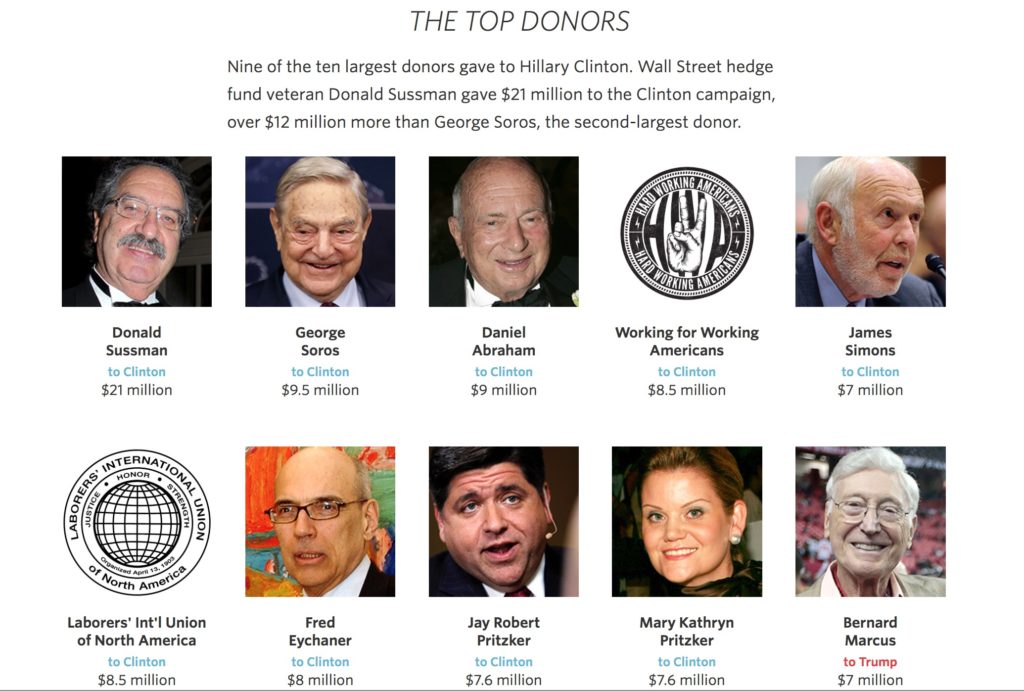

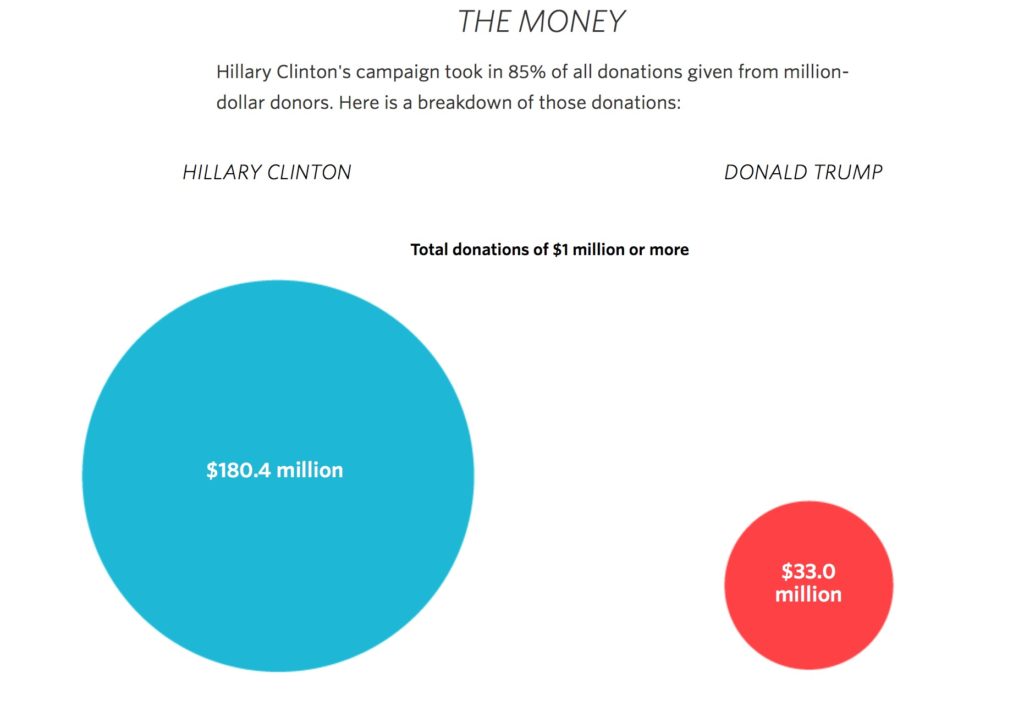

A couple of days ago the Wall Street Journal published a very powerful piece titled, The Million-Dollar Donors. What you’ll see should sufficiently dash any and all fantasies that Hillary Clinton is for the average person.

The internet was ablaze with speculation Friday morning following Wikileaks’ publication of a potentially disturbing email thread between John Podesta, Hillary Clinton’s campaign chairman, and his brother Tony, an influential Democratic lobbyist.

In the email, Tony asks his brother if he is able to attend a “Spirit Cooking dinner.” He says the artist hosting the dinner, Marina Abramovic, “wants [him] there,” and a previous email in the thread shows the artist requesting John’s presence at her New York City home.

Abramovic, a Serbian performance artist, has apparently conducted these dinners since the 1990s. While the title “Spirit Cooking dinner” suggests they constitute a harmless – if not spiritual — practice, some components of the “recipes” are raising alarm.

