US equity futures and global markets are lower this morning with bond yields and the USD flat as collapsing German eco data and elevated oil prices reignited stagflation concerns across the euro area. As of 7:45am, emini S&P and Nasdaq 100 futures were down 0.2%. The Bloomberg Dollar Spot Index edged higher along with the Japanese yen, while oil-linked currencies retreated as Brent crude dipped from 2023 highs; commodities are weaker with a sell-off in energy and metals complexes. Treasury yields were little changed in a lackluster day for bond markets. Gold fell for a second day, while Bitcoin climbed for the first time in three days.

In premarket trading, tech is underperforming; sentiment was dented by headlines that China’s government workers were told not to use iPhones. As a result, the world’s biggest company, AAPL, is trading -0.7% pre-mkt with MegaCap names all in the red; meanwhile keep an eye on the Huawei chip story. Yesterday’s Fedspeak was dovish, but we have three speakers today and four speakers tomorrow, so let’s see if the tone sharpens. Corporate mentions of ‘recession’ have fallen ~75% from their 22 Q2 peak and are now below their 5-yr average (62 vs. 82). Today’s macro data focus includes ISM Services, Beige Book, and Mortgage Applications (they dropped -2.9% after rising 2.3% last week).

The Stoxx 600 index retreated 0.7%, falling for the sixth straight session (see below) after German factory orders plummeted in July, showing that the woes of Europe’s biggest economy are continuing into the third quarter.

It also bears asking: with China and Europe imploding, just how much longer can the lie of US “economic growth” continue? Fears of stumbling growth and sticky inflation were also fanned by Brent crude prices holding just below $90 per barrel after the largest OPEC+ oil producers extended their supply cuts to year-end.

The collapsing economy in Europe and the ongoing economic collapse in China put pressure on equity futures in the US, if only for the moment, where signs are mounting that the Federal Reserve won’t cut interest rates any time soon. Because, you see, under the economic miracle of Bidenomics, the US can decouple from the rest of the world.

“The euro zone and UK are dabbling with recession, which markets had forgotten about three months ago,” said Rupert Thompson, chief economist at Kingswood Holdings. “It’s clear growth will head in the wrong direction in the coming months, which means equity markets will remain under downward pressure.”

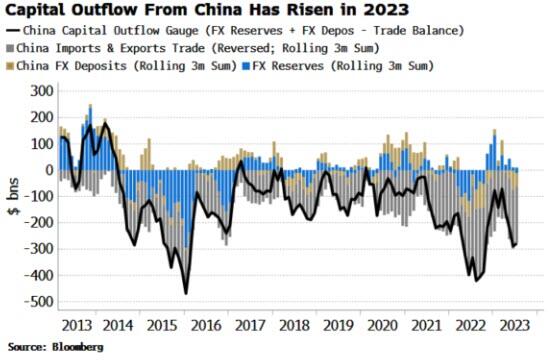

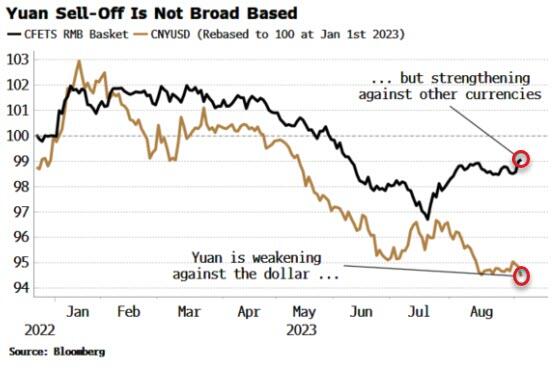

Meanwhile, the soaring dollar forced Japan, whose yen may as well be renamed to lira, issued its strongest warning in weeks against rapid declines in the yen on Wednesday, with its top currency official saying the nation is ready to take action amid speculative moves in the market. The yen plumbed a 10-month low against the greenback. Shortly after, China’s central bank offered the most forceful guidance on record with its daily reference rate for the yuan, as the managed currency weakened toward a level unseen since 2007.

