The benefits of learning a foreign language are extensive and go way beyond the ability to converse with people from other countries.

Speaking a second language broadens the horizon, takes the guesswork out of restaurant orders on vacation and even makes the Super Bowl Halftime Show more enjoyable.

It has professional benefits as well, as multilingualism is a much sought-after skill in today’s globalized world. Even though you can get by pretty well speaking only English, learning a second, or third, language is always going to be worth it.

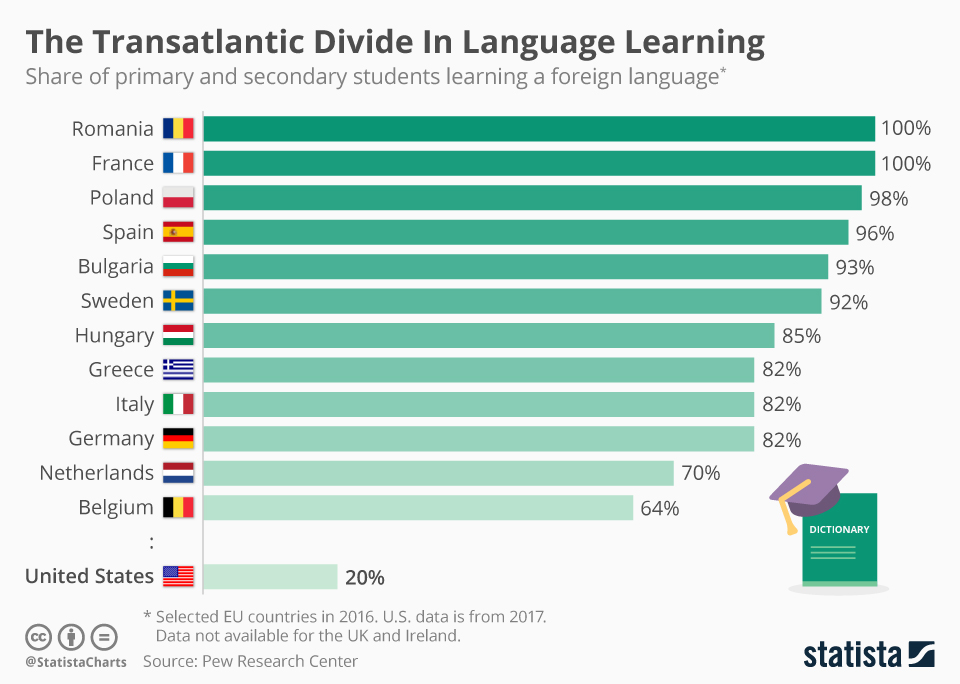

While learning foreign languages is ubiquitous in Europe, where most students start learning English as early as primary school, the story in the U.S. is completely different. Most European countries have a national-level mandate for studying languages at school but such standards are non-existent on the other side of the Atlantic where such legislation only exists at school district or state-level, if at all.

This is a far cry from the enrollment rates seen across Europe, as Eurostat data shows.

Many European countries have enrollment rates close to 100 percent, with an average of 91 percent of primary and secondary school students learning at least one foreign language across the European Union.

More than one in three students in the EU even study two or more foreign languages, showing that many student learn more than “just” English.

While English is by far the most widely taught foreign language across Europe, Spanish is the most popular second language in the U.S.

Of the 10.6 million students enrolled in a foreign language class in 2014/2015, 7.4 million studied Spanish and 1.3 million learned French.

Long-awaited banking regulation—also known as the Basel III Endgame framework—will be released next month, said the Federal Reserve’s top banking regulator.

Fed Vice Chair for Supervision Michelle Bowman, appearing at a Senate Banking Committee hearing on Feb. 26, confirmed that regulators are expected to release an updated Basel III proposal at the end of March.

But while this is the chief goal, Bowman hinted that the deadline might need to be extended.

She told lawmakers that officials at the Fed, Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation have reached a consensus on the reproposal.

Basel III is a regulatory blueprint crafted in the fallout of the global financial crisis of 2008. It features a number of capital reforms and tighter requirements for how large U.S. banks measure credit, market, and operational risk.

In recent months, Bowman has teased that Basel III has retooled capital requirements, a move that could bolster lending by traditional lenders, particularly in the mortgage market.

“We’re very focused, as we were thinking about the Basel approach, in ways that we could right-size and recalibrate the approach for residential mortgage lending so that we could encourage the banks to get back into the mortgage business,” Bowman told senators.

“We’re refocusing our supervision in a laser focus on material financial risks.”

This comes shortly after Bowman suggested new mortgage capital rules for U.S. banks would be integral to the Basel III proposal.

Appearing at an American Bankers Association event on Feb. 16, Bowman stated that one change could tie a mortgage’s risk weight to its loan-to-value-ratio, effectively removing the one-size-fits-all approach. Another update could remove a provision requiring that banks deduct mortgage‑servicing assets from regulatory capital.

