History has a way of repeating itself. Or maybe it’s that people cling to defunct beliefs, stubbornly refusing to learn from experience. Such stubbornness is on display when pundits, legislators, and President Joe Biden blame inflation on corporate “greed.” The fix, they claim, is price controls. But such controls would only bring further economic calamity.

To explain hikes in the prices of meat, poultry, and energy, many politicians and pundits say we must look no further than cold-hearted corporate CEOs padding their bottom lines at the expense of ordinary Americans. Companies today are allegedly so greedy that they use the pandemic as an excuse to charge extortionate prices. For example, Sen. Elizabeth Warren (D–Mass.) told MSNBC’s Chris Hayes that “giant corporations who say, wow, a lot of talk about high prices and inflation. This is a chance to get in there and not only pass along costs, but to inflate prices beyond that and just engage in a little straightforward price gouging.”

Playing along with this blame game is Biden, who asserts that “oil and gas companies shouldn’t pad their profits at the expense of hardworking Americans.”

Biden is not the first president to demonstrate ignorance of the complex factors that determine prices at the pump. His and others’ grandstanding complaints about high prices—especially as they rise during inflationary times—aren’t novel. George Mason University’s Don Boudreaux recently highlighted a still-relevant observation from 1976 by the late UCLA economist Armen Alchian:

“Direct attacks on the symptoms known to flow from inflation are politically convenient. As inflation occurs, politicians and the public blame businessmen and producers for raising prices and mulcting the public….The so-called shortage of gasoline and energy in the United States was precisely and only such a political attack.”

Today, we should remember Alchian’s sobering description of what happened when economically illiterate politicians attempted to control inflation by imposing price controls:

“Inflate the money stock; when prices rise, impose price controls to correct the situation. These controls lead to shortages which ‘require’ government intervention to assure appropriate use of the limited supply and to allocate it and even to control and nationalize the production of energy. The powers of political authorities are increased; the open society is suppressed.”

The unrealistic assumptions underpinning the logic of those who argue for price controls are quite amazing. First, hikes in prices apparently have no impact on consumers’ demand for goods. That’s because monopolies are supposedly everywhere, and most goods—we are to believe—are so indispensable to consumers that we will buy nearly all of them at any price.

In addition, the price controllers bizarrely assume that when faced with bans on price increases, producers (who are also coping with inflation and other challenges) will keep supplying the same goods to market. So, the only impact price controls are said to have is to decrease the amounts consumers pay, while having no effect on consumption or production.

This belief, of course, is nonsense. When prices rise, consumers reduce their demands for goods (unless inflation expectations come into play, and consumers increase purchases today to avoid even higher prices tomorrow). Also, companies prohibited by law from raising their prices will reduce their supplies, thus creating the shortages Alchian warned about.

To believe that inflation is the product of corporate greed requires even more obliviousness to reality. Inflation is truly a general and ongoing increase of all prices, including wages (which are the price of our labor). This reality means that all companies would have to be getting greedier simultaneously, and that all workers are, at the same time, overcome with similar avarice.

On that note, if corporate greed is sufficient to allow companies to get away with raising prices, why isn’t it sufficient to allow them to resist demands for higher wages?

The fact is that inflation isn’t caused by corporate greed. Readers of this column know by now that it’s caused by government’s excessive deficit spending, fueled in part by loose monetary policy. Therefore, getting rid of inflation requires an increase of interest rates theoretically higher than the current inflation, along with some overdue fiscal discipline. Reforms like deregulation that promote faster growth in the supply of goods and services would also help.

What we don’t need, but what we’ll likely get, is more government spending and more debt accumulation. The result will only fuel the inflation fire. Let’s hope that we at least avoid making matters even worse with price controls.

Efforts to punish Russia for invading Ukraine rely not just on funneling weapons to the beleaguered defenders but also on economic sanctions to deny Vladimir Putin’s regime resources and to inflict pain until the aggression stops. Among the targets are “Russian elites and their families,” in President Joe Biden’s words, whose assets are being seized to pressure the regime. But calling somebody an “oligarch” is no substitute for legal proceedings, and the U.S. government is stretching already sketchy asset forfeiture powers in ways that will, no doubt, create precedents for the future.

“Did you see these yachts we’re—that are being picked up?” President Biden boasted this week. “Think about the—the incredible amounts of money these oligarchs have stolen. These yachts are a hundred—millions and millions of dollars.”

The president riffed off a Justice Department announcement of the seizure of “a $90 million yacht— named the Tango — belonging to sanctioned Russian oligarch Viktor Vekselberg.” Spanish authorities took the yacht using a U.S. warrant issued as part of Task Force KleptoCapture, launched after the invasion “to hold accountable corrupt Russian oligarchs.” KleptoCapture is a catchy name, but it glosses over the fact that, while many wealthy Russians are close to Putin’s regime, calling them “oligarchs” isn’t the same as demonstrating that they share responsibility for the war.

“The western media employ the term ‘oligarch’ to describe super-wealthy Russians in general, including those now wholly or largely resident in the west,” Anatol Lieven of the Quincy Institute for Responsible Statecraft wrote last month in the Financial Times. “The term gained traction in the 1990s, and has long been seriously misused. In the time of President Boris Yeltsin, a small group of wealthy businessmen did indeed dominate the state, which they plundered in collaboration with senior officials. This group was, however, broken by Putin during his first years in power.”

Putin still has an inner circle of cronies who wield power and bear responsibility for invading Ukraine, but being Russian, rich, and labeled “oligarch” isn’t proof of being one of them. That’s important, because the West, in general, and the United States, in particular, is supposed to prove that private individuals engaged in crimes before imposing punishment.

“Serious legal questions surround the seizures of boats, planes and other property owned by oligarchs,” warns George Washington University Law School’s Jonathan Turley. “In these largely uncharted waters, many of the owners are likely to get back their yachts and other property after the headlines have receded. The United States and Western countries have considerable authority to seize property, but less authority to keep it. The reason is that, unlike Russia, these countries are bound by property rights and rules of due process.”

True, few people harbor much sympathy for Russians of any sort these days; Rep. Eric Swalwell (D–Calif.) infamously called for expelling Russian students from the country. And owning a yacht that can be seized, let alone one worth $90 million, doesn’t guarantee much sympathy from the public. But being rich doesn’t erase your rights, and it means that you have the resources to defend yourself in ways not always available to regular people subject to official attention.

“While freezing an asset is a relatively simple task, seizing and taking over properties is more involved. It requires a lengthy legal process that takes years in many cases, according to several experts on the subject,” Janaki Chadha observed in Politico. “Seizures can be further complicated by the fact that ownership of most if not all of the Russian oligarchs’ properties is shielded by shell companies.”

Contrast that with the experience of Terry Abbott from whom Indiana police seized $10,000 in 2015. “Cops used a process known as civil forfeiture, allowing them to proceed with pocketing those funds prior to securing a criminal conviction,” Billy Binion reported for Reason. “Naturally, Abbott attempted to challenge that action in court. But he lost his attorney—as the money he would use to pay for that counsel had been taken by the state.”

“While I support further reforms to expand the role of a criminal conviction in asset forfeiture, this bill is a step forward to create higher burdens of proof imposed on the seizure of private property by the government,” Pennsylvania Gov. Tom Wolf (D) said upon signing a reform measure in 2017.

But unpopular targets can breathe new life into abusive practices, and Vekselberg’s property was seized under the same authority as was wielded against Abbott. The federal government sued and seized the yacht itself without proving its owner engaged in wrongdoing. Of course, Vekselberg has the resources to battle the U.S. government through the courts. In the meantime, the property must be kept up.

