pressured as daily COVID-19 infections continued to ramp up in Australia’s most-populous states and with better-than-expected GDP doing little to brighten the mood, given that the strong economic growth for Q2 was made somewhat stale by the lockdowns throughout the entirety of Q3 so far. Nikkei 225 (+1.3%) outperformed amid reports PM Suga is to order the compiling of an economic package and additional budget within the week, while data also showed Japanese companies’ recurring profits nearly doubled Y/Y during the prior quarter. Hang Seng (+0.6%) and Shanghai Comp. (+0.7%) eventually weathered the miss on Chinese Caixin PMI data which slipped into contraction territory for the first time since April last year and effectively supported the argument for PBoC easing. However, price action was choppy as crackdown concerns also lingered amid the continued tightening of Beijing’s regulatory grip with China to curb overly fast growth in medicine expenses and the PBoC is to implement new disclosure measures for Chinese non-bank payment apps when they make new products or conduct foreign stock market listings. Finally, 10yr JGBs declined amid spillover selling from global counterparts including the bear steepening stateside and pressure in European bonds following the firm Eurozone inflation data, while the outperformance in Japanese stocks and lack of BoJ purchases in the market today also contributed to the headwinds for JGBs.

Top Asian News

Stocks in Europe trade with respectable gains across the board (Euro Stoxx 50 +1.2%; Stoxx 600 +0.9%), despite a somewhat mixed APAC lead and with little in terms of fresh fundamentals to sour risk appetite. US equity futures see gains of a lesser magnitude and have been waning off best levels, with the RTY (+0.6%) outpacing the ES (+0.3%), YM (+0.3%) and NQ (+0.2%), ahead of the ADP and ISM Manufacturing PMI later today before Friday’s pivotal jobs report. Back to Europe and sticking with PMIs where we have had the manufacturing finals across Europe – with the resonating theme being ongoing supply chain issues. The DAX (+0.7%) narrowly underperforms the region after the German manufacturing metric was slightly revised lower, deviating from the revision higher seen in France and the forecast beats printed in Italy and Spain – with the IBEX (+2.2%) the clear European outperformer at the time of writing, although more-so on the back of solid sectorial performances seen in Retail, Travel & Leisure and Banks. Sectors across Europe are predominantly in the green, with the only laggards the Basic Resources and Chemicals sectors. Sectors do not portray a clear theme nor bias. In terms of individual movers, Pernod Ricard (+3.5%) is firmer post-earnings where it announced the resumption of its EUR 500mln share buyback programme. Carrefour meanwhile trades at the foot of the Stoxx 600 after Billionaire Bernard Arnault’s Agache group announced the sale of its 5.7% stake in the Co. via accelerated bookbuilding. Meanwhile, Stoxx will announce the results of its annual review of the Euro Stoxx 50 Index at the close of business on 1 September, to be effective Friday, 17 September – JPM expects BBVA (+2.2%) and Stellantis (+0.3%) to replace Engie (+2.0%) and Amadeus (+2.6%).

Top European News

In FX, a marked change in fortunes for the Yen following its fleeting breach of 100 DMA resistance vs the Dollar yesterday, as Usd/Jpy rebounds sharply through 110.00 and the 50 DMA (110.10) towards 110.50 alongside US Treasury yields amidst further bear-steepening and renewed risk appetite. The Yen may also be factoring in reports that Japanese PM Suga is preparing an economic package and supplementary budget, plus pretty dovish/downbeat from BoJ’s Wakatabe, and the same could be said for the Franc in wake of SNB’s Zurbruegg saying that he expects low global interest rates will remain unchanged for some time to come, while noting vulnerabilities on the Swiss mortgage and real estate markets currently at a high level. Furthermore, the Bank sees clear signs of unsustainable mortgage lending on the one hand and heightened risks of a price correction on the other. Usd/Chf is back in the high 0.9100 area following its flirt with the round number on Monday, and with little downside reaction to a firmer Swiss manufacturing PMI. Conversely, Gold is coping relatively well with the rise in UST yields and risk-on environment on the Usd 1800/oz handle, albeit back below 100 and 200 DMAs after hurdling both and closing above yesterday, as the Greenback grinds higher and DXY attempts to form a base beyond 92.500 having bounced from a 92.395 low on Tuesday. The index is now hovering within a 92.790-640 band awaiting ADP, Markit’s final US manufacturing PMI, ISM and comments from Fed’s Bostic.