For years, critics have argued that the original Basel III proposal would have reduced lending due to higher capital mandates and would have led to higher funding costs for borrowers.

Proponents say higher capital requirements are necessary to prevent a similar financial crisis in the future.

But while the focus has been on Basel, Bowman argued that other issues also need to be addressed, including the Consumer Financial Protection Bureau’s stringent requirements and the sizable penalties banks face if they make mistakes on mortgage applications.

“I think it’s important that we think about this in a broader manner and holistically as we approach thinking about banks getting back into the mortgage space,” Bowman said.

Support for Homeownership

Overall, Bowman noted, the upcoming reproposal could spark affordable homeownership, ensure banks of all sizes come off the sidelines, and support market liquidity.

“My approach is to calibrate the new framework from the bottom up, rather than reverse engineer changes to achieve predetermined or preconceived outcomes to capital requirements,” she stated.

This comes as a group of eight major banking and housing associations urged regulators to ease mortgage capital requirements.

In a letter to the Fed, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corp., the organizations stated that today’s regulatory environment discourages bank participation in mortgage markets, exacerbating housing affordability challenges.

The groups said they support current efforts to alter the Basel III Endgame rule, casting the process as an opportunity to strengthen mortgage‑market stability and create space for banks to play a larger role in home lending.

“Adequate capital reduces the likelihood of bank failures that threaten broader financial stability, which can prove costly for households, financial institutions, and taxpayers,” the letter stated. “However, excessive capital requirements that are misaligned with empirically derived risk assessments can negatively affect the cost of and access to credit.”

Revitalizing the mortgage market has been one of the current administration’s objectives to ensure more households have an opportunity to become homeowners.

In his record-length State of the Union address, President Donald Trump noted that his economic agenda balances the needs of current homeowners and homebuyers.

“Low interest rates will help reduce the Biden‑created housing affordability crunch,” Trump said. “We want to protect those values. We want to keep those values up. We’re going to do both.”

As of Feb. 26, the average 30-year fixed-rate mortgage is 5.98 percent, according to Freddie Mac’s Primary Mortgage Market Survey.

A recent National Association of Realtors poll found that 85 percent of U.S. voters believe homeownership is central to the American dream.

New revelations from Rep. Anna Paulina Luna expose Jeffrey Epstein’s network as a sophisticated honeypot operation likely tied to foreign intelligence, designed to compromise powerful figures through sex trafficking and blackmail.

Luna, leading the congressional probe, asserts the scandal runs deeper than previously known, with inconsistencies in plea deals for key female accomplices fueling suspicions of a cover-up to protect the elite.

Based on evidence reviewed in the investigation, Luna stated that Jeffrey Epstein was running an intelligence-gathering operation, stating “In my professional opinion, I do believe it was a honeypot operation.”

Based on our congressional investigation it is my professional opinion that Jeffrey Epstein was running a honey pot operation. I am calling on Oversight to bring these 4 women in for questioning as co-conspirators to child sex trafficking. pic.twitter.com/KmxEovN9hC

“It has become very evident…that Jeffrey Epstein was running an intelligence gathering operation,” Luna continued, noting “We might be able to get justice.”

She elaborated, “I do believe that Jeffrey Epstein was targeting many politicians, many influential people, especially in regards to economic policy. I do believe that it was possible that not just (Bill Clinton), but Secretary Clinton as well as a number of other people were targeted.”

Luna called for subpoenas on four women identified as co-conspirators: Sarah Kellen, Nadia Marcinkova, Adriana Ross, and Lesley Groff.

?Congresswoman Anna Paulina Luna drops BOMBSHELL, reveals she believes Jeffrey Epstein was running an Intelligence gathering Honey Pot Operation based on evidence and testimony.

She is also calling on on four co-conspirators involved in trafficking who she says are being… pic.twitter.com/WUgdiv2G34

These individuals received immunity under Epstein’s 2008 non-prosecution agreement, despite allegations of scheduling abuse, recruiting victims, and participating in acts.

Luna also highlighted other discrepancies, such as Susan Hamblin sending an email in which she told Epstein his “littlest girl was naughty,” yet receiving victim status and a plea deal.

? Rep Anna Luna just revealed that Epstein “victim” Susan Hamblin sent the “your littlest girl was naughty email”

“Susan Hamblin sent this email. She took a plea deal and was given “victim” status under previous DOJ. DOJ should look into charges.

The Congresswoman also pointed to Nadia Marcinkova, who sent explicit emails as an adult co-conspirator but was granted victim status.

This email was sent by a woman named Nadia. The same Nadia that was listed as co-conspirator in the NY case. She was then given a plea deal and “victim” status.

