In California, the first reparations panel in the nation has spent two years trying to decide which African-Americans are eligible for reparations.

According to the Associated Press, the state’s panel on reparations, which was first created following a law signed by Governor Gavin Newsom (D-Calif.) in 2020, has been plagued with internal divisions over how many black Americans should receive financial compensation for alleged “racism.”

Since it was first formed in June, some of the panel’s nine members have argued that only direct descendants of actual slaves prior to the Civil War should receive handouts, while others call for a more liberal distribution of funds to every black American. The warring factions led to the panel delaying its originally-planned vote last month.

Despite having existed for two years, the panel has no concrete plan yet for what their reparations would look like. Supporters say that compensation would account for various historical instances of discrimination such as slavery, segregation, and alleged racism in incarceration rates. Some of the proposals for compensation include free college, grants to churches and community organizations, and financial handouts in buying homes and starting up businesses.

Kamilah Moore, the committee’s chairwoman, has voiced her support for only giving reparations to direct descendants of slaves, having pointed out that broader reparations based simply on race are far more likely to be struck down in court.

If the plan focused solely on race, then it would surely face “hyper-aggressive challenges that could have very negative implications for other states looking to do something similar, or even for the federal government,” Moore explained. “Everyone’s looking to what we’re going to do.”

But another committee member, Lisa Holder, argues that lineage does not matter in modern America, and that all black Americans are discriminated against.

“No one asked me if my ancestors were enslaved in the United States or if they were enslaved in Jamaica or if they were enslaved in Barbados,” said Holder.

“We have to embrace this concept that black lives matter, not just a sliver of those Black lives, because black lives are in danger, especially today.”

A full report by the committee is due by June of this year, and a detailed reparations proposal is due by July of next year, at which point the state legislature will consider a vote to pass it into law.

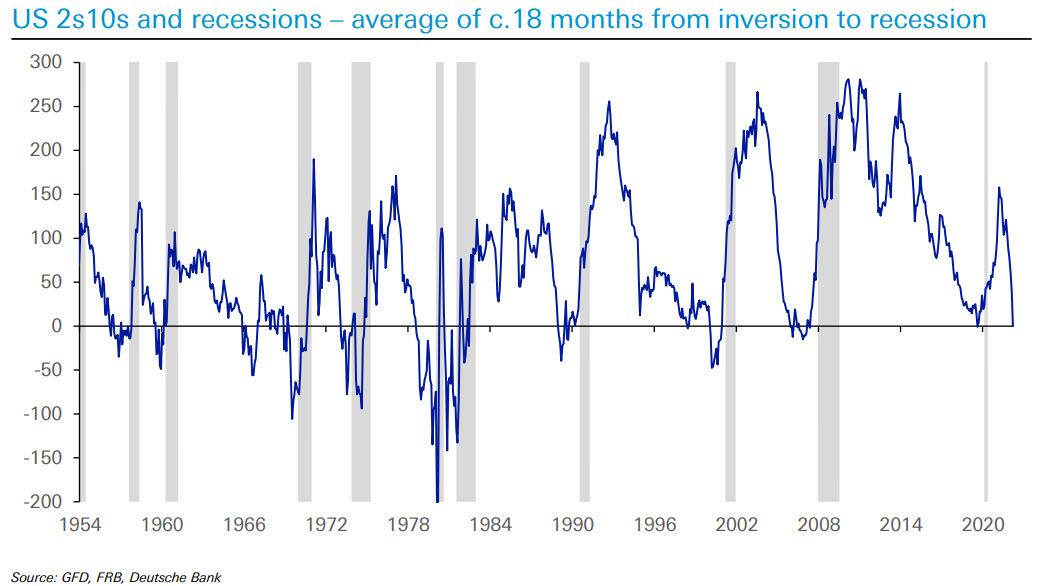

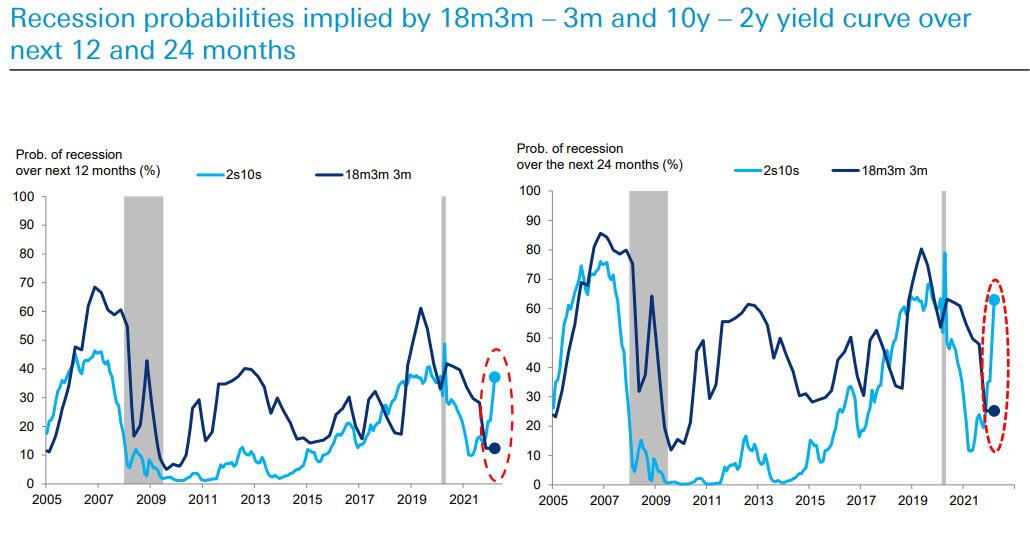

Shortly before the close on Thursday, the closely-watched 2s10s yield curve, better known as the recession harbinger, inverted again for the second time in three days, and this time it will likely fail to bounce as the US slides ever closer to its recession D-Day.

To be sure, the Fed and most of permabullish sellside strategists have spent most of their time in recent days to “explain away” why the yield curve doesn’t actually matter, with the Fed going so far as penning an absolutely idiotic paper titled “(Don’t Fear) The Yield Curve, Reprise“, in which the authors who have never had a real job in their lives reference FDR in making the point that the 2s10s is only notable in that “it can only make things worse if investors not only fear the prospect of a recession, but at the same time, are spooked by that fear itself, which is mirrored in inverted term spreads.” Instead of addressing a level of stupidity that once upon a time was prohibited at the Fed, we will merely show a chart comparing the 2s10s and superimpose the Consumer Optimism Gap (as defined by the spread between the Conference Board Expectations and Current situation), to show the clear correlation and that a plunge in the 2s10s coincides with a collapse in optimism… and the start of a recession.

Not convinced? That’s ok, because thanks to DB’s Jim Reid we have a full presentation (available to professional subs) which shows exactly what happens after every single inversion. Below we excerpt some of the key findings:

