Futures, Yields And Oil All Rise As Trump Arrives In China

US equity futures are up (alongside oil and yields, go figure), reversing yesterday’s modest losses, as optimism around the earnings potential of AI outweighs concerns over hot inflation readings bringing dip buyers back to drive tech stocks higher, with traders betting that the tech rally has further room to run while also hoping on good news from the Trump-Xi summit set to start today in Beijing. As of 7:30am ET, S&P futures were up 0.2% and Nasdaq futures rose 0.7% thanks to a rebound in Semi stocks in the Asian and EMEA sessions. In premarket trading, semis are bid as yesterday’s dip buyers appear to be once again rewarded. NVDA is up 2.5% as CEO Huang joining Trump’s China trip. Chip and memory sotcks, the key drivers of the past month’s narrow rally in the artificial-intelligence trade, posted broad gains. While there were no material updates on US / Iran, today attention shifts elsewhere as Trump’s China trip kicks off (with both Elon and Jensen on board AF1); the President appears to be in deal-making mode and China is said to oppose SoH tolls, though the Middle East is not expected to be a focal point. The dollar climbed 0.2% as commodities are mixed with strength in Ags and copper, while oil is unchanged erasing all of its overnight losses. Mag7 names underperforming broader indices as Cyclicals ex-Energy are outperforming. Today’s macro data focus is on PPI following the hawkish CPI print yesterday

In premarket trading, Mag 7 stocks are mixed: Nvidia up 2.4% as CEO Jensen Huang joins President Donald Trump on his visit to China.

(Tesla +1.2%, Alphabet +0.4%, Amazon +0.3%, Meta -0.1%, Microsoft -0.2%, Apple -0.3%)

- Chipmakers, opticals and storage firms gain as supply for global memory chips, key to AI infrastructure build-outs, tightens further. The sector is also getting a boost from Huang’s trip to China.

- Arteris Inc. (AIP) gains 24% after the semiconductor company’s first-quarter revenue beat estimates and it raised its full-year revenue guidance following strong AI-driven demand.

- Karman Holdings (KRMN) is down 5.6% after the aerospace & defense company reported adjusted earnings per share for the first quarter that matched the average analyst estimate.

- Nextpower (NXT) rises 13% after the solar-equipment company raised its fiscal 2027 outlook for revenue. It also said it agreed to acquire the assets of Zigor Corp.’s power conversion business and its US based subsidiary, Apex Power.

In other corporate news, Subprime lender Goeasy adopted a shareholder rights plan as its results showed more consumer credit strain. Hedge fund Dymon Asia Capital is on track to reach $8 billion in AUM by the third quarter as more global investors seek to back Asia-based hedge funds. In AI news, Anthropic is said to be in talks to raise new capital of at least $30 billion at a $900 billion valuation. The company also warned investors to avoid a number of secondary marketplaces as unauthorized sellers of the company’s shares. AI chipmaker Cerebras Systems is said to be guiding prospective investors that it expects to prices its IPO above the top of its marketed range. Capacity constraints and a tightening supply of critical components threaten to throttle the brisk growth for China’s AI hardware suppliers, not for a lack of AI demand. SoftBank reported a surge in quarterly profit due to valuation gains on its OpenAI investment, boosting confidence at the Japanese company to bet even more on the ChatGPT maker.

Tech stocks are rallying again as investors count on the vast earnings potential of AI to withstand worries over elevated oil prices, with flows from the Middle East showing no sign of normalizing. Traders are also banking that this week’s summit between Trump and China’s Xi Jinping could unlock a series of trade deals, especially around semiconductors.

“The most difficult question for investors right now is to find hedge trades in case the war in Iran drags on and oil prices stay high,” said Marija Veitmane, head of equity research at State Street Global Markets. “The best place to hide would be companies with stronger earnings and margins, as well as highly visible and predictable earnings. All roads lead to tech.”

One of the aims from the Trump-XI meeting in China this week is to avoid another rare earth shock. However, an analysis from Bloomberg Economics sees China as likely to keep dominating rare earth supply chains through at least 2030. AI chip technology is another likely topic for discussion, especially now that Nvidia’s CEO has joined a roster of US business leaders accompanying Trump on the visit.

Higher oil costs have started to seep into consumer prices, pushing bond yields up as investors fear central bankers will have little choice but to tighten policy. Markets will get another reading Wednesday on US inflation, with producer prices expected to show the war pushing costs up throughout the supply chain.

