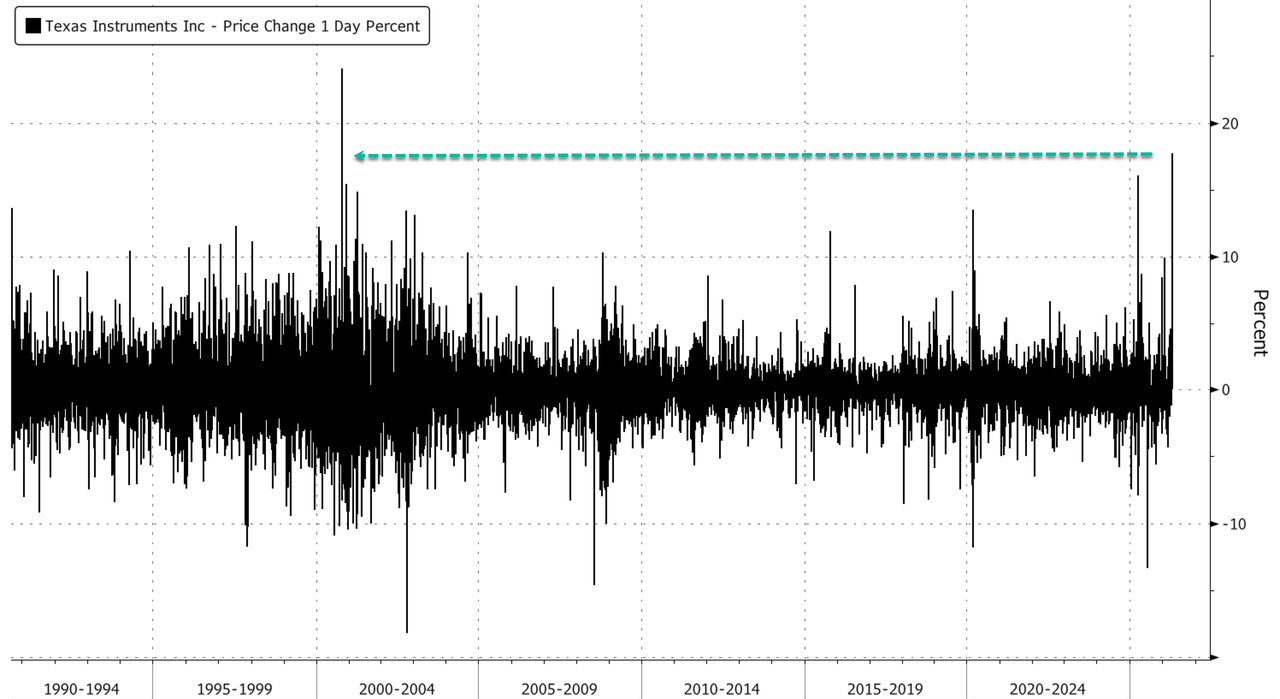

Texas Instruments Jumps Most Since Dot-Com On Upgraded Outlook; Goldman Sees Analog Recovery

Shares of Texas Instruments jumped the most since the Dot-Com bubble era after the chipmaker issued a stronger-than-expected second-quarter forecast, signaling that demand is rebounding across industrial markets and data centers. Goldman analysts told clients the guidance suggests the “analog recovery is continuing.”

Revenue guidance of $5 billion to $5.4 billion and profit guidance of $1.77 to $2.05 a share both came in well above the Bloomberg Consensus estimate of estimate $4.85 billion, while first-quarter results also beat expectations.

Here’s a snapshot of first-quarter results (courtesy of Bloomberg):

EPS $1.68 vs. $1.28 y/y, estimate $1.38

Revenue $4.83 billion, +19% y/y, estimate $4.53 billion

- Analog revenue $3.92 billion, +22% y/y, estimate $3.68 billion

- Embedded processing revenue $723 million, +12% y/y, estimate $683 million

- Other revenue $178 million, -16% y/y, estimate $168.7 million

Operating profit $1.81 billion, +37% y/y, estimate $1.54 billion

Capital expenditure $676.0 million, -40% y/y, estimate $689.9 millio

Free cash flow $1.40 billion, estimate $1.2 billion

R&D expenses $510 million, -1.4% y/y, estimate $530.7 million

Cash and cash equivalents $3.55 billion, +28% y/y, estimate $3.25 billion

CEO Haviv Ilan told analysts on an earlier call that the resurgence in demand for industrial components was broad-based across all geographies and segments. He added that while the company’s revenue remains below its previous peak, that’s only spurring optimism that upside momentum will continue.

“There is a lot of room to grow,” Ilan said. “I saw it across all sectors in industrial.”