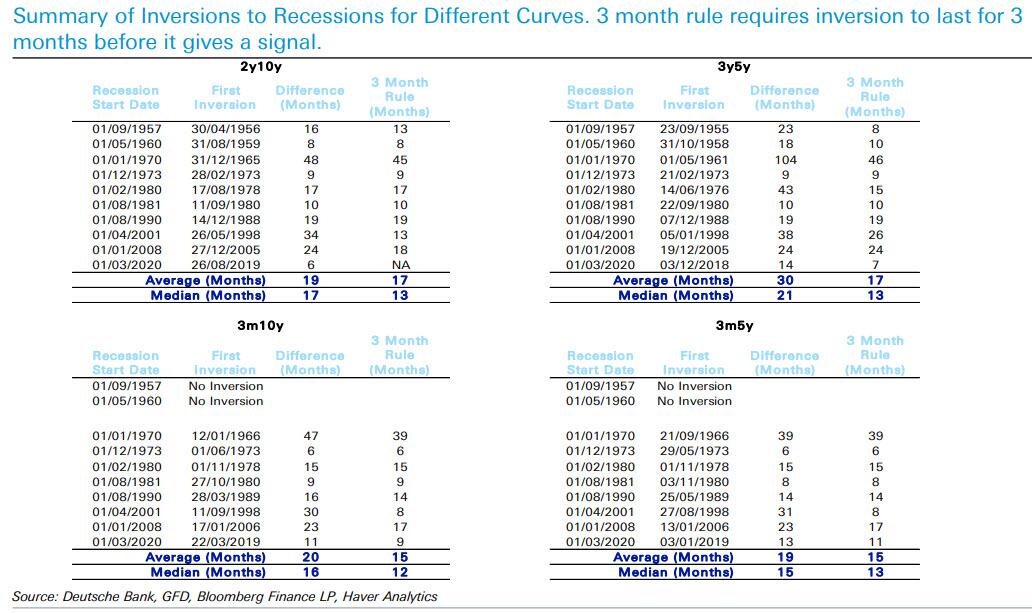

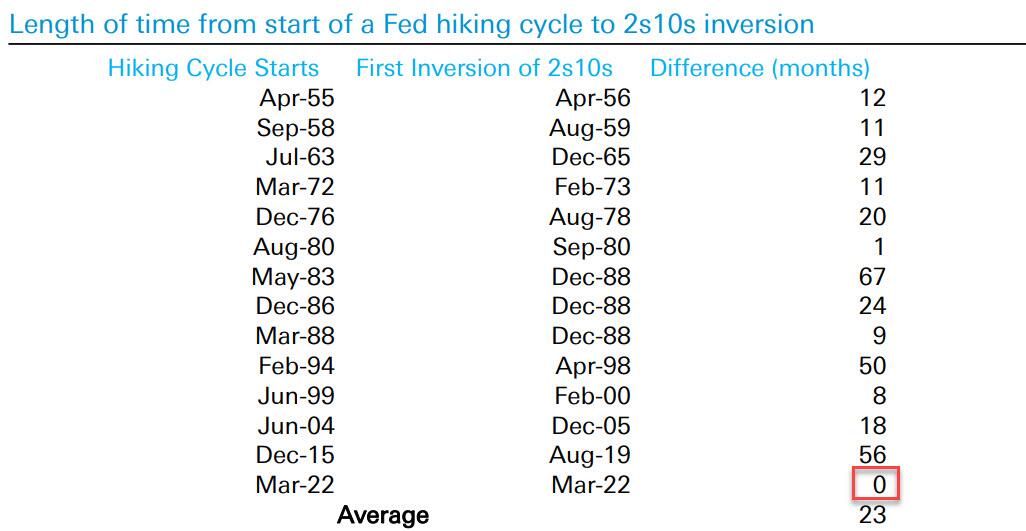

1. Every recession in the last 70 years has only happened AFTER the 2s10s has inverted. We have now seen an inversion on March 29th intra-day and again on March 31. History would say US recession risks now elevated 12-24 months out.

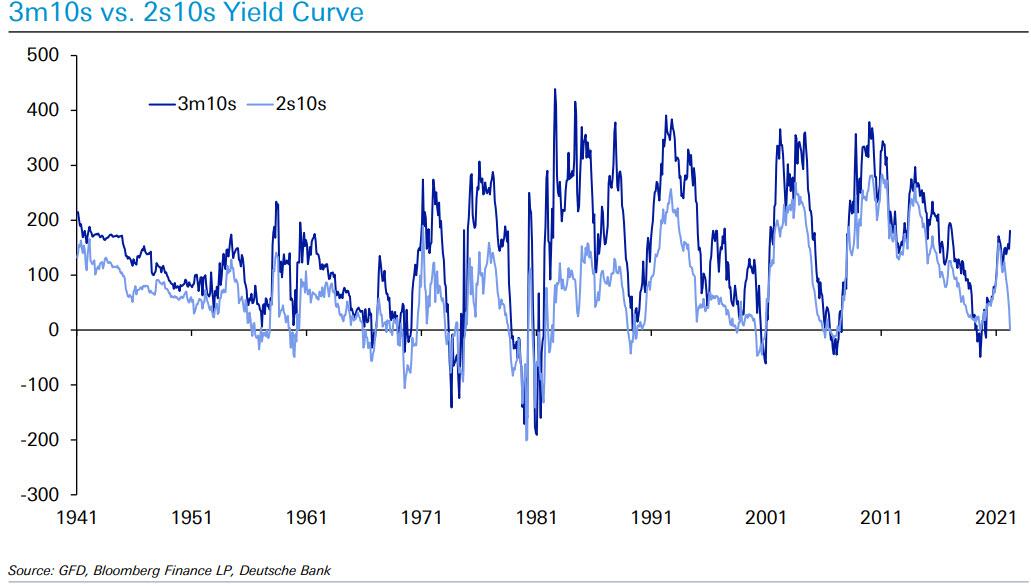

2. Bulls will point out that while all yield curves between 2Y and 10Y have inverted, anything involving 3M money is still historically steep, and that there is a record directional divergence between any yield curve measure including 3m money and those not. This argument is disingenuous as it only reflects that the Fed is so far behind the curve and anchoring the 3M. This, naturally, won’t last as Fed hikes aggressive over next 12 months…

3. While the steep 3M curve will invert soon enough once the Fed hikes a handful of times, which also means it only has “noise” value, it also means that it’s only the 2s10s matters as it’s inverted before EVERY recession going back 70 years (3 month money ones didn’t invert pre-50s/60s recessions). Also, it goes without saying, an inversion for 3 months is a stronger signal than a brief inversion.

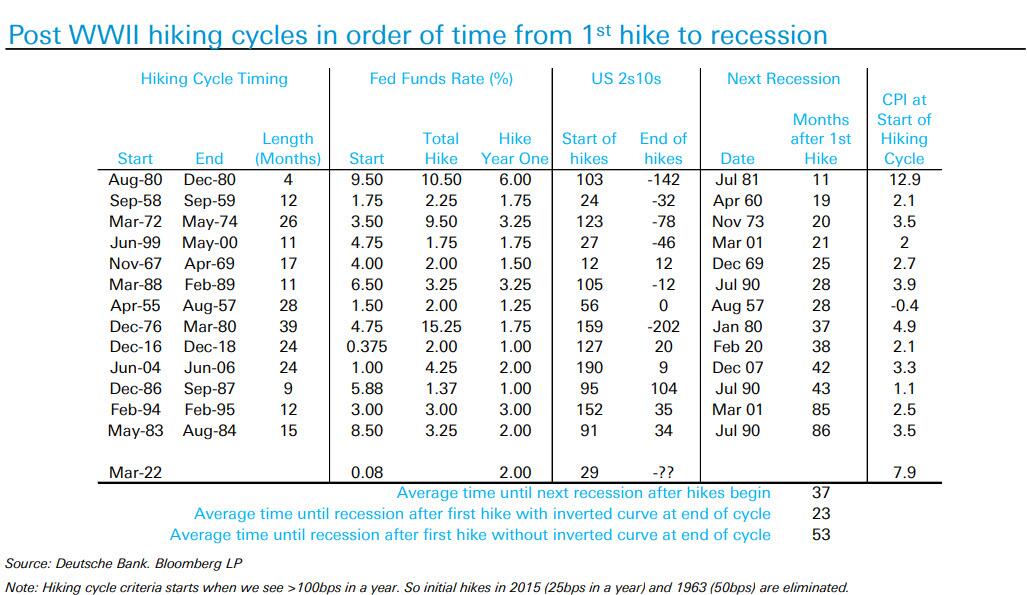

4. Furthermore, while bulls will argue that a 2s10s inversion means there is still a long time before the recession (roughly 18 months), the reality is that recessions after 1st Fed hike in a cycle occur sooner when 2s10s inversion happens during hiking cycle… Well, this inversion occurred in record time post the start of the hiking cycle.

5. Another remarkable datapoint: on average it takes around 2 years after the Fed starts hiking for the 2s10s to invert…. This time around it took just 2 weeks.

* * *

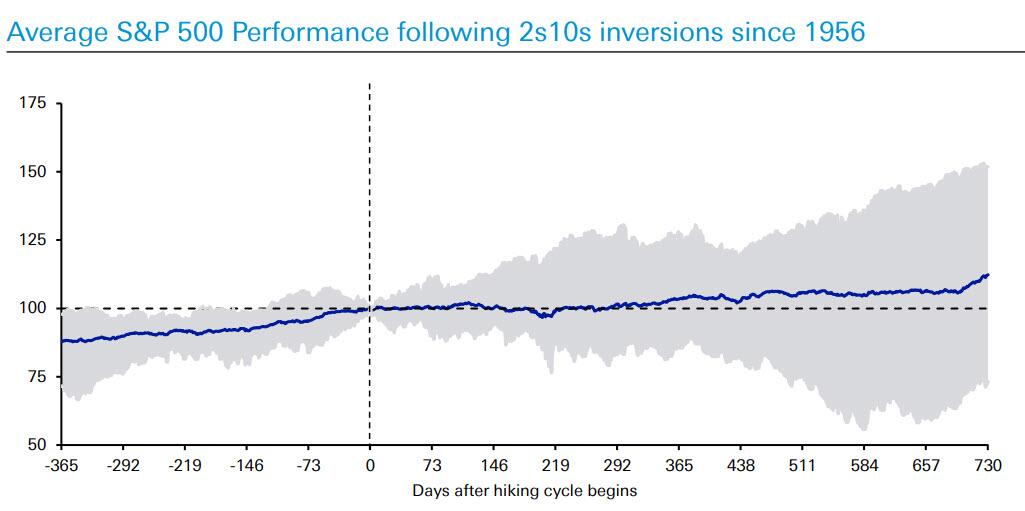

Now let’s take a look at how some assets perform after inversions.