Going back to equity markets, European bourses are lower in a rather muted session, with the Stoxx 50 down 0.6% as stocks react to recent cross-asset moves. Banks are the main underperformers while other cyclical sectors such as miners and energy give up early strength. Real estate continues to trade well as the peak rate narrative in Europe continues to get traction (despite a slew of European Central Bank officials’ warning: don’t assume no action at next week’s meeting). The retrace higher in yields continues to get attention given the implications for equity valuations along with USD strength while the gap higher in oil risks fuelling a resurgence in global inflation. The UBS desk has been 60:40 better to buy on hedge fund demand in energy and semis while it has been a better seller of staples and telcos. It has also been active two-way in software with long-only buying and hedge-fund selling. Telcos are in focus following news of a stake build in Spain Telefonica. Here are the notable European movers:

- InPost gains as much as 11% as company reported 2Q earnings that beat expectations thanks to rising parcel volume, higher pricing in Poland and reduction of losses in UK

- Swiss Life rises as much as 3.1% after the life insurer reported 1H earnings analysts describe as “mixed,” praising the share buyback program but noting subdued real estate numbers

- Telefonica jumps as much as 3.7% after the government-backed Saudi Telecom Co. invested about $2.25b to snap up a nearly 10% stake in the Spanish telecommunications operator

- Halfords gains as much as 4.3% after the car parts and bicycle retailer reported revenue growth for the 20-week period to Aug. 18. A solid update with strong performance strong overall, Liberum says

- Clas Ohlson gains as much as 11.5% after the Swedish retail group reported better-than-expected first-quarter earnings, with Kepler Cheuvreux lauding the firm’s cost control and strong margins

- Bridgepoint rises as much as 3.3% after it announced a deal to add Energy Capital Partners which Morgan Stanley says is strategically consistent with previously identified aim to diversify capabilities

- European renewable-energy stocks fall, with an index tracking the sector hitting a three-year low, as sentiment further soured as Barclays initiated Vestas with an underweight rating

- Darktrace drops as much as 9.3% before paring losses after the UK cybersecurity company reported results that Jefferies analysts say show “strong underlying progress, but not without debate”

- Idorsia falls as much as 9.5% after the Swiss drug developer repurchased the rights for aprocitentan from Janssen Biotech, Jefferies says the deal removes some hopes Janssen would acquire the firm

- WH Smith drops as much as 6% after the UK newsagent and bookstore provided an update which RBC said was in line with expectations overall. Investec lowered its above-consensus estimates.

Earlier in the session, Asian stocks were mixed as losses in Chinese equities amid caution on the impact of government stimulus countered gains in Japan on a forex boost. The MSCI Asia Pacific Index fluctuated in a narrow range, with Tencent and Samsung among the biggest drags while Toyota and Sony provided support. Hong Kong and mainland China indexes were among the region’s worst performers as investors continued to monitor Beijing’s measures to stem the economic slide. That said, Chinese property developers notched dramatic gains on speculation that further stimulus is forthcoming.

- The Hang Seng and Shanghai Comp suffered from tech weakness but losses stemmed as developers surged on hopes of further support measures and with Sunac up by over 60% after its return to the Stock Connect; additionally, further support came via China’s Premier Li and reports of a Hong Kong Financial task force meeting.

- “The big trend for investors is to reduce exposure to Chinese equities, so every time there is some government measures to boost the market, people will sell into it,” said Vey-Sern Ling, managing director at Union Bancaire Privee. “That will be the case until we start to see positive impact from the measures, like better macro numbers and better housing sales.”

- Japan’s Nikkei 225 bucked the trend after it reclaimed the 33,000 status and with tailwinds from a weaker currency.

- Australia’s ASX 200 was dragged lower by tech and with most sectors pressured aside from energy which benefitted from the higher oil prices, while better-than-expected GDP data for Australia failed to inspire a turnaround.

- Key stock gauges in India extended their winning run to a fourth straight session, the longest such streak since mid-July, led by gains in consumer-focused companies and index major HDFC Bank. The S&P BSE Sensex rose 0.2% to 65,880.52 in Mumbai, while the NSE Nifty 50 Index advanced by a similar magnitude. The MSCI Asia Pacific Index was up 0.1% for the day. A gauge of consumer-focused companies on NSE climbed 0.8% on optimism for strong demand in the upcoming festive period in the country.

