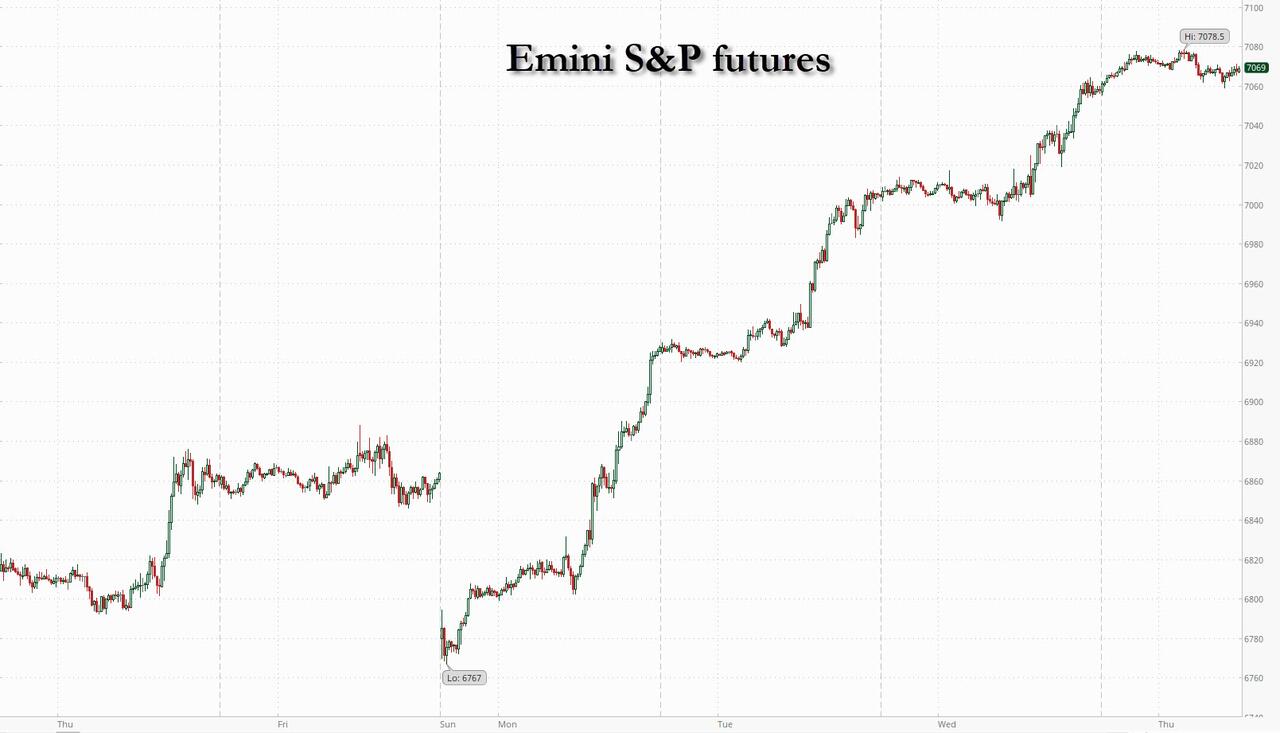

“The Roaring 2020s Are Back”: S&P Futures Hit New Record With Nasdaq Up 12 Straight Days On Iran Truce Optimism

Stock futures are edging higher on continued optimism about an extended truce in the Middle East, while Taiwan Semi’s solid results have sparked another leg higher in AI trade. As of 8:15 am ET, S&P 500 futures rose 0.1%, while Nasdaq 100 contracts +0.2%, and on pace for a 12th day of gains. The early hours of the session saw a sharp rally in technology stocks after TSMC’s upbeat revenue outlook highlighted the resilience of AI chip demand. In premarket trading, Mag 7 stocks were mostly higher led by MSFT +1.8% and TSLA +1.3%. On geopolitical headlines, the White House remains optimistic on the second round of talk (key Pakistani negotiator visits Tehran); Israel’s security cabinet met to discuss a possible ceasefire. Bond yields are 0-2bp lower with a modest gain in the dollar. Brent rose toward $96 a barrel as movements through the Strait of Hormuz remained all but paralyzed. Bonds rose, led by gains in Europe where central bank policymakers signaled they’re in no rush to raise interest rates. The dollar snapped an eight-day losing streak while gold rose above $4,800 an ounce. April’s strong stock rebound is being driven by a new kind of FOMO, according to Ed Yardeni, with Goldman saying that “despite the sharp market rebound, positioning has not fully caught up.” Still, while equities are “definitely pricing” the end of the war, we are “not there yet,” cautioned HSBC’s Patrick George while the IMF and World Bank are also worried that markets are underestimating the war’s economic damage. Today’s US economic data calendar includes April New York Fed services business activity, Philadelphia Fed business outlook, weekly jobless claims (8:30am) and March industrial production (9:15am). Fed speaker slate includes Williams (8:35am) and Miran (10:35am)

In premarket trading, Mag 7 stocks are mixed: Microsoft +1.3%, Tesla +0.7%, Meta Platforms +0.5%, Nvidia -0.4%, Alphabet -0.2%, Apple +0.8%, Amazon -0.1%

- Nuclear and uranium companies are set to extend this week’s rally after the White House released rules for establishing a National Initiative for American Space Nuclear Power. Oklo (OKLO) +7%, NuScale Power (SMR) +10%.

- Quantum computing shares are on track to extend gains for a third consecutive session after Nvidia unveiled a suite of new open-source AI models aimed at accelerating progress within quantum computing.

- Allbirds (BIRD) tumbles 21% as the newly minted AI stock takes a breather after soaring more than 580% on Thursday.

- Hims & Hers (HIMS) rises 9%, with shares on track to extend the previous day’s 14% rally, after Health Secretary Robert F. Kennedy Jr. said the FDA is seeking to remove 12 peptides from Category 2 restrictions.