In a video of the artist conducting a Spirit dinner in 1997, she uses a thick, red, liquid substance — bubbling at the top of a bucket — to scrawl unsettling phrases and commands on a white wall.

“With a sharp knife, cut deeply into the middle finger of your left hand. Eat the pain,” one of the recipes reads.

Another calls for breast milk and semen to be mixed together and consumed on “earthquake nights.”

Still another reads, “Fresh morning urine. Sprinkle on nightmare dreams.”

The vulgarity of these statements and others has convinced some that Abramovic and the Podestas engaged in satanic rituals. At the very least, some recipes appear to be highly ritualistic. One advocates holding a python on one’s lap while sitting on a block of ice to fight high blood pressure.

Another says to “[t]ake 13 leaves of uncut cabbage, 13,000 grams of jealousy. Steam for a long time in a deep iron pot until all water evaporates. Eat just before attack.”

On the other hand, other phrases and sentences included in Spirit dinners appear to be fanciful, mystical activities — and less morbid:

“7 days without eating. 7 days without talking. 7 days without sleeping. 7 days without sexual intercourse. 7 days not reading or writing. 7 days not watching television. 7 days not answering telephone or fax.

“On the 7th day, take a bath in almond oil. Eat one coriander seed. One almond. One tablespoon of honey mixed with royal jelly.”

The recipes make frequent reference to crystals.

One recipe calls for “3 glass of water that a ruby has been soaking in for 3 days. 1 pomegranate.”

Another involves brushing one’s hair with a quartz brush until memories are released. Others reference tourmaline and meteorite, among other crystals.

On one hand, Abramovic is a provocative performance artist, and the extremeness of her work could easily be attributed to her offbeat take on art. She has claimed to be a mystic and that she predicted an earthquake in Italy, as well as the Pope being shot.

“You will need to be able to withstand a great deal of conversation about clairvoyants and tarot cards and didgeridoos and kundalini life forces and monks and gurus and ‘how the soul can leave the body through the center of the fontanel of the head’ to make it very far in this memoir.”

The Times also observed that “[s]he likes to say things like, ‘I’m only interested in an art which can change the ideology of a society.’ Her art, judged on that scale, shrinks further in size.”

While the rituals she suggests performing with the Podestas are undoubtedly unsettling, they are not secretive. The Museum of Modern Art called the recipes “evocative instructions for actions or thoughts,” and prints of her work are featured on their website.

However, just because the displays are in plain sight does not mean they are inherently innocent. Considering Anti-Media does not have a satanic or occult specialist on staff, however, we are unable to provide insight into whether the “recipes” constitute actual satanic behavior or are simply the highly unusual expressions of an established Eastern European artist.

One thing is clear: the Clinton campaign is attempting to distance itself from the emails and Spirit Cooking dinners.

“This is not the first or last time that WikiLeaks has tweeted propaganda while doing Putin’s bidding,” CNET reported the campaign said in an email, evidently continuing to invoke Cold War rhetoric to detract from Wikileaks’ publications.

For her part, Abramovic tweeted Friday she is not a satanist (despite her Twitter handle being AbramovicM666) and asked people to enjoy art and stop asking her about politics.

This is puzzling considering she was the one who reached out to the Podestas to invite them to her dinner, though it’s unlikely she ever assumed those emails would make it into the public eye.

Did Clinton’s campaign manager engage in satanic rituals? Were they simply spiritual? Were they the jumbled musings of an aging artist? What do you think?

As outgoing president Obama makes his final media rounds to bolster support for Hillary and to make the case for his legacy, he sat down with HBO’s Real Time host Bill Maher to say that humility in foreign policy “is a useful trait” – although one wonders just when the US has been humble about interfering in foreign sovereign states’ domestic affairs – even as he claimed that America is “an indispensable nation” that has “a lot to be proud of” in the world, thanks to having the most powerful military force.

While the interview focused on the president’s foreign and domestic problems, the commander-in-chief also shared his thoughts on why the US needs a military that costs over $600 billions a year: “The US having the most powerful military on Earth… helps up check the impulses of some other bad folks,” Obama said, giving North Korean leader Kim Jong-un and his country’s nuclear weapons program as an example. What he did not add is that as a result of being virtually unopposed around the globe, the US can interfere with impunity in every nation’s affairs, and then claim moral superiority when others try to follow in its own footsteps.

Obama also highlighted that the US has a natural inclination to intervene globally, though sometimes things go “haywire.”

“Bad things happen around the world and our natural instinct is – we should do something. There are times where our intervention makes a difference, but there are a lot of times where the unintended consequences can result in more problems when we intervene. And sorting out where those issues play out is, I think, one of the biggest challenges that any president has,” he said. Alas, due to her far more direct interventionist leanings, it is likely that Hillary Clinton will have a far lower filter when deciding whether to get involved in foreign conflicts, as her State Department tenure has demonstrated.

While the president didn’t elaborate on which of his decisions to employ America’s military might had caused unintended consequences, the destruction of Libya in 2011 under Hillary Clinton’s supervision may come to mind first. NATO’s bombing campaign helped rebels topple the country’s government, and, five years on, Libya is a fractured nation over which competing militant groups, terrorists, and criminals run rampant. In his earlier interviews, Obama said that he regretted not having a plan of action for after the intervention.

Yet Obama said he still believes the US and its military should continue to play a major role in the world. “As flawed as our foreign policy can be, and whatever blind spots we have, we really are the indispensable nation,” he bragged.

