The Atomic Crab

By Benjamin Picton, senior market strategist at Rabobank

The Atomic Crab

The Dow Jones hit a fresh all-time high yesterday, surging 1.73% to close at 51,562. The S&P500 posted more modest gains while the NASDAQ closed slightly lower as investors rotated out of some growth-oriented tech names and back towards healthcare and financials with more of a value or cyclical flavor.

Treasuries traded in a narrow range to close with yields little changed, while European sovereigns mostly saw modest declines in yields with the slightest hint of bull steepening evident in some curves. The Bloomberg Dollar spot index was down slightly but is inching higher again in early trade this morning.

Oil markets continue to be a point of focus. Front-month Brent futures closed 2.84% lower yesterday as markets remain of a Pollyanna state of mind over the status of the Strait of Hormuz. Dated Brent went the other way to post a (very) small gain yesterday after a 3.61% lift on Wednesday. The Singapore gasoil for spot delivery index was down 4.45% to $136.57/bbl.

Scuttlebutt over the status of US-Iran peace talks continued to dominate headlines yesterday. Following Donald Trump’s announcement of a Israel/Lebanon ceasefire that was contingent on Hezbollah ceasing its attacks on Israel we had confirmation this morning that Hezbollah has no intention of halting strikes. Hezbollah leader Naim Qassem made a statement on Thursday saying that “as long as the occupation exists, the resistance will continue” and calling the negotiations between the Lebanese government and Israel “absurd, humiliating and shameful.”

For Israel’s part, defence minister Katz has said that Israeli attacks in Southern Lebanon will continue and that the IDF will maintain “freedom of action” including in Beirut – which has been a red line for the Americans. Benjamin Netanyahu has recently faced criticism at home for being seen to be too compliant with American demands over strikes in Lebanon. Netanyahu faces an election in October, which polling suggests he may lose. Peace on all fronts was an Iranian condition precedent for reopening Hormuz and commencing the 60-day nuclear talks, but it seems that neither belligerent is interested.

Meanwhile, Donald Trump’s language on the Iran peace talks has gone from “deal imminent”, to “a deal soon, maybe” to “actually, we really don’t need a deal”. Trump showed signs of crabwalking away from a key demand that Iran hand over its stockpile of highly enriched uranium by saying that he does not need a deal with Iran to secure the uranium, but that there was no reason to send US troops into Iran to do so because the uranium is “entombed”.

Regular readers will recall that RaboResearch updated our Iran war baseline forecast two weeks ago to say that we didn’t think a meaningful deal would stick in the short term, and that the Strait of Hormuz would consequently remain functionally closed until September at least. The incompatibility of the two parties’ nuclear demands was a key factor in this judgement, so it is significant that Trump is now showing hints of softening his position on this point. However, capitulation on the highly enriched uranium or the limits of Iran’s nuclear enrichment program shifts the needle back towards US strategic defeat, with potentially grave consequences for all who have prospered under 80-years of Pax Americana.

We noted here yesterday that Bloomberg had reported that the IAEA had published a restricted document arguing that the nuclear risk posed by Iran is now higher than it was prior to the war. Subsequently, Bloomberg has reported that Iran has permitted IAEA monitors to inspect its Bushehr nuclear plant within the last week, but that Iran has steadfastly refused to comply with requests to verify the condition and location of its highly enriched uranium.

