Democrats Release New $2.2 Trillion Stimulus Proposal With $417BN In State And Local Aid Tyler Durden

Mon, 09/28/2020 – 19:00

Late on Monday, in an apparent attempt to break the covid fiscal stimulus impasse in Congress but without actually providing a tangible compromise, House Democrats released a fresh $2.2 trillion coronavirus relief bill proposal, which Nancy Pelosi said was a “compromise measure that reduces the costs of the economic aid” which will allow the Democrats to go to the public and say “we tried, the Republicans killed it.”

The plan follows through on discussions last week to prompt a last-ditch attempt at negotiations with the White House to break an impasse on Covid-19 relief that’s lasted since early August.

In a letter to Democratic lawmakers released by Pelosi’s office, she said the legislation “includes new funding needed to avert catastrophe for schools, small businesses, restaurants, performance spaces, airline workers and others.”

“Democrats are making good on our promise to compromise with this updated bill,” she said. “We have been able to make critical additions and reduce the cost of the bill by shortening the time covered for now.”

The problem is that since the total bill remains at a level that Senate Republicans have previously rejected. Furthermore, the proposal also includes $238 billion for State Fiscal Relief and $179 billion in Local relief, both of which Trump has previously said remains a non-starter.

State Fiscal Relief – $238 billion in funding to assist state governments with the fiscal impacts from the public health emergency caused by the coronavirus, including $755 million in CARES Act Coronavirus Relief Fund repayment for the District of Columbia.

Local Fiscal Relief – $179 billion in funding to assist local governments with the fiscal impacts from the public health emergency caused by the coronavirus.

Shortly after the bill was published, Pelosi and Treasury Secretary Mnuchin spoke at 6:30 p.m. via phone according to press reports. The two agreed to speak again tomorrow morning.

While the latest Democrat proposal has a virtually nil chance of passing, readers can read the 87 proposal in its entirety below (pdf link):

via ZeroHedge News https://ift.tt/3i9oB1h Tyler Durden

California EV Mandate Could “Lead To Disaster” For State’s Already Fragile Electric Grid Tyler Durden

Mon, 09/28/2020 – 18:40

Now that genius California lawmakers have mandated that all cars in the state must be electric by 2035, it seems like a good time to ask what, exactly, this is going to do to the state’s already fragile power grid.

In what will likely come as a surprise to lawmakers who we can almost guarantee didn’t think about this in advance, it turns out that electrifying all of the state’s vehicles could be “an immense burden” on the state’s grid, according to Bloomberg.

In fact, this past week’s executive order could drive up power demands in the state by as much as 9.5% over the next 10 years and 25% by 2035. This could be a “nightmare” scenario for a state where power is often so tight that rolling blackouts are ordered to prevent the system from collapsing during heat waves.

Additionally, if everyone were to plug in their vehicles at the same time, at night, the problem could be concentrated and even worse.

Erica Bowman, director of resource and environmental planning and strategy at utility Southern California Edison said: “It could go either way. It really depends on planning.”

What planning means is the idea that people would have to stagger when and how they plug in their vehicles for charging, taking into account when the state’s solar energy kicks in and when wind power peaks. Ah, yes, what a wonderful quality of life California offers, where you’ll soon have to ask permission to plug in your car just to get from point A to point B.

Everyone plugging their car in at 6PM after work could “lead to disaster”, according to the report. It’s the same time everyone also decides to turn on their air conditioning, stoves and televisions. At the same time, solar power plunges around sunset, forcing gas plants to pick up the slack. If gas plants are down or there’s no imports available, you wind up with a rolling blackout scenario, like the state had last month.

Jules Kortenhorst, chief executive officer of the Rocky Mountain Institute, said cars will have to “talk to the grid” to figure out when the best time to charge is: “The car will talk to the grid. ‘It’s 6 pm. Wait 15 minutes, because I’m crunched a bit.’ You won’t spend a second thinking about it.”

Californians bought about 1.9 million cars and light duty trucks last year. The state will simply need more power if it mandates that they are all EVs going forward. It will also need to deploy charging stations much faster than it has in the past.

Pedro Pizzaro of Edison International concluded: “It’s not doable a year from now, but it is doable a decade from now. And that gives society time to deploy infrastructure for chargers and get consumers comfortable.”

And California citizens, already leaving the state in droves due to rising taxes, will be on the hook to pay for it all. But hey, back to saving the planet at all costs!

via ZeroHedge News https://ift.tt/36dCyZM Tyler Durden

From Friday’s decision by Judge Lynn Adelman (E.D. Wis.) in Anderson v. Hansen:

[Heidi] Anderson is the mother of two children who attend schools within the Elmbrook School District. On August 11, 2020, the Elmbrook Board of Education held a public meeting to address the District’s procedures for dealing with the COVID-19 pandemic. One of the measures under consideration was a requirement that all children attending school in person wear masks to minimize the transmission of the virus through respiratory droplets. Anderson attended the meeting in person and signed up to speak about the proposal.

Anderson opposes mask mandates in general, and she was against the District’s proposal to require children to wear masks at school. The Board allowed her to express her views during the time allotted for citizen comments about the proposal. She was given two minutes to speak. When she was called to the podium, she delivered remarks that lasted over eight minutes.

During her remarks, Anderson gave a variety of reasons for opposing the mask proposal. Some reasons related to her faith. Anderson is Christian, and she believes that wearing masks is inconsistent with the Christian faith. During her remarks, she expressed her view that “[s]ix-foot distance and masks are a Pagan ritual of Satanic worshipers.” She stated that because her family is Christian and does not practice Satanic worship, her children are not made to “stand six feet apart from each other with facial coverings.”

Towards the end of her remarks, Anderson turned her attention to Dr. [Mushir] Hassan, a medical doctor and school board member whom the Board had designated as its medical liaison:

“[Mrs. Anderson:] Dr. Mushar, and I hope I’m saying this correctly, you are not the right choice to be the Board liaison. You do not practice in infectious disease, you have political leaning contrary to the will of this district. You online state that you’re a big Obama fan and you comply mentally with his control philosophy, and you have publicly slammed our president Trump online. I’m finishing. As a leader in the Islamic community—

“[Interjection by School Board President:] Heidi, we have to avoid defamatory comments.

“[Mrs. Anderson:] This is not defamatory. I’m stating facts. [To Dr. Hassan:] You are a leader in the Islamic community are you not, and a leader on the Board—

“[Board President:] Heidi.

“[Mrs. Anderson:] O.K. Well listen, my kids are Christians. They are not subject to wearing face coverings. Christian children should not be forced to wear face coverings any more than children who are Islamic or Muslim should be forced to, as you’ve put it, ‘be subject to the American style sexualization of children,’ and have to wear less clothing than you’re comfortable with your children wearing….

“[To the Board generally:] You are employed by the people of Brookfield and Elm Grove, you are elected to serve us. And the Elmbrook School administration works at our pleasure. You do not work for Madison, or any other unelected entity—our government is of the people, by the people, and for the people. This is one country, one nation under God, and we look to God for these answers when we can’t figure it out and I would suggest that you all do that. There is a wonderful prayer that he taught us to pray, it’s called the Lord’s prayer, and you can find it in your Bible. Thank you for your time.”

The board meeting was broadcast over the Internet. Anderson later learned that her comments had sparked controversy online. Some observers described her remarks as “ignorant,” “Islamophobic,” and “insensitive.” In response to these comments, the Elmbrook School District contacted community members and told them that the District condemned Anderson’s remarks. The District also “censored” a portion of Anderson’s comments, which I assume means that the District edited the archived video recording of her comments to remove the comments she directed towards Dr. Hassan. Further, on August 12, 2020, the day after the meeting, the School Board published a statement on its website in which it apologized to Dr. Hassan and expressed its view that Anderson’s statement was unacceptable….

[After some more back-and-forth, Superintendent Dr. Mark Hansen] informed Anderson that she would not be allowed on any District property without the prior approval of either the superintendent or the principal of her children’s school…. Anderson may not attend a Board of Education meeting or participate in events at her children’s school, including her daughter’s dance recitals, without first obtaining permission from the superintendent or the school principal. Moreover, because Anderson’s polling place is located inside an elementary school in the District, she may not vote in person without first receiving permission from the superintendent or a school principal….

Anderson sued, and Judge Adelman ruled that she was entitled to a preliminary injunction, because she had “a very high likelihood of success on the merits of her First Amendment claim”:

At the outset, I note that this case does not require me to determine whether Anderson’s comments towards Dr. Hassan displayed religious intolerance or were inappropriate, hateful, or offensive. For even if they were, the First Amendment would protect the plaintiff’s right to make them. See Matal v. Tam (2017) (“Speech that demeans on the basis of race, ethnicity, gender, religion, age, disability, or any other similar ground is hateful; but the proudest boast of our free speech jurisprudence is that we protect the freedom to express ‘the thought that we hate.’ “); id. (Kennedy, J., concurring) (recognizing that, with few exceptions, “it is a fundamental principle of the First Amendment that the government may not punish or suppress speech based on disapproval of the ideas or perspectives the speech conveys”); Rosenberger v. Rector (1995) (“It is axiomatic that the government may not regulate speech based on its substantive content or the message it conveys.”). Thus, basic First Amendment principles prevent the District from subjecting the plaintiff to adverse action for no other reason than it considered her speech at the board meeting intolerant, offensive, or hateful….

The government may place reasonable time, place, and manner restrictions on speech and regulate its own meetings. Thus, the District could have enforced its two-minute time limit for citizen comments and cut the plaintiff off once she exceeded the limit. Moreover, if the plaintiff’s comments to Dr. Hassan amounted to a personal attack rather than an attempt to express a viewpoint on the mask proposal, the board members could have told the plaintiff to keep her remarks focused on the issues or taken other action to prevent her from continuing to speak on topics that were not germane to the board meeting.

