Futs are lower following the S&P’s best weekly performance of the year (sparked by dovish comments by Fed chair Powell during the last FOMC) which sent the market up +2.3%. At 7:50am, S&P futures were 0.4% lower and Nasdaq futures dropped 0.6%, dragged by MegaCap tech names which were mostly lower with AMD and Intel down more than 2% after the FT reported they are being banned from Chinese government computers; NVDA swung from gains to losses after a report that Google, Intel and QCOM execs plan on battling NVDA on AI dominance (well what else can they do?). Meanwhile, JPM says to keep an eye on NFLX on bullish headlines; stock is +29% YTD which would be third among Mag7 names. Europe’s Stoxx Europe 600 dipped following nine straight weeks of gains, the longest run in 12 years. Elsewhere, treasury yields ticked higher and the Bloomberg dollar spot index was slightly lower with the yen a tad stronger after some aggressive jawboning by cartoonish Japanese officials. Oil gained on escalating geopolitical unrest following the Moscow concert hall attack on Friday that killed at least 137 people. The next 2 weeks have a lighter macro data calendar so keep an eye on Fedspeak (3x this week) and bond auctions for bond yield catalysts which could Equity sector performance. Month-end/Quarter-end rebalancing could also pressure stocks.

In premarket trading, Intel and AMD declined after a FT report said China was seeking to limit the use of US-made chips in government computers. United Airlines shares fell as US aviation authorities mull measures to curb growth at the carrier following a series of safety incidents. Here are some other premarket movers:

- Canopy Growth (CGC US) rose 13%, set to extend gains for a seventh consecutive session — its longest streak since January 2019.

- Walt Disney (DIS US) rose 1.3% after Barclays upgraded the media company to overweight from equal-weight, saying that a “narrative reset” since first-quarter results should be followed by positive estimate revisions.

As we enter a quiet week after multiple central bank shockers, traders are in wait-and-see mode ahead of economic data that will include the Fed’s preferred inflation gauge due Friday, when many markets will be closed for a holiday. While conviction has grown that the Fed will cut rates this year following dovish comments by Chair Jerome Powell last week, investors are becoming uneasy about stock valuations after the recent rally.

“When upward catalysts get rare and valuations are rich, risks become visible,” said Jeanne Asseraf-Bitton, head of research and strategy at BFT IM in Paris. “The coming weeks will be more complicated.”

European stocks slipped after a ninth straight week of gains for the index, the longest winning streak in nearly 12 years; the Stoxx slid 0.4% led by consumer product, retail and media shares which were the worst performers. Shares in European defense firms rose following a terrorist attack in Moscow on Friday evening that killed at least 137 people, in an assault claimed by the Islamic State. Dassault Aviation SA climbed 4.5% and Rheinmetall AG was up 3.6%. Swedish landlord SBB jumped after buying back a batch of bonds at a 60% discount, while Direct Line Insurance Group Plc plunged after Ageas said on Friday it won’t make a third takeover offer. Even after this year’s gains, European equity valuations are not yet over-stretched, according to Goldman Sachs Group Inc. strategists who forecast the Stoxx Europe 600 could still rise about 6% over the next 12 months. Here are some of the the biggest movers in Europe on Monday:

- European defense stocks including Rheinmetall and Leonardo gain after a terrorist attack in Moscow on Friday evening killed at least 137 people, in an assault claimed by the Islamic State.

- Zalando gains as much as 1.2% after Deutsche Bank raises its price target, citing the German online retailer’s balance of sales growth and margin expansion.

- Tullow Oil rises as much as 8.1% after BofA upgrades the UK energy firm to buy after it “reached an inflection point in its deleveraging journey.”

- Believe gains as much as 6.7% after the board invited Warner Music Group to submit a binding, unconditional and fully financed offer after its expression of interest.

- SBB soars as much as 17% after buying back hybrid securities and notes with a total aggregate principal amount of about €408 million, at a 60% discount.

- Inwido gains as much as 4.6% after Nordea reinitiated coverage of the Swedish window manufacturing group with a buy recommendation.

- Gamma Communications rises as much as 4.7% after it announced a new £35 million share buyback and delivered in-line annual earnings.

- Direct Line falls as much as 16% after Belgium’s Ageas said it will halt its pursuit of the insurer after two takeover proposals were rejected this year.

- Kingfisher shares drop as much as 4.6% after the retailer’s full-year sales missed expectations and its 2025 outlook also disappointed.

- Shelf Drilling and Borr Drilling both slide after DNB flagged the new “indirect risk” from Saudi Aramco scaling back its drilling.

Earlier in the session Asian stocks edged lower, dragged by selloffs in Japan and South Korea after last week’s strong rallies, while Chinese stocks advanced. The MSCI Asia Pacific Index dipped as much as 0.3%, erasing an early gain. Sony and Samsung were among the biggest drags, while China delivery firm Meituan gained after it reported better-than-expected earnings. Japanese equities declined as some investors took profit following the Nikkei 225 Stock Average’s ascent to a record high last week even as the central bank ended its negative-rate policy.