- PepsiCo Inc. (PEP) gains 1% after quarterly revenue and earnings beat expectations as the maker of Doritos and Lay’s sees improvement in salty snacks volume following recent price cuts.

- PPG Industries (PPG) rises 3% after the supplier of paints and coatings posted preliminary first quarter adjusted earnings per share that topped expectations.

- QuidelOrtho Corp. (QDEL) sinks 17% after the health care services provider posted disappointing preliminary first-quarter revenue as US flu-like illness visits fell by about 30% from the year-earlier period.

- Travelers (TRV) slips 1.4% after the insurance company posted first quarter results where net premiums written declined 1.7% from the year-ago period.

- U.S. Bancorp (USB) rises about 1% after first-quarter profit beat estimates, as Chief Executive Officer Gunjan Kedia rounds out her first year leading the largest regional bank and boosting its stock.

- Voyager Technologies (VOYG) gains 6% after the defense and space company signed an order with NASA for the seventh Private Astronaut Mission to the International Space Station.

Elsewhere in AI, Nvidia’s Jensen Huang said the US should seek greater cooperation with China on AI research. Politicians are also weighing in on the global AI race, with House Republicans calling for US sanctions against Chinese entities that improperly extract results from leading US AI models to develop their own competing systems. Today’s Big Take focuses on Anthropic’s race to assess the dangers of Mythos.

Stock markets have rebounded as signs of easing tensions in the Middle East, combined with a fresh burst of AI optimism and corporate earnings, pushed investors to abandon their cautious views. Sentiment was boosted by lack of bad Iran news again: this time, the US and Iran are said to be considering a two-week ceasefire extension to allow more time to negotiate a peace deal; the next meeting between US / Iran may take place later this week with chatter from Pakistani media that Trump is said to be in attendance. April’s strong stock rebound is being driven by a new kind of FOMO, the fear of missing out on peace, according to Ed Yardeni, who said that for stocks, the V-shaped recovery this month makes it feel “like the Roaring 2020s are back.” Still, while equities are “definitely pricing” the end of the war, we are “not there yet,” cautioned HSBC’s Patrick George. The IMF and World Bank are also worried that markets are underestimating the war’s economic damage.

In the latest developments in the conflict, Pakistan stepped up efforts to help the US and Iran prolong a ceasefire that’s set to expire next week.

“Investors have become conditioned to buy every dip,” said Michael Bell, head of market strategy at RBC BlueBay Asset Management. “The outlook is binary, either Hormuz reopens soon or it doesn’t. With equity markets already assuming Hormuz will reopen soon, the upside is perhaps limited.”

The AI narrative is back in focus after TSMC raised its outlook for 2026, forecasting revenue growth of more than 30% and saying that capex is likely to lean toward the upper end of its forecast ($56 billion). Elon Musk’s Terafab project, which aims to reshape the chipmaking landscape dominated by TSMC, is reaching out to chip industry suppliers and asking them to move at ‘light speed’ on his project.

“TSMC describing AI demand as ‘extremely robust,’ pushing capex to the upper end of a $52-56 billion range, and signaling that the next three years of investment will significantly exceed the last three; that is not the language of a cycle nearing its peak,” said Amanda Lyons, information technology sector lead and head of research at Energy Group Capital.

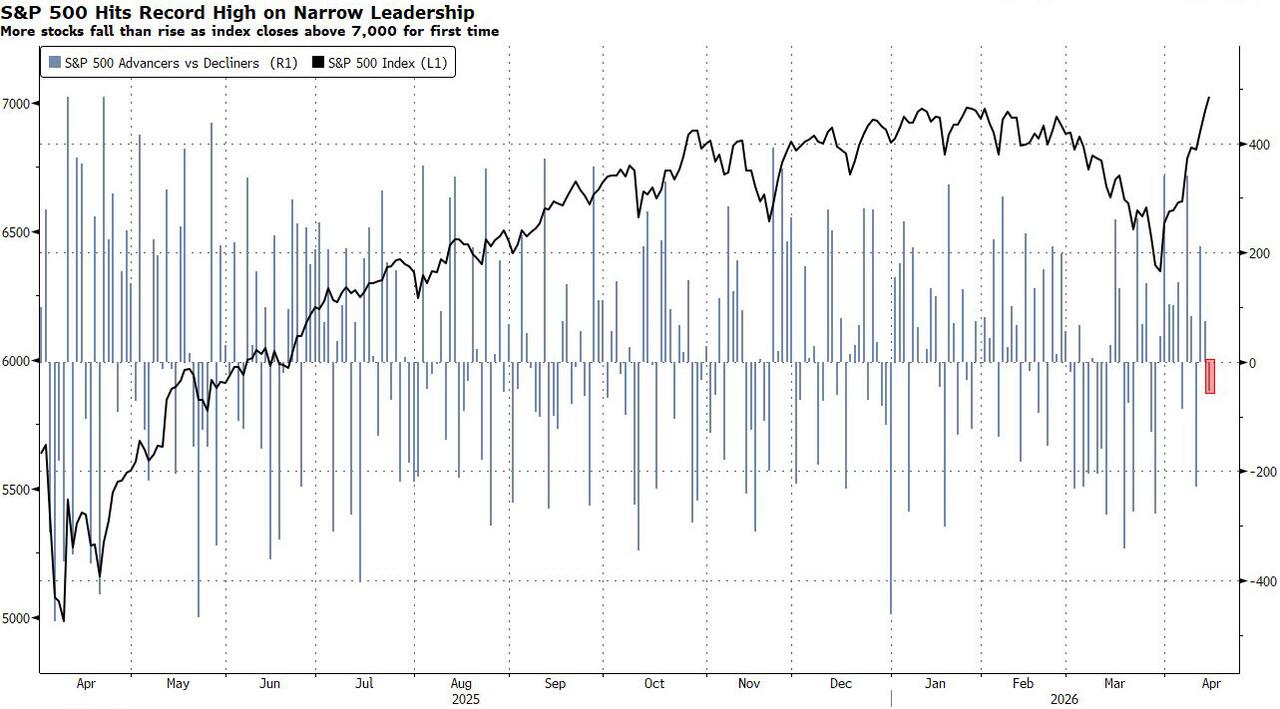

While the S&P 500 hit a new record on Wednesday, valuation ratios are still well below the levels seen in late 2025, indicating that earnings forecasts are moving up faster than stock prices. The current 12-month forward blended PE multiple for the S&P 500 of about 21 times compares to a peak of 23 times in November. The rally is also without breadth, with more decliners than advances as the gauge passed 7,000.

