9/29/2005: Chief Justice Roberts takes oath.

from Latest – Reason.com https://ift.tt/3kQm8L0

via IFTTT

another site

9/29/2005: Chief Justice Roberts takes oath.

from Latest – Reason.com https://ift.tt/3kQm8L0

via IFTTT

Our news roundup is dominated by the seemingly endless ways that the US and China can find to quarrel over tech policy. The Commerce Department’s plan to use an executive order to cut TikTok and WeChat out of the US market has now been enjoined. But the $50 Nick Weaver bet me that TikTok could tie its forced sale up until January is still at risk, because the administration has a double-barreled threat to use against that company – not just the executive order but also CFIUS – and the injunction so far only applies to the first.

I predict that President Xi is likely to veto any deal that appeals to President Trump, just to show the power of his regime to interfere with US plans. That could spell the end of TikTok, at least in the US. Meanwhile, Dave Aitel points out, a similar but even more costly fate could await much of the electronic gaming industry, where WeChat parent TenCent is a dominant player.

And just to show that the US is willing to do to US tech companies what it’s doing to Chinese tech companies, leaks point to the imminent filing of at least one and perhaps two antitrust lawsuits against Google. Maury Shenk leads us through the law and policy options.

The panelists dismiss as PR hype the claim that it was the threat of “material support” liability that caused Zoom to drop support for a PFLP hijacker’s speech to American university students. Instead, it looks like garden variety content moderation aimed this time at a favorite of the far left.

Dave explains the good and the bad of the CISA order requiring agencies to quickly patch the critical Netlogon bug.

Maury and I debate whether Vladimir Putin is being serious or mocking when he proposes an election hacking ceasefire and a “reset” in the cyber relationship. We conclude that there’s some serious mocking in the proposal.

Dave and I also marvel at how Elon Musk, for all his iconoclasm, sure has managed to cozy up to both President Xi and President Trump, make a lot of money in both countries, and take surprisingly little flak for doing so. The story that spurs this meditation is the news that Tesla is so dependent on Chinese chips for its autonomous driving engine that it’s suing the US to end the tariffs on its supply chain.

In quick hits and updates, we note a potentially big story: The Trump administration has slapped new restrictions on exports to Semiconductor Manufacturing International Corporation, China’s most advanced maker of computer chips.

The press that lovingly detailed the allegations in the Steele dossier about President Trump’s ties to Moscow hasn’t been quite so enthusiastic about covering the dossier’s astounding fall from grace. The coup de grace came last week when it was revealed that the main source for the juiciest bits was flagged by the FBI ten years ago as a likely Russian foreign agent; he escaped a FISA order only because he left the country for a while in 2010.

The FISA court has issued an opinion on what constitutes a “facility” that can be tapped with a FISA order. It rejected the advice of Cyberlaw Podcast regular David Kris in an opinion that includes all the court’s legal reasoning but remains impenetrable because the facts are all classified. Maury and I come up with a plausible explanation of what was at stake.

The Trump administration has proposed section 230 reform legislation similar to the white paper we covered a couple of months ago. The proposal so completely occupies the reasonable middle of the content moderation debate that a Biden administration may not be able to come up with its own reforms without sounding fatally similar to President Trump.

And in yet more China news, Maury and Dave explore the meaning of Nvidia’s bid for ARM, and Maury expresses no surprise at all that WeWork is selling off a big chunk of its Chinese operations

Oh, and we have new theme music, courtesy of Ken Weissman of Weissman Sound Design. Hope you like it!

Download the 330th Episode (mp3)

You can subscribe to The Cyberlaw Podcast using iTunes, Google Play, Spotify, Pocket Casts, or our RSS feed. As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect the opinions of their institutions, clients, friends, families, or pets.

from Latest – Reason.com https://ift.tt/3n2WvIM

via IFTTT

Confirmed COVID-19 Deaths Top 1 Million Mark, With Many More Uncounted: Live Updates

Tyler Durden

Tue, 09/29/2020 – 06:59

Summary:

* * *

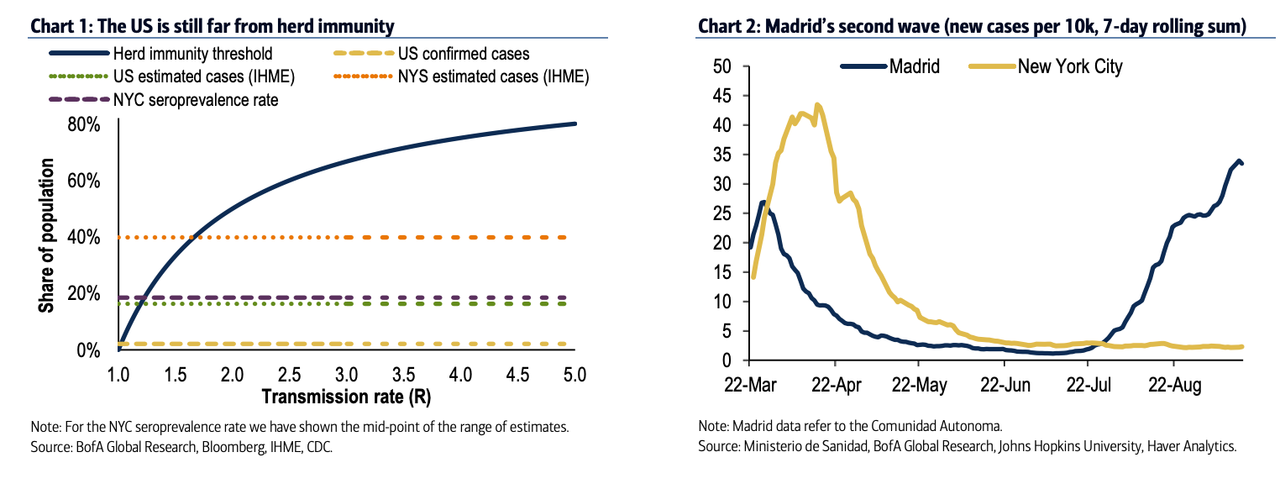

Update (0730ET): With the virus’s mortality rate in focus Tuesday morning, we’d like to share with readers some findings from a Bank of America note exploring the concept of “herd immunity”. A population is said to have “herd immunity” when the number of people who have already been sickened (and therefore now have immunity, at least in theory) exceeds the outcome of the formula “1 – (1/R)” where “R” is the transmission rate of the virus, ie the average number of people infected by each person with COVID-19. When the transmission rate drops below 1, the virus is said to be slowing.