In commodities, Crude futures have largely retraced their overnight gains, with WTI and Brent both back towards the bottom end of today’s ranges. The choppiness comes in the run-up to the JMMC meeting at 15:00BST/10:00EDT and the decision-making OPEC+ confab at 16:00BST/11:00EDT – subject to delays. Expectations have solidified around a 400k BPD hike, i.e., a continuation of the current plan, with all sources thus far pointing in that direction. That being said, it’s worth keeping in mind that OPEC+ has a tendency to massage expectations and then surprise markets. The full Newsquawk preview can be accessed here, and the exclusive Twitterdeck is available here. Elsewhere, spot gold and silver are uneventful and contained to recent ranges awaiting Tier 1 US data. Industrial metals are slightly more interesting following later-confirmed reports that China is releasing a third batch of metals totalling 150k tonnes, comprised of 30k tonnes of copper (prev. 30k), 70k tonnes of aluminium (prev. 90k) and 50k tonnes of zinc (prev. 50k). LME copper slumped back under USD 9,500/t and resides near session lows at the time of writing – with the disappointing Chinese Caixin manufacturing PMI also weighing on the red metal.

US Event Calendar

DB’s Jim Reid concludes the overnight wrap

So I now have 16 weeks holiday from looking after the kids which is a nice relief. After 2 weeks non stop with them that’s the bare minimum required. They are all lovely individually but together they are awful, especially the twins. A graph of the amount of fights I had to break up over the last couple of weeks would require a log scale. The biggest problem is they don’t bear grudges so this increases the number of fights. The pattern is a major bust up, five minutes of hysteria, move on, forget about it, play for a few minutes until the next conflict and then the loop starts up again.

So holidays are coming to an end and dark September mornings writing the EMR are well and truly here. Given it’s the start of the month today, Henry will shortly be releasing our monthly performance review for August. Normally the summer holidays are a relatively quiet period for markets, and last month very much fit into that pattern, but that didn’t stop equities powering ahead to fresh all-time highs as they advanced for a 7th successive month. In fact, both the S&P 500 and the STOXX 600 are now up by over +20% YTD on a total returns basis, with a third of the year still remaining. At the other end of the leaderboard however, oil prices saw their biggest decline so far this year in August, as fears of weakening economic demand and concerns about the delta variant of Covid took their toll. More details in the report out shortly.

It might be the start of September today, but investors will be grappling with a number of familiar themes this morning. The tapering and inflation debate was a hot topic yesterday but more from Europe for once rather than the US. This coupled with weak data served to dampen sentiment and spark a selloff across various asset classes. The most significant data yesterday came from the Euro Area, where the flash CPI estimate for August came in at a far stronger-than-expected +3.0% (vs. +2.7% expected), which is the highest since November 2011, and was also above every economists’ estimate on Bloomberg. Then we had some weak consumer confidence data from the US Conference Board, which backed up the weak reading from the University of Michigan earlier in the month.And both the European inflation reading and US consumer sentiment data came against the backdrop of weak PMIs out of China heading into yesterday’s session.

Looking at yesterday’s developments, that strong Euro Area inflation print was by some way the most impactful on markets, and gave further ammunition to the ECB’s hawks who’ve been calling for a withdrawal of emergency support. Although core inflation only exceeded expectations by 0.1%, the +1.6% reading marked the highest core inflation since July 2012, which was the month that former ECB President (and now Italian PM) Mario Draghi made his “whatever it takes” pledge. At a similar time to the inflation release, Dutch central bank governor Knot said that he believes in an immediate slowdown in ECB purchases and supports ending their pandemic emergency purchase programme in March. Furthermore, Austrian governor Holzmann said that he was in favour of reducing the pace of purchases in Q4. With both the strong inflation reading and the hawkish comments, European sovereign bonds witnessed a significant selloff, with yields on 10yr bunds climbing +5.6bps to -0.38%, which is their biggest one-day move since March, whilst those on 10yr BTPs (+9.9bps) saw their biggest one-day move higher since February.