- Hang Seng and Shanghai Comp. were initially indecisive as participants digested recent earnings releases, although eventually strengthened after the slew of rhetoric from Chinese officials including Premier Li who noted relatively big room for macro policy.

- Nikkei 225 pulled back from record highs as investors booked profits amid some mild yen strength.

- ASX 200 finished higher with early outperformance in property and tech owing to softer yields.

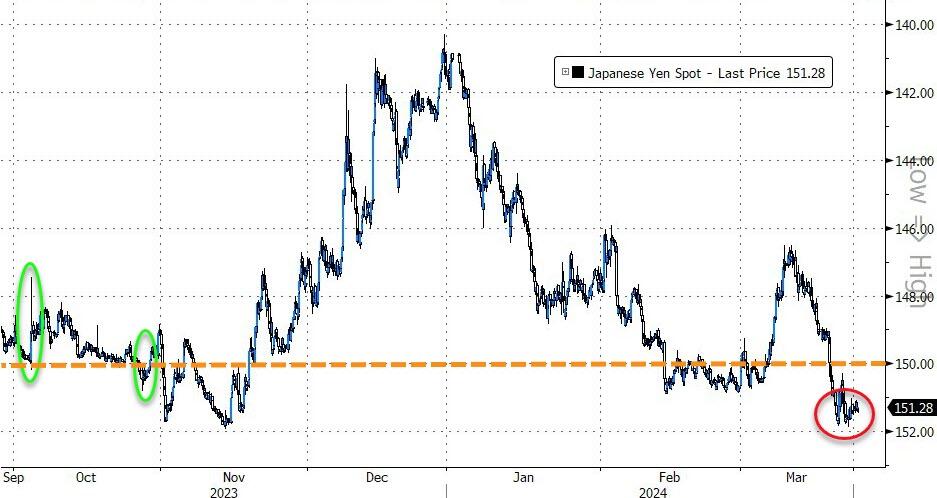

In FX, the Bloomberg Dollar Spot Index dropped 0.1%, while the yen strengthened after Japan’s top currency official warned about excessive currency speculation. The focus remains on China’s yuan after the central bank signaled its support for the managed currency. The onshore yuan rose as much as 0.5% to 7.1902 per dollar, the most since December

- USD/JPY fell as much as 0.2% to 151.05, after Japan’s top currency official warned against speculative moves in the yen

- USD/CNY fell as much as 0.5% to 7.19, after a stronger-than-expected daily fixing

- Risk-sensitive currencies including the Norwegian krone, New Zealand dollar and Australian dollar led Group-of-10 gains

In rates, treasuries were slightly cheaper across the curve following similar price action across core European rates, with rate futures near lows of the day. Treasury yields cheaper by 2bp to 3.5bp across the curve with losses led by belly, flattening 5s30s spread by 1.2bp on the day; 10-year yields around 4.23%, cheaper by 3bp with bunds and gilts marginally outperforming in the sector. The holiday-shortened week’s auction cycle begins with $66b 2-year note sale at 1pm; $67b 5-year and $43b 7-year follow Tuesday and Wednesday. WI 2-year yield at around 4.58% is ~11bp richer than February’s, which tailed the WI by 0.2bp

In commodities, oil gained on escalating geopolitical unrest following the Moscow concert hall attack on Friday that killed at least 137 people.

Bitcoin climbs higher and back on a USD 67k handle, whilst Ethereum sits just shy of USD 3.5k.

