Shanghai Stock Exchange Postpones Ant IPO After BABA’s Ma Summoned By China Regulators Tyler Durden

Tue, 11/03/2020 – 08:14

The world’s largest IPO – Ant Group’s $35 billion dual-offering – is in peril as the Shanghai Stock Exchange has suspended the listing amid questions about regulatory compliance.

This decision follows reports that four Chinese regulators including the central bank and banking watchdog called billionaire Jack Ma and Ant Group Co.’s top executives to a rare joint supervisory interview on Monday, underscoring rising government scrutiny of the company before its stock-market debut.

Your company originally applied for listing on the Science and Technology Innovation Board of the Shanghai Stock Exchange (hereinafter referred to as the Exchange) on November 5, 2020. Recently, it happened that your company’s actual controller, chairman and general manager were jointly conducted supervisory interviews by relevant departments, and your company also reported changes in the financial technology regulatory environment and other major issues.

This major event may cause your company to fail to meet the issuance and listing conditions or information disclosure requirements. In accordance with Article 26 of the “Administrative Measures for the Registration and Administration of Initial Public Offerings on the Science and Technology Innovation Board (Trial)” and Article 60 of the “Shanghai Stock Exchange Review Rules for the Issuance and Listing of Stocks” and soliciting the opinions of sponsors, the Exchange has decided Your company has suspended its listing.

Your company and the sponsor shall make an announcement in accordance with the regulations, explaining the relevant circumstances of major issues and your company’s suspension of listing. The firm will maintain communication with your company and sponsors.

Alibaba shares are down almost 5% in the pre-market on the news…

When Jillian Ostrewich showed up to vote in the 2018 midterm elections, a pollworker denied her entry. At issue was Ostrewich’s shirt, a Houston firefighters tee with union insignia, which was deemed to violate a prohibition on wearing politicized regalia within 100 feet of a polling place. Rules against “electioneering” at the polls are typically understood to restrict signs, posters, and verbal attempts to sway voters, but Texas has laid out a more stringent approach—and running amok of electioneering law there can constitute a criminal offense.

If Ostrewich’s outfit choice sounds benign, that’s because it was. But one measure on the ballot, Proposition B, was an initiative dealing with firefighter pay. So the “election judge” at Ostrewich’s polling place ordered her to turn her shirt inside-out or go home; she felt violated but complied, went to the back of the line, and eventually cast her vote.

“On the merits, the electioneering statutes violate the Free Speech Clause of the First Amendment,” argues a suit by the nonprofit Pacific Legal Foundation (PLF). In making her case, Ostrewich’s attorneys invoke Minnesota Voters Alliance v. Mansky (2018), a Supreme Court precedent that struck down a similar law in Minnesota. The Texas statutes “are facially unconstitutional under [Minnesota Voters Alliance],” the suit says, “because they do not provide to the tens of thousands of election workers that enforce them any ‘objective, workable standards’ about ‘what may come in [and] what must stay out,’ resulting in ‘erratic application’ of the law.”

That erratic application was on full display in Ostrewich’s case: A county administrator specifically advised that her union shirt be exempt from any electioneering charges, though that guidance came the day after Ostrewich voted. The t-shirt “did not mention any candidate, measure, or political party, much less take a position,” writes PLF. Texas electioneering law also prohibits any clothing bearing a slogan or the name of a past candidate, including those not in Texas and those no longer living.

“I think one of the very troubling aspects of the Texas law is that election judges disagree on what is and what is not electioneering,” says Wen Fa, the lead attorney on Ostrewich’s suit. “Some judges see Black Lives Matter as electioneering. Others do not. Some people see Second Amendment t-shirts as electioneering. Others do not. Some see Tea Party t-shirts as electioneering. Others do not.”

One of the more open-and-shut cases came in 2016, when Brett Mauthe wore a “Make America Great Again” hat paired with a “Basket of Deplorables” shirt, both clearly indicating his support for presidential candidate Donald Trump. Mauthe agreed to remove the hat but refused to turn his shirt inside-out. He was arrested and eventually released on $500 bond, as if he was somehow a danger to the public.

That sort of crackdown is rare; enforcement is typically limited to arguments between clerks and voters. But then, arguments are one of the things the law is supposed to stop. “States are worried about other voters being offended that someone is supporting Trump, or supporting Biden, or supporting whichever other candidates, so they prevent voters from wearing them in the first place,” notes Fa. (Fa knows of no evidence that any voter-on-voter confrontations have stemmed from a t-shirt in Texas.)

“If you just ask a person on the street,” says Fa, “you would not really think of this as a criminal offense. People have the right to express themselves. They have the right to express their political opinions. And their right to free speech does not stop on election day.”

from Latest – Reason.com https://ift.tt/2HYDrf2

via IFTTT

Election Day: Futures, Oil Soar As Americans Hit The Polls Tyler Durden

Tue, 11/03/2020 – 07:53

US equity futures, global stocks and crude oil surged for a second day on Tuesday as a “gust of optimism” swept across global equity markets as millions of Americans headed to vote. The dollar tumbled amid rising bets on FX vol while yields rose.

Emini were up 39 points, or 1.2% to 3,340, up almost 120 points from Sunday night lows. PayPal dropped 4.8% after it forecast current-quarter profit below expectations. Shares of big U.S. banks including Bank of America Corp, Citigroup Inc, JPMorgan Chase & Co and Goldman Sachs Group Inc, which are sensitive to the economic outlook, gained between 1.4% and 2% in premarket trading, boosted by a steeper yield curve. The VIX retreated for a second day after touching a 20-week high last week on surging coronavirus cases globally.