With sovereign bond yields moving sharply higher in Europe, equities indices lost ground with the STOXX 600 closing the session -0.38% lower. In the US the S&P 500 similarly fell back, with the index down -0.13% from the previous day’s record highs after drifting lower in the US afternoon. This occurred as macroeconomic data continues to surprise to the downside as the Conference Board’s consumer confidence reading came in at a 6-month low of 113.8 in August (vs. 123.0 expected). Looking at the sectoral breakdowns, the FANG+ index of megacap tech stocks was an outperformer, managing to close +0.36% higher to just about achieve a new all-time closing high, its first since mid-February. Meanwhile, yields on 10yr US Treasuries were up +3.0bps to 1.309%, however US banks (-0.58%) reversed earlier gains as cyclicals largely lagged.

Asian markets are generally trading higher this morning with the Nikkei (+1.17%), Hang Seng (+0.62%), Shanghai Comp (+0.86%) and Kospi (+0.25%) all advancing. Meanwhile, yields on 10y USTs are up +2.2 bps to 1.332% and those on Australia and New Zealand’s 10y sovereign bonds are up +9.2bps and +9.3bps respectively after the global sell-off yesterday. Futures on the S&P 500 are up +0.29% and those on the Stoxx 50 are +0.65%. Elsewhere, oil prices are up c.+0.70% ahead of today’s OPEC+ meeting.

Overnight China’s Caixin manufacturing PMI came in at 49.2 (vs. 50.1 expected and 50.2 last month). This was in contrast to yesterday’s official manufacturing PMI reading of 50.1 which was relatively stable. The Caixin PMI is more representative of smaller and private companies while the official PMI covers larger, state owned enterprises. Given the weakness in the PMIs, our China economist Yi Xiong is of the view that the PBoC should soon cut the MLF rate to support growth (to read more click the link here). Looking at other Asian manufacturing PMIs, Japan’s final manufacturing reading got revised up +0.3pts from the flash to 52.7 while Australia’s final manufacturing PMI also saw a similar upward revision of 0.3pts to 52.0. Taiwan’s continued to remain well in expansionary territory with a reading of 58.5 (vs. 59.7 last month). Meanwhile, Vietnam’s dropped substantially to 40.2 from 45.1 last month and South Korea’s reading softened to 51.2 from 53.0 but Indonesia’s improved to 43.7 (vs. 40. 1 last month). These readings generally point to a slightly softer manufacturing activity in the region during the month as most countries imposed restrictions to curb the spread of the delta variant.

In other overnight news, the BoJ Deputy Governor Masazumi Wakatabe indicated in a speech that the central bank may revise down its economic assessment at this month’s policy meeting as the spread of the delta variant has caused the expansion and extension of the state of emergency.

With September having arrived, we’re now finally in the month of the German election, for which yet more polls yesterday showed the centre-left SPD in the lead. The first from Ipsos had them at 25%, ahead of the CDU/CSU on 21% and the Greens at 19%. And then another from Forsa had a slightly tighter race at the top, with the SPD on 23%, the CDU/CSU on 21%, and the Greens on 18%. The SPD’s candidate for chancellor, German finance minister and Vice-Chancellor Olaf Scholz, has sought to project himself as the heir to Chancellor Merkel, with whom he’s currently serving in the grand coalition with. But yesterday Chancellor Merkel herself took aim at this portrayal, saying that a major difference between the two is that she would never go into coalition with Die Linke, whereas she said it “remains an open question” whether Scholz was of this view.

Turning to the pandemic, there was some positive news as European Commission President von der Leyen confirmed that 70% of adults in the EU were now fully vaccinated. Meanwhile vaccine “passports” are becoming more widespread with Italy requiring travellers on planes, ferries and long-haul trains show proof of vaccinations or a negative Covid-19 test.

Looking at yesterday’s other data, inflation in France came in at a stronger-than-expected +2.4% (vs. +2.1% expected) in August, using the EU harmonised measure, whilst the Italian reading also surprised to the upside at +2.6% (vs. +2.1% expected). Over in the US, the MNI Chicago PMI for August fell to 66.8 (vs. 68.0 expected), though the S&P CoreLogic Case-Shiller national home price index was up +18.6% year-on-year in June, which is the fastest since that series begins in 1988.

