Those trusting the Fed to be visibly weak, corrupt and incompetent forever might be in for an unwelcome surprise.

When even the crash test dummies are nervous, it pays to pay attention. Being in a mild crash isn’t too bad if all the protective devices inflate as intended. But in a horrific crash where nothing goes as planned, it’s like speeding in a ready-to-explode Pinto and being side-swiped by a semi on Dead Man’s Curve.

The stock market is in the Pinto, and the smell of gasoline is so strong it’s overpowering the smell of old Cheetos and stale beer. The Federal Reserve is driving, and it’s got a crazy glint in its eyes that everyone dismisses– to their immense regret when the Pinto goes off the cliff and flames envelop the wreckage.

We’re talking metaphorically here. The pain of catastrophic financial losses isn’t physical. But that doesn’t mean it won’t hurt for years or even decades.

Here’s a brief recap: The Fed says inflation is under control, will soon subside, and is no biggie.

In other words, the Fed believed it wielded Jedi Mind Tricks (to convince the masses that there was nothing to worry about as “this isn’t the inflation you’re looking for”) and that it was living in a Wizard of Oz world in which it possessed supernatural powers: if we say inflation is declining, it will decline.

Put simply, the Fed is completely delusional. If you need more proof, consider their risible claim that Fed policies aren’t the cause of soaring wealth inequality, when the evidence that the Fed has destabilized society by boosting wealth inequality to new heights is incontestable to all but con artists and the delusional.

Now that inflation is a raging conflagration, the Fed’s threadbare credibility is in tatters. The Fed is a laughing stock, and the only way to restore a few shreds of credibility to crush inflation by whatever means are necessary.

The poor fools in the back seat of the Pinto don’t believe the Fed would ever put their beloved stock market at risk. But the Fed has no choice. Of course they’re trying another lame Jedi Mind Trick, claiming they can crush inflation and restore their credibility in an imaginary “soft landing,” but no one believes this.

The truth few seem willing to entertain is the Fed has to crash the market because there is no other way to restore its shredded credibility. Having blown the opportunity to restore some basic discipline, the Fed has been revealed as 1) delusional, disconnected from reality, drifting in a la-la land of fantasy, and 2) weak, corrupt and incompetent, a bad combination, as it has done nothing but kiss the derrieres of billionaires for years while claiming to serve those it has impoverished (the bottom 90%).

The crash test dummies want no part of the Fed’s Pinto Joy Ride to Doom. Maybe the Pinto does a couple of 360 spins and doesn’t fly off Dead Man’s Curve. Maybe the crash just dents the fender. Those trusting the Fed to be visibly weak, corrupt and incompetent forever might be in for an unwelcome surprise.

For freak’s sake, people, wake the freak up. There’s no risk in la-la land, but this is reality. Risk is on a SpaceX rocket ride to heights unknown.

My first book, Unprecedented, told the story of the Affordable Care Act during President Obama’s first term, culminating with NFIB v. Sebelius. My second book, Unraveled, recounted the ACA during Obama’s second term, including Hobby Lobby, King v. Burwell, and Zubick. I am working on the third book in the trilogy, Undefeated, which recounts the ACA during President Trump’s term, and into the Biden administration. This book will focus on Little Sisters of the Poor and California v. Texas, among other topics. From beginning to end, this twelve-year arc represents, I think, the complete debates over the ACA. To be sure, people still will object to Obamacare, but now the law has been woven into the fabric of our society.

Yesterday, former-President Obama visited the White House. And the namesake of the law took a victory lap. His light-hearted remarks offer a useful summary of Obamacare’s many twists and turns since 2010.

I think it’s been well documented just how difficult it was to pass the ACA. (Laughter.) There — there’s — you can get a lot of testimony here, in case folks haven’t heard.

As a country, we had been talking about reforming healthcare for 100 years. Unlike almost every other advanced economy on Earth, we didn’t have a system that guaranteed access to healthcare for all of its citizens. Millions of people didn’t have health insurance, often because their employers didn’t provide it or because it was too expensive.

But despite the fact that our healthcare system didn’t work well, it was hard to change. Healthcare represents about one-fifth of our economy; that’s trillions of dollars that are involved. So there were a lot of different economic interests that were vying to maintain the status quo.

And because the majority of Americans did have healthcare, some people naturally worried that they’d lose what they had. The media was skeptical of past failures. There was a lot of misinformation, to say the least, flying around. And it’s fair to say that most Republicans showed little interest in working with us to get anything done. (Laughter.) That’s fair to say.

But despite great odds, Joe and I were determined, because we’d met too many people on the campaign trail who’d shared their stories, and our own families had been touched by illness.

And as I said to our dear friend Harry Reid, who is missed — wish he was here today, because he took great pride in what we did — I intended to get healthcare passed even if it cost me reelection — which, for a while, it looked like it might. (Laughter.)

But for all of us — for Joe, for Harry, for Nancy Pelosi, for others — the ACA was an example of why you run for office in the first place, why all of you sign up for doing jobs that pay you less than you can make someplace else; why you’re away from home sometimes and you miss some soccer practices or some dance recitals.

Because we don’t — we’re not supposed to do this just to occupy a seat or to hang on to power. We’re supposed to do this because it’s making a difference in the lives of the people who sent us here.

And because of so many people, including a lot of people who are here today, made enormous sacrifices; because members of Congress took courageous votes, including some who knew that their vote would likely cost them their seat; because of the incredible leadership of Nancy and Harry, we got the ACA across the finish line together. (Applause.)

And the night we passed the ACA — I’ve said it before — it was a high point of my time here, because it reminded me and it reminded us of what is possible.

But, of course, our work was not finished. Republicans tried to repeal what we had done — again, and again, and again. (Laughter.) And they filed lawsuits that went all the way to the Supreme Court three times. I see Don Verrilli here who had to defend a couple of them. (Applause.)

They tried explicitly to make it harder for people to sign up for coverage.

And let’s face it: It didn’t help that when we first rolled out the ACA, the website didn’t work. (Laughter.) That was not one of my happiest moments. (Laughter.)

So, given all the noise and the controversy and the skepticism, it took a while for the American people to understand what we had done. But lo and behold, a little later than I’d expected, a lot of folks, including many who had initially opposed healthcare reform, came around.

And today, the ACA hasn’t just survived; it’s pretty darn popular. And the reason is because it’s done what it was supposed to do. It’s made a difference.

First, 20 million and now 30 million people have gotten covered thanks to the ACA. (Applause.)

It’s — it’s prevented insurance companies from denying people coverage based on a pre-existing condition. It’s lowered prescription drug costs for 12 million seniors. It’s allowed young people to stay on their parents’ plan until they’re 26. It’s eliminated lifetime limits on benefits that often put people in a jam.

So, we are incredibly proud of that work.

But the reason we’re here today is because President Biden, Vice President Harris, everybody who has worked on this thing understood from the start that the ACA wasn’t perfect. To get the bill passed, we had to make compromises. We didn’t get everything we wanted. That wasn’t a reason not to do it. If you can get millions of people health coverage and better protection, it is — to quote a famous American — a pretty “big deal.” (Laughter and applause.) That’s what it is. (Applause.) A big deal.

But there were gaps to be filled. Even today, some patients still pay too much for their prescriptions. Some poor Americans are still falling through the cracks. In some cases, healthcare subsidies aren’t where we want them to be, which means that some working families are still having trouble paying for their coverage.

Here’s the thing: That’s not unusual when we make major progress in this country. The original Social Security Act left out entire categories of people, like domestic workers and farm workers. That had to be changed. In the beginning, Medicare didn’t provide all the benefits that it does today. That had to be changed.