“A vessel is treated very much like a person or corporation,” Michael Karcher, a maritime lawyer toldRobb Report, which focuses on luxury lifestyles. “The boat can run up its own bills. Then, if the yacht is in someone’s boatyard, there’s the question of ‘Can we do any business with them?'” The publication also predicts “prolonged legal battles and hefty costs to maintain these gigayachts.”

Ultimately, the United States government may lose, adds Turley, because “prosecutors would have to show that large corporations that have operated for decades in international markets are now deemed criminal enterprises for the purposes of these properties. It is not clear that governments now seizing the property will be able to establish the nexus between an alleged crime and these proceeds or property for some, if not most, of the oligarchs.”

A proposed bill might provide a firmer legal basis for seizures. “The legislation encourages the administration to confiscate any property – including luxury villas, yachts, and airplanes – valued over $5 million from Russian oligarchs previously sanctioned by the U.S. government for their involvement in the Kremlin’s invasion and human rights violations in Ukraine,” according to Rep. Tom Malinowski (D–N.J.) who is co-sponsoring the bill with Rep. Joe Wilson (R–S.C.). But rather than address due process concerns, the bill makes private property forfeit based on little more than officials’ claims that its owners are linked to Putin. Lowering the bar to forfeiture reverses reform efforts and may come back to haunt us.

Russian billionaires will probably survive economic sanctions in relative comfort. But the precedent set by labeling people as untouchables and then imposing penalties without proof of a crime will set the tone for future abuses. Powers used against wealthy Russians now will be deployed in the years to come against people who cross the authorities and have fewer resources for defending themselves.

4/8/1952: President Truman signs executive order 10340. The Supreme Court declared this executive order unconstitutional in Youngstown Sheet & Tube Co v. Sawyer(1952).

Efforts to punish Russia for invading Ukraine rely not just on funneling weapons to the beleaguered defenders but also on economic sanctions to deny Vladimir Putin’s regime resources and to inflict pain until the aggression stops. Among the targets are “Russian elites and their families,” in President Joe Biden’s words, whose assets are being seized to pressure the regime. But calling somebody an “oligarch” is no substitute for legal proceedings, and the U.S. government is stretching already sketchy asset forfeiture powers in ways that will, no doubt, create precedents for the future.

“Did you see these yachts we’re—that are being picked up?” President Biden boasted this week. “Think about the—the incredible amounts of money these oligarchs have stolen. These yachts are a hundred—millions and millions of dollars.”

The president riffed off a Justice Department announcement of the seizure of “a $90 million yacht— named the Tango — belonging to sanctioned Russian oligarch Viktor Vekselberg.” Spanish authorities took the yacht using a U.S. warrant issued as part of Task Force KleptoCapture, launched after the invasion “to hold accountable corrupt Russian oligarchs.” KleptoCapture is a catchy name, but it glosses over the fact that, while many wealthy Russians are close to Putin’s regime, calling them “oligarchs” isn’t the same as demonstrating that they share responsibility for the war.

“The western media employ the term ‘oligarch’ to describe super-wealthy Russians in general, including those now wholly or largely resident in the west,” Anatol Lieven of the Quincy Institute for Responsible Statecraft wrote last month in the Financial Times. “The term gained traction in the 1990s, and has long been seriously misused. In the time of President Boris Yeltsin, a small group of wealthy businessmen did indeed dominate the state, which they plundered in collaboration with senior officials. This group was, however, broken by Putin during his first years in power.”

Putin still has an inner circle of cronies who wield power and bear responsibility for invading Ukraine, but being Russian, rich, and labeled “oligarch” isn’t proof of being one of them. That’s important, because the West, in general, and the United States, in particular, is supposed to prove that private individuals engaged in crimes before imposing punishment.

“Serious legal questions surround the seizures of boats, planes and other property owned by oligarchs,” warns George Washington University Law School’s Jonathan Turley. “In these largely uncharted waters, many of the owners are likely to get back their yachts and other property after the headlines have receded. The United States and Western countries have considerable authority to seize property, but less authority to keep it. The reason is that, unlike Russia, these countries are bound by property rights and rules of due process.”

True, few people harbor much sympathy for Russians of any sort these days; Rep. Eric Swalwell (D–Calif.) infamously called for expelling Russian students from the country. And owning a yacht that can be seized, let alone one worth $90 million, doesn’t guarantee much sympathy from the public. But being rich doesn’t erase your rights, and it means that you have the resources to defend yourself in ways not always available to regular people subject to official attention.

“While freezing an asset is a relatively simple task, seizing and taking over properties is more involved. It requires a lengthy legal process that takes years in many cases, according to several experts on the subject,” Janaki Chadha observed in Politico. “Seizures can be further complicated by the fact that ownership of most if not all of the Russian oligarchs’ properties is shielded by shell companies.”

Contrast that with the experience of Terry Abbott from whom Indiana police seized $10,000 in 2015. “Cops used a process known as civil forfeiture, allowing them to proceed with pocketing those funds prior to securing a criminal conviction,” Billy Binion reported for Reason. “Naturally, Abbott attempted to challenge that action in court. But he lost his attorney—as the money he would use to pay for that counsel had been taken by the state.”

“While I support further reforms to expand the role of a criminal conviction in asset forfeiture, this bill is a step forward to create higher burdens of proof imposed on the seizure of private property by the government,” Pennsylvania Gov. Tom Wolf (D) said upon signing a reform measure in 2017.

But unpopular targets can breathe new life into abusive practices, and Vekselberg’s property was seized under the same authority as was wielded against Abbott. The federal government sued and seized the yacht itself without proving its owner engaged in wrongdoing. Of course, Vekselberg has the resources to battle the U.S. government through the courts. In the meantime, the property must be kept up.

“A vessel is treated very much like a person or corporation,” Michael Karcher, a maritime lawyer toldRobb Report, which focuses on luxury lifestyles. “The boat can run up its own bills. Then, if the yacht is in someone’s boatyard, there’s the question of ‘Can we do any business with them?'” The publication also predicts “prolonged legal battles and hefty costs to maintain these gigayachts.”

Ultimately, the United States government may lose, adds Turley, because “prosecutors would have to show that large corporations that have operated for decades in international markets are now deemed criminal enterprises for the purposes of these properties. It is not clear that governments now seizing the property will be able to establish the nexus between an alleged crime and these proceeds or property for some, if not most, of the oligarchs.”

A proposed bill might provide a firmer legal basis for seizures. “The legislation encourages the administration to confiscate any property – including luxury villas, yachts, and airplanes – valued over $5 million from Russian oligarchs previously sanctioned by the U.S. government for their involvement in the Kremlin’s invasion and human rights violations in Ukraine,” according to Rep. Tom Malinowski (D–N.J.) who is co-sponsoring the bill with Rep. Joe Wilson (R–S.C.). But rather than address due process concerns, the bill makes private property forfeit based on little more than officials’ claims that its owners are linked to Putin. Lowering the bar to forfeiture reverses reform efforts and may come back to haunt us.

Russian billionaires will probably survive economic sanctions in relative comfort. But the precedent set by labeling people as untouchables and then imposing penalties without proof of a crime will set the tone for future abuses. Powers used against wealthy Russians now will be deployed in the years to come against people who cross the authorities and have fewer resources for defending themselves.

4/8/1952: President Truman signs executive order 10340. The Supreme Court declared this executive order unconstitutional in Youngstown Sheet & Tube Co v. Sawyer(1952).