“The election outcome will drive all markets over the next day or two,” Torsten Slok, chief economist at Apollo Global Management told Bloomberg. “How they move depends on the extent to which we have clarity about the results.”

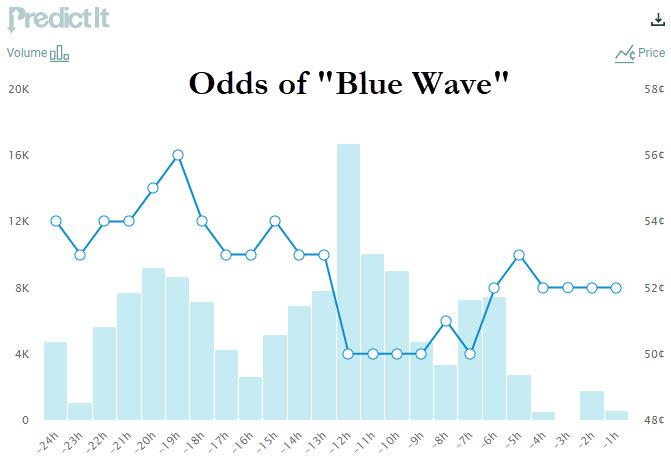

After slumping to five-week lows last week, the S&P 500, and to a lesser extent the Nasdaq, began November on a strong footing amid rising bets that a decisive blue sweep today could hopes of a bigger stimulus package after the election, even though the latest PredictIt odds for a Democratic Sweep (Biden + Dem Senate) remains just a fraction above a coin toss.

“Currently, the market is betting on a Biden win,” said Christian Stocker, UniCredit’s lead equity sector strategist. “Under a Biden presidency, the U.S. economy should be more supportive for equity markets – an economy with more stimulus programs will be perfect for the outperformance of cyclical sectors.” Of course, analysts unanimously predicted a market crash if Trump wins in 2016 and everyone knows what happened next: the S&P has surged about 55% since Trump clinched a “shock” victory in 2016 as lower tax rates under his administration boosted corporate profits. Much of that will be undone by a Biden admin.

At the same time, traders hedged prospects of post-vote volatility, pushing a measure of expected swings in China’s yuan to its highest level in more than nine years.

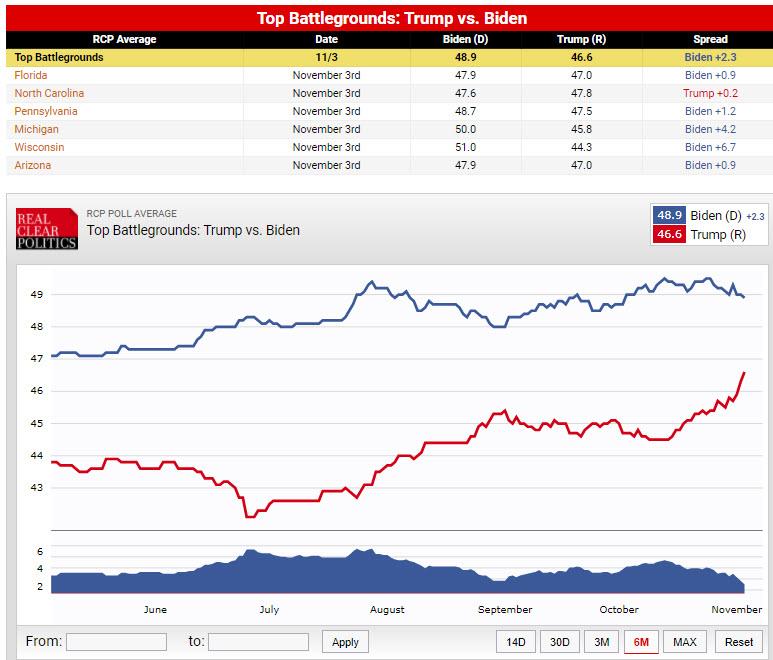

Still, the competition in swing states is seen as close enough that Republican President Donald Trump could still piece together the 270 Electoral College votes he needs to stay in the White House for another four years. In fact, the latest RCP battleground states tracker show that the spread between the two candidates is the closest it has been.

Investors are also bracing for wild market swings in case there is no immediate outcome on Tuesday night due to a protracted ballot count or a disputed result.

Then, once the U.S. election passes, investors will contend with the Federal Reserve delivering a policy decision Thursday before the October jobs report Friday.

Looking at global markets, European shares extended their recovery rally on Tuesday helped by the sliding dollar with investors putting coronavirus worries on the back burner for now, as attention turned to the U.S. presidential election. The pan-European STOXX 600 index rose 1.7%, bouncing off five-month lows hit last week on worries over new partial lockdowns across the continent. Growth-sensitive cyclical sectors such as oil and gas , miners, banks and automakers led the rally – all rising more than 2%.

Among individual stocks, French bank BNP Paribas gained 5.5% as a surge in currency and commodity trading helped it beat quarterly profit expectations. Fashion house Hugo Boss jumped 6.7% after it reported a return to profitability in the third quarter and said it was focused on driving a recovery of its business online and in China. Shares in German meal-kit delivery company HelloFresh , which has more than doubled in value this year due to strong demand on the back of the pandemic, fell 3.5% after quarterly results. Bayer slipped 1.0% as it took impairment charges of 9.25 billion euros ($10.79 billion) and warned of higher costs from its settlement over claims that its Roundup weedkiller causes cancer.