Throughout history, what you see is that it’s important to get something started, to plant a flag, to lay a foundation for further progress.

The analogy I’ve used about the ACA before is that: In the same way that was true for early forms of Social Security and Medicare, it was a starter home. (Laughter.) It secured the principle of universal healthcare, provided help immediately to families. But it required us to continually build on it and make it better.

And President Biden understands that. And that’s what he’s done since the day he took office. As part of the American Rescue Plan, he lowered the cost of healthcare even further for millions of people. He made signing up easier. He made outreach to those who didn’t know they could get covered — make sure that they knew; made that a priority.

And as a result of these actions, he helped a record 14.5 million Americans get covered during the most recent enrollment period. (Applause.)

That, ladies and gentlemen, is what happens when you have an administration that’s committed to making a program work. (Applause.)

And today — today, the Biden-Harris administration is going even further by moving to fix a glitch in the regulations that will lower premiums for nearly 1 million people who need it and allow 200,000 more uninsured Americans get access to coverage.

I’m a private citizen now, but I still take more than a passing interest in the course of our democracy. (Laughter.) But I’m outside the arena, and I know how discouraged people can get with Washington — Democrats, Republicans, independents. Everybody feels frustrated sometimes about what takes place in this town. Progress feels way too slow sometimes. Victories are often incomplete. And in a country as big and as diverse as ours, consensus never comes easily.

But what the Affordable Care Act shows is that if you are driven by the core idea that, together, we can improve the lives of this generation and the next, and if you’re persistent — if you stay with it and are willing to work through the obstacles and the criticism and continually improve where you fall short, you can make America better — you can have an impact on millions of lives. You can help make sure folks don’t have to lose their homes when they get sick, that they don’t have to worry whether a loved one is going to get the treatment they need.

President Joe Biden understands that. He has dedicated his life to the proposition that there’s something worthy about public service and that the reason to run for office is for days like today.

So, I could not be more honored to be here with him as he writes the next chapter in our story of progress. I’m grateful for all the people who have been involved in continuing to make the ACA everything it can be.

And it is now my great privilege to introduce the 46th President of the United States, Joe Biden. (Applause.)

In addition to the proposed ban on coal imports, the sanctions package was also said to include new restrictions on the Russian banking sector and bans on certain chemical exports:

Russian vessels and trucks will also be prevented from accessing the EU, further crippling trade with Russia, the source said, adding that exceptions will be made for energy products, food and medicines.

The EU will also ban all transactions with VTB and another three Russian banks which had already been excluded from the SWIFT messaging system, the source said.

Dozens more individuals, including oligarchs and politicians, will be added to the EU sanction list, the source said.

The latest reports are chiefly concerned with this last measure. According to Bloomberg and the FT, the EU is discussing Wednesday whether to sanction Russian aluminum tycoon Oleg Deripaska (best known to Americans for his relationship with Paul Manafort, and for being targeted with sanctions by the Trump Administration which forced him to dilute his stake in Rusal), along with a handful of other executives, including Alexander Shulgin, the head of Russian e-commerce platform Ozon, Boris Rotenberg, a close business associate of President Putin, and Said Kerimov, who controls Russia’s largest gold miner Polyus, according to Bloomberg.

As for Rotenberg, a Finnish citizen, he made his fortune thanks to tenders and contracts from state-controlled oil and gas companies. He and his nephew, Igor, are set to be placed under sanctions for their close ties to Putin. Arkady Rotenberg, Boris’s brother, is already under sanctions.

The new list of individuals targeted by the EU also includes Vladimir Bogdanov, director-general of Surgutneftegas, Russia’s third-largest oil producer which accounts for about 10 per cent of the country’s crude production.

But it’s not just businessmen who are being targeted. Per the FT, Ekaterina Tikhonova and Maria Vorontsova, Putin’s daughters from his first marriage, are also being targeted for allegedly benefiting from the Russian state. Of course, sanctioning Putin’s daughters would only have “symbolic” significance, since neither of them control significant assets, as BBG explained.

If approved, those targeted by the sanctions will be subject to asset freezes and travel bans.

As far as Gref and Shulgin are concerned, the bloc’s justification for targeting them is based on their attendance at a televised meeting with Putin in the Kremlin on the day the invasion began. Ambassadors from EU member states are meeting in Brussels on Wednesday to discuss the proposal before it is officially proposed to become law.

The latest round of EU measures is also expected to include export bans worth €10bn in areas including quantum computers and advanced semiconductors, and bans worth €5.5bn, on products including wood, cement, seafood and liquor. The EU is not expected to hit Russian oil exports in the current round of sanctions, but officials are discussing ways of including the sector in future rounds of penalties.

German media reports on Wednesday suggested that the sanctions on Russian coal could be just the beginning, and that further bans on gas and oil might be possible (of course, the consequences for the German economy would be extremely dire if this were to happen).

EU Council President Charles Michel told the EU Parliament on Wednesday that “I think that measures on oil and even gas will also be needed sooner or later.” Of course, that’s much easier said than done.

When it comes to the sanctions on Russian coal, Germany’s coal importers’ group VDKi on Wednesday said the country should be able to find alternatives to Russian hard coal imports by the peak demand winter season – the only issue is that it will likely cost more, driving inflation in the bloc even higher.

My first book, Unprecedented, told the story of the Affordable Care Act during President Obama’s first term, culminating with NFIB v. Sebelius. My second book, Unraveled, recounted the ACA during Obama’s second term, including Hobby Lobby, King v. Burwell, and Zubick. I am working on the third book in the trilogy, Undefeated, which recounts the ACA during President Trump’s term, and into the Biden administration. This book will focus on Little Sisters of the Poor and California v. Texas, among other topics. From beginning to end, this twelve-year arc represents, I think, the complete debates over the ACA. To be sure, people still will object to Obamacare, but now the law has been woven into the fabric of our society.

Yesterday, former-President Obama visited the White House. And the namesake of the law took a victory lap. His light-hearted remarks offer a useful summary of Obamacare’s many twists and turns since 2010.

I think it’s been well documented just how difficult it was to pass the ACA. (Laughter.) There — there’s — you can get a lot of testimony here, in case folks haven’t heard.

As a country, we had been talking about reforming healthcare for 100 years. Unlike almost every other advanced economy on Earth, we didn’t have a system that guaranteed access to healthcare for all of its citizens. Millions of people didn’t have health insurance, often because their employers didn’t provide it or because it was too expensive.

But despite the fact that our healthcare system didn’t work well, it was hard to change. Healthcare represents about one-fifth of our economy; that’s trillions of dollars that are involved. So there were a lot of different economic interests that were vying to maintain the status quo.

And because the majority of Americans did have healthcare, some people naturally worried that they’d lose what they had. The media was skeptical of past failures. There was a lot of misinformation, to say the least, flying around. And it’s fair to say that most Republicans showed little interest in working with us to get anything done. (Laughter.) That’s fair to say.

But despite great odds, Joe and I were determined, because we’d met too many people on the campaign trail who’d shared their stories, and our own families had been touched by illness.

And as I said to our dear friend Harry Reid, who is missed — wish he was here today, because he took great pride in what we did — I intended to get healthcare passed even if it cost me reelection — which, for a while, it looked like it might. (Laughter.)

But for all of us — for Joe, for Harry, for Nancy Pelosi, for others — the ACA was an example of why you run for office in the first place, why all of you sign up for doing jobs that pay you less than you can make someplace else; why you’re away from home sometimes and you miss some soccer practices or some dance recitals.