To the day ahead now, and the main data highlight will be the release of the global manufacturing PMIs and the ISM manufacturing reading from the US, but there’s also the Euro Area unemployment rate for July, along with the ADP’s report of private payrolls from the US for August. Otherwise, central bank speakers include the ECB’s Weidmann and the Fed’s Bostic.

Tyler Durden

Wed, 09/01/2021 – 07:58

via ZeroHedge News https://ift.tt/3Dxngxv Tyler Durden

Ohio Judge Orders Hospital To Treat Ventilated COVID-19 Patient With Ivermectin

By Lil Hai of Epoch Times

A Butler County judge in Ohio has ordered a hospital to administer Ivermectin to a ventilated COVID-19 patient, granting an emergency relief filed by the patient’s wife.

Butler County Common Pleas Judge Gregory Howard ruled last week that West Chester Hospital, part of the University of Cincinnati’s health network UC Health, must “immediately administer Ivermectin” to patient Jeffrey Smith following his doctor’s prescription of 30 mg of Ivermectin for 21 days, the Ohio Capital Journal reported.

Smith, 51, is a Verizon Wireless engineer in Butler County. According to the lawsuit (pdf) filed by his wife Julie Smith, Smith tested positive for COVID-19 on July 9, and he was admitted to West Chester Hospital on July 15. On the same day, he was moved to an intensive care unit (ICU).

Smith’s condition continued to decline, and he was placed on a ventilator on Aug. 1. By Aug. 19, the ventilator was operating at 80 percent volume, with Smith’s chances of survival dropping to less than 30 percent, court documents read. At that time, the hospital claimed to have exhausted all options in its COVID-19 treatment protocol.

“At this point, there is nothing more the defendant can do, or will do, for my husband,” Julie wrote in an affidavit included in her complaint.

“However, I cannot give up on him, even if the defendant has,” Julie continued. “There is no reason why the defendant cannot approve or authorize other forms of treatments so long as the benefits outweigh the risks.”

Julie had read about some lawsuits reported by Chicago Tribune and The Buffalo News where patients in severe condition from COVID-19 later recovered after being given Ivermectin.

These patients had won lawsuits forcing their hospitals to treat them with Ivermectin. The plaintiffs in these cases were all represented by attorney Ralph Lorigo, chairman of New York’s Erie County Conservative Party, who later became one of Julie’s attorneys.

According to court documents, Julie requested that the hospital treat her husband with Ivermectin, but the hospital refused to even though she offered to release them from “any and all” responsibility.

Julie then sought medical advice from Dr. Fred Wagshul, who later prescribed Ivermectin to her husband. But the hospital still refused to do so, prompting her to file a lawsuit against the hospital.

“With absolutely nothing to lose, with little to no risk, and with the defendant likely to begin palliative care, there is no basis for it to refuse Dr. Wagshul’s order and prescription to administer Ivermectin,” Julie said in the affidavit.

Wagshul is a founding member of the Frontline COVID-19 Critical Care Alliance (FLCCC), a nonprofit organization that is working during the pandemic to develop effective treatment protocols to prevent COVID-19 infection as well as treat patients with COVID-19.

In October of 2020, FLCCC adopted Ivermectin as a core medication in its protocols for preventing and treating COVID-19. Its website references many recent studies reporting Ivermectin to be a safe, effective, and inexpensive drug against COVID-19, the disease caused by CCP (Chinese Communist Party) virus.

“Ivermectin is so safe,” Wagshul told Dayton247Now. “It essentially has no drug interactions and no side effects.”

The UC Health hasn’t responded to a request from The Epoch Times for comment. According to the Ohio Capital Journal, it hasn’t challenged the judge’s ruling.

Federal Agencies Oppose Ivermectin For COVID-19

Ivermectin is a drug that has been approved by the Food and Drug Administration (FDA) to treat certain infections caused by internal and external parasites. A Japanese scientist and an Irish-American scientist were awarded the Nobel Prize in 2015 for their discovery of Ivermectin, given the drug’s success at improving the health and wellbeing of millions of individuals infected with river parasites in the poorest regions of the world.

President Joe Biden’s top medical adviser, Dr. Anthony Fauci, has advised people against using Ivermectin to treat COVID-19.