The intuition, according to the BofA team, is that if the share of the population with immunity – we’ll call that “P” – is greater than the herd immunity threshold, or 1 – (1/R), then the probability that a person who is exposed to the disease gets sick – which is always (1 – P) – would be less than 1/R, or the rate of spread. Therefore the average number of people infected by each person who is exposed to the disease is less than one, since R*(1 – P) < 1, and so the disease dies out instead of spreading.

Where does that leave the US?

Of course, finding accurate numbers to plug in for these variables is harder than it seems since most of the “herd” isn’t “branded”, as BofA points out.

* * *

As outbreaks in New York, Moscow, London, Madrid and Marseilles intensify, the death toll for the global COVID-19 pandemic topped 1 million, according to the latest batch of mortality data reported on Monday. Though the pace of new fatalities accelerated sightly day over day, the world still reported fewer than 4k new deaths – 3,912, to be exact – bringing the tally to 1,002,296.

The number of new cases reported yesterday also rebounded, with 275,892 new cases according to Johns Hopkins final reading; as of 0630ET on Tuesday, the global tally had climbed to 33,384,153.

As the AP pointed out, while the official death toll is 1 million, the real total could be as much as 2x higher, according to a projection that has been widely cited in the Western press. Here’s the AP:

Even then, the toll is almost certainly a vast undercount because of inadequate or inconsistent testing and reporting. And more people are dying daily, shrouding families and communities in grief in almost every corner of the world.

In terms of the big news from overnight and the morning session, Bloomberg reported just moments ago that Tianjin-based CanSino Biologics is launching Phase 2 trials in eastern China. The trials will also test the company’s COVID-19 vaccine in two doses, according to the trial protocol posted on database. The trial will involve 481 volunteers, including minors aged between 6-18 and people aged 56 or older, as well as those who have previously received the company’s Ebola vaccine, which was developed using a similar technology. The trial is double-blind, randomized and placebo-controlled.

Here’s the rest of the news overnight.

After imposing new social distancing measures, Spain is set to extend its temporary leave schemes until the end of January, as the pandemic continues to hammer its economy.

The cabinet will meet on Tuesday to approve an extension of the emergency schemes, known as ERTEs, until Jan. 31. The benefits for laid off or under-employed workers were expected to expire on Wednesday.

After President Trump again announced plans to supply 150 million rapid COVID-19 tests to the states, Novacyt, the Anglo-French biotech company has agreed to supply testing equipment and rapid coronavirus tests to the UK government. The company will supply 300 PCR testing machines and test kits for £150 million for the first 14 weeks, potentially extending supply of the common antigen test by another 10 weeks for £100 million (Source: FT).

Maharashtra, the Indian state hardest hit by coronavirus and home to India’s financial capital, Mumbai, will reopen restaurants and bars beginning next month as PM Modi seeks to revive the Indian economy. The state has 1.3 million confirmed COVID-19 infections and 35,000 deaths. It also has more cases than Russia, the world’s fourth-most-affected country (Source: FT).

City council leaders from Liverpool, Leeds and Manchester upped the pressure on the government to reduce new ‘local lockdown’ measures as they crush the local economy. In a letter to health secretary Matt Hancock and business secretary Alok Sharma, the leaders complained that hotel occupancy is at around 30% normal levels and footfall has fallen by more than 2/3rds due to the local lockdown measures (Source: FT)

The Australian state of Victoria reported 10 new coronavirus infections on Tuesday morning, as authorities eased lockdown measures in Melbourne after suppressing an outbreak.

With the US death toll slowly moving higher, Texas reported its smallest daily increase in deaths in about three months on Monday, as just 11 deaths were counted as COVID-19 deaths. California also reported its smallest increase in deaths in three weeks on Monday, and its lowest daily tally in a week. (Source: JHU).

via ZeroHedge News https://ift.tt/3n0ziqO Tyler Durden

Our news roundup is dominated by the seemingly endless ways that the US and China can find to quarrel over tech policy. The Commerce Department’s plan to use an executive order to cut TikTok and WeChat out of the US market has now been enjoined. But the $50 Nick Weaver bet me that TikTok could tie its forced sale up until January is still at risk, because the administration has a double-barreled threat to use against that company – not just the executive order but also CFIUS – and the injunction so far only applies to the first.

I predict that President Xi is likely to veto any deal that appeals to President Trump, just to show the power of his regime to interfere with US plans. That could spell the end of TikTok, at least in the US. Meanwhile, Dave Aitel points out, a similar but even more costly fate could await much of the electronic gaming industry, where WeChat parent TenCent is a dominant player.

And just to show that the US is willing to do to US tech companies what it’s doing to Chinese tech companies, leaks point to the imminent filing of at least one and perhaps two antitrust lawsuits against Google. Maury Shenk leads us through the law and policy options.