“The PPI data today will likely confirm the spike in inflation,” said Joachim Klement, head of strategy at Panmure Liberum. “Inflation in the US is rising so quickly that even if Kevin Warsh wants to cut interest rates, he may not have any arguments to do so by the time he shows up at the Fed.”

In other assets, oil inventories are falling around the world at a record pace and will continue to drop for months, according to the IEA. Copper extended gains above $14,000 a ton, inching toward a record high seen earlier this year, as supply risks mount on mine disruptions around the world.

Looking at earnings, Dynatrace is set to report numbers before the market opens. Earnings from Cisco and Birkenstock follow later in the day. Cisco’s growth outlook for the year remains durable given stable enterprise demand and quickening investment in AI networking infrastructure, BI said.

Conferences include Bank of America global healthcare in Las Vegas and Bank of Montreal global farm to market / chemicals in New York.

In Europe, the Stoxx 600 trades higher by 0.3% rebounding from the previous session’s losses as investors parse earnings reports and track a broader rally in technology. Here are some of the biggest movers on Wednesday:

- Alstom gains as much as 5.2% after the French rolling-stock group reported its latest earnings, which analysts say is a reassuring update following its preliminary FY release on April 17, when it also withdrew its FY guidance, sending shares 27% lower on the day.

- Merck KGaA shares jump as much as 9.4%, the most in more than seven months, after the German company reported better-than-expected results for the first quarter and boosted its adjusted Ebitda forecast for the full year.

- Umicore gains as much as 15% following an upgrade to buy from neutral at Goldman Sachs, which sees clear re-rating potential for the Belgian materials technology group based on the performance of its Recycling division.

- E.On shares gain as much as 4.6% after the German power company reported first-quarter results. Analysts at Jefferies and RBC Capital tout strength in retail operations.

- Alfen surges as much as 27% after delivering first-quarter results above analyst expectations, driven by its Smart Grid and Energy Storage divisions.

- Adecco shares drop as much as 14% after the recruitment company posted a disappointing margin in the first quarter and warned this will contract in the second.

- Siemens shares fluctuate after announcement of a share buyback and results that are described as slightly disappointing by some analysts, who say strength in its core Digital Industries and Smart Infrastructure divisions was offset by a weaker margin in Mobility.

- Swatch shares fall as much as 7.6%, the most in over a year, as Oddo BHF doubts whether the pocket watch models of the Swiss watchmaker’s collaboration with Audemars Piguet will bring a sustained boost in revenue.

- Norbit drops as much as 7.4% after the Norwegian sensor technology firm reported its latest earnings. DNB Carnegie says both first-quarter results and second-quarter guidance were on the “softer side” and could lead to 6-8% cuts to full-year 2026 Ebit estimates.

- Vistry shares fall as much as 13% as the UK homebuilder cautions that first-half profit in 2026 is likely to be significantly lower than in the previous year and pauses its share buyback program.

Earlier in the session, Asian equities climbed on Wednesday, as a rally in South Korea more than offset a selloff in Taiwan. The MSCI Asia Pacific Index was up as much as 0.7%, with SK Hynix and Samsung Electronics the biggest boosts as tech sentiment was supported by news that Nvidia CEO Huang joined US President Trump’s trip to China as a last-minute addition. Alibaba’s ADR has been choppy in pre-market trade, currently lower by 1.7% after 4Q revenue fell short of estimates. Korea’s benchmark gained 2.6%, while Japanese stocks extended their advance to a third day. Investors in Asia are increasingly driven by expectations around the AI infrastructure buildout and are focused on whether the technology’s lofty promises will translate into earnings. That has largely overshadowed concerns about supply chains and energy risks stemming from the war in the Middle East.

In FX, the Bloomberg Dollar Spot Index rose 0.2%, a third day of gains, after a report on Tuesday showed the US consumer-price index rose 3.8% from a year ago.NZD/USD fell 0.5% to 0.5923, as the kiwi led G-10 losses against the dollar. EUR/USD fell 0.3% to 1.1702, a one-week low; French unemployment rose to the highest level in five years. GBP/USD slips 0.1% to 1.3522; Keir Starmer faces growing pressure to step down as Britain’s prime minister