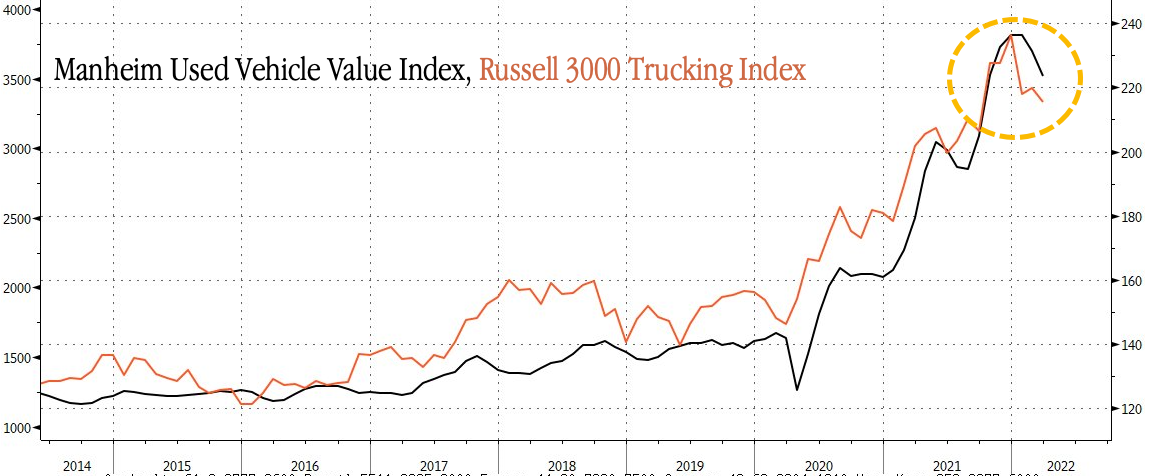

Are Used Car Prices About To Peak For Real This Time?

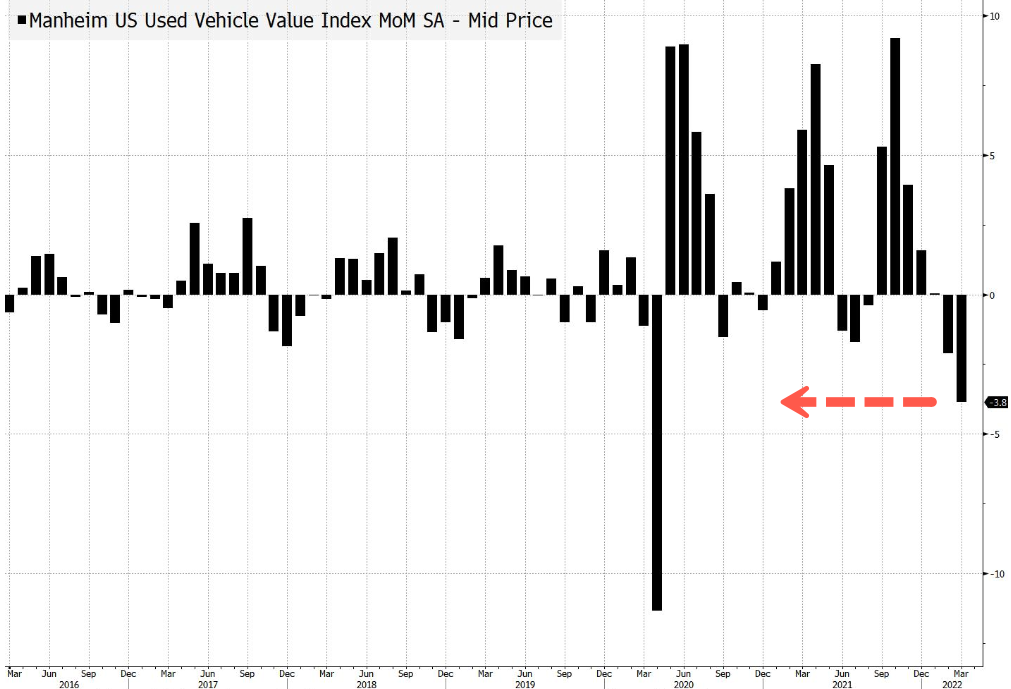

The Manheim Used Vehicle Value Index, a wholesale tracker of used car prices, fell 3.8% in March from February, the largest monthly decline since April 2020 (only Feb 2007 and two prints in the fall of 2008 were worse before that). Given its significance as a contributor to the overall headline inflation rates in the US, this could well be a critical inflection point (as rising rates begin to work their disinflationary way through the economy and peak supply chain crisis passes).

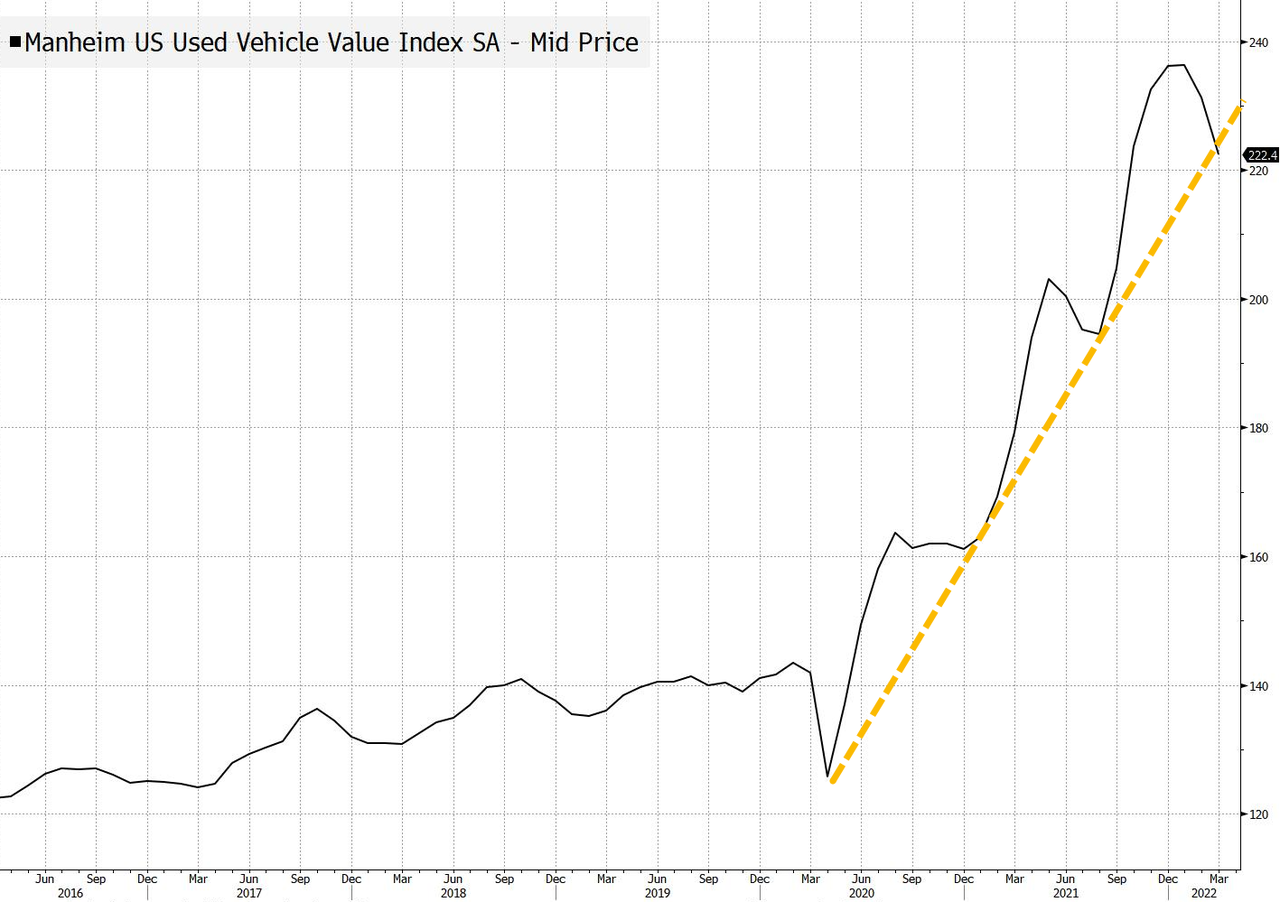

Used car prices have gone bonkers over the last two years, reaching record highs in February, but appear to have stalled since February. Last month, the used car index declined to 222.4 (the lowest since Sept 2021). That is still up about 24.5% from a year ago (but, most notably the upside momentum is slowing).