The panelists dismiss as PR hype the claim that it was the threat of “material support” liability that caused Zoom to drop support for a PFLP hijacker’s speech to American university students. Instead, it looks like garden variety content moderation aimed this time at a favorite of the far left.

Dave explains the good and the bad of the CISA order requiring agencies to quickly patch the critical Netlogon bug.

Maury and I debate whether Vladimir Putin is being serious or mocking when he proposes an election hacking ceasefire and a “reset” in the cyber relationship. We conclude that there’s some serious mocking in the proposal.

Dave and I also marvel at how Elon Musk, for all his iconoclasm, sure has managed to cozy up to both President Xi and President Trump, make a lot of money in both countries, and take surprisingly little flak for doing so. The story that spurs this meditation is the news that Tesla is so dependent on Chinese chips for its autonomous driving engine that it’s suing the US to end the tariffs on its supply chain.

In quick hits and updates, we note a potentially big story: The Trump administration has slapped new restrictions on exports to Semiconductor Manufacturing International Corporation, China’s most advanced maker of computer chips.

The press that lovingly detailed the allegations in the Steele dossier about President Trump’s ties to Moscow hasn’t been quite so enthusiastic about covering the dossier’s astounding fall from grace. The coup de grace came last week when it was revealed that the main source for the juiciest bits was flagged by the FBI ten years ago as a likely Russian foreign agent; he escaped a FISA order only because he left the country for a while in 2010.

The FISA court has issued an opinion on what constitutes a “facility” that can be tapped with a FISA order. It rejected the advice of Cyberlaw Podcast regular David Kris in an opinion that includes all the court’s legal reasoning but remains impenetrable because the facts are all classified. Maury and I come up with a plausible explanation of what was at stake.

The Trump administration has proposed section 230 reform legislation similar to the white paper we covered a couple of months ago. The proposal so completely occupies the reasonable middle of the content moderation debate that a Biden administration may not be able to come up with its own reforms without sounding fatally similar to President Trump.

And in yet more China news, Maury and Dave explore the meaning of Nvidia’s bid for ARM, and Maury expresses no surprise at all that WeWork is selling off a big chunk of its Chinese operations

Oh, and we have new theme music, courtesy of Ken Weissman of Weissman Sound Design. Hope you like it!

Download the 330th Episode (mp3)

You can subscribe to The Cyberlaw Podcast using iTunes, Google Play, Spotify, Pocket Casts, or our RSS feed. As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect the opinions of their institutions, clients, friends, families, or pets.

from Latest – Reason.com https://ift.tt/3n2WvIM

via IFTTT

If you were alive and on social media in early June, you were almost certainly swamped by scores of media and cultural organizations putting out statements, Instagram posts, and self-critical columns expressing solidarity in the fight against systemic prejudice.

“We recognize that there is much work to be done, and we are committed to engaging in this work to eradicate institutional racism,” announced the Poetry Foundation, publisher of Poetry magazine. “I have tried to diversify our newsroom over the past 7 years, but I HAVE NOT DONE ENOUGH,” confessed the editor in chief of Variety. The women’s lifestyle publication Refinery29, like many websites, changed its homepage color to black instead of its usual peppy pink.

Within days, the heads of all those institutions were out of a job.

In summer 2020, the American media experienced something like a collective nervous breakdown. Against the backdrop of the coronavirus and associated lockdowns, with whole sections of the industry teetering on the edge of collapse, newsrooms from coast to coast engaged in a series of internal revolts about race, defenestrating editors over everything from headlines to Halloween costumes.

Current and former employees launched self-styled “name-and-shame” campaigns on Twitter to out editors and organizations whose commitment to diversity and equity were deemed insufficient. A Broadway actress created a public spreadsheet called “Theaters Not Speaking Out”; participants were encouraged to “add names to this document who have not made a statement against injustices toward black people.” Heads rolled at The Philadelphia Inquirer, the Los Angeles Times, Bon Appétit, the National Book Critics Circle, Chicago’s Second City Theater, The New York Times, and scores of other cultural institutions and corporations.

“Institutional leaders, in a spirit of panicked damage control, are delivering hasty and disproportionate punishments instead of considered reforms,” noted a group of 153 writers and academics, including such left-leaning luminaries as Salman Rushdie and Noam Chomsky, in a joint letter published online by Harper’s magazine on July 7. “Editors are fired for running controversial pieces; books are withdrawn for alleged inauthenticity; journalists are barred from writing on certain topics; professors are investigated for quoting works of literature in class; a researcher is fired for circulating a peer-reviewed academic study; and the heads of organizations are ousted for what are sometimes just clumsy mistakes.”

The Harper’s letter, like the actions that precipitated it, revealed a split within the broader intelligentsia. On one side are people defending the values of liberalism—free speech, due process, individualism. On the other are those chipping away broadly at institutions they judge to be abetting a corrupted, discriminatory power structure. One side laments each broken egg; the other is busy making omelets.

That divide was on stark display within minutes of the letter’s publication, as an entire generation of left-leaning commentators and journalists rose up nearly as one to douse the whole effort with bile. “The signatories, many of them white, wealthy, and endowed with massive platforms, argue that they are afraid of being silenced,” snarled a counter-letter signed by 164 writers three days later. “The irony of the piece is that nowhere in it do the signatories mention how marginalized voices have been silenced for generations in journalism, academia, and publishing.”

There is an asymmetry of approach between anti-liberals—of both left and right—and their increasingly alarmed critics. While the latter camp tends to treat controversies and individuals on a case-by-case basis, the former is forever trying to herd people into binary categories. In the words of bestselling author Ibram X. Kendi, “You’re either racist or antiracist; there’s no such thing as ‘not racist.'”

