Korean Bubble Mania: Retail Investors Max Out On Margin Debt, Choose To “Risk Complete Collapse” Than Miss Stock Rally

For many years, Koreans were bitcoin’s best friend.

After bitcoin emerged about a decade ago as the asset class with the most pronounced momentum – both to the upside and the downside – Korea’s daytrading army, famous for being totally unable to do any fundamental valuation analysis but legendary for its wilnningness to piggyback on any momentum with suicidal leverage, became enamored with bitcoin and the result were face-ripping meltups and heartstopping crashes, a daily breathless rollercoaster where 10% moves in hours if not minutes had become the norm.

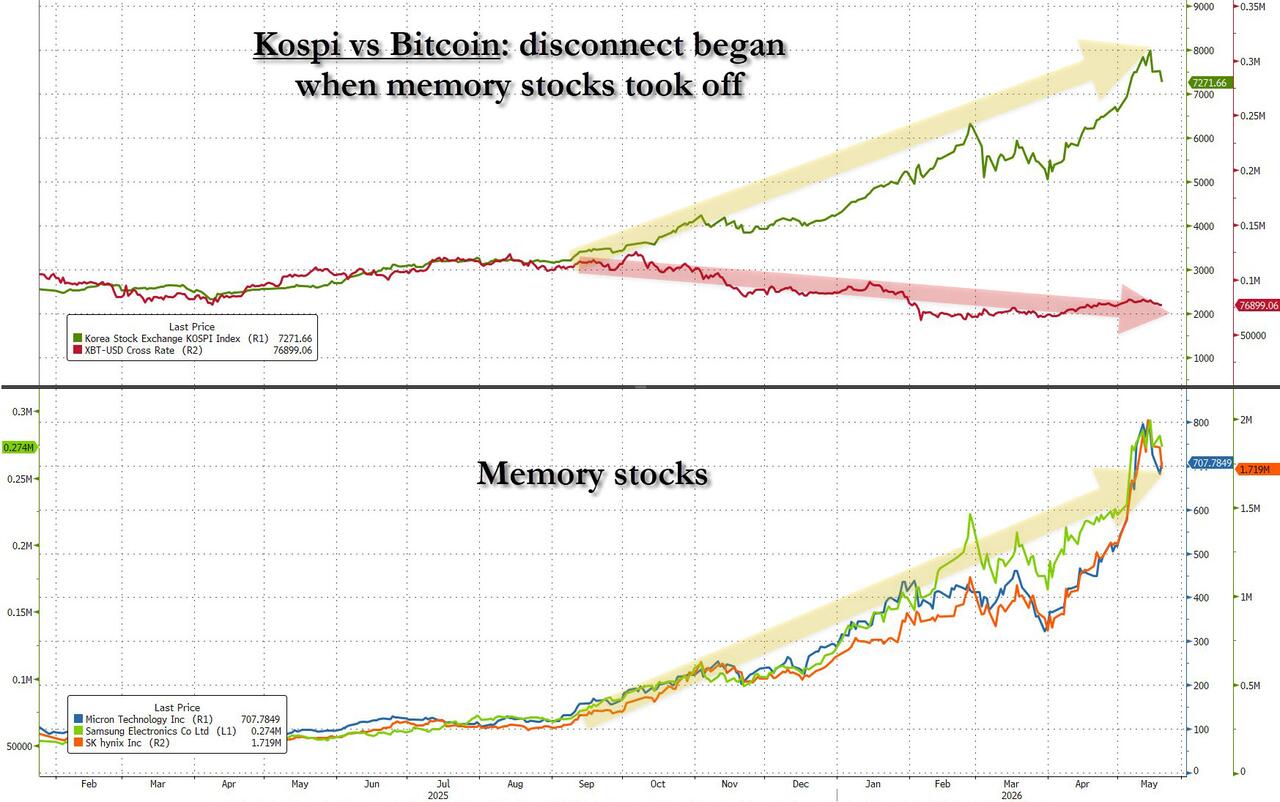

But then, last September something snapped. After bitcoin had tracked Korea’s Kospi index closely for years, the two series – formerly joined at the hips for years – diverged and went their separate ways, the Kospi soaring to never before seen levels, while bitcoin stagnated, shrinking ever lower as its former momentum-addicted traders abandoned it for something shinier, and with much more momentum: memory stocks.