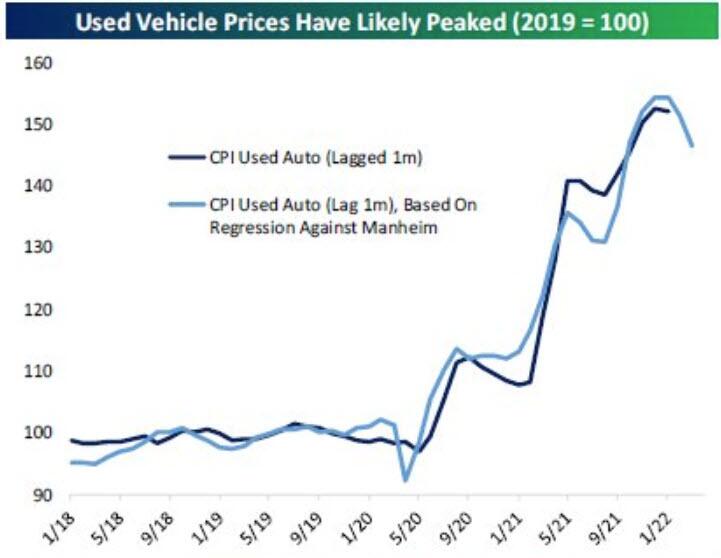

As Bespoke shows in the chart below, CPI for used vehicles hasn’t been perfectly correlated to the Manheim index, but the two are at least loosely related. Manheim tends to lead used auto CPI, and has fallen faster during recent price slowdowns than the BLS estimate of prices paid by consumers.

As a result, we are skeptical that the 2.1% decline in prices for February will lead to a huge CPI Used Auto drop in March, but it will likely work out to 1-2%. Similarly, we are skeptical that a 3.9% drop MoM in March Manheim Used Auto prices will lead to a similarly large fall in the equivalent CPI index for April.

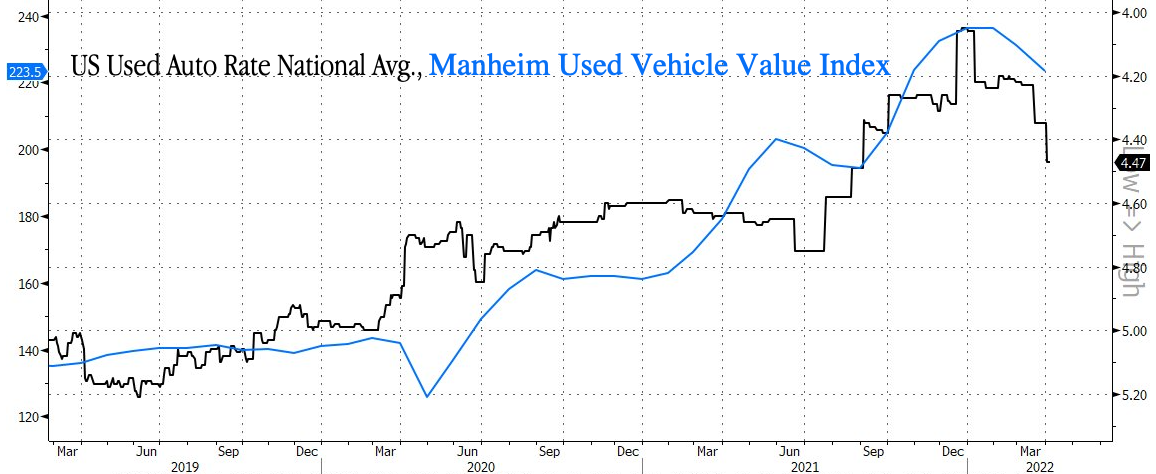

Notably, given The Fed’s recent hawkishness, used car prices crested just as the average interest rate for used vehicles sank as low as 4% and has since moved higher…

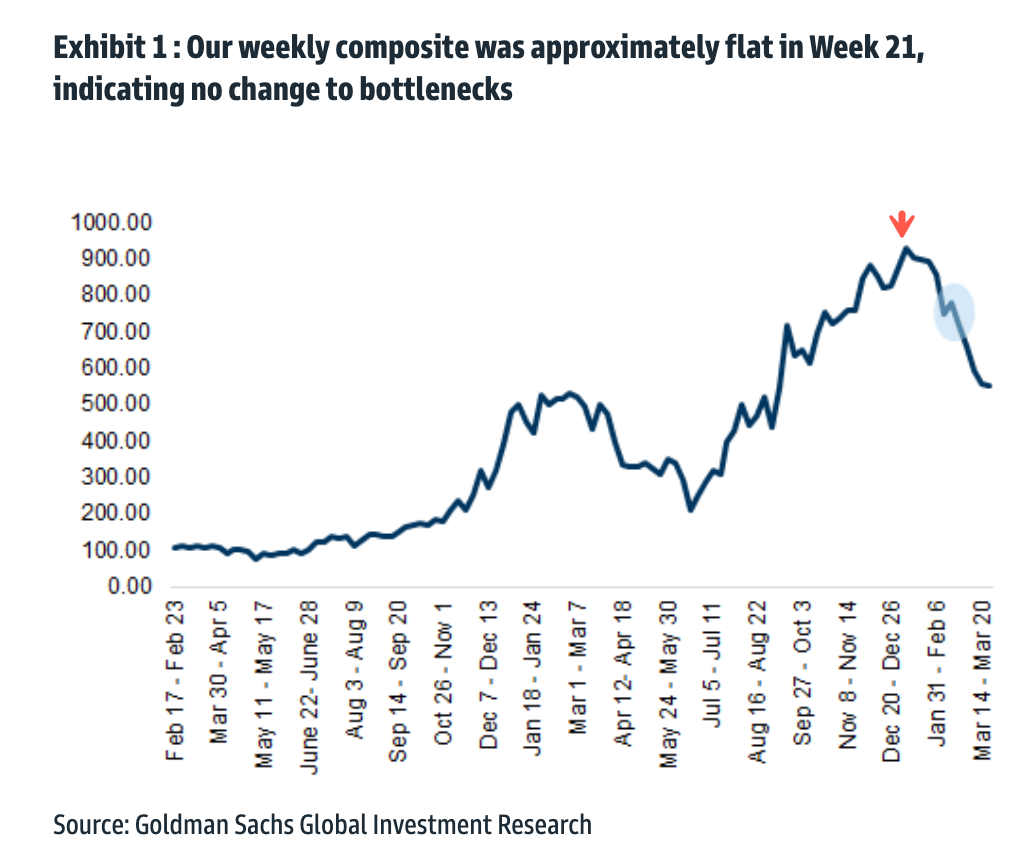

Since early February, we’ve pointed out that used car prices could be at “yet another major inflection point.” By late March, used car prices declined even more as Goldman Sachs and others suggested peak supply chain congestion might have already passed. Goldman’s high-frequency congestion scale of global supply chains is well off its high of 10 earlier this year, currently at 6/10. The index is still elevated, though it appears to be passed the peak, encouraging news for automakers who may soon boost new car supply.