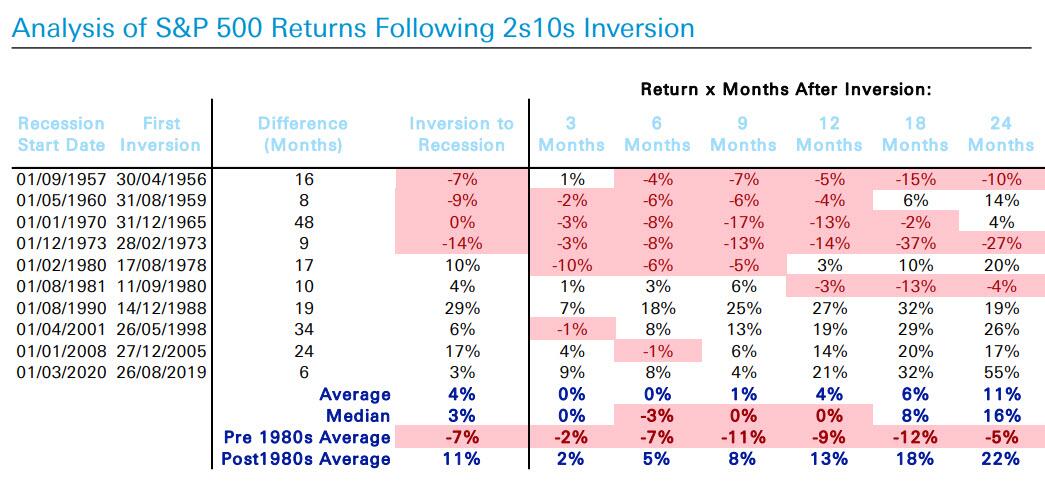

For S&P the supercycle matters: pre-1980 inversions almost always led to a sell-off. Post 1980, inversion and recessions have been relatively inconsequential hiccups in structural 40-year bull market.

… so as Jim Reid notes, the average performance following inversions is misleading as it’s a period of two dramatically different halves.

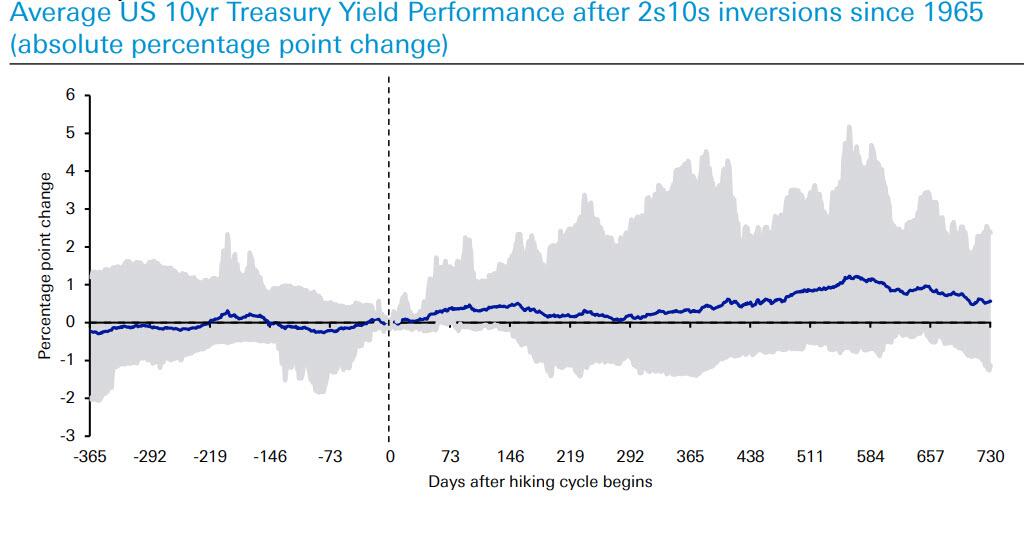

Yields still tend to go up for in the months after inversion starts with only one example of mildly lower yields around the 4 month point…

In any case, the 2s10s indicates that odds of a recession in the next 24 months are a solid 60%+ and rising by the day.

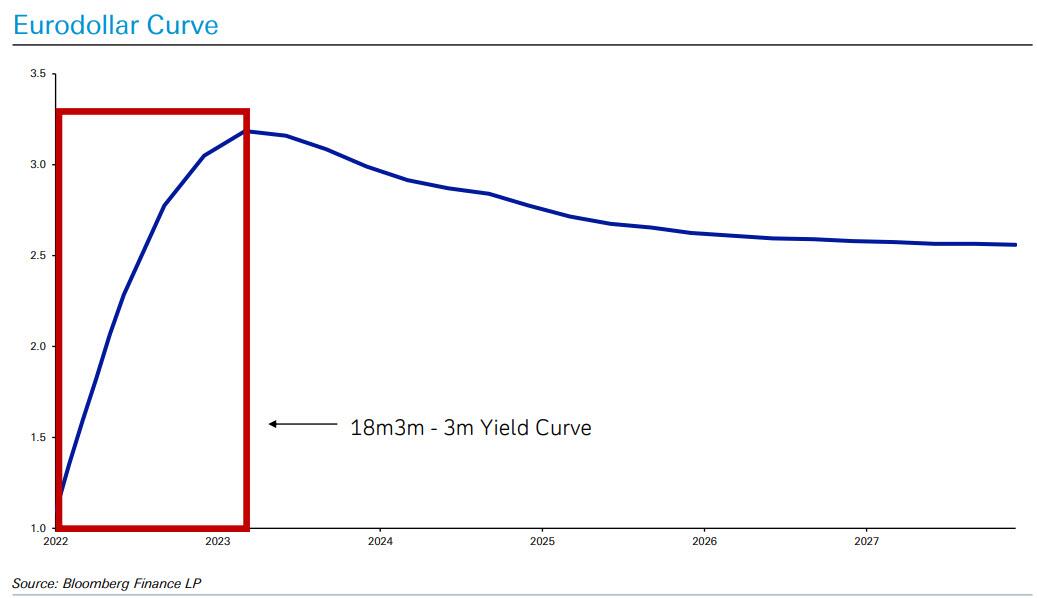

Meanwhile, in a humorous counter to the 3M polyannas, the reason why the 3M 3M18M is still steep is that with the Fed behind the curve,18m3m-3m is the steepest point on the yield curve, with cuts priced shortly after. Yes: in just over a year, the US will be in recession! The market likely will stop pricing additional hikes if they believe a recession is imminent. As Reit notes, “18m3m-3m should flatten soon as hikes are delivered, upgrading its implied recession signal over time.”

* * *

Two other observations why the inverted yield curve is a guaranteed signal of imminent recession: just before the 2008, Bernanke said this time was different, and to ignore the flat yield curve…

“I would not interpret the currently very flat yield curve as indicating a significant economic slowdown to come, for several reasons. First, in previous episodes when an inverted yield curve was followed by recession, the level of interest rates was quite high, consistent with considerable financial restraint. This time, both short- and long-term interest rates–in nominal and real terms–are relatively low by historical standards. Second, as I have already discussed, to the extent that the flattening or inversion of the yield curve is the result of a smaller term premium, the implications for future economic activity are positive rather than negative. Finally, the yield curve is only one of the financial indicators that researchers have found useful in predicting swings in economic activity. Other indicators that have had empirical success in the past, including corporate risk spreads, would seem to be consistent with continuing solid economic growth. In that regard, the fact that actual and implied volatilities of most financial prices remain subdued suggests that market participants do not harbor significant reservations about the economic outlook.”

… and also right before the bursting of the dot com bubble, William McDonough said the same in Feb 2000.

“Typically, the inverted yield curve is seen as a sign of a coming recession, McDonough said. ”I don’t see that as the explanation,” he said. He said an expected drop in supply of long-term debt, as a result of reduced U.S. government debt sales and announced buybacks, is more likely the reason. Without those conditions, the inverted yield curve probably wouldn’t exist, he said.”

Just a few days later, the dot com bubble burst.

There is much more in the full DB presentation available to pro subs.

Today, there was a hearing in the U.S. District Court for the District of Columbia in the matter of the United States v. Michael Sussmann, the former DNC/Clinton/Perkins Coie lawyer accused of providing false statements relating to the Alfa Bank/Trump Organization hoax to then-FBI general counsel James Baker in the fall of 2016. Here is more background on his indictment and how Sussmann and his allies passed Trump transition data to the CIA.