Because we don’t — we’re not supposed to do this just to occupy a seat or to hang on to power. We’re supposed to do this because it’s making a difference in the lives of the people who sent us here.

And because of so many people, including a lot of people who are here today, made enormous sacrifices; because members of Congress took courageous votes, including some who knew that their vote would likely cost them their seat; because of the incredible leadership of Nancy and Harry, we got the ACA across the finish line together. (Applause.)

And the night we passed the ACA — I’ve said it before — it was a high point of my time here, because it reminded me and it reminded us of what is possible.

But, of course, our work was not finished. Republicans tried to repeal what we had done — again, and again, and again. (Laughter.) And they filed lawsuits that went all the way to the Supreme Court three times. I see Don Verrilli here who had to defend a couple of them. (Applause.)

They tried explicitly to make it harder for people to sign up for coverage.

And let’s face it: It didn’t help that when we first rolled out the ACA, the website didn’t work. (Laughter.) That was not one of my happiest moments. (Laughter.)

So, given all the noise and the controversy and the skepticism, it took a while for the American people to understand what we had done. But lo and behold, a little later than I’d expected, a lot of folks, including many who had initially opposed healthcare reform, came around.

And today, the ACA hasn’t just survived; it’s pretty darn popular. And the reason is because it’s done what it was supposed to do. It’s made a difference.

First, 20 million and now 30 million people have gotten covered thanks to the ACA. (Applause.)

It’s — it’s prevented insurance companies from denying people coverage based on a pre-existing condition. It’s lowered prescription drug costs for 12 million seniors. It’s allowed young people to stay on their parents’ plan until they’re 26. It’s eliminated lifetime limits on benefits that often put people in a jam.

So, we are incredibly proud of that work.

But the reason we’re here today is because President Biden, Vice President Harris, everybody who has worked on this thing understood from the start that the ACA wasn’t perfect. To get the bill passed, we had to make compromises. We didn’t get everything we wanted. That wasn’t a reason not to do it. If you can get millions of people health coverage and better protection, it is — to quote a famous American — a pretty “big deal.” (Laughter and applause.) That’s what it is. (Applause.) A big deal.

But there were gaps to be filled. Even today, some patients still pay too much for their prescriptions. Some poor Americans are still falling through the cracks. In some cases, healthcare subsidies aren’t where we want them to be, which means that some working families are still having trouble paying for their coverage.

Here’s the thing: That’s not unusual when we make major progress in this country. The original Social Security Act left out entire categories of people, like domestic workers and farm workers. That had to be changed. In the beginning, Medicare didn’t provide all the benefits that it does today. That had to be changed.

Throughout history, what you see is that it’s important to get something started, to plant a flag, to lay a foundation for further progress.

The analogy I’ve used about the ACA before is that: In the same way that was true for early forms of Social Security and Medicare, it was a starter home. (Laughter.) It secured the principle of universal healthcare, provided help immediately to families. But it required us to continually build on it and make it better.

And President Biden understands that. And that’s what he’s done since the day he took office. As part of the American Rescue Plan, he lowered the cost of healthcare even further for millions of people. He made signing up easier. He made outreach to those who didn’t know they could get covered — make sure that they knew; made that a priority.

And as a result of these actions, he helped a record 14.5 million Americans get covered during the most recent enrollment period. (Applause.)

That, ladies and gentlemen, is what happens when you have an administration that’s committed to making a program work. (Applause.)

And today — today, the Biden-Harris administration is going even further by moving to fix a glitch in the regulations that will lower premiums for nearly 1 million people who need it and allow 200,000 more uninsured Americans get access to coverage.

I’m a private citizen now, but I still take more than a passing interest in the course of our democracy. (Laughter.) But I’m outside the arena, and I know how discouraged people can get with Washington — Democrats, Republicans, independents. Everybody feels frustrated sometimes about what takes place in this town. Progress feels way too slow sometimes. Victories are often incomplete. And in a country as big and as diverse as ours, consensus never comes easily.

But what the Affordable Care Act shows is that if you are driven by the core idea that, together, we can improve the lives of this generation and the next, and if you’re persistent — if you stay with it and are willing to work through the obstacles and the criticism and continually improve where you fall short, you can make America better — you can have an impact on millions of lives. You can help make sure folks don’t have to lose their homes when they get sick, that they don’t have to worry whether a loved one is going to get the treatment they need.

President Joe Biden understands that. He has dedicated his life to the proposition that there’s something worthy about public service and that the reason to run for office is for days like today.

So, I could not be more honored to be here with him as he writes the next chapter in our story of progress. I’m grateful for all the people who have been involved in continuing to make the ACA everything it can be.

And it is now my great privilege to introduce the 46th President of the United States, Joe Biden. (Applause.)

Most people seem to think that tighter monetary policy will bring on a recession, but they believe that it will solve the inflation problem. In his podcast, Peter Schiff explained why they’ve got it half right. We are heading toward a recession, but it’s not going to solve the inflation problem. In reality, we’re heading for stagflation.

Inflation is a problem globally, but the only major central bank talking about fighting inflation is the Fed. The European Central Bank and the Bank of Japan continue to hold interest rates down and run quantitative easing, despite rising prices in both economies. And as Peter said, all the Fed is doing is talking. It won’t actually fight inflation.

Their inconsequential, tiny rate hikes are going to do anything. In fact, the only reason they’re raising rates at all is to pretend they can keep on doing it. But at some point, they will reverse course because the bond market has that right. These higher rates are going to cause a recession, and it’s not going to take that many hikes to push the economy into recession given how addicted the economy is and how overleveraged the economy is. So, once the impact on the economy and on the financial markets is felt, then the Fed is going to give up all the tough talk and inflation is going to continue to get worse.”

As Peter mentioned, the bond market is already signaling recession warnings with inversions of the yield curve. Meanwhile, bonds had their worst quarter in 40 years. And the data is starting to reveal cracks in the economy.

Construction spending disappointed, coming in 0.4% below expectation. It was up 0.5%. The expectation was a 0.9% increase. This reflects an increase in the dollars spent on construction, not an increase in construction per see. Peter said he thinks construction is slowing down due to rapidly rising costs.

What’s happening is we’re constructing fewer structures, but we are paying a lot more to construct the ones we are building, and that’s why construction spending is going up — because builders are spending more money to build fewer homes. So, again, this is not good news. This is bad news for the economy.”

ISM manufacturing numbers also came in weaker than expected. Manufacturing grew in March, but it was down from February. The expectation was for the ISM to come in at 59, up slightly from 58.6 in February. The actual number was 57.1.

We also got the March jobs numbers last week. Most pundits spun them as good news with the addition of 431,000 jobs and significant upward revisions the January and February. But this was largely a function of huge adjustments made by the BLS. Nevertheless, the unemployment rate dropped down to 3.6%. Of course, government numbers understate unemployment. But this is still a low number.

Most mainstream economists, particularly those at the Fed, believe low unemployment is correlated to inflation. That being the case, Peter said interest rates should be much higher.

We have a huge inflation problem, and the Fed continues to drag their feet. Even though they acknowledge that it’s a big problem, they’re doing nothing about solving it. Raising interest rates from zero to 25 basis points in the face of this huge problem is not solving it. It’s continuing to make it worse. They are throwing gasoline on a fire even though they acknowledge that the fire is burning, which again proves it’s not about inflation. The Fed knows they can’t fight inflation. But they also know they can’t admit that. So, they’re trying to solve the problem by pretending they’re fighting inflation even though they continue to create it.”

There are all kinds of reasons bandied about for rising prices. But ultimately, it is the Federal Reserve and its expansion of the money supply.