The Manicheans have special contempt for those who refuse such designations, especially when they’re otherwise on the same side of the political spectrum. That the Harper’s authors came mostly from the left and prefaced their brief complaint with a swipe at President Donald Trump bought them no sympathy from their progressive tormentors. So signatory Yascha Mounk founds an earnest new publication called Persuasion, even while being dismissed by such leftists as The Daily Beast‘s Laura Bradley as belonging to a “coven of fools.”

This witch-burning moment will hopefully recede, but the fuel in this accursed year will continue piling up.

from Latest – Reason.com https://ift.tt/30jzfwr

via IFTTT

If you were alive and on social media in early June, you were almost certainly swamped by scores of media and cultural organizations putting out statements, Instagram posts, and self-critical columns expressing solidarity in the fight against systemic prejudice.

“We recognize that there is much work to be done, and we are committed to engaging in this work to eradicate institutional racism,” announced the Poetry Foundation, publisher of Poetry magazine. “I have tried to diversify our newsroom over the past 7 years, but I HAVE NOT DONE ENOUGH,” confessed the editor in chief of Variety. The women’s lifestyle publication Refinery29, like many websites, changed its homepage color to black instead of its usual peppy pink.

Within days, the heads of all those institutions were out of a job.

In summer 2020, the American media experienced something like a collective nervous breakdown. Against the backdrop of the coronavirus and associated lockdowns, with whole sections of the industry teetering on the edge of collapse, newsrooms from coast to coast engaged in a series of internal revolts about race, defenestrating editors over everything from headlines to Halloween costumes.

Current and former employees launched self-styled “name-and-shame” campaigns on Twitter to out editors and organizations whose commitment to diversity and equity were deemed insufficient. A Broadway actress created a public spreadsheet called “Theaters Not Speaking Out”; participants were encouraged to “add names to this document who have not made a statement against injustices toward black people.” Heads rolled at The Philadelphia Inquirer, the Los Angeles Times, Bon Appétit, the National Book Critics Circle, Chicago’s Second City Theater, The New York Times, and scores of other cultural institutions and corporations.

“Institutional leaders, in a spirit of panicked damage control, are delivering hasty and disproportionate punishments instead of considered reforms,” noted a group of 153 writers and academics, including such left-leaning luminaries as Salman Rushdie and Noam Chomsky, in a joint letter published online by Harper’s magazine on July 7. “Editors are fired for running controversial pieces; books are withdrawn for alleged inauthenticity; journalists are barred from writing on certain topics; professors are investigated for quoting works of literature in class; a researcher is fired for circulating a peer-reviewed academic study; and the heads of organizations are ousted for what are sometimes just clumsy mistakes.”

The Harper’s letter, like the actions that precipitated it, revealed a split within the broader intelligentsia. On one side are people defending the values of liberalism—free speech, due process, individualism. On the other are those chipping away broadly at institutions they judge to be abetting a corrupted, discriminatory power structure. One side laments each broken egg; the other is busy making omelets.

That divide was on stark display within minutes of the letter’s publication, as an entire generation of left-leaning commentators and journalists rose up nearly as one to douse the whole effort with bile. “The signatories, many of them white, wealthy, and endowed with massive platforms, argue that they are afraid of being silenced,” snarled a counter-letter signed by 164 writers three days later. “The irony of the piece is that nowhere in it do the signatories mention how marginalized voices have been silenced for generations in journalism, academia, and publishing.”

There is an asymmetry of approach between anti-liberals—of both left and right—and their increasingly alarmed critics. While the latter camp tends to treat controversies and individuals on a case-by-case basis, the former is forever trying to herd people into binary categories. In the words of bestselling author Ibram X. Kendi, “You’re either racist or antiracist; there’s no such thing as ‘not racist.'”

The Manicheans have special contempt for those who refuse such designations, especially when they’re otherwise on the same side of the political spectrum. That the Harper’s authors came mostly from the left and prefaced their brief complaint with a swipe at President Donald Trump bought them no sympathy from their progressive tormentors. So signatory Yascha Mounk founds an earnest new publication called Persuasion, even while being dismissed by such leftists as The Daily Beast‘s Laura Bradley as belonging to a “coven of fools.”

This witch-burning moment will hopefully recede, but the fuel in this accursed year will continue piling up.

from Latest – Reason.com https://ift.tt/30jzfwr

via IFTTT

“We Are Not Amused!” Queen Of England Hurt By Commercial Real-Estate Collapse

Tyler Durden

Tue, 09/29/2020 – 05:00

Authored by Nick Corbishley via Wolf Street,

Crown Estates, which manages the Queen of England’s portfolio, recently wrote down the value of 17 shopping and leisure centers by 17%, cutting Her Majesty’s net worth by £552 million. As The Economist points out, this is “fairly small beer” set against the £13.4 billion valuation of the Queen’s property portfolio, which includes some of London’s toniest real estate.

But the Queen will not be left out of pocket, since her income — set at 25% of the profits generated by the Crown Estate — will be topped up with a taxpayer bailout. In fact, thanks to the Sovereign Grant Act of 2011, the overall amount given to the Queen each year in order to fund her official duties is never allowed to fall, regardless of what is happening in the broader economy.

“In the event of a reduction in the Crown Estate’s profits, the sovereign grant is set at the same level as the previous year,” a spokesperson told The Independent.

“The revenue from the Crown Estate helps pay for our vital public services – over the last 10 years it has returned a total of £2.8 billion to the Exchequer.”

Any profits made by the Crown Estate are passed to the Treasury which, in turn, hands 25% of the profits back to the Queen through the sovereign grant. This year, things will be a little different. To cover the fall in value of the Crown’s Estate, the estate has struck an agreement with the Treasury that allows it to begin making “staggered” revenue payments to the government, thus keeping a larger share of the profits to itself.