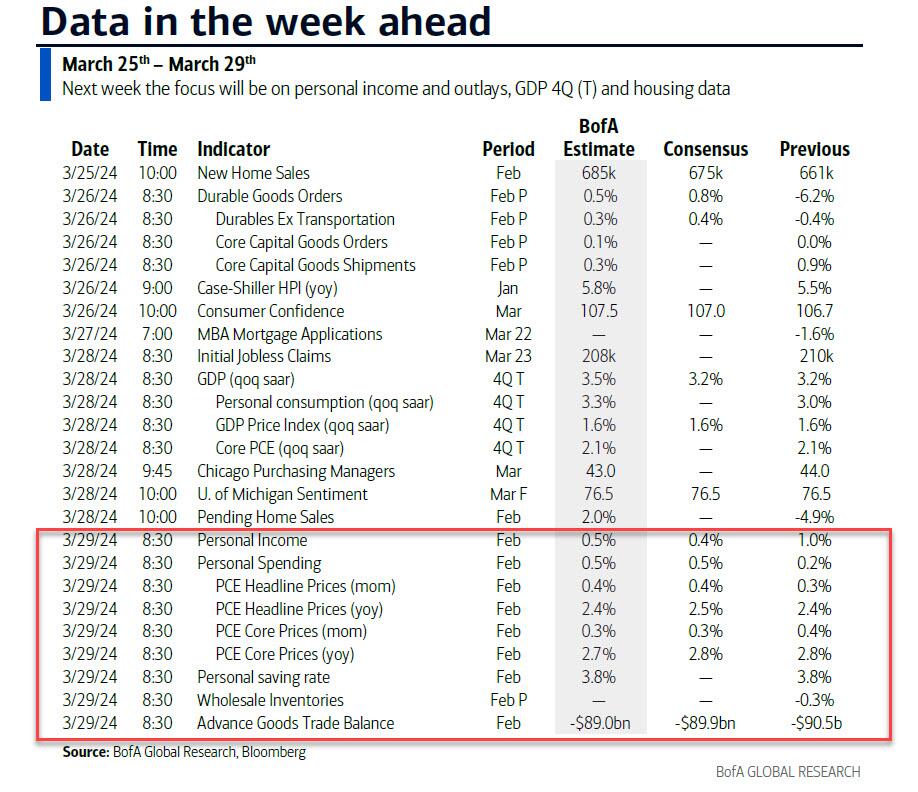

Looking at today’s calendar, the US economic data schedule includes February Chicago national activity index (8:30am), new home sales (10am) and March Dallas Fed manufacturing activity (10:30am). Later this week we get data on durable goods orders, consumer confidence, 4Q GDP revision, University of Michigan sentiment, and personal income/spending with PCE deflators. Fed speakers scheduled include Bostic (8:25am), Goolsbee (9:05am) and Cook (10:30am). Waller, Daly and Powell are slated to appear later this week

Market Snapshot

- S&P 500 futures little changed at 5,292.75

- STOXX Europe 600 little changed at 510.02

- MXAP down 0.5% to 176.50

- MXAPJ down 0.1% to 534.29

- Nikkei down 1.2% to 40,414.12

- Topix down 1.3% to 2,777.64

- Hang Seng Index down 0.2% to 16,473.64

- Shanghai Composite down 0.7% to 3,026.31

- Sensex up 0.3% to 72,831.94

- Australia S&P/ASX 200 up 0.5% to 7,811.94

- Kospi down 0.4% to 2,737.57

- German 10Y yield little changed at 2.32%

- Euro little changed at $1.0817

- Brent Futures up 0.4% to $85.74/bbl

- Gold spot up 0.1% to $2,166.70

- US Dollar Index little changed at 104.36

Top Overnight News

- Chinese Premier Li says the country has further room to broader policy support given subdued inflation and low levels of gov’t debt. BBG

- China has introduced new guidelines that will mean US microprocessors from Intel and AMD are phased out of government PCs and servers, as Beijing ramps up a campaign to replace foreign technology with homegrown solutions. As markets hit record highs, the ratio of corporate insider selling to insider buying is at the highest level since the first quarter of 2021, according to Verity LLC, which tracks insider trading disclosures. FT

- The US and Japan are planning the biggest upgrade to their security alliance since they signed a mutual defense treaty in 1960 in a move to counter China. President Biden and Prime Minister Kishida will announce plans to restructure the US military command in Japan to strengthen operational planning and exercises between the nations. They will unveil the plan when Biden hosts Kishida at the White House on April 10. FT

- The Islamic State claimed responsibility for the terror attack in Russia (and the US said it has no reason to doubt the authenticity of that claim), but Moscow/Putin suggested Ukraine could have some culpability. NYT

- The Russian oil-export machine funding the Kremlin’s war in Ukraine is finally getting some grit in its gears. Indian oil refiners — Moscow’s second-biggest customers after China since the 2022 invasion — will no longer accept tankers owned by state-run Sovcomflot PJSC because of the risk posed by sanctions. BBG

- Treasury issuance has expanded in recent years, sending the size of the US gov’t bond market to a record ~$27T (up ~70% since the end of ’19 and nearly 6x larger than before the ’08-’09 financial crisis). WSJ

- Peter Thiel, Jeff Bezos and Mark Zuckerberg are leading a parade of corporate insiders who have sold hundreds of millions of dollars of their companies’ shares this quarter, in a signal that recent stock market exuberance could be peaking. FT

- Atlanta Fed President Bostic now anticipates just one rate cut this year (his prior outlook was for two cuts), and forecasts it happening later than previously assumed. BBG

- United is said to face temporary FAA limits on adding routes and flying customers on newly delivered aircraft after safety issues. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed amid a lack of major macro drivers heading into month-end and a slew of data releases. ASX 200 finished higher with early outperformance in property and tech owing to softer yields. Nikkei 225 pulled back from record highs as investors booked profits amid some mild yen strength. Hang Seng and Shanghai Comp. were initially indecisive as participants digested recent earnings releases, although eventually strengthened after the slew of rhetoric from Chinese officials including Premier Li who noted relatively big room for macro policy.

Top Asian News

- Chinese Premier Li said China’s economic rebound momentum continues to consolidate and strengthen with economic development off to a good start judging by the first two months and though the economy sees some fluctuations, the long-term trend of the economy turning for the better won’t be changed. Premier Li said they will carefully study the issues of market access, match of supply and demand, as well as cross-border data flows, while there will be some regulations in some of these areas soon. Furthermore, Li said China will strive to boost domestic demand and that there is relatively big room for macro policy, according to Reuters.