“Don’t do it. There’s no evidence whatsoever that it works, and it could potentially have toxicity,” Fauci told CNN on Sunday. “There’s no clinical evidence that indicates that this works.”

Last Thursday, the Centers for Disease Control and Prevention (CDC) issued an official health advisory (pdf), reiterating its opposition to the use of Ivermectin for COVID-19 treatment.

“Ivermectin is not authorized or approved by FDA for prevention or treatment of COVID-19,” the advisory reads. “The National Institutes of Health’s (NIH) COVID-19 Treatment Guidelines Panel has also determined that there are currently insufficient data to recommend Ivermectin for treatment of COVID-19.”

“Adverse effects associated with Ivermectin misuse and overdose are increasing, as shown by a rise in calls to poison control centers reporting overdoses and more people experiencing adverse effects,” the advisory continued.

FDA warned on its website that taking large doses of Ivermectin is “dangerous and can cause serious harm.” The agency also stressed that Ivermectin products for animals are different from products for people because animal drugs are often highly concentrated.

“Such high doses can be highly toxic in humans,” FDA said.

Tyler Durden

Wed, 09/01/2021 – 07:46

via ZeroHedge News https://ift.tt/3t5YXSn Tyler Durden

9/1/1823: Justice Smith Thompson takes judicial oath.

from Latest – Reason.com https://ift.tt/3DBfwKN

via IFTTT

The closest approximations to eternal toddlers in our society may be government officials told there are limits on the extent to which they can screw with human lives. They rant, they pout, and sometimes they even vow to poke and prod others anyway, daring anybody to make them stop. The distilled essence of a thwarted brat was on prominent display last week when New York City’s mayor raged at the United States Supreme Court for daring to say that, even during a time of perceived crisis, a government agency can’t unilaterally let people squat on private property.

“A group of right wing extremists just decided to throw families out of their homes during a global pandemic,” Mayor Bill de Blasio responded to a decision voiding the Biden administration’s extension of the national eviction moratorium. “This is an attack on working people across our country and city. New York won’t stand for this vile, unjust decision.”

The reaction was especially off the wall given that the Supreme Court warned that the Centers for Disease Control and Prevention (CDC) have no authority to suspend property rights. Even President Joe Biden conceded that his executive branch didn’t have the authority the CDC asserted during both his and the preceding Trump administration.

“The bulk of the constitutional scholarship says that it’s not likely to pass constitutional muster,” the president admitted on August 3. Not that a lack of authority held him back.

“But, at a minimum, by the time it gets litigated, it will probably give some additional time while we’re getting that $45 billion out to people who are, in fact, behind in the rent and don’t have the money,” Biden added, explaining that he was going ahead with the eviction moratorium despite a lack of authority to do so because it’s all for a good cause.

That should be an interesting precedent for future officials who decide that a lack of authority is no reason to refrain from bypassing checks and balances or even outright ignoring fundamental rights while the matter “gets litigated.” After all, Biden is far from rare among government officials in invoking good intentions as justification for wandering far beyond the bounds of permissible authority.

“Today’s decision is a direct threat to public safety and the lives of innocent Californians, period,” California Gov. Gavin Newsom snorted after a federal judge struck down the state’s ban on some semi-automatic rifles. He ignored the court’s finding that the type of firearm restricted by the law “is the kind of versatile gun that lies at the intersection of the kinds of firearms protected under District of Columbia v. Heller” landmark 2008 Supreme Court Second Amendment decision.

“What’s not up for debate is that our early and decisive action saved lives,” sniffed Pennsylvania Gov. Tom Wolf after another federal judge pointed out that “the Constitution cannot accept the concept of a ‘new normal’ where the basic liberties of the people can be subordinated to open-ended emergency-mitigation measures.”

Maybe it’s something in New York’s water, but former President Donald Trump sounded positively de Blasio-esque in 2017 when a judge thwarted his will (or, perhaps more accurately, de Blasio later emulated his former constituent’s lead).

“The opinion of this so-called judge, which essentially takes law-enforcement away from our country, is ridiculous and will be overturned!” Trump huffed after a federal judge overturned his ban on travel from seven Muslim-majority countries.

Then again, this was the same guy who told an audience, “I have the right to do whatever I want as president but, I don’t even talk about that.”