Contradicting his own earlier statement on humility, Obama exposed American hubris when laying out the case of US importance around the globe, which goes beyond its military presence: “There is not an international meeting I go to in which, if we were not sitting at the table, nothing gets done. For the most part, other countries don’t have either the capacity or the inclination,” he said. “When you have a bunch of authoritarian governments out there and a creeping authoritarian impulse around the world, we also are the ones who are pushing back – imperfectly, but most effectively – against locking up journalists and killing human rights activists and making sure that poor people get food and dealing with health crises,” he said.

While Obama didn’t elaborate on how successful America was in pushing back against Turkey’s impulse to arrest journalists or Saudi Arabia’s executions of human rights activists, for example, he insisted that the world needed America’s influence.

“Our values and our ideals actually matter. We do a lot of good around the world. There are some things that we do that are either ineffective or imperfect, but there is a lot to be proud of,” the president said.

Before wrapping up, Obama reiterated his call to vote for Hillary Clinton, whose tenure at state department has left US foreign policy in tatters, and prompted both China and Russia to challenge US superpower status, while her use of an unprotected server for confidential communications may have exposed numerous US state secrets to foreign espionage agencies.

Thelatest confirmation that the US economy continues to deteriorate comes not from the Federal Government but from state-level data, where year-over-year growth in state tax revenues slowed dramatically in the last two quarters. As Goldman notes, this has subtracted an average of 0.25 percentage points from GDP growth, raising the question of whether municipal finances could again be a persistent headwind to growth.

Via Goldman Sachs,

For several years following the 2008-9 recession, spending cuts by state and local governments were a meaningful drag on US growth. Faced with declining revenues and constrained by balanced budget rules, most states were forced to retrench, even as the rest of the economy began to recover. State and local government spending declined almost continuously from Q4 2009 through Q1 2014, subtracting an average of about 0.25 percentage points (pp) from annualized GDP growth over this period (Exhibit 1). As budgets eventually recovered, spending began to pick up, and state and local government outlays added about 0.25pp to GDP growth from Q2 2014 through Q1 2016. However, over the last two quarters, spending by states and localities stumbled again, raising the question of whether municipal finances could again be a persistent headwind to growth.

Exhibit 1: State and Local Government Spending Has Been a Drag on Growth in the Last Two Quarters

Source: Department of Commerce, Goldman Sachs Global Investment Research

The weakness in local and state government spending relates to both capital investment and current consumption. The more cyclical investment category—of which 80% is structures-related—subtracted 0.4pp from GDP growth in Q2 2016 and 0.2pp in Q3 2016. Investment spending decelerated from an average of +7% in 2014Q3-2016Q1 to -17% over the last two quarters. The less cyclical consumption component decelerated over the same period from 2% to 1% in real terms and now looks broadly in line with the currently still soft paces of hiring (0.5% year-on-year) and nominal ECI wage growth (2%) at the state and local level.

While the GDP data can be subject to revisions and other problems, other indicators support the idea that municipalities have indeed pulled back on spending. For example, the value of public construction contracts has declined by $25 billion (or more than 10%) since mid-2015 according to Dodge Data & Analytics, roughly in line with the Census Bureau’s estimate of the value of public construction put-in-place (left panel of Exhibit 2).[1] In addition, no single construction category appears to be driving the weakness: over the last year, construction spending has dropped in 11 out of the 12 subcategories in Census data (education-related construction is the only exception). The right panel of Exhibit 2 shows that a mix of infrastructure-related categories—including sewage and waste disposal, power, transportation and highway and street—account for most of the $22 billion decline in the value of state and local construction put in place over the last year.

Exhibit 2: The Decline in State and Local Construction Spending Runs Across Infrastructure Categories

Source: Department of Commerce, Dodge Data Analytics , Goldman Sachs Global Investment Research

Weakness in revenue growth likely explains part of the slowdown. State tax revenues rose by an average of $40 billion per year in 2010-2015 but declined $23 billion (annualized) in Q2 2016 vs. Q2 2015. Most of the deceleration in state tax revenues reflects softer individual income tax receipts, but declines in corporate income taxes and natural resource “severance taxes”—incurred when natural resources are extracted in a given state—also played a role. While state tax revenue has been weaker, local tax revenue has been holding up quite steadily, plausibly reflecting their relatively large reliance on property taxes, which lag home prices.

Exhibit 3: State Tax Revenue Has Declined

Source: Department of Commerce, Goldman Sachs Global Investment Research

State-level details suggest that the revenue weakness may relate to exposure to natural resource sectors and, to a lesser extent, the financial services sector. Exhibit 4 breaks down the growth of state tax revenues for three groups of states: the 9 energy states[2] (whose job growth is closely tied to changes in energy prices), the 3 finance states (New York, Connecticut and Delaware with a financial services employment share higher than 8%) and the 38 remaining other states. Exhibit 4 shows that the decline in state tax revenues has been significantly more pronounced since mid-2014 in the energy states than in the two other groups. Tax collection has also decelerated more sharply in the finance states—especially Connecticut—since mid-2015. Tax revenue growth has held up better in the other states, but has also slowed over the last year. Simple regression analysis supports the conclusion from the chart: the exposure to the energy job cycle[3] and the employment share in the financial sector are both statistically significant in explaining year-on-year growth rates of state-level tax revenues in 2016 Q2 and account for roughly 40% of the cross-state variation. In a nutshell, the weakness in state and local government spending—particularly on capital investments—looks real and appears to be driven by fundamentals.