In rates, treasuries yields are flat, with yields within about 1bp of Tuesday’s close, with oil prices steady. US 10-year yield near 4.46%, 2-year near 3.99% are little changed, with UK 2-year about 2bp lower on the day. Gilts outperform in choppy session, though gains were trimmed after report that cabinet minister Wes Streeting is preparing to trigger a leadership contest. Focal points of US session include April PPI data and $25 billion 30-year new-issue bond auction. Treasury refunding auctions conclude with $25 billion 30-year bond sale at 1pm New York time, following tails for 3- and 10-year notes over past two days. WI 30-year yield near 5.02% is 14.4bp cheaper than last month’s, which tailed by 0.5bp. IG dollar issuance slate includes a couple of offerings so far. Twelve companies priced a combined $15.6 billion of debt Tuesday, paying about 3.8 basis points in new issue concessions on deals that were 4.3 times covered. Two companies opted to stand down and are expected to try again Wednesday after PPI release

In commodities, WTI crude oil futures are little changed, hold recent gains around $102 as Middle East tensions simmer and global stockpiles shrink at a record pace. Brent, meanwhile, fluctuated around $108 a barrel after rising more than 8% over the past three sessions. Oil inventories are falling around the world at a record pace and will continue to drop for months, the International Energy Agency said.. Spot gold trades down 0.4% as silver adds 0.5%. Bitcoin up 0.3%.

Economic data slate includes April PPI at 8:30am. Fed speaker slate includes Collins (11:30am), Kashkari (1:15pm) and Logan (7pm)

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.8%

- Russell 2000 mini +0.2%

- Stoxx Europe 600 +0.5%

- DAX +0.6%

- CAC 40 -0.2%

- 10-year Treasury yield little changed at 4.46%

- VIX -0.1 points at 17.94

- Bloomberg Dollar Index +0.2% at 1194.95

- euro -0.4% at $1.1696

- WTI crude -0.7% at $101.47/barrel

Top Overnight News

- The discussions about possibly replacing “Operation Epic Fury” with “Operation Sledgehammer” underscore how seriously the administration is considering resuming the war started on Feb. 28, and could allow Trump to argue that it restarts the 60-day clock that requires congressional authorization for war. NBC

- U.S. Intelligence Shows Iran Retains Substantial Missile Capabilities. Secret new assessments say Iran has operational access to 30 of its 33 missile sites along the Strait of Hormuz, suggesting that its military remains far stronger than President Trump has asserted. NYT

- Both Iraq and Pakistan have cut deals with Iran to ship oil and liquefied natural gas from the Gulf, according to five sources with knowledge of the matter, in a demonstration of Tehran’s ability to control energy flows through the Strait of Hormuz. RTRS