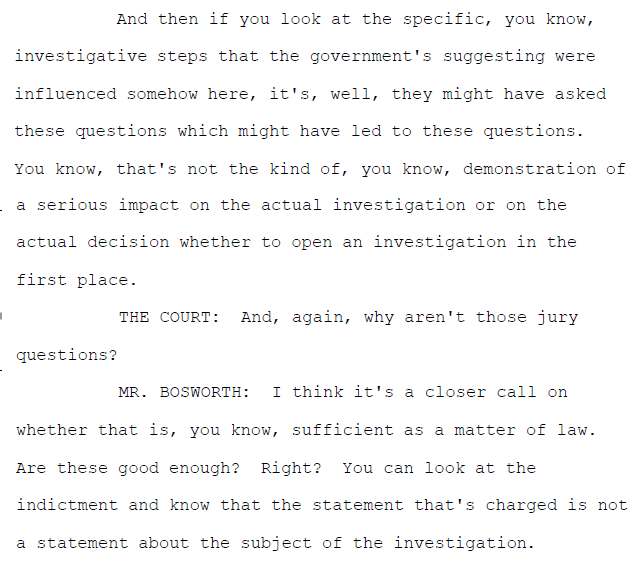

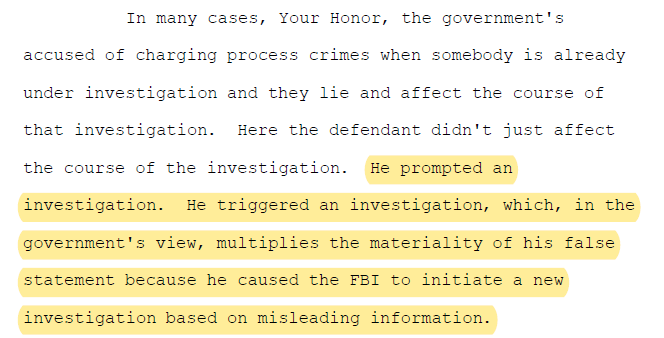

About the hearing – we have the transcript (link at the bottom). The hearing related to Sussmann’s efforts to dismiss the indictment, with the defense alleging that Sussmann’s alleged lies were not material.

The Court looked on that argument with skepticism. And rightly so, as the issue of materiality is typically a question for the jury. Sussmann’s lawyers did him no favors by admitting it was a “closer call” on whether the government’s arguments of materiality should be presented to the jury.

The Special Counsel’s argument on materiality was more more effective, explaining what Sussmann did and why his lies mattered:

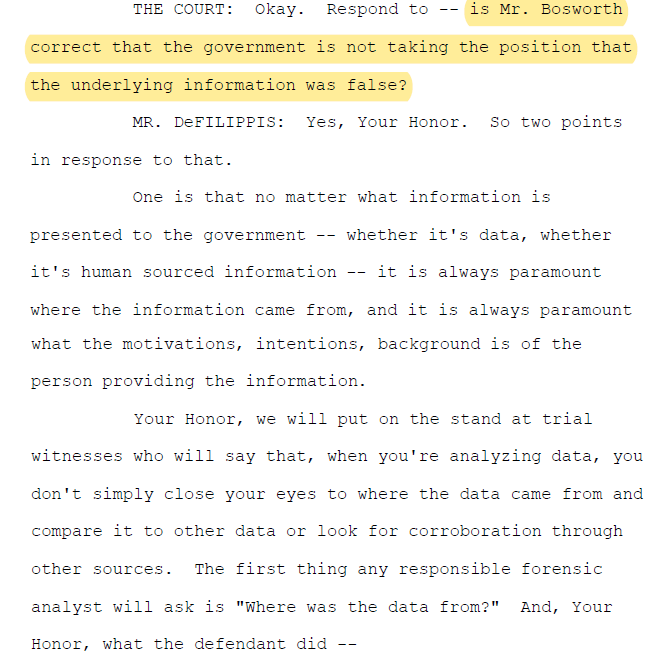

Interestingly, the Court also asked if the underlying information – the Alfa Bank/Trump Organization data that Sussmann provided the FBI – was “false”. On that question the Special Counsel declined to show their hand.

Why does this matter? Because it has been long-suspected that the the Alfa/Trump data was manipulated, if not outright invented. Recall this discussion in the Sussmann indictment, where the researchers discussed the inability “to defend against the criticism that this is not spoofed traffic”:

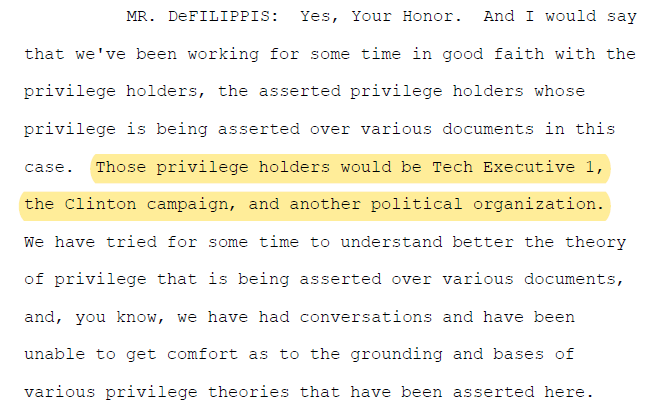

Now we get to the juicy parts of the hearing. The Special Counsel is in possession of a number of documents from the Clinton Campaign, Rodney Joffe (more about him here), and Hillary for America. And there is a fight over whether some of those documents are privileged.

The Special Counsel provided one example, stating that the Clinton Campaign is putting out bogus claims of privilege over the communications of Rodney Joffe. These are likely to fail. The Clinton Campaign was not copied on the e-mails, there might very well be a crime-fraud exception to any assertion of privilege, and because Joffe wasn’t providing legal advice to Hillary.

Fusion GPS is making similar claims of privilege to keep their documents secret.

They’ve tried these types of abuses of “privilege” in a civil case, and we previously discussed why those efforts were bound to fail, perhaps most notably because Fusion GPS has admitted they were doing political work not subject to privilege. Fusion GPS cannot now claim they were performing legal or litigation-focused work.

Moreover, even if this were legal work, Fusion GPS waived privilege when leaking their research to the media, government officials, and other third parties. Oops.

“They’re In Desperate Need Of Capital” – SoftBank Halts Investments As It Scrambles To Raise Cash

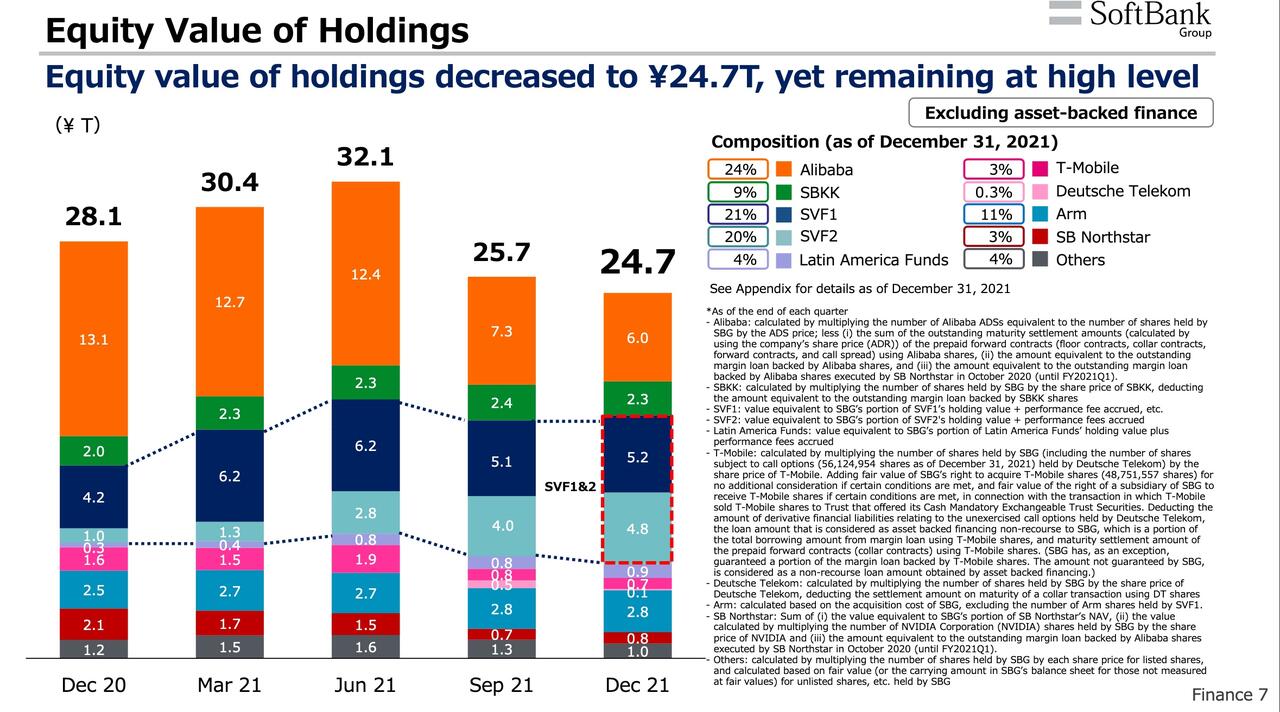

2021 was a difficult year for Softbank, and so far, 2022 is shaping up to be even more punishing. The Japanese telecoms giant/VC firm/conductor of the “AI Revolution” booked massive losses on its investment portfolio as massive bets on Didi and Grab soured (among other holdings), saddling the firm with tens of billions of dollars in losses for 2021 (this according to the firm’s most recent earnings report). And as shares of Alibaba and other prominent SoftBank holdings continued to tumble during Q1, dragging SoftBank shares lower in tandem, the situation has only continued to deteriorate.