Exhibit 4: Tax Revenues Have Declined More in States Exposed to Energy and Financial Services

Source: Department of Commerce, Goldman Sachs Global Investment Research

However dire the current situation is, Goldman however finds a silver lining…

That being said, we do not see a return to the municipal budget stress of the immediate post-crisis years (at least until unfunded pension obligations become a more immediate issue). Instead, state and local government spending looks more likely to rebound moderately over the coming year.

First, we expect overall GDP growth to accelerate, which should support tax revenues. Encouragingly, federal data available through Q3 suggests that individual income tax receipts have not slid further. Sales tax revenue has also underperformed retail sales over the last few quarters, and may have scope to rebound.

Second, our equity strategy colleagues still expect growing public construction spending over the next two years based on their analysis of state budget plans—and federal support for infrastructure spending could give an added boost.

Third, pension issues aside, most states have run their budgets more conservatively in recent years—aggregate “rainy day” funds, for example, bottomed at $21bn in FY 2010 but have since recovered to $49bn (according to NASBO). Unless the economy slows meaningfully, a lengthy period of municipal retrenchment looks unlikely.

Demographic biases, 'shy' Trump supporters, and 'tweaks' have turned this election cycle's poll trends into farce and propaganda. Once again, as the news gets worse by the hour for Hillary Clinton, The Burning Platform's Jim Quinn notes that the mainstream media polls over the last few days have again reverted to Clinton with a comfortable lead.

Really?? She's one email away from prison!

Her minions are talking.

The FBI is preparing to pounce.

But the Clinton News Network and the rest of the “in the bag for Hillary” press have the balls to publish polls showing her gaining ground.

The LA Times poll begs to differ.

It predicted Obama would win by over 3% in 2012 when the rest of the MSM polls had Romney winning.

As of a couple weeks ago this poll had Clinton in the lead. Things looked bleak after the audiotape. But, as of this morning it shows Trump with his biggest lead yet, 5.4%. That’s outside the margin of error.

He is picking up momentum as we approach the finish line. We’ll see who will be eating crow in in a few short days.

Last week I wrote that election week would be Hell Week all across the United States because of rage and violence and contested election results (regardless of who appears to win). I also warned that the week now past would prove to be a turbulent precursor to the coming chaos. True to that prediction, the week that started appropriately with Halloween turned into Hillary’s own personal Hell Week — a DNC nightmare that spread a chilling fog over the US stock market and gave shudders to the Wall Street and Pennsylvania Avenue establishment.

Falling stock market experiences longest losing streak in 36 years

The S&P 500 and the Nasdaq closed lower on Friday to make nine days of straight decline. The fall has been shallow (only 3% for the S &P), but the run has been long — the longest since December, 1980. The decline is also peculiar in that stock prices have almost always risen in the run-up to an election. The S&P also touched down to its 200-day moving average during the middle of the day Friday before recovering slightly. That is considered a critical red line.

The S&P has experienced similar but shorter declines three times times in the last twenty years, two of which signified major market changes. It did it when Lehman Bros. fell in 2008 and just before Standard & Poor’s downgraded the United State’s credit rating for the first time in history in July and August of 2011, after which the stock market plunged. So, a downhill run this long is associated with a bad turn of events and a market sell-off.

Both of those downhill runs had a steeper fall (29% and 15%). The third time was a spillover from the European crisis, and did not precede a stock-market crisis in the US (only a 9% fall).

There have been eight times when the S&P 500 descended gradually over the course of the three months preceding an election, as it this year. All of those declines were about the size of this one, and in seven out of the eight times, the incumbent party lost the presidency. It’s widely known that, at the end of the day, Americans vote their pocketbooks. Right now, Hillary’s poll numbers are declining faster than the stock market.

If I’m right that the reason the market has been flatlining (with a gradual decline) for months now is that the Fed and/or the US government are buying stocks through proxies to prop it up (see “Is the Fed Fix in for the election?“), then a 3% drop may be more significant than it sounds. If the market persists in falling, despite extraordinary efforts by the establishment to prop it up for the election, that could indicate a market that is so inclined to fall that it keeps slipping even with the price fixing in place.

To me, with all we’ve seen in FBI-seized emails and Wikileaks emails about the Democrats manipulating everything they can to win this election (from bussing in illegal voters in primaries to siding against Bernie inside the DNC to slanting polls by oversampling Democrat voters), it’s almost a given that the Obama Administration (with its huge increase in deficit spending at the end of summer) and the Fed (whose chair woman Trump intends to fire) are doing everything possible to keep the stock market from falling, as bad economic news would surely put a stake through Clinton’s heart.

Alternatively, the falling market could be the fixers’ strategy to make sure that everyone sees that Wall Street fears a Trump victory in order to convey the message that a Trump win will be a stock-market disaster — given that the market’s fall has timed out with Hillary’s own fall. In that case, they will pull their support efforts on purpose if Trump wins so he can take the fall for the Fed’s failure.

When they blame Trump for the market fall that comes if he wins, just bear in mind that stock markets don’t have disasters when recoveries are real and the economy is as fine as Obama has been telling us all that it is. They only crash when the structure is so rickety that it doesn’t take much to knock it into a shambles.

Hillary has fallen

This time it wasn’t just a trip on the stairs or fainting on the way into her getaway car. This time Hillary is falling politically as Democratic support shifted out from under her because of one scandal too many. The fulcrum for all events in this crazy week was the FBI director’s announcement of more problematic Clinton emails discovered on the computer of a sex fiend who is appropriately named after the body part that he loves to display. Given that the kinds of websites Wiener was fond of frequenting are notorious for putting spy ware on computers, one can be certain any confidential State Department emails that made it from Hillary’s server onto Wiener’s device had as much privacy as Wiener’s personal parts.