It’s a nice deal if you can get it. Most other UK commercial landlords can’t, though many larger property owners have certainly been lobbying the government for support, which for the moment is not forthcoming.

Meanwhile, conditions in both the retail and office markets continue to deteriorate. The U.K.’s ongoing retail crisis and work-from-home (WFH) revolution have between them wiped out roughly half of the market cap of large REITs such as Land Securities Group Plc, British Land Company, and Shaftesbury so far this year.

Last week, the government extended its ban on evictions of commercial property tenants from September 30 to December 31, which angered some landlords who have seen the yields on their investments slide as businesses struggle to pay rent. First passed on March 26, the moratorium on evictions was an essential lifeline for many retail businesses or offices whose incomes had dropped dramatically during the lockdown.

But it also shifted financial stress from tenants to property owners and their lenders. And the longer it drags on — it has now been extended twice in six months — the more the stress grows.

U.K. commercial property firms have so far collected just 68% of the rent they were due in June, according to data issued on Wednesday by Re-Leased, after having collected only 18.2% on the due date. Unsurprisingly, retail landlords have been hit the hardest, having so far received just 60% of rents due for the June quarter, compared to 75% and 76% respectively for the industrial and office sectors.

Despite the recent frenetic efforts of the British government to undo the WFH revolution it set in motion, the UK has significantly lagged behind mainland Europe in getting workers back behind their desks. This week, the government reversed policy once again, as covid cases began surging, urging all “office workers who can work effectively from home” to do so “over the winter,” .

This is going to have a dire impact not only on the owners of office buildings but also on the shops, restaurants, bars, cafes and other struggling city-center retail and leisure businesses that depend on the custom of office workers. Many leisure and hospitality businesses are already reeling from the government’s imposition this week of a 10 o’clock curfew for bars and restaurants. The owners of these properties are also feeling the pinch.

Shaftesbury, a real estate investment trust (REIT) that mainly rents to independent retailers in London’s West End, reported on Friday that for the six months to September so far, it had collected just 41% of rent due. Ten percent of rents are expected to be subject to deferred collection arrangements; 23% are being waived and 26% remain outstanding. By the end of August, its vacancy rate had risen to 9.7% of estimated rental value, compared to 4.8% at the end of March.

As retail vacancy rates have risen, the balance of power has gradually shifted, from landlord to tenant. Even if evictions were allowed, in this crisis it will be very tough for landlords to find a replacement for an evicted tenant — which makes landlords somewhat more flexible in dealing with their tenants.

And many tenants aren’t paying their rents, either because they can’t or are choosing not to, in the hope of renegotiating the terms of their lease contract. Shaftesbury is letting tenants defer quarterly rent for a third consecutive quarter, while British Land, part-owner of the sprawling Broadgate office and retail complex in the City of London, is considering extending support to its smaller hospitality and shop tenants for the next quarter, reports Bloomberg.

It’s the main reason why fashion retailer New Look was able to secure such attractive terms from its landlords — including Landsec and British Land — in its latest voluntary insolvency procedure. By placing its store leases at the heart of its negotiations, the firm was able to ensure that 402 of its 470 stores would move to a turnover-linked model, whereby rent will be charged at between 2% and 12% of revenues. For the remaining 68 stores the firm will not have to pay rent for the next three years.

The property owners may not have liked the terms, but given New Look’s size and the huge holes its demise would have left in an already decimated brick-and-mortar retail landscape, they had little choice but to grudgingly accept them. By setting a precedent for turnover-based rents, it’s only a matter of time before other large stores begin asking for the same treatment.

* * *

via ZeroHedge News https://ift.tt/3ieomlC Tyler Durden

Pineville, Louisiana, police officer John Goulart Jr. claimed he’d been shot in the leg in an ambush. But officials now say he shot himself and made up the story about the ambush. Goulart has been charged with criminal mischief and malfeasance in office. “Everything shows it was an accidental discharge,” said Deputy Chief Darrell Basco. Basco said Goulart fired two rounds from his service weapon, one of which struck one of the doors of his patrol car.

from Latest – Reason.com https://ift.tt/33cUHVH

via IFTTT

Pineville, Louisiana, police officer John Goulart Jr. claimed he’d been shot in the leg in an ambush. But officials now say he shot himself and made up the story about the ambush. Goulart has been charged with criminal mischief and malfeasance in office. “Everything shows it was an accidental discharge,” said Deputy Chief Darrell Basco. Basco said Goulart fired two rounds from his service weapon, one of which struck one of the doors of his patrol car.

from Latest – Reason.com https://ift.tt/33cUHVH

via IFTTT

How A Bunch Of French Math Nerds Built SocGen’s Now-Crumbling ‘Structured Products’ Empire

Tyler Durden

Tue, 09/29/2020 – 04:15

It has been years since European banks’ dominated traditional investment-banking business lines like trading and M&A. But things weren’t always this way. Before the financial crisis, and before regulators around the world started scrutinizing banks’ derivatives businesses to try and curb risk.