A Biden win is widely considered supportive for European equities on expectations of a bigger stimulus package and better trade ties with the United States: “It’s reflation trade for European stocks,” said Christian Stocker, UniCredit’s lead equity sector strategist. “Currently, the market is betting on a Biden win. Under a Biden presidency, the U.S. economy should be more supportive for equity markets – an economy with more stimulus programmes will be perfect for the outperformance of cyclical sectors.”

However, Stocker does not expect the gains to last long as coronavirus cases increase at an alarming rate in Europe, pushing major economies like Germany, France and the United Kingdom to reimpose tighter restrictions and causing economists to cut fourth-quarter economic growth expectations.

Earlier in the session, the MSCI Asia Pacific Ex-Japan Index added 1.4%. Japan’s markets were closed for a holiday. Asian stocks gained led by the materials and energy sectors, after climbing in the last session. Trading volume for MSCI Asia Pacific Index ex-Japan members was 13% above the monthly average for this time of the day. The Shanghai Composite Index rose 1.4%, driven by Kweichow Moutai and China Life.

Boosting reflation trades, oil held gains after jumping the most in three weeks on Monday on increasing signs OPEC+ will delay a planned easing of output cuts. WTI futures rose as much as 3.2% to $38/bbl in New York, and was trading 2.1% higher. Brent also gained as much as 2.9% to reach $40.10.

In FX, the Bloomberg Dollar Spot Index was set for its biggest decline in more than three weeks. The euro rose toward $1.17 and overnight volatility in euro-dollar surged to the highest level since March. Currency options traders are betting that the U.S. election outcome won’t be a game-changer for the euro, at least in terms of immediate market reactions. Commodity currencies led Group-of-10 gains, with the Norwegian krone advancing the most, as oil prices rose on broader risk-on sentiment and as OPEC+ inched closer to delaying a planned easing of output cuts. The Australian dollar bounced, after earlier falling against all G-10 peers after the Reserve Bank cut interest rates and expanded its quantitative easing program. The nation’s benchmark bond yields extended a decline.

In rates, the treasuries curve resumed bear-steepening as investors sought riskier assets with long-end yields cheaper by nearly 3bps. Large block sale in Ultra 10-year note futures during London morning further weighed. Yields were cheaper by 0.5bp to 3.5bp across the curve, steepening 2s10s, 5s30s by 2.5bp and 1.9bp; 10-year yields around 0.87% after topping at 0.879%, cheapest since June. Treasuries outperformed bunds and gilts by ~0.5bp and 1bp respectively.

Looking at the day ahead, though all eyes will be on the US election, there’ll also be data on US factory orders and durable goods for September and the ECB’s Knot will be speaking. Eaton Corp. and Sysco are among companies reporting earnings.

Market Snapshot

S&P 500 futures up 1.4% to 3,347.75

STOXX Europe 600 up 1.4% to 352.70

MXAP up 1% to 175.45

MXAPJ up 1.4% to 584.09

Nikkei up 1.4% to 23,295.48

Topix up 1.8% to 1,607.95

Hang Seng Index up 2% to 24,939.73

Shanghai Composite up 1.4% to 3,271.07

Sensex up 1.3% to 40,254.98

Australia S&P/ASX 200 up 1.9% to 6,066.36

Kospi up 1.9% to 2,343.31

German 10Y yield rose 2.4 bps to -0.616%

Euro up 0.5% to $1.1695

Italian 10Y yield fell 1.2 bps to 0.636%

Spanish 10Y yield rose 1.4 bps to 0.135%

Brent futures up 3.6% to $40.39/bbl

Gold spot up 0.2% to $1,898.56

U.S. Dollar Index down 0.5% to 93.66

Top Overnight News from Bloomberg

Twitter Inc. put a warning label on a post by Trump claiming that a Supreme Court decision allowing an extension for counting votes in Pennsylvania would lead to cheating and induce violence

Large parts of Europe are preparing for tougher measures to fight the pandemic: U.S. Prime Minster Boris Johnson said there is “no alternative” to imposing a coronavirus lockdown across England to stop the health service being overwhelmed, as he revealed plans for whole cities to be tested to root-out asymptomatic carriers of the disease

The Italian government is readying new relief funding of at least 1.5 billion euros ($1.8 billion) for businesses affected by a coming wave of new shutdowns to combat the spread of Covid-19, people familiar with the matter said

Starting Nov. 5, the Reserve Bank of Australia will begin purchasing Australian Government securities and securities issued by the state and territory central borrowing authorities in the secondary market under the A$100 billion bond purchase program

President Donald Trump’s and Democrat nominee Joe Biden’s campaigns claimed the inside track to victory on election eve, but girded their supporters to prepare for a photo finish in the hotly contested presidential contest

The virus continued its unrelenting surge across the U.S., with cases soaring in key battleground states ahead of the presidential election. France reported record daily cases as large parts of Europe prepare for tougher measures to fight the pandemic

Oil edged higher after jumping the most in three weeks on Monday on increasing signs OPEC+ will delay a planned easing of output cuts

Gold held an advance to trade near $1,900 an ounce ahead of Tuesday’s U.S. election as uncertainty boosted demand for the haven asset