To the extent that the economy gets weaker, they’re going to try to expand the money supply even more aggressively to try to stimulate it, which is why we’re going to have more inflation during the next recession.”

All of this adds up to stagflation.

In this podcast, Peter also talks about the stock market, the dollar, the bond market and commodities.

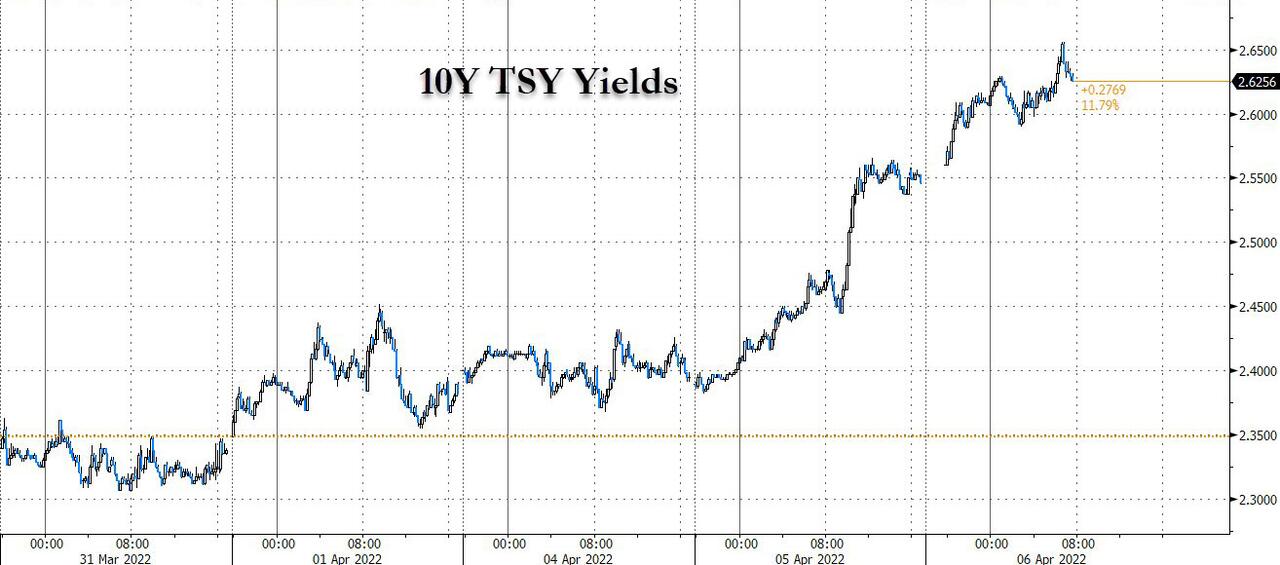

Futures, Treasuries Tumble On Fed Tightening Fears As FOMC Minutes Loom

There is a scene in My Cousin Vinny where Joe Pesci’s puzzled wannabe-lawyer character asks the judge if he was really serious ’bout dat.

On Tuesday and overnight, incredulous algos and 15 year old hedge fund managers had a similar question to the Fed about its market-crushing, rate-hiking intentions, after yesterday the Fed’s in house permadove and Hillary Clinton donor, Lael Brainard, shocked markets when she not only made the case for accelerated rate hikes but also a faster balance sheet drawdown after she said that curbing inflation is “paramount” and the central bank may start trimming its balance sheet rapidly as soon as May.

As a result, investors once again feared out that a more restrictive U.S. central bank could end up tipping the world’s largest economy into a downturn, or even a recession, something which is now Deutsche Bank’s base case for 2024. The virus resurgence in Asia and the war in Ukraine are also clouding the outlook for prices and growth.

“Market participants finally acknowledged that central banks are serious and will raise interest rates significantly to bring inflation rates down,” Florian Spate, a senior bond strategist at Generali Investments, wrote in a note. “We expect the selloff to lose momentum but the general trend for yields is likely to point still upwards.”

It also meant a plunge in both US stocks and bonds, and a continuation of this selloff across global markets overnight, which then fed back into US future weakness again this morning and saw tech companies lead U.S. index futures lower on Wednesday as concerns mounted over the pace of the Federal Reserve’s monetary tightening and a worsening pandemic in China.

Futures on the Nasdaq 100 were down about 1.5% and contracts on the S&P 500 slid -1% with tech heavyweights among the worst performers in premarket trading. Global stocks and bonds also fell. The Stoxx Europe 600 index was down more than 1%, with travel, carmakers and tech leading declines. 10Y yields soared as high as 2.65% and a gauge of the dollar’s strength rose to a three-week peak.

Tesla, Nvidia, Applied Materials, Amazon, Alphabet, Qualcomm and Boeing were among the worst performers in premarket trading. Starbucks slipped after the company announced the ousting of its top lawyer. Here are some other notable movers:

Shares of Spirit Airlines (SAVE US) fall 2.6% in U.S. premarket, erasing some of prior day’s steep gains after the budget carrier received a $3.6 billion takeover offer from JetBlue (JBLU US) that topped a competing bid by Frontier Group. JetBlue -4.3%.

Twitter (TWTR US) slips 1.3% after two-day surge of about 30%. Elon Musk refiled the disclosure of his stake to classify himself as an active investor, making the change after taking a seat on the social media company’s board.

Array Technologies’ (ARRY US) strong order book and better-than-expected FY22 guidance were welcomed by analysts, however they also highlight margin pressure and potential impacts from an antidumping and countervailing duties (AD/CVD) investigation. Array gains 11% premarket.

Tech companies led U.S. index futures lower on Wednesday as concerns mounted over the pace of the Federal Reserve’s monetary tightening and a worsening pandemic in China. Apple (AAPL US) -0.8%.

Gogo (GOGO US) gains 11% premarket on news that it will join the S&P Smallcap 600 Index before trading opens April 8, according to S&P Dow Jones Indices.

US-listed Chinese stocks fall in premarket trading Wednesday, tracking Asian peers, as a selloff in bonds pressures tech shares. The decline in Chinese ADRs follows a 3.8% drop in Hang Seng Tech Index, the most in more than a week, with Alibaba and JD.com among the biggest decliners In premarket trading, Alibaba drops 2.2%, JD.com falls 2.5% and Pinduoduo declines 2.8%; Baidu -1.6%, while Bilibili -1.2%. Among electric carmakers, Nio -2.4%, Li Auto -2% and XPeng -2.4%.

Even more hawkish surprises from the Fed may be on deck: according to Swissquote analyst Ipek Ozkardeskaya, the Fed minutes expected on Wednesday afternoon may hint at a 50 basis-point hike at the next meeting. The latest comments from policy makers, surging inflation, strong jobs data and rising wages all support an accelerated tightening campaign, she said. “The market risks remain tilted to the downside,” said Ozkardeskaya. “If there is a good time for the Fed to hit the brakes on its ultra-lose policy, it is now.”

The selloff was broad based and also hammered rates, with the 10-year Treasury yield rising as high as 2.65%, taking it back into the ranges traded in 2018 and 2019. Money-market traders are betting on the steepest Fed tightening in almost three decades following Brainard’s comments. Sovereign debt across Europe retreated after bonds in Australia and New Zealand tumbled.

“The QE honeypot looks close to being empty now,” Jeffrey Halley, a senior market analyst at Oanda, wrote in a note. “I’m not sure we will get a soft landing, and nor am I sure the FOMO gnomes of the equity market will be able to continue ignoring reality, particularly if U.S. yields continue to rise.”