That got a lot of coverage at the time, but the conduct of many officeholders makes it clear that Trump just said what other officials believe. Since then, as Wolf, Newsom, Biden, and now de Blasio illustrate, saying the quiet part out loud has become increasingly popular. Politicians and their supporters resent restrictions on the exercise of power, lash out at anybody who would keep their actions within any sort of limits, and openly exercise authority that they publicly acknowledge doesn’t exist.

Undoubtedly, people who go into government have always chafed at any effort to make them live within legal and constitutional constraints. Government, after all, is defined by the use of coercive power. That the power is supposed to be exercised only within limits must be frustrating to people who were attracted by the opportunity to coerce others for reasons that they always argue are the very best.

Worse, recent years have seen growing animosity between political factions in the United States which have grown impatient with protections for the rights of their enemies. Driving this, in part, is “‘partisan moral disengagement,’ which entails seeing the other party as evil, less than human and a serious threat to the nation,” as political scientists Lilliana Mason and Nathan Kalmoe wrote earlier this year. Why, many people ask themselves, respect restraints that stand in the way of purging evil from this world?

Then the pandemic, involving real public health threats as well as exaggerated fears, ruptured limits on the exercise of power.

“Governors in most states possess the power to act unilaterally and without need for any legislative approval, in ways not fully appreciated prior to the coronavirus, and in ways that are already leading to a reconsideration of some state emergency-power arrangements,” John Dinan, a Wake Forest University professor of politics, noted last year. It was an updated acknowledgement of Robert Higgs’s observation that crises drive growth in government power (and it rarely returns to its original state).

Even before the stresses and strains of the last few years, government officials were already attracted to power and inclined to test its limits. Factionalization and crisis have eroded the restraints on that power. And now, like toddlers, the people who rule over us feel justified in doing what they please to those at their mercy and are outraged by anybody who pushes back.

from Latest – Reason.com https://ift.tt/3DAjUJQ

via IFTTT

9/1/1823: Justice Smith Thompson takes judicial oath.

from Latest – Reason.com https://ift.tt/3DBfwKN

via IFTTT

The closest approximations to eternal toddlers in our society may be government officials told there are limits on the extent to which they can screw with human lives. They rant, they pout, and sometimes they even vow to poke and prod others anyway, daring anybody to make them stop. The distilled essence of a thwarted brat was on prominent display last week when New York City’s mayor raged at the United States Supreme Court for daring to say that, even during a time of perceived crisis, a government agency can’t unilaterally let people squat on private property.

“A group of right wing extremists just decided to throw families out of their homes during a global pandemic,” Mayor Bill de Blasio responded to a decision voiding the Biden administration’s extension of the national eviction moratorium. “This is an attack on working people across our country and city. New York won’t stand for this vile, unjust decision.”

The reaction was especially off the wall given that the Supreme Court warned that the Centers for Disease Control and Prevention (CDC) have no authority to suspend property rights. Even President Joe Biden conceded that his executive branch didn’t have the authority the CDC asserted during both his and the preceding Trump administration.

“The bulk of the constitutional scholarship says that it’s not likely to pass constitutional muster,” the president admitted on August 3. Not that a lack of authority held him back.

“But, at a minimum, by the time it gets litigated, it will probably give some additional time while we’re getting that $45 billion out to people who are, in fact, behind in the rent and don’t have the money,” Biden added, explaining that he was going ahead with the eviction moratorium despite a lack of authority to do so because it’s all for a good cause.

That should be an interesting precedent for future officials who decide that a lack of authority is no reason to refrain from bypassing checks and balances or even outright ignoring fundamental rights while the matter “gets litigated.” After all, Biden is far from rare among government officials in invoking good intentions as justification for wandering far beyond the bounds of permissible authority.

“Today’s decision is a direct threat to public safety and the lives of innocent Californians, period,” California Gov. Gavin Newsom snorted after a federal judge struck down the state’s ban on some semi-automatic rifles. He ignored the court’s finding that the type of firearm restricted by the law “is the kind of versatile gun that lies at the intersection of the kinds of firearms protected under District of Columbia v. Heller” landmark 2008 Supreme Court Second Amendment decision.