The European Central Bank’s emergency bond purchases decelerated to the slowest pace on record last week, a sign that market demand for more stimulus is waning amid a rally in the region’s government debt

A quick look at global markets courtesy of NewsSquawk

Asian equity markets were higher across the board after following suit from the gains on Wall St where all major indices were lifted heading into the US election as polls continued to point to a Biden win and with stronger than expected global PMI data also adding to the constructive risk tone. ASX 200 (+1.9%) rallied throughout the session amid the RBA policy meeting where the central bank delivered a package of loosening measures including cutting key rates by 15bps as expected and a AUD 100bln boost to QE, with the broad upside led by the energy sector after oil prices rebounded on reports that Russia is considering postponing the tapering in OPEC+ cuts until the end of Q1. KOSPI (+1.9%) was also buoyed as participants shrugged off a negative inflation print and mixed vehicle sales data from South Korea’s top 2 automakers, while LG Display was among the notable gainers amid reports it is to supply mini-LEDs for Apple’s iPad. Hang Seng (+1.9%) and Shanghai Comp. (+1.4%) conformed to the upbeat risk tone after a mild liquidity injection by the PBoC and as all regional bourses joined the global rising tide, aside from Japanese markets which remained closed in observance of Culture Day.

Top Asian News

Malaysia Holds Key Rate at Record-Low as Virus Threatens Growth

Oil Giant Aramco Keeps Dividend Despite 45% Slump in Profit

Australia’s RBA Cuts Rates, Announces A$100 Billion Bond Buying

Thailand Approaches Former PMs to Head Reconciliation Panel

European cash equities trade with strong gains across the board (Euro Stoxx 50 +1.9%) after the region picked up the bullish APAC baton and as traders gear up for the US Presidential Election (full cheat sheet available in the Research Suite), with the latest betting odds from Betfair Exchange suggesting a rise in Trump’s re-election chances to 39% from 35%, whilst FiveThirtyEight overnight projected a Biden win at 89% vs. 10% for President Trump. Back to Europe, major bourses mostly experience broad-based gains with modest outperformance seen in the France’s CAC 40 (+2.1%) and Italy’s FTSE MIB (+2.2%) amid a firm performance in the banking sector – after BNP Paribas (+5.5%) posted a +30% YY increase in FICC revenues on the back of a “sharp rise in credit,” alongside a “rebound in forex and emerging markets and a good performance of rates.” As such, this has lifted the regional banking sector which resides as one of the top performers alongside the Basic Resources and Oil & Gas sectors, with the latter on account of rising oil prices. The other end of the spectrum sees some of the more defensive sectors including Health Care lagging on account of the overall risk-appetite, albeit Travel and Leisure continues to bear the brunt of the impact from nationwide lockdowns in Europe. In terms of individual movers, earnings see Pandora (+4%) and Hugo Boss (+4.8%) higher, with the latter also flagging “exceptionally strong” Chinese business in October. Looking at some M&A updates, Suez (+0.6%) failed to materially benefit from Veolia (+2.0%) confirming its intention to make a public takeover bid for Suez at EUR 18/shr. This came after Veolia announced around a month ago a 29.9% stake acquisition from Engie at the same price. Meanwhile, G4S (+4%) rejected the takeover proposal from Allied Universal.

Top European News

U.K. Boosts Testing as Johnson Seeks Lockdown Exit Strategy

Dutch Fall for Covid Conspiracies in Warning to Europe’s Leaders

Italy Is Said to Ready $1.8 Billion in New Aid as Shutdowns Loom

London Has to Shelve Cross-City Rail Line to Secure Tube Bailout

In FX, another bullish session in prospect for stocks, oil and other risk assets has enticed Buck bears back out of the woods, while the looming Presidential vote outcome is also keeping the Greenback on tenterhooks. Indeed, the DXY has faded just above 94.000 and ahead of Monday’s 94.285 peak to post a deeper low at 93.622 vs yesterday’s 93.871 base in the run up to relatively secondary US releases that fill the void before the primary issue is known or the vote proves too close to declare and is contested.

AUD – The Aussie has reclaimed all and more of its knee-jerk post-RBA losses even though dovish expectations were exceeded by the Central Bank cutting the benchmark rate, 3 year yield target and TFF by 15 bp to 0.1%, while lowering the rate for Exchange Settlements to zero and unveiling a new Aud 100 bn QE remit for an initial 6 months and aimed at 5-10 year bonds. However, Aud/Usd has spiked from the low 0.7000 zone all the up to and just beyond 0.7100, while the Aud/Nzd cross has staged a firmer rebound from closer to 1.0600 towards 1.0675 as the Kiwi lags ahead of 0.6700 vs its US counterpart in advance of NZ labour data.

CAD/GBP/EUR/CHF – Also forging gains largely at the expense of their US rival, but the Loonie also deriving more momentum from the ongoing recovery in oil as it probes through 1.3150 before Canadian trade on Wednesday. Meanwhile, Sterling is within striking distance of 1.3000 again and retesting 0.9000 offers/resistance against the Euro amidst unconfirmed reports that EU officials may have made a key concession to the UK on zonal attachment methodology in respect of fishing rights. Nevertheless, the single currency is equally close to 1.1700 vs the Dollar having breached the 100 DMA at 1.1661 and the Franc has pared declines from sub-0.9200 to 0.9160+ following in line Swiss CPI readings.

JPY – The G10 underperformer, albeit without local sponsorship as Japanese markets celebrate Culture Day, as the Yen fails to sustain gains above 104.50 due to the aforementioned pick-up in risk appetite on the second day of November.