Here, however, the District’s policy cannot be viewed as a reasonable time, place, and manner restriction or another permissible regulation of speech. The policy is not reasonably tailored to prevent the plaintiff from exceeding time limits, veering off topic, or being belligerent at future board meetings. Instead, the policy flatly bans the plaintiff from entering school property for any purpose without permission. This ban has no rational connection to enforcing restrictions on citizen comments at board meetings and thus can only be viewed as a way of punishing the plaintiff for the comments she made during the prior board meeting.

The defendants contend that their policy is designed to ensure that religious harassment is not tolerated on school property…. Perhaps the District is arguing that the policy is a prophylactic measure designed to prevent Anderson from entering onto school property and harassing others based on their religion. But this justification for the policy would be preposterous. It is not rational to think that because Anderson made religiously intolerant statements during her citizen comments at a public board meeting that she will roam the halls of the Elmbrook schools and harass those she encounters on the basis of their religion.

Moreover, in the unlikely event Anderson does engage in such behavior, the District could intervene at that time. As the defendants note in their brief, no person has an unlimited right to be present on school property, and the District has adopted a general rule that allows building administrators to eject disruptive persons from school grounds, Thus, if Anderson causes a disruption on school property, the District could have her removed even if the policy at issue in this case were not in force. This shows that the policy serves no rational purpose other than to punish Anderson for having expressed views with which the District disagrees….

Anderson seems like rather a fool to me, but, no, she can’t be banned from school district property because she criticized a public official at a school board meeting, whether her criticism stemmed from hostility to Muslims or anything else.

from Latest – Reason.com https://ift.tt/3jaRdbS

via IFTTT

What I am wondering about: Why hasn’t US late night TV “comedy” circuit dug into Joe Biden when he provides them with so much material? Am I the only one who’s been puzzled about that?

It’s not specifically about Biden, he’s just a tool in a game, for late night comedy, it’s all about Donald Trump, and they ignore that beyond him, there’s a naked bloody battle between two US political parties. But why would comedians want to take sides in that battle? And is doing that a good idea for their careers? I could have opened with: ”Late Night Biden? There’s no such thing, Joe’s fast asleep by then”! But the only people who would say such a thing today are in the Trump camp, not in late night “comedy”.

When I was living in Montreal and Ottawa I was a big admirer of US late night TV. Carson was way before my time, but Letterman was still there. Never was a big Leno fan. And then came the next generation, Jon Stewart was great, so was Stephen Colbert in his right wing parody on Jon’s show. Only, what happened then? You now have your Stephen Colbert 2.0 (no parody, no fun), Trevor Noah, Seth Meyers et al, Jimmy Kimmel perhaps.

All of whom have been doing the Orange Man Bad theme for four years running, all the while thinking that is funny. But repetition is predictable, and doing the same “jokes” about the same topic day after day is not funny. Sure, for your echo chamber perhaps, but come on! Things are either funny or they are not. Once they’re only funny in your head, or kitchen, or whatever, they no longer are. It’s not a big stretch.

Late night talk show became late night comedy with Jon Stewart, but nobody continued the format after he left. His successors did the same thing the NYT, WaPo, MSNBC and CNN did: play only to half their potential audience. Simply because they knew it was great for ratings and clickbait. Half the audience doesn’t sound good, but wait till you see that who’s left pays a hundred times more attention, because they hate the subject of your “jokes” even more than you do.

Saturday Night Live announced recently that Jim Carrey will play Joe Biden on SNL, and all I could think of is the great Twitter comment that said: “Nobody can be funnier playing Joe Biden than Joe Biden.” Dead on. So why would Carrey try? To make Biden less funny? You’d almost think so.

Of course I see that following US late night TV is almost impossible if you no longer live in North America. But from what I have managed to see of Jon Stewart’s successors it’s all the same. It’s party politics disguised as fun. It’s echo chamber induced deafness. But yeah, that’s just me, I’m sure people who for whatever reason don’t like Trump, or never did, may have been laughing their hearts out every single night for 4 years. But that doesn’t define “humor”. Real humor is something everyone can share.

In very much the same vein, I used to really dig Bruce Springsteen. But when he started campaigning for Obama, and the whole The Rising thing happened in DC, I no longer did. Not because of Obama, but because a songwriter, much like a late night comedian, should always steer clear of partisanship. That is, in my never very humble opinion.

Bob Dylan never did. He gave his opinion, but never about individuals. Well, maybe in Jokerman, but that was never about campaigning. Obama went on to bomb 8 different countries, kill 100s of 1000s of people in those countries, and establish open air slave markets in Libya while he was at it. Anyone ever ask Springsteen how he feels about that?

And I was still thinking: let it go. Because the whole thing has become so polarized, you’re never going to reach out from one end of the spectrum to the other anyway. The trenches have been dug. But then I see things like this, from a site named Deadline (Hollywood history since 1996):

President Donald Trump hasn’t promised that there will be a peaceful transfer of power if he loses to Joe Biden for the 2020 presidential Election. While the president remains mum, late-night hosts Trevor Noah and Seth Meyers warn viewers about what Trump’s refusal to leave in peace may bring. “Trump refusing to say that he would leave office if he loses is a scary thought because who knows what could happen with that kind of threat,” Noah grieved during Thursday’s episode of The Daily Show.

The Comedy Central host said during his segment that the President’s potential move would be unlike any other. Saying that “the world’s oldest democracy is about to become the world’s newest dictatorship,” Noah said that such political refusal seems un-American. “I never thought I’d see the day where an American president would threaten not to accept an election defeat,” he said. “Let’s be honest, this is something you hear about in some random country where America steps in to enforce democracy. I feel like now it’s only fair that those countries should send peacekeepers to the U.S.,” he added.

If Trump truly refuses to vacate the presidency for Biden, “one of the world’s most famous landlords” will turn “into the world’s most famous squatter,” Noah kidded during the segment. He also quipped that Trump, in order to remain in the White House for as long as possible, might live in the basement as Biden sits atop – à la Bong Joon-Ho’s Parasite. Similarly, Meyers criticized Trump for his failure to confirm a peaceful transfer of power. “He’s threatening a coup d’etat even though I’m sure he has no idea what the phrase ‘coup d’etat’ means,” the Late Night host said. “He probably thinks it’s a lyric from Moulin Rouge!“

Like Noah, Meyers said Americans are seeing democracy transform into an “autocratic regime” in real time. He even quipped that if Trump stays in office, it won’t be long until he parks a military tank on Pennsylvania Avenue and dons green fatigues and a long beard.

But of course, and you read my mind on this, Trump is not the funniest topic anymore. Certainly not after 4 years depleting that topic night after night. That doesn’t mean there was never anything funny about him, it means 4 years is a long time to spend on one topic. Biden, however, is a whole different story. But I’ve never seen any of these late night comic geniuses, who all have dozens of people writing “jokes” for them, go for -or after- Biden.

Are they scared of doing that? Do they fear their viewers won’t like that angle? Are they fully in cahoots with the DNC and MSM? Or, more to the point, should they ever let things like that play into their decisions of what will be funny or not? Well, apparently they do. Because Biden has come up with more whoppers than we can even try to keep track of, and not a word- that I’ve seen- from late night US comedy. I truly wonder what Jon Stewart thinks about that, just like I wonder what Springsteen has to say about open air slave markets in Libya.

Here are a few Biden bloopers for your perusal that those very well-paid masters of comedy didn’t think were funny…

Be your own judge…

No, I did not go looking for them, on purpose. I really just happen-stanced upon them. I have no doubt there are tons more of these videos. They’re just not late night comedy material, apparently. Please tell me why that is. Please tell me why all these people who live off of those shows find nothing about this funny, while I, time and again, think it’s hilarious.

It’s not a party political issue, It’s just really funny. Or, alternatively, please tell me why it’s not. Or even just imagine if Trump had said the things Biden did in these tapes, and none of the late night hosts would have presented that as funny. I’m waiting.

At this point, I don’t think there’s any possible way you could convince me that Joe Biden is not a whole huge lot funnier than all the Late Night shows put together. But you can try!

And after you watched all that, but only after you did, please tell me how you will feel if on January 20, 2021, that booming voice will announce: “Ladies and Gentlemen, the President of the United States of America”!

* * *

“As we get herded into our echo chambers of self-reinforcing information, we lose more and more sense of the real world and of each other. With it, our ability to empathise and compromise is eroded.”

– Jonathan Cook, commenting on the Julian Assange hearings.

Real Vision senior editor Ash Bennington hosts managing editor Ed Harrison to make sense of the biggest 3-day breakout in equities since April. Through the lens of Ed’s most recent piece in “Credit Writedowns.” Ed and Ash explain why low interest rates tend to make growth stocks more valuable relative to value stocks, and why the recent rally in small-cap value stocks might be short-lived. Ed looks forward to his interview with hedge fund legend Leon Cooperman, which airs tomorrow, on Tuesday, September 29. The pair also discuss discount rates, portfolio rebalancing, and endogenous credit creation.

via ZeroHedge News https://ift.tt/2SdMZ7n Tyler Durden

China Calls For ‘Green Revolution’ – Right After Approving “New Fleet Of Coal Plants” Tyler Durden

Mon, 09/28/2020 – 18:00

Chinese President Xi Jinping announced plans last week to boost China’s Paris climate accord target – calling for a green revolution and promising to achieve a peak in carbon dioxide emissions before 2030, and carbon neutrality before 2060.

A screen in Beijing shows China’s Xi Jinping appearing by video link at the United Nations on Sept 22, 2020.PHOTO: AFP (via Straits Times)

“China will scale up its intended Nationally Determined Contributions (to the Paris agreement) by adopting more vigorous policies and measures,” he said, urging the rest of the world to adopt a “green recovery of the world economy in the post-Covid era.”

