.

.

.

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/GXPrUnR30TY/story01.htm williambanzai7

another site

.

.

.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/GXPrUnR30TY/story01.htm williambanzai7

.

.

.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/GXPrUnR30TY/story01.htm williambanzai7

How many U.S. citizens end up pleading guilty in

How many U.S. citizens end up pleading guilty in

a courtroom each year without ever getting access to an attorney?

In which counties are pre-trial detainees least likely to obtain

release through bail? Greg Beato suggests that instead of spying on

us, the government use its technological power to data-driven

oversight to the nation’s halls of justice.

from Hit & Run http://reason.com/blog/2013/11/14/greg-beato-on-number-crunching-the-court

via IFTTT

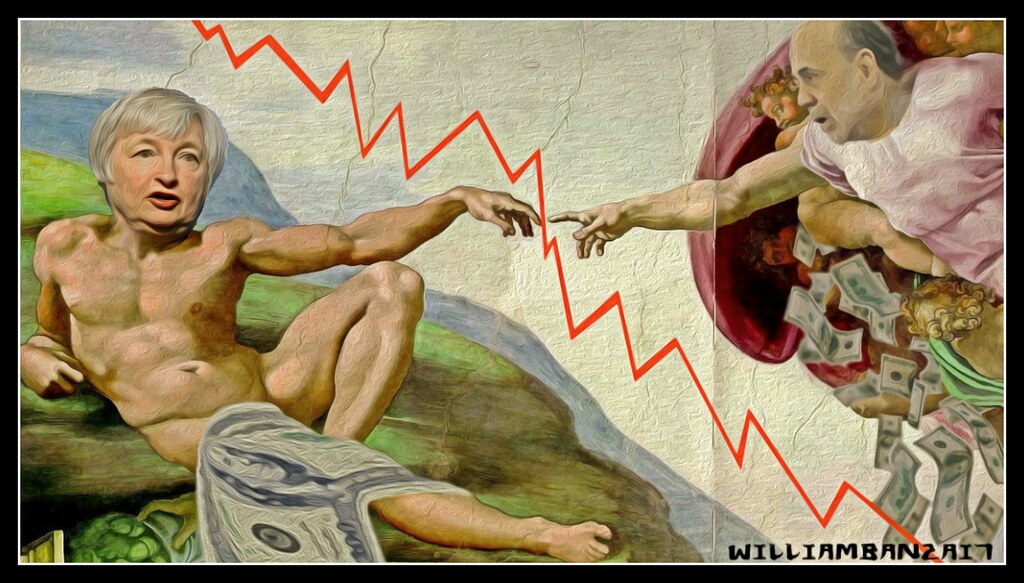

Following our earlier preview, we expect the Q&A to have some potential fireworks as the politicians demand she "get to work" as soon as possible. If you are playing buzzword bingo at home – drink if she says "bubble", "depression", "data-dependent", "fiscal", or "screw you Schumer."

Live feed from Senate:

Live feed via Bloomberg (click here if embed is not functioning):

Live feed from C-Span – click image for feed.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/FxH2lGliilA/story01.htm Tyler Durden

Following our earlier preview, we expect the Q&A to have some potential fireworks as the politicians demand she "get to work" as soon as possible. If you are playing buzzword bingo at home – drink if she says "bubble", "depression", "data-dependent", "fiscal", or "screw you Schumer."

Live feed from Senate:

Live feed via Bloomberg (click here if embed is not functioning):

Live feed from C-Span – click image for feed.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/FxH2lGliilA/story01.htm Tyler Durden

On any other 30yr auction day, i would be selling 30yr bonds right here (9am in NY) (30yr bond yield @ 3.79% and UB futures @ 140-21 both higher in price by 4 basis points on the day) in anticipation of the 16bln 30yr bonds (32bln 10yr equivalents) to be auctioned in 4 hours.

(pictures 30yr UB bond futures vs inverse DX)

However, today is not any other day. Unemployment claims are slightly up…more than expected, labor productivity is up, and unit labor costs are down. All of these point to no desire to increase hiring. That is bad for the consumer (because the consumer is labor), and hence bullish for bonds. These numbers ought to also be bearish for stocks (a weaker consumer does not increase spending)…but it seems the QE fever is still keeping S&P futures high before the open. In a world where more QE = higher stock prices…Yellen’s prepared remarks released yesterday made no mention of taper, and were highly supportive of QE continuation (though she did not explicitly state that). The remarks were vague, but erred on the side of continuing current accommodative policy (so, QE-4-ever).

This causes a conundrum. Regardless of Yellen’s testimony and Q&A session this morning, there will still be a 30yr bond auction at 1pm (ET). Given the strength and low volume yesterday, and the current bullish tone of the bond market (4bps stronger from yesterdays closes) the bond market does not feel like there is a significant setup of short 30yr positions. This must take place before the auction. Primary dealers must each bid for their pro-rata share of the auction (so about 800mm each). No dealer wants to come out of a 30yr bond auction long 800mm 30yr bonds…its just too much risk in a world where directional risk is shunned.