- China’s Finance Minister said the government is confident and capable of achieving full-year economic and development goals, while China will prioritise support for sci-tech innovation and manufacturing development and allocate more fiscal resources to ensure employment, according to Reuters.

- China’s Industry Minister said they will accelerate new industrialisation, promote continuous optimisation and upgrading of industrial supply chains, while they will accelerate the modernisation of the industrial system, fully abolish restrictions on foreign investment access in the manufacturing sector, and deepen in-depth cooperation with enterprises from all countries.

- China NDRC head said the state planner will implement a batch of major sci-tech projects based on the development of new productive forces, while it will crack down on monopolies and unfair competition activity, as well as publish a new version of a negative list for market access, according to Reuters.

- China’s Vice Commerce Minister said they will further expand high-level opening up to the outside world and create more market opportunities by opening up for development, while China will continue to tap and unleash the potential of domestic demand, providing more trade and investment opportunities.

- China’s Commerce Minister met with Micron’s (MU) president and said that they welcome the Co. to expand its footprint in the Chinese market and ramp up investment projects while firmly obeying China’s laws and regulations, while China’s Commerce Minister also met with the chairmen of AMD (AMD), Exxon (XOM) and Medtronic (MDT), according to Reuters.

- China blocked the use of Intel (INTC) and AMD (AMD) chips in government computers.

- US Treasury Secretary Yellen will travel to China in April, according to POLITICO.

- US Secretary of State Blinken said the US expresses deep concern over Hong Kong’s security law.

- BoJ January meeting minutes noted that members said the likelihood of reaching the price goal was gradually rising and members discussed the positive and side effects of the Bank’s unconventional monetary policy. Members also agreed that Japan’s economy had recovered moderately and shared the recognition that, although exports and production had been affected by the slowdown in the pace of recovery in overseas economies, they had been more or less flat.

- Japan’s top currency diplomat Kanda said they have been closely watching FX moves with a high sense of urgency and will take appropriate steps to respond to an excessive weakening of the yen without excluding any measures, while he added the current yen weakness does not reflect fundamentals and is due to speculation.

- China’s STCN reports that “there are market rumours that real estate-related documents will be issued soon, which will focus on two directions” (cont)

- Nissan (7201 JT) targets an additional 1mln units in sales by end-FY2026 vs FY2023; 30 new Models to be launched by FY26, of which 16 will be electrified; dividend and buyback to target total shareholder return of over 30%. Executive says the global EV market is not stopping but starting to plateau to more normal cadence of growth

European bourses, Stoxx600 (-0.2%) initially struggled to find direction, though succumbed to slight selling pressure as the session progressed. European sectors are mostly lower; Energy benefits from broader strength in the crude sector, whilst Kingfisher (-2.5%) weighs on Retail. US equity futures (ES -0.2%, NQ -0.3%, RTY U/C) are mostly but modestly lower, in-fitting with price action seen in Europe; AMD (-2.1%)/ Intel (-2.5%) suffer in the pre-market after China blocked the use of AMD/INTC chips in government computers. Modest pressure in Apple (AAPL), Alphabet (GOOG), and Meta (META) following the EU Commission announcing a digital-market probe into the names.

Top European News

- UK Chancellor Hunt said the Conservative Party will keep the triple lock for pension increases in its election manifesto, according to Reuters.

- BoE announced Q2 QT schedule on Friday in which it will sell short-dated Gilts across four auctions of GBP 800mln and will sell medium-dated Gilts across four auctions of GBP 750mln, while it will sell long-dated Gilts across three auctions of GBP 600mln with its total sales at GBP 8bln in Q2.

FX

- USD is a touch softer vs. peers but with price action in the FX space broadly contained as newsflow has proved to be non-incremental. Current high of 104.47 is just below Friday’s 104.49 peak.

- EUR is contained with catalysts currently lacking to inspire price action. EUR/USD holding above Friday’s 1.0801 low. June 25bps ECB cut price at ~87%.

- Jawboning from Kanda failed to see the JPY regain much ground vs. the USD with the pair not far off the 2023 high at 151.91 and 2022 high at 151.94.

- Antipodeans are both a touch firmer vs. the USD with not much in the way of pertinent newsflow. AUD/USD briefly pierced Friday’s low at 0.65101 but has stopped shy of testing last week’s low at 0.6503 which lies just ahead of the 0.65 mark.

- Yuan regaining some ground vs. USD with Chinese banks said to be selling dollars and a firmer fix from the PBoC. USD/CNH down as low as 7.2327 but yet to test Friday’s 7.2175 low.

- PBoC set USD/CNY mid-point at 7.0996 vs exp. 7.2267 (prev. 7.1004).

- Chinese major state-owned banks were seen selling dollars for yuan in the onshore FX market to stabilise the Chinese currency, according to sources cited by Reuters.

Fixed Income

- USTs are slightly softer ahead of a handful of speakers, New Home sales and then a 2yr sale which is potentially incrementally weighing on the fixed space; currently near lows around 110-22.

