Submitted by David Stockman via Contra Corner blog,

The Fed’s public relations firm of Hilsenrath & Blackstone was out this morning with the official line on the market’s tremors of recent days. It seems that $10 trillion in freshly minted digital money at the world’s major central banks over the last eight years—-that is, a tripling of their balance sheets to $16 trillion—- is not enough. Not only is 2% inflation still MIA, but it now threatening to enter the dark side:

Behind the spate of market turmoil lurks a worry that top policy makers thought they had beaten back a few years ago: the specter of deflation.

Never mind that there is nothing close to a sustained run of negative consumer price indices anywhere in the world. The recent modest abatement of what has been 45 years of relentless consumer price inflation throughout the DM economies can be readily explained by short-term oil and commodity price movements and exchange rate fluctuations. Indeed, the money printers are always gumming about inflation-ex food and energy— so here it is.

During the most recent twelve months, the CPI-ex food and energy is up 1.7%, and that compares to 1.8% in the prior year and 1.9% in each of the two years before that. Indeed, since the turn of the century the CPI less food and energy has risen by an average of 1.9% annually. So now that it has tumbled all the way down to 1.7%——a fractional emission of pure statistical noise from the government data machine—-we are suddenly drifting into a deflationary crisis?

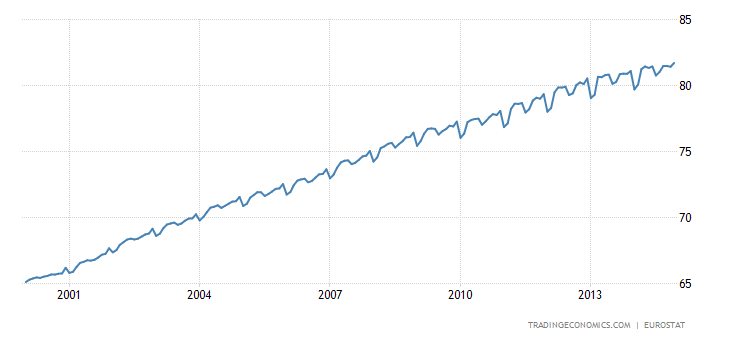

And, no, the data is no different for Europe. There is no sudden lurch into a sustained downward price spiral. Instead, European consumers are enjoying a period of only marginal erosion of their purchasing power. Thus ,during the most recent twelve months, core inflation in the euro area has risen by 0.7% and that is virtually the same rate as the prior year. Going back to the pre-crisis peak in September 2007, the average core inflation rate has been 1.1% for seven years running. Again, there is no step-wide plunge in the consumer inflation trend—-just a reasonable approximation of price stability.

Self-evidently, the current brief interval of inflation slowdown has happened before. So what has occurred during recent months cannot be described as some deeply embedded structural condition that changes the whole course of economic life.

In fact, what possible explanation do the Keynesian money printers have for what they imply to be an economic disease that could be called SODS (sudden onset deflation syndrome). That notion is empirically false as shown above, but by their lights where did it come from all of a sudden? The overwhelming driving force in financial markets and worldwide economies during the past few years has been the ultra-stimulative, “unconventional” monetary policies. No one disputes that—especially the fast money traders who rightly insist that its always and everywhere about the Fed.

Certainly, the monetary politburo in the Eccles Building would never agree that ZIRP and QE are responsible for deflation. So, it must be some kind of horror show dead hand from the grave—-a relapse of the financial crisis contagion. But of course they never explained where that came from, either.

Well, they did say that central bank policy had nothing to do with it. Not even Greenspan’s desperate slashing of money market rates to an unprecedented 1% in the spring of 2003 had anything to do with the explosion of variable rate mortgages and the “refi” stampede. The latter resulted in gross mortgage originations at a $5 trillion annual rate compared to historic originations in the $1 trillion range, and provided the catalyst for the housing price explosion and mortgage equity withdrawal (MEW) based consumption boom which followed.

Nope, it was all greed and animal spirits getting too frisky. Why that keeps happening after periods of extreme central bank stimulus and Wall Street coddling, they don’t say. Likewise, now we have “deflation” suddenly welling up among the masses on main street. The latter are held to be reluctant to spend, thereby causing inflation to weaken and the spending impulse to consequently falter even more.

This outbreak also remains unexplained, but the cure is the same: More monetary accommodation which means that ZIRP and N-ZIRP (“near ZIRP” or trivial increases in the target rate after ZIRP is officially lapsed) must be extended as far as the eye can see.