This is the backdrop in the minds of bond traders as we approach Yellen’s testimony and Q&A session. We will be reacting to her testimony with this in mind. However…to be clear…if she does not indicate a desire to extend QE (either in fact, or by indicating a lower unemployment threshold) then there should be good selliing of 30yr bonds to setup for the 1pm 30yr bond auction.

Typically, bond traders want to come out of the 30yr bond auction long bonds…but typically that occurs from a very low price, as the market usually sells off going into the auction. Today that is not the case (so far). I expect today to have unusually high volatility in the bond market….but we will just have to wait and see.

I’ll be active on twitter today…so feel free to join in the conversation.

http://govttrader.blogspot.com/

https://twitter.com/govttrader

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/F08nAmtHL_4/story01.htm govttrader

“Give Us Cash or Lose Your Kids and Face Felony Charges: Don’t

Cops Have Better Things to Do?!” is the latest video from ReasonTV.

Watch above or click on the link below for video, full text,

supporting links, downloadable versions, and more Reason TV

clips.

from Hit & Run http://reason.com/blog/2013/11/14/give-us-cash-or-lose-your-kids-and-fac

via IFTTT

This evening I’m going to be moderating a talk by Paul Cantor at

George Mason University. The topic is “The

Economics of Apocalypse: Flying Saucers, Alien Invasions, and the

Walking Dead.”

Everywhere we look in pop culture today, the world is

coming to an end. Whether it’s the result of natural disasters,

alien invasions, or zombie plagues, our way of life is threatened

and our institutions are crumbling, leaving Americans to fend for

themselves (or prey upon each other).Drawing upon his new book, The

Invisible Hand in Popular Culture: Liberty vs. Authority in

American Film and TV, University of Virginia Professor of

English Paul Cantor will discuss opposing visions of individualism

vs. collectivism in today’s catastrophe narratives.

The event will begin at 7 and end at 8:30. You can find us at

Founders Hall Auditorium on GMU’s Arlington campus, at 3351 Fairfax

Drive.

from Hit & Run http://reason.com/blog/2013/11/14/tonight-jesse-walker-and-paul-cantor-dis

via IFTTT

Earlier today consulting company McKinsey, which has now become the new Moody’s, released a 72 page report titled “QE and ultra-low interest rates: Distributional effects and risks” which contains the following pearls of wisdom: “The impact of ultra-low rate monetary policies on financial asset prices is ambiguous. We found little conclusive evidence that ultra-low interest rates have boosted equity markets. Although announcements about changes to ultra-low rate policies do spark short-term market movements in equity prices, these movements do not persist in the long term.” Uhh, does McKinsey have an S&P chart that goes back to 2008? One would think whoever commissioned this report can at least pay for “bigger charts.” Continuing: “Moreover, there is little evidence of a large-scale shift into equities as part of a search for yield. Price-earnings ratios and price-book ratios in stock markets are no higher than long-term averages.”

We will spare any analysis, in-depth or otherwise, of the report: it merits none, and certainly not for those who watch the farce that the “market” has become.

Sadly, by issuing such drivel McKinsey has just tarnished what little reputation and credibility it may have had.

Instead we will just point out, visually, what McKinsey is saying: namely that the chart below which shows the causation between the S&P and the Fed’s balance sheet, doesn’t exist and is purely a figment of overactive realists’ imaginations.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/3ZKVsxI5i9M/story01.htm Tyler Durden

Earlier today consulting company McKinsey, which has now become the new Moody’s, released a 72 page report titled “QE and ultra-low interest rates: Distributional effects and risks” which contains the following pearls of wisdom: “The impact of ultra-low rate monetary policies on financial asset prices is ambiguous. We found little conclusive evidence that ultra-low interest rates have boosted equity markets. Although announcements about changes to ultra-low rate policies do spark short-term market movements in equity prices, these movements do not persist in the long term.” Uhh, does McKinsey have an S&P chart that goes back to 2008? One would think whoever commissioned this report can at least pay for “bigger charts.” Continuing: “Moreover, there is little evidence of a large-scale shift into equities as part of a search for yield. Price-earnings ratios and price-book ratios in stock markets are no higher than long-term averages.”

We will spare any analysis, in-depth or otherwise, of the report: it merits none, and certainly not for those who watch the farce that the “market” has become.

Sadly, by issuing such drivel McKinsey has just tarnished what little reputation and credibility it may have had.

Instead we will just point out, visually, what McKinsey is saying: namely that the chart below which shows the causation between the S&P and the Fed’s balance sheet, doesn’t exist and is purely a figment of overactive realists’ imaginations.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/3ZKVsxI5i9M/story01.htm Tyler Durden