That all sounds nice – except that as AFP (viaStraits Times) notes, “fresh spending on coal to rev up a virus-hit economy threatens to nullify its audacious bid to lead the world into a low carbon future.”

The fossil fuel has powered China’s economic surge over the last 30 years, and the nation burns about half the coal used globally each year.

Between 2000 and 2018, its annual carbon emissions nearly tripled, and it now accounts for nearly a third of the world’s total greenhouse gases linked to global warming.

Despite pledges to wean the economy off coal with the world’s most ambitious investment in renewables, China’s coal consumption climbed back in June this year to near the peak levels seen in 2013.

That was in part due to a pivot back to coal after geopolitical uncertainty in the Saudi peninsula, China’s main oil supplier. –AFP via Straits Times

After COVID-19 drove China’s economy to contract for the first time in three-decades, Chinese officials revved up the production of coal plants in order to revive provincial economies in dire circumstances.

According to Li Shuo, senior climate and energy officer at Greenpeace China, there’s a “tension at the heart of China’s energy planning” which “pits Beijing’s strategic interests against the immediate goals of cash-strapped provincial governments, makes it difficult to walk the talk” about a cleaner future. “China’s energy policy is like a two-headed beast, with each head trying to run in the opposite direction,” he added.

China accounts for nearly a third of the world’s total greenhouse gases linked to global warming.PHOTO: AFP

So, while Xi is making grandiose pronouncements about a ‘green revolution’ – the backdrop is that in the first half of 2020, China approved 23 gigawatts-worth of new coal power projects, which is more than the previous two years combined according to the report, citing San Francisco-based environmental NGO, Global Energy Monitor (GEM).

“A new fleet of coal plants is in direct contradiction with China’s pledge to peak emissions before 2030,” said Lauri Myllyvirta, China analyst at Centre for Research on Energy and Clean Air.

Meanwhile, China’s coal surge will most likely destroy the market for renewables within the country – as China uses Soviet-style energy distribution quotas, where power suppliers are allocated a monthly supply cap – which has pushed local governments to boost allocation for inexpensive coal, leaving less room for renewables regardless of investment in new technologies.

Wind and solar farms have been forced to idle and dozens of new renewable projects have been cancelled since late last year as small private operators struggle to make money. –Straits Times

“Local governments prefer to buy more coal-generated power to protect mining jobs,” said Li.

via ZeroHedge News https://ift.tt/3n1neW3 Tyler Durden

With the 2020 US Presidential election fast-approaching, many investors are likely wondering how November’s election results will shape markets and the economy in the months and years ahead. In this quarter’s version of Evergreen Roundtable, we are offering different viewpoints from several members of our investment team on six important questions related to the 2020 US Presidential election:

What equity sectors benefit from a Biden v. Trump victory?

Would a Biden presidential triumph hurt stock prices?

What are the most important issues (from an investment implication standpoint) the next POTUS will face? (Tax reform, health care reform, more Covid-19 related regulations, climate change agenda, China policy, etc)

What is the likelihood of a unified government and how will that impact future policy reform?

Under a Joe Biden presidency, how would this affect US energy policy and our view towards both energy and renewable energy investments?

Please discuss individual and corporate tax changes under both Biden and Trump along with any potential changes to taxes on capital gains, inheritance, & wealth, along with any adjustments to tax credits?

Evergreen’s investment decisions are not made by any single individual. Instead, our team confers nearly every business day to discuss our various investment strategies. This team consists of people with very different lenses through which they view the world and, oftentimes, these daily investment discussions become quite “spirited.” We foster the competition of ideas. Evidence and logic outweigh seniority or rank.

Jeff Eulberg (Managing Director, Family Office, Partner), Jeff Dicks (Director of Portfolio Management), Tyler Hay (Chief Executive Officer), and Mark Nicoletti (Managing Director, Family Office) all weigh in on this special edition newsletter. As always, we welcome your feedback and appreciate your loyal readership.

WHAT EQUITY SECTORS BENEFIT FROM A BIDEN V. TRUMP VICTORY?

Tyler Hay

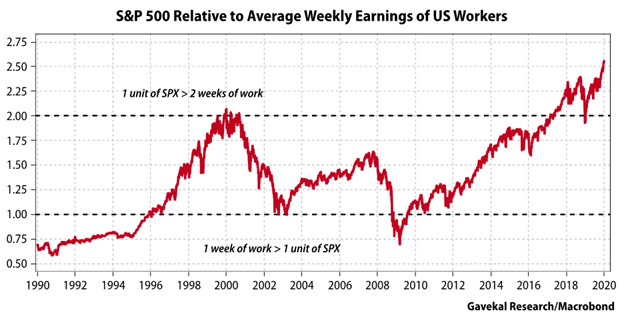

Many investors are counting on the presidential election to be a pivotal event for equity markets. This may be true in some areas, but as a whole, I think this viewpoint misses the mark. Instead, I’ve directed my focus to the effects of fiscal versus monetary policy. Said more simply: the stock market has returned on average 14.5% per year from 2009-2019, while over the same time period, workers’ wages have only increased 2.9%. Meaning Wall Street and those people who own assets (real estate, stocks, bonds, etc.) have seen a massive surge in wealth following the Great Recession while the average worker has been left in the dust.

Regardless of which candidate wins, either will almost certainly be forced to face this reality. I can think of a number of ways whoever is elected may choose to address this growing wealth gap. There’s a punitive approach, in which you try to slow down the success of the “winners”. This could manifest itself in raising taxes on the wealthy. The reason that I think a “wealth tax” is likely is that Biden’s most recent tax plan clearly looks to be headed in this direction. Another punitive approach would be the pursuit of antitrust regulations aimed at some of the tech giants. While the merits of antitrust regulation or higher taxes should remain a topic for another day, the pursuit of either policy would likely not be welcomed news for the stock market. More benign tactics to address the disparity in wealth could be an increase in the minimum wage, a universal basic income, and a national infrastructure upgrade similar to Roosevelt’s WPA, or Works Progress Administration, a key part of his New Deal. (The latter being most pragmatic in my view.) Instead of focusing on who wins the election, I’d advise investors to focus on how each candidate proposes tackling the growing wealth gap, which is the real elephant in the room for markets.

Mark Nicoletti

Should the President prevail in November, the original post-Hilary ‘Trump trade’ from four years ago will probably still hold this time. Which stocks are poised to do well on the premise of tax cuts and deregulation? Financials, energy, and more broadly value stocks, should thrive. However, this rosy scenario carries one major potential asterisk: a re-escalation in the trade war with China. Post a Trump re-election, the dollar will likely strengthen temporarily, as it did four years ago.

The Biden trade, as stated above, hinges in my opinion on the presumption of a Blue Wave. His plan to raise corporate taxes from 21% to 28% is, and should be, one of any prudent investor’s major concerns. His policies would be bullish for publicly- traded pass-through tax entities, including REITs (which are not required to pay corporate taxes). If you examine how stocks have been moving this summer in response to odds for a Biden victory, it’s telling. Relative to the market as a whole, technology, consumer discretionary, communication services, and healthcare have all outperformed when the polls have favored Biden. Meanwhile, financials, industrials, and energy have all tended to move inversely. This scenario is the exact opposite of what happened after the Trump victory in November ’16 when cyclical stocks outperformed and defensive sectors (excluding tech) lagged behind.

WOULD A BIDEN PRESIDENTIAL TRIUMPH HURT STOCK PRICES?

Mark Nicoletti

As do most of my peers, in some way or another, I interface with our firm’s clients on a regular basis. My unscientific opinion is that there are three predominant issues on the minds of our client base. They are, in order of concern: 1) The election 2)The pandemic 3)The Fed’s policies.

Although I’ve definitely learned more from our clients than they have from me over the years, I would argue these sentiment readings are in reverse order to the threat they potentially pose to portfolios.

Among them, I believe the Fed’s easing policies (still) have the most potential impact on asset prices, followed by the backdrop of the ongoing pandemic, and lastly the election results. I’m not suggesting the markets won’t rally on a Trump victory or a working vaccine coming to market – they probably will. I’m also not suggesting investors shouldn’t prepare as effectively as possible for the upcoming election – they absolutely should. I’m simply suggesting that, although political uncertainty will always cause market volatility, the fundamental impact of a Biden victory is not the most critical market input.

The reality is that Biden’s manifesto contains multiple policies that could safely be described as business-unfriendly, such as tax increases and regulation, which can weigh on corporate profitability. However, this same manifesto is also likely to include additional rounds of fiscal stimulus. While I acknowledge the likelihood of a negative short-term impact on risk assets resulting from a Biden victory, I think it might be short-lived.

Time will tell.

This election comes at one of the more turbulent times America and, indeed, the world has seen in decades. The ongoing pandemic, social unrest, and bipartisanship are (or should be) all clear concerns, but, given the fact that an unprecedented number of Americans are expected to vote by mail, there is a material risk that any election result is contested. That sort of chaos, which I’d call likely, is almost certain to cause a market selloff. During the 5-week Bush-Gore fiasco in 2000, the market dropped 12%.

Jeff Eulberg

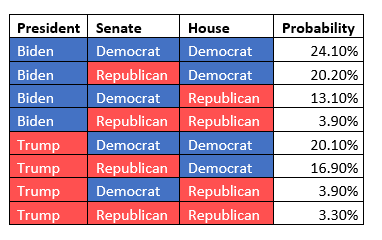

In order to anticipate market swings, we must first do our best to understand current market expectations. Depending on the National poll, Biden holds anywhere from a 4% to 10% lead over Donald Trump. Yet, important swing states are much tighter, and the electoral map is far from a slam dunk for Biden. Beyond paying close attention to the races in those key states, we also look at gambling markets where bettors are truly putting their money where their mouths are. Currently, Biden has a slight lead at -135 (bet $135 to win $100) to Trump at -110 (bet $110 to win $100).

