From Sean Corrigan of Diapason Commodities Management

No Zero Bound on Reason

Now it may be that Professor Krugman can insist that the grossly inequitable distributional effects which this brings about – letting the GINI out of the bottle as we have elsewhere categorised it – are somehow benign (his irrational hatred of the thrifty clearly overlapping with his bien pensant contempt for the rich with whom he presumably identifies them and thus overcoming his equally demagogic distaste for bankers). But we are far more sympathetic to the analysis presented by that eminently more reputable economist, Axel Leijonhufvud, who, in an address to Cordoba University in Argentina a few months back, dealt decisively with just this malign side-effect of the central banks’ ‘every tool is a hammer’ approach to policy, declaring that:

“Most of all, reliance on monetary policy has the inestimable advantage that its distributive consequences are so little understood by the public at large. But relying exclusively on monetary policy has some unpalatable consequences. It tends to recreate large rewards to the bankers that were instrumental in erecting the unstable structure that eventually crashed. It also runs some risks. It means after all doubling down on the policy that brought you into severe trouble to begin with.”

Prof. Leijonhufvud, noting that the privileges extended to our limited liability money-creators are ‘in effect transfers from taxpayers as well as from the mostly aged savers who cannot find alternate safe placements for their funds in retirement’ and talked of the effortless enrichment to be had by those who can borrow at near zero rates from the central bank and leverage it up multiple times to buy higher-yielding government paper, all the while patting themselves on the back – and padding themselves in the pocket – for their genius.

Coincidentally, we were sent a report condemning the large French banks’ lack of progress in restoring their finances to anything resembling a structure which could endure the slightest adverse gust were all these implicit and explicit state guarantees not so readily extended to them. Taking a quick look – more at random than out of any more studied approach to finding the worst offender – we checked the broad-brush financials for one of them, Credit Agricole, on the Bloomberg.

Mon vieux CA disposes of assets of around €1.8 trillion – not far short of a year’s worth of French GDP – against which it holds in reserve an official ‘Tier 1 Risk- Based Capital Ratio’ of 10% and a ‘Total Risk-Based Capital Ratio’ of what looks likely a highly conservative 15.4%. But therein lies the rub – namely, in the weasel words ‘Risk-Based’ and ‘Tier 1’. If we look at a good, old-fashioned measure like, say, tangible common equity to total assets, the cushion between continued existence and business failure falls to the exiguous level of 1.27%.

Putting that another way, for every euro of equity to hand, this one bank has piled €78.74 of assets – funding a hefty portion of them, no doubt with the BdF’s favourite little, officially-endorsed, ECB collateral-eligible, exceedingly short-dated TCNs. Our good Swedish professor would be in danger of choking on his smorgasbord if he were to read of such a degree of state-sponsored hyperextension.

We would also gently remind the reader here that, in Hayek’s sophisticated reading of the economic problems we create for ourselves which we quoted above, he relied heavily on a similar concept of distributional unevenness – rather than of an indiscriminate aggregate shortfall – for an explanation of why the Gutenberg School of Economic Quackery should never be allowed the final word.

So, no, Prof. Krugman, savers cannot presume to be ‘guaranteed’ a positive real return on the sums they set aside (though you no doubt hope that those looking after your own, no doubt substantial nest egg will manage to achieve this very feat). But what they can rightly demand from a just society is that the only risks they run are everyday commercial ones and they are not systematically robbed by feckless politicians following the kind of crude leftist trumpery which you and your kind never cease to espouse.

Finally, no treatment of these issues would be complete without a brief nod to the spreading predilection for invoking an explanation for the inconvenient fact that we are not responding in textbook fashion to the potions, poultices, and bleedings being administered to us by our leeches at the central banks. This is the hackneyed old idea that we have somehow lapsed into a period of ‘secular stagnation’ – a wasting disease wherein our utter satiety with all the riches which a technologically mature society can shower upon us leaves us enfeebled and enervated, all compounded by the fact that our ineffable ennui has led us to procreate with ever decreasing regularity to the point it is threatening, horror of horrors, to make our blue sapphire of a planet a little less crowded than once we feared it might become.

Heaven forbid, but the latest sermoniser to propagate this nonsense was none other than Larry Summers – the man some thought might actually be a bit, well, less open-handed had anyone had the temerity to risk installing him as Blackhawk Ben Bernanke’s successor – suggesting that maybe Madame Yellen was not the worst choice, after all.

Dear old Larry has come over all Zero Bound constipated, fretting that the natural, real rate of interest has somehow become fixed down there at negative 2%-3% where conventional policy (if you can still remember of what that used to consist) cannot get at it – unless we blow serial bubbles, that is, these episodes in mass folly and gross wastefulness now being raised to the level of such perverse desiderata of which Krugman’s only partly-facetious call for a war on Mars forms an infamous example.

In fact, this entire notion is another piece of nonsense to spring from the one of Keynes’ least cogent ramblings, the notoriously insupportable notion of ’Liquidity Preference’ – a logical patch fixed over the lacunae in his reasoning when, having insisted that saving must always equal investment, all he could think of to determine the rate of interest was our collective desire to hold money for its own sake. From such intellectually bastard seed soon sprang, fully-armed like Minerva from the head of our economic Jove, the even worse confusion of the ‘Liquidity Trap.’