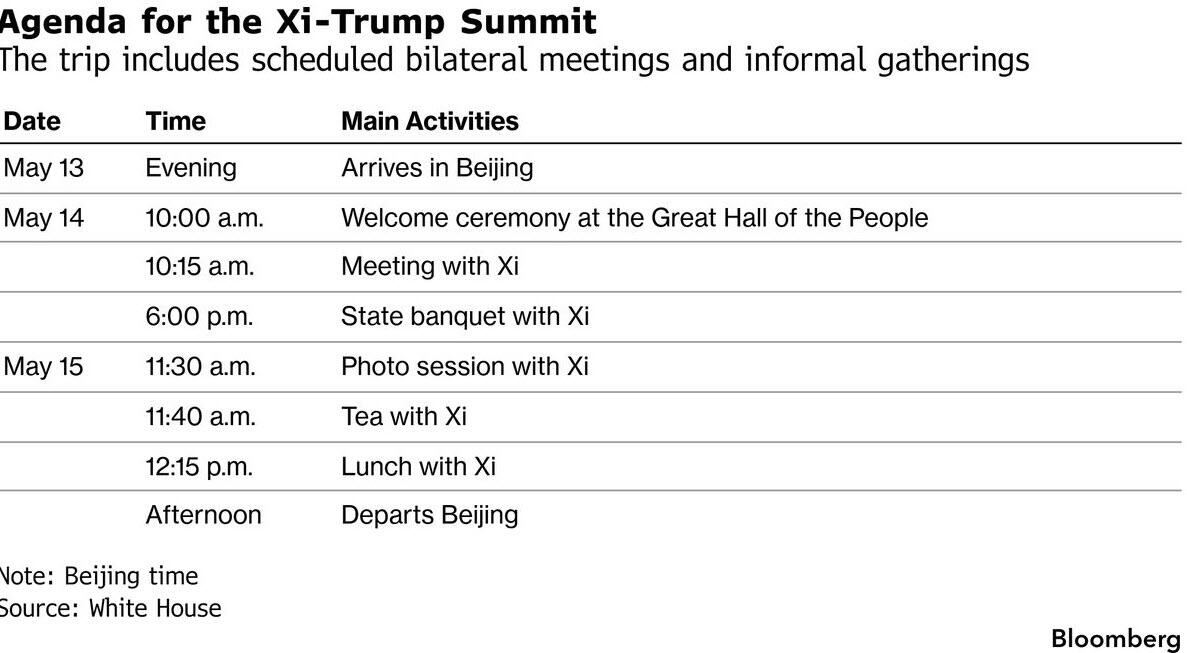

- Trump said he would urge China’s Xi Jinping to “open up” to U.S. business on his way to a summit in Beijing on Wednesday, adding Nvidia’s Jensen Huang to a group of CEOs travelling with him. The CEOs accompanying Trump are drawn mainly from companies seeking to resolve business issues with China, such as Nvidia, which has struggled to get regulatory permission to sell its powerful H200 artificial intelligence chips there.

- OpenAI investment gains helped drive a surprise rise in SoftBank’s quarterly profit, while Tencent and Alibaba revenue missed. BBG

- China’s tech-heavy ChiNext index hit a record as an AI-driven rally lifted chipmakers and tech suppliers. BBG

- Construction projects are stalling around the world as the closure of the Strait of Hormuz disrupts the supply of crucial materials and drives up prices for oil-derived products like paint and insulation. FT

- For the first time in three years, inflation is outstripping growth in Americans’ paychecks. Blame the gas pump. Americans are currently paying about $4.50 a gallon for regular gasoline, according to AAA, up more than 50% since the initial U.S.-Israeli attack on Iran in late February. Pay increases aren’t keeping up. WSJ

- Oil broke a run of three straight daily gains even as the Strait of Hormuz remains practically shut and Trump repeated his threats against Iran. Inventories are falling at a record pace of about 4 million barrels a day, the IEA said. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following on from the mostly subdued handover from Wall Street, where sentiment was dampened by tech weakness, higher oil prices and firmer-than-expected inflation, while the geopolitical situation remained uncertain with Iran said to require five confidence-building conditions for it to enter a second round of talks with the US. ASX 200 declined amid weakness in the top-weighted financial sector after shares in Australia’s largest lender CBA, slumped around 10% following its earnings results, while the recent federal budget announcement failed to spur risk appetite and was seen by analysts to hit consumer stocks. Nikkei 225 clawed back initial losses after encouraging current account and bank lending data, and despite hawkish market pricing of around a 70% chance for a BoJ rate hike next month. Hang Seng and Shanghai Comp were mixed as participants digested earnings releases and with the focus on the looming Trump-Xi summit, while the US President is on his way to Beijing with various CEOs on Air Force One, including the late addition of NVIDIA’s Jensen Huang.

Top Asian News

- BoJ said there was no meeting held between the US Treasury Secretary Bessent and BoJ Governor Ueda.

- US Treasury Secretary Bessent said that thanks to the powerful bond between US President Trump and Japanese PM Takaichi, the relationship between the US and Japan is stronger than ever before, while he was happy to share with the PM the belief that the fundamentals of the Japanese economy are indeed strong and resilient. Furthermore, he said they exchanged views on the US-Japan investment program, critical minerals, President Trump’s upcoming visit to Beijing, and other subjects of mutual interest.

European bourses (STOXX 600 +0.4%) have begun to reverse the losses seen at the start of the week, despite the mixed Asia-Pac and stateside trade. The DAX 40 is the outperformer, helped by a flurry of positive earnings, while the CAC 40 lags its peers despite the gains in STMicroelectronics and ArcelorMittal. Sectors point to a more mixed picture. Basic Resources tops the pile, as copper extends above USD 14k/t while aluminium, nickel and iron ore are also bid. The underperformer is Media, closely followed by Travel & Leisure. TUI reported Q2 earnings, in which it sees strong demand in the Holiday Experiences Business Area in H2.

Top European News

- UK Labour-affiliated union group TULO said Labour cannot continue on this path, is it clear the PM will not lead Labour into the next election.

- SNP to force a vote on UK PM Starmer via an amendment to King’s Speech debate.

- UK government appoints loyalists to fill gaps left by government resignations.