Over the last six months, the market rally has coincided with Biden’s polling gains. This could lead one to conclude that investors aren’t concerned about a Biden presidency. I would argue that the market might not be alarmed due to the potential change in the executive branch but would become much more concerned if the Republicans were likely to lose control of the Senate, too. In the Senate, the Democrats need to keep their current seats and flip three others from the GOP. Four races are seen as competitive for incumbent republicans (North Carolina, Maine, Arizona, and Colorado). Meanwhile, the Democrats are fighting to maintain a seat from Alabama in a state where Trump won by more than 29% in 2016. At this point, I believe the Senate will remain controlled by the GOP, thus, I don’t anticipate a lasting market sell-off due to the Presidential election results.

If Biden wins the election and the Senate was to flip to the Democrats, I would anticipate a short-term market sell-off. The market would foresee higher taxes and increased regulations, obviously not conducive to higher earnings. Ultimately, I wouldn’t recommend selling equities in any of the above scenarios. I’ve long believed that adjusting your allocations due to a change in the Presidency is misguided. While Biden would like to raise taxes, he’s unlikely to do so in the middle of a recession. And, if he does, that would lead to a challenging mid-term in 2022 and could swing the Senate back to the conservatives. Regardless of who wins in 2020, the market environment for the next 4 years will be very challenging. The next President will have a tremendous amount of work to do to get the economy moving in the right direction and current market valuations don’t leave much room for error.

WHAT ARE THE MOST IMPORTANT ISSUES (FROM AN INVESTMENT IMPLICATION STANDPOINT) THE NEXT POTUS WILL FACE? (TAX REFORM, HEALTH CARE REFORM, MORE COVID-19 RELATED REGULATIONS, CLIMATE CHANGE AGENDA, CHINA POLICY, ETC)

Tyler Hay

My previous answer could have easily been copied here (as I do think it’s the most important long-term issue facing our country). That being said, I do not think the wealth gap is the most urgent matter the next POTUS will face. We are now nine months into this global pandemic and so much uncertainty remains, such as:

Will there be a second wave as countries in the Northern Hemisphere head into winter?

Can we effectively re-open the economy with social distancing?

Should we bite the bullet and re-open, just telling those at-risk to seclude themselves until a treatment/vaccine arrives?

How long until a vaccine/therapy emerges?

Will enough people even get vaccinated, should one become available?

How effective will a vaccine be?

Is COVID here to stay like the seasonal flu?

Is a robust testing system a nation’s best approach in a COVID world?

I think it’s wildly optimistic to assume that this Pandemic will be turned off like the flip of a switch, instead it’s more likely to dim over time. In the meantime, the economy, particularly in certain areas, is being decimated. It goes without saying that no president wants to preside over a flagging economy. The approach we’ve taken so far has been the equivalent of trying to hold our breath underwater; eventually, we have to come up for air. Therefore, the next 4 years will largely be defined by how the next POTUS navigates this ongoing virus crisis.

Jeff Eulberg

The most important issue for the next President will be managing the impact of the Coronavirus. If we can’t keep our hospital systems from being overwhelmed, it will be all but impossible to achieve much else during the term. If corona is managed, the next most important task will be reviving the U.S. economy. While always a top concern, the pandemic has amplified this need with over 11 million Americans currently out of work, along with the steepest decline of Gross Domestic Product (GDP) in history. At this point, we have no idea how society will adjust to our new normal. What jobs have been lost permanently? To compound issues, the next President will be tasked with achieving this goal as the nation is more divided than any time in my lifetime.

As I highlighted in my market reaction discussion, I don’t currently believe the Democrats will be able to gain control of the Senate, leaving either President with a split congress. And, much like the US population, Congress is also incredibly divided and unable to find much common ground (see: the long-awaited stimulus package 2.0). Therefore, it will be an uphill battle for either to make sweeping changes in an effort to jump-start the US economy.

One bipartisan idea that will likely be implemented is a large infrastructure spending bill. From an investment perspective, this would lead us to look at cyclical companies that would benefit from such a package. Fortunately, many of these companies currently offer attractive valuations, especially relative to some of the highflyers of the last 6 months.

WHAT IS THE LIKELIHOOD OF A UNIFIED GOVERNMENT AND HOW WILL THAT IMPACT FUTURE POLICY REFORM?

Mark Nicoletti

There are four plausible electoral scenarios, two of which result in a unified government. The impact of divided vs. unified government is enormous; and probably a better predictor of future policy change than which candidate prevails.

Historically, election platform policies often struggle to become legislation but this time around, there is plenty at stake. Tax reform, broader regulation, and COVID-19 related responses, among others, are all potential battlegrounds.

This notwithstanding, the potential for a unified Democratic government is greater than in recent years, and probably the only scenario worthy of dissection. It’s quite possible voters view Biden and the Dems as more trustworthy on healthcare reform and possessing greater ability to navigate a second wave of Covid-19.

If victorious with a Blue Wave tailwind, Joe Biden will seek to increase spending on climate change mitigation, expand federal-funded healthcare, and raise taxes on corporations and high-income earners. The initial investment implications of this scenario will undoubtedly focus on taxes and the negative business sentiment more regulation will bring. The longer-term scenarios to be weighed are almost certainly climate policy and energy efficiency, and the corresponding winners and losers due to changes in both.

Jeff Dicks

One way to calculate the odds of a unified government is to simply look at the betting odds for the President, the House, and the Senate. According to www.electionbettingodds.com, the odds of Republicans taking the presidency, controlling the Senate, and controlling the House, are 44.3%, 45.5%, and 16.3% respectively. For all three of these events to occur, we can multiply each of them together, which works out to 3.29% odds of a Republican sweep. At the Kentucky Derby, this would be like betting on a 30-1 longshot, which can happen, but not very often. In that scenario, in terms of policy reform, it would be very much a continuation of what we have seen the last four years. On the tax side, the Republicans have floated an unspecified tax cut for individuals. In addition, there would be a potential tax credit for moving manufacturing abroad to America, with extra emphasis on bringing manufacturing jobs from China to the US. These firms would potentially be able to deduct 100% of expenses to hopefully incentivize the shift stateside. Within Trump’s second term agenda, there would be a focus on lowering prescription drug prices and attempting to reduce insurance premiums. We’d also likely see a continuation of the tough stance against illegal immigration, a refunding of our police, and continued deregulation of the energy industry. Donald Trump’s second term agenda can be found via the following link. The agenda is rather ambitious but was a bit lacking in terms of actual details surrounding key objectives in another term. As mentioned, at this point, a Republican sweep appears unlikely, but elections in the past have been difficult to call and predict.

The flip side shows the odds of the Democrats winning the Presidency, the Senate, and the House at 53.1%, 54.4%, and 83.60% respectively. This works out to a 24.15% chance of a Democrat sweep. Out of any combination, a Blue sweep currently commands the best odds. However, some sort of split would be the most likely over a united government at over 70%, given the 24% odds and 3% odds of a Democratic and Republican sweep respectively. The policy shift under a Blue sweep would be significant since there are limited barriers to implementing these policies. The Biden administration would look to unwind most of the tax cuts under the Tax Cuts and Jobs Act. For instance, Biden has proposed raising the corporate tax rate to 28% from 21% (this was lowered from 35% to 21% under President Trump). In addition, Biden would look to raise taxes on the individual side and to increase the capital gains tax for high-income earners to the ordinary income rate. Biden would also look to expand health care coverage, and like Trump, look to lower healthcare costs. The Democrats’ platform would prioritize climate change via restriction on the energy industry and expansion in terms of pro-renewable energy policy (see energy response below). Overall, stricter regulation is expected across most industries with this impact being felt most acutely among financials, pharmaceuticals, and even technology. A Blue wave would be less restrictive on immigration, along with dialing back the Trump administration’s travel and immigration bans, reinstating protections for “dreamers,” and rescinding funding for a border wall. Finally, an infrastructure spending bill would likely get passed, which appears to have bipartisan support. From a financial markets perspective, that corporate tax increase may be the most market-moving item under this scenario. RBC capital markets estimates the proposed increase would likely fall 5.5%-10% with higher corporate taxes.

Here are the odds of each scenario currently bases on the current odds.

UNDER A JOE BIDEN PRESIDENCY, HOW WOULD THIS AFFECT US ENERGY POLICY AND OUR VIEW TOWARDS BOTH ENERGY AND RENEWABLE ENERGY INVESTMENTS?

Jeff Dicks

US energy policy would be one area that would see a rather large shift under a Biden presidency. Day 1 President Biden has publicly stated he will restrict new oil and gas drilling on federal lands and waters. It’s worth noting this is a much scaled-down ban relative to what was floated by Elizabeth Warren, which proposed banning all drilling on federal lands. A few points here would be that producers will likely move to other regions where production is primarily on private lands, as well as stockpile public land permits ahead of Biden taking office. With that said, this policy will restrict energy production in the US relative to current policy. With the collapse in energy prices due to Covid-19, we have seen a major reduction in capital expenditures across the energy industry both in the US and abroad. Further restriction on production likely would lead to higher energy prices over the near-to-medium term. We believe the beneficiary of lower US production would be international energy producers that can make up the production shortfall, as well as benefit from higher prices.