In commodities, WTI and Brent front month futures continue their upward trajectory in early EU hours following an overnight session of consolidation, with prices underpinned by sentiment and feeling a second wind from Russia’s comments yesterday which suggested the largest non-OPEC producer is actively discussing rolling over current output curbs through Q1 2021 as opposed to a wind-down from January. In terms of upcoming meetings, the JTC and JMMC are set to meet on Nov 16/17th – with source reports/leaks likely heading into and during the events, followed by the decision-making OPEC/OPEC+ meetings on Nov 30th/Dec 1st. Over in the Gulf of Mexico, operations are resuming following the passing of Hurricane Zeta, with BSEE’s latest estimate suggesting 28% (Prev. 46%) of oil and 16% (Prev. 20%) of natgas production still shut in. Price action in the crude complex will likely be dictated by overall market sentiment heading into election, barring any OPEC-specific headlines and the weekly Private Inventory report. WTI Dec and Brent Jan hover off session highs around 38/bbl (vs. low USD 36.57/bbl) and USD 40/bbl (vs. low 38.65/bbl) respectively. Elsewhere spot gold and spot silver benefit from the Dollar’s decline despite the earlier positive correlation, with the yellow metal retesting USD 1900/oz to the upside at the time of writing, whilst spot silver regained a footing above USD 24/oz. Finally, LME copper trades firmer as the red metal coattails on risk appetite and benefits from the softer Dollar.

US Event Calendar

10am: Factory Orders, est. 1.0%, prior 0.7%; Factory Orders Ex Trans, est. 0.55%, prior 0.7%

10am: Durable Goods Orders, est. 1.9%, prior 1.9%; Durables Ex Transportation, est. 0.8%, prior 0.8%

10am: Cap Goods Orders Nondef Ex Air, est. 1.0%, prior 1.0%; Cap Goods Ship Nondef Ex Air, prior 0.3%

Wards Total Vehicle Sales, est. 16.5m, prior 16.3m

DB’s Jim Reid concludes the overnight wrap

US Election Day is finally here. It comes 9 months after the first primaries were held back in February, and caps off an astonishing campaign that has witnessed the arrival and spread of Covid-19, the end of the longest-ever economic expansion, racial unrest throughout the country, and the installation of a new Supreme Court Justice in near record time. And as well as the all-important presidential race, congressional elections for both the House of Representatives and the Senate are also taking place today that will have a major impact on the ability of the new president to enact their agenda.

To give you the context heading into tonight, the final polling averages place former Vice President Biden clearly ahead of President Trump, with an +8.4pt lead in FiveThirtyEight’s average, and a +6.7pt lead in RealClearPolitics’ one. And for reference, that’s noticeably larger than the lead Hillary Clinton had in polling averages back in 2016 (around +3pts). Nevertheless, the US President is determined not by the national popular vote, but by the Electoral College, and it’s true to say that matters are somewhat tighter there than the national polling would imply, since Mr. Biden’s lead in the likely tipping-point state of Pennsylvania is just +4.5pts and +2.6pts in the two averages.

In terms of timings, the first polls will close in parts of Indiana and Kentucky at 11:30pm London time, but given neither of these are battleground states, the real action will begin at midnight when polls close in Georgia as well as parts of Florida. Then at half past midnight, we’ll begin to get results from the other swing states of Ohio and North Carolina, before 01:00 sees polls close in Pennsylvania along with the rest of Florida. If Mr. Biden were to take any of Florida, Ohio or North Carolina it would likely be game-over for President Trump, as all 3 states are critical to Mr. Trump’s map in a way they simply aren’t for Mr. Biden. Florida is also a must-watch as mail-in votes there must be received by Election Day, so all the early ballots cast are expected to be tabulated by 01:30, meaning that we could have a winner declared by 05:00 tomorrow morning in what is a critical state for the president.

However, if Mr. Trump is ahead in those three states (FL, OH, NC) or running competitively, attention will likely turn to the Midwestern states and Pennsylvania, as he’ll need some further wins here in order to reach the winning line of 270 electoral votes. But in Pennsylvania, two counties that account for 117k requested mail-in ballots have already said they won’t begin to count those ballots until tomorrow, so if it does come down to the result there, it could be some days before we know the final outcome. So whether we’ll be able to bring you the results in tomorrow’s EMR will all depend on how close the election is. In the last 3 elections, we either had the result by morning or the writing was very clearly on the wall as to which candidate would emerge victorious. If it’s a repeat of 2000, however, it could be over a month before we actually know who the next president is.

From a market perspective, it’s important to remember that it’s not just the presidential result that matters, but also who controls both houses of Congress, as that will affect the ability of the new president to pass legislation, not least on whether we’ll get a major stimulus package in Q1 of next year. While the House of Representatives is seen as an incredibly likely win for the Democrats (97% in the FiveThirtyEight Model), their chances in the Senate stand at a noticeably lower 74%, so there remains the possibility that we could get a Republican Senate alongside a Biden White House. Indeed, our US economists view that as the most negative outcome for growth next year, because Republican senators would likely remain resistant to a big fiscal package, as they’ve already done in recent weeks even with Mr. Trump in the White House. This contrasts with their view on a Democratic sweep of the presidency and both houses of Congress, which they see as providing the most fiscal stimulus to the economy next year. So it’s clear that control of the Senate will be critical to the policy mix we can expect to see in 2021.