Another concerning fact about the latest record high: it was reach with more decliners than advancers, suggesting the leadership of this meltup is becoming dangerously narrow.

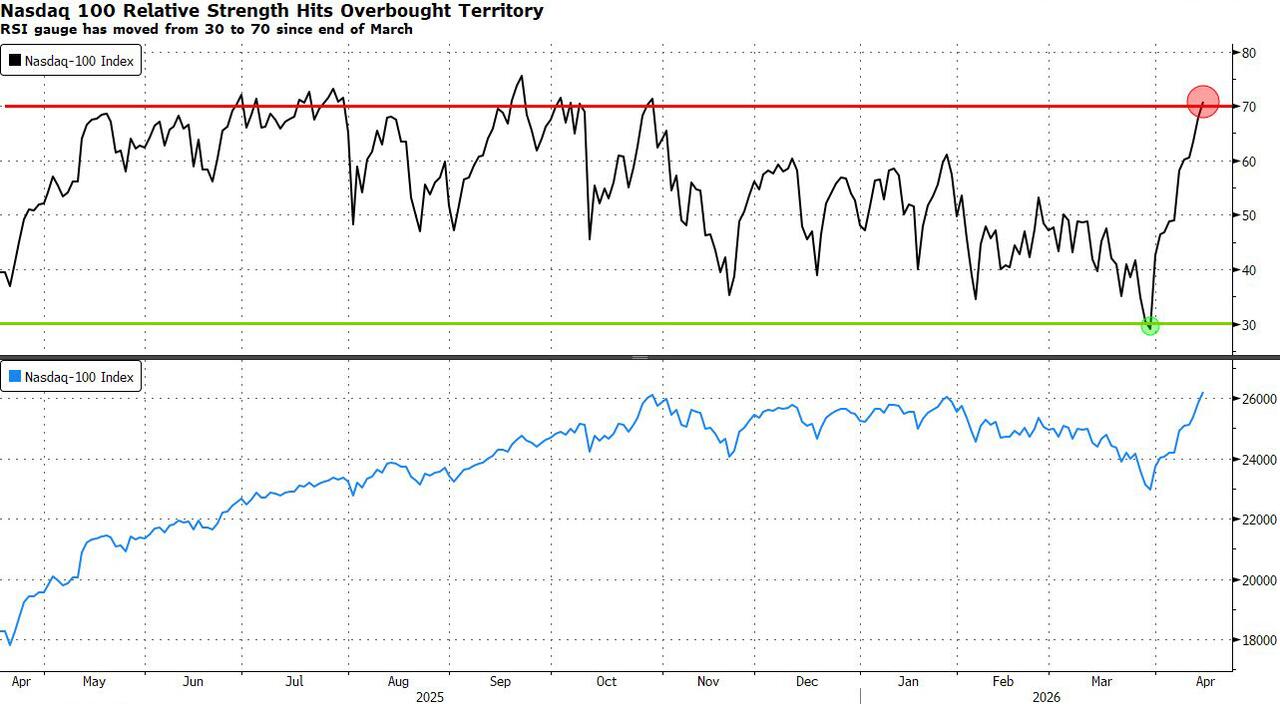

Lack of breadth however hasn’t stopped the Nasdaq from going from oversold to overbought in 2 weeks.

Technology stocks have been snapped up in recent weeks after lagging the market for much of the year, putting the Nasdaq 100 on course for its longest winning streak since 2017 if the gauge extends gains on Thursday.

Claudia Panseri of UBS Wealth Management said her exposure to artificial intelligence stocks is focused on the US and China and is “more selective” than two years ago. “We also prefer companies which are still investing using cash, rather than companies issuing bonds,” Panseri told Bloomberg TV.

Some stocks face a volatile option expiry into Friday, with $3.3 trillion notional of options open interest expiring across US indexes, ETFs and single stocks. Investors are “scrambling” for the “under-owned right tail” according to Nomura’s cross asset desk strategist Charlie McElligott.

Meanwhile, the latest private credit headlines have a more reassuring tone, with Goldman Sachs’ global head of alternatives for wealth saying she expects private credit firms to keep drawing capital despite recent redemption episodes. That follows Blue Owl shares posting their biggest two-day gain since November 2022, and reassurances from US banks that their exposure to private credit is manageable.

Technology stocks fueled gains in Europe where the Stoxx 600 rose 0.4%. Technology and retail shares are leading gains, while telecoms and food beverage stocks are the biggest laggards. Optimism surrounding the sector got a boost after Taiwan Semiconductor Manufacturing Co. raised its revenue outlook for 2026. Here are the biggest movers Thursday:

- Entain shares rise as much as 6.6% after its first-quarter online gaming revenue grew faster than expected, offsetting weaker retail and adverse sports results, according to analysts

- Tesco shares rise as much as 3.5% after the UK’s largest supermarket chain delivered annual earnings ahead of expectations

- Mitie Group rises as much as 4.5%, touching a record high, after the support services provider delivered a trading update

- Barry Callebaut shares drop as much as 17%, hitting the lowest level since November, after the Swiss chocolate maker reported first-half earnings that missed estimates and lowered guidance for the year

- Kering shares fall as much as 4.6% after the French owner of Gucci outlined financial ambitions at its capital markets day that analysts deemed cautious