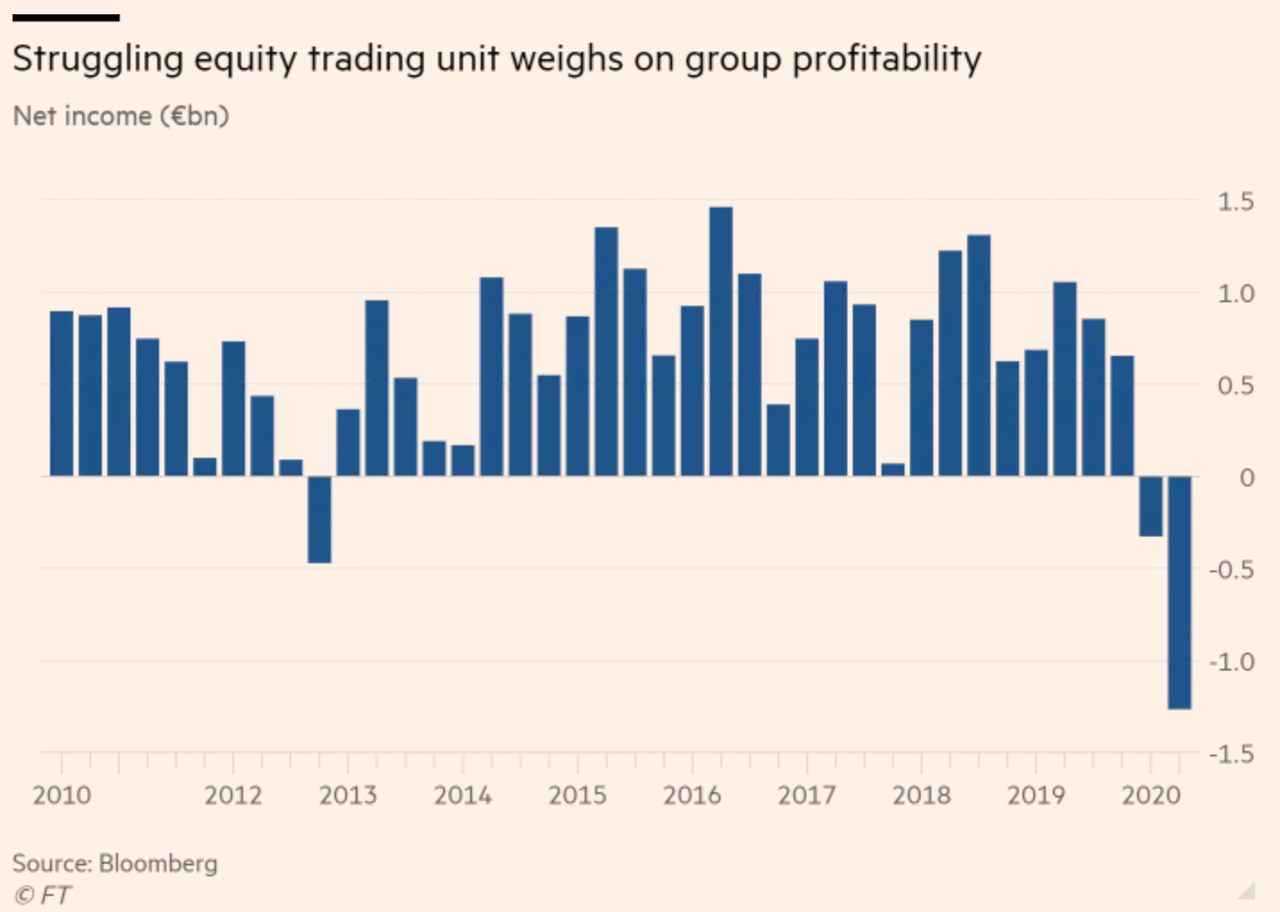

But while Deutsche Bank has become the poster-child for post-GFC decline – as its ambitions to become a global rival to JP Morgan crumbled to dust – Societe Generale, the French banking giant that reaped massive profits during the late 1990s and 2000s via its pioneering ‘structured products’ business, is also presiding over the twilight of a business line that was once the bank’s profit center, but has been blamed for massive losses during the coronavirus downturn this spring.