Currently the Senate is split 53-47 to the Republicans, and in the event of a 50-50 tie, the Vice President casts the deciding vote. So that means to win control of the chamber, the Democrats would need to take a further 3 seats if Mr. Biden wins the presidency, and 4 seats if President Trump is re-elected. With Democrats likely to lose a seat in Alabama, the five key races to watch for Senate control will be in Arizona, Colorado, Iowa, Maine and North Carolina. It’s also worth noting that in Georgia, one of the races is a special election in which numerous candidates are running from both parties (no primary election took place) and none are expected to get the 50% + 1 votes needed to avoid a runoff under Georgia rules. The other Senate race in the state is also very close, with a chance of a third-party candidate keeping the winner under 50%, triggering a runoff as well. Those runoffs wouldn’t take place until January 5, so in the event that control of the Senate were not clear, then majority control could come down to runoff elections in a single state in January.

In the graph in the body of today’s EMR we show the three-day intra-day move of 10-year treasuries and the US dollar between election day and the day after the results came through. Interestingly between polls closing and 13:00 the day following the election, 10-year US treasuries sold off nearly 40bps as the market fear over a Trump victory turned exceptionally quickly to one of reflation. 10 days after the election they were +64bps higher than the intra-day Asian market lows on election night. That we haven’t actually got inflation is an interesting postscript but could this election be the tipping point to genuine MMT? The point of the graph is to indicate that big moves can happen around such events. Although we don’t have the Asian session data from 4-years ago, S&P futures fell -5% overnight on election night in the initial response to Mr. Trump’s victory, causing circuit breakers to pause trading, before sharply rallying to finish the day +6.1% higher than these lows.

Ahead of this critical election for markets, global equity indices rebounded yesterday as they recovered from last week’s sell-off, and by the close the S&P 500 had risen +1.23% as part of a broad-based rally that saw nearly 90% of the index move higher. Tech struggled to keep pace with the NASDAQ moving between gains and losses before finishing up +0.42%. Volatility remained elevated, however, amidst the uncertainty over both the election and Covid-19, and the VIX index fell just -0.9pts to 37.1pts, which is still above its closing levels throughout the entirety of Q3. Over in Europe meanwhile, indices saw even larger advances, and the Stoxx 600 (+1.61%), the DAX (+2.01%) and the CAC 40 (+2.11%) all performed strongly.

The strong performance extended across multiple asset classes, with sovereign bonds rallying on both sides of the Atlantic. Yields on 10yr Treasuries fell -3.0bps to 0.843%, while those on bunds (-1.3bps), OATs (-1.1bps) and gilts (-4.3bps) similarly declined. For bund yields, that decline took them to their lowest level since March, and over in southern Europe, yields on Spanish debt also fell -1.4bps to a 1-year low.

Asian markets have tracked Wall Street’s lead this morning with the Hang Seng (+2.08%), Shanghai Comp (+1.13%), Kospi (+1.45%) and ASX (+1.93%) all up. S&P 500 futures are also up +0.42% ahead of the election. Japanese markets are closed for a holiday. In Fx, the Australian dollar is down -0.21% as the RBA reduced the cash rate by 15bps to 0.10% and said that it planned to buy AUD 100bn of 5y-10y bonds over the next 6 months. More than expected.

Though the coronavirus is likely to be somewhat lower down the headlines over the next couple of days, further restrictions were imposed in Europe yesterday as Italy announced a new three-tiered system in order to avoid another national lockdown. Shopping malls will close during weekends across the country, while secondary schools will be shut and Museums will close nationally. Other than these measures, Prime Minister Conte is resisting a full national lockdown. In the U.K. it was announced late last night that the city of Liverpool will be the first to have mass rapid testing on the population with the hope that this can be rolled out nationally in the weeks ahead. On the eve of the election in the US, Massachusetts Governor Baker has instituted new restrictions in his state. Residents are to stay home between 10 p.m. and 5 a.m. except for essential activities, and many businesses will therefore shut at 9:30 pm and indoor gatherings at private residences are limited to 10 people. This comes as multiple states in the Midwest announced positivity rates in the double digits and hospitalisations in Houston, Texas are back at August levels. Click on ‘view report’ above to see the usual COVID-19 tables at the end of the PDF.

The main data highlight yesterday were the release of the October manufacturing PMIs from around the world. The ISM manufacturing reading in the US surpassed expectations to reach a 2-year high of 59.3 (vs. 56.0 expected), and the employment index also rose to 53.2, its highest since June 2019. Over in Europe the final manufacturing PMIs saw some slight upward revisions from the flash prints, with the Euro Area reading at 54.8 (vs. flash 54.4), and the German PMI at 58.2 (vs. flash 58). The problem is that this is backward looking now and also reflects a manufacturing sector less lockdown than services (80-90% of most western economies) are now starting to be.

To the day ahead now, and though all eyes will be on the US election, there’ll also be data on US factory orders for September and the ECB’s Knot will be speaking. Good luck resting ahead of a big night ahead.

via ZeroHedge News https://ift.tt/2GmtBCW Tyler Durden

Much of the world is holding its breath, waiting for the outcome of tomorrow’s US election. And even though I see politics as the sad relic of the Bronze Age, this election may have some serious consequences, and so I think it’s worth a few brief comments.

My first concern is simply that all my readers stay safe. In all likelihood there will be violence following this one.