Not only Austrians, not only Robertsonians, not only Wicksellians like our man Axel Leijonhufvud have shown this to be a nonsense – easy enough since all of these generally look in some way at the balance being struck between the funds made available for loan according to potential savers’ subjective degree of time preference and the eagerness with which these funds are sought with regard to would-be entrepreneurs’ estimations of the profitability of their projects. But even Keynes himself all but confessed he had the whole thing backwards less than a year after that infernal tract, ‘The General Theory’, was first published.

Responding then to concerted criticism of his peculiar concept of interest rate determination as an internal mental conflict conducted in the heads of ‘framing’- prone, stick-in-the-mud, ‘college bursar’ bond-buyers who would, he felt, resolutely reject unusually low market rates on gilts in favour of accumulating cash hoards , he was forced to admit that the main part of that demand for money which he found to be the root of all macroeconomic evil was not at all related to people’s supposedly irrational desire to hoard it for its own sake, but rather was due to their wholly unobjectionable aim of ensuring a ready supply of funds prior to making planned outlays from them, s

omething Keynes, with uncharacteristic humility, admitted in print that he ‘should not have previously overlooked’.

Since Summers himself made reference to a man dubbed the ‘American Keynes’ – that avid New Dealer Alvin Hansen – who raised this spectre, seventy years ago, let us also refer the reader to the complete dismissal of this strain of thought accomplished by George Terborgh in his contemporary 1945 work, ‘The Bogey of Economic Maturity’.

As Terborgh summarised in what he called a ‘thumbnail sketch’ of this theory:-

‘Formerly youthful, vigorous, and expansive… the American economy has become mature. The frontier is gone. Population growth is tapering off. Our technology, ever increasing in complexity, gives less and less room for revolutionary inventions comparable in impact to the railroad, electric power, or the automobile’

— Robert Gordon and Tyler Cowen are hardly the trailblazers they like to imagine they are, either, it appears –

‘The weakening of these dynamic factors leaves the economy with a dearth of opportunity for private investment… Meanwhile… savings accumulate inexorably… and pile up as idle funds for which there is not outlet in physical capital, their accumulation setting in motion a downward spiral of income and production… the mature economy thus precipitates chronic over-saving and ushers in an era of secular stagnation and recurring crises from which there is no escape except through the intervention of government.’

‘In short, the private economy has become a cripple and can survive only by reliance on the crutches of government support.’

Two hundred-odd closely-argued and empirically-rich pages later, Terborgh sums up as follows:-

‘If… we suffer from a chronic insufficiency of consumption and investment combined, it will not be… because investment opportunity in a physical and technological sense is persistently inadequate to absorb our unconsumed income; but rather because of political and economic policies that discourage investment justified, under more favourable policies, by these physical factors.’ Here! Here!

As Wikipedia laconically notes in its biographical sketch of Terborgh’s protagonist, Hansen, the verdict of history was unrelenting:-

‘The thesis was highly controversial, as critics… attacked Hansen as a pessimist and defeatist. Hansen replied that secular stagnation was just another name for Keynes’s underemployment equilibrium. However, the sustained economic growth beginning in 1940 undercut Hansen’s predictions and his stagnation model was forgotten.’

So, why should we not forget it, too? Only because, as Terborgh was only too aware, the popularity of such views is a gilt-edged invitation for continued, large-scale interventionism by the Bernankes, Summers, and Yellens of this world and there will surely come a point where the slow drip, drip of these will utterly undercut the foundation of our modern order and usher in to office a much darker series of opportunistic overlords and aspiring saviours.

On that somewhat sombre note, we will leave matters for now, with only this series of question to ask of our present leaders by way of an epilogue:

If, as you and your ilk mostly do, you affect to fear that we are somehow exhausting the planet’s capacity to give our species a domicile, how can you also be worried that we may be slowing down, dying out, and using less—and doing so, moreover, in a wholly voluntary fashion?

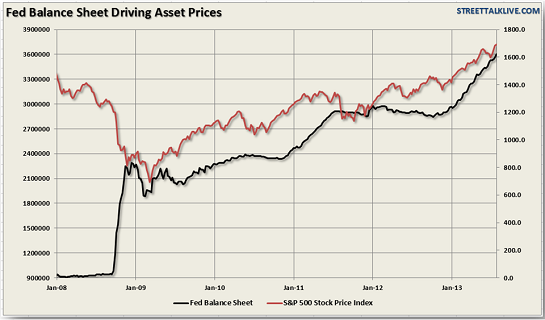

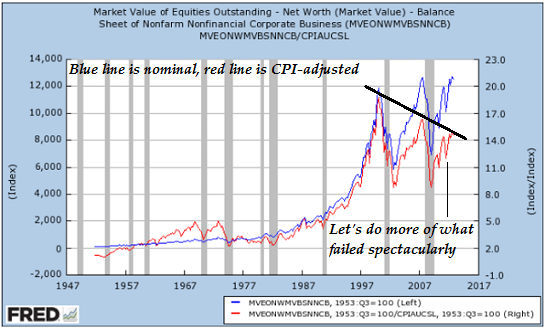

Furthermore, if you really do believe that we are on the verge of such a ‘stagnation’ as you describe—with all it implies for the potential dwindling of income streams and the drying up of future returns on capital—how can you reconcile the current, extraordinary buoyancy in the stock market with your firm insistence that no part of the policies you have been implementing can have contributed to what must therefore be an untoward degree of optimism in the valuation of its components?

Answers, please, on a postcard.

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/TkaqQ6fAT6I/story01.htm Tyler Durden