- EasyJet shares fall as much as 8.7%, the most since June 2022, as the low-cost airline forecasts a 1H26 headline pretax loss of between £540 million ($733 million) and £560 million

- Heidelberger Druckmaschinen shares drop as much as 9.2%, pulling back from a two-month high, after the printing press maker issued a profit warning

Earlier in the session, Asian tech stocks also climbed to a record high, while Taiwan’s total market cap topped $4.1 trillion to overtake the UK. Asian markets rose, with a key regional benchmark on course for a third-straight day of gains, on optimism over corporate earnings and a potential US-Iran ceasefire extension. The MSCI Asia Pacific Index advanced as much as 1.5%, with Samsung Electronics and Alibaba among the biggest boosts. Technology stocks led gains, with a sector gauge climbing to a new record high. South Korea’s Kospi, Japan’s Nikkei 225 and Hong Kong’s Hang Seng Tech Index rose more than 2% each, while Taiwan’s total market cap climbed above $4.1 trillion to overtake the UK. Investors are renewing their interest in the artificial intelligence theme with support from resilient earnings at Asian tech hardware makers. At the same time, an outlook for an eventual end to the Middle East conflict and tamer energy prices is gaining traction. Among key moves, EV battery maker CATL climbed more than 10% in Hong Kong after better-than-expected earnings. Meanwhile, chip giant TSMC raised its revenue outlook for 2026, an upbeat forecast that underscores the resilience of AI chip demand.

In FX, the Bloomberg Dollar Spot Index is up 0.2% and on course to snap an eight-day losing streak. The kiwi is the laggard among the G-10’s, falling 0.4% against the greenback. The pound falls 0.2% having derived little support from stronger-than-expected UK GDP data.

In rates, treasuries are slightly richer across the curve with gains led by the front-end and belly, supported by a wider bull steepening move seen across European bonds with oil prices steady. US yields lower by up to 2bp across front-end and belly with 2s10s, 5s30s spreads steeper by around 0.5bp and 1.2bp on the day. US 10-year trades around 4.265%, richer by 1.5bp on the day with bunds and gilts outperforming by 1.5bp and 1bp in the sector. In Europe, both UK and German 2-year yields outperform, richer by over 5bp on an outright basis, follows UK manufacturing data printing lower-than-expected. The US session includes weekly claims and a couple of Fed speakers.

In commodities, brent crude futures climb 1.6% to around $96.40 a barrel. European government bonds gain, led by the short-end as traders pare bets on interest rate hikes by the Bank of England and European Central Bank this year. UK and German 2-year yields fall 4 bps each. Precious metals advance, although are off their best levels.

Today’s US economic data calendar includes April New York Fed services business activity, Philadelphia Fed business outlook, weekly jobless claims (8:30am) and March industrial production (9:15am). Fed speaker slate includes Williams (8:35am) and Miran (10:35am)

Market Snapshot

- S&P 500 mini +0.1%

- Nasdaq 100 mini +0.3%

- Russell 2000 mini little changed

- Stoxx Europe 600 little changed

- DAX little changed

- CAC 40 +0.3%

- 10-year Treasury yield little changed at 4.28%

- VIX little changed at 18.14

- Bloomberg Dollar Index little changed at 1193.41

- euro -0.2% at $1.178

- WTI crude +1.7% at $92.84/barrel

Top Overnight News

- Pakistan is stepping up efforts to ensure the US and Iran prolong a ceasefire that’s set to end next week, allowing more time for the warring sides to negotiate a lasting peace deal. The US and Iran are considering a two-week ceasefire extension, according to a person familiar with the matter, with neither side desiring to restart fighting. BBG

- The Trump administration wants automakers and other American manufacturers to play a larger role in weapons production, reminiscent of a practice used during World War II: WSJ

- Energy Secretary Chris Wright and Interior Secretary Doug Burgum will urge the heads of top U.S. oil and gas companies in a call Thursday to increase drilling in a bid to lower oil prices. Politico

- China’s economy picked up speed early in 2026, riding an export surge before the Iran war sent energy costs soaring and put global demand – vital to Beijing’s growth ambitions – at risk. The 5.0% year-on-year pace in the first quarter sits at the top of China’s full-year target range of 4.5%-5.0%, highlighting a resilience that sets it apart from much of Asia, helped by ample strategic oil reserves and a diversified energy mix. RTRS

- Australian employment rose by 17,900 in March, missing expectations and driven entirely by full-time roles, while the jobless rate held at 4.3%. BBG

- The UK economy grew 0.5% in February, beating estimates to post its strongest monthly reading since January 2024. Activity was boosted by the services sector, though the data predate the Iran war. BBG

- Policymakers at the European Central Bank are leaning toward keeping interest rates unchanged this month, postponing their verdict on whether the fallout of the Iran war warrants a response. BBG

- Senator Thom Tillis is blocking Trump’s Fed chair nominee, Kevin Warsh, until the Justice Department drops an investigation into Powell. And the stalemate is leaving him in limbo with no clear off-ramp in sight. Politico

- Anthropic’s Mythos is so skilled at hacking that access is tightly controlled. The system’s ability to autonomously find and exploit vulnerabilities is forcing banks and governments to rethink cybersecurity. BBG

- Foreign holdings of Treasuries soared to a record $9.49 trillion in February. Canada led with a $50.5 billion increase, while Japan remained the largest holder. BBG

Iran Conflict

- The Trump admin’s goal is to bring both sides to the brink of an overarching deal to end the conflict that can then be pushed over the finish line in a second face-to-face meeting, according to ABC, citing officials. The officials acknowledge that technical talks to hammer out the fine details and implementation of the arrangement will likely take longer to complete, perhaps eventually necessitating an extension of the initial ceasefire, but that pushing back the truce’s expiration date isn’t a top priority for the administration at the moment.