The decline in the stock market can be partially tied to Hillary’s decline in the polls because the market had been pricing in a Hillary victory. Wall Street feels more comfortable with Clinton (the status-quo candidate) than it does with Trump, and why shouldn’t it? Hillary loves banksters because they pay her handsomely just to come and talk with them.

Even the polls that were rigged by oversampling in favor of Hillary, as admitted by Democrats in their pilfered emails, plunged in less than a week from having Clinton in a seven-point lead to having Trump in the lead. Most of them eventually recovered a little to Hillary having a slight lead; but the race is much tighter than it was when I wrote a week ago that this week would be a bumpy ride. Now that the cat was let out of the bag by FBI Director Comey, the election that was largely viewed by mainstream media as ‘in-the-bag for Hillary is also out of the bag. One more hiccup in revelations about Hillary could cost her what small edge she has retained.

The final standing for the polls at the end of the week is that several of the swing states that Trump needs in order to win have moved from predicting victory for Clinton to a toss-up. Most significantly, the two are now tied in Florida and North Carolina, must-win states for Trump. Ohio, a major electoral prize has also moved into the toss-up category. Indiana has moved from “leans Republican” to “solidly Republican.” Little New Hampshire, not important for its electoral vote, has a reputation for choosing the president (in the sense that the way NH votes winds up being the way the US as a whole votes — at least in the primaries). NH has moved from the Democrat side of the ledger into a fifty-fifty split. Michigan is now also a fifty-fifty tie, as are swing states Colorado and Pennsylvania.

Hillary and Obama lose it

Naturally, this deconstruction in the Democratic Party has made Hillary desperate, and that desperation drove her this week to doing an even better job of living up to one of her moniker’s — Shrillary:

About three minutes into her 20-minute stump speech, a heckler shouted “Bill Clinton is a rapist!” as he waved a neon green sign declaring the same statement.

[Hillary] Clinton pointed a finger at the protester, and raged…

“I am sick and tired of the negative, dark, divisive, dangerous vision and the anger of people who support Donald Trump,…” Clinton shouted. (The New York Post)

Nothing divisive there on Hillary’s part — just dividing the nation into the “us and them” categories of her wonderful supporters versus the homicidal maniacs who believe in Trump. That’s particularly rich coming from a woman who is raging while she says it and whose campaign enticed hecklers to initiate actual physical violence at Trump’s rallies. Shrillary apparently loves D-words, instead of F-words, when she rants because you can add that set to her recent “deplorables” as a description of Trump supporters. Maybe that’s because the name “Donald” starts with a “D” so that letter haunts her mind.

If that’s how she divisively and negatively and darkly paints the half of all American voters who now stand on Trump’s side, then one has to wonder how far away marshal law is if Hillary wins the election and people continue to protest Hill or Bill when they, again, hold the Offal Office. Aren’t “divisive, dark and dangerous deplorables” the kind of people that require the nation be protected by the National Guard? One can see how thinking and speaking of people in such villainous terms will make it easier to justify military action against them.

Of course, I don’t doubt that some of Trump’s supporters are mad enough that a win by Hillary could cause them to resort to violence. That is unfortunately what sometimes happens when the establishment remains deaf to the proletariat for too long. A citizen’s revolt won’t be far off if the establishment wins this one, even when running a scandal-drenched candidate who is hated by many Democrats.

While the Dems try to paint the Trumpettes as being the ones who will cause violence in the elections, I think violence from Black People Matter is even more likely, and we have already seen violence against two Republican headquarters. The Twittererverse has already been running calls for Black people to get violent if Trump wins. Expect some angry immigrants, too — especially those that don’t mind being illegal in the first place. So, there is as much likelihood of rage and chaos from the Hillary side as Hillary said this week should be feared from the dangerousTrump side.

Hillary is not the only one growing more Shrill. The Commander in Chief lost control of this own crowd this week when the entire audience started booing a lone, aged person wearing a Trump shirt:

Obama repeatedly tried to get the focus off the protester and back on him, but failed.

“Hold up, hold up,” he said as the crowd booed.

Between smiles and stern looks, Obama finally snapped at his audience.

“Hey everybody, everybody, hey!” he yelled, growing increasingly impatient.

“Listen up! Hey! I told you to be focused and you’re not focused right now!” he shouted, pointing at the crowd.

“Listen to what I’m saying! Hold up!” he continued as the audience ignored him and continued chanting.

“Hold up!” he said several more times as the crowd continued to focus on the protester.

“Everybody sit down and be quiet. Everybody sit down and be quiet for a second. Now listen up! I’m serious, listen up!”

Obama went on to say the “older gentleman” was supporting his candidate and “he’s not doing nothing.”

But the crowd continued to boo and heckle the protester.

“This is what I mean about folks not being focused,” Obama said.

After telling the crowd to “not boo, vote,” the professor continued to lecture his audience. “Now, I want you to pay attention because if we lose focus, we could have problems.” (The American Mirror)

If Obama’s warning to the crowd about focus is right, it looks like Democrats could have problems because this crowd of Hillary supporters certainly lost its focus, and a rarely outwardly angry Obama lost all ability to control his own supporters. So, what’s coming the day after the election if Trump wins? Riots that an angry Obama is no more able to control than he was able to control his own audience?