If Mr. Trump wins, the street troops of the left will do what they’ve been doing this year, and perhaps more so. They are, after all, facing a dead end. If their perennial strongholds (NY, NJ, IL, CA and others) aren’t massively bailed out, and fast, their political machines will collapse.

I don’t expect very much violence immediately following a Biden win. Granted, there could be some (there are always a few actual crazies around, and I do tend to be optimistic), but I’ve never known disappointed conservatives to riot, and the militia guys tend to head to a sheriff’s department, seeking to be deputized. The threat of violence from the right would be if the Blues are seen to steal the election. If that happens clearly enough, all bets are off.

(My preference, of course, would be for good people to drop out of the status quo, and to use their energies building something better and less corruptible.)

All that said, caution is warranted.

The People Who Really Matter

Now, with that note behind us, I’d like you to remember that the people who have the ultimate say in what happens in the world are the productives… the people who build, grow, repair and invent everything. The political class merely takes what they produce, lives high off of it, and plays at being powerful with it.

The producers of the world have been frightened, seduced, deceived and bullied into compliance with the political class, but it needn’t be that way and if fact will not always be that way. Furthermore, these organizations aren’t nearly as omnipotent as people believe. The current propaganda stream, interestingly enough, features the elites of the European Union bandying about plans for a Great Reset and a Fourth Industrial Revolution.

By doing this, they are admitting that their existing system will not last. Otherwise they wouldn’t need to sell people on something new.

Whatever comes out of this election, our goal is to make the producers of the world understand that they don’t need the political class. We can arrange our own affairs just fine without their glorious wisdom (cough, cough). We can also toughen up emotionally and cease being terrified by every imaginary fear that comes down the road.

What To Remember

That’s really about all I have to say today. I’ll conclude with a quote from Buckminster Fuller. Please try to keep this passage in mind as the breathless election results come in, followed by highly-emotional commentary. This is how things really are:

If you take all the machinery in the world and dump it in the ocean, within months more than half of all humanity will die and within another six months they’d almost all be gone; if you took all the politicians in the world, put them in a rocket, and sent them to the moon, everyone would get along fine.

Stay safe and remember that politics is all about subverting you emotionally and then reaping your production. The rest are details.

via ZeroHedge News https://ift.tt/3jU8rK0 Tyler Durden

“At Least 1” Terrorist On The Run, 1 Dead After Vienna Attack That Killed 4 Tyler Durden

Tue, 11/03/2020 – 07:09

Now that the dust has cleared, police in Vienna have finally had some time to piece together more details from Monday’s brutal attack in the Central European city. Vienna is a European cultural powerhouse, but it has seen far fewer terror attacks over the last 20 years than many of its neighbors. But on Monday night, a gang of assailants struck at six areas in downtown Vienna, attacking pedestrians and police.

Overnight, the number killed in the attack swelled to 5, 4 victims, and 1 assailant, while 17 others were wounded in the shooting, The dead attacker was identified as a 20-year-old Austrian-North Macedonian dual national who had one prior terror conviction. Interior Minister Karl Nehammer confirmed that the prior conviction was for membership in a terrorist organization. The attacker who was killed, whose name was Kujtim Fejzulai, was sentenced to 22 months in prison in April 2019 because he had tried to travel to Syria to join the Islamic State, though he was granted early release under juvenile law.

At least one other attacker is believed to be on the run, Nehammer said. The terrorist who was shot in killed was wearing what authorities initially believed to be an explosive vest, though it “turned out to be a dummy”.

His apartment was raided in the night, authorities said. Though there were reports on Monday about a gang of attackers striking at six separate locations, it’s currently unclear exactly how many participated in last night’s attack. The FT and AP reported that it isn’t clear whether Fejzulai, a known ISIS member, was acting alone.

The victims included two men and two women. 7 others are in life-threatening condition from gunshot wounds and cuts. During comments made early Tuesday morning in Vienna, Chancellor Sebastian Kurz affirmed that the incident was “clearly an Islamic terror attack.”

“It was an attack out of hatred for our fundamental values, hatred for our way of life, hatred for our democracy in which all people have equal rights and dignity.”

Authorities still couldn’t say whether more attackers might be on the run. Workers were asked to stay home if possible on Tuesday, and children were dismissed from school until further notice. The city’s public transit was closed.

Some 1,000 officers were on duty to help with the investigation while the army was brought in to guard soft targets across the city.

The shooting started at around 2000 local time as people headed downtown to enjoy one last drink before new coronavirus lockdown measures came into effect. The assailant who was killed was shot at around 2010, according to Vienna police chief Gerhard Puerstl.

Kurz’s government ordered three days of official mourning, with flags to be flown at half-mast. A minute of silence was held at noon on Tuesday.

Thousands of videos purporting to show the incident were uploaded to social media last night, authorities said, including the video below, purporting to show the moment a terrorist was captured.

The attack comes as France has been hit particularly hard, with at least two incidents where victims were ‘decapitated’ by attackers armed with knives last month. President Emmanuel Macron publicly defended the right for secularists to publish cartoons featuring the prophet Mohammad. Several Muslim world leaders have attacked Macron for his defense of the Charlie Hebdo cartoons. A class on freedom of expression featuring the cartoons allegedly motivated a young Islamic extremist to murder French teacher Samuel Paty.