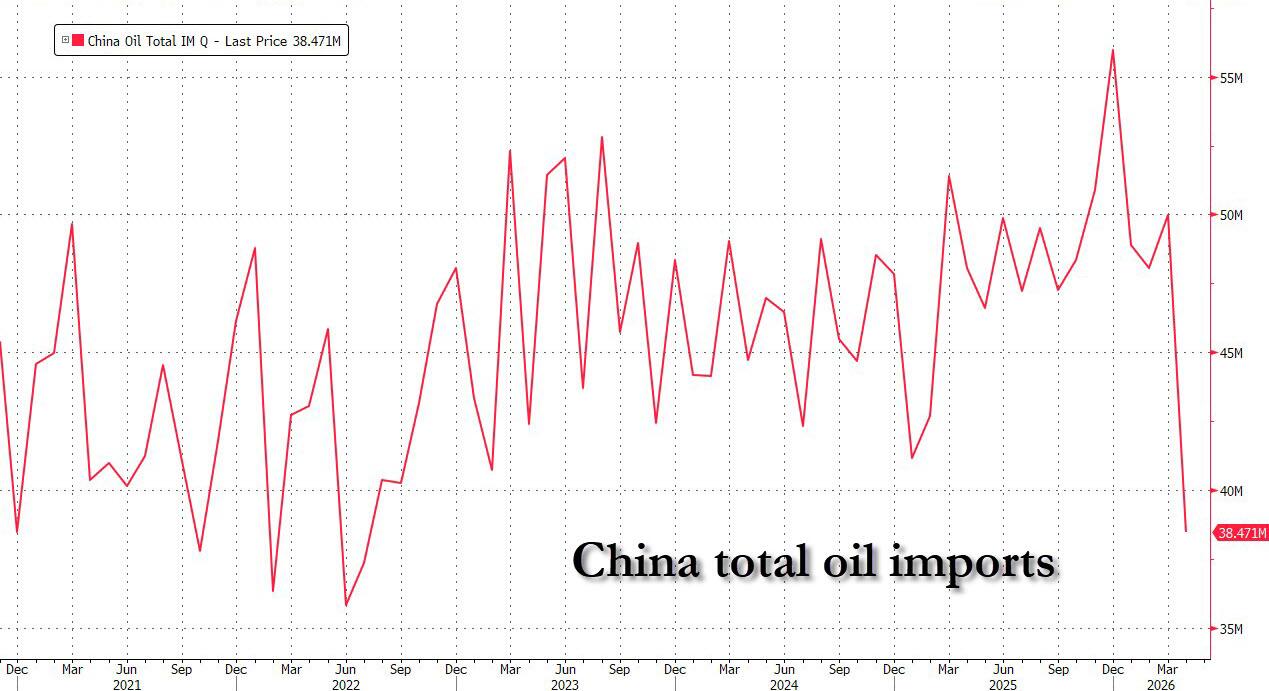

Needless to say, while the US-Iran stalemate continues global oil and oil products stocks continue to run down towards dangerously low levels. Vitol board member Tom Baker recently said that the oil trader estimated global demand destruction at about 4 million barrels a day, mostly from emerging Asia and Africa. China alone has reportedly reduced daily imports by close to 4 million barrels, while strategic reserve releases coordinated by the IEA have also been running close to 4 million barrels a day.

It’s not entirely clear whether or not there is some double counting in the Vitol estimates and China import drop-off, but the back of the napkin calculation gets us somewhere close to the ~12mbbl/day estimated supply loss from the Hormuz closure, and goes some way toward explaining why oil prices have remained remarkably low. Nevertheless, this remains a stocks to flows problem, and the cracks cannot be papered over indefinitely without supply tightness also being felt materially in developed markets.

While China’s reduction in oil imports helps planet earth rebalance energy flows, movements are afoot in Australia to counter Chinese monopsony power over the iron ore trade. China recently formed the state-owned China Mineral Resources Group to coordinate purchases of iron ore cargoes for China’s steel industry and exert market power to ensure that suppliers are paid in CNY, rather than USD. Australian firms supply more than 50% of global iron ore, but those firms have seen their market power eroded by alternative supply coming online in west Africa and an inability to coordinate to counter Chinese market power.

The Australian Financial Review this morning reports overtures from iron ore majors to the Australian government to counter monopsony buying power and give producers more say over how much they are paid and in which currency. Could we see state-backed single desk iron ore marketing in the land down under? Australia’s second-closest neighbour Indonesia recently did just that for coal, palm oil and ferroalloys, and has the world’s largest reserves of nickel – a critical input for Chinese stainless steel and EV battery production.

Elsewhere, there are again renewed hopes for peace prospects in Ukraine as Kyiv’s long-range drone strikes continue to cause havoc deep inside Russia. Vladimir Putin’s St Petersburg International Economic Forum (a kind of Davos for dictators) was recently interrupted by Ukrainian drone strikes on nearby Russian oil infrastructure – prompting Putin to vow that Russia will bolster its defenses against Ukrainian air attacks.

At the same time, Russia’s spring/summer offensive appears to have stalled and news outlets are reporting that Putin is signalling openness to a compromise on Ukraine in line with discussions held with President Trump in Alaska. Putin says that Ukraine needs to accept those compromises, but might there be some wiggle room for Ukraine to extract a better deal given the changed battlefield calculus? For his part, Zelenskyy is pushing for face-to-face talks with Putin to reach peace terms, but Putin says that he will only meet once terms have already been agreed, and that he will only meet in a neutral third-party country, which rules out EU member states in his view.

Tyler Durden

Fri, 06/05/2026 – 10:55

via ZeroHedge News https://ift.tt/6rVHUhO Tyler Durden