Biden will also make a big shift to becoming net-zero carbon emissions by 2050. Getting our country there will require companies to carry the cost of the pollution being emitted, which likely lowers the profitability profile for corporate America. Along these lines, Biden will rejoin the Paris Climate Agreement and make a push towards limiting carbon emissions internationally. In the US, as we have continued to shift away from coal to natural gas and renewables, we have seen CO2 emissions per capita go down since 1970. Globally, a critical aspect of reducing carbon emissions is shifting countries like China away from coal. China makes up over 28% of carbon emissions, and per capita emissions have more than tripled in China since 1980. We would point out that regardless of the President, this is a very important shift that needs to take place. This is also a shift that will benefit companies exposed to producing and transporting natural gas in the US. We feel this trend will be critically important for our environment, and also a smart place to allocate capital over the next 20 years.

Biden has expressed the desire to make a very large investment into clean energy, which would expand the power generating capacity in areas like wind and solar. It will be important to allocate funds efficiently given many European countries have seen higher electricity costs from similar programs. With that said, it’s been promising to see that many areas across the country have seen dramatically lower costs for clean energy. From an investment standpoint, we have continued to increase our exposure to companies tied to clean energy, and under a Biden presidency, we believe this area would gain shares against traditional energy power generation. Ultimately, we would expect to continue to allocate a larger proportion of our clients’ assets in companies that benefit from this trend.

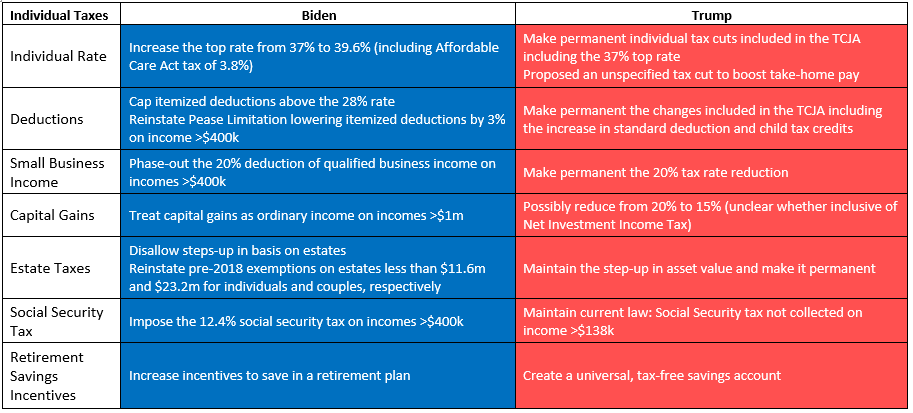

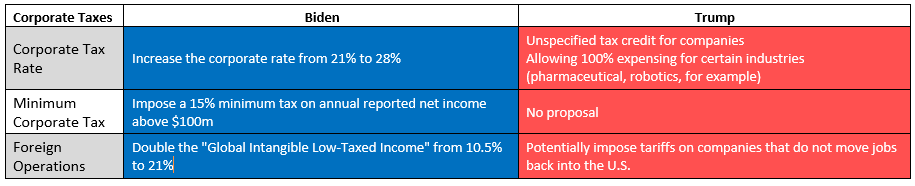

PLEASE DISCUSS INDIVIDUAL AND CORPORATE TAX CHANGES UNDER BOTH BIDEN AND TRUMP ALONG WITH ANY POTENTIAL CHANGES TO TAXES ON CAPITAL GAINS, INHERITANCE, & WEALTH, ALONG WITH ANY ADJUSTMENTS TO TAX CREDITS?

Jeff Eulberg

The table above outlines the key differences in both tax plans. Biden is campaigning to roll back several of Trump’s recent tax changes. However, what Biden wants to do and what he can do are two very different things. As mentioned in all of my answers for this piece, without the Democrats flipping the Senate, many of these proposals will never be implemented. Further, even if the Democrats can flip the Senate, Biden is unlikely to make an aggressive attempt to raise taxes with so many Americans unemployed and the economy just starting its recovery process. If a major tax hike was implemented, the low hanging fruit for the Democrats would be to raise taxes on two smaller voting groups – the wealthy and corporations.

I would anticipate a corporate tax increase to at least 28%. From an economic standpoint, Evergreen has written several times that the Trump administration’s dramatic corporate tax rate cut in 2017, when the economy was in a strong growth phase, was misguided. Most disturbingly, it led to unprecedented deficits during good economic times. Thus, while a partial reversal will certainly impact earnings, longer-term it wouldn’t appear to be a catastrophic shift.

Wealthy individuals could see increased ordinary income and capital gain rates with meaningful estate tax adjustments. In 2017, we were shocked to see the Federal estate tax exemption go from just over $5.6m to $11.2m. If a new tax bill was to pass, these increases will very likely be rolled back before they’re set to lapse in 2025. If we get closer to November and it appears that the Democrats are likely to flip the Senate, you can expect us to advise on potential estate tax techniques to utilize the higher exemptions, recommend liquidating concentrated long-term gain positions and pulling income forward to 2020. That said, for now, much of the tax increase concern might be a bit overblown and an inevitable outcome of election season rhetoric.

via ZeroHedge News https://ift.tt/338F55K Tyler Durden

Meet The Mastermind Behind JPMorgan’s Gold And Silver Manipulation “Crime Ring” Tyler Durden

Mon, 09/28/2020 – 17:20

There was a time when the merest mention of gold manipulation in “reputable” media was enough to have one branded a perpetual conspiracy theorist with a tinfoil farm out back. That was roughly coincident with a time when Libor, FX, mortgage, and bond market manipulation was also considered unthinkable, when High Frequency Traders were believed to “provide liquidity”, when the stock market was said to not be manipulated by the Fed, and when the ever-confused media, always eager to take “complicated” financial concepts at the face value set by a self-serving establishment, never dared to question anything.

All that changed in November 2018 when a former JPMorgan precious-metals trader admitted he engaged in a six-year spoofing scheme that defrauded investors in gold, silver, platinum, and palladium futures contracts. John Edmonds, then 36, pled guilty under seal in the District of Connecticut to commodities fraud, conspiracy to commit wire fraud, commodities price manipulation, and spoofing, a trading technique whereby traders flood the market with “fake” bids or asks to push the price of a given futures contract up or down toward a more advantageous price, and to confuse other traders or HFTs which respond to trader intentions by launching momentum in the other direction. As FBI Assistant Director in Charge Sweeney explained at the time, “with his guilty plea, Edmonds admitted he intended to introduce materially false and misleading information into the commodities markets.”

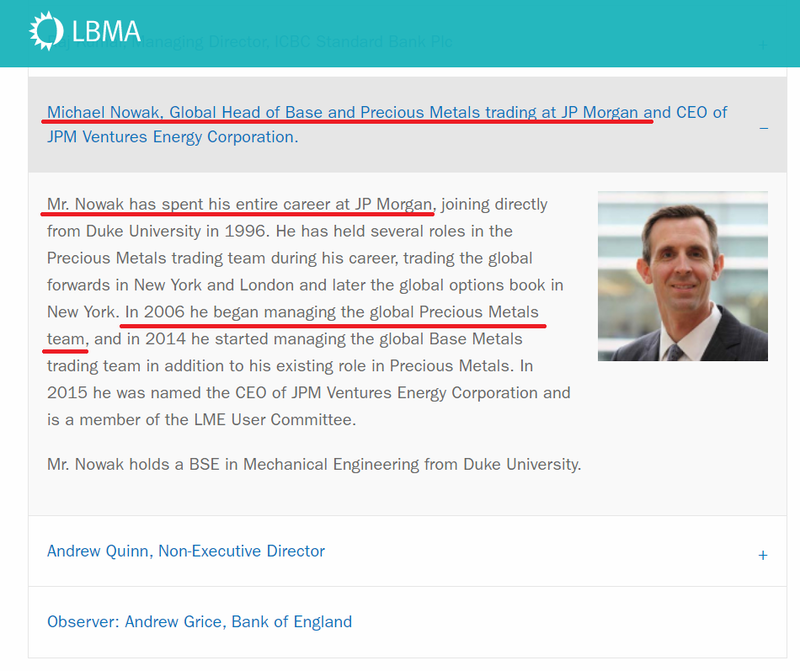

Today, Bloomberg is finally catching up to years of “conspiracy theory” reporting, such as this article published here in 2014 and titled “Gold Rigging By Bullion Banks Exposed: The Complete Chart“, with a sweeping expose about the precious metals manipulation and spoofing scandal, focusing on the precious metals trading desk at JPM and its top trader, Mike Nowak.

And although Bloomberg inexplicably did not mention it even once in its lengthy report, Nowak’s desk was under the direct purview of Blythe Masters, who from 2007 until 2014 was the head of Global Commodities at JPMorgan.

Which is ironic because going all the way back to 2012, the “tinfoil hat” crowd was abuzz with speculation that central banks, perhaps in league with the big broker dealers and occasionally aided by HFT momentum ignition, were conspiring to manipulate precious metals prices. When questioned about this in an interview with CNBC, Masters denied that JPMorgan was engaged in any manipulation, and instead insisted that JPM’s precious metals desk was reputable a “client-driven business.”

“Our business is a client-driven business where we execute on behalf of clients to help them with their…risk management objectives,” Blythe Masters said before going on to claim that the bank runs a “balanced book”, where its long and short positions are always evened out. But the punchline was when Master, who is perhaps best known for discovering the Credit Default Swap, said that manipulating markets to benefit the bank’s positions to the detriment of clients would be “wrong, and we don’t do it.”

Oops.

Masters quietly quit JPM two years later – perhaps sensing that the regulators are starting to sniff around the precious metals business and just after she was named by FERC for organizing the manipulation of power markets in California and the Midwest (JPM settled for $410 million). Unfortunately for her former subordinate, Mike Nowak, who until recently was the top JPM precious metals trader, he is now in the crosshairs of a unprecedented RICO case alleging his trading desk operated like an ongoing criminal conspiracy due to its abuse of “spoofing” a strategy that has been blamed as illegal market manipulation that may have caused the 2010 flash crash.