The firm’s investment losses – spurred by a crackdown in Beijing (which has sheered $9 billion off the firm’s Didi holdings, and that’s just one stock), the war in Ukraine, and other factors outside SoftBank’s control – could represent an existential threat, since SoftBank borrows heavily against its own shares to finance investments in early-stage companies. Because of this heavily leveraged structure, if the company’s financial position deteriorates too aggressively, it could trigger a brutal margin call “doom loop” that could force it to sell even more of its holdings. Masa Son lost his first fortune during the dot-com blowup. The last thing he wants is to be financially ruined a second time.

To try and guard against this eventuality, Masa Son has reportedly ordered his lieutenants to halt investments in new firms as the company seeks to conserve cash as the value of its portfolio continues to deteriorate.

SoftBank founder Masayoshi Son has told his top executives to slow down investments, as the world’s largest tech investor seeks to raise cash amid falling tech stocks and a regulatory crackdown in China.

The Japanese billionaire made the remarks to his leadership team at a recent meeting, according to people briefed on the discussions, as the group responds to the massive hit to the value of its holdings in recent months. The previously unreported discussions offer a rare glimpse into the growing tension within SoftBank, which has disrupted the tech investing landscape since launching its first Vision Fund in 2017.

Instead of looking for new innovative tech companies to pump money into (or soliciting backers for a third iteration of its ‘Vision Fund’), SoftBank is evaluating its portfolio to decide which holdings might be best suited for liquidation. One insider said the firm doesn’t expect valuations of its Chinese holdings to rebound any time soon.

“Valuations for Chinese companies listed overseas have collapsed,” said one person close to SoftBank’s China team. “We don’t expect a turnround anytime soon.” One person familiar with the company’s plans added that SoftBank is pushing to raise cash and is evaluating assets that could be liquidated.

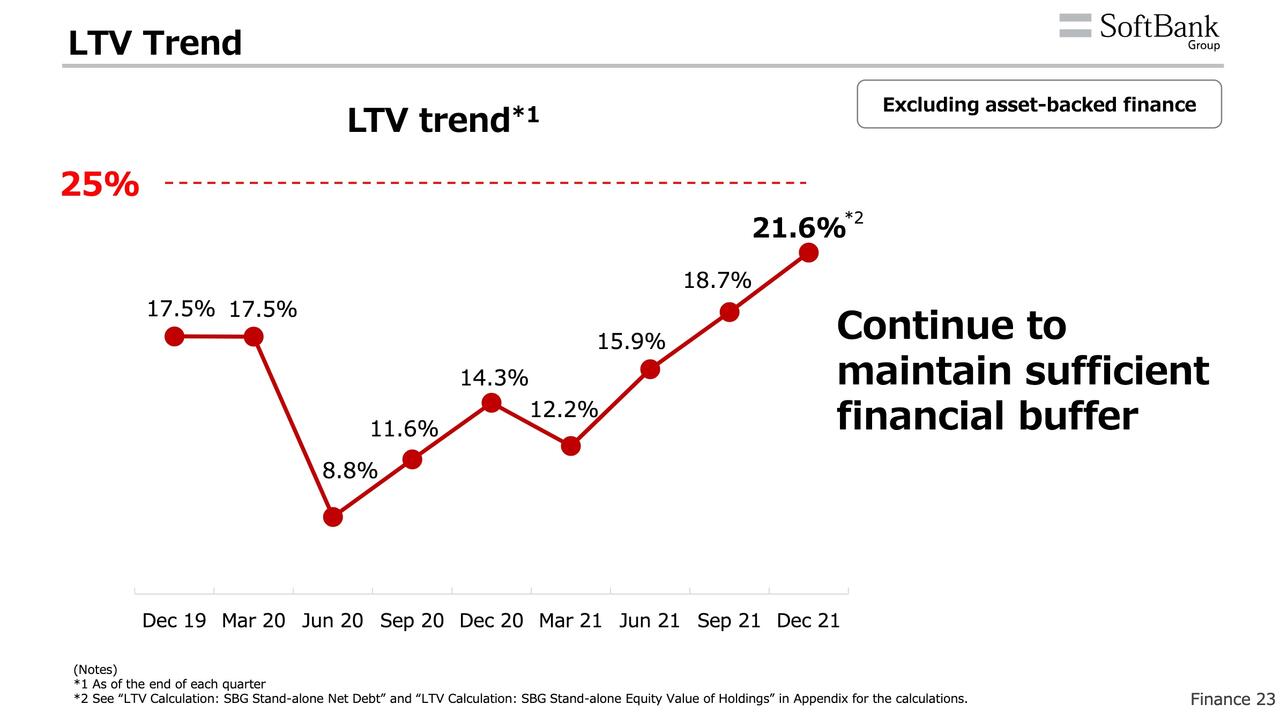

As the firm pointed out in its latest quarterly report, its loan-to-value ratio (a key metric in the eyes of financial analysts) is getting dangerously close to the red line separating a sustainable from an unsustainable debt burden.

The company’s shares have shed 40% of their value over the past year, and during Q1, its portfolio shed another $20 billion and $30 billion.

Back in October 2019, we speculated that SoftBank might be the tech bubble era’s “short of the century”. Aside from a few short-lived rallies, our timing on that call could not have been better.

SoftBank’s present difficulties follow one of the busiest years for dealmaking in the firm’s history: it closed investments in 195 private companies last year, the most in recent memory.

Now, in a bid to raise cash, SB is scrambling to borrow against its stake in British chipmaker Arm Holdings (which is headed or an IPO spinoff following the collapse of a deal to sell it to Nvidia) and other holdings. Still, to many on Wall Street, this strategy reeks of desperation.

In a bid to raise cash, SoftBank has also used stock in Coupang and other large holdings in the Vision Fund as collateral for loans. The Japanese tech group is also finalising loans worth as much as $10bn tied to the IPO of UK chip designer Arm Holdings, following the collapse of its $66bn sale to US rival Nvidia last month. “If you look at all the action, it’s very clear that they are in desperate need of capital,” said Amir Anvarzadeh, a strategist for Japan equity at Asymmetric Advisors who has recommended shorting SoftBank.

The firm’s long-term solution focuses on its Vision Fund. Executives at SoftBank’s second Vision Fund, which manages $40 billion of SoftBank’s own money, say they’re hoping to make fewer investments of a higher quality. The big question now, as Alibaba shares continue to struggle in the face of a crackdown by Beijing: how much longer can SoftBank hold out without being forced to sell more shares of its ‘golden goose’?

One of the highest priorities of the Biden administration’s trade agenda is resetting the U.S.-China trade relationship with a view to putting American farmers and exporters on a level playing field with their Chinese counterparts, U.S. Trade Representative Katherine Tai said on March 30.

In a prepared statement before a House Ways & Means Committee hearing, Tai criticized the prominent role of state-owned enterprises in China’s imports and exports as well as “labor rights suppression, a weak environmental regime, [and] other distortions that put market-oriented participants out of business.”

She also noted Beijing’s failure to meet purchase commitments under the “phase one” trade agreement signed in January 2020. Those purchase agreements stipulated that China would import at least $200 million more of U.S. goods and products in 2020-2021 than the country bought in 2017.

“We absolutely need to enforce all our agreements, phase one included, and that’s why we’ve spent the last several months fighting for our farmers who have a lot at stake in the purchase agreements,” Tai said during the hearing.

U.S. concerns about Beijing’s abusive trade practices led Tai and her team in October 2021 to initiate a dialogue with the Chinese regime, emphasizing the importance of meeting phase one obligations, she said in the statement.

But it became clear to Washington that Beijing did not consider the agreement to be binding and met only those commitments that the regime felt served its own interests, the statement said. Tai called this cherry-picking when it comes to meeting obligations a “familiar pattern” that U.S. officials encounter when dealing with Chinese regime officials, whether in the context of the World Trade Organization or bilateral talks.

While these experiences have not completely turned Washington off to the possibility of dialogue with Beijing, she said, it is clear that the old approach by itself is insufficient.

To that end, Tai urged Congress to pass the America COMPETES Act, a bill aimed at expanding semiconductor manufacturing in the United States and curbing reliance on Chinese products and know-how.

The trade official also emphasized that the Biden administration has forcefully demonstrated to the Chinese regime the resolve of the United States to enforce the Uyghur Forced Labor Prevention Act, which banned the importation of all products from China’s Xinjiang over Uyghur forced labor concerns.

“The challenge that we face from China is significant and it goes to how we as the U.S. continue to be able to compete and have thriving industries,” Tai told the lawmakers.

March Payrolls Preview: Can Wage Growth Slow Enough To Dent The Fed’s 50bps Rate Hike

With the Fed’s rates “lift off” already a done deal, traders will frame Friday’s March jobs data (which comes just hours after the month of March is in the actual history books) in the context of monetary policy, where money markets are assigning a 76% probability that the Federal Reserve will lift interest rates by a 50bps increment in May. Accordingly, as Newsquawk writes in its NFP preview, there will be much attention on the average hourly wages measures in the jobs report for signs about how the recent surge in inflation is affecting Americans’ real incomes, and for any evidence of the so-called second-round effects of inflation. The consensus looks for wages to rise in the month, lifting the annual measure, but some desks argue that the pressure is easing in the labor market, which should see wage growth ease in the months ahead. Meanwhile, proxies in the month continue to suggest a healthy labor market (initial jobless claims fell in the payrolls survey week, while business surveys suggest firms are ramping up hiring). While the data will likely cause the typical stock price volatility over the release, analysts have said that it would take a significant miss, accompanied by weakness in other economic data, for the Fed to waiver from its seeming intent to raise rates by 50bps in May.