As shown in the chart below, the Kospi-Bitcoin divergence started right around the time last September when memory stocks like Micron, Samsung and SK Hynix began what would be an absolutely historic meltup for the ages (if not so much for bitcoin).

And while we had previously showed our readers a behind the scenes peeks into Korea’s crypto trading culture, nothing prepared us for what is taking place right now… because what is taking place is nothing short of absolute batshit insanity.

Consider this: a single post uploaded May 8 by a Korean civil servant on Blind, the anonymous workplace community app, quickly set off a frenzy online. The post included a screenshot of his brokerage account showing he had poured a staggering 2.3 billion won ($1.7 million) into shares of semiconductor giant SK Hynix, one of the key driving forces behind Korea’s roaring stock market.

But even more striking is that the 1.7 billion won of that investment was financed through margin loans borrowed from his brokerage!

“I believe the semiconductor market will continue its upward climb through 2028, but I’m taking a more aggressive approach to grow my assets faster,” he wrote. Four days later, on May 12, he returned with an update claiming he had already locked in 267 million won in profits.

That same day, another Blind post surfaced – this time from a Seoul Metro employee in her 20s, who wrote that rather than missing out on the rally, she would “risk complete collapse,” adding that she had used 150 percent margin financing to fully leverage into stocks.

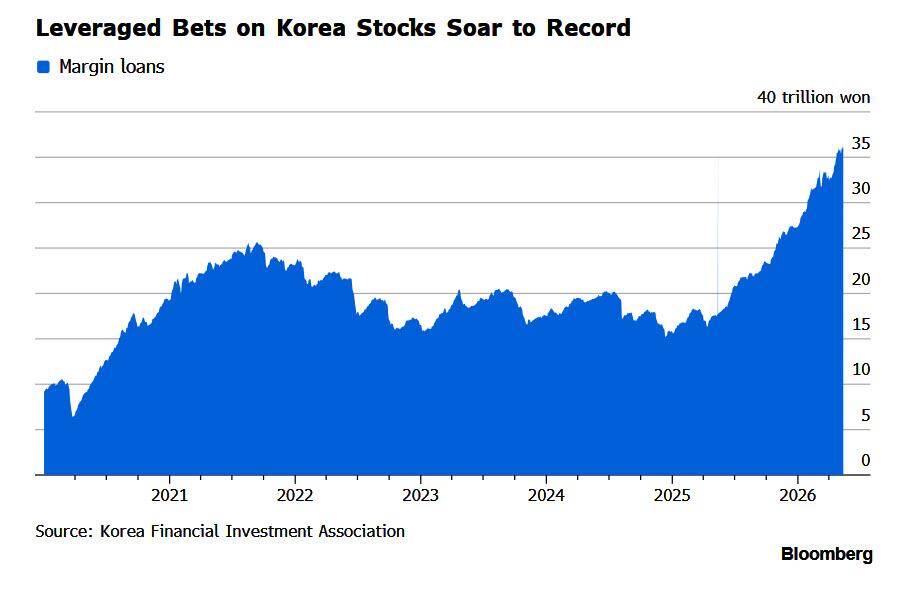

As Korea’s bull market barrels ahead, the Korea Times writes that more momentum-addicted retail investors are turning to borrowed money to magnify returns, despite huge risks of losing more than 100% of one’s capital. As of Friday, outstanding margin loans used for stock purchases had ballooned to a record 36.47 trillion won, according to the Korea Financial Investment Association.

While retail investors end up with all the risk, for Korea’s securities firms, the recent retail mania and associated borrowing boom has become a lucrative windfall.

According to recent industry data, the nation’s 10 largest brokerages – Korea Investment & Securities, Mirae Asset, Samsung, Kiwoom, NH, KB, Shinhan, Hana, Meritz and Daishin – generated a combined 600 billion won in interest income from margin lending in the first quarter of this year, up 55.9% from a year earlier.