In a lengthy feature detailing the federal investigation into Nowak’s desk, Bloombergreveals how Nowak’s scheme was exposed to the world after regulators came knocking and former subordinates turned against him, and how the ‘spoofing’ practice’ first arrived at JPMorgan alongside several new faces from Bear Stearns, which JPM “bought” back in 2008 in a government-backstopped deal for pennies on the dollar.

Testimony from Edmonds and other turncoat traders might help earn guilty verdicts against Nowak and three co-defendants from JPM. If prosecutors win more guilty verdicts against Nowak and his team, it could set a new precedent for how the big banks use tools like RICO to go after the big banks.

In charging Nowak and others, prosecutors are testing an unusual application of a law formulated to battle mobsters, the Racketeer Influenced and Corrupt Organizations Act. Prosecutors say Nowak’s trading desk was a criminal racketeering operation within the confines of America’s biggest bank. Traders on Nowak’s desk engaged in spoofing as a core business practice, doing it more than 50,000 times over nearly a decade, they said..

The Justice Department has famously used the RICO statute to bring down mafia bosses and drug gangs. It has used other statutes to extract penalties and guilty pleas from big banks accused of market manipulation. But it’s been decades since the government has attempted to apply the anti-racketeering law to members of a major bank’s trading desk, placing Nowak and others in crosshairs once trained on the likes of the Latin Kings and the Gambino crime family.

As has traditionally been the case in various DoJ cases against Wall Street spoofers, the evidence includes Bloomberg extensive and damning trader chat transcripts obtained by the court. Bloomberg offers an example early in the report.

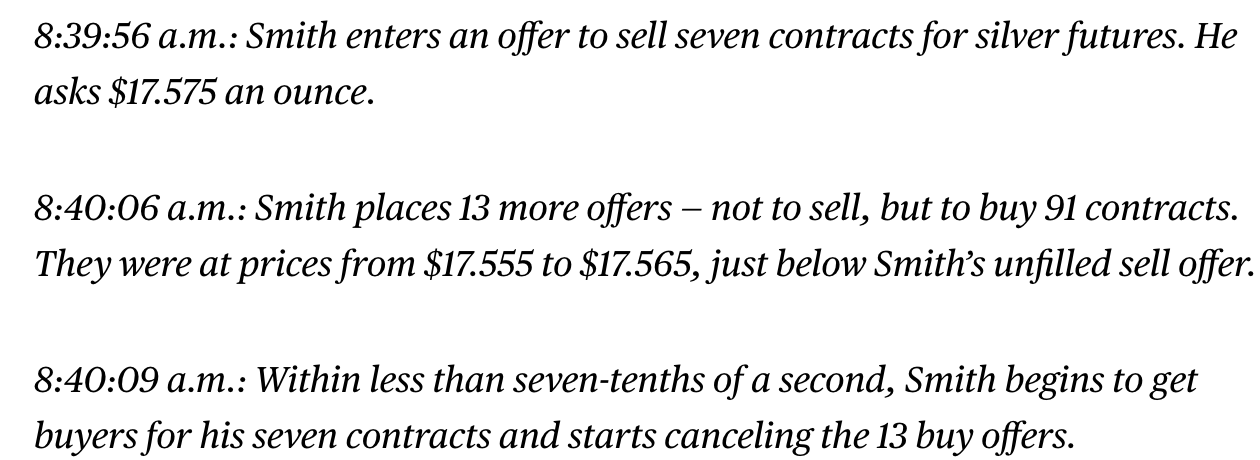

At that point, instead of consummating the purchase, Nowak received an instant message from a Bear Stearns manager across the street: “Smith just bid it up to … sell.”

Here’s another none-too-subtle exchange.

While much of the details behind the DOJ case had already been known to the market, for the first time the report explained how federal prosecutors based in Connecticut initially stumbled on to the JPM precious metals desk. As the DoJ was upping its focus on market manipulation with cases involving FX and other asset classes, prosecutors started looking for patterns in the raw trading data provided by the exchanges. When they looked for individual traders cancelling a bevy of orders on one side while executing on the other, they noted it as a possible example of spoofing. Quickly, trades made by Edmonds and other members of Nowak’s desk stood out.

One can imagine that when prosecutors decided to ‘shake the tree’ and confront Edmonds with the evidence he quickly folded. The team soon secured another cooperating witness from the Bear Stearns side, and they were off.

The arrest of Nowak – who was also on the board of the LBMA (which described itself as the “the world’s authority on precious metals”) until he was kicked off in Sept 2019 once the charges against him were revealed…

… sent a shockwave through the industry as others wondered whether they could also come under scrutiny: because “if he could come under scrutiny, couldn’t anyone?”

Nowak’s trial is on pace for next year, according to filings in the case. One expert said the odds will be stacked against Nowak since the government should be able to use a JPMorgan settlement in its favor.

“The company — and all its information and all of its personnel — is now sitting at the prosecutors’ table,” one lawyer said.

Curiously, in a non-too trivial defense, Bloomberg explained that Nowak believed that spoofing was more or less required to help human traders fend off algorithm-driven HFT firms from siphoning up all the profits. He may have a point. Here is how Bloomberg describes the attempt by upstart HFTs market manipulators to steal market share from such established manipulators are JPM:

For generations, metals changed hands in open-outcry pits where hundreds of traders screamed prices and obscenities. Nowak, introverted and brainy, came along in time for electronic trading and the problems it posed. Firms and individuals with fast internet connections and proprietary algorithms were swarming in and out of positions to profit on small daily price moves.

For long-time readers, none of this is news – after all this is precisely the dynamic we explained first in 2009 and watched it grow and flourish for much of the 2010s. At the same time, some of the most notable traders across Wall Street were directly engaging with these HFTs in a furious battle of life and death, as humans constantly tried to outsmart the machines. One such approach was to spoof them (HFT powerhouse Citadel recently filed a lawsuit it was “defrauded” by humans who successfully spoofed its algos).

Traders at big operations like JPMorgan’s found that within a second of placing a bid, their price was often countered by high-frequency traders who would match and close a position before the traders had a chance to complete their deal. These algos not only snapped up trades but also created momentum in the market that pushed prices away from the traders’ targets.

One way to outsmart them, current and former brokers and traders say, was to put up and remove an offer on the opposite side of the market. That would cause the algorithms to recalculate market supply and demand, leaving an opening for the traders to get the deal done at the price they wanted.

Early on, some of Nowak’s traders were attempting to counter the algos by placing a single large order opposite the one they wanted filled, according to prosecutors. The Bear traders’ twist was to place multiple orders, at different prices, that in aggregate were substantially larger than the genuine order — a technique the government calls layering. The orders, made in rapid succession after the genuine order, would be canceled as soon as the genuine order was filled. Think of it like trying to sell a hamburger. You conjure a mob in front of your burger joint, creating the perception of demand. Once a real customer steps up and buys the burger, you make the mob vanish.

While this strategy is familiar to everyone who wishes to create a buzz – such as the fake lines to buy iPhones in front of Apple stores – the problem is that in capital markets at least, spoofing is illegal. Unfortunately, since HFTs were also legal – and they should never have been allowed in a post Reg-NMS world – it left traders relying on their own devices to outsmart the robots, and that’s why spoofing became more and more popular and prevalent.

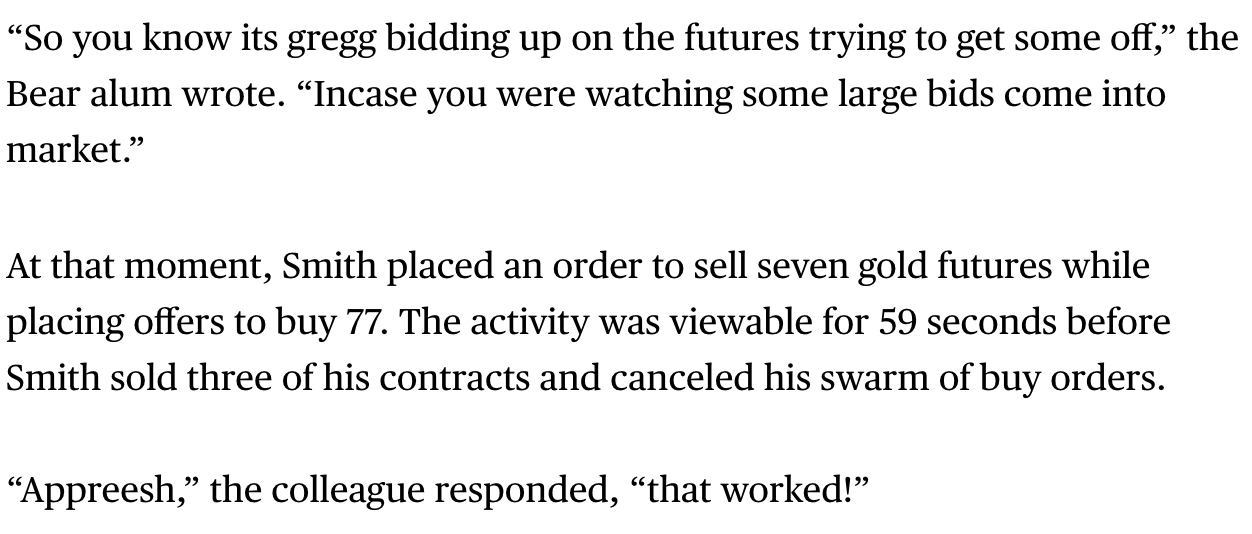

The layering worked in futures markets in part because participants see a second-by-second barrage of offers to buy and sell, but not who’s making them. And whereas one big order might stand out, a lot of small ones might not. That made it important to warn colleagues when layering was in progress. One of the former Bear traders did just that for a new JPMorgan colleague in early 2009, according to prosecutors.