In Europe, automotive, travel, technology and consumer companies were the worst performers, leading declines in the Stoxx Europe 600 Index which dropped 1.5%. Delivery Hero sank 5% in Germany. Imperial Brands rose 3.1% after the U.K. cigarette producer forecast a slight increase in profit this year. Here are some of the biggest European movers today:

Chr. Hansen shares rise as much as 5.5%, leading gains on the Stoxx 600 and the Health Care sub-index, after the nutritional ingredients manufacturer reported consensus-beating 2Q earnings.

Imperial Brands shares climb as much as 3.5% after the company said its FY outlook is in line with the revised guidance issued last month. It’s been a solid start to the year, RBC says.

IWG shares rise as much as 6% after the stock is raised to buy from hold at Peel Hunt, with the broker seeing multiple ways the flexible offices firm could create value.

Avio shares rise as much as 15% the most intraday in a year after the stock was raised to buy from neutral at Banca Akros after Amazon’s “massive order” for Ariane 6 launches.

Huber + Suhner shares climb to a record high after UBS upgrades to buy from neutral, citing “under-appreciated” prospects for the maker of radio- frequency and fiber-optic technology.

Semiconductor stocks lead European tech stocks lower on Wednesday as a selloff in bonds steepens amid hawkish commentary from Federal Reserve Governor Lael Brainard.

Among semiconductor stocks, ASML drops 3.4%, ASM International -5%, Infineon -3.7%, Nordic Semi -7.6%, BE Semi -4.8%

Royal Mail shares fall as much as 4.6%, hitting the lowest since Dec. 21, as Barclays cut its PT on the postal group to 400p from 640p with FY23 likely to be a challenging year.

Stroeer shares drop after HSBC cut the advertising firm’s rating to hold, saying the stock may find it difficult to withstand cyclical headwinds as the Ukraine war weighs on economic growth.

Avon Protection shares drop as much as 25% with Jefferies saying the protective-equipment maker’s latest update is “disappointing.”

Earlier in the session, Asian stocks traded lower across the board following the losses on Wall Street as Mainland China returned from its long-weekend. ASX 200 conformed to the downbeat tone which isn’t helped by the RBA’s hawkish hold yesterday. Japan’s Nikkei 225 saw most of its construction and machinery-related names with losses. KOSPI was pressured by its large tech exposure. Hang Seng was also weighed on by its tech exposure as yields continued to rise overnight. The Shanghai Comp returned for the first time this week following its domestic holiday and saw less pronounced losses, with the Real Estate sector feeling relief from reports that over 60 Chinese cities ease policies on housing purchases to support the market.

In rates, the Treasuries selloff extended with the curve steepening sharply out to the 10-year sector after Tuesday’s aggressive selloff — spurred by hawkish Fed comments — was extended during the Asia session. Wednesday’s focal points include the March FOMC minutes release, expected to feature balance-sheet runoff details. Yields are higher by as much as 8bp after the 10-year rose as much as 11bp to nearly 2.66%, highest since March 2019; The 2s10s curve is steeper by ~4.5bp on the day near 7bp, while 2s10s30s fly cheapens around 5bp follows Tuesday’s 9bp jump wider; 10s30s curve spread is back around 2bp after briefly inverting for first time since 2006. Into the selloff, long-end swap spreads have widened, 10- and 30-year by 1bp-2bp.

In FX, Bloomberg dollar spot index fades a push higher to trade flat. GBP and NZD are the strongest performers in G-10 FX, CHF and JPY underperform.

In FX, a gauge of the dollar’s strength rose to a three-week peak.

In commodities, WTI crude rose above $103 a barrel, before stalling near $104 . Worries remain that Russia’s growing isolation over the war in Ukraine may further disrupt commodity flows. Fresh sanctions on Russia are expected, including a U.S. ban on investment in the country and a European Union proscription on coal imports. Most base metals trade in the red; LME lead falls 0.7%, underperforming peers. Spot gold rises roughly $6 to trade near $1,929/oz.

Crypto markets experienced sudden selling pressure overnight with Bitcoin losing USD 45k, a level it has

acquired a foothold on during the European session

Market Snapshot

S&P 500 futures down 1% to 4,475.00

STOXX Europe 600 down 0.9% to 458.77

German 10Y yield little changed at 0.66%

Euro little changed at $1.0912

Brent Futures up 0.9% to $107.63/bbl

MXAP down 1.4% to 179.00

MXAPJ down 1.2% to 593.59

Nikkei down 1.6% to 27,350.30

Topix down 1.3% to 1,922.91

Hang Seng Index down 1.9% to 22,080.52

Shanghai Composite little changed at 3,283.43

Sensex down 0.8% to 59,672.08

Australia S&P/ASX 200 down 0.5% to 7,490.09

Kospi down 0.9% to 2,735.03

Brent Futures up 0.9% to $107.63/bbl

Gold spot up 0.0% to $1,923.71

U.S. Dollar Index little changed at 99.50

Top Overnight News from Bloomberg

Money-market traders are betting the Federal Reserve will implement 225 basis points of interest-rate hikes by the end of the year. Factoring in the hike already delivered in March, that would mean an increase of 2.5 percentage points for the whole year. The Fed hasn’t done that much tightening in one year since 1994, a famously brutal year for bond investors that even included a 75 basis-point hike

The Bloomberg Global Aggregate Index fell below a measure of so-called par value Tuesday, with its price falling to 99.9 — under the key 100 level at which bonds are often sold to investors. It’s the first time since 2008 that the gauge has traded at a discount to face value

The Federal Reserve will unveil details of its likely plans to shrink its massive balance sheet with the release of minutes of the U.S. central bank’s March meeting, as policy makers confront the highest inflation in four decades

Leaving the European Central Bank to fight the current bout of energy-driven inflation alone would only work at a steep cost to society, according to Executive Board member Fabio Panetta

German factory orders fell in February, dropping for the first time in four months in the runup to Russia’s invasion of Ukraine and underscoring concerns over slower growth in Europe’s largest economy

Turkey’s Recep Tayyip Erdogan approved on Wednesday a set of changes to the country’s electoral rules that would bolster his party’s prospects and consolidate the shift toward an all- powerful presidency set to be tested at the ballot box next year

The U.S., European Union and Group of Seven are coordinating on a fresh round of sanctions on Russia, including a U.S. ban on investment in the country and an EU ban on coal imports, following the discovery of civilian murders and other atrocities in Ukrainian towns abandoned by retreating Russian forces

The European Union’s foreign policy chief described a summit with Chinese President Xi Jinping as a “deaf dialog,” casting doubt on how much cooperation the Asian nation will offer to end the war in Ukraine

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac markets traded lower across the board following the losses on Wall Street; Mainland China returned from its long-weekend. ASX 200 conformed to the downbeat tone which isn’t helped by the RBA’s hawkish hold yesterday. Nikkei 225 saw most of its construction and machinery-related names with losses. KOSPI was pressured by its large tech exposure. Hang Seng was also weighed on by its tech exposure as yields continued to rise overnight. Shanghai Comp returned for the first time this week following its domestic holiday and saw less pronounced losses, with the Real Estate sector feeling relief from reports that over 60 Chinese cities ease policies on housing purchases to support the market.

Top Asian News

Hong Kong Chief Secretary John Lee Resigns, Government Says

China Backs Ex-Security Chief to Lead Hong Kong, SCMP Says

Singaporeans Need $73,549 Just for Right to Buy a Car

EU’s Top Envoy Calls Summit With China’s Xi a ‘Deaf Dialog’

European bourses deteriorated further from a tepid cash open, in-fitting with the Wall St./APAC handover, Euro Stoxx 50 -1.6% Such downside was exacerbated by weak Construction PMIs and as yields continue to make further advances ahead of ECB’s Lane & FOMC Minutes. As such, the NQ -1.0% is the morning’s laggard, though price action thus far has seen the ES give-up 4500 ahead of the 200-DMA at 4484.