Leaders from around the world offered their condolences to Austria, and condemned all violence tied to radical Islamist extremists.

via ZeroHedge News https://ift.tt/3elCB80 Tyler Durden

Lady Gaga Slammed On Social Media After Mocking Swing State Voters As Rednecks Tyler Durden

Tue, 11/03/2020 – 06:45

Singer Lady Gaga has come under fire from working class Americans across the country after a video she posted to Twitter shows her not only endorsing Joe Biden, but apparently mocking rednecks in swing states while doing so.

This weekend the singer posted a video of herself opening a can of beer, dressed in camo, while standing next to a large pickup truck and preaching about who she voted for.

“Hey, this is Lady Gaga. I’m voting for America, which means I’m voting for Joe Biden,” she opens the video by saying. “And if you live in Minnesota, Pennsylvania, Georgia, Michigan, Florida, or Arizona, I encourage you to vote,” she continues, in an obvious attempt to drum up support in swing states.

“Cheers to the 2020 election,” she says after taking a drink from her beer and then slamming the can on the ground.

The video, which was supposedly trying to make some kind of statement (though we don’t know what) was widely slammed by swing state voters on social media.

One woman responded: “I don’t own a truck, never worn camo or drank a beer so if this is your idea of #TrumpSupporters you’re dead wrong; we’re college educated, hard working people who love our country but nice try GaGa.”

Another voter from South Carolina and highlighted by The Daily Mail said: “Stunts like this, are exactly why Trump is going to win. Average, hardworking Americans are sick of ‘celebrities’ mocking them for what they wear, drive, eat, drink, and where they choose to work or live.”

“This is one of the most tone-deaf things I’ve seen this whole election cycle. You’ve just produced an ad for Trump’s re-relection,” said a third voter.

Amber Athey from Arlington, Virginia lambasted the singer: “Real rednecks wouldn’t have wasted that perfectly good beer, Gaga. I speak from experience.”

Another social media user called the video “cringe AF”, stating: “Love ya Gaga but this Vid is Cringe AF. It feels insincere & literally makes me not want to vote at all. I honestly wish you never got involved in politics publicly because it’s distracting from the Power of your Musical & Performing Talents. Politics is a Dirty Game Sis.”

Trump’s campaign communications director Tim Murtaugh also lashed out at the singer, who Tweeted a photo of herself in Pennsylvania on Sunday in response: “Nothing exposes Joe Biden’s disdain for the forgotten working men and women of Pennsylvania like campaigning with ant-fracking activist Lady Gaga.”

He continued: “This desperate effort to drum up enthusiasm for his lackluster candidacy is actually a sharp stick in the eye for 600,000 Pennsylvanians who work in the fracking industry.”

Wouldn’t it be something if Gaga’s video had the opposite of its intended effect in swing states? We’ll know tomorrow exactly how effective it was.

via ZeroHedge News https://ift.tt/3oRFgLn Tyler Durden

Our interview this week is a deep dive into the mess created by the EU Court of Justice in Schrems II – and some pretty good ideas for how companies might avoid the mess, courtesy of a U.S. Government white paper. I interview Brad Wiegmann, Senior Counselor for the National Security Division at the US Department of Justice about the white paper. We cover a host of arguments and new facts that may help companies navigate the wreckage of Privacy Shield and preserve the standard corporate clauses they’ve relied on for transAtlantic data transfers. And, yes, the phrase “hypocritical European imperialism” does cross my lips.

In the news, we can’t let election eve pass without a look at all the election security threats and countermeasures now being deployed. I argue that the election security threat is the second coming of Y2K – a threat that is almost certainly an overhyped bogeyman, but one we can’t afford to ignore. Jamil Jaffer and Pete Jeydel push back. Silicon Valley’s effort to ensure that no one questions the legitimacy of a Biden victory also comes in for some criticism on my end – and is defended by Nate Jones. My nomination for Flakiest Silicon Valley Election Security Techno-nostrum is the banning of post-election political ads. That just guarantees that speech about the election will default to the biggest “organic” voices on the internet and to the speech police at each platform. Or was that the intent?

Confused about all the TikTok and WeChat litigation? It’s pretty simple, really: the US hasn’t won a single case, and it’s gone down hard in three separate opinions, the latest by US District Judge Beetlestone of Philadelphia. This could be Trump Derangement at work, but the fact is that the Chinese platforms have a plausible argument that Congress prohibited the use of IEEPA to “indirectly regulate” distribution of speech. Banning a social platform might seem to fit within that prohibition, but the result is crazy: it implies that TikTok could replay all the Russian election interference memes from 2016, and the government would be helpless to stop it. On appeal, we may see the courts taking a broader view of the equities. Or they may be tempted to say, “Well, Congress screwed this up, let Congress unscrew it.”

Nate and I try to sum up what we learned from the social media speech suppression hearing on the Hill. Nate sees no common ground emerging despite wide unhappiness with Silicon Valley’s role in regulating speech. I am more optimistic that a Congress looking to make progress could agree on first steps toward transparency practices on the platforms. The companies themselves seem to have decided that this is table stakes as they strive to avoid worse.

Nate gives us a quick view of the platform speech debate in Europe. My summary: Silicon Valley is already incentivized by EU law to oversuppress; now they’re asking for immunity when they oversuppress, which means, of course, even more suppression.

You can subscribe to The Cyberlaw Podcast using iTunes, Google Play, Spotify, Pocket Casts, or our RSS feed. As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect the opinions of their institutions, clients, friends, families, or pets.

from Latest – Reason.com https://ift.tt/3mOZ8Nv

via IFTTT