“So you know its gregg bidding up on the futures trying to get some off,” the Bear alum wrote. “Incase you were watching some large bids come into market.”

At that moment, Smith placed an order to sell seven gold futures while placing offers to buy 77. The activity was viewable for 59 seconds before Smith sold three of his contracts and canceled his swarm of buy orders.

“Appreesh,” the colleague responded, “that worked!”

Altogether, Smith, a lead gold trader, executed some 38,000 layering sequences over the years, or about 20 a day, prosecutors said in filings. (Smith has pleaded not guilty). Nowak himself primarily traded options, but he would dip into the futures market to hedge those positions. He tried his hand at layering in September 2009, according to filings, and went on to use the technique some 3,600 times.

So what was the damage?

Well, according to the government, JPMorgan’s traders caused tens of millions of dollars in losses for those on the other side of the transactions – which included not just HFTs but regular, retail traders – and “harmed market integrity.” As a result, JPMorgan’s precious metals trading desk — which brings in as much as $250 million in annual profit — generated millions of dollars in unlawful gains.

What may explain the brazen manipulation not only at JPM but at every other abnk is that the CFTC – those toothless regulators once led by late Bart Chilton – looked into allegations of market manipulation of the silver market by JPMorgan not once, not twice, but three times… and found nothing (to much mockery).

Nowak, who held leadership roles on the LME and the London Bullion Market Association, was asked to explain the bank’s trading. In 2010, he sat for two days of interviews with CFTC investigators, explaining the bank’s trading strategies.

“To your knowledge, have traders at JPMorgan in the metals group put up bids and offers to the market which they didn’t intend to execute and then pulled them before they got hit or lifted?” one CFTC investigator asked.

“No,” Nowak responded.

The CFTC closed the third of those three inquiries in 2013 without taking action. JPMorgan has cited those CFTC investigations while defending against civil lawsuits, accusing plaintiffs of rehashing “implausible theories” of silver futures manipulation that were rejected by regulators.

It turns out those theories were not only plausible but true, and they were only validated thanks to an upstart, young prosecutor name Avi Perry, an assistant U.S. attorney in Connecticut with a Yale law degree. As Bloomberg puts it “Perry didn’t set out to target JPMorgan’s operation so much as JPMorgan’s trading found him.”

Perry started hunting for market manipulation around 2018, as the Justice Department was upping its game in the area. For years, prosecutors had built market manipulation cases by following up on tips and pulling trading data on suspects. Now they were doing deep dives into raw data to uncover targets, parsing records filed directly with the exchanges.

In the real-time scrum of futures markets, where offers are made and pulled all day long, it’s nearly impossible to discern potential manipulation. But the government had an edge. The data feed of the trades includes each trader’s exchange credentials, allowing investigators to sort for suspicious patterns and attribute it to individuals.

Perry also had a valuable guide to the market. His lead FBI investigator, Jonathan Luca, previously worked as a gold and silver futures trader at Morgan Stanley. Together, they created a screen for precious metals trading data. The idea, according to two people familiar with the analysis, was to turn up sequences in which a trader placed and canceled a profusion of orders on one side of the market while executing a trade on the other. The bigger the mismatch between genuine and pulled offers, and the more a given trader did it, they said, the more it would be considered a red flag for potential spoofing.

When they ran the screen, traders at JPMorgan stood out.

The rest is history, and two years later JPMorgan is facing a record $1 billion wrist-slap, which one assumes is a fraction of the profits the bank made by manipulating gold and silver for over a decade, and a few traders are set to spend a few months in “Club Fed”-style minimum security prisons.

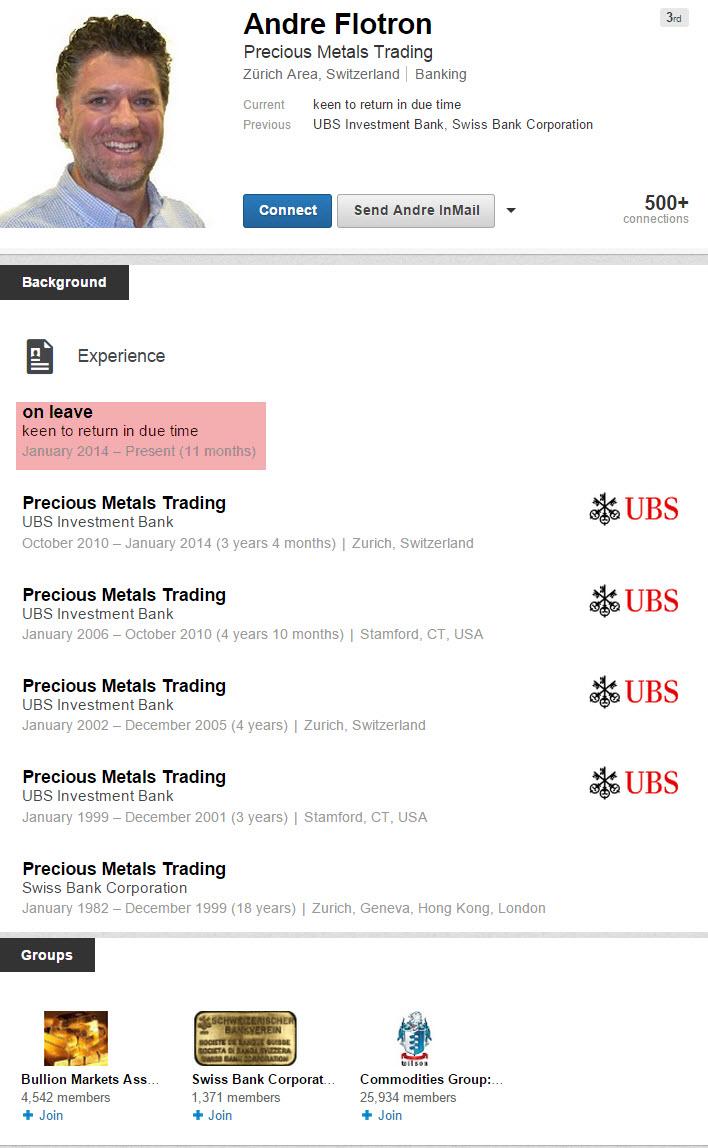

It didn’t come without complications though. Readers may recall one of the other notable gold manipulator names mentioned here over the past decade, that of UBS former gold desk head in Zurich, Andre Flotron (mentioned here , here, here and here). Well, Andre walked after Perry failed to present a convincing case and most of the charges against the former UBS gold trader were dismissed and he was acquitted. Defense lawyers and even some fraud prosecutors wondered if the government’s spoofing initiative was waning, according to Bloomberg.

But Perry did not give up and in 2018 his bosses recruited him for a job at the Justice Department’s fraud section in Washington, whose prosecutors have built some of the biggest U.S. corporate crime cases. With the trading analysis in hand, he went looking for individuals who might talk.

It’s unclear how Perry and the FBI approached Edmonds, who at times had placed orders with as many as 400 contracts on the opposite side of a genuine one, but they likely did so without raising alarms inside JPMorgan. Edmonds had left JPMorgan in 2017 after declining the bank’s offer to relocate to Singapore, and by the fall of 2018 was working at another bank.

Perry and his team talked to Edmonds at least twice in the weeks before he traveled to Connecticut to enter his secret guilty plea on Oct. 9, 2018.

Several months later, Perry secured the cooperation of one of the Bear traders who moved to JPMorgan. Pleading guilty, that trader said he personally manipulated trades while working from offices in New York, London and Singapore, and said spoofed trades were a fixture at the bank for nearly a decade.

However, in Nowak’s office there was little sign of dark clouds. Although banks often place individuals on leave when legal action may be pending, Nowak and Smith remained at their desks well after the charges against Edmonds were made public in November 2018.

Things then rapidly escalated, and to prosecutors, the evidence fit the template for a racketeering conspiracy, aka RICO, most famouslyused in cases against mafia families in the 1970s — a pattern of illegality over time, with individuals working together to further the goals of the allegedly criminal enterprise. Racketeering charges were leveled against Michael Milken in 1989 but dropped when he reached a settlement with authorities. The statute was successfully applied in the early 1990s against eight traders in the Chicago Mercantile Exchange soybean pits, according to Bloomberg.

Using the RICO template, by the summar of 2019, Perry had secured the government’s indictment of Nowak, Smith and a third trader. It was filed under seal in federal court in Chicago, where the trades took place. The charges were made public in September, and Nowak appeared in handcuffs in federal court in Newark, New Jersey — accused of conspiracy to participate in or conduct a criminal racketeering enterprise, attempted price manipulation, bank fraud, wire fraud, commodities fraud and spoofing. In addition to the half-dozen people who’ve been charged, the government documents referred to seven more individuals as unindicted co-conspirators. It’s not clear whether any of them have cooperated or what additional information they may have provided in the year since.

Nowak’s trial is scheduled for next year, and the government should be able to use the recent $1 billion JPMorgan settlement to its favor, Bloomberg said citing Michael Koenig, a former federal prosecutor who’s now a partner at Hinckley, Allen & Snyder who added that “the company — and all its information and all of its personnel — is now sitting at the prosecutors’ table.”

* * *

Yet now that all the “tinfoil” conspiracy theories involving the JPMorgan commodity trading desk have been confirmed, the bank is set to pay $1 billion to settle all ongoing legal cases (and is yet another reason why Jamie Dimon is richer than you), and a bunch of traders may go to prison for a few months, one name is strangely missing.