Margin loans allow investors to borrow money from brokerages to buy stocks by pledging existing assets as collateral. While this can amplify gains, it also comes with annual interest rates ranging from 7 to 9%, and if share prices fall too sharply, brokerages force-sell holdings to recover their loans.

For now, bullish sentiment shows few signs of cooling: with the benchmark KOSPI climbing from the 4,000 range late last year to surpass the historic 8,000 mark in less than half a year, many retail investors appear willing to embrace higher-risk strategies in pursuit of faster gains, similar to what happened in China during the 2015 bubble when margin debt hit daily record highs.

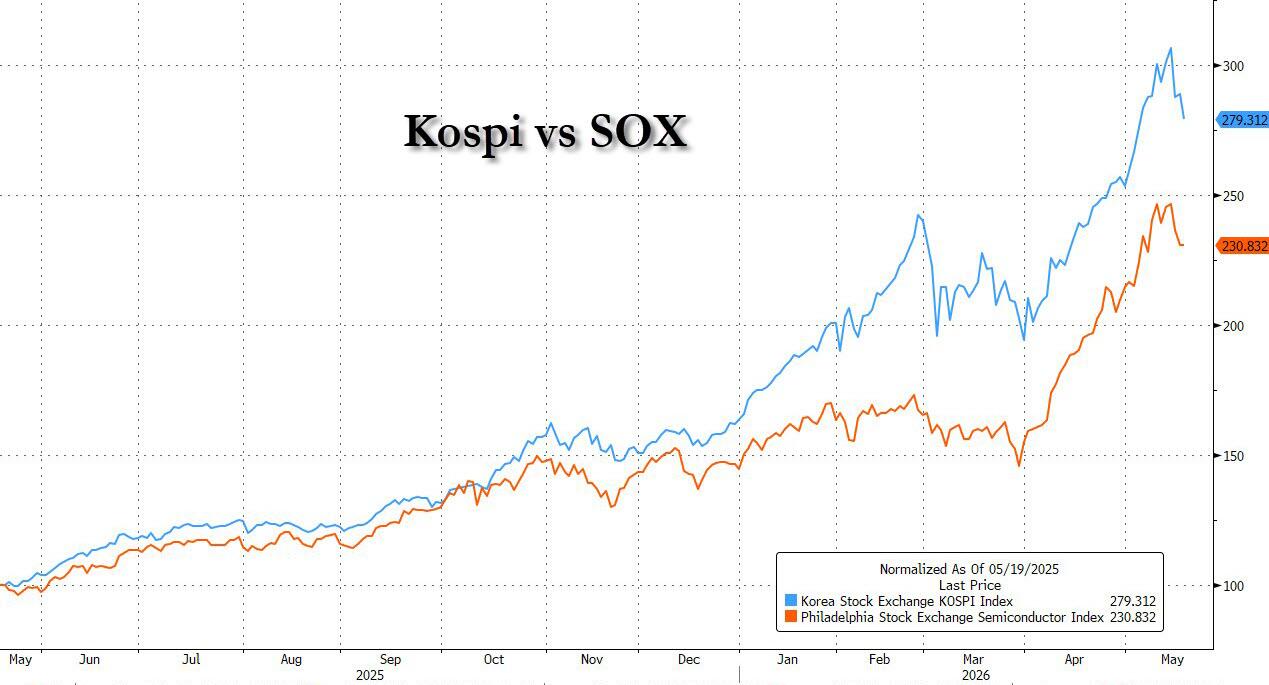

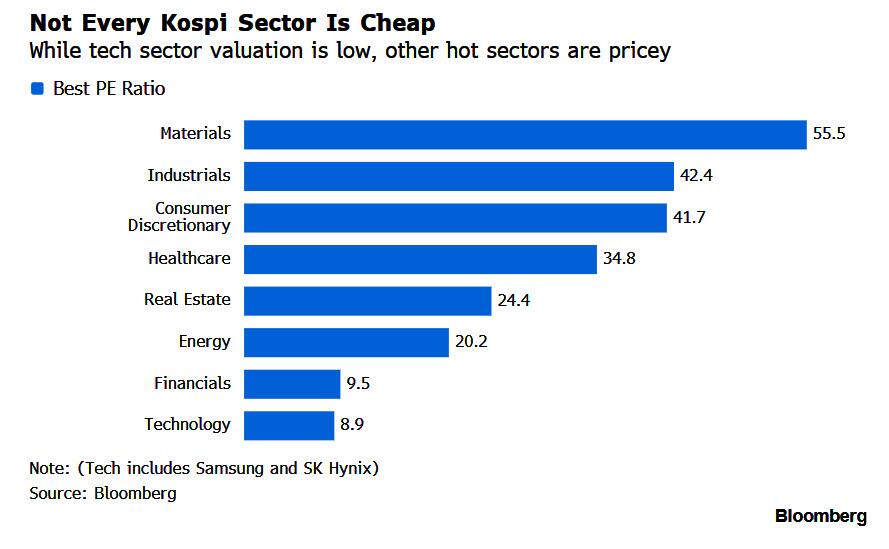

Up 75% this year, the quick ascent of South Korea’s Kospi Index has largely been driven by Samsung Electronics and SK Hynix, which accounted for more than two-thirds of the advance. The surge reflects record profits at the chipmakers, and with valuations still below regional and global peers, some investors argue the rally lacks the excesses typical of past boom-and-bust cycles.

Wall Street, of course, is more than eager to encourage reckless risk taking: in a May 10 report, JP Morgan raised its base-case KOSPI target to 9,000, with a bull-case projection of 10,000, arguing that investors should “stay positioned for further upside and not preemptively anticipate a cycle-end.”