There’s a big difference between minors that were victimized versus ones that became adults and then chose to do… pic.twitter.com/NOXGDdgg6m

Luna demanded, “The DOJ NEEDS to re-open these cases, adding that the “Previous DOJ let them off.”

She added, “Why were a number of Epstein’s co-conspirators given plea deals for trafficking minors? Child sex traffickers do not deserve plea deals or immunity. EVER.”

Why were a number of Epstein’s co-conspirators given plea deals for trafficking minors? Child sex traffickers do not deserve plea deals or immunity. EVER. pic.twitter.com/wT4CEQz1Gd

Barry Levine, author of “The Spider,” reinforced on Jesse Watters’ show that female co-conspirators received plea deals for trafficking.

Levine noted models from around the world were involved, echoing Luna’s foreign ties concerns.

Barry Levine knocked it out of the park on Watters right now. FEMALE Co-conspirators were given plea deals! There is a lot here. Trafficking etc. everyone needs to see this segment. pic.twitter.com/B2dfYbBLDG

Jesse Watters highlighted, “Hillary did seem perceptive to the idea.”

BREAKING: Rep Anna Paulina Luna says Hillary was PRESSED on Jeffrey Epstein’s FOREIGN INTELLIGENCE TIES ?@RepLuna: “It’s safe to say, Epstein was TIED to Foreign Intelligence… RUSSIA, IRAN, ISRAEL” ?

In another major development in the case, former President Bill Clinton testified under oath that President Trump was not involved at all with Epstein to his knowledge.

?? BREAKING: Democrats are DONE. President Bill Clinton testifies UNDER OATH that President Donald Trump WAS NOT involved with Jeffrey Epstein

“Trump has never said anything to me to make me think he was involved [with Epstein].”pic.twitter.com/seQ15pfTrI

Clinton stated, “Trump has never said anything to me to make me think he was involved [with Epstein].”

Luna confirmed, “President Trump has been exonerated. He is not considered a person of interest in our Congressional investigation.”

President Trump has been exonerated. He is not considered a person of interest in our Congressional investigation. Democrats continue to insist otherwise to smear him and sabotage his presidency. It’s a political game to them. pic.twitter.com/QlwlWE3YFd

She accused Democrats of smearing Trump, saying, “Democrats continue to insist otherwise to smear him and sabotage his presidency. It’s a political game to them.”

“We had cooperation, we asked the victims directly and he was exonerated,” Luna said.

Fresh documents from the mass file release have also revealed a shocking intrusion into the FBI’s NYC office on Super Bowl Sunday in 2023, resulting in the loss of approximately 100TB of evidence.

FBI Special Agent Aaron Spivack detailed the breach in a declaration, stating, “500 terabytes of data was gone as a result of the intrusion. I was able to recover about 400 terabytes of that data, however. I was told to Google how to recover the data. No one else tried to help us.”

Spivack described discovering unusual activity: “Around 3:30pm or so we located the log files and began combing through, which is when we noticed strange IP activity that took place yesterday from two IP addresses. The activity included combing through certain files pertaining to the Epstein investigation.”

He continued, “I reached out to one of the case agents to see if they were in the office yesterday, thinking that maybe they inadvertently changed a setting on the NAS or if they noticed anything strange about them.”

Further investigation revealed, “Around 4/4:30pm we dove into the IPs and checked all of our computers to see which had the IPs in question. One computer, our discovery computer, matched one of them and is located in a room next to the lab. The other IP is one we don’t recognize, but it is the same address as the IP on our network, leading us to believe it was a computer that accessed our network somehow.”

Spivack concluded, “We were not able to identify the computer, but it had to have accessed our network either by being plugged into the network, or possibly by telnetting in virtually.”

This breach raises serious questions about security lapses and potential efforts to suppress evidence in the Epstein case.

These disclosures build on anomalies detailed in our prior reports, where DOJ documents referenced Epstein’s death as a “MURDER” and highlighted red flags like mismatched autopsy details and missing footage.

The inconsistencies point to elite protection of the operation.

Theories that both Epstein and Ghislaine Maxwell were intelligence operatives linked to Mossad, other foreign entities and a “supra government” shielding elites have exploded online.

As demands for the full client list grow, these revelations expose a web of elite impunity. The public deserves unredacted truth to dismantle any remaining deep state shields.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

If You’re Freaking Out About A Future Jobless AI Dystopia…

Amid an armada of dystopian futurists, projecting linear thoughts into a future of ‘AI uber alles’, Marc Andreessen stands as a beacon of potential utopian light, seeing a future that looks very different and very positive for young and old alike.

In a brief few minutes, the co-founder of Netscape and VC firm Andreessen Horowitz (a16z) believes instead that we are living through a unique (and most incredible) time in history with the rise of AI coming right as human civilization needs it…

“we’re going to have AI and robots precisely when we actually need them [with populations shrinking] to keep the economy from actually shrinking.”