Top European News

U.K. Covid Cases at Highest Level as Immunity Wanes, Study Finds

Erdogan Changes Turkey’s Electoral Laws to Bolster His Rule

BNP Allows Staff in Europe to Work From Home Half the Time

Infineon, STMicro Attractively Valued Despite Softer 2023: Citi

In FX, dollar fades fast following rapid rise to fresh 2022 high post-hawkish Fed Brainard and pre-FOMC minutes – DXY reaches 99.759 before retreat to sub 99.500. Swedish Krona outperforms after latest comments from Riksbank member Floden upping the ante for a near term repo rise, EUR/SEK capped below 10.3000. Franc lags as yield and policy divergence weigh and EUR/CHF cross rebounds in a fashion that suggests official intervention, USD/CHF tests 0.9350 and EUR/CHF close to 1.0200 vs sub-1.0150 at one stage. Euro and Pound take advantage of Buck pull back and some chart support to recoup losses, EUR/USD and Cable back on 1.0900 and 1.3100 handles after dip through 1.0895 Fib and 1.3050. Yen reverses more repatriation gains as BoJ maintains YCC, USD/JPY hovering beneath 124.05 peak.

In commodities, WTI and Brent are firmer, shrugging off the tepid tone and benefitting from geopolitical premia. amid ongoing sanction announcements/ discussions. However, the benchmarks are once again in relatively thin ranges of circa. USD 3.00/bbl at present. US Private Energy Inventory Data (bbls): Crude +1.08mln (exp. -2.1mln), Cushing +1.791mln, Gasoline -0.543mln (exp. +0.1mln), Distillate +0.593mln (exp. -0.8mln). Gas flows via Yamal-Europe pipeline resume eastward, according to Gascade data, according to Reuters; however, subsequently reported that such flows have stopped. Spot gold/silver are modestly firmer, benefitting from the general risk tone and as the USD takes a breather from recent advances.

Central Banks

ECB’s Wunsch said the inflation target is essentially met and expects the deposit rate to be raised to zero by year end. He said the ECB’s rate could rise to 1.5-2% in the longer term, but caveat that even within the ECB there has been no discussion about raising interest rates, according to Reuters.

ECB’s Panetta says they would not hesitate to tighten policy if supply shocks fed into domestic inflation, not seeking any de-anchoring of inflation expectations. Asking the ECB to bring down high inflation in the near-term would be extremely costly.

RBA’s Deputy Governor Bullock notes Australian labour market is tight, was seeing some response in wages, with unemployment at 4.0%. Expects some revision upward in inflation forecasts; are now seeing more underlying inflation pressures.

Riksbank’s Floden says inflation will be much higher in the coming year than predicted in February. We must raise the policy rate much earlier than previously planned. Evident we must reassess and substantial adj. monetary policy plans.

US Event Calendar

07:00: April MBA Mortgage Applications, prior -6.8%

14:00: March FOMC Meeting Minutes

Central Banks

09:30: Fed’s Harker Discusses the Economic Outlook

14:00: March FOMC Meeting Minutes

DB’s Henry Allen concludes the overnight wrap

DB Research have released a significant World Outlook document yesterday, in which we’ve updated our views on the global economy and financial markets given developments since the start of the year. In terms of the key takeaways, we’ve downgraded our growth forecasts, with an out-of-consensus view that a US recession is now the base case by the end of next year, since higher inflation will require a more aggressive tightening in monetary policy from central banks, and we now see the Fed moving much faster, with 50bp hikes at the next 3 meetings, and a terminal rate of 3.6% by mid-2023. The outlook has been further dampened by Russia’s invasion of Ukraine, which has pushed up energy prices and led to further disruption for key commodity markets and supply chains.

With the outlook moving in a more stagflationary direction, we expect growth to slow materially in the second half of 2023, tipping the US into recession by the end of that year. Indeed historically, there’s been just 2 occasions over the last 70 years when the Fed has raised rates by 300bps and left inflation on a downward trajectory without causing a recession. And as we’ve written many times in the EMR, the recent inversion of the 2s10s curve has on average preceded the start of a recession by around 18 months (see more in our recent chartbook here). Over in the Euro Area, we’re also forecasting a more aggressive tightening cycle, with the ECB raising rates by 250bps between this September and December 2023. But unlike in the US, we think Euro Area growth will be modestly above zero in the winter of 2023-24. Along with the updated call for US recession, Jim’s also expecting credit spreads to widen out by the end of next year. See the full credit update from him here.

Many of those themes we wrote about in the World Outlook were echoed in markets over the last 24 hours, with a massive bond selloff that was turbocharged by some hawkish rhetoric from Fed Governor Brainard (who’s also been nominated to become Vice Chair). Among the headlines, she said the FOMC would “continue tightening policy methodically” and would start reducing the balance sheet “at a rapid pace as soon as our May meeting.” Furthermore, she went on to say that she expected the balance sheet “to shrink considerably more rapidly than in the previous recovery, with significantly larger caps and a much shorter period to phase in the maximum caps compared with 2017-19.” Today’s FOMC minutes should give more detail about what QT may look like, which our US econ team and Tim from our team covered here. And there was also a comment that inflation was “subject to upside risks”. Brainard is typically perceived to be dovish, that the comments came from her left little doubt about the consensus of the entire committee voting bloc.

Those remarks saw market pricing shift to expect even more aggressive moves from the Fed over the rest of the year. In fact by yesterday’s close, futures were pricing in an 83% chance of a 50bps move at the next meeting in May, whilst the amount of tightening priced for 2022 as a whole hit its highest yet as well, with 220bps worth of further hikes on top of the 25bps from last month. If realised, that would be the largest amount of Fed tightening in a single calendar year since 1994, when they moved Fed funds up by 250bps, and remember that our economists’ latest forecasts now see the Fed matching that 250bps worth of hikes this year as well. Terminal rates are also repricing higher, with 1y1y OIS rates hitting their highest level this cycle at 3.17%, up from 1.11% at the start of the year.

These expectations of a more aggressive Fed led to a major selloff in Treasuries across maturities, with yields on 10yr Treasuries up by +15.2bps to 2.55% by the close, echoing the volatility in yields we saw at the start of last month as Russia’s invasion of Ukraine got underway, and marking the largest daily rise in the 10yr yield since the Covid-induced volatility in March 2020. That also marks the first time the 10yr yield has closed above 2.5% since May 2019, and the move went alongside a large rise in real yields (+9.7bps) as well, which at -0.31% put it at levels not seen since March 2020 as well. Another feature of yesterday was that the big rise in yields at the long end of the curve proved enough to un-invert the 2s10s curve, which ended the day in positive territory for the first time since last Wednesday, at 2.5bps. And this morning those moves have gained added momentum, with the 10yr Treasury up another +7.1bps to 2.62%, and the 10yr real yield up +5.8bps to -0.25%.

That selloff in Treasuries was echoed in Europe too yesterday, with yields on 10yr bunds (+10.8bps), OATs (+14.9bps), BTPs (+19.3bps) and gilts (+10.7bps) all seeing similarly big rises. From Europe, one interesting point to note is that the spread of French 10yr yields over bunds widened to 54bps yesterday, which is its widest level in almost 2 years. That came amidst a broader underperformance in French assets yesterday, with the CAC 40 index losing -1.28% as the tightening polls ahead of the first round this Sunday have led to increasing doubt as to whether President Macron will win another term in office. He’s still ahead in the polls for now, but the gap between himself and his main challenger Marine Le Pen has narrowed in Politico’s polling average from a peak of 30%-17% less than a month ago to just 27%-21% now. Furthermore, the second round average is at 54%-46%, which is also significantly tighter than Macron’s 66%-34% victory over Le Pen in 2017.