- US President Trump told guests Monday night he wants to bring the war in Iran to a swift end; said only way to get Iran back to negotiating table was to increase the pressure, according to WSJ citing officials at the dinner.

- US President Trump posted “Trying to get a little breathing room between Israel and Lebanon. It has been a long time since the two leaders have spoken, like 34 years. It will happen tomorrow. Nice!”.

- Pakistani Army Chief is heading to the US on Friday as part of mediation efforts between the US and Iran, Al Jazeera reported citing a Pakistani security source.

- Pakistan’s Foreign Ministry said the US and Iran are willing to hold talks and the process is continuing but no date decided for next round of US-Iran talks.

- A military advisor to the Islamic Revolution Leader said Iranian Armed Forces’ launchers are ready to hit American warships and sink all of them, Press TV reported.

- A senior Iranian official said the fate of Iran’s highly enriched uranium and the duration of its nuclear restrictions remain unresolved, adding that fundamental disagreements persist over nuclear issues. Iranian official said there are greater hopes for extending the ceasefire and holding a second round of talks after the trip, adding that the Pakistani army chief’s visit to Iran helped reduce differences in some areas.

- Iranian officials will meet with Pakistan’s army chief on Thursday in Tehran and will discuss US proposals, according to TASS.

- Iran and the Pakistani mediator will discuss details of the messages exchanged between Tehran and Washington tomorrow, Thursday; via Al Jazeera citing Iranian TV.

- Journalist Abas Aslani posted source said Iran-US talks are far less positive [than reported] due to contradictory US stances & Israeli spoiler efforts, media push hyping success of talks is a PR manoeuvre to calm markets and shield Trump from pressure.

- Iran’s ambassador to Pakistan said Islamabad is the sole venue for Iran–US talks.

- Diplomatic sources suggest that “Washington is pressing forcefully to cool down the Lebanese front”, via Kan’s Kais; “Second round of negotiations between Israel and Lebanon will take place in Washington soon”. “Second round of negotiations between Israel and Lebanon will take place in Washington soon, and that the current contacts are focused on achieving a temporary ceasefire that will lay the groundwork for ending the war.”

- Two Israeli officials said the meeting of the political security cabinet ended without a decision on a ceasefire in Lebanon, according to Axios’s Ravid.

- Israeli media citing informed sources state that a ceasefire in Lebanon will not happen soon despite Trump’s statements.

- Israeli army has not received any instructions so far to prepare for a ceasefire in Lebanon, via Al Arabiya citing local reported.

- Lebanese officials say a ceasefire between Israel and Lebanon is expected ‘soon’, according to FT.

- The next meeting between Israel and Lebanon is expected to be held early next week, via Sky news Arabia citing Israel Hayom.

- Iran’s Interior Minister has ordered border governors to neutralise the threat of a naval blockade by strengthening and developing border trade by increasing imports of basic goods and exports of goods, utilising all national and regional capacities.

- Iranian politician affiliated with Resistance Front of Islamic Iran, Mohsen Rezaei said they will not leave the Strait of Hormuz until the full realisation of Iran’s rights, adds that this time, Iran has set preconditions.

- Iranian Parliament Speaker Ghalifbaf said US should withdraw from ‘Israel first’ mistake and must comply with agreement, also said resistance and Iran are one soul both in war and ceasefire.

- Hezbollah fires long-range missiles at Tel Aviv, according to Defapress.

- Iranian military affiliated outlet Defapress claims that four ships broke the US naval blockade over the past 24 hours, citing satellite data.

- Israeli warplanes carried out a strike on the town of Shihabiya in southern Lebanon.

- US Central Command said US blockade has turned back 10 vessels in the Strait of Hormuz today.

- China’s Foreign Minister Wang Yi stressed to Iran that the Strait of Hormuz needs to reopen and stressed freedom of navigation in Hormuz, while he said Hormuz reopening is a unanimous call from the international community.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly gained following the positive lead from Wall Street, where the S&P 500 and Nasdaq printed fresh all-time highs, amid tech strength and peace talk optimism. ASX 200 bucked the trend and gave back initial gains, and more, as notable outperformance in tech was offset by losses in energy, resources, materials, financials and miners. Nikkei 225 rallied to a fresh record high after reclaiming the 59,000 status amid the hopes for a Middle East resolution and with the index led by the momentum in tech stocks. Hang Seng and Shanghai Comp were higher with further upside seen as the dust settled following the mixed Chinese GDP and activity data, in which GDP growth for Q1 missed expectations, but GDP Y/Y topped forecasts and printed at the high-end of China’s official 2026 GDP growth target. Meanwhile, Industrial Production data for March was better-than-expected, but Retail Sales disappointed.

Top Asian News

- Japan’s top FX diplomat Mimura said told US Treasury Secretary Bessent will upgrade FX developments as needed, and both sides agreed to coordinate closely on FX.

- Japanese Finance Minister Katayama said regarding exchange rates, agreed to further intensify communication with US Treasury Secretary Bessent.

- Japanese Finance Minister Katayama said many central bankers are adopting a wait-and-see stance, as raising interest rates could have a negative impact on the economy, adds it is impossible to predict when the current situation ends and spillover effects.

- Senior Japanese Financial Regulator official said Japan sees private credit as potential pillar in new strategy to meet corporate funding demand driven by M&A surge, according to reported.

- China NBS said the economy had a good start in Q1, but the external situation is becoming more complex, adds China is to expand domestic demand and optimise supply. China will implement proactive macro policies. Expects a complex, volatile external environment. China will consolidate economic recovery foundation. Sees mixed signs of strong supply and weak demand.

- Deutsche Bank upgrades China’s 2026 real GDP growth to 4.9% (prev. 4.5%).

- Barclays raises China 2026 GDP growth view to 4.6% (prev. saw 4.0%).