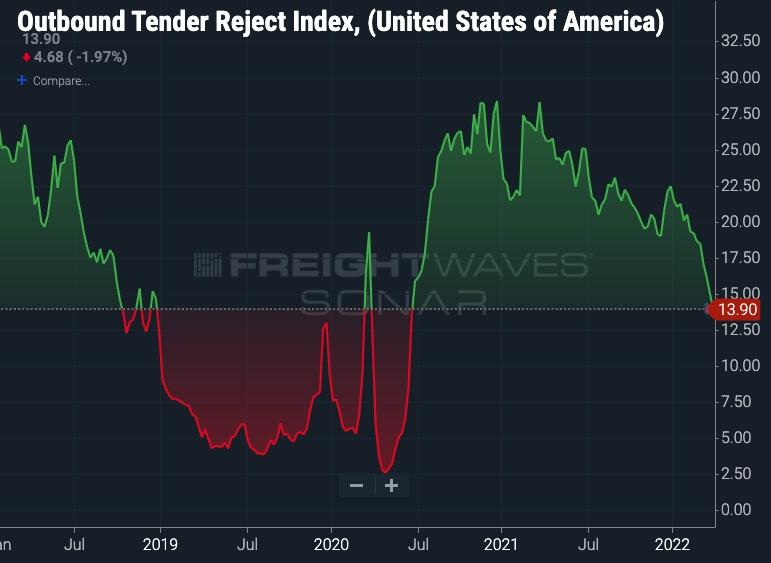

Another key to the puzzle of figuring out if used car prices have reached a climax is a new warning about a looming freight recession. FreightWaves’ CEO Craig Fuller explains that tender rejections, the best indicator of real-time supply/demand in the trucking sector, will soon go negative. The last time this happened was during the 2019 freight recession. This could mean that consumer spending, the most significant part of the economy, could be pulling back as consumer sentiment remains crushed by soaring inflation

Fuller’s freight recession call could also suggest a durable goods slowdown. Perhaps this would also mean consumers could go on a buyer strike as they’re battered by high inflation.

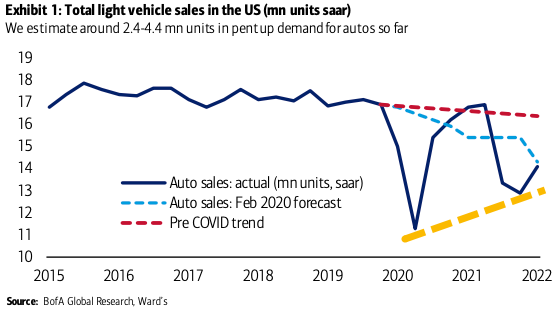

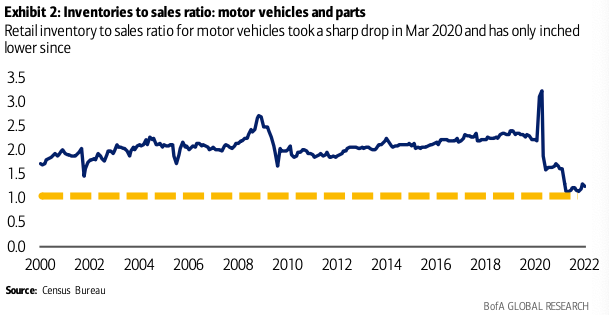

However, BofA’s US economist Anna Zhou points out there’s “pent-up demand for cars should provide another boost to consumer spending when the supply side constraints ease, though this might not happen until later this year.”

Zhou said the supply-demand imbalance has driven up prices of used cars while retail inventories to sales ratio is at multi-decade lows. She even said as dealers face low supplies of new cars, they are forced to continue bidding up used cars to keep inventories full.

We have pointed out several factors that could produce a top in used car prices, such as soaring interest rates, supply chain alleviation, impending freight recession, and also provide readers with a counterargument from BofA that suggests there’s still a lot of pent-up demand out there. The good news is that used car prices have faded from record highs and may mean overall inflation will peak soon.

Making a box of Cocoa Puffs is a complicated global affair. It could start with cocoa farms in Africa, corn fields in the U.S. or sugar plantations in Latin America. Then thousands of processors, transporters, packagers, distributors, office workers and retailers join the supply chain before a kid in Minnesota, where General Mills is based, pours the cereal into a bowl.

Now imagine the challenge that General Mills faces in counting the greenhouse gas emissions from all of these people, machines, vehicles, buildings and other products involved in this Cocoa Puff supply chain – then multiply that by the 100-plus brands belonging to the food giant.

Thousands of public companies may soon have such a daunting task to comply with a new set of climate rules proposed by the Securities and Exchange Commission.

Hailed by prominent environmental groups as a long sought victory, the sweeping plan released in late March would force companies to grapple with the unpredictable impact of climate change by disclosing reams of new information to investors. What are your company’s climate risks, such as severe weather, and the possible financial impacts? How have the threats affected your business strategies and what’s the plan to avoid the dangers? The most consequential and controversial piece of the SEC’s proposed regulations would require corporations to calculate their total greenhouse gas footprint, including from the supply chain.

The regulations also carry political weight for Democrats in the runup to the midterms in November. The Biden administration and centrist Sen. Joe Manchin of West Virginia are trying once again to breathe life into clean energy legislation that died earlier this year amid a feud between them. If this latest effort at compromise fails – with Manchin reportedly looking for federal support for fossil fuels as well as renewable energy – then much of President Biden’s ambitious climate agenda will be left riding on the SEC proposal.

SEC head Gary Gensler says shareholders are demanding climate risk disclosures to make smarter investment decisions and hold companies accountable for “greenwashing” their operations. The regulations will also provide investors in the Environmental, Social, Governance (ESG) movement more leverage in their ongoing campaigns to pressure companies to reduce their carbon footprints.

While many companies like Walmart and business groups like the Chamber of Commerce generally support the idea of required climate disclosures, they object to what they see as the SEC’s heavy-handedness in standardizing rules across the economy. The Chamber is calling for flexibility so companies can customize their climate disclosures based on what’s relevant to their businesses and investors.

The biggest beef from companies is the rule that would require them to calculate and disclose supply chain emissions, called Scope 3.

Big companies have thousands of suppliers operating in hundreds of countries, making the task of coming up with a reasonable accounting enormously complicated. First of all, many suppliers of products and services are private companies not under the control of the SEC. They may refuse to cooperate in a count because of the costs and the implications that they might have to change their business practices to reduce emissions, said Professor Gerald Patchell, who has analyzed the problems of supply chain reporting.

Another obstacle is that many smaller suppliers, like General Mills’ cocoa farmers in Africa, don’t have the capacity to measure the emissions from their own fertilizers, tractors and farming practices. So companies will have to rely on broad country or industry averages that likely don’t reflect the actual emissions created by the suppliers, according to researchers.

“The data that companies will be asked to collect from thousands of suppliers is mind-boggling and certainly unprecedented,” said Patchell, who researches environmental policy and business. “It’s an idealized concept of what can actually be done by a company.”

The upshot is that regulations meant to bring clarity to investors on climate risk may end up providing highly unreliable emissions disclosures, leaving them “worse off,” wrote SEC Commissioner Hester Peirce, a Trump appointee who voted against the 500-page proposal. It “forces investors to view companies through the eyes of a vocal set of stakeholders, for whom a company’s climate reputation is of equal or greater importance than a company’s financial performance.”

Two decades ago, the international environmental group CDP pioneered the strategy of organizing institutional investors to pressure companies around the world to reveal at least a piece of their carbon footprint. The CDP pitch: If companies figure out which parts of their sprawling global operations produce the most emissions – from farming and manufacturing to distribution and consumer use – they are better able to reduce them.