Simply put, Andreessen says that fears of AI-driven mass job loss are overly simplistic.

After decades of unusually slow technological change and low job churn, AI could restore historical productivity levels (exemplified by the period from 1870-1930), sparking opportunity, innovation, and net job growth rather than displacement.

Declining populations and reduced immigration will make human labor increasingly valuable. AI’s timing is “miraculous”, Andreessen exclaims, preventing economic shrinkage from depopulation.

In even radical scenarios, explosive productivity leads to output gluts, collapsing prices, and massive real-wealth gains – equivalent to “giant raises” for everyone – while making safety-nets more affordable.

Whether incremental or transformative, Andreessen sees the outcome as fundamentally positive economic news.

“…there’s all this concern among young people that their jobs are not going to be there for them. AI is replacing them…”

Andreessen replies (emphasis ours):

So the job-substitution/job-loss thing is very reductive. I think it’s an overly simplistic model. And again it goes back to what I said at the very beginning which is we’ve actually been in a regime for 50 years of very slow technological change in the economy… like at half the rate of the previous era and a third the rate of like 100 years ago.

And so we’re coming out of this kind of phase where we’ve had like almost no technological progress in the economy. We’ve had remarkably little job churn as a result of that relative to any historical period. And so even if AI triples productivity growth in the economy, which would like be a massively big deal, it would take us back to the same level of job churn that was happening between 1870 and 1930.

And if you go back and you read accounts of 1870 to 1930, people just thought the world was awash with opportunity. Right? At that rate of technological transformation, kids were able to develop new careers into new areas of the economy, building new kinds of products and services. A huge part of everything in our modern world today was kind of invented and proliferated during that period.

And so even if AI triples the pace of economic change in the economy, it’s going to translate to a much higher rate of economic growth; it’s going to translate to a much higher rate of job growth. And there will be some level of like task level and job level substitution that will take place but that will be swamped by the macro effects of economic growth and innovation that will happen and that then corresponding to that there will be hiring blooms quite honestly I think all over the place

And then again go back to the fact that this is all happening in the face of declining population growth and increasingly population shrinkage. So human workers in many, many, many countries over the next you know 10, 20, 30 years are going to be at more and more of a premium, literally because you’re going to have shrinking population levels.

[While] we don’t really want to get into you know politics particularly but it does feel like the world broadly is going to reverse course on the rates of immigration that we’ve had for the last 50 years. it seems to be kind of a broad-based thing happening – rise in nationalism, concerns about the rate of immigration – and immigration historically in countries like the US ha ebbed and flowed over time based on how the national mood shifts.

And so in a country like the US (or any country in Europe), if you combine declining population with less immigration, the remaining human workers are going to be at a premium not at a discount. And so I think that the combination of faster productivity growth, faster economic growth, and then slower population growth and less immigration – actually means there’s going to be much less of this kind of dystopian/no-jobs thing. I just think it’s probably totally off-base.

“That is extremely interesting. So, what I’m hearing is you’re not super worried about job loss. Is the key here that the timing kind of just works out, this population decrease, you know, like all these kind of have to line up for there not to be this massive job loss with AI?”

Andreessen replies (emphasis ours):

Yeah.

Well, look, if we didn’t have AI, we’d be in a panic right now about what’s going to happen to the economy. Right? Because what we what we’d be staring at is a future of depopulation and depopulation without new technology would just mean that the economy shrinks. Right?

So it would mean that the economy kind of itself kind of shrinks over time, the opportunity diminishes, and there are no new jobs, there are no new fields. There’s no new source of consumer demand for spending on things. And so you would be very worried about going into period of severe decline or stagnation.

Essentially you’d be looking at these very dystopian scenarios of like an economy self-euthanizing over time.

So you’d be very worried about the opposite of what everybody thinks that they’re worried about. The only reason we’re not worried about that is because we now know that we have the technology that can substitute for the lack of population growth and also for the for the lack of immigration that’s likely.

And so, I would say the timing has worked out miraculously well in the sense that we’re going to have AI and robots precisely when we actually need them, to keep the economy from actually shrinking.

And that’s just like a fundamentally good news story.

To get to the mass-job-loss thing that people are worried about, you’d have to look at like far, far, far higher rates of productivity growth. You’d have to look at rates of productivity growth that are 10, 20, 30, 50% a year – something like that – which are orders of magnitude higher than we’ve ever had in any economy in the history of the planet.

It’s possible that we get that. I mean, look, I have my utopian temptation along with everybody else.

If AI radically transforms everything overnight, then maybe… let’s play out the kind of utopian scenario.

You get to a much higher level of productivity growth.

You get to a much higher level of technological change.

Corresponding to that you’ll have a massive economic boom.

You’ll have massive growth in the economy and then corresponding with that you’ll have a collapse in prices.

And so the price of goods and services that are affected by (or commoditized by) AI will collapse.