The investment bank pointed to a “higher for longer” memory chip upcycle, fueled in large part by sustained artificial intelligence-driven demand, while also identifying brokers, insurers, holding companies and dividend-heavy sectors as major beneficiaries of the country’s broader market transformation.

Not everyone agrees.

For one, signs of froth are literally everywhere one looks. Key market measures showing uneven earnings growth, rising volatility and record margin debt are beginning to give some investors pause. “This is a party you want to enjoy while staying near the exit,” said Mo Young, a portfolio manager at RootN Global Investors in Seoul. The problem with this is that everyone thinks they can sell before everyone else does. That “strategy” always ends in tears.

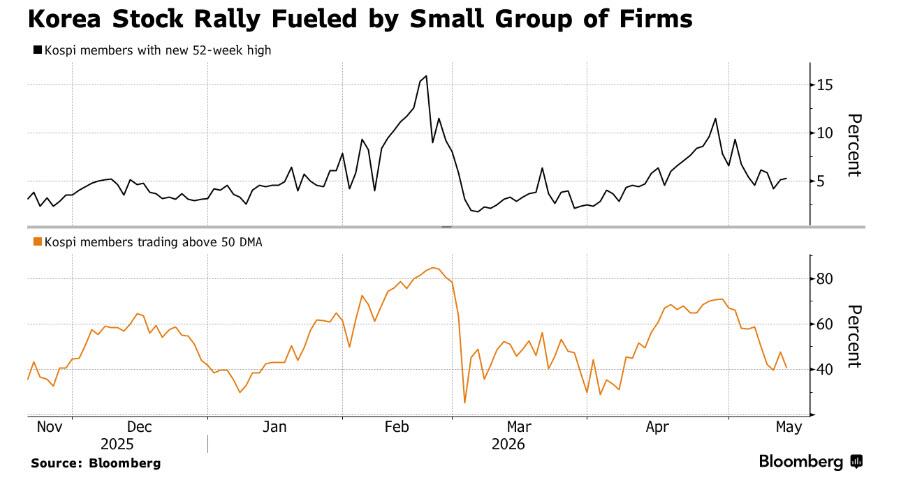

Just like in the US, Korea’s market breadth shows that the rally remains highly concentrated. Just 33% of benchmark stocks are now trading above their 50-day average, down from 70% three weeks ago. Meanwhile, 2% of members – mostly memory and chip stocks – are hitting new 52-week high despite the Kospi’s successive records, which underscores the narrowness of the gains.

“In other words, buying the index is not simply buying a diversified slice of Korea; it is increasingly a concentrated bet on memory semiconductors,” said Christian Heck, a New York-based portfolio manager at First Eagle Investment Management.