For automakers, most emissions come from driving vehicles, not making them. For tech firms, it’s the opposite. Manufacturing devices is a bigger climate issue than using them.

CDP’s campaigns have made grinding progress over the years. In 2021, it gathered more than 160 global investment firms, including bond giant Pimco, Harvard Management Company and hedge fund AQR Capital Management, to target 1,300 companies worldwide. They are asked to make a long list of climate-related disclosures on CDP’s platform.

Some companies have resisted the pressure while others likely have been shamed into making rudimentary examinations of their emissions to appease investors. In all, about 570 U.S. public companies – an estimated 15% of the total – have reported a bit of climate data to London-based CDP, with Intel and PepsiCo among the dozens that earned high marks for transparency.

More recently, some companies have come to see climate change as a direct threat to the bottom line, particularly those that depend on commodities like General Mills. It didn’t require much pushing from investors to begin studying its own supply chain to find that farming is by far its biggest emissions hot spot, mostly through the use of chemical fertilizers and tilling of the soil which releases sequestered carbon.

In a candid 2021 Global Responsibility Report, the company said extreme weather events were already hurting its ability to deliver quality food products.

With the backing of CDP and investment goliaths like BlackRock, the SEC now wants to turn this scattershot voluntary reporting into a mandatory regime for most public companies. The easier pieces force companies to report emissions from operations they own or control such as a corporate headquarters (Scope 1), and the energy they use (Scope 2). Some firms already send this data to CDP without much trouble.

The Scope 3 rule on counting emissions from the chain of thousands of suppliers, on the other hand, may be a world of trouble. The agency acknowledges that it doesn’t have a handle on the costs but that they may be “significant” as companies hire consultants, accountants and data specialists to do the job.

But since the vast majority of emissions come from supply chains, environmental groups are advocating that Scope 3 remain in the final SEC regulations after the 60-day public comment period. Big companies could start making disclosures to the agency as early as 2024, although lawsuits challenging the authority of the SEC to make climate rules are likely.

“We see the disclosure of Scope 3 emissions as essential in order to make sure that companies have plans to be able to address those emissions,” said Julie Nash, a senior program director at Ceres, another prominent investor advocacy group. “Disclosure is the essential first step.”

Ceres, however, also knows how tough it will be for companies to calculate supply chain emissions from its own campaign focusing on the food industry. The industry is the perfect target. It produces a third of all greenhouse gas emissions worldwide, according to a UN agency. For many of these companies, the supply chain generates about 80% of their total emissions.

Last year, Boston-based Ceres organized more than 30 institutional investors, including giants such as Allianz Global Investors, to press 50 food companies to report Scope 3 emissions. Ceres used the same reporting requirements – called the Greenhouse Gas Protocol – as the SEC proposes in its rules.

The protocol covers 15 reporting categories from the beginning of a product’s creation to the end of its life. McDonald’s, for instance, would have to account for emissions from the production of beef it buys from many countries. The disclosures would include processing and transporting the ingredients, packaging the products, disposing of waste and burning energy along the way. Then there are emissions from business offices, the commuting of 200,000 employees and the operations of 40,000 restaurants globally.

So how is Ceres’ young campaign going? So far, few if any of the 50 companies are fully reporting their supply chain emissions. Only 23 disclose some of them, according to Ceres.

Nash says the complexity of counting emissions and the lack of data pose big obstacles for food companies. Consider how a food company would have to account for beef supplied from Brazil.

The cattle may move to five different ranches before reaching the slaughterhouse. The company would need to know precise details of the operations of each of those ranches. What did the cattle eat at each ranch? How efficiently did the animals turn food into meat? Did their grazing cause the destruction of forests, which store carbon in trees and soil? Each of these factors, which differ depending on the ranch and the country, significantly affects the carbon footprint of cattle.

“It’s very difficult for companies to trace this information because there are so many different stages in the supply chain,” said Nash, a Ph.D. who directs Ceres’ food and forest program. “So there’s a great deal of work that’s needed to improve traceability and transparency to have the most accurate numbers for a Scope 3 analysis.”

General Mills stands out among the 50 companies. A spokesperson for the company, which makes breakfast cereals, soups, pizza, and pet food, says it follows almost all of the reporting protocols in its quest to reduce its emissions 30% by 2030.

The company’s Scope 3 calculations revealed that 54% of its emissions come from growing and transporting crops and turning them into food ingredients, according to its website. General Mills breaks out 28 categories of emissions, including packaging at 8%, and consuming its products, such as shopping and cooking, at 17%.

But how accurate are any of these emissions numbers?

It’s impossible to say. The maker of Cocoa Puffs doesn’t send bean counters to every cocoa farm in Ghana and Cote d’lvoire to find out the precise types of fertilizers, tractors, fuel and agricultural practices they use. That would be prohibitively expensive, given that the company has suppliers operating in more than 100 countries.

Instead, General Mills and other companies use Life Cycle Assessment (LCA) computer models to tally emissions. But these models, like those used in everything from economics to climate science, are only as accurate as the consultants who design them and the data that’s fed into them.

The data is the biggest problem. General Mills hired the consulting firm Quantis to calculate its supply chain emissions. Quantis uses national averages for particular businesses like cocoa farms in Ghana that may be several steps removed from the actual farms that supply General Mills, creating uncertainty about the accuracy of the estimates. Nor do computer models typically include some of the biggest sources of emissions, such as the release from tilling the soil and from converting forests and grasslands, which sequester carbon, to crops. Quantis didn’t respond to a request for an interview.

“We need a more accurate estimate of our baseline emissions,” Steven Rosenzweig, a soil scientist at General Mills, told the U.S. Department of Agriculture in February. “Using these databases means our current footprint is static, it doesn’t change from year to year. It also might be based on the global average that isn’t very relevant to the practices that farmers in our supply sheds are using.”

To make better Scope 3 estimates, Rosenzweig said, companies need to develop more sophisticated data tracking systems, which will require satellites to monitor changes to land use.

In the meantime, General Mills is taking the ambitious step of attempting to transform the agricultural practices of its farmers in the U.S. and abroad who supply key ingredients like wheat, oats, dairy and cocoa. The company and industry partners are financing efforts to support and train farmers in regenerative agriculture. It uses less fertilizer and tilling to reduce emissions and other methods to improve the health of soil, which is rapidly degrading worldwide.

General Mills has more than 115,000 acres enrolled in its regenerative management programs and aims for one million acres by 2030. “We consider regenerative agriculture to be our greatest opportunity for meeting our commitment to reduce our climate footprint by 30% by 2030,” Rosenzweig said.

Advocates of the SEC proposal say today’s reporting flaws will be improved as more companies develop Scope 3 expertise and collect better data to share with each other. The number of companies that disclose emissions to CDP continues to grow every year, showing it’s just a matter of time.

Professor Patchell disagrees, saying that forcing companies to make such elaborate disclosures is a waste of resources. Big firms already have a general understanding of the main sources of their emissions, such as agriculture in the food industry. The money needed to produce a precise accounting of emissions, he says, would be better spent on actually reducing them. McDonald’s, for instance, didn’t need a full accounting of its greenhouse gas footprint to pledge to reach net-zero by 2050.

Given the difficulties in determining supply chain emissions, the SEC has carved out a few exemptions. For instance small firms, such as those with less than $100 million in revenue, won’t have to comply. The companies also will be shielded from lawsuits for passing on faulty data provided they have a reasonable basis for disclosing it.

The SEC says it will help investors judge the reliability of the disclosures by requiring companies to reveal the sources of the data, including economic and government studies, suppliers, consultants and other third parties. Asking investors to wade through all those footnotes is a tall order, but it’s not unlike what they already do with other financial disclosures, said Michael Lepech, a Stanford professor of environmental engineering who has worked with LCA models.