There’ll be price deflation and then as a consequence of price deflation everything that people are buying today gets a lot cheaper and that’s the equivalent of a gigantic increase in wealth right across the society.

This is actually worth talking about because people I think people get kind of sideways on this issue.

So if AI is going to transform the economy as much as the utopians or dystopians (or whatever kind) think that it will, the necessary economic calculation of what happens is massive productivity growth.

The consequence of massive productivity growth literally means mechanically more output requiring less input, right?

So you get more economic output for less input, right? So you’re substituting in AI for human workers.

And as a consequence, you get like this massive boom in output with much lower input costs.

The result of that is you get lots of goods and services in all those affected sectors. The result of those gluts is you get collapsing prices, right?

The collapsing prices mean that the thing today that cost you $100 now cost you $10 and now cost you $1.

That’s the equivalent of giving everybody a giant raise, right?

Because now they have all this additional spending power.

That additional spending power then translates to economic growth, right?

The development of new fields. Everybody’s materially much better off very quickly. And then by the way, to the extent that you do have unemployment coming out the other side of that, it’s now much cheaper to provide the kind of social safety net to prevent people from being immiserated, right?

Because the prices of all the goods and services that a welfare program has to pay from, they’re all collapsing, right? And so the price of healthcare collapses, the price of housing collapses, the price of education collapses, the price of everything else collapses because of the incredible impact that AI is having.

And so in this kind of utopian/dystopian scenario that people have, there’s no scenario in which everybody’s just poor. In fact, it’s quite the opposite.

Everybody gets a lot richer because prices collapse and then it’s actually much easier to pay for the social safety net for the people who, for some reason, can’t find a job.

And so, maybe we end up in that scenario.

I mean, the optimistic part of me says, yeah, maybe AI is that powerful and maybe the rest of the economy can actually change to accommodate that and maybe that’ll happen.

But the result of that is going to be a much better news story than people think it’s going to be.

Everything I’ve just described, by the way, is just a very straightforward extrapolation on very basic economics. I’m not making any like bold predictions in what I just said. This is just a straightforward mechanical process that plays itself out if you have higher rates of productivity growth, which are necessarily the results of higher rates of technological growth.

And so, to be clear, I think we’re looking at a world that’s not like radically transformed the way that maybe the utopians think that it will be or the dystopians think it will be.

I think it’ll be more incremental.

But I think that incremental shift is overwhelmingly going to be a good news process. And then even if it’s much faster, it’s also going to be a good news process. It’ll just be a good news process in the other way that I described.

Tl;dr: Bloomberg macro strategist, Michael Ball, warned that President Trump’s urging of Iranians to overthrow the government gives Saturday’s US and Israeli strikes on Iran the potential to usher in a more prolonged higher-volatility era rather than being a one-off tradeable shock.

Traders will be closely watching for updates on crude production and shipping disruptions, and any spike in oil will move across global rates and FX and eventually weigh on equities – but Trump’s post-strike comments make it harder for markets to assume this is one and done.

A limited strike would likely see the usual pattern:

Crude and gold spike, equities wobble, then volatility compresses if production is unaffected and Strait of Hormuz flows keep moving, leading the risk premium to ebb quickly.

But a longer-term campaign framed around leadership removal is different.

It will stretch the uncertainty window, raise the probability of wider tail risk outcomes, keep oil prices elevated and volatility high and force broader risk premiums to reflect a more uncertain growth and inflation backdrop.