Oudea

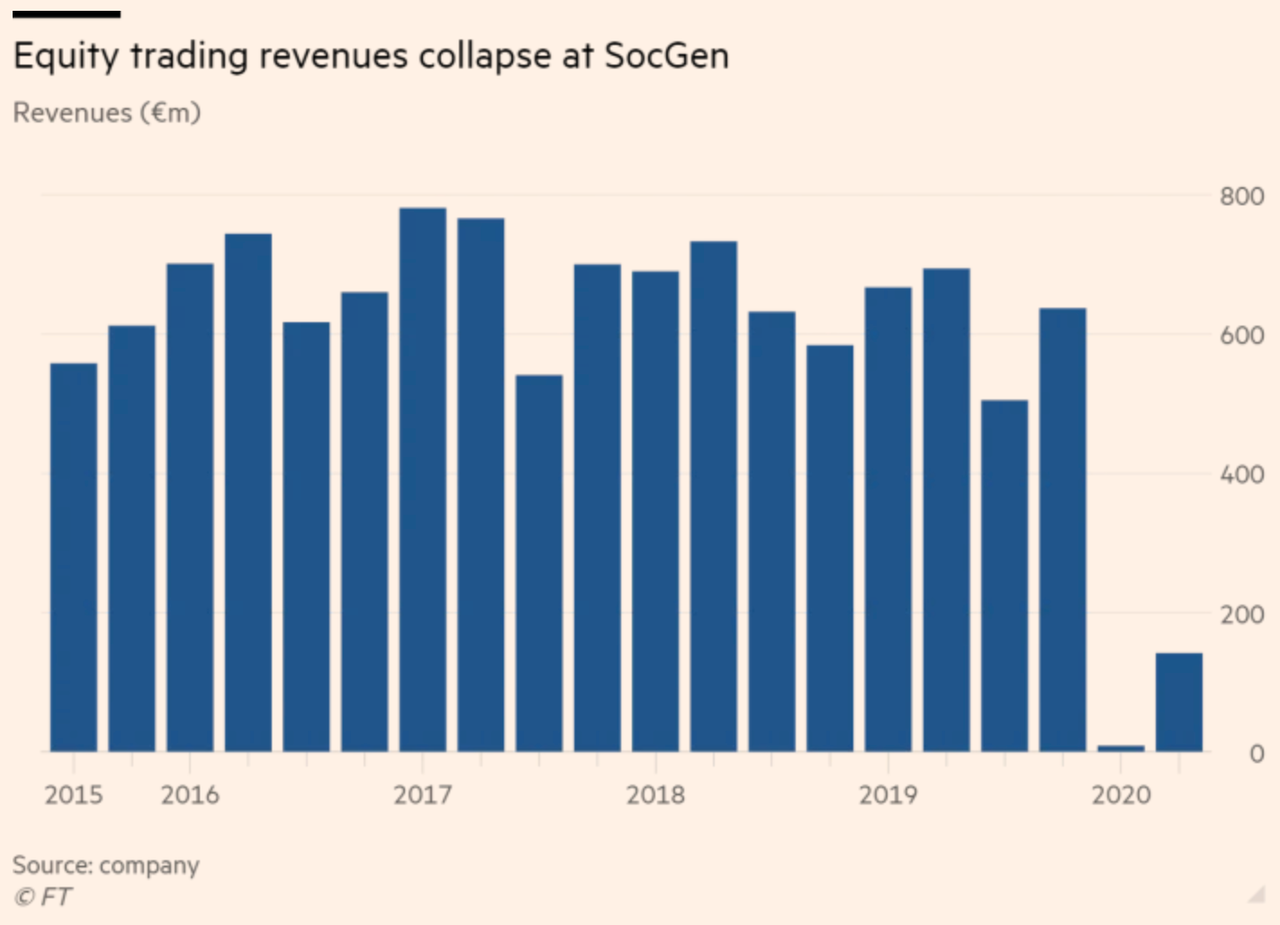

As the FT reminds us, the French bank fell to a shocking loss of €326 millions ($380 million) in the first quarter after revenue in its equity trading unit (long hailed as a key strength) collapsed almost 99% to just €9 million ($10.5 million) after the bank saw “the worst environment you can imagine” for its structured products business, CEO Frédéric Oudéa explained.

Another major loss was reported in August, after Q2 earnings were reported.

A loss that was attributed almost entirely to the group’s

With shareholders revolting, Oudéa promised to cut back on the bank’s structured products business, foregoing €250 million in revenue while targeting “cost savings” of €450 million ($523 million). The cuts are the biggest threat to a business line that set SocGen apart from its European peers, and helped establish the bank as a powerhouse in equity derivatives thanks to its ‘structured products’ business. These products, purchased by retail and institutional investors, charge relatively high fees, but purport to lock in moderate profits while smoothing out volatility.

30 years ago, however, the business was just the twinkle in the eye of a legendary French banker named Antoine Paille. 30 years ago, Paille was a 31-year-old software engineer with a big dream. He and a small team of engineers from a venerable French academy were bequeathed a basement office in downtown Paris, where they birthed the bank’s structured products business. Here’s the FT with more.

Thirty years ago, a group of maths and engineering graduates from Paris’s elite grandes écoles changed the direction of one of France’s oldest and most important banks.

Under Antoine Paille, a 31-year-old software engineer, the small team was given a basement office a few streets from the Palais Garnier opera house in Paris with instructions to build a new business for Société Générale, the lender founded in the 19th century.

Mr Paille believed that SocGen’s dive into options and equity derivatives, which would eventually be packaged up for professional and retail investors into so-called structured products, could provide the bank with an advantage over its larger global competitors. He proved to be right.

French banks, including SocGen, Natixis and BNP Paribas, eventually all became global leaders in these types of products, which encapsulated derivatives which promised to minimize volatility while maximizing the upside for clients. But in a world of low interest rates, and increasingly strenuous global competition, bankers were forced to make the products increasingly complex – and increasingly risky – just to keep up with the competition. “Correlation” offerings and “autocalls” soon dominated the landscape.

But the original products have changed, becoming increasingly complicated structures that tried to maintain returns in a world of low interest rates and copycat products. “Normally when we created a product, we’d have it to ourselves for about a year and a half, then others would start to copy it,” said one former member of the structured products team. Simple “plain vanilla” guaranteed return products morphed into correlation offerings based on baskets of stocks, and on to autocalls, which pay out a coupon similar to a bond as long as losses or gains are within a certain threshold.

One banker reminisced to the FT about SocGen’s first slam-dunk structured product, called “Everest”, which the banker described as “beautiful”.

“Everest was beautiful,” another banker reminisced, remembering a correlation product that was sold to retail investors and named by Christophe Mianné, one of the leading lights in equity derivatives in the 1980s, after he saw a film about the mountain projected near SocGen’s Paris headquarters in La Défense.

Here’s how it worked…

Everest had a duration of 10 years and guaranteed that clients’ capital would be returned. Additional returns were based on the performance of 10 or more stocks, with redemption based on the performance of the weakest member of that chosen basket.

…and – more importantly – here is the pitch:

“We told investors that if you invest 100 then after ten years we would give you 200, minus the performance of the worst stock you chose,” said someone who used to sell the products. If the worst performing stock went to zero, then clients received only their capital back and if all the stocks performed well they got the upside. The risk that all the stocks would move in the same direction at the same time was the bank’s to wear.

Among the original group of bankers brought in to package and sell these products was Jean Pierre Mustier, who eventually rose to lead SocGen’s investment bank, before being unceremoniously fired after the financial crisis, when regulators came down hard on SocGen’s structured products business (he’s now the CEO of UniCredit). Mustier’s rise was almost as meteoric as the structured products business.