“The index itself is no longer obviously cheap, and broad exposure requires underwriting a very large semiconductor-cycle bet,” he added. “Selectivity is essential.”

Palvir Bahia, a fund manager at Polar Capital which manages $40.5 billion said his fund is “monitoring the rising margin debt closely as the market rally has led to an increase in margin debt which heightens market volatility, particularly on down days when retail investors are forced to sell in order to maintain account balances.”

The risk of forced retail liquidations has dragged in the chief of the country’s financial watchdog who expressed concerns that retail investors could suffer losses amid increased market volatility, according to the Financial Supervisory Service (FSS) on Tuesday.

During a meeting on consumer risk response a day earlier, FSS governor Lee Chan-jin said retail investors could increasingly pivot toward highly volatile, risky assets as the country is set to introduce single-stock leveraged, or inverse, exchange-traded funds (ETFs) next week.

And just in case record margin debt and historic call buying wasn’t enough, the watchdog warned that the introduction of single-stock leveraged ETFs could further accelerate capital flights to high-risk financial products. Because that’s just what Korea’s stock bubble needs.

A bubble which may burst any minute since cracks are starting to show in the index itself.

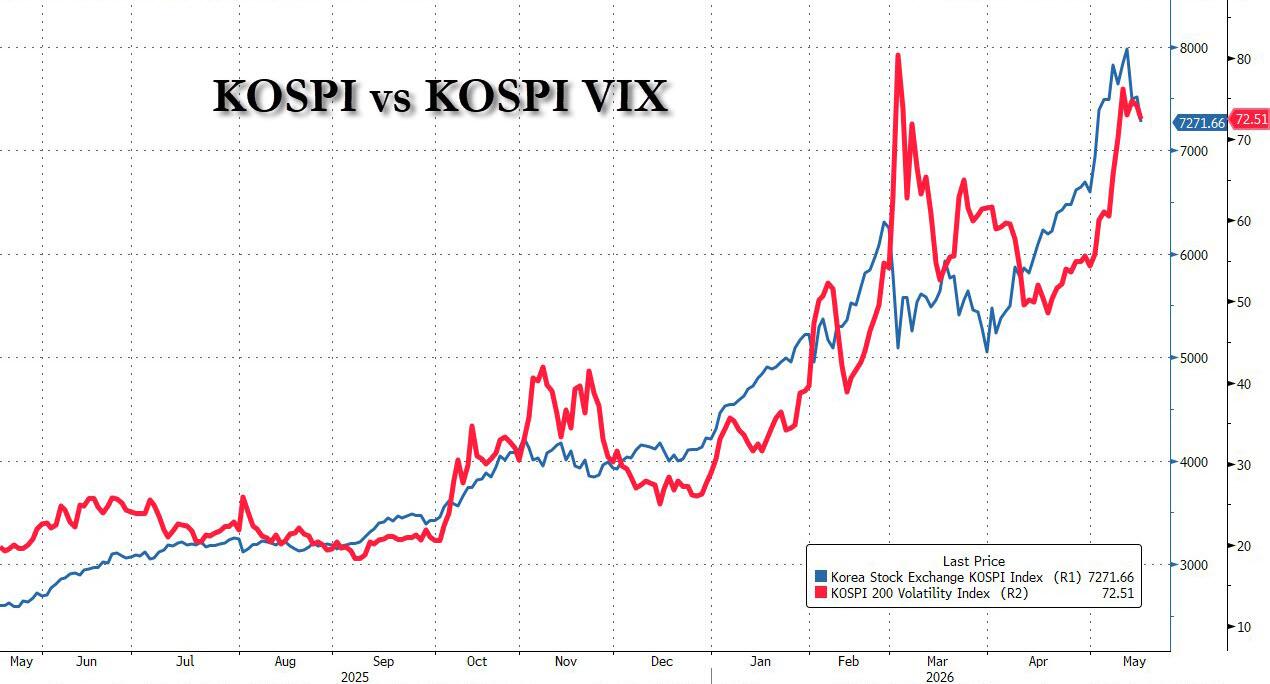

The Kospi dropped nearly 5% on Tuesday, the worst performer across Asia, as chip stocks tracked US peers lower amid rising bond yields. The index is now testing the ultra-steep trend line, with the 21-day moving average sitting just below current levels. As Market Ear notes, “these are short-term make-or-break levels for the AI melt-up.”