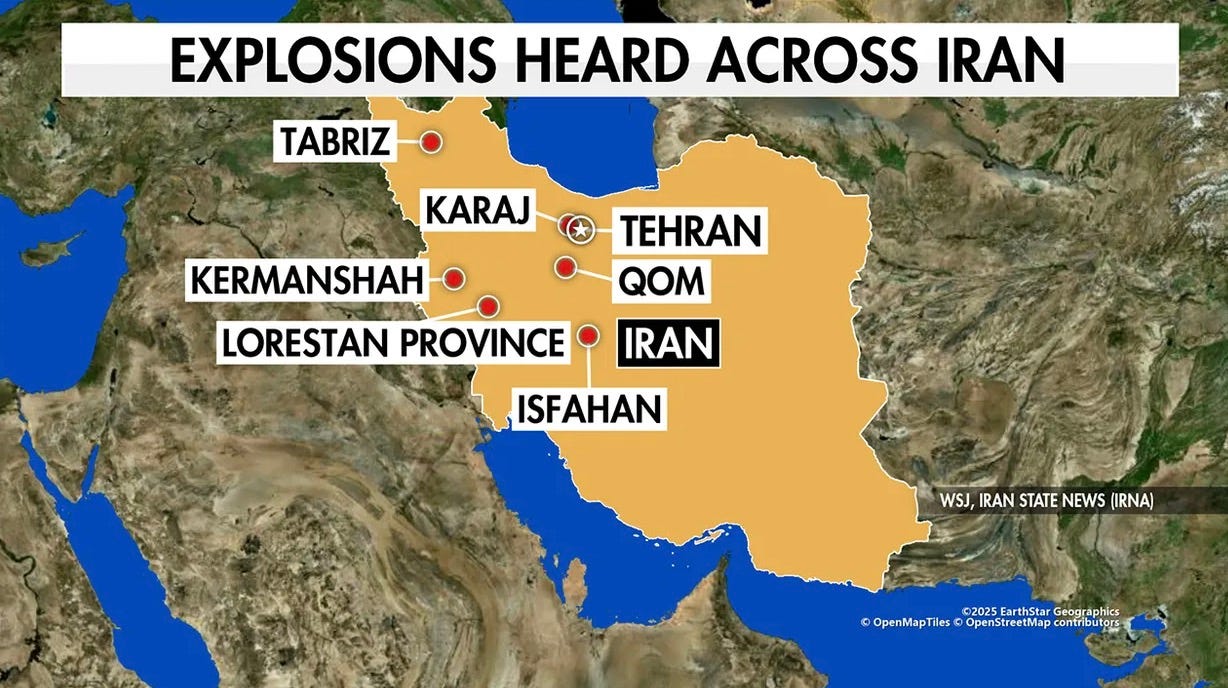

Most of the U.S. woke up today to news that that the U.S. and Israel have started “major combat operations” and a broad military campaign against targets across Iran.

Someone was obviously in the know that full-scale military action involving Iran was about to kick off Friday night and was positioning ahead of it.

Anyone who tells you the options market can’t telegraph news or hint at where the market is headed isn’t paying attention.

Order flow doesn’t predict everything – but sometimes it absolutely signals that something big is coming.

The operation against Iran reportedly began with strikes in Tehran and other strategic locations late last night/early this morning. President Donald Trump urged Iranian civilians to take shelter during the attacks, but also made unusually direct comments suggesting that once operations conclude, Iranians should reclaim control of their government. The framing went well beyond nuclear concerns and referenced decades of hostility between Washington and Tehran since the 1979 revolution.

Initial targets reportedly included areas associated with Iran’s Supreme Leader, Ayatollah Ali Khamenei, though it was not immediately clear whether he was present. Smoke was seen rising over parts of Tehran as the strikes unfolded.

According to various live reports (AP, CNN, Bloomberg) up until this morning, Iran responded quickly. The Revolutionary Guard announced it had launched drones and missiles toward Israel in what it described as an initial wave of retaliation. Air raid warnings sounded across Israel as the military moved to intercept incoming fire.

The stated rationale from Washington and Jerusalem centered on escalating tensions over Iran’s nuclear program and missile capabilities. U.S. naval assets had been repositioned in the region in recent weeks as diplomacy stalled. Israeli Prime Minister Benjamin Netanyahu characterized the joint action as necessary to eliminate what Israel sees as a direct and existential threat.

The regional fallout has been swift. Iraq and the United Arab Emirates closed their airspace. Sirens were reported in Jordan. Bahrain said a missile targeted the headquarters of the U.S. Navy’s Fifth Fleet. Explosions were reported in Qatar. Syria later shut down portions of its southern airspace. Several major airlines suspended flights as a precaution.

European leaders issued a joint appeal for restraint, emphasizing the need to prevent further escalation and protect civilians. They stressed the importance of nuclear safety and adherence to international law while noting that the European Union has long pursued diplomatic efforts alongside sanctions targeting Iran’s leadership and Revolutionary Guard. EU officials said they are coordinating with member states to assist citizens in the region.

Meanwhile, Iran’s Revolutionary Guard said it had struck multiple facilities in retaliation, including U.S. installations in Bahrain, Qatar, and the UAE, as well as military targets in Israel.

Ayatollah Khamenei had not made a public appearance in the days leading up to the attack and had reportedly been moved to a secure location during prior hostilities. His current status has not been confirmed publicly. According to a person familiar with the planning, the operation had been coordinated between the U.S. and Israel for months and is expected to continue for several days.

So what does it mean for markets on Monday?

The way I see it, there are two very different paths that are possible here.

One path is that this becomes a non-event by Monday morning. We have precedent.

The U.S. military operation ordered by Donald Trump against Venezuela occurred over the weekend in early January, rather than on a weekday, and involved strikes in and around Caracas and the capture of President Nicolás Maduro.

Markets reopened on the following Monday, and major stock indexes, including U.S. equities and energy shares, were generally steady to higher as investors weighed the news and focused on the implications for oil-related sectors and broader fundamentals rather than selling off sharply in response to the weekend geopolitical event.

In those instances, traders ultimately treated the events as tactical and contained rather than the start of prolonged war. If investors conclude that objectives are narrow, retaliation is limited, and oil flows remain uninterrupted, markets could interpret the move as decisive rather than destabilizing.