“What’s not up for debate is that our early and decisive action saved lives,” sniffed Pennsylvania Gov. Tom Wolf after another federal judge pointed out that “the Constitution cannot accept the concept of a ‘new normal’ where the basic liberties of the people can be subordinated to open-ended emergency-mitigation measures.”

Maybe it’s something in New York’s water, but former President Donald Trump sounded positively de Blasio-esque in 2017 when a judge thwarted his will (or, perhaps more accurately, de Blasio later emulated his former constituent’s lead).

“The opinion of this so-called judge, which essentially takes law-enforcement away from our country, is ridiculous and will be overturned!” Trump huffed after a federal judge overturned his ban on travel from seven Muslim-majority countries.

Then again, this was the same guy who told an audience, “I have the right to do whatever I want as president but, I don’t even talk about that.”

That got a lot of coverage at the time, but the conduct of many officeholders makes it clear that Trump just said what other officials believe. Since then, as Wolf, Newsom, Biden, and now de Blasio illustrate, saying the quiet part out loud has become increasingly popular. Politicians and their supporters resent restrictions on the exercise of power, lash out at anybody who would keep their actions within any sort of limits, and openly exercise authority that they publicly acknowledge doesn’t exist.

Undoubtedly, people who go into government have always chafed at any effort to make them live within legal and constitutional constraints. Government, after all, is defined by the use of coercive power. That the power is supposed to be exercised only within limits must be frustrating to people who were attracted by the opportunity to coerce others for reasons that they always argue are the very best.

Worse, recent years have seen growing animosity between political factions in the United States which have grown impatient with protections for the rights of their enemies. Driving this, in part, is “‘partisan moral disengagement,’ which entails seeing the other party as evil, less than human and a serious threat to the nation,” as political scientists Lilliana Mason and Nathan Kalmoe wrote earlier this year. Why, many people ask themselves, respect restraints that stand in the way of purging evil from this world?

Then the pandemic, involving real public health threats as well as exaggerated fears, ruptured limits on the exercise of power.

“Governors in most states possess the power to act unilaterally and without need for any legislative approval, in ways not fully appreciated prior to the coronavirus, and in ways that are already leading to a reconsideration of some state emergency-power arrangements,” John Dinan, a Wake Forest University professor of politics, noted last year. It was an updated acknowledgement of Robert Higgs’s observation that crises drive growth in government power (and it rarely returns to its original state).

Even before the stresses and strains of the last few years, government officials were already attracted to power and inclined to test its limits. Factionalization and crisis have eroded the restraints on that power. And now, like toddlers, the people who rule over us feel justified in doing what they please to those at their mercy and are outraged by anybody who pushes back.

from Latest – Reason.com https://ift.tt/3DAjUJQ

via IFTTT

Biden Told Afghan President To “Create Perception” Taliban Wasn’t Winning “Whether It Is True Or Not”

Despite all evidence to the contrary, President Biden appeared before the American people on Tuesday to try to sell his version of the American withdrawal from Afghanistan.

With a straight face, Biden half-shouted to the American people about the “extraordinary success” of the evacuation effort – an assessment that seemed completely at odds with the reality of the situation – before trotting out some equally specious stats: the US had successfully evacuated 90% of Americans who wanted to leave Kabul, and Biden committed to doing everything in his power to help those left behind.

But just as President Biden was delivering his prepared remarks, Reuters was quietly publishing a leaked transcript from the president’s final call with Ashraf Ghani, which took place in late July. The call offers a more realistic picture of a Biden Administration obsessed with the optics of the pullout, who was still pushing the Afghans to focus on an irrelevant strategy shift to try and make it look like they were doing something in the face of Taliban defeat.

A few weeks later, the Afghan president fled Kabul with sacks full of plundered cash just before the Taliban surrounded the city. He’s now believed to be hiding in the UAE.

Although Biden seemed aware that the situation on the ground appeared grim, Biden demanded that Ghani project “a different picture” to the press and the international community “whether or not it was true”.

“I need not tell you the perception around the world and in parts of Afghanistan, I believe, is that things are not going well in terms of the fight against the Taliban,” Biden said. “And there is a need, whether it is true or not, there is a need to project a different picture.”

Biden told Ghani that if Afghanistan’s prominent political figures were to give a press conference together, backing a new military strategy, “that will change perception, and that will change an awful lot I think.”