In FX, the US economy’s perplexing resilience has boosted the dollar, with conviction growing that the European Central Bank will hold off raising interest rates at its meeting next week. The Bloomberg Dollar Spot Index rises 0.1%, adding to Wednesday’s gain, and near a 5-1/2-month high against a basket of developed-market currencies after a run of seven weekly gains. The yen is off its best levels, having earlier benefited from some modest jawboning by the Japanese government. The euro got a brief boost from comments by ECB rate-setter Klaas Knot, who said markets may be underestimating the chances of a September interest-rate hike. “Our long-term view is that the dollar is overvalued, but for now cyclical pressures are in the other direction, so the pressure is for the dollar to strengthen,” said Thompson, who expects the ECB to hold rates steady next week.

In rates, treasuries held small gains as the US trading day begins, trimming yields from the highest levels in a week reached amid Tuesday’s corporate new-issue explosion and crude oil price jumping to YTD highs. Yields are lower across the curve by 1bp-2bp, 10-year around 4.25%, down from session high near 4.27%. Yields climbed 8bp-9bp Tuesday as 20 corporate borrowers raised a combined $36.2b, the most in a day since April 2020, reinforcing the reputation of the first trading day after US Labor Day as magnet for IG issuers; Nippon Life Insurance Co. has announced a benchmark-sized offering for Wednesday’s session. Focal points of US session include ISM services gauge at 10am New York time and comments by Boston Fed’s Collins at 8:30am.

In commodities, crude futures decline, with WTI falling 0.7% to trade near $86.10. Spot gold falls 0.1%. Goldman Sachs warned of upside risks to its end-year Brent target of $86 per barrel and UBS Global Wealth Management forecast Brent and US WTI benchmark to end the year at $95 and $91 per barrel, respectively.

Looking to the day ahead now, and data releases include German factory orders for July, Euro Area retail sales for July, and the August construction PMIs from Germany and the UK. Over in the US, we’ll also get the ISM services index for August, the final services and composite PMIs for August, and the July trade balance. From central banks, the Bank of Canada will announce their latest policy decision, the Federal Reserve will release their Beige Book, and we’ll hear remarks from BoE Governor Bailey and the Fed’s Collins and Logan.

Market Snapshot

- S&P 500 futures down 0.2% to 4,492.00

- MXAP little changed at 162.86

- MXAPJ down 0.4% to 507.38

- Nikkei up 0.6% to 33,241.02

- Topix up 0.6% to 2,392.53

- Hang Seng Index little changed at 18,449.98

- Shanghai Composite up 0.1% to 3,158.08

- Sensex down 0.4% to 65,549.72

- Australia S&P/ASX 200 down 0.8% to 7,257.05

- Kospi down 0.7% to 2,563.34

- STOXX Europe 600 down 0.7% to 453.51

- German 10Y yield little changed at 2.63%

- Euro up 0.1% to $1.0733

- Brent Futures down 0.8% to $89.36/bbl

- Gold spot down 0.1% to $1,923.72

- U.S. Dollar Index little changed at 104.74

Top Overnight News

- China ordered officials at central government agencies not to use Apple’s iPhones and other foreign-branded devices for work or bring them into the office, people familiar with the matter said. The move by Beijing could have a chilling effect for foreign brands in China. Apple dominates the high-end smartphone market in the country and counts China as one of its biggest markets, relying on it for about 19% of its overall revenue. WSJ

- The White House is seeking detailed information on Huawei’s latest flagship smartphone, which analysts have described as an important milestone for the Chinese tech group four years after US restrictions crippled its handset business. FT

- Speculative bets that Chinese authorities will widen support for its property sector sent some of the country’s ailing developers surging by the most on record. Heavily indebted developers with depressed valuations were among those to rally the most, with Sunac China Holdings Ltd. soaring 68% alongside a spike in trading volume. China Evergrande Group closed up 83% — capping the biggest gain since its 2009 listing. BBG

- Xi was “reprimanded” over China’s current direction by retired party elders at a recent retreat, with a warning that the country can’t survive further turmoil. Nikkei

- Taiwan’s CPI for Aug overshoots the Street at +2.52% (up from +1.88% in Jul and ahead of the consensus +2.1% forecast), although the core number eases to +2.56% (down from +2.73% in July). BBG

- Universal Music has struck a deal to reshape the economics of music streaming, with changes aimed at directing more money to professional musicians and away from a “sea of noise” that chief executive Lucian Grainge has criticized this year. The world’s largest record company and the French streaming service Deezer have agreed an arrangement they expect will lift payouts to professional artists by 10 per cent, in the first big shift in the music streaming business model since the launch of Spotify in 2008. FT