Wall Street Expectations:

Consensus is for 490k nonfarm payrolls to be added to the US economy in March, with the rate of job creation easing to below recent trend rates (12-month average 556k, 6-month average 583k, 3-month average 582k).

Jobless rate is expected to fall by 0.1ppts to 3.7% (the Fed sees the jobless rate ending this year at 3.5%).

Wage metrics will attract a lot of attention amid the recent surge in inflation and inflation expectations; policymakers have been attentive to the possibility of both a wage-price spiral and second round effects; average earnings are expected to rise 0.4% M/M (vs unchanged in February), pushing the annual measure up to 5.5% Y/Y (from 5.2% in February).

POLICY DEBATE: Fed Chair Powell recently said that the central bank would move to a more restrictive policy if that was needed to restore price stability (translation: the Fed can and will create a recession to contain inflation, something markets refuse to believe) . UBS said that Powell was referring to a deliberate policy of pushing growth below trend; “it is important to note that this policy option was presented in a conditional way–if that is what is required– deliberately pushing policy to generate growth below trend would only be required if there were evidence of a wage-cost spiral developing, and there is not really evidence of that at the moment.” Other analysts point out that average hourly earnings have outperformed other indicators, and accordingly, some relative underperformance could be seen ahead. Either way, the consensus remains that the Fed will raise interest rates by a 50bps increment in May (money markets assign a probability of around 76% of that happening), and it would therefore take a dreadful labor market report combined with other weak data metrics for the Fed to back away from that course.

WAGES: Anecdotally, the compensation software provider Payscale, citing its data, said US firms were planning to give the highest pay increases in years, but these would still not match inflation. But Capital Economics says that the easing in job postings on Indeed.com suggests that there has been a softening in labor demand. While it notes that the relationship isn’t perfect, it would be consistent with employment growth easing too, and would match the slowdown in GDP. “The apparent drop-back in job openings also implies that there is now less excess demand for workers, consistent with broader evidence that labour shortages are starting to ease,” and it argues that the “unemployment rate, which is still above its pre-pandemic low, hasn’t proved a useful gauge of labour market slack over the past year”; while it expects this rate will fall in March other indicators suggest that conditions are no longer tightening. “After rising to their highest levels on record last year, the share of small firms struggling to fill job vacancies and the net share of consumers saying jobs are easy to find have both edged lower in recent months,” and “that suggests that the upward pressure on wages will also ease.” The consultancy sees the rate easing back to 5.0% Y/Y in the months ahead.

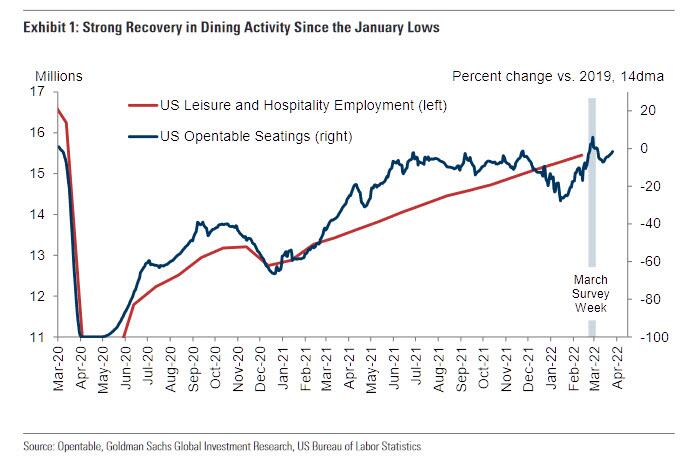

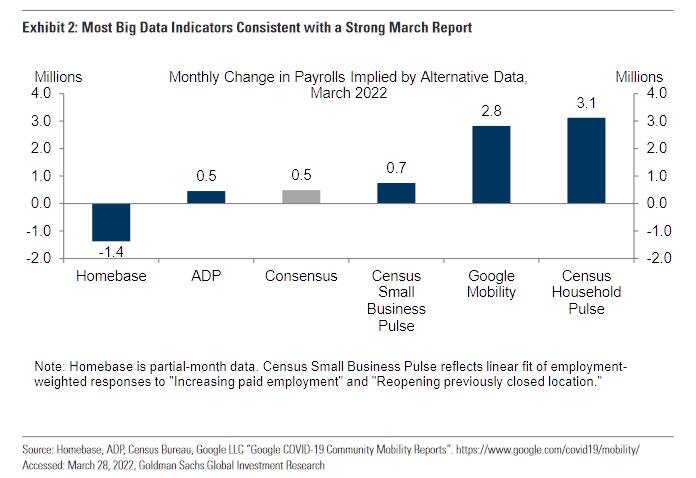

JOB ADDITIONS: Weekly initial jobless claims and continuing claims that coincide with the BLS’ employment report survey period both declined (initial claims eased to 215k from 249k into the February jobs report, while continuing claims eased to 1.35mln from 1.47mln). The ADP’s gauge of private payrolls was more-or-less in line with market expectations (455k vs expected 450k), while the February data was revised up a little (to 486k from 475k). The ISM business surveys have not been released ahead of the March jobs data– these usually offer us some insight about hiring activity. The comparable Markit PMI data, however, noted that companies were stepping up hiring, with the rate of overall jobs creation the highest since April 2021; “manufacturers and service providers alike recorded steeper upturns in employment,” the report said, “numerous firms noted that investment in recruitment campaigns was starting to show gains.” Goldman estimates that payrolls rose by an above-consensus 575k in March as “dining activity rebounded further in March, and most Big Data indicators are consistent with strong job gains.” Additionally, the bank believes that “fierce competition for workers incentivized firms to pull forward recruiting activities earlier in the spring hiring season.”

CONSUMER CONFIDENCE: Within the Conference Board’s gauge of consumer confidence, the number of consumers saying that jobs were “plentiful” rose to 57.2% from 53.5%, a new record high; the number of consumers who said jobs were “hard to get” fell to 9.8% from 12%, taking the differential to 47.4 from 41.5, boding well for those expecting the unemployment rate to decline. However, the survey also revealed that consumers were mixed in their views about the short-term outlook for the labour market, where the number expecting more jobs in the months ahead falling, even though those who anticipate fewer jobs also fell. Consumers were also mixed about their short-term financial prospects. “Confidence continues to be supported by strong employment growth and thus has been holding up remarkably well despite geopolitical uncertainties and expectations for inflation over the next 12 months reaching 7.9%—an all-time high,” the Conference Board said, adding that “these headwinds are expected to persist in the short term and may potentially dampen confidence as well as cool spending further in the months ahead.”

ARGUING FOR A STRONGER-THAN-EXPECTED REPORT:

Public health. After reaching new highs in December and early January, covid infections fell sharply in February and March, returning to last summer’s relatively low levels. Dining activity also rebounded sharply over the last two months. Coupled with the rise in ADP’s estimate of leisure and hospitality jobs, Goldman expects a significant contribution from leisure-sector payrolls in tomorrow’s report (our estimates embed a rise of 150k, mom sa).

Big Data. High-frequency data on the labor market also generally indicate strong growth in March employment. While Homebase is an outlier to the downside, that signal was overly pessimistic in five of the last six reports.

Seasonality. Some firms frontloaded spring hiring because of what Goldman believes was fierce competition for workers. In past tight labor markets, job growth tends to be stronger in the first quarter than in the second quarter. That being said, the March pace often slows relative to February’s.

Employer surveys. The employment components of business surveys generally increased in March. Goldman’s services survey employment tracker increased 1.8pt to 55.7 and our manufacturing survey employment tracker increased 0.5pt to 57.9. This resilience in domestic business surveys also argues against a meaningful employment drag from the Russia-Ukraine war.

Job availability. The Conference Board labor differential—the difference between the percent of respondents saying jobs are plentiful and those saying jobs are hard to get—increased by 5.4pt to an all-time high of +47.4. JOLTS job openings edged down by 17k in February to 11.3mn but remained above the pre-pandemic peak. Jobless claims. Initial jobless claims decreased during the March payroll month, averaging 209k per week vs. 231k in February. Continuing claims in regular state programs decreased 132k from survey week to survey week.

ARGUING FOR A WEAKER-THAN-EXPECTED REPORT

Job cuts. Announced layoffs reported by Challenger, Gray & Christmas increased by 4% month-over-month in March, after decreasing by 8% in February (SA by GS).

NEUTRAL/MIXED FACTORS

ADP. Private sector employment in the ADP report increased by 455k in March, in line with expectations but somewhat below tomorrow’s consensus for private payrolls (+496k mom sa).