- A relatively contained start to the week for Bunds with the docket thin on the data front, though action could stem from a handful of ECB speakers later today. The calendar doesn’t pick up within Europe until Wednesday’s Flash HICP before the EZ number post-Easter; modest downside has been seen in Bunds, to a low of 132.84 thus far.

- Gilt price action mirrors EGBs, awaiting fresh fundamentals following the “dovish” shift by the BoE. BoE’s Mann (Hawk) will be closely watched to see if she has entirely abandoned her long-held call for further tightening; currently around 99.80.

Commodities

- Crude is firmer despite a lack of fresh fundamental headlines, albeit remains within overnight ranges; Brent May is back around USD 86.00/bbl.

- Weakness across precious metals as the stronger Dollar exerted pressure while Friday newsflow remains quiet; XAU dipped under yesterday’s low (2,166.45/oz) and trades within a current USD 2,162.64-2,186.13/oz range.

- Base metals are softer across the board following the risk aversion from Chinese markets overnight coupled with the recovery in the Greenback.

- Iraq Oil Ministry blamed foreign companies operating in Iraqi Kurdistan for a delay in the restart of crude exports from the region, while it added that OPEC and secondary sources reports show crude production between 200k-225k bpd in the region without the knowledge or approval of the ministry, according to Reuters.

- Russia’s Kuibyshev oil refinery halts primary unit CDU-5 (70k bpd) after weekend drone attack, via Reuters citing sources.

Geopolitics: Middle East

- A leading Hamas source said Israeli media leaks about concessions and compromises offered to Hamas are miserable propaganda aiming to cover up its intransigence and evade responsibility for obstructing the agreement in front of the families of its prisoners, according to Al Jazeera.

- US Vice President Harris said an Israeli assault on Rafah ‘would be a huge mistake’ and she did not rule out ‘consequences’ if Israel invades Rafah, according to an interview with ABC News.

- UN Secretary-General Guterres visited Rafah and said it is time for an immediate humanitarian ceasefire, while he added there is a clear international consensus that any ground intervention in Rafah will cause a humanitarian catastrophe.

- UKMTO said a vessel was struck by an unidentified projectile 23NM west of Yemen’s Mukha and the resulting fire was extinguished by the crew, while the crew were reported safe.

- “Israel Broadcasting Corporation: Truce negotiations have reached an impasse due to Hamas’ demands”, according to Al Arabiya.

Geopolitics: Moscow Terror Attack

- The death toll from the Moscow concert hall attack on Friday was at least 137, while Russian President Putin declared a day of mourning on Sunday and said all attackers have been found and detained, according to Reuters.

- Russia’s FSB said the perpetrators of the Moscow attack were heading towards the Russia-Ukraine border and had contacts on the – Ukrainian side, according to IFAX. There were also comments from Russian lawmaker Kartapolov who said there should be a clear answer on the battlefield if Ukraine is found to be behind the Moscow attack, according to RIA.

- Ukrainian President Zelensky said Russian President Putin and others seek to divert blame for the Moscow concert massacre and that Putin could use the terrorists he sent to their deaths in Ukraine to stop terrorism in Russia.

- US National Security Council spokesperson said the US government shared information with Russia earlier this month about a planned attack on Moscow, while the spokesperson added that Ukraine has no involvement in the attack on Russia and Islamic State bears sole responsibility for the attack. It was also reported that Islamic State released footage of the attack on the concert hall.

- France raised its security alert after the attack on Moscow, according to reports citing the French PM.

Geopolitics: Other

- Ukraine’s military said it hit two Russian large landing ships, as well as a communications centre and infrastructure used by Russia’s Black Sea fleet during strikes on Crimea.

- Russia violated Poland’s airspace with a cruise missile attack on western Ukraine, while it was later reported that Russia’s air strike hit a Ukrainian facility in the western Lviv region and took control of the village of Krasnoye in the Donetsk region, according to IFAX.

- Russia scrambled a MiG-31 jet after US bombers approached near the Russian border over the Barents Sea, according to RIA.

- Gunmen reportedly stormed a police station in the Armenian capital of Yerevan, according to TASS.

- China’s coastguard used water cannons against Philippine ships in the South China Sea, while China’s Defence Ministry warned the Philippines against provocative actions and to stop infringing and making any remarks that may lead to the intensification of conflicts and escalation of the situation. Furthermore, the Defence Ministry said China will continue to take decisive measures to firmly safeguard its territorial sovereignty and maritime rights and interests if the Philippines repeatedly challenges China’s bottom lines.

- Philippines’ Foreign Ministry summoned the Chinese Embassy’s Charge D’Affaires and protested against aggressive actions by China’s Coast Guard and maritime militia against rotation and resupply mission over the weekend, while it added that China has no right to be in Second Thomas Shoal and demanded that Chinese vessels leave the vicinity of Second Thomas Shoal and the Philippine Exclusive Economic Zone immediately.