- ECB officials warn markets that next week’s meeting outcome hasn’t been decided. ECB’s Knot warns markets not to underestimate the risk of a rate hike at next week’s meeting. RTRS / BBG

- Investors are warning hedge funds that they will face redemptions and further pressure to cut their fees unless they can improve their performance, highlighting the strain placed on the industry by a dramatic rise in global borrowing costs. FT

- Enbridge agreed to buy three utilities from Dominion Energy in a $9.4 billion deal to create North America’s largest natural gas provider. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly in the red following the subdued handover from Wall Street where sentiment was clouded by the higher yield environment, a stronger dollar and rising oil prices. ASX 200 was dragged lower by tech and with most sectors pressured aside from energy which benefitted from the higher oil prices, while better-than-expected GDP data for Australia failed to inspire a turnaround. Nikkei 225 bucked the trend after it reclaimed the 33,000 status and with tailwinds from a weaker currency. Hang Seng and Shanghai Comp suffered from tech weakness but losses stemmed as developers surged on hopes of further support measures and with Sunac up by over 60% after its return to the Stock Connect; additionally, further support came via China’s Premier Li and reports of a Hong Kong Financial task force meeting.

Top Asian News

- China’s Premier Li says they expect to achieve around the 5% economic growth target which was set earlier in the year.

- Chinese diplomat Liu said the US and China are major trading partners and that China opposes decoupling.

- US Commerce Secretary Raimondo said she does not expect any changes to Trump-era tariffs on China until the ongoing USTR review is completed, according to a CNBC interview.

- BoJ Board Member Takata said Japan’s economy is recovering moderately and Japan is seeing early signs of achieving 2% inflation, while he added that there is a sign of change in Japan’s trend inflation as rising wages push up inflation expectations. However, he believes the BoJ must patiently maintain easy policy given very high uncertainty on the outlook and noted that inflation is already exceeding the BoJ’s 2% target but there is some distance to achieving it stably and in a sustainable fashion.

- Japan Chief Cabinet Secretary Matsuno says it is important for FX to move stably reflecting fundamentals, sharp FX movers are undesirable. Will respond appropriately to FX moves if necessary, without ruling out any option.

European bourses are in the red, Euro Stoxx 50 -0.5%, in a similar fashion to the subdued APAC handover though performance for both regions lifted off lows towards the China close. Pressure in Europe also emanated from soft German data, though this comes with mitigating factors, and hawkish commentary from ECB’s Knot. Sectors are similarly lower aside from Telecom, where support stems from reports that Saudi’s STC has amassed a near-10% stake in Telefonica. Stateside, futures are also under pressure, ES -0.3%, but to a slightly lesser extent than the above action as the region is more tentative ahead of key US data and Central Bank speak. Apple (AAPL) iPhone and other foreign-branded devices have been banned in China for use by government officials at work, according to WSJ sources.

Top European News

- ECB’s Knot says markets may underestimate a September hike, via Bloomberg; the September decision will be a close call. A further hike is only a possibility and not a certainty. Advises caution against pessimism on the blocs economy. ECB inflation outlook won’t differ much from the last quarter.

- German Chancellor Scholz says to the Bundestag that he wants to propose a German pact to make the nation more fast, modern and secure. Will continue to promote the establishment of innovative firms such as chip factories. Rules out a debt-financed stimulus programme for Germany.

- Germany’s IFW sees 2023 German GDP -0.5% vs. prev. view of -0.3%, 2024 at +1.3% vs. prev. view +1.8% and 2025 at +1.5%.

FX

- DXY dips, but retains a firm underlying bid within 104.590-870 range irrespective of intervention.

- Yen pares losses vs. Buck after Japanese jawboning, but USD/JPY fails to breach 147.00 having peaked around 147.81.

- Euro underpinned against Buck as EGB/UST spreads converge, but EUR/USD capped ahead of 1.0750 and top of 2.53 bn expiry band starting at 1.0740.

- Aussie elevated near 0.6400 vs Greenback as Yuan rebounds from overnight lows sub-7.3200 in response to onshore and offshore intervention.

- Loonie lags pre-BoC as oil comes off the boil and Usd/Cad straddles 1.3650.