Hillary leaks

And I’m not just talking about her Depends or her colostomy bag. The State Dept. issued a zinger on Friday, just four days before the election with the revelation that one of Hillary’s deleted (“personal”) emails was classified and was sent to Chelsea and several others not believed to have classified clearance.

Ironically, one of Hillary’s statement’s in the leaked email was,

“Wow — you can’t make this up — sorry to have missed all of that! Let me know if you learn anything else. (The Daily Caller)

ALL of the text from the body portion of the email was redacted before release by the State Dept. because of its confidential nature. Ah well, it’s just state secrets about foreign governments.

You are right, Hillary, you just can’t make this stuff up. It gets richer by the day.

Hillary is becoming Hellary, as happens around this time of year. Her crimes have coiled around her like a forked tail until she has forked herself only to find her goose is cooked. This Halloween Week Hellary emerged from her human form, and her DNC minions went wild. You can see it in the trembling stock market; you can see it in Hellary’s trembling rage as she rants against a protestor in the video linked to above, and you can see it in the president losing patience as Hillary’s supporters focus on a single protestor, instead of on the president of the United States.

You can see it in the latest sign of Hillary’s growing desperation that re-emerged late in the week: she back to ranting her Russian paranoia, employing her most desperate argument yet, which had something to do with one of Trump’s computer systems being on the same server as a Russian bank. (We all know how villains like to hang out together on the same internet servers, never mind that the server is not owned by Trump or by the bank.) Clinton said this proved that Trump is Pawn of Putin.

Even the New York Times, a dedicated Hillary supporter, said this latest move was desperate and had absolutely no basis in fact. Wikileaks’ founder, Julian Assange also came out and said that the Russian government was not the source of the leaks. (I don’t think he’s been shown to be lying in anything he’s said yet, which is exactly why government’s hate him so viscerally.)

If you must have a good Russian conspiracy, I think all of the evidence to election tampering in Trump’s favor should be spun something like this:

The Russians paid Clinton’s campaigners to hire illegal immigrants to stir up violence at Trump rallies so that they could, then, hack the same campaigners’ emails to prove her campaign was doing this. These are the same Russians who installed a badly worn, cold-war reset button at the base of Hellary’s brain stem that turns her legs off when she’s getting into vehicles or going up and down stairs or causes her to omit ordors that were rumored this week as being between rotting cabbage and pig urine. Sometimes the button’s wiring shorts and causes her head to bobble in a jerking fashion or causes her to utter shrill chirps when saying words like “TURRR-key.”

The faulty wiring is also responsible for her smile, which stretches straight back like the Cheshire cat or only curls up at the tips like the Joker’s, making one feel that she is dreaming of how she is eventually going to torture whatever critic she is smiling at. When they installed the button, the Russians failed to connect it to her eye sockets. As a result, her eyes don’t smile with her but continue to stare like a raptor targeting prey. This causes the subliminal disconnect her audience experiences that makes them want to run nauseous out of the theater like they did during the original projection of The Exorcist.

Her plastic skin is starting to melt, and her burned wires are showing, and her vocal lexicon has been reduced to just the stuttering d-d-d-section of the d-d-dictionary.

Politics can be a divisive topic, where issues and events can polarize the population into opposite sides of the spectrum. With this in mind, Lending Club took a look at the state of debt in the United States during this Presidential election race and break down how personal debt compares between red (Republican) and blue (Democrat) states.

So, when we take a look at average personal loan debt and credit card loan debt by state, what do the balance sheets say?

The answer: it’s close!

Below, we’ve compiled a graphic that shows whether red, blue, or battleground states have the most debt along with the top highlights.

Debt Overview Highlights:

Highest average personal loan debt:

Hawaii (Blue state)

It may be out in the middle of the Pacific Ocean, but residents of this vacation destination state are also big debtors, with an average personal loan debt of $11,327. Looks like surf’s not the only thing that’s up in Hawaii.

Lowest average personal loan debt:

New Mexico (Battleground state)

New Mexico was the setting for the hit TV series Breaking Bad, but it certainly looks like it’s not breaking the bank with a nationally-low $5,480 average of personal loan debt.

Highest average credit card debt:

Alaska (Red state)

Although some things may be frozen in Alaska, it looks like credit cards aren’t one of those things; the average credit card debt in the state is $6,778. Alaska residents, check out Lending Club’s personal loan calculator to see if you can consolidate your debt at a lower rate!

Lowest average credit card debt:

Iowa (Red state)

Taking the lead in more than just being the first state primary, Iowa also has good financial momentum when it comes to its average credit card debt of $4,299. It looks like Iowa knows how to caucus and keep their average credit card debt down.

Not to put too fine a point on it, but in the libertarian moral universe, liberal government programs are bad and private charity is good. In fact, one of the core libertarian arguments against government aid is not just that it is wasteful and inefficient but that it displaces private acts of philanthropy. Over time, this erodes a functioning civil society that thrives on voluntary altruism that Alexis de Tocqueville praised as the true and unique spirit of America. (Sorry Ayn Rand!)

This is one reason — beyond just ordinary human decency — that libertarians should be particularly alarmed that alt-righters are now going after Chobani yogurt founder Hamdi Ulukaya for using his own money and his own resources to help resettle Syrian refugees legally admitted into America after “extreme vetting.” (It takes up to three years of screening by multiple agencies before refugees are admitted into the country which is why the risk of an American being killed by a refugee-perpetrated terrorist attack is one in 3.6 billion, lower odds than dying by their clothes catching fire. Even then, since Syria’s civil war began in 2011, the U.S. until last year had admitted fewer than 1,600 of Syria’s estimated four million refugees. After a lot of international shaming, the Obama administration took in 10,000 Syrian refugees this year, still a pittance given that more people have been displaced in this conflict than in World War II.)