European bourses (STOXX 600 +0.2%) are broadly gaining, albeit only modestly. The CAC 40 is the outperformer, rebounding from Wednesday’s luxury-driven selloff. The FTSE 100 is also slightly higher this morning, after UK GDP came in far stronger than expected in February (0.5% vs exp. 0.1%). Sectors point to a positive bias. Top of the pile lies Technology, supported by strong TSMC earnings, which has lifted peers such ASML. Telecoms is the underperformer, with a downgrade for Telia weighing on the broader sector.

Top European News

- EU Inflation Rate MoM Final (Mar) M/M 1.3% vs. Exp. 1.2% (Prev. 0.6%, Low. 1.2%, High. 1.2%).

- EU Inflation Rate YoY Final (Mar) Y/Y 2.6% vs. Exp. 2.5% (Prev. 1.9%, Low. 2.5%, High. 2.6%).

- EU Core Inflation Rate YoY Final (Mar) Y/Y 2.3% vs. Exp. 2.3% (Prev. 2.4%).

- UK Balance of Trade (Feb) -0.720B vs. Exp. -3.6B (Prev. 3.922B).

- UK Goods Trade Balance (Feb) -18.79B vs. Exp. -20.2B (Prev. -14.45B, Low. -20.5B, High. -14B).

- UK GDP YoY (Feb) Y/Y 1.0% vs. Exp. 1.0% (Prev. 0.8%).

- UK GDP MoM (Feb) M/M 0.5% vs. Exp. 0.1% (Prev. 0%, Low. 0.0%, High. 0.3%).

Trade/Tariffs

- UK Europe Minister Nick Thomas-Symonds is expected to offer an update on the state of play in negotiations; EU Trade Chief Sefcovic, and European Parliament President Roberta Metsola, will also provide keynotes, reported Politico.

- USTR Greer said US-China Board of Investment is to be a government forum, adds there’s no situation where there’s no trade between US and China, also said the Trump admin wants to be pragmatic regarding China.

FX

- DXY edged higher throughout the entirety of the European session following punchy Iran rhetoric. The index marked a session high of 98.21, rising from its earlier trough of 97.83 made in Asia. (Full Middle East analysis on the headline feed) As it stands, both US and Iran continue communication, but there is no confirmation yet on second-round talks or a ceasefire extension – not to mention Lebanon, which remains a key point. Aside from geopolitics, POLITICO reported this morning, “a growing chorus of Republicans, eager to install Warsh, are joining the call for the administration to end the probe” into Fed Chair Powell. This comes ahead of Warsh’s hearing next week. The session ahead sees remarks from Fed’s Williams (voter), who will speak at a Federal Home Loan Bank of New York event, while Miran (voter, dovish dissenter) will speak on the global outlook.

- GBP knee-jerked higher on a stronger-than-expected UK GDP report from February, but now trades with very mild losses given the Dollar strength this morning. In brief, on a monthly basis, GDP rose 0.5%, while yearly saw an increase of 0.1%. This set of metrics did not encapsulate the US-Iran war and as such, MPC members will likely refer to the second-round effects of the energy shock before opting to adjust rates. Cable continues to trade towards recent highs and is essentially at pre-war levels. The pair attempted to breach 1.36, a rally which faltered at 1.3594.

- Antipodeans trade mixed. While Aussie is a touch firmer against a resilient USD following jobs data – Kiwi sits at the bottom of the pile as bets for RBNZ tightening pare a touch with markets implying 77bps of easing by year end (prev. c. 83bps). NZD/USD began falling in Asia, though losses extended throughout the European morning to trade at session lows of 0.5893, the move likely to face support @ 0.5892.

- JPY had a choppy overnight session with USD/JPY marking a session low of 158.27 after successful jawboning from Finance Minister Katayama; she told G7 members that Japan was watching FX with a high sense of urgency. She also reiterated close communication with the US Treasury. This, as is typically the case with the Japanese Finance Ministry, indicates officials are uncomfortable with the extent of JPY weakness, with JPY nearing the key 160 mark. Since these comments, JPY pared the entirety of the strength Katayama gave to the haven, pressured by the gains in the USD.

Central Banks

- ECB officials are said to be leaning towards an April rate hold.

- ECB’s Schnabel said that the memory of high inflation remains fresh, and inflation expectations could be more fragile. Can afford to take time to analyse the Iran shock. We are in a relatively favourable position because we were successful in bringing down inflation to 2% before the war started, have monetary policy stance that is broadly neutral. To carefully consider data that may indicate inflation becoming entrenched or having second-round effects.

- ECB’s Demarco said policymakers must be patient on rate decisions, but warns an adverse scenario could materialise; adverse scenario could require two rate hikes; longer-term inflation expectations anchored.

- ECB’s Muller said rate move at April meeting still cannot be ruled out, adds may not have all the data this month to determine if interest rates will have to be raised to tame an inflation surge and June meeting will offer greater body of information. No hard evidence of second-round effects of inflation.

- Goldman Sachs expects the ECB to deliver 25bp rate hikes in June and September 2026 (prev. saw hikes in April and June). Analysts expect energy prices to remain persistently high through 2026, significant pass-through into inflation is likely in coming months and ECB’s communication has remained largely hawkish on the path ahead.

Fixed Income

- Global fixed benchmarks opened the European session with a positive bias, but have gradually edged off best levels as the risk tone deteriorated as the morning progressed. Initial optimism was facilitated by comments from both Israeli and Lebanese officials, who said that a ceasefire is expected soon, and talks are expected to continue in the near-term. On the Iranian front, President Trump said that “he wants to bring the war in Iran to a swift end”. Thereafter, in early morning trade, a military advisor to the Islamic Revolution Leader said Iranian Armed Forces’ launchers are ready to hit American warships and sink all of them – a comment which weighed on the risk tone at the time, leading to upside in the crude complex, which pressured global fixed paper.