A steady stream of talented maths graduates churned out by French universities, along with a plan to build centralised teams and sell the products at scale, allowed SocGen to steal a march on rivals. Insiders say a “start-up culture” allowed them to beat US banks which were selling bespoke products to institutional clients. One ex-SocGen banker said the US banks were not as interested in structured products because they were making enough money elsewhere. By the early 2000s, SocGen’s equity derivatives unit employed close to 2,000 people and had grown into the bank’s profits engine, accounting for 95 per cent of its investment bank earnings.

Despite the business’s tremendous success, the regulatory backlash was swift, and the bank was forced to retreat from riskier practices that were also – as it turns out – extremely lucrative.

Though the bank continued to invest in its structured products business, Mustier was eventually forced out of the investment bank as Oudéa ascended to the CEO role. This precipitated a shift away from investment-banking and market making as the bank’s central focus, and led to a steep decline in the structured products business.

SocGen is not giving up on structured products, despite the hit from Covid-19 forcing it to pull back. Instead it is trying to walk a tightrope between reducing risk and remaining true to its core identity. It will do that, said Jean-François Grégoire, head of global markets at the bank, by trying to push new ranges of products that reduce the potentially large losses the bank faces in market turmoil, leaning once again on its ability to engineer. “The innovation that we’ve been pushing [this time] is completely different. It’s innovation that goes towards creating products that are easier to manage for us and that are still very profitable for the customers,” Mr Grégoire said.

Of course, any product that can’t withstand intense market “ructions” – the FT’s favorite word to describe the chaotic limit-up/limit-down swings seen in March – is bound to run into problems in a market universe where payment for order flow, algorithmic trading and uneven liquidity exacerbates volatility, creating new challenges for risk managers across Wall Street.

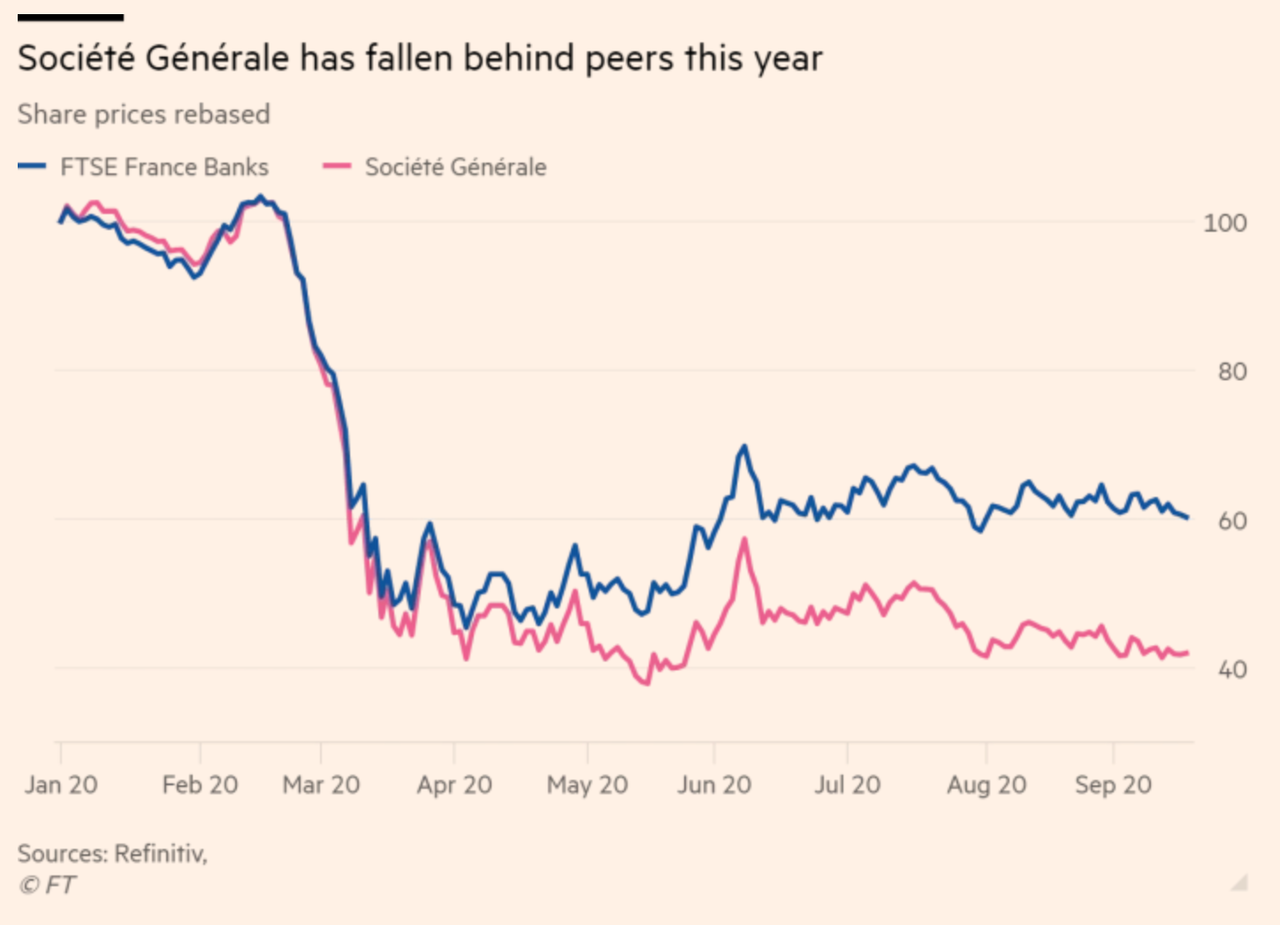

So far, the market reaction has placed SocGen behind the curve for 2020, as its shares lag French banks.

via ZeroHedge News https://ift.tt/2GbPp45 Tyler Durden