- UK government whips believe Wes Streeting will make his move on Thursday, to avoid clashing with the King’s Speech, while they also believe Andy Burnham doesn’t have an MP ready to quit, and that aside from the 87 MPs who’ve publicly called for Starmer to go, the same number privately want him to step down, according to Sky News reporter Jon Craig.

Trade/Tariffs

- The US White House has reportedly not ruled out potential Chinese direct investment in the US, Semafor reported.

- US President Trump posted that NVIDIA CEO Huang is on Air Force One along with a number of CEOs of large US companies, including Tesla, Boeing, Cargill, Citi, Goldman Sachs, GE Aerospace, Micron & Qualcomm. Trump added that his first request to Chinese President Xi will be to open up China so that these brilliant people can work their magic.

- US Treasury Secretary Bessent and Vice Premier He held talks. Following the conclusion, Chinese state media reported that China and the US held candid, in-depth and constructive exchanges.

- EU Commission has outlined a potential compromise to break the EU-US trade deal deadlock, with specific reference to the sunrise clause, Politico reported.

FX

- G10s trade under a relatively strong USD, with recent upside in DXY as it vaulted its 100-DMA (98.45) and 200-DMA (98.52), to make a current peak at 98.58.

- USD continues to be driven by oil/yields as geopolitics remain in focus. Today, US President Trump is expected to arrive in China for his summit with Xi, where talks are expected to take place on Thursday and Friday. No breakthrough is expected in US-China relations, though the situation in Iran will likely be one of the core topics, with some fearing an Iran-for-Taiwan bargain. (Full analysis at 06:50BST on the headline feed). The session also sees a number of Fed speakers, including Collins, Kashkari and Logan.

- GBP trades a touch lower against a strong buck, but stronger against the Euro despite continued political uncertainty. As it stands, the PM intends to stay in his post and run in any leadership contest against challengers (likely Streeting. Potentially, Miliband, Rayner, Carns, and/or Burnham). Theoretically, if a contest were to be triggered now, Starmer would be the favourite (100+ MPs back him, against c. 90 who have expressed no-confidence). Recent newsflow has been around a very brief Starmer-Streeting meeting. We are unlikely to see a readout due to the King’s speech later today. In terms of timing, at 14:30 BST, two backbench (Junior) Labour MPs will ask “typically light-hearted” questions, according to Politico. Opposition leader Badenoch speaks third, then the PM will respond to her questions.

- EUR/GBP trades towards the lower end of Tuesday’s 0.8653-0.8697 range, Cable continues to move lower as it did on Tuesday, currently supported by the 1.3530, with further support lower at 1.35, the previous session’s low. Ultimately, any leadership change would likely be a shift to the left and therefore weigh on the Pound.

Central Banks

- ECB’s Muller said the EU has not fallen into stagflation.

- ECB’s Villeroy said the ECB must be ready to intervene on second round effects; underlying inflation is currently under control.

- ECB’s Rehn said inflation expectations are still anchored.

- ECB’s Radev said once again, seeing an external price shock.

- ECB’s Dolenc said can expect consumer expectations from inflation to rise. Energy prices have a limited effect on the economy for now.

- ECB’s Elderson said banks need to update resilience plans to cater for the higher probability of severe disruptions because of Anthropic’ s Mythos AI tool.

- Riksbank Minutes: Market expectations regarding central bank policy rates have been closely interlinked with the inflation risks stemming from energy prices.

- BoJ will continue to closely monitor how the Middle East situation will affect economy and prices, according to an official.

- UBS sees the Fed to cut 25bps in December 2026 and March 2027 (prev. forecast cuts in September and December).

Fixed Income

- Global benchmarks are incrementally firmer/flat this morning as crude benchmarks pull back from recent highs, and as geopolitical/political newsflow remains light.

- USTs are firmer by a couple of ticks and currently trade within a narrow 109-31+ to 110-04 range, but ultimately residing near the prior day’s trough at 110-01. As a reminder, US paper was pressured on Tuesday amidst higher energy prices and after a hotter-than-expected US CPI report, which has led markets to reprice hawkishly. Most recently, UBS pushed back its call for a cut at the Fed to December 2026 and March 2027 (prev. forecast cuts in September and December). Focus today will be on US PPI and a flurry of Fed speakers.