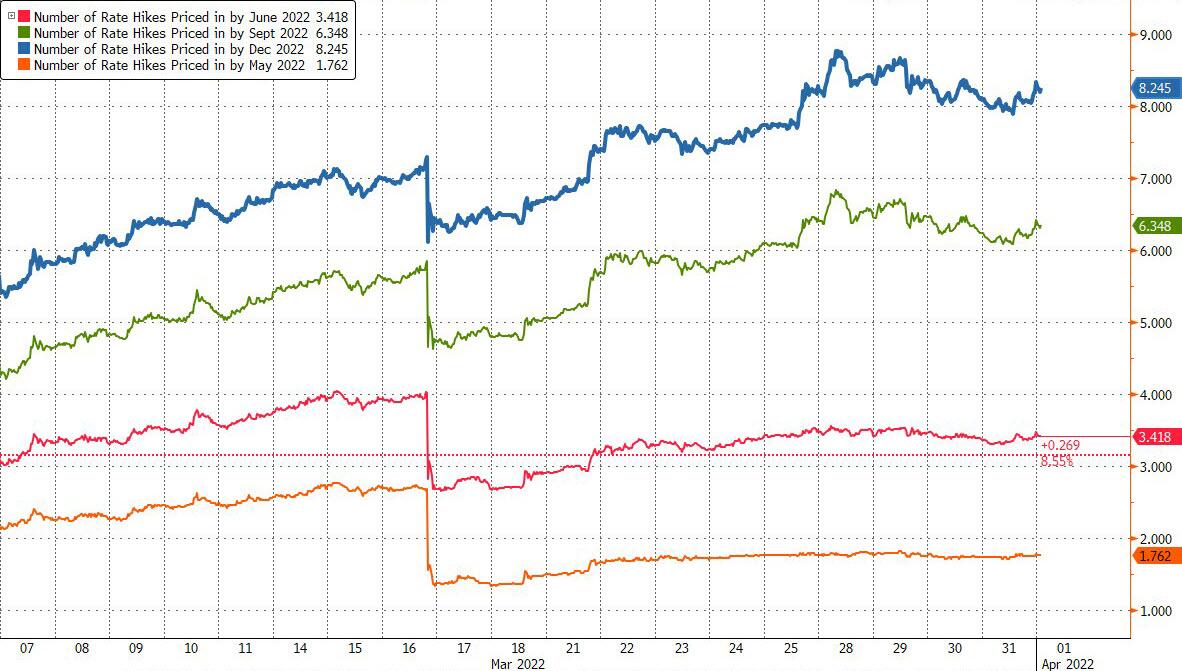

Mauled Treasuries To Get Some Respite, Fed Priced-In

Authored by Ven Ram, currency & rates strategist at Bloomberg,

As brutal as the bond-market backdrop has been, losses in Treasuries may abate in the second quarter even as the Federal Reserve takes aim at quelling inflation that is running at a breakneck pace.

The odds of a repeat of the first-quarter selloff are approximately 1-in-30,000…

The Bloomberg Treasury Index incurred a loss of 5.91% since the start of the year through Tuesday, the worst in data going back nearly 50 years.

That represented a 2.5 standard-deviation move to the left — in itself an extreme probability in a normal distribution of returns that is confirmed by running the Kolmogorov-Smirnov test.

Fundamentals also suggest that losses may moderate.

Two-year yields surged about 160 basis points this quarter, the most since 1984. That increase came on top of a 46-basis point move in the last quarter of 2021, suggesting the market has priced in the bulk of the Fed’s likely tightening.

The possibility of a de-escalation of conflict in Ukraine sent breakeven rates lower across the curve, with the markets heaving a sigh of relief on what that would mean for inflation.

The inversion of the two- and 10-year part of the yield curve may also alter investor behavior.

While there are more authentic markers of a true curve inversion, the negative spread may become a self-fulfilling prophecy: if economic agents in sufficient number believe a slowdown is in the offing and modify their decisions accordingly, we could get a veritable speed-bump.

Notice how the curve inverted well after news of Ukraine broke on Tuesday, suggesting that there is already a bid to mop up the yields currently available on the longer maturity.

That is classic investor behavior ahead of typical slowdowns.

The confluence of the de-escalation of conflict and fears of a slowdown — whether well-founded or otherwise — may therefore offer a tactical long bias for bonds.

While Fed speakers including Chair Jerome Powell have remarked that they are open to raising rates by 50 basis points if need be, they have stopped short of suggesting that such a scenario would be their base case.

Even though headline inflation is already running around 8%, the Fed seems reluctant to deploy outsized increases for fearing of creating an adverse feedback loop in the economy.

What could go wrong with this outlook?

Possibly, double-digit inflation. A monster print of that magnitude may force the Fed to raise rates by 50 basis points in May and keep volatility on the front burner.

That scenario apart, the current backdrop of markets having priced in an aggressive Fed trajectory and a possible de-escalation in Ukraine hostilities taken together suggests that the denouement for Treasuries may be less sordid in the months ahead.

German Chemical Giant Warns Of “Total Collapse” If Russian Gas Supply Cut

CEO of Germany’s multinational BASF SE, the world’s largest chemical producer, has warned that curbing or cutting off energy imports from Russia would bring into doubt the continued existence of small and medium-sized energy companies, and further would likely spiral Germany into its most “catastrophic” economic crisis going back to the end of World War 2.

Company CEO Martin Brudermuller issued the words in an interview with Frankfurter Allgemeine newspaper just ahead of German officials by midweek giving an “early warning” to industries and the population of possible natural gas shortages, as Russia appears ready to firmly hold to Putin’s recent declaration that “unfriendly countries” must settle energy payments in rubles, related to the Ukraine crisis and resultant Western sanctions.

According to Bloomberg he mused that while “Germany could be independent from Russia gas in four to five years” it remains that “LNG imports cannot be increased quickly enough to replace all Russian gas flows in the short term.”

But in the meantime, Brudermuller described that “It’s not enough that we all turn down the heating by 2 degrees now” given that “Russia covers 55 percent of German natural gas consumption.” He emphasized that if Russian gas disappeared overnight, “many things would collapse here” – given that “we would have high levels of unemployment, and many companies would go bankrupt. This would lead to irreversible damage.” He continued:

“To put it bluntly: This could bring the German economy into its worst crisis since the end of the Second World War and destroy our prosperity. For many small and medium-sized companies in particular, it could mean the end. We can’t risk that!”

The dire warning of coming disaster in the event Russian gas is shut off came in response being questioned over whether it’s at all possible to abandon Russian energy.

Asserting that this issue is not “black and white” – and that the German economy stands on the brink of catastrophe, the BASF CEO said that if this standoff continues to escalate it will “open the eyes of many on both sides”…

Below is the question posed by the newspaper, and Brudermuller’s response:

And what if, for example, Putin’s demand for payment in rubles leads to an immediate stop in gas supplies?

“A delivery stop for a short time would perhaps open the eyes of many – on both sides. It would make clear the magnitude of the consequences. But if we don’t get any more Russian gas for a long time, then we really have a problem here in Germany. At BASF, we would have to scale back or completely shut down production at our largest site in Ludwigshafen if the supply fell significantly and permanently below 50 percent of our maximum natural gas requirement. Minister Habeck has already activated the early warning level of the gas emergency plan.”

Separate sources estimate that at Ludwigshafen alone this scenario would immediately lead to some 40,000 employees being possibly laid off, or at least put on short-time working hours.

The chemical group BASF is one of the largest energy consumers in Germany, its CEO Brudermüller considers an import boycott of Russian natural gas to be irresponsible. He explains the consequences with many bankruptcies, destruction of corporate Germany.https://t.co/sPcWiJFnyg

He warned further in the interview that many Germans are currently greatly underestimating the consequences of what Russia shutting off the taps would mean… nothing less than a historic crisis:

“Many have misconceptions. I notice that in many of the conversations I have. People often make no connection at all between a boycott and their own job. As if our economy and our prosperity were set in stone.”

He explained that higher prices are already having a huge impact on the food supply given at this point BASF has been forced to reduce the production of ammonia for fertilizer production.

Brudermuller called this “a catastrophe and we will feel it even more clearly next year than this one. Because most of the fertilizers that the farmers need this year have already been bought. In 2023 there will be a shortage, and then the poor countries in particular, for example in Africa, will no longer be able to afford to buy basic foodstuffs.” In a very alarming statement and forewarning, he added: “There is a risk of famine.”

National Institutes of Health (NIH) documents obtained by a nonprofit watchdog in a federal court suit reveal that the agency deleted Covid-19 genetic sequencing information from the Wuhan Institute of Virology at the Chinese lab’s request.

The Arlington, Virginia-based Empower Oversight Whistleblowers and Researchers (EO) obtained, as a result of a Freedom of Information Act (FOIA) request and lawsuit, more than 230 pages of documents dating from 2020 that include emails, memoranda, and other correspondence among and between the lab and multiple NIH officials.