In that scenario, dip buyers step in, volatility fades, energy spikes briefly, and by midweek the narrative shifts back to earnings, AI, and Fed policy.

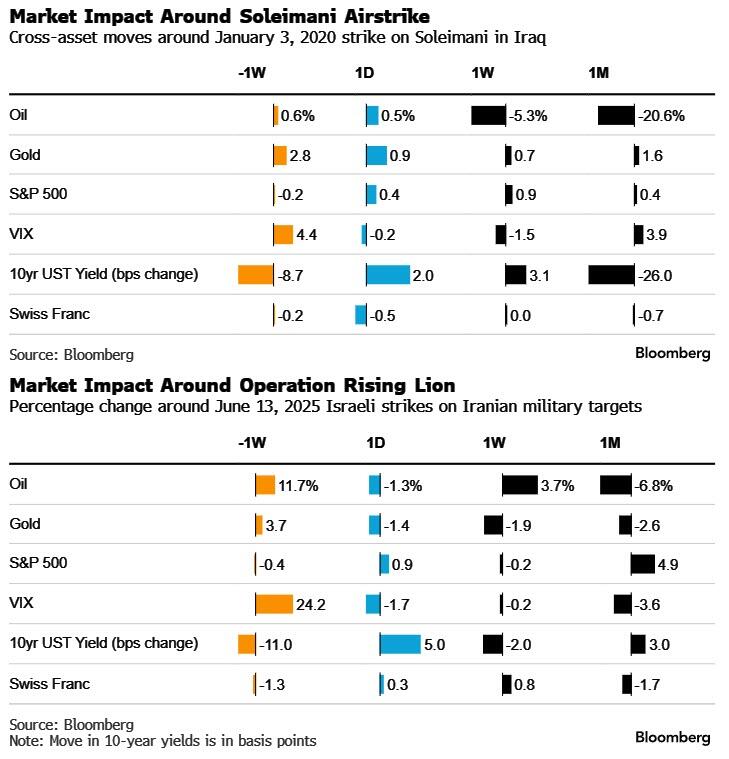

Relevant precedents include the air strike to take out Qassem Soleimani in January 2020, and last year’s extensive Israeli strikes as part of Operation Rising Lion and US strikes on nuclear sites in Iran that comprised Operation Midnight Hammer.

If anyone knows the “I’m long gold and silver at the right time, futures have skyrocketed but by the time the cash open comes they’re already red” scenario, it’s me.

It happened the last time Israel attacked Iran last year — futures were crushed overnight but by the next morning’s cash open, rhetoric had softened and the market had already recovered.

But there’s still always the “other” scenario, too: escalation, both geopolitically and financially.

A worst-case outcome would involve a drawn-out regional conflict marked by heavy missile exchanges and the activation of Iranian proxy groups across Lebanon, Iraq, Syria, and elsewhere. Fighting could spread across multiple fronts, potentially pulling in additional regional actors and forcing deeper U.S. military involvement. Iran could attempt to disrupt shipping through the Strait of Hormuz or target regional energy infrastructure, creating a meaningful shock to global oil supply. Even temporary disruptions could push crude sharply higher, intensify inflation pressures, and rattle global risk assets.

A prolonged conflict could destabilize the Iranian state itself, creating internal fragmentation, humanitarian crisis, or a power vacuum. Alternatively, a regime under severe pressure might accelerate nuclear development as a deterrent. Either direction introduces multi-year instability.

The economic consequences would likely include higher energy costs, rising shipping and insurance expenses, and a broad tightening of financial conditions — all while global growth is already fragile.

There is also an ugly scenario that I don’t think is extremely likely, but needs to be taken very seriously.

That matters because private credit has been one of the pillars of liquidity supporting risk assets over the past several years.

If stress there deepens, it can spill into broader credit markets quickly.

At the same time, last week’s ugly PPI data complicated the Federal Reserve’s position. Sticky inflation limits how aggressively policymakers can ease if financial conditions tighten. If you combine a Fed that looks constrained, early tremors in private credit, aggressive bank selling, and now the introduction of a serious geopolitical shock, the margin for error to keep a market trading at a Shiller PE of 40x shrinks.

If energy prices spike and inflation expectations rise, yields could climb at the same time growth expectations fall — a stagflationary mix that equities historically struggle with.

That is the type of setup that can turn a contained event into a liquidity event.

And once liquidity events begin, correlations go to one.

Positioning into Monday becomes less about prediction and more about preparation.

My 26 Stocks I’m Watching for 2026 were built with this type of uncertainty in mind. Precious metals names provide a hedge against geopolitical instability and currency debasement. Energy exposure benefits if crude moves higher or supply risk premiums expand. Select emerging markets with commodity leverage can outperform in resource-driven cycles. Consumer staples offer defensive ballast if broader indices wobble.