As I noted in my Reason feature, “Muslim in America,” post 9-11, a cottage industry of Muslim baiters has sprouted in this country that has turned demonizing Muslims from a hobby to a livelihood. Led by Pamela Geller of the Draw-the-Mohammad-Cartoon fame and gutter sites such as World Net Daily and Breitbart, they make their living off of depicting every Muslim community in America as a precursor to a caliphate in the United States. And now they’ve all turned their collective sights on Chobani’s Ulukaya.

Ulukaya, a Muslim, is the kind of immigrant success story that has Made America Great – Again and Again and Again. He came as a student in the 1990s to New York from a Turkish town near Syria. But within a few years, he started selling feta cheese and kosher yogurt made from his family recipe to a Long Island grocery store. His products were so popular that by 2005 he had purchased a defunct Kraft factory with an $800,000 loan and within 10 years turned it into a $1.5 billion yogurt empire employing 2,000 people with plants in New York and Twin Falls, Idaho. In fact, during my recent visit to Syracuse, an old white cab driver who drove me to Colgate University regaled me with stories all the way of just what a boon Chobani had been to local dairy farmers (the company purchases 4 million pounds of milk everyday) and local youth looking for decent employment (Ulukaya pays workers far above minimum wage, offers generous benefits such as company-paid maternity leave and recently pledged to give away 10 percent of the company’s shares to employees).

But because Ulukaya is an immigrant himself, even before the current refugee crisis, he had made it a point to hire fleeing refugees, both in upstate New York and Idaho which has a history of resettling refugees that dates back to at least the 1970s when the Vietnamese Boat People started arriving on America’s shores. Indeed, Idaho, which for half a century has relied on immigrant labor for its agricultural economy, has among the largest refugee populations in the country on a per capita basis. And Ulukaya has always employed these refugees – first Nepalese, Vietnamese and others – and now also Syrians and other Muslims. About 30 percent of Ulukaya’s Twin Falls factory labor force is composed of refugees because, he believes, “the minute a refugee has a job, that’s the minute they stop being a refugee” — and, one might add, they become far less likely to rely on government welfare. He offers them transportation from their camps and special translation services to help them settle into their new workplace. None of this costs local taxpayers a dime. Nor does it displace native workers given that unemployment in Twin Falls is less than 4 percent.

All of this is not just laudable, but entirely in keeping with America’s pre-welfare state tradition in the early 20th Century when fraternal organizations of various ethnic groups funded by members provided insurance and other social services to new arrivals, as University of Alabama libertarian economist David Beito has richly documented.

But where most people see goodness and success, alt-righter nativists see darkness and danger.

Chief anti-Muslim conspiracy monger Geller got the ball rolling against Ulukaya this summer. She dubbed his plea during the annual Davos summit to corporate CEOs to assist Syrian refugees as “stealth jihad in Davos.” This Cassandra warned these companies that if they employ fleeing Muslims they should be prepared for lawsuits for prayer rooms, prayer times, or stopping the line for Islamic rituals. “He [Ulukaya] is Muslim — they won’t hurt him,” she declared. “But mark my words: Airbnb, LinkedIn, MasterCard, UPS and IKEA will all be the target of Islamic supremacists.”

World Net Daily followed suit with its own charming little anti-Ulukaya jihad, running a piece with a headline – subsequently changed, as The Daily Beast’s Jamie Kirchik reported — “American Yogurt Tycoon Vows to Choke U.S. With Muslims.” The story claimed, falsely, that refugees were being sent to Twin Falls specifically to work at the Chobani plant.

The worst, however, was Breitbart that dedicated a reporter to filing regular dispatches from Twin Falls. One dispatch misleadingly linked an alleged 500 percent spike in tuberculosis a few years ago to the opening of a Chobani plant. The spike consisted of six cases over eight counties, not just in Twin Falls, up from one case the year before. But the real kicker, Kirchik notes, is that none of cases were found to be Chobain employees. Another “story” — in the true sense of the term — mischaracterized an inappropriate sexual encounter of minor refugee boys with a five-year-old girl as a “gang rape.”

A white nationalist organization misnamed the American Freedom Party used such ammo for robocalls all across Idaho to discredit the state’s refugee resettlement program by informing listeners that the “nonwhite invasion of their state and all white areas constitutes white genocide.” This is the same racist outfit that endorsed Trump, points out Kirchik, calling him the “Great White Hope,” and paid for robocalls on his behalf in the run-up to the Iowa caucuses.

Accusing immigrants of bringing disease, crime and debauchery is a perennial leaf in the nativist playbook. Indeed, 150 years before Breitbart and WND arrived on the scene, nativist, Know Nothing publications such as WASP and Judge were running cartoons depicting immigrants as harbingers of “disease, immorality and filth.”

But an added twist in the age of social media, reportedThe New York Times last week, is that alt-righters have mobilized on twitter to issue death threats not just against Ulukaya but also Shawn Barigar, the mayor of Twin Falls. The rap against Barigar is that he is a “globalist corporatist” who is colluding with Ulukaya to help him secure cheap labor and Islamicize America — accusations that have ominous and obvious parallels with anti-Semitic Nazi propaganda that accused Jews of taking over international banks in order to undermine Western civilization.