As we have observed previously, the Kospi is basically two memory stocks, Samsung Electronics and SK Hynix, which is why the Kospi is basically the SOX on steroids.

With everyone ignoring stocks and plowing their margin debt right into calls for leverage upon leverage, the Kospi VIX is now a broken market. The spot-up, vol-up regime which signals a “melt-up” phase driven by FOMO and extreme positioning, has been unlike anything seen before, resulting in many investors dismissing buying protection due to stratospheric vols. First, the VIX soared as stocks surged (due to call buying); now vol stays high as the KOSPI sells off. Vols at these levels are pricing around 4.5% daily index moves going forward! That’s not just extreme, that’s batshit insane, and virtually guarantees that all levered investors will be wiped out unless they have tons of available cash balances to absorb margin calls, which they don’t.

With Samsung and SK Hynix posting record profits, signs of froth are also emerging in smaller stocks where earnings growth is virtually non-existant. Non-tech firms have driven just 4% of the 12-month earnings gain since September, according to William Bratton, head of cash equities research for APAC at BNP Paribas.

Valuations are particularly stretched in materials sectors, which include electric-vehicle firms, trading at nearly 60 times forward earnings. Battery maker Posco Future M Co. stands out at over 300 times, despite carrying the highest number of sell ratings on the Kospi, Bloomberg data shows.

“If there is a meaningful slowdown of inflow from retail investors or systematic traders, or if hedge funds reduce their big positions that were most profitable, the market structure could become even more fragile,” Kim added.

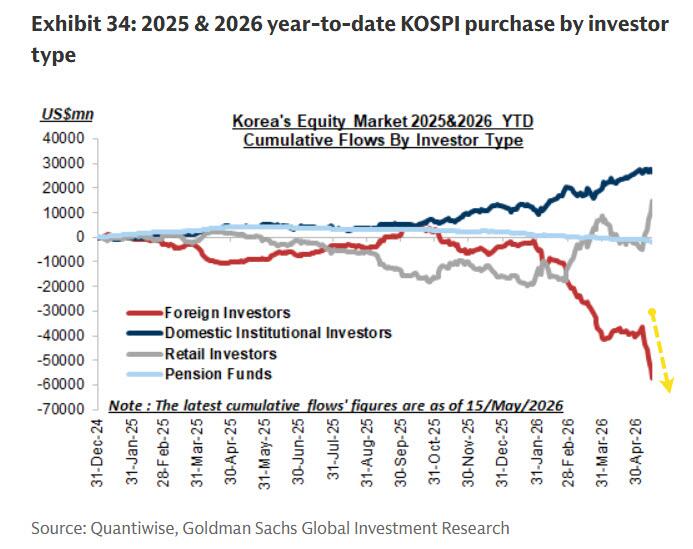

And it’s about to get much more fragile: as Goldman notes, foreigners have net sold the Kospi for the 9th consecutive day (and have been aggressively selling for much of 2026) with today’s latest selling focused in Tech (-$3.4bn). And while local institutions were net sellers for most part of the day, they closed as small net buyers with buying concentrated in Tech (+$168mn). Meanwhile, the willing target of everyone else’s distribution, retail investors, have continued to be net buyers and absorbed all of the supply from foreigners… the same retail investors who are now levered to the gills and are out of funds, so they are buying with the bank’s money.

As we pointed out a week ago, hedging Korea, and partly the broader AI mania, via EWY looked interesting. The last major upside overshoot at the start of the Iran war, eventually mean-reverted all the way back toward the 50 day moving average. Having previously outlined the EWY put spread logic, with the unwind starting to accelerate again, it’s time to start thinking about rolling strikes lower to keep max optionality.

KOSPI may be turning from the leader of the AI melt-up into the market’s most important stress signal, and when it blows, millions of levered retail investors will lose everything they own, and more thanks to the magic of leverage.

Tyler Durden

Tue, 05/19/2026 – 18:00

via ZeroHedge News https://ift.tt/GtAygmv Tyler Durden