- Bunds are essentially flat in a quiet 124.59 to 124.87 range. Earlier this morning German Wholesale Prices M/M topped expectations, with the Y/Y figure also rising from the prior. The statistics office cited the war in the Middle East as the region for the jump in prices, “particularly for energy products and raw materials”. Despite the jump in prices, Bunds were choppy but ultimately little moved. Thereafter, EZ GDP 2nd estimate was not subject to revisions, whilst Employment Change Q/Q fell from the prior. No move following the German 2047/2054 auctions.

- Gilts initially gapped higher at the open, peaking at 86.31, as UK paper found some reprieve following on from a dire session seen in the prior session; traders may have also priced in the chance of quiet domestic politics, ahead of the King’s speech. However, since the cash open, UK paper has gradually trundled lower and is now only firmer by a handful of ticks – conforming to the action seen across peers. From a yield perspective, the 10yr remains above the 5% mark and a little short of the peaks made on Tuesday (5.13%).

- Markets remain on watch for domestic politics, and particularly on Wes Streeting after his short meeting with PM Starmer – UK journalists are questioning whether this signals increased likelihood of a potential leadership challenge. Before the duo met, Sky News reported that UK government whips believe Wes Streeting will make his move on Thursday, to avoid clashing with the King’s Speech, while they also believe Andy Burnham doesn’t have an MP ready to quit.

Commodities

- In geopolitics, US President Trump said Iran will either make a deal or be “decimated”, while reaffirming the effectiveness of the blockade. Meanwhile, Iran reiterated five conditions before entering nuclear talks, including sanctions relief, reparations and recognition of sovereignty over the Strait of Hormuz. US intelligence reportedly assessed Iran still retains significant missile capabilities along the Strait of Hormuz. Further, Sources familiar with negotiations said Iran’s top conditions before nuclear talks include ending the war on all fronts, lifting sanctions, releasing frozen funds, compensation for war damages and recognition of Iranian sovereignty over the Strait of Hormuz.

- Elsewhere, the IEA released its monthly oil market report today, in which it forecasts world oil supply to fall by 3.9mln bpd in 2026, assuming Strait of Hormuz flows gradually resume from June (prev. forecast 1.5mln bpd fall); Sees total world oil supply 1.78mln bpd lower than demand in 2026 (vs. prev. forecast 0.41mln bpd higher). IEA noted the war in the Middle East is depleting global oil inventories at a record pace.

- WTI July and Brent July futures have trimmed losses seen overnight, with the former in a USD 96.79-98.58/bbl range and the latter in a USD 106.09-107.56/bbl. Dutch TTF is now flat intraday after recovering from sub-EUR 46/MWh lows to levels north of EUR 46.50/MWh.

- Spot gold resides in a USD 4,685.90-4,727/oz range, well within yesterday’s USD 4,638.36-4,773.58/oz parameter, with the 100 DMA at USD 4,786.96/oz. Spot silver takes a breather from six straight sessions of gains, with the precious metal pulling back a touch after hitting resistance around USD 87.80/oz. Elsewhere, Shanghai Futures Exchange adjusted the price limit for the AG2705 silver futures contract to 17%.

- Base metals are posting varying gains across the board amid a broadly but cautiously positive risk appetite across Europe and US markets, and despite a firmer USD. 3M LME copper resides north of USD 14k/t in a 14,086.58- 14,191.48/t range at the time of writing.

- IEA OMR: world oil supply to fall by 3.9mln bpd in 2026 assuming Strait of Hormuz flows gradually resume from June (prev. forecast 1.5mln bpd fall); Sees total world oil supply 1.78mln bpd lower than demand in 2026 (vs. prev forecast 0.41mln bpd higher). Sees world oil demand falling by 420k bpd in 2026 on Iran war (prev. forecast 80k bpd drop).

- US Private Inventory Data (bbls): Crude -2.2mln (exp. -2.3mln), Distillates -0.3mln (exp. -1.3mln), Gasoline +0.5mln (exp. -2.5mln), Cushing -1.8mln

- US NEC Director Hassett said this is a temporary energy shock and that President Trump is confident the Strait of Hormuz will be open soon, while Hassett said regarding the SPR that they are releasing as fast as possible. Furthermore, he said Trump’s view is that we should modernise the gasoline tax.

Geopolitics

- US President Trump posted “When the Fake News says that the Iranian enemy is doing well, Militarily, against us, it’s virtual TREASON in that it is such a false, and even preposterous, statement. They are aiding and abetting the enemy! All it does is give Iran false hope when none should exist.”