Covid-19 was first detected in China in late 2019, before it spread worldwide. Since the first death from the virus in the United States was reported in January 2020, an estimated 1 million Americans and 6 million globally have reportedly succumbed to the virus.

Controversy has raged in the United States over whether the virus originated in an animal-to-human transfer in a Wuhan-area wet market, as Chinese officials have insisted, or if it escaped from the Wuhan lab where research was being done on such viruses, some of which was being supported with NIH funds through the New York-based nonprofit EcoHealth Alliance.

Among the NIH officials prominently mentioned in the documents are then-NIH Director Dr. Francis Collins and National Institute for Allergies and Infectious Diseases (NIAID) Director Dr. Anthony Fauci, who actively participated in the discussions and decision-making described in the materials obtained by EO.

“On June 5, 2020, a Wuhan University researcher requested that NIH retract the researcher’s submission of BioProject ID PRJNA637497 because of error. The Wuhan researcher explained ‘I’m sorry for my wrong submitting,’” EO said in a statement on March 29.

“BioProject ID PRJNA637497 is also referred to as Submission ID SUB7554642. Three days later, on June 8th, the NIH declined the researcher’s request, advising that it prefers to edit or replace, as opposed to delete, sequences submitted to the SRA,” EO reported.

But then, on June 16, 2020, NIH officials reversed themselves and deleted the genetic sequencing data, as requested by the Wuhan researcher.

That researcher was quoted by EO as explaining to NIH: “Recently, I found that it’s hard to visit my submitted SRA data, and it would also be very difficult for me to update the data. I have submitted an updated version of this SRA data to another website, so I want to withdraw the old one at NCBI in order to avoid the data version issue.”

After some discussion about what would be deleted, the NIH concluded the discussion by reassuring the Wuhan researcher that it “had withdrawn everything.”

The documents also indicate, according to EO, that after researcher Jesse Bloom, a virologist at the Fred Hutchinson Cancer Research Center, “alerted NIH about the deleted sequences, [Collins] and [Fauci] hosted a Sunday afternoon Zoom meeting. The invitation Collins sent out for the meeting asks invitees to read Bloom’s [June 22, 2021] preprint paper closely and provide their ‘advice on the interpretation and significance of’ it.”

According to EO, the documents show that “Professor Trevor Bedford of the Fred Hutchinson Cancer Research Center later sent the group an email stating that the deleted data seemed to support the idea that the pandemic began outside the Huanan market in Wuhan and that the matter must be analyzed properly.”

If the virus’s spread began outside of the market, it would undermine the official Chinese government claim, and thus reinforce claims of experts in the United States and elsewhere that the pandemic likely escaped from the Wuhan lab.

The EO report also claims that NIH communications staff members were using off-the-record emails to advise “reporters toward more favorable coverage concerning termination of public access to the sequences by The Washington Post, and away from coverage by The New York Times, whose ‘tone’ had been criticized in communications among NIH officials.”

In addition, EO said NIH claims to have retained copies of the deleted data “for preservation purposes,” although the federal agency has refused to conduct a transparent examination of it.

An NIH spokesperson told The Epoch Times in an email that the sequences in question were submitted in March 2020 by a researcher at a China-based institution for posting in SRA, which it said it managed by NIH’s National Center for Biotechnology (NCBI).

“In June 2020, in response to a request by the same researcher, NCBI gave the sequence data the status of ‘withdrawn,’ which removes sequencing data from all public means of access but does not delete them. NCBI subsequently reassigned the status of the sequence data to ‘suppressed,’ which means that sequence data are removed from the search process but can be directly found by accession number. This action to reassign the data was identified as part of NLM’s ongoing review into the matter. We are working to make more information available,” the spokesperson said.

Collins, Fauci, and the NIAID did not respond to requests for comment.

The EO document release is likely to strengthen congressional efforts to get all the facts concerning the NIH’s role in funding the Wuhan lab research that may be at the center of the CCP virus’s creation and spread around the world.

Sen. Roger Marshall (R-Kan.), a physician who is a member of the Senate Committee on Health, Employment, Labor and Pensions (HELP), told The Epoch Times that “the NIH deleting key data at the onset of the pandemic has only caused more questions regarding its involvement on the emergence of” the virus.

“The American people deserve to know the truth behind the origins of COVID-19, as well as how we can best prepare for, prevent, and recover from future global pandemics,” Marshall said. “As a physician, I think we always need to know the what, where, how, and why when giving a diagnosis. For this reason, it couldn’t be more important that we get to the bottom of this deleted data and ensure that NIH operates at the interest of our national security.”

The HELP panel on March 15 approved legislation—the PREVENT Pandemics Act—that requires the establishment of a government task force to investigate the origins of the CCP virus. That legislation includes eight provisions authored by Marshall.

“This legislation is in response to the congressional inquiries and various media investigations–including The Epoch Times–revealing national security issues with federal agencies authorizing dangerous research with certain foreign entities that may have contributed to the COVID-19 pandemic,” Marshall’s office told The Epoch Times.

“Dr. Marshall secured his bipartisan 9/11-style COVID Task Force to investigate the origins of COVID-19, as well as find out how we can prepare for, prevent, and recover from future global pandemics,” his office said, adding that he seeks “to ensure that American organizations would never be allowed to conduct dangerous research capable of pandemic proportions with organizations in countries that threaten our national security.”

Sen. Marsha Blackburn (R-Tenn.) told The Epoch Times via email that “the radical left has systematically worked to cover the Chinese Communist Party’s tracks and hide the truth of COVID origins.”

“Dr. Fauci, the NIH, and liberal media giants weaponized the COVID-19 pandemic to shut down schools, businesses, and life for hardworking Americans. The report from Empower Oversight exposes what we’ve always known about COVID-19—it’s all about big government control,” she added.

Another Republican senator, Joni Ernst of Iowa, proposed last November to ban all federal funding of EcoHealth Alliance and the “gain-of-function” virus research it supported with federal funds at the Wuhan lab. Other congressional Republicans have also called for a federal investigation of the nonprofit.

Sri Lanka Turns Off Street Lights As Energy Crisis Worsens; Fishermen Unable To Sail For Lack Of Fuel

Tiny Sri Lanka is struggling through an economic crisis that is having terrible repercussions for its economy, as a brutal energy crisis threatens to blossom into shortages of food and other essential goods.

Thanks to an energy crisis (and China’s reluctance to allow the country to restructure its debts), Sri Lanka is resorting to turning off its street lights to save electricity as its worst economic crisis in decades bites, forcing – among other cutbacks – the temporary closure of the local stock market as the impact of the crisis is felt (the Colombo Stock Exchange reduced daily trading to two hours from the usual four-and-a-half because of the power cuts for the rest of this week at the request of brokers).

The island nation of 22 million people is struggling with rolling power cuts for up to 13 hours a day as the government is unable to make payments for fuel imports because of a lack of foreign exchange.

According to Reuters, the energy-drained country expects a diesel shipment paid for under a $500 million line of credit from neighboring India is expected to arrive on Saturday, but the situation isn’t expected to improve any time soon, as power restriction will need to continue, according to the country’s power minister.

“We have already instructed officials to shut off street lights around the country to help conserve power,” Power Minister Pavithra Wanniarachchi told reporters.

…

“Once that arrives we will be able to reduce load shedding hours but until we receive rains, probably some time in May, power cuts will have to continue,” Wanniarachchi told reporters, referring to the rolling power cuts.

“There’s nothing else we can do.”

Another reason for the power crisis (and a lesson for all nations that are aiming to ramp up ‘green’ energy sources): Water levels at reservoirs feeding hydro-electric projects had fallen to record lows, while demand had also hit record levels during the hot, dry season, she said.

As Reuters explains, the crisis in Sri Lanka is the result of a confluence of factors that have drained the country’s foreign exchange reserves.

The crisis is a result of badly timed tax cuts and the impact of the coronavirus pandemic coupled with historically weak government finances, leading to foreign exchange reserves dropping by 70% in the last two years.

Sri Lanka was left with reserves of $2.31 billion as of February, forcing the government to seek help from the International Monetary Fund and other countries, including India and China.

And if the situation doesn’t improve soon, the small country’s energy crisis could metastasize into a food crisis. Because, as the AFP explains, without fuel, the country’s fishermen have been stranded on shore, unable to reel in the day’s catch. And the ramifications are being felt by families across the country.

“If we queue up by five in the morning, then we will get fuel by three in the afternoon, on good days,” Arulanandan, a seasoned member of Negombo’s close-knit fishing community, tells AFP.

“But for some, even that is not possible, because by the time they get to the end of the queue, the kerosene is gone.”

As they look for somebody to blame, the locals have settled on one key culprit: Beijing, and its ‘debt diplomacy’, which seems to have caught Colombo in its trap.

One of the reasons behind economic crisis in Sri Lanka is its huge debt to China.

Sri Lanka asked China to restructure debt repayments.

China will implement its debt trap diplomacy in Sri Lanka

Instead of claiming Indian territory, Nepal should learn from the Sri Lankan crisis