US equities were also affected by the more hawkish rhetoric from Governor Brainard, and the S&P 500 fell -1.26% as investors continued to price in higher interest rates. Cyclical sectors were among the worst performers, and technology stocks lost significant ground with the NASDAQ (-2.26%) and the FANG+ index (-3.28%) both undergoing serious declines. In Europe the situation was somewhat better, although the main indices there closed before the later decline in the US, meaning that the STOXX 600 still advanced +0.19%. As mentioned however, that masked serious regional divergences, with the FTSE 100 advancing +0.72%, whilst the Germany’s DAX (-0.65%) and France’s CAC 40 (-1.28%) both lost ground.

Staying on Europe, there were further developments on Russian sanctions yesterday, with the EU proposing a 5th package of measures that would include an import ban on Russian coal, among others. Commission President von der Leyen said that they were working on further sanctions “including on oil imports”, but there wasn’t yet a discussion about banning either oil or gas, with differing opinions among the member states on such a move.

That pattern of losses has been seen overnight in Asia as well, where equity markets are trading in negative territory amidst that continued rise in Treasury yields overnight. The Nikkei (-1.89%) is leading losses across the region with the Hang Seng (-1.69%) trading sharply lower as the index reopened after a holiday. Stocks in mainland China are also struggling with the Shanghai Composite (-0.29%) and CSI (-0.52%) both down after their own reopenings following holidays, which also comes as the Caixin services PMI dropped to 42.0, its lowest level since February 2020 and beneath the 49.7 reading expected by the consensus. Looking ahead, equity futures are pointing towards further losses today, with contracts on the S&P 500 (-0.04%) and the DAX (-0.41%) both falling.

Data releases took something of a back seat yesterday, but we did get the release of the final services and composite PMIs from around the world, with many European countries having upward revisions relative to the flash readings. For example, the Euro Area composite PMI came in at 54.9 (vs. flash 54.5), whilst the UK composite PMI came in at 60.9 vs. flash 59.7). The US was one of the few exceptions, where the composite PMI was revised down to 57.7 (vs. flash 58.5), and the ISM services index also came in modestly beneath expectations at 58.3 (vs. 58.5 expected), although that did mark a rebound following 3 consecutive months of declines.

To the day ahead now, and the release of the FOMC minutes from the March meeting will be one of the main highlights later. Otherwise, central bank speakers include ECB Vice President de Guindos, Chief Economist Lane, and Philadelphia Fed President Harker. Data releases include the UK and German construction PMIs for March, German factory orders for February, and Euro Area PPI for February.

Shanghai Residents Rebel As Cases Surge, Lockdown Extended ‘Indefinitely’

China’s NHC reiterated its commitment to its “dynamic” zero-tolerance policy on Wednesday as local authorities in Shanghai confirmed the worst fears of the financial hub’s approximately 26 million residents: what was initially introduced as a 9-day staggered lockdown has been extended “indefinitely” as the number of newly confirmed cases soared to a new record on Tuesday.

Authorities counted more than 13,000 new cases in Shanghai alone, more than half of the 20,000+ new cases across the entire country. According to Bloomberg, these tallies have surpassed the toll from the early days of the pandemic, when the virus was still raging in Wuhan.

To be sure, the surge in cases is partially a factor of the latest mass-testing regime, but that hasn’t stopped the CCP from imposing the most draconian lockdown since Wuhan (as we explained earlier, backing down would be an intolerable capitulation for President Xi and local authorities, whose careers are now in jeopardy due to factors that are completely out of their control).

Following an unceasing torrent of scandals, including separating COVID positive children from their parents, covering up nursing home deaths and failing to address shortages of food and medicine, the population of Shanghai has reached its breaking point.

Many have accused the CCP of violating its contract with the people. And in one particularly memorable scene, thousands of Shanghaiers took to their balconies to chant in protest, in defiance of the CCP’s lockdown strictures.

Depictions of the truly dystopian scene spread like wildfire on American social media…

Shanghai’s 25 million people under lockdown indefinitely. Chinese social media shows some breaking out of lockdown to protest, chanting: “we want freedom”; “why are you starving us?”

Much of the dissent is censored. Most of videos in our story were erased from the internet @cnnpic.twitter.com/QUHrfqEhiG

…as locals chanted from their balconies, government drones responded and warned them to retreat inside and not “open their windows” (apparently a violation of the lockdown rules).

As seen on Weibo: Shanghai residents go to their balconies to sing & protest lack of supplies. A drone appears: “Please comply w covid restrictions. Control your soul’s desire for freedom. Do not open the window or sing.” https://t.co/0ZTc8fznaVpic.twitter.com/pAnEGOlBIh

Unable to even walk their dogs, stories of locals allowing their dogs to poop and pee inside their apartments have spread like wildfire. Here’s more from Al Jazeera:

Now five days into the latest lockdown, Vicky, who prefers not to share her family name, has found herself doing something entirely unexpected: trying to convince a friend’s rescue dog, Mocha, that it is ok to go to the toilet inside her apartment.

“She is currently staring at me right now with sad puppy eyes like ‘why aren’t we going out?’ and I don’t know how to explain it to her,” Vicky told Al Jazeera by Skype. “So far, I have just tried to communicate to her that one, if you poop on the floor, I won’t be mad at you, and two, if you pee and bathroom it’s fine, I will just hose it down. It’s not a big deal.”

Shanghai reported 311 new symptomatic cases and more than 16,000 asymptomatic infections on April 5, the local government announced on Wednesday, with both measures higher than the day before. The lockdown was supposed to end yesterday, but has been extended indefinitely until authorities have had an opportunity to ‘review the data’, as China Daily reported.

As we reported yesterday, roughly 40,000 personnel (38K military and 2,000 ‘medics’) have been dispatched to the city. Many volunteers and medical workers get up early to prepare for the daily testing and other duties (while others stay up all night).

After facing a massive backlash over separating COVID positive children (some less than a year old) from their parents, local authorities have decided to abandon that policy, Reuters reports.

However, a new controversy has emerged as the government has reportedly started murdering the pets of COVID-positive individuals.

Here is some fun news.

1- China is separating Covid positive children from their parents

2- Murdering the pets of Covid positive patients in one city

Meanwhile, stories of sick Shanghaiers being denied medical care have stoked a panic among the locals, exacerbating existing fears about food shortages as millions are now being forced to rely on the government to deliver supplies.

The economic impact from the latest round of lockdowns can already be seen in the data: just last night, China’s Caixin Services PMI crashed to 42.0 in March from 50.2 in February, the largest single-month decline since February 2020.