“When you read a financial statement, businesses talk about significant uncertainties associated with the assets and liabilities,” he said. “It’s just buried in the extensive notes. And carbon accounting is in many regards no different than that.”

But the Chamber of Commerce, a business lobby, says the Scope 3 mandate may leave investors more confused than informed. The Chamber is pushing for an open-ended reporting mandate based on general principles to determine what’s relevant for investors rather than precise rules, such as the Scope 3 protocol. Companies and their investors should be left to determine the necessary metrics, which means some may choose to report Scope 3 and others won’t, said Evan Williams, director of the chamber’s center for capital markets.

Critics of this principles-based approach say it’s so vague that companies will find ways to avoid any meaningful accounting of their carbon footprint.

“There is that concern,” Williams said. “But what we have seen is that companies are responsive to their investors, and if they demand more information on climate risks, the companies have provided it.”

The Iranian metal band Confess’ third album, Revenge at All Costs, is so brutal that the Iranian government sentenced them to 74 lashes, which is probably—horrifyingly—a better advertisement for it than any promotional materials their record label could cook up.

In 2015, Iranian authorities arrested Confess singer and guitarist Nikan Khosravi and his bandmate Arash Ilkhani. The two metalheads were charged with blasphemy and anti-government propaganda for the band’s pointed anti-religious lyrics and criticisms of the state. Khosravi spent 18 months in Tehran’s infamous Evin prison while awaiting trial, three of them in solitary confinement.

After they were found guilty and sentenced to six years behind bars, Khosravi and Ilkhani were granted political asylum in Norway and fled their home country. They channeled the whole experience into their third album. In a genre where aggression is sometimes an affectation or escape fantasy, Confess’ anger is concrete, political, and personal. It’s not a put-on when Khosravi screams on “Phoenix Rises,” the album’s third track, “They can’t fucking break me for who I am.”

The Revolutionary Tribunal of Tehran gave “Phoenix Rises” a negative review when it was released as a single and raised Khosravi and Ilkhani’s combined sentences to 14 and a half years in prison and 74 lashes in absentia.

Stylistically, Confess lands somewhere in the realm of the new wave of American heavy metal, groove metal, and metalcore. Think athletic mid-tempo guitar riffs, breakdowns, and hardcore vocals. If you’re a fan of Lamb of God, Slayer, and Sepultura, you’ll find a lot more to like here than Iranian authoritarians did. Lamb of God and Clutch collaborator Gene “Machine” Freeman produced the album, giving it a polished touch.

Khosravi’s fury cuts through the mix and commands your attention from start to finish. You can hear why the mullahs were scared.

The Iranian metal band Confess’ third album, Revenge at All Costs, is so brutal that the Iranian government sentenced them to 74 lashes, which is probably—horrifyingly—a better advertisement for it than any promotional materials their record label could cook up.

In 2015, Iranian authorities arrested Confess singer and guitarist Nikan Khosravi and his bandmate Arash Ilkhani. The two metalheads were charged with blasphemy and anti-government propaganda for the band’s pointed anti-religious lyrics and criticisms of the state. Khosravi spent 18 months in Tehran’s infamous Evin prison while awaiting trial, three of them in solitary confinement.

After they were found guilty and sentenced to six years behind bars, Khosravi and Ilkhani were granted political asylum in Norway and fled their home country. They channeled the whole experience into their third album. In a genre where aggression is sometimes an affectation or escape fantasy, Confess’ anger is concrete, political, and personal. It’s not a put-on when Khosravi screams on “Phoenix Rises,” the album’s third track, “They can’t fucking break me for who I am.”

The Revolutionary Tribunal of Tehran gave “Phoenix Rises” a negative review when it was released as a single and raised Khosravi and Ilkhani’s combined sentences to 14 and a half years in prison and 74 lashes in absentia.

Stylistically, Confess lands somewhere in the realm of the new wave of American heavy metal, groove metal, and metalcore. Think athletic mid-tempo guitar riffs, breakdowns, and hardcore vocals. If you’re a fan of Lamb of God, Slayer, and Sepultura, you’ll find a lot more to like here than Iranian authoritarians did. Lamb of God and Clutch collaborator Gene “Machine” Freeman produced the album, giving it a polished touch.

Khosravi’s fury cuts through the mix and commands your attention from start to finish. You can hear why the mullahs were scared.

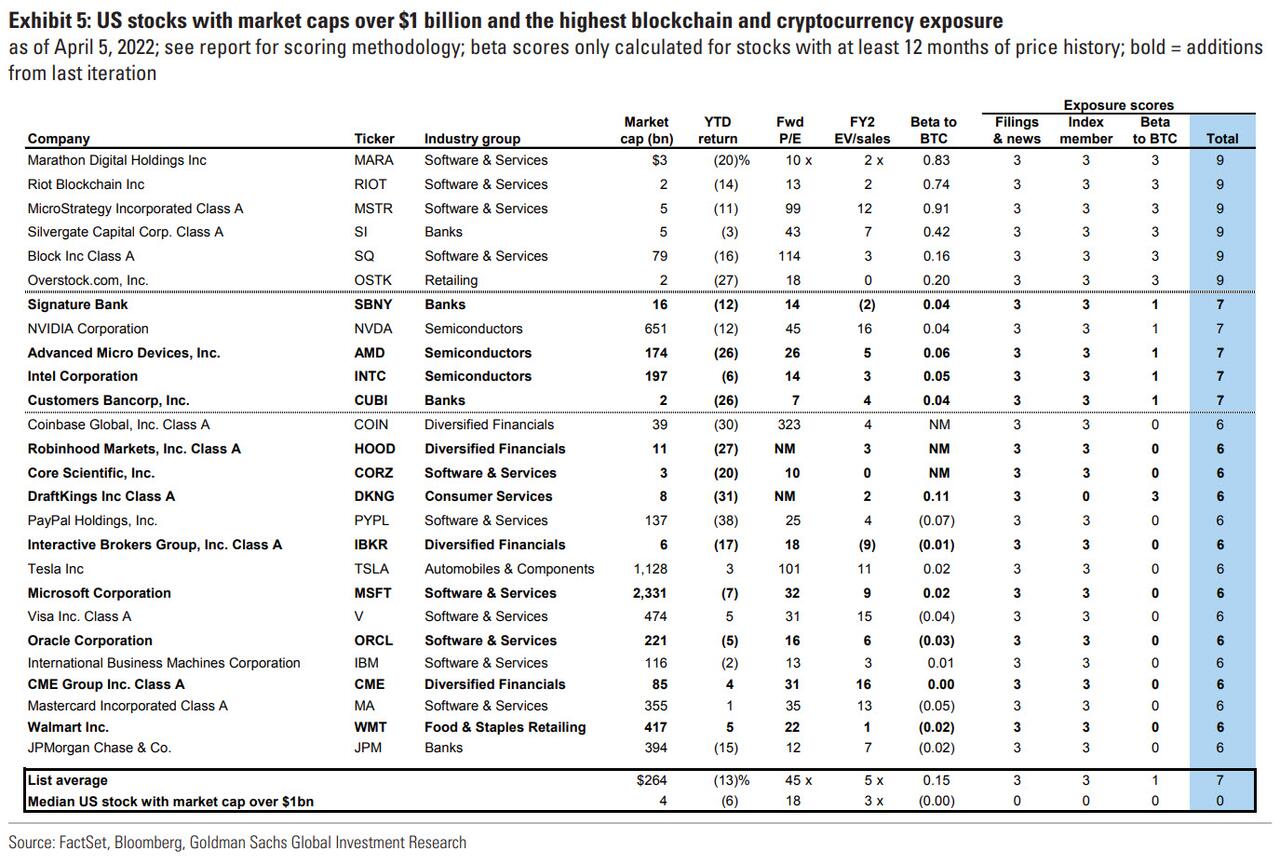

Goldman Updates Blockchain-Exposed Equities Basket As Bitcoin-Stocks Correlation Hits Record High