I’m not scrambling to overhaul that list. The bigger adjustment for people positioned similarly will be mostly mental. You prepare for a range of outcomes.

Green futures because traders assume containment. A sharp red open if oil gaps higher and risk parity funds de-risk. A volatility spike that fades by midday. Or a genuine air pocket if credit markets continue Friday’s mini-bank run and seize up.

This is also a reminder of how quickly narratives shift. On Thursday, the focus was inflation prints and private credit stress. By Saturday morning, we are discussing potential regional war that’ll take “days, not hours”, according to U.S. officials. Markets are reflexive and forward-looking, but they are not omniscient. Complacency builds quietly during extended rallies, especially when liquidity has repeatedly rescued drawdowns.

Sharp downturns often arrive before policymakers step in. If history is any guide, meaningful volatility tends to precede intervention — not follow it.

And again the larger lesson: things change fast, and they change without notice. Complacency kills, even in markets that appear permanently supported.

“Tone Down My Opinions”: Police Visit Maryland Man Over Facebook Rage Posts About Soaring Power Bill

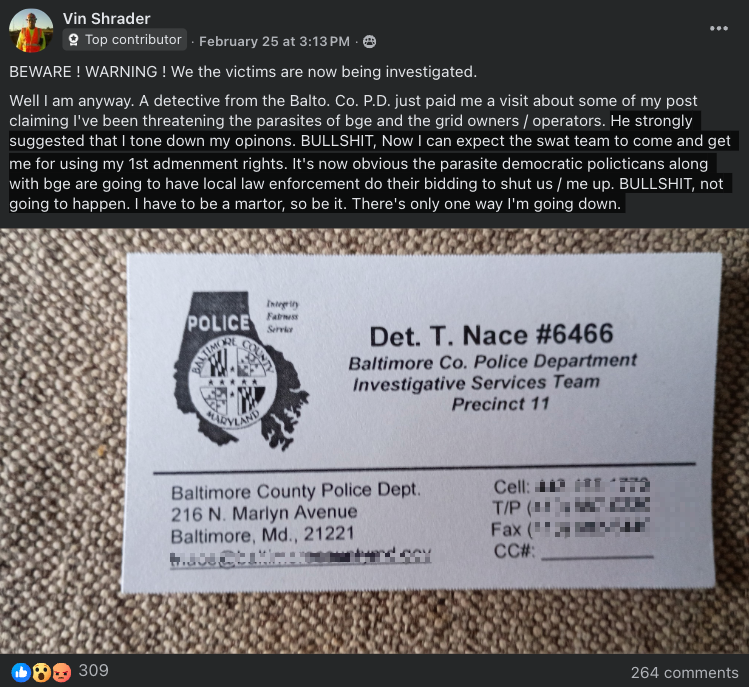

A Baltimore County, Maryland resident in a Facebook group called “BGE Victims,” which has 22,000 Marylanders venting about the power bill crisis, revealed earlier this week that a Baltimore County Police detective “paid [him] a visit” over posts in the online group that allegedly threatened “the parasites of BGE and the grid owners/operators.”

Baltimore resident Vin Shrader – or at least that’s his online name – said, “A detective from the Balto. Co. P.D. just paid me a visit about some of my post claiming I’ve been threatening the parasites of bge and the grid owners / operators,” adding, “He strongly suggested that I tone down my opinons.”

Shrader continued, “BULLSHIT, Now I can expect the swat team to come and get me for using my 1st admenment rights. It’s now obvious the parasite democratic policticans along with bge are going to have local law enforcement do their bidding to shut us / me up. BULLSHIT, not going to happen. I have to be a martor, so be it. There’s only one way I’m going down.”

The Maryland power bill crisis first came to our attention in August 2024, when years of poor power-grid management by Democrats (mostly due to backfiring ‘green’ policies) in the state collided with surging electricity demand from AI data centers (read here).

Fast forward to today: the power bill crisis in the one-party rule state of Democratic Party kings and queens, headed by leftist Gov. Wes Moore, who has presidential ambitions, is getting hammered in the polling numbers (new data from Annapolis-based Gonzales Research & Media) as struggling Marylanders are financially crushed by mounting power-bill debt and venting their frustration in the group of 22,000.

All along, it was inevitable that the power bill crisis in the Mid-Atlantic would become a “major political issue” and that it was only a matter of time before the people revolted against local politicians who’ve been wearing green blinders for a decade, if not longer.

We don’t want to be the bearer of bad news for residents in the region, but the epic grid mismanagement by Democrats, now colliding with the era of data centers, almost certainly means this crisis is not going away anytime soon and will likely become one of the most pressing issues in Mid-Atlantic states like Maryland.

FYI to the 22,000 members of the group: It seems as if “Big Brother” is watching…