- “Pakistan’s Foreign Ministry is all set to hold a consultative meeting of its envoys in Middle East, West Asia and important capitals on Thursday in Islamabad”, Pakistani journalist Mallick posted.

- Iranian Foreign Ministry spokesman said Iran will obtain a more accurate assessment of the American position through Pakistani mediators, Al ArabyTV reported. Further stated that Tehran rejects maximalist demands regarding its Nuclear Program and considers them unjust.

- Iranian Foreign Minister Araghchi said a lack of good faith and the dishonesty of the US is the most significant obstacle to a definitive end to the war, while he commented that the main cause and origin of the current situation in the Strait of Hormuz is the US and Israeli regime’s military aggression against Iran, and subsequently the repeated violation of the ceasefire through the continued blockade of Iran’s maritime ports. Furthermore, he said they are holding consultations to draft regulations concerning arrangements for the Strait of Hormuz in accordance with international law.

- Pakistan and Iraq have struck agreements with Iran to transport liquefied gas and oil via the Strait of Hormuz amid shipping risks, according to sources.

- China-flagged supertanker attempts to exit Hormuz, according to reports citing data.

- India, Japan and most European nations joined the Hormuz Strait draft resolution, while 112 countries back the resolution, according to Al Jazeera.

- A group of bipartisan US senators is writing to Secretary of State Rubio to pledge their support for the Taiwan Relations Act, Semafor reported; Twelve senators signed the letter.

- North Korea leader Kim inspected munitions factories and called for modernisation and efficiency gains in the arms industry, according to KCNA.

US Event Calendar

- 7:00 am: United States May 8 MBA Mortgage Applications, prior -4.4%

- 8:30 am: United States Apr PPI Final Demand MoM, est. 0.5%, prior 0.5%

- 8:30 am: United States Apr PPI Ex Food and Energy MoM, est. 0.3%, prior 0.1%

- 8:30 am: United States Apr PPI Final Demand YoY, est. 4.8%, prior 4%

- 8:30 am: United States Apr PPI Ex Food and Energy YoY, est. 4.34%, prior 3.8%

- 11:30 am: United States Fed’s Collins Speaks on US Economy

- 1:15 pm: United States Fed’s Kashkari in Moderated Discussion

- 7:00 pm: United States Fed’s Logan in Moderated Conversation

DB’s Jim Reid concludes the overnight wrap

In nearly two decades of writing the EMR it’s rare that I finish it off while watching the sun break through the clouds and go down over an ocean but that’s the scene as I type this evening from the US West Coast. For the amount of times I finish it in the cold and dark, I hope you’ll give me this treat! Rest assured there is no glass of wine influencing this daily!

I wish markets were as serene as the view, with increased nervousness that a US-Iran deal looks further away than most would have hoped when the more positive news flow came through a week ago. In response to that uncertainly Brent was up a further +3.42% to $107.77/bbl yesterday whilst WTI (+4.19%) also crossed the $100/bbl threshold to $102.18/bbl. Although we’ve edged down just under a percent in Asia, we’ve now edged back above the levels seen before the positive Axios story broke last week that a deal could be imminent. The higher oil price led to a sell-off in fixed income and equities yesterday which wasn’t helped by a hotter core US CPI print than the market expected, even if it was in-line with our forecast.

Turning to rates first, that CPI print and worries over sustained costs from a prolonged conflict drove the 10yr Treasury yield (+4.9bps) to 4.46%, its highest since June 2025. The moves were similar for 2yr (+3.7bps to 3.99%) and 30yr yields (+3.9bps to 5.02%), with the latter now just 7bps below the post-2007 high it reached in May last year. That higher US April CPI print showed headline inflation rising +0.6%m/m as expected (+3.8% y/y vs +3.7% y/y exp.) but core inflation slightly beating consensus estimates (+0.4%m/m vs +0.3%m/m and +2.8%y/y vs +2.7%y/y exp.).

In addition to the upside surprise in core, there were a few concerning details within the data. The effects of the Middle East conflict pushed up categories like energy (+3.8% m/m), airfares (+2.8% m/m) and postage and delivery services (+3.5% m/m), while grocery prices (+0.68% m/m) saw their largest monthly rise since 2022. And the Cleveland Fed’s trimmed mean CPI measure came in at +0.43% m/m, its sharpest monthly rise since January 2024. Kevin Warsh has been a proponent of looking more at this measure. Unfortunately it doesn’t seem to be moving in the dovish direction he expected. For more on the release and implications, see our US economists’ reaction piece here.