That of Blythe Masters, the person who was in charge of all JPMorgan commodity trading in the period 2007 – 2014 when most of these traders got their start in the spoofing business.

While we wait to find out how and why the DOJ missed this key JPMorgan staffer who supervised and made the spoofing possible for nearly a decade, and who was previously busted by FERC for similarly manipulating the energy market in California and Michigan (because merely rigging gold prices was not enough for the bank that also wanted to moonlight as Enron), we will remind readers of an interview Masters gave to CNBC in 2012 in which a primary topic, ironically, was whether or not Jamie Dimon’s firm manipulates the prices of precious metals, and particularly silver.

What followed was – as we know now – an avalanche of lies:

“JPM’s commodities business is not about betting on commodity prices but about assisting clients”… “it’s about assisting clients in executing, managing, their risks and ensuring access to capital so they can make the kind of large long-term investments that are needed in the long run to expand the supply of commodities”…

“There’s been a tremendous amount of speculation particularly in the blogosphere on this topic. I think the challenge is it represents a misunderstanding as the nature of our business. As i mentioned earlier, our business is a client-driven business where we execute on behalf of clients to achieve their financial and risk management objectives. The challenge is that commentators don’t see that. So to give you a specific example, we store significant amount of commodities, for example, silver, on behalf of customers we operate vaults in New York City, Singapore and in London. And often when customers have that metal stored in our facilities, they hedge it on a forward basis through JPMorgan who in turn hedges itself in the commodity markets. If you see only the hedges and our activity in the futures market, but you aren’t aware of the underlying client position that we’re hedging, that would suggest inaccurately that we’re running a large directional position. In fact that’s not the case at all.

“We have offsetting positions. We have no stake in whether prices rise or decline. Rather we’re running a flat or relatively flat matched book.

And the punchline from the 2012 interview:

“What is commonly out there is that JPMorgan is manipulating the metals market. It’s not part of our business model. it would be wrong and we don’t do it.”

Eight years later, JPMorgan is paying $1 billion because it was manupalting the metals market and was lying about it. Which begs the question: does this mean that manipulation is also part of JPM’s business model? We can’t wait for someone to ask Jamie Dimon this question at the upcoming JPMorgan earnings call

via ZeroHedge News https://ift.tt/3icConK Tyler Durden

Mayor Bill de Blasio is aggressively pushing for a $12.4 billion federal bailout – because New York City faces an unprecedented $7 billion budget deficit over the next two years.

Last week, in a public relations stunt, the mayor announced a one-week unpaid furlough of himself and 494 employees within his office – a taxpayer savings of a paltry $860,000.

So, how did the city get so deep into trouble?

Our auditors at OpenTheBooks.com dug into the skyrocketing city payroll. In 2016, there were 76,166 employees with pay exceeding $100,000. By 2019, there were more than 114,000 – a 50-percent increase in six-figure earners.

In 2019, plumber helpers earned $172,988; thermostat repairmen made up to $198,630; regular laborers hauled away $213,169; electricians lit up $253,132; and plumbers pocketed up to $286,245.

School janitors ($256,000) out-earned the principals ($154,000). Four deputy mayors made over $241,641 each and 5,998 city employees out-earned New York governor Andrew Cuomo ($178,000).

The city has 331,520 full-time equivalent employees – up from 297,349 in 2014.

However, 592,432 people pulled a paycheck at some point last year at a total cost of $29.5 billion. (This included base salary, overtime, and “other pay,” but not healthcare or pension benefits. Those perks add 30-percent.)

Office of the Mayor – $52 million payroll cost

Mayor Bill de Blasio’s base salary was $258,541 plus free rent at Gracie Mansion and regular police-escorted trips to the gym – even as he closed schools, restaurants, and gyms.

First Deputy Mayor Dean Fuleihan made $278,980 and three deputy mayors earned between $241,641 and $246,124. Even de Blasio’s executive chef Feliberto Estevez cooked up $124,285.

First Lady Chirlane McCray, de Blasio’s wife, works within the Office of the Mayor as a volunteer. However, fourteen city employees aid McCray with salaries that cost taxpayers $2 million per year.

McCray’s aides included senior advisors, communications advisors, and a policy director along with a chief of staff, two deputy chiefs of staff, a press secretary, speechwriter, videographer, and others, according to news reports.

The head count of McCray’s payroll (14) exceeded U.S. First Lady Melania Trump’s staff (11). Michele Obama employed 24 staffers as First Lady.

(The mayor responded for all agencies – review the comment at the end of this column.)

Department of Education — $13 billion payroll cost

Only in New York City can school janitors out-earn the principals. We found 40 “custodial engineers” who earned between $154,000 and $256,000, while 57 principals made less than $154,000.

Last year, over 50,000 educators earned a six-figure salary, including 37,324 teachers and substitutes.

The public schools spent a hefty $28,808 per student – twice the national average ($12,612) – while fourth and eighth grade math and reading tests significantly underperformed state and national averages.

Chancellor Richard Carranza made $357,973 – exceeding the salary of the U.S. education secretary Betsy Devos ($199,900).

Police Department — $5.2 billion payroll cost

The Police Department (NYPD) payroll included 59,970 employees last year, and nearly half, or 26,018, made six-figures or more. Included in the cost was $728 million in paid overtime.

However, only one police officer was in the top five NYPD most highly compensated.

Four “stationary engineers” – employees who operate industrial machines – led the payroll. Thanks to excessive hours and lax rules, these workers made between $84,850 and $101,740 in overtime. Stationary engineer Daniel Boyne was the highest paid person in the department ($261,682).

An additional 1,971 NYPD employees including chief Terrence Monahan ($236,943) out-earned governor Andrew Cuomo’s $178,000 salary.

Fire Department — $1.8 billion payroll cost

The Fire Department (NYFD) payroll included 18,679 employees last year, 8,970 of whom made six-figures or more. Top earners include four assistant chiefs paid between 264,558 and $302,810. Commissioner Daniel Nigro did not make the top ten earners with his $237,517 salary.

The department also created another kind of fire when it fired the whistleblower who discovered an alleged affair between the previous commissioner and a staffer.

Former administrator Lyndelle Phillips sued over an allegation of unlawful termination and settled the lawsuit last year. She collected $500,000 in back pay in 2019 and became the highest paid person on the entire city’s payroll.

An additional 856 NYFD employees out-earned the governor’s $178,000 salary.

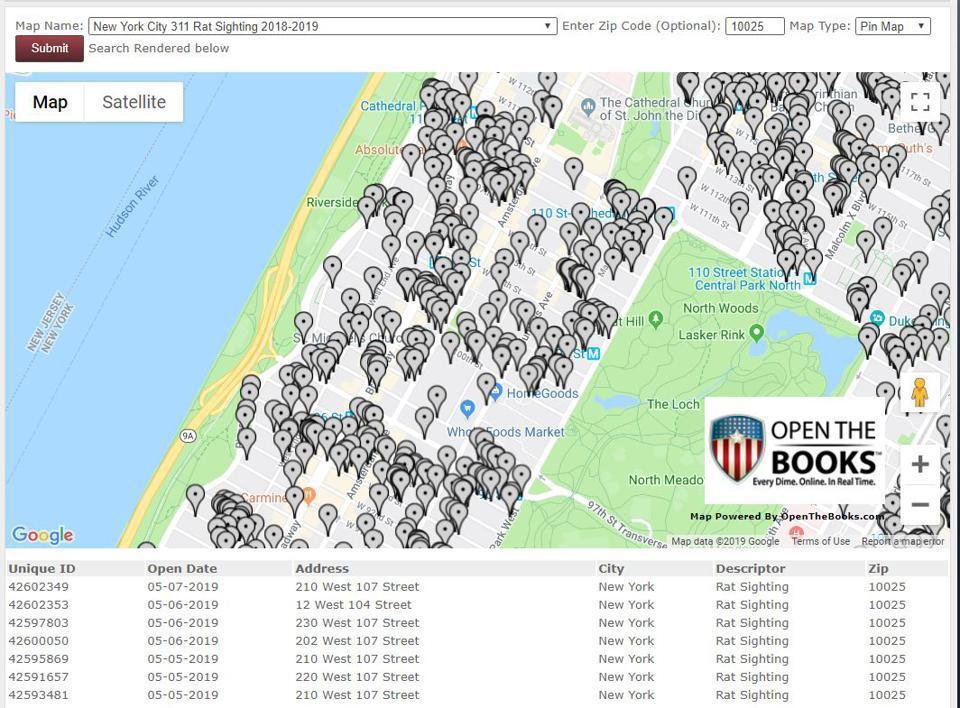

Rats Out-Fox New York City Bureaucrats — $32 million ‘War on Rats’ campaign

In 2017, Mayor Bill de Blasio declared war on the city’s rat population and demanded “more rat corpses.” The city council minted $32 million for the rat extermination campaign.

Despite a city workforce of 331,000, the rats outsmarted the bureaucrats.

Human Rights Commission — $10.5 million payroll cost

The chair of the Human Rights Commission (HRC) Carmelyn Malalis made $222,990 last year. By comparison, the top paid staffer at the federal Equal Opportunity Commission made $189,600 and the U.S. Attorney General made $199,700.

The HRC mission is to “combat discrimination and fight to ensure that everyone can live in, work in, or visit New York City free from discrimination and harassment.”

However, in a strange twist, the HRC doesn’t pay their interns. While ethically and legally questionable, the internships are available only to students privileged enough to attend college who can work a minimum of 112 unpaid work hours over a four-month period.

Maybe the HRC should investigate its own agency.

Overtime and “other” pay — $3 billion payroll cost

In 2019, city workers claimed an extra $1.9 billion by working 32 million hours of overtime — an average cost per hour of nearly $60. This allowed some workers to double and triple pay.