- US State Department said the US stands with the Philippines and condemns dangerous actions by China in the South China Sea. This was after China said it took control measures on Philippine vessels that ‘intruded’ into the Second Thomas Shoal waters on March 23rd.

- US and Japan plan the biggest upgrade to security pact in more than 60 years, according to FT. It was also separately reported that the US military command in Japan will be revamped, while Japan’s Chief Cabinet Secretary Hayashi said they are discussing ways to strengthen military cooperation with the US amid a move to a joint command structure in Japan but nothing decided yet.

- North Korean leader Kim visited a tank unit and called for airtight combat readiness. It was also reported that North Korean leader Kim’s sister said bilateral relations depend on Japan’s political decision and that Japanese PM Kishida showed intention to meet with North Korea’s leader recently, according to KCNA.

US Event Calendar

- 08:30: Feb. Chicago Fed Nat Activity Index, est. -0.34, prior -0.30

- 09:00: Bloomberg March United States Economic Survey

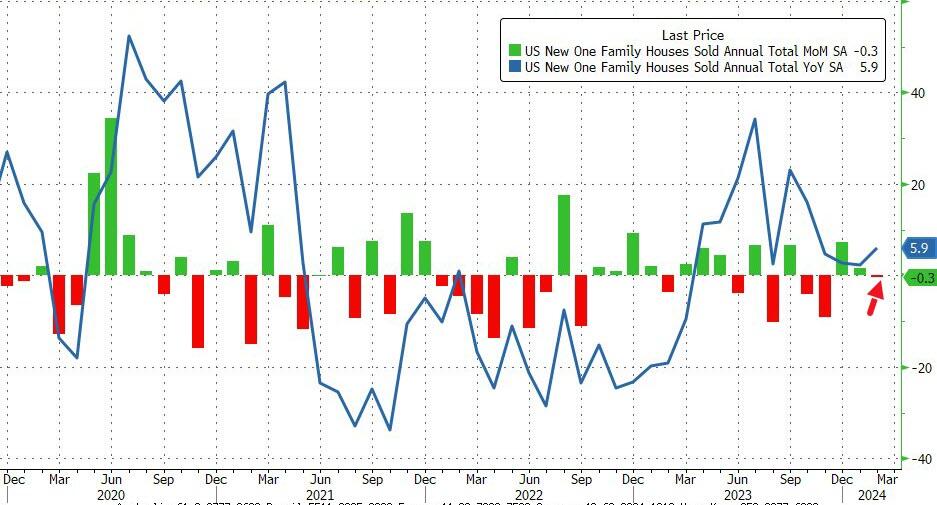

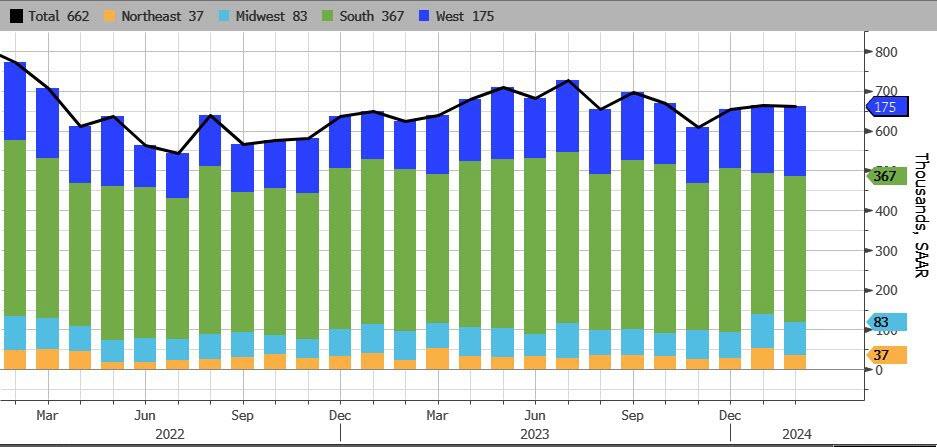

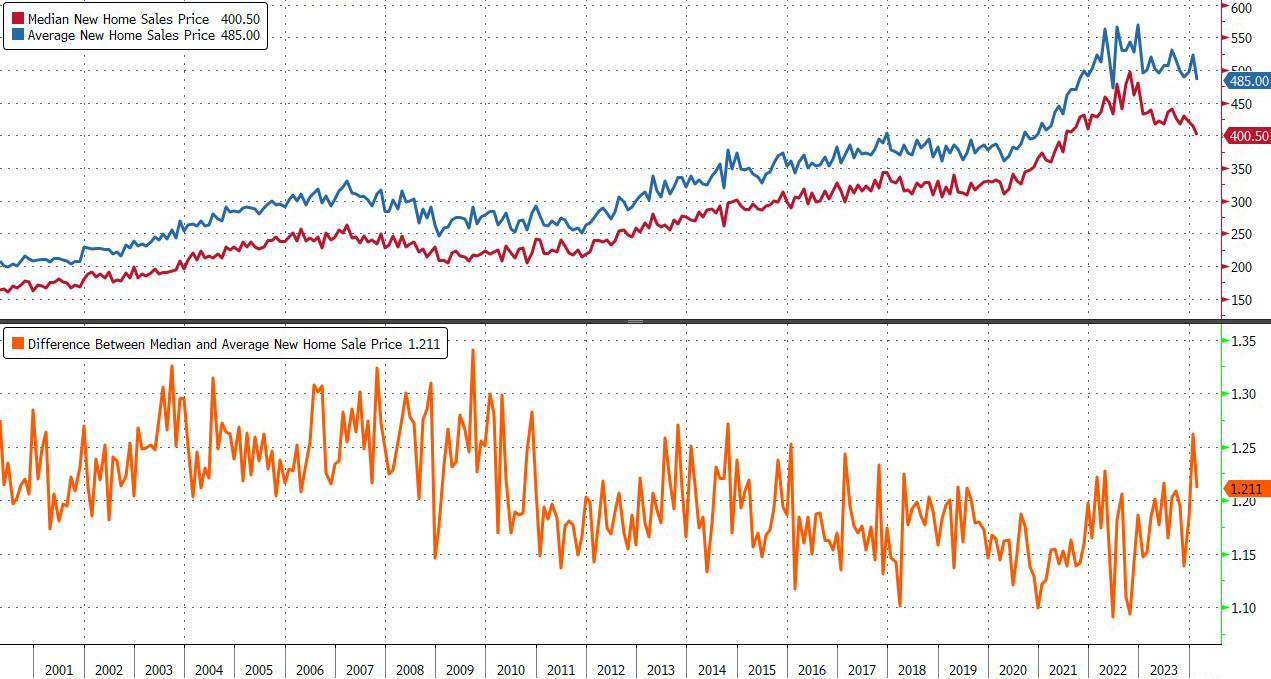

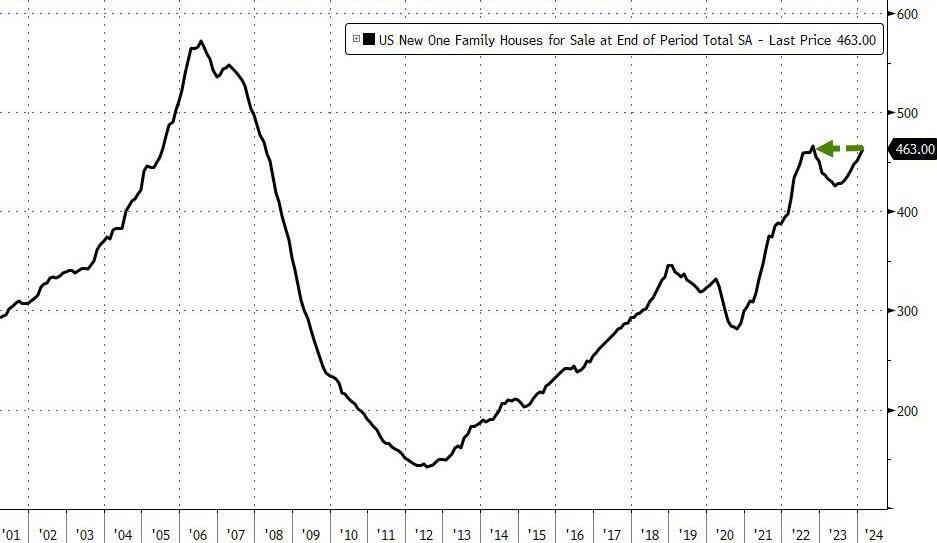

- 10:00: Feb. New Home Sales MoM, est. 2.1%, prior 1.5%

- 10:00: Feb. New Home Sales, est. 675,000, prior 661,000

- 10:30: March Dallas Fed Manf. Activity, est. -11.5, prior -11.3

Central Banks

- 08:25: Fed’s Bostic Participates in Moderated Conversation

- 09:05: Fed’s Goolsbee Appears on Yahoo Finance

- 10:30: Fed’s Cook Speaks on Dual Mandate

DB’s Jim Reid concludes the overnight wrap

This morning we’ll publish the results of our latest Global Financial Market Survey. One of the most interesting implied threads running through it is that a “no landing” edges out “soft landing” as the most likely path for the US economy by YE 2024 with “hard landing” now a distant third. However, why aren’t markets more concerned about a “no landing” at the moment? One possibility is that respondents seem happy for central banks to tolerate an extended period of above-target inflation while macro volatility is high. They feel comfortable with this perhaps due to the fact that their 5yr inflation expectations continue to edge down. So you could say a Goldilocks “no landing” for now with the economy running hot but with central banks not leaning against it! Whether that proves too optimistic time will tell but as you’ll see at the end, US equities had their best week of the year last week largely because the FOMC seems very confident of their ability to cut rates in June even with recent hot inflation prints.