- PBoC set USD/CNY mid-point at 7.1969 vs exp. 7.3097 (prev. 7.1783)

- China’s major state-owned banks were seen withdrawing yuan liquidity in the offshore FX market and were seen selling dollars in the onshore spot FX market, according to sources cited by Reuters.

Fixed Income

- Bonds off worst levels in Europe before solid UK and German auctions, but Bunds and Gilts remain below par between 130.48-131.16 and 93.36-70 respective parameters.

- T-note idling within tight 110-05/109-29 band awaiting US trade data, services ISM, Fed speakers and latest Beige Book.

Commodities

- A session of consolidation for crude after Tuesday’s Russia and Saudi induced gains; WTI Oct’23 and Brent Nov’23 are lower by around USD 0.70/bbl having slipped through and tested the USD 86.00/bbl and USD 89.00/bbl figures respectively.

- Gas markets are attentive to the commencement of Australian LNG strikes on Thursday.

- While metals feature near unchanged performance for spot gold, base metals are softer but in a similar fashion to Chinese bourses that have lifted off lows.

- US Congress is set to sell off a 1mln bbl emergency reserve of gasoline which was created in the aftermath of Hurricane Sandy amid questions about the reserve’s usefulness, according to Bloomberg.

- Russian President Putin spoke by phone to Saudi Crown Prince MBS, according to Ria; both praised high-level of OPEC+ coordination.

Geopolitics

- India’s Foreign Minister said he doesn’t think the absence of Russian President Putin and Chinese President Xi from G20 has anything to do with India. Furthermore, he stated that G20 countries are negotiating to arrive at a consensus and have a declaration but added that there is a very sharp North-South divide and a sharper East-West polarisation.

US event Calendar

- 07:00: Sept. MBA Mortgage Applications -2.9%, prior 2.3%

- 08:30: July Trade Balance, est. -$68b, prior -$65.5b

- 09:45: Aug. S&P Global US Composite PMI, est. 50.4, prior 50.4

- 09:45: Aug. S&P Global US Services PMI, est. 51.0, prior 51.0

- 10:00: Aug. ISM Services Index, est. 52.5, prior 52.7

- 14:00: Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

There has been little back-to-school optimism in markets over the last 24 hours, with a decent selloff for equities and bonds as the US returned from holiday. There were several factors driving the moves, but a highlight was another rise in oil prices that saw Brent crude (+1.17%) surpass the $90/bbl mark for the first time since November. That followed an announcement from Saudi Arabia that they’d be extending their unilateral production cut of 1 million barrels per day until December, as well as one from Russia that they’d be extending their own cutback of 300k barrels per day over the same period. Russia’s move was in line with earlier comments, and actually a partial reversal of the 500k cut seen in August, but the length of the extension by Saudi Arabia was a surprise, as during the summer it had extended its production cut for one month at a time. So this added to the tight oil supply outlook (though oil prices did reverse by 1% from their intra-day peak as Europe closed).

This run-up in oil prices continues a trend that’s been going since the end of June, back when Brent was still only at $72/bbl. At the lows in June, Oil was c.-45% YoY. Now it’s nearly flat, down about -3% YoY as I type. The move has already had a clear impact on gasoline/petrol prices, and is expected to lead to some hot CPI reports in August, so the risk is that this further run-up will only add to those pressures in the September/October numbers. This could pose a tricky dilemma at a time when several growth indicators are already turning lower, particularly in Europe, since central bankers will have to decide whether to focus on above-target inflation, or whether they should ease up on rate hikes given the downturn in growth. It’s true that this won’t directly show up in core inflation since it’s energy, but the risk is you ultimately get second-round effects in other categories. In addition, since central banks’ targets are still measured in headline terms, it’s going to be harder for them to pivot in a dovish direction the longer inflation stays above target.

Another factor that has likely added to the recent bond sell off has been the anticipation of unusually high corporate bond issuance, with over $36bn of debt coming to market in the US as it returned from the Labor Day weekend. The $120bn of dollar IG issuance expected this month is just a shade over the median September issuance in recent years, but we’ve gotten off to a flyer with perhaps some strong front-loading given corporate blackouts and the FOMC meeting later in the month. The pressure on US Treasury yields then comes as investors hedge the interest rate risk.