The hawkish market interpretation was later reinforced by comments from Chicago Fed Goolsbee, who said that the print was “worse than expected” with services inflation being amongst the worst affected. In response, the amount of fed hikes priced by next April rose to a new high of 20bps (+6.0bps on the day). The next big watchpoint for the Fed will be today’s PPI report for April, which our US analysts expect to rise +0.5% for headline and +0.3% for core. So that’s a tough inflation backdrop as Kevin Warsh takes over as Fed Chair later this week, with the Senate confirming him to the Fed Board in a 51-45 vote yesterday while the final vote to confirm him to a 4-year term as Chair is expected today.

The hawkish inflation data combined with the Middle East conflict led to a challenging backdrop for equities. However, this also wasn’t helped by chipmakers and tech selling off with the Philly Stock Exchange Index falling back by -3.01%, although well off the -6.75% intra-day lows. Elsewhere, the S&P 500 (-0.16%), Nasdaq Composite (-0.71%) and Magnificent 7 (-0.49%) also fell but again bounced off the lows. The S&P 500 was down by -1% at one point, but a partial in tech and a rotation into defensive sectors including healthcare (+1.93%) and consumer staples (+1.56%) helped limit the losses. The mood was more challenging in Europe, with multiple indices declining with the Iran and oil fears. That included the DAX (-1.62%), CAC 40 (-0.95%) and Stoxx 600 (-1.01%), although the FTSE 100 (-0.04%) losses were not as steep.

Staying with Europe, UK politics weighed on bond yields throughout the session. During yesterday’s cabinet meeting, PM Starmer reiterated his call that he would stay on despite the number of MPs wanting Starmer to quit crossing the 81 required to mark a leadership challenge if they coalesced around a candidate. It’s important to note that any calls or letters for Starmer to resign don’t trigger anything unless MPs explicitly back an alternative candidate. So even as four ministers resigned from government yesterday, it does look increasingly possible that he will see this through for now, with Polymarket odds of Starmer leaving by June 30 down to 33% this morning from as high as 80% on Monday night. We have the King’s Speech today which sets out the upcoming legislative agenda of the government. With the fate of Starmer still in the balance though, yields on the 10yr yield (+10.4bps to 5.10%) rose to its highest level since 2008, and the 30yr gilt yield (+9.5bps to 5.77%) reached its highest since 1998. Other markets are also at multi-year highs, but the UK has underperformed over most recent periods.

Indeed the 30yr German bund yield also rose to its highest level since 2011 yesterday. We did receive the German May Zew investor expectations, which rose to -10.2 vs -19.5 estimate. So that was not as bad as feared. Elsewhere, 10yr bond yields also sold off across bunds (+6.1bps), OATs (+7.9bps) and BTPs (+9.3bps). So it was an overall rough day for global bonds.

In Asia, the KOSPI (+1.25%) is back to leading the way again, after earlier dropping by -3.0%, while the Nikkei (+0.15%) is edging higher. Chinese related stocks are edging lower with US futures flat and European futures up just over half a percent. Yields on the 20-year JGBs have increased by +4.2bps, trading at 3.49%, surpassing its January peak to reach the highest level since 1997.

Finally, we saw some ongoing headlines around Ukraine and Russia. Putin’s press secretary Dmitry Peskov said it was still too early to talk about “specifics” as he addressed Putin’s comment over the weekend that the war in Ukraine is “coming to an end”. While Ukraine talks have been on hold since January, recent comments may signal an emerging shift in Moscow’s stance amid Russia’s slowing military momentum and rising domestic discontent according to opinion polls. This is more of a slow-burn story but one that saw European defence stocks post a fourth consecutive decline yesterday, with Rheinmetall (-1.99%) falling to its lowest level since March 2025. Those moves also came as CBS News reported a memo outlining terms of a potential US-Ukraine defence deal that would see Ukraine export military tech to the US.

To the day ahead now, data includes US April PPI, Germany April wholesale price index, Eurozone March industrial production, Q1 employment. For Central Banks the Fed’s Collins and Kashkari will speak, as will the ECB’s Lagarde, lane and Radev, and the BoE’s Mann

Tyler Durden

Wed, 05/13/2026 – 07:59

via ZeroHedge News https://ift.tt/58VCYR9 Tyler Durden