Chobani’s saga shows of course the ongoing radicalization of the restrictionist movement both in its demands and its methods. No longer is it content on calling into the Rush Limbaugh and other right-wing talk shows to oppose amnesty for illegals in the name of an alleged rule of law. Now it touts its nativism openly and makes no pretense of its agenda to stop all immigration — family-based, refugees, economic migrants including, mind you, the high-skilled variety that Alabama Republican Senator Jeff Sessions, a nativist hero, recently attacked at a Trump rally, suggesting that the H-1B visa program for foreign techies should be scrapped. And it is willing to use any means necessary to accomplish its ends — including violence and intimidation to stop private acts of charity by private individuals on trumped up (no pun intended) charges of harm to natives.

This is a profoundly indecent and anti-freedom movement that should spook all decent people, but especially libertarians.

We look at the funding currencies for the risk on versus risk off mode of evaluating financial market capital flows from an investing standpoint. You are swimming upstream in a Carry Unwinding Mode like a Salmon. Check out the main components of the US Dollar Index and compare their interest rates versus the United States. This serves as the fundamental basis for the Carry Trade Structure, and we have seen major deleveraging of these Carry Trades before the Presidential Election this upcoming Tuesday. Look for these trends to reverse after the election event is over with next week.

"The strongest form of persuasion is fear," explains Dilbert cartoon creator Scott Adams, and Clinton’s team of persuaders has convinced her followers that Trump is dangerous. As Adams details, if you remove that part of her spell, Trump wins. Here’s how…

1. Trump’s Tough Talk Inspires violence: Ask Clinton supporters if they have seen the Project Veritas video of Clinton operatives talking about paying people to incite violence at Trump rallies. The people on the video have been fired, and we haven’t seen violence at Trump rallies since.

2. Temperament: Ask Clinton supporters if they have seen the video of Clinton ranting “Why aren’t I already fifty points ahead?” She looks either inebriated or deranged. Mention that the people who know Trump personally have reported that he is both smart and sane in person. Even his enemies who know him personally don’t claim he has a temperament problem. If he did, is there any chance we wouldn’t have heard about it by now?

3. Trump might insult foreign leaders into a war: Trump and Putin seem to get along fine. Netanyahu said he could work with Trump. Mexico isn’t likely to start a war over trade, or the wall. Trump says North Korea is China’s problem, which is literally the safest thing you could say. And China’s leaders are adults who know Trump says offensive things now and then. China will pursue its own interests, and none of those interests involve going to war over some words. Likewise, other leaders are adults too. They won’t change their foreign policy over some insults.

5. Trump might start a war: Trump owns buildings and property around the world. As a general rule, people who own a lot of real estate don’t start wars because their own assets are at risk. But Clinton is “sponsored” – via the Clinton Foundation and speaking fees – by defense companies that profit from war. Likewise, Clinton is sponsored by foreign countries whose interests don’t align with American interests. Clinton supported war in Iraq and Libya, and she threatens Russia, just as the money trail suggests she would. Trump talks mostly about having a strong military to avoid war. He gains nothing by war.

6. Alcohol: Normally alcohol would not be a risk factor in picking a president because usually both candidates are social drinkers. But Trump has never had an alcoholic beverage while Clinton tells us she enjoys social drinking. Having a few social drinks is not a problem unless you plan to drive a car…or make a nuclear launch decision. If we don’t trust a social drinker to operate a motor vehicle, can we trust a social drinker to manage a nuclear arsenal?

If you have ever drunk-texted, or received a text from someone who has, you already know how much “social drinking” can influence decisions.

7. Group Violence versus Crazy Individuals: Have you noticed that when you see election-related violence from a group, it is always Clinton supporters? That happened at Trump’s San Jose rally, and it happened with the homeless woman protecting Trump’s star on the Walk of Fame. When Trump supporters do something violent they are usually acting alone, and crazy. When Clinton supporters get violent it comes in the form of mobs who are NOT crazy. That’s the dangerous kind of violence because they are literally Stronger Together.

8. Pacing and Leading: When normal politicians change their minds we label it flip-flopping or – more kindly – “evolving” in their thinking. When a Master Persuader does it, you are seeing pacing and leading, which is a major tool of persuasion. Pacing involves matching people – in this case emotionally – and later using that bond to lead them. We see Trump doing this often.

a. Trump paced his base by saying he would deport 11 million undocumented immigrants. Once he had his base on his side emotionally, he led to them to his current policy of deporting only the people who committed crimes while here. Have you heard any Trump supporters complain about it lately?

b. Trump paced his base by saying he would ban all Muslim immigration to stop terrorist infiltration. Once he had them on his side emotionally, he led them first to a ban on specific problem countries, and then again to “extreme vetting,” which is a lot like Clinton’s plan. Trump supporters followed, and you don’t hear them complaining.

c. Early in the primaries Trump paced the racists in the Republican party by not disavowing them as clearly and as loudly as even the racists thought he would. Since then he has led Republicans to think that some form of a “New Deal” for African-Americans might be worth a look.

d. At the Republican National Convention, Trump used his emotional connection to his supporters to declare he was the strongest voice to protect the LGBTQ community. Republicans stood and cheered.

Months ago, Adams predicted that Trump would soften his immigration proposals, as he saw him from the start as a Master Persuader, not a crazy person, and not a common flip-flopper.

In my opinion, Trump might be the safest president we have ever had.

He can lead the dark parts of his base toward the light (as Nixon went to China) and he has no incentive for war.

Claims about his “temperament” are mostly about his penchant for insults, and that isn’t a mortal danger to anyone.