On a very related theme, the most exciting event of the week happens once markets are actually closed for the month and Q1 is done and dusted in performance terms. Strangely, the monthly US personal income and spending report, which contains the crucial core PCE, is released on Good Friday when bond and equity markets are closed. The flash CPIs in Italy and France also come out on Friday, with the Spanish print due on Wednesday. Staying on the inflation theme, Tokyo CPI is out on Thursday, with the summary of opinions from last week’s BoJ meeting on Wednesday. This will garner some attention given the once-in-a-generation shift in policy. Australian CPI is out on Wednesday.

Staying with central banks, there are lots of Fed speakers this week that can add some colour to last week’s generally dovish FOMC. They are listed in the day-by-day week ahead at the end. In terms of the key US data, today sees new home sales, tomorrow sees durable goods and consumer confidence, Wednesday the final consumer sentiment reading and pending home sales, while Thursday sees the final release of Q4 GDP, trade data, the Chicago PMI and, of course, initial jobless claims.

In terms of that core PCE print on Good Friday, DB expects +0.27% vs. 0.42% last month. In Powell’s press conference, he remarked that the month-over-month print for core PCE could be “well below 30bps” at the end of the month. Taking him at his word does offer downside risk to our economists’ forecast. They believe upward revisions to the January healthcare services prices could square these two numbers.

In Europe, our European economists’ inflation chartbook covers recent trends and their forecasts here. For March readings, they expect the headline Eurozone index to come in at 2.5% (vs 2.6% in February) and core at 3.1% (3.1%). On a country level, their projections include 2.4% for Germany (2.8% next week), 2.5% for France (3.2% Friday), 1.3% in Italy (0.8% Friday) and 3.5% in Spain (3.0% Wednesday).

In Asia, the Nikkei (-0.64%) is the worst performer, retreating from its all-time high set on Friday as the Japanese yen saw some stabilisation after the nation’s top currency diplomat offered a verbal warning on potential intervention by the government (more below). Elsewhere, the KOSPI (-0.48%) is also losing ground after opening higher while Chinese stocks are bucking the regional trend with the Hang Seng (+0.48%), the CSI (+0.38%) and the Shanghai Composite (+0.44%) edging higher. S&P 500 (-0.12%) and Nasdaq futures (-0.11%) are slightly lower. 10yr UST yields (+1.2bps) are slightly higher at 4.21% as I type.

Coming back to Japan, top currency official Masato Kanda warned against the yen’s recent weakness, commenting that it is not in line with fundamentals and is clearly driven by speculation. He added that the government is closely watching currency moves and stands ready to take appropriate action against excessive fluctuations.

Staying with Asian FX, the onshore yuan rose as much as +0.48% to 7.1943 per dollar, after the PBoC signaled its support for the currency via a stronger-than-expected daily reference rate, marking the largest strengthening bias since November.

Recapping last week now, the S&P 500 had the best week of the year, rising +2.29% amid growing optimism that rate cuts by many major central banks are now on their way. The index saw a marginal retreat on Friday (-0.14%) after hitting record highs for three consecutive sessions. Tech stocks led the gains, as the NASDAQ rose +2.85% (and +0.16% on Friday) and the Magnificent Seven jumped +4.31% (+0.89% Friday). That said, the rally in equity was still fairly broad, as the equal-weighted S&P 500 index rose +1.78% (-0.64% on Friday).

Global equities were also on the stronger side. The STOXX 600 gained +0.96% (-0.03% on Friday), whilst the DAX and FTSE 100 rose +1.50% and +2.63%, respectively. For the former, this was another record high, and for the latter, the largest weekly increase since September. Otherwise, the Nikkei was a key outperformer, soaring +5.63% (and +0.18% on Friday), after the BoJ decided to end negative rates earlier in the week without any negativity, quite the opposite as the country went a step closer to normality. The Yen fell -1.55% during the week (-0.14% on Friday) as the BoJ were seen as relatively dovish and at 151.41 closed the week within a whisker of 34 year lows.

This broader risk asset strength was driven by investors increasing their bets on the amount of expected rate cuts for this year, particularly after the relatively dovish central bank meetings across both sides of the Atlantic, including the first G10 rate cut of the cycle being delivered by the SNB. The amount of Fed cuts expected by December rose +12.4bps (and +4.4bps on Friday) to 84.5bps. The expected probability of a June cut is now 86%, up from just over 60% at the start of the week. Over in Europe, it was a similar story, with the amount of cuts priced in by year-end rising by +4.7bps for the ECB and by +18.9bps for the BoE.

The dovish backdrop drove a sharp decline in global sovereign bond yields last week. US 10yr yields fell -10.8bps on the week, including a -6.9bps fall on Friday, while 2yr yields were down -13.9bps (-4.7bps Friday). German bunds outperformed, with yields falling -11.9bps (and -8.2bps on Friday), as strong data in the latter half of the week limited the rally in US Treasuries.

The risk-on sentiment also supported a rally in other asset classes. US IG and high-yield spreads fell -1bps and -6bps, respectively, seeing their lowest weekly close since November 2021 and January 2022, respectively. In commodities, gold hit a record of $2,181/oz earlier on Thursday but fell -0.71% on Friday to $2,165/oz, although prices were still up +0.44% on the week.