It’s also clear that Biden knew it was only a matter of time before the Taliban completed its takeover of the country. His main goal was making sure Ghani did everything in his power to try and manage the Afghan Army’s defeat with as little embarrassment as possible.

Despite probably knowing that details from his final call with Ghani would surface, Biden repeated his claims that nobody could have anticipated the Taliban’s rapid advance.

During the call, the Afghan president pleaded with Biden for more air support and a raise for Afghan soldiers who hadn’t received one in a decade, Biden offered mostly platitudes.

“We are going to continue to fight hard, diplomatically, politically, economically, to make sure your government not only survives, but is sustained and grows,” said Biden.

By the time the two leaders spoke on July 23, roughly 23 days before the fall of Kabul, Taliban insurgents controlled roughly half of Afghanistan’s district centers as the situation in the country rapidly deteriorated. Around this time, Biden insisted that the fall of Afghanistan to the Taliban wasn’t inevitable.

Although the situation in Afghanistan was already dire, and the American forces were withdrawing their air support, Biden continued to push Ghani about holding a press conference to announce a new military “strategy” that was really just window dressing.

“But I really think, I don’t know whether you’re aware, just how much the perception around the world is that this is looking like a losing proposition, which it is not, not that it necessarily is that, but so the conclusion I’m asking you to consider is to bring together everyone from [Former Vice President Abdul Rashid] Dostum, to [Former President Hamid] Karzai and in between,” he said.

“If they stand there and say they back the strategy you put together, and put a warrior in charge, you know a military man, Khan in charge of executing that strategy, and that will change perception, and that will change an awful lot I think.”

Ghani responded by saying Afghanistan was facing not just the Taliban, but their foreign backers.

“We are facing a full-scale invasion, composed of Taliban, full Pakistani planning and logistical support, and at least 10-15,000 international terrorists, predominantly Pakistanis thrown into this.”

In other words, the problem of defeating the Taliban wasn’t going to be fixed by a press conference. And the new “strategy” of abandoning rural areas to protect population centers was really the last available course of action, since the Taliban dominated the rural districts.

The bottom line is this: President Biden clearly knew the dissolution of the Afghan government and swift triumph of the Taliban was inevitable, but he was so preoccupied with managing the optics of the pullout, that he neglected to focus on planning for the final stages of the US withdrawal, all while appearing to believe his own BS about changing the strategy on the ground.

Tyler Durden

Wed, 09/01/2021 – 07:01

via ZeroHedge News https://ift.tt/3juOc90 Tyler Durden

US Navy Helicopter Crashes Off San Diego Coast

A US helicopter embarked from USS Abraham Lincoln stationed in San Diego crashed into the sea while conducting routine flight operations off the coast, according to U.S. 3rd Fleet Public Affairs.

The Sikorsky SH-60 Seahawk was carrying a crew of six when it crashed into the ocean approximately 60 nautical miles off the coast of San Diego around 1630 local time Tuesday.

“An MH-60S helicopter embarked aboard USS Abraham Lincoln (CVN 72) crashed into the sea while conducting routine flight operations approximately 60 nautical miles off the coast of San Diego at 4:30 p.m. PST, Aug. 3.

“Search and rescue operations are ongoing with multiple Coast Guard and Navy air and surface assets. More information will be posted as it becomes available.

“Currently, one crew member has been rescued and search efforts continue for the other crewmembers continue.” -U.S. 3rd Fleet Public Affairs

The cause of the crash was not immediately known.

If you’ve ever been to San Diego, the Seahawks are a common fixed rotor military helicopter seen in the skies.

Retired Air Force Maj. Glenn Ignazio told FOX 5 the Seahawk has an “exceptional safety record” over two decades. The helicopter was first introduced in 1979.

“The Blackhawk main body that it is built off of is the same aircraft that is used throughout the Air Force, the Army and, of course, many militaries around the world,” Ignazio said. “It’s a very safe aircraft.”

More updates will follow on the status of the remaining crew members that Coast Guard and Navy air and surface assets continue to search for in the early hours on Wednesday.

Tyler Durden

Wed, 09/01/2021 – 06:50

via ZeroHedge News https://ift.tt/38t6P71 Tyler Durden