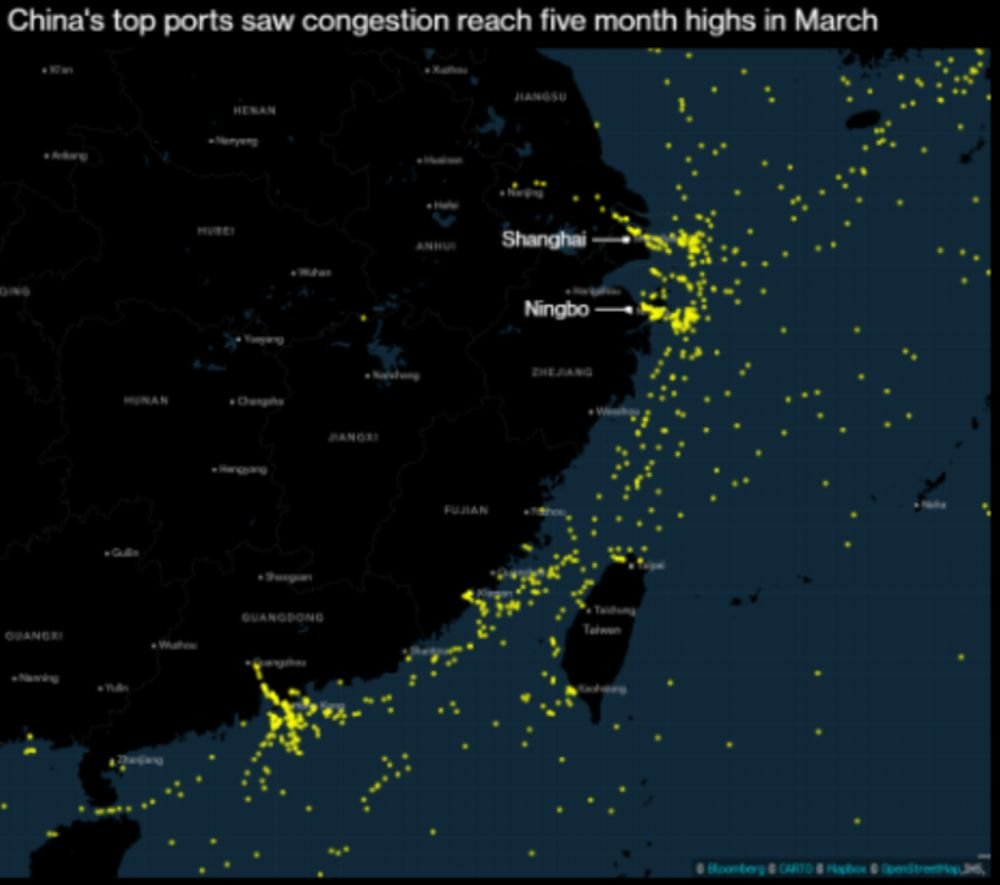

And although authorities have done everything in their power to keep ports open, congestion surged to its highest level in recent memory in March.

As social media has devolved from a free speech zone to a censorious minefield (my take) or a cesspool of misinformation from which people should be protected (according to people who are wrong) or just a shitty-algorithm-driven mess (probably true), the standard response to critics has been: build an alternative! A fair number of alternatives now exist, some more successful than others. But now tech billionaire Elon Musk puts forward a new approach: buy a stake in an existing platform and champion a culture of free speech. This may well be a boon for open discourse in the short term, but a permanent cure for intolerance requires more.

“Elon Musk took a 9.2% stake in Twitter Inc. to become the platform’s biggest shareholder, a week after hinting he might shake up the social media industry,” Bloomberg Newsreported on Monday. Musk also gained a seat on the company’s board of directors.

The “shake up” refers to hints Musk dropped about starting a new social media platform that would use open-source algorithms and have a stronger dedication to free speech than much-criticized mainstream platforms including Facebook, YouTube, and, especially, Twitter. Tellingly, though, Musk not only became Twitter’s largest shareholder, but before the Schedule13G disclosing the acquisition was revealed, he asked Twitter users whether they thought “Twitter rigorously adheres” to free speech. About 70 percent of self-selected respondents said “no.”

Among those endorsing Musk’s take on Twitter’s need for change is, apparently, Twitter founder Jack Dorsey, who retweeted a related poll about the importance of basing the social media platform on open-source algorithms. He stepped down as Twitter’s CEO last year and will leave the company’s board next month. Dorsey took flack during his tenure as CEO, but there were signs that he was a free speech advocate navigating conflicting demands from government, politicized staff, and mutually loathing factions in a divided society.

“The pressure comes from both above and below. You’ve got the United States Senate basically saying: ‘Nice little social network you got there. Real shame for anything to happen to it,'” tech entrepreneur David Stack told Bari Weiss last week. “From below, you’ve got the employees and the tweet mobs and basically forming these boycotts and subjecting the management of the company to pressure.”

Dorsey criticized his own company’s suppression of the since-verified Hunter Biden laptop story, long resisted his own employees’ calls to ban former President Donald Trump from the platform, and told Congress that neither tech companies nor government should be “arbiters of truth.” His departure was not a good sign for a service that once touted itself as “the free speech wing of the free speech party.”

“Anyone who harbors concerns that social media have already grown too intolerant of dissenting opinions—too inclined to silence viewpoints that depart from liberal orthodoxy—should be worried about Dorsey leaving,” Reason‘s Robby Soave wrote at the time.

Dorsey now regrets the centralization of the internet and champions Bluesky, a project intended to restore the ability for “people to freely interact and create content, without a single intermediary.” Platforms built on such a decentralized approach would lack kill switches or the ability to turn public panics into policy; users would exercise control over their own experiences.

But one problem that alternative platforms have faced aside from public pressure and commercial shunning is attracting users. While some half-assed attempts (coughParlercough) at building new social media platforms have made the existential mistake of relying on services provided by companies hostile to their missions, it is possible to build an independent platform that’s relatively self-contained.

“Over the past four years we have been banned from multiple cloud hosting providers and were told that if we didn’t like it we should ‘build our own,'” Gab, a Twitter competitor favored by the nationalist right announced in 2020. “So, that’s exactly what we did.”

Since then, Gab has expanded into video and now is working on an advertising service and payment systems. But, while successful, it caters to a niche community that shares its very particular worldview. That, I’m happy to say, is not all of us.

For many people hoping for a renewed “free speech wing” commitment at a larger platform shared by people of multiple points of view, Musk’s large stake in Twitter and his presence on its board comes as a promising sign. A self-proclaimed “free-speech absolutist” and critic of politicized environmental, social, and governance standards for investing and business management, Musk is already sending a message to the tech industry, to Twitter staffers, and to the censorious multitude, whatever his intentions.

“Will Musk now agitate for Twitter to alter its policy on moderating content in the name of freer speech?” The New York Timesspeculated on Monday. “Will he push for Twitter to open up its algorithm, which the company’s co-founder and former C.E.O. Jack Dorsey appeared to support last week? (Musk and Dorsey are friendly.)”

But the problem with any movement based around one person is that the whole movement is only as good as that person and shares his or her flaws and vulnerabilities. Musk is already at war with the Securities and Exchange Commission, which isn’t shy about weaponizing its power against opponents. His Twitter move could draw further regulatory attention and potentially hobble his efforts. Musk also faces accusations of retaliation against critics within his company and in the outside world. Whatever the truth of those claims, it’s easy to see that the clout he wields at Twitter might just as easily be wielded against free speech as in its favor.

For now, Elon Musk’s acquisition of a large stake in Twitter and a board seat allowing him to influence the social media company’s policies is a welcome temporary victory for free speech advocates. If nothing else, it’s a reminder to the self-righteous set that their dominance isn’t inevitable and that calls for tolerance of dissent are, once again, coming from inside their own institutions.

But the long-term solution for protecting free speech can’t lie in the hands of one person. We need alternatives that cater to different audiences and aren’t reliant on the good will of their critics. We should encourage decentralization that lets people control their own experience and eliminates the ability of any government or pressure group to muzzle those deemed unworthy. And, most importantly, we have to encourage a culture of free speech that values protections for dissent without regard for our agreement or disagreement with other people’s views.