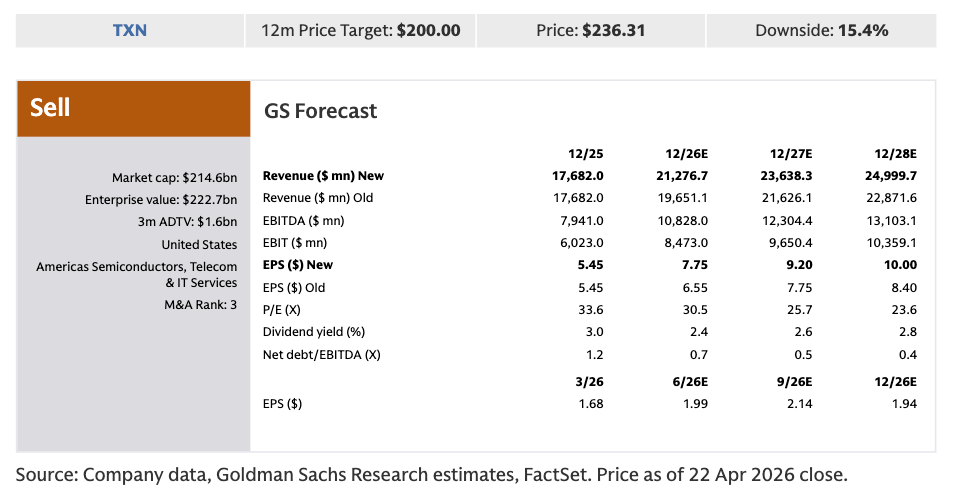

Institutional commentary from Goldman analyst James Schneider had some very positive takeaways from earnings:

Key stock takeaways: We expect the stock to trade higher following a quarter and guidance that came in well above the Street. We believe expectations were somewhat elevated given management’s constructive commentary at recent conferences, and based on our conversations we believe most investors were positioned more constructively ahead of the quarter.

We see the strong recovery in the industrial end market as a particularly encouraging read-across for the sector. Although we continue to see a recovery across the analog sector (including for TI), we believe peers have managed their inventory levels far more proactively — and hence we believe gross margins are likely to recover much faster for peers (along with significant upward earnings revisions) than for TI.

We continue to have a preference for peers (including Microchip, NXP, and Analog Devices) who are likely to see greater upward earnings revisions in the near term, and we retain our relative Sell rating on TXN given the ongoing gross margin headwinds we expect in the coming quarters.

Schneider continued:

Read-through to our coverage: We expect a positive initial reaction for the analog group, with the most direct read-across for MCHP (Buy) and ADI (Buy) given their relatively high industrial exposures.

He raised Goldman’s 12-month price target to $200 from the previous $175 and maintained a “sell” rating:

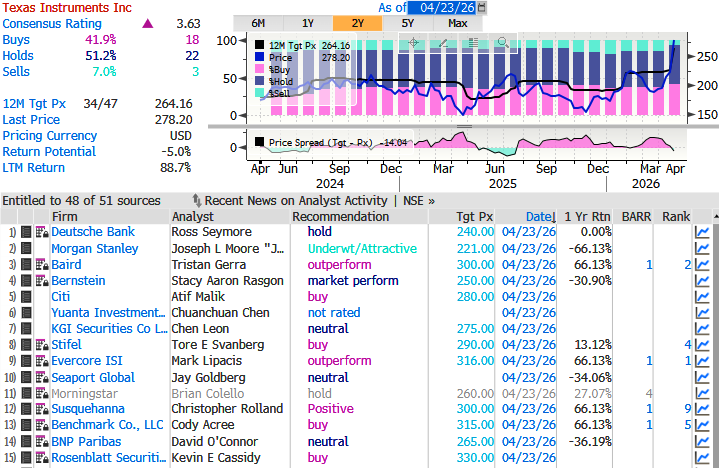

Here’s what other institutional desks are saying:

Barclays (raised to equal-weight from underweight, PT to $250 from $175)

-

Upgrade reflects multiple quarters of growth in the company’s Industrial business

-

While a lot seems baked into the stock, “Industrial exposure is the place to be in Analog today”

BofA Global Research (raised to buy from neutral, PT to $320 from $235)

-

Upgrades rating after solid 1Q earnings on “industrial strength, data center power content, and US-based manufacturing”

-

“Pricing has not been a factor, but could offer incremental good news in 2H which we conservatively model below seasonal trends”

Truist Securities (hold, PT $225)

-

The results show broad-based upside, including “strong cash flow performance”

-

“Capital allocation was constructive for equity”

-

The outlook is better than expected

Bloomberg Intelligence

- “Texas Instruments’ 1Q results and 2Q outlook significantly beat consensus, solidifying a robust and broad recovery across its industrial markets, likely aided by new data-center sales”

Evercore ISI (outperform, PT to $316 from $270)

- The results were better than expected, while the outlook is “above seasonal”

Citi (buy, PT to $280 from $235)

- The results are strong, while the outlook is “well above seasonal”

Bloomberg Consensus Breakdown:

Traders rewarded Texas Instruments for its upgraded earnings outlook with buying panic mania on Thursday.

Shares in late-afternoon trading were up nearly 20%, the largest intraday move since the 24% gain on October 19, 2000.

Shares are in bluesky breakout territory:

Professional subscribers can read Goldman’s TI takeaway here at our new Marketdesk.ai portal

Tyler Durden

Thu, 04/23/2026 – 17:25

via ZeroHedge News https://ift.tt/PBZitRw Tyler Durden