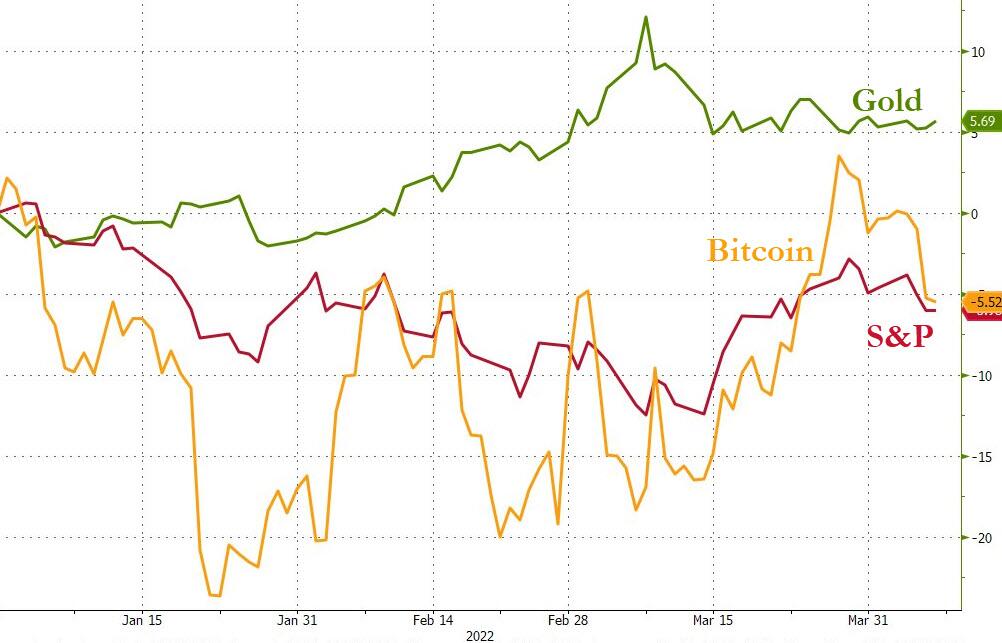

In a world of heightened risks, investors often lean into ‘stores of value’ as a way to insulate capital from elevated volatility. So far, in 2022, gold has once again proven to be a preferred ‘store of value’ with the commodity gaining 5.7% YTD (even as the S&P has lost 6% of its value).

However, as Goldman’s Chris Hussey notes, as we leg further into the digital age, it is tempting to think that the world may increasingly gravitate towards digital stores of value like Bitcoin, in place of gold (a metal that has been used to shield against volatility for thousands of years now). But Bitcoin has done little to shield investors from the volatility, equally as weak as stocks year-to-date, suggesting that the cryptocurrency is still being used as a proxy for risk rather than a shield.

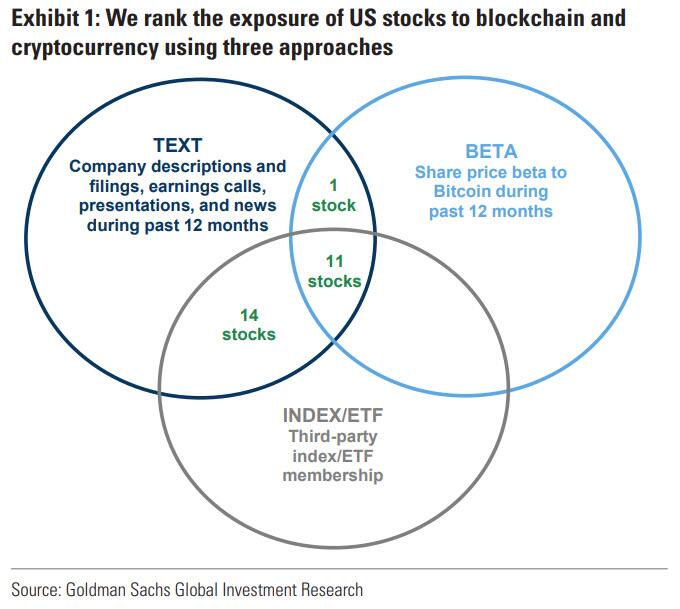

Against this backdrop, Goldman’s David Kostin and team have refreshed their blockchain stock basket.

Goldman combines three approaches to screen for US stocks with blockchain and cryptocurrency exposure.

Their approach results in a screen of 26 US stocks with market caps over $1 billion and high exposure to blockchain technology and/or cryptocurrency.

On average, these stocks have underperformed the S&P 500 by 8 percentage points YTD (-13% vs. -5%)

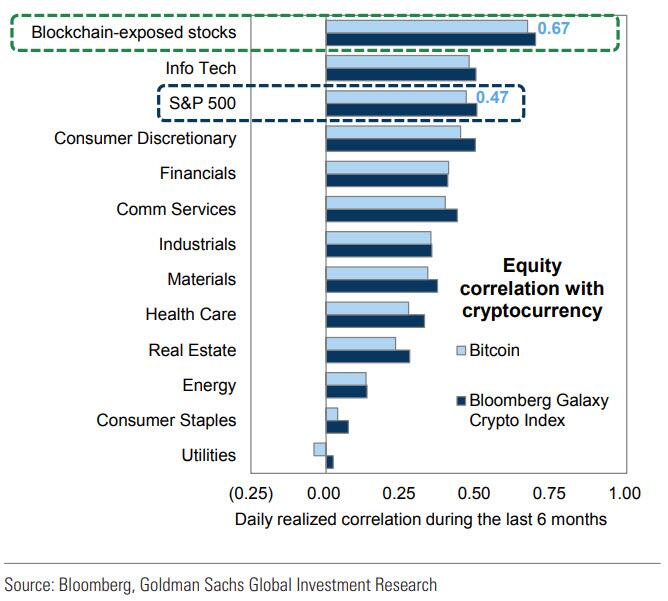

While the stocks on this list are correlated with Bitcoin…

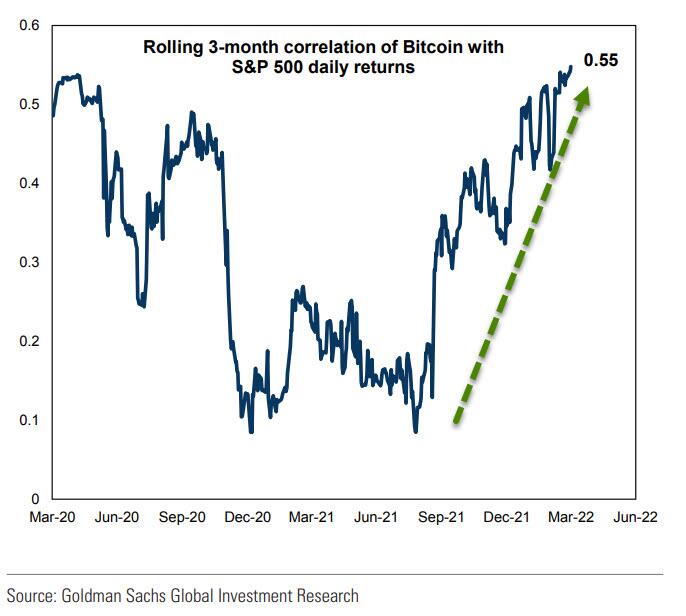

…Bitcoin itself has become increasingly more correlated with equity index returns in recent months…

What will break that correlation? When The Fed flip-flops back to QE?