- USTs are firmer by a couple of ticks and currently trades at the lower end of a 111-11 to 111-17 range. Ultimately, moving at the whim of geopolitical developments, with markets now awaiting clear details on when/if the second round of Iran-US talks will begin. From a domestic perspective, weekly initial jobless claims (215k expected from 219k) and continuing claims (exp. 1.84mln from 1.794mln), NY Fed services activity, Philly Fed manufacturing are all due.

- Bunds are firmer by around 15 ticks and currently trade within a 125.32 to 125.62 range. German paper, as above, is off its best levels as the risk tone slipped a bit. Domestic newsflow has been fairly limited this morning, aside from an updated Goldman Sachs call for the ECB; analysts now expect the ECB to deliver 25bps rate hikes in June and September 2026 (prev. saw April and June), citing expectations that energy prices will stay high through 2026, feed through materially into inflation in the coming months and keep ECB communication largely hawkish. As it stands, money markets fully price in a 25bps hike in July. Focus later will be on the ECB Minutes (Mar), where the Bank kept rates steady – traders will be cognizant of any commentary pertaining to the Middle East situation.

- Gilts are incrementally lower and trade within an 88.68 to 89.07 range. Slightly underperforming vs peers, given the hawkish impulses from a stronger-than-expected UK GDP report. In brief, on a monthly basis, GDP rose 0.5%, while yearly saw an increase of 0.1%. ING writes “UK output surged in February, but it’s in line with a trend dating back to 2022, where growth is stronger in the first quarter than across the rest of the year. We’re taking this latest data with a pinch of salt”.

Commodities

- Regional mediators are actively working to extend the US-Iran ceasefire and secure a second round of talks, with both sides agreeing in principle to reconvene, though no date or venue has been set. The Trump administration is pushing a two-stage strategy: use sustained economic and military pressure to force Iran toward the brink of a broader deal, then finalise it in a follow-up face-to-face meeting, with technical negotiations on implementation likely to extend beyond the current truce. A senior Iranian official said the fate of Iran’s highly enriched uranium and the duration of its nuclear restrictions remain unresolved, adding that fundamental disagreements persist over nuclear issues.

- Pakistan has taken a central mediation role, coordinating messages between Tehran and Washington and engaging both politically and militarily, although officials confirm no timeline has been agreed for the next round. Despite publicly downplaying the need for a ceasefire extension, US officials acknowledge it may ultimately be required to keep negotiations alive as talks progress.

- Crude prices edged higher following yesterday’s losses as traders feel the ceasefire could be prolonged and negotiations restarted. Brent Jun holds above USD 95/bbl this European morning (in a USD 94.43-96.85/bbl range) while WTI Jun sits in a 87.32-89.82/bbl parameter.

- Spot gold trades modestly higher, just above USD 4,800/oz and well within yesterday’s USD 4,786-4,871/oz range. Base metals are flat/positive with 3M LME copper holding above USD 13k/t in a current USD 13,281.00-13,376.58/t range. Overnight data showed China’s Q1 growth accelerated on strong exports (Y/Y printed at the top end of China’s 2026 target of 4.5-5%), while March retail sales rose but slowed from February; analysts said the Iran war still poses risks to the outlook.

- Australia said it secures 100mln litres extra of diesel from Brunei and South Korea.

- Repsol (REP SM) is set to take back operational control of its Venezuelan oil assets and boost production following an agreement with the country’s government, according to FT.

- White House is expected to urge heads of oil and gas companies to increase drilling, according to POLITICO.

- Australia’s Energy Minister reported that a fire at Viva Energy’s (VEA AT) refinery is still not under control, while diesel and jet fuel output continues, but refinery fire may hit petrol production more.

Geopolitics (ex Iran)

- Ukrainian President Zelensky posted “there can be no normalization of Russia as it is today. Pressure on Russia must work”, following heavy drone attacks, via X.

- Explosions reported in Ukraine’s capital, Kyiv, while the Mayor said air defence systems have been activated

US Event Calendar

- 8:30 am: United States Apr 11 Initial Jobless Claims, est. 213k, prior 219k

- 8:30 am: United States Apr Philadelphia Fed Business Outlook, est. 10, prior 18.1

- 8:30 am: United States Apr 4 Continuing Claims, est. 1810k, prior 1794k

- 9:15 am: United States Mar Industrial Production MoM, est. 0.1%, prior 0.2%

- 9:15 am: United States Mar Capacity Utilization, est. 76.3%, prior 76.3%

- Individual investors are once again snapping up so-called “meme” stocks, an early sign that retail’s animal spirits are returning to the US equity market after the mid-month tax deadline and as geopolitical tensions abate.

Central Bank speakers

- 8:35 am: United States Fed’s Williams Gives Keynote Remarks

- 10:35 am: United States Fed’s Miran Speaks in Moderated Discussion

DB’s Jim Reid concludes the overnight wrap

I’m back in the hotseat this morning after a holiday which saw the temperatures on the slopes range from -20 degrees at the start to +25 degrees by the end. It was truly remarkable. Just as I was driving home, I then picked up the most virulent form of man-flu which knocked me out for a few days, including any desire to have early EMR starts this week. All I could do over the weekend was lie on the sofa and watch 30 hours of Masters’ golf coverage. It was brutal. I’ll leave you to assess whether there was sympathy at home or not.

Just as I went on holiday, on March 30th the S&P 500 closed at 6343.7 and at an 8-month low. Fast forward 11 business days and we closed last night above 7,000 (+0.80% at 7,023) for the first time, some +10.71% higher and at record highs. Few would have believed this was possible at the time, but this episode has been a high beta version of the usual geopolitical playbook where the negative impact on average lasts 15 days and the full recovery usually takes another 15-20 days. In this example the decline was slightly beyond the 75th percentile through history and the trough took a week longer to arrive than the average but the recovery took a week or so less. However, the geopolitical playbook has broadly worked.