Coupled with the negative news on inflation, this drove a sell off across the curve. 10yr Treasury yields were up +8.3bps by the close to 4.26%, which builds on their +7.1bps move on Friday after the jobs report. This is the largest 2-session increase since early July. In the meantime, real yields were back near their highs for this cycle, with the 10yr real yield up +3.9bps to 1.96%, which is just shy of its post-GFC closing high of 1.98% on August 21. And with real yields climbing further, that helped the US Dollar Index (+0.55%) to close at its highest level since March, at the time of SVB’s collapse. As we’ll see in the Asia section below we are seeing the FX intervention noise increase again.

Over in Europe it was much the same story, with yields on 10yr bunds (+3.3bps), OATs (+3.8bps) and BTPs (+5.1bps) all rising on the day. As well as the oil news, in Europe we also had the ECB’s latest Consumer Expectations Survey for July. That showed 3yr median inflation expectations ticking up a tenth to 2.4%, whilst 1yr expectations remained at 3.4%. So still above the ECB’s 2% target, and a change from the declining expectations that we saw in June.

In several respects though, the bigger story in Europe came from the final PMIs yesterday, which showed an even weaker picture than the flash readings. For instance, the final composite PMI for the entire Euro Area came in at 46.7 (vs. flash 47.0), and the services PMI came in at 47.9 (vs. flash 48.3). So that’s more evidence for increasingly weak growth in Europe ahead of the ECB’s decision next week, and will only add to the fears of stagflation.

For equities, it was difficult to advance against this backdrop, and the S&P 500 (-0.42%) saw a moderate decline. This was a broad-based reversal, with 83% of the index down on the day. The S&P 500 equal weight index was -1.2%. The only real exceptions were energy stocks (+0.49%) and technology (+0.39%). Indeed, tech mega caps had a good day, with the FANG+ index up +1.10%. By contrast, small-cap stocks suffered, with the Russell 2000 (-2.10%) experiencing its worst daily performance in 4 months. Notably, the S&P 1500 homebuilding index, which had been up nearly 50% year-to-date, saw its worst day since October 2022 (-5.49%), partially on sensitivity to higher real rates. Meanwhile in Europe, the STOXX 600 (-0.23%) lost ground for a 5th day running, continuing its series of small losses.

Asian equity markets are broadly trading lower this morning but with no incremental sell-off versus the US close. As I glance through my screens, Chinese equities are the biggest underperformers with the Hang Seng (-0.82%) leading losses followed by the CSI (-0.71%) and the Shanghai Composite (-0.42%). Elsewhere, the KOSPI (-0.64%) is also slipping while the Nikkei (+0.68%) is vastly outperforming its regional peers, rising for the eighth consecutive day. S&P 500 (-0.12%) and NASDAQ 100 (-0.20%) futures are moving a little bit lower.

Early morning data showed that Australia’s economic growth slowed at an annual pace in the June quarter (+2.1%) compared to an upwardly revised +2.4% annual rate in the previous quarter (v/s +1.8% expected) as the impact of rising interest rates and a disappointing post-Covid recovery in China is taking its toll. On a quarterly basis, the Q2 GDP expanded +0.4%, matching market expectations and against a revised +0.4% in the previous three months.

In FX, the Japanese yen (+0.12%) slightly strengthened against the dollar to trade at 147.55 albeit still trading near a fresh 10-month low even after Japan issued its strongest warning over sharp currency moves. Top currency diplomat Masato Kanda stated that the government will monitor foreign exchange moves and will consider timely action if speculative moves persist. The Yuan fell to 10-month lows even with a strong fix by the authorities. Local bank selling of dollars after the lows has moved it back to -0.1% on the day.

There wasn’t much in the way of other data yesterday. We did get the Euro Area PPI reading for July, which showed producer prices were down -7.6% over the year to July as expected. That’s the biggest annual decline since July 2009 after the GFC. Otherwise, US factory orders fell by -2.1% in July (vs. -2.5% expected).

To the day ahead now, and data releases include German factory orders for July, Euro Area retail sales for July, and the August construction PMIs from Germany and the UK. Over in the US, we’ll also get the ISM services index for August, the final services and composite PMIs for August, and the July trade balance. From central banks, the Bank of Canada will announce their latest policy decision, the Federal Reserve will release their Beige Book, and we’ll hear remarks from BoE Governor Bailey and the Fed’s Collins and Logan.