The rally is continuing in Asia this morning with the Nikkei (+2.06%) leading the gains and hitting fresh all-time highs on the back of technology and chip-related stocks. The KOSPI (+1.64%) is also rising significantly, back to around +47% YTD. Elsewhere the Hang Seng (+1.38%), CSI (+0.90%), and the Shanghai Composite (+0.53%) are all higher after a decent monthly dump of data this morning (details below). The S&P/ASX 200 (-0.34%) is a rare decliner. S&P 500 (+0.15%) and Nasdaq (+0.26%) futures are continuing to edge up.

Coming back to China, GDP grew +5.0% year-on-year in the first quarter, surpassing forecasts of a +4.8% increase and showing an improvement from +4.5% in the preceding quarter. Additional data on economic activity released presented a mixed yet still resilient outlook, as industrial production increased by +5.7% in March compared to the same month last year, exceeding expectations of a +5.3% rise. However, retail sales advanced by +1.7% in March, falling short of the anticipated +1.9% increase, thereby underscoring ongoing weakness in domestic demand. New home prices continued their downward trend, decreasing by -0.21% in March, following a -0.28% decline in the previous month. So the property slump continues.

When it comes to the latest move higher, risk assets took their cue to continue to climb yesterday after the AP reported that the two sides were “in principle” in agreement on extending their April 7 truce, with Bloomberg later reporting that a two-week extension was being considered. So that raised hopes about a more durable ceasefire. White House Press Secretary Leavitt said that the sides remained locked in negotiations but that the US had not “formally requested an extension of the ceasefire.” On the Iranian side there was some optimism for a deal on the back of comments from Iranian Foreign Ministry spokesman Baghaei who told reporters that while the country’s right to peaceful use of nuclear energy “cannot be revoked”, the level and type of enrichment is “negotiable”.

As well as the new record for the S&P 500, the Nasdaq (+1.59%) reached a record of its own as the Mag 7 saw even larger gains (+2.48%). Technology and Consumer-oriented cyclicals drove the S&P gains again, with Autos (+6.59%), Software (+4.29%), Tech Hardware (+1.57%), and Consumer Services (+1.42%) the major outperformers, while commercial-oriented cyclicals lagged such as Cap Goods (-1.73%) and Materials (-1.29%).

Alongside the news from the Middle East, positive earnings helped to support US equities, with both Morgan Stanley (+4.52%) and Bank of America (+0.97%) advancing after their latest results. Coupled with other positive surprises, that’s helped to underscore the narrative of ongoing US economic strength, despite the recent surge in energy prices. Private credit concerns have also seen a couple days of respite as the two-day move in Blue Owl Capital is now over +17%, the biggest two-day rally since late-2022 after the company’s shares fell to its lowest publicly traded level last Friday.

Meanwhile, markets were intrigued by the story that US shoe brand AllBirds surged by +582% after it announced that it would rebrand as an AI compute business. From sneakers to servers, laces to latency, footware to firmware, comfort to compute! Bet you wish I was back on holiday or on the sofa!

In fixed income, treasury yields also rose after officials questioned the case for rate cuts. For instance, Cleveland Fed President Hammack said that her baseline was to keep rates on hold for a good while, and even Treasury Secretary Bessent said that he would “understand if the Fed needs to wait on rate cuts” even if he ultimately saw large cuts beyond that. So that helped yields to rise across the curve, with the 10yr yield (+3.6bps) rising to 4.283%, whilst the 2yr yield (+1.7bps) rose to 3.76%. This comes as Fed futures are again not pricing in a full Fed cut over the next 12 months. The latest data also supported those rate moves, with the Empire state manufacturing index for April up to a 5-month high of 11.0 (vs. 0.0 expected).

Earlier in Europe, equities were more subdued, particularly after some more negative earnings reports came through. That included French companies Kering (-9.29%) and Hermes (-8.22%), which weighed on the CAC 40 (-0.64%). And ASML also fell -4.22%, despite raising its full-year sales forecast. So equities took a hit across the continent, with the STOXX 600 (-0.43%) falling back, despite the more positive headlines about potential US-Iran talks.

Sovereign bonds also lost ground, with yields on 10yr bunds (+2.0bps), OATs (+2.4bps) and gilts (+3.4bps) moving higher. However, expectations for an imminent ECB rate hike continued to decline, with pricing for an April hike down to a one-month low of 23.9% at the close yesterday. 58.3bps of hikes were priced in by year end at yesterday’s close, down from 81bps on March 24th.

Markets generally continue to trade on optimism that the conflict will ultimately be sorted out in weeks even if the current situation in the Strait of Hormuz remains unchanged. The US naval blockade is far from over, with US Central Command posting on X yesterday that no vessels have been able to make it past US forces, with 9 vessels complying with US direction to turn back to Iran.

Trump also announced that President Xi had given him a call, later posting that China is “very happy” that he is “permanently opening up” the Strait of Hormuz, and have agreed to not send their weapons to Iran. His post followed an earlier FT report that Iran had secretly acquired Chinese spy satellite to target US military bases across the Middle East during the conflict.

Finally, Australia’s labour market data showed that the unemployment rate remained unchanged at 4.3% in March. Meanwhile, employment experienced a modest increase of 17,900, compared to the anticipated 20,000, for the month. Firms contributed by adding 52,500 full-time positions, indicating a degree of underlying resilience despite a slight slowdown in hiring. This data emerges as the RBA cautions that it may be necessary to further increase interest rates in the upcoming months to mitigate inflation, which is already significantly above the target and poses a risk of rising even higher.

To the day ahead now, data releases include the US April New York Fed services business activity, Philadelphia Fed business outlook, March industrial production, and initial jobless claims. We’ll also get the ECB’s account of the March meeting, and hear from the Fed’s Williams and Miran, the ECB’s Schnabel, Kazaks, Rehn and Kocher, and the BoE’s Taylor.

Tyler Durden

Thu, 04/16/2026 – 08:45

via ZeroHedge News https://ift.tt/x0aFPvU Tyler Durden