All of this is empirical nonsense, of course. In fact, its a blatant con game. The only reason that there is an appearance of a troublesome “inflation shortfall” is that recent rates have been below the arbitrary 2% “policy” target that has been set by Keynesian central bankers all around the world.

Moreover, when this 2% target is taken with such literalistic rigor as to rival creationist doctrine regarding the scriptures, it can make trivial differences appear profound; and to cry out for new forms of policy action—which is what the monetary central planners are actually all about.

In fact, there is no proof anywhere that 2% inflation on the CPI enables extra GDP growth. It’s just a flat-out invention of the monetary scholastics who have seized control of the world’s financial system.

The truth is, the 50% gap between 2% and 1% inflation is a distinction without a meaningful difference. Indeed, there is no difference at all when it comes to the fundamentals of true economic growth and wealth creation—-except that higher inflation is always slightly worse. Yet due to the unquestioned status of the 2% inflation target, the central banks are getting a free pass in the public debate.

In fact, it is worse than that. They are being postured by their public relations firms in the financial press as fireman at the ready to remedy the very problems they have previously created. Thus, Hilsenrath & Blackstone note,

….fresh signs of slow global economic growth, falling commodities prices, sagging stock markets and declining bond yields…… suggest the deflation risk hasn’t gone away…

Com’on. The welcome decline in oil prices and other commodities that is currently helping to ease the inflation indices is not anything bad that needs to be combatted. It represents an overdue cooling of the 14-year global commodity boom that the combined central banks of the world have stimulated through their massive support for artificial economic growth fueled by cheap credit; and by the free money induced transformation of commodities into still another speculative asset class.

Here is the major commodity index. Since 2000 it has risen at a 8% annual rate—-a trend that could never be sustained under a regime of sound money and disciplined credit management. And now that the world economy has reached the maximum extent of the central bank enabled boom and has begun to falter, the Fed’s PR men are out flogging a new mission. That is, for the central banks to arrest the dangerous collapse of global commodity prices.

It puts you in mind of the boy who killed his parents and then threw himself on the mercy of the court because he was an orphan.

So here’s the real reason the nonsense of 2% inflation targeting and the specter of deflation is being fed to the compliant financial press by the policy apparatchiks running the central banks, IMF and the major nation treasury departments. In a word, governments have buried themselves in debt, and are desperate for an excuse to inflate away the real burden.

So they have invented the Big Lie of the present era. Namely, that the cause of low growth is “low-flation”. And the simplistic arithmetic behind this false proposition is a wonder to behold. In the case of the Euro-zone, for instance, real growth has been registering at less than 1% per year and with inflation in the same zone, nominal GDP is hardly growing at all.

Yet public debt continues to soar and there is no political will to stop it outside of Germany. Already the EC fiscal compact agreed to two years ago is being cast aside because it is inconvenient for the socialist politicians and opportunists who run France and Italy, in particular, but most of the balance of the EC as well.

So the financial policy elite has invented a “twofer”. Get inflation above 2% and, presto, growth will rebound to the 2-3% zone of Keynesian “potential GDP” growth. Soon enough, the public debt/GDP ratios will stop rising and all will be well.

Indeed, the data for Italy shows the real scam behind the deflation scare in spades. Its nominal GDP has been essentially flat for seven year running, yet is public debt has continued to rise inexorably. In a word, it is buried in a debt trap.

Moreover, Italy is only an advanced case of the universal condition in the DM economies. Stated differently, the specter of deflation is not about economic analysis or honest monetary policy options. Its just a cover story for an intended fraudulent default on public debt of monumental proportions.

The fly in the ointment, however, is that this inflationary default scheme can never work. Central banks have buried the world in massive malinvestment and unsustainable credit fueled growth that will eventually collapse. So a classic hyper-inflation will never break-out because there is too much capacity in the world economy to permit labor, commodity and industrial prices to explode.

At the end of the day, the central banks can’t levitate inflation, and they surely cannot cause production, enterprise and labor productivity on the supply side of the economy to accelerate by sloshing N-ZIRP liquidity through the money markets. The latter impossibility is already proven by the anemic recovery in the US and the triple dip now enveloping Europe.

In fact, bringing the monetary firemen in to douse with more kerosene the massive financial fires they have already started would only defer the day or reckoning–if even that. It would just mean that the financial casinos of the world would be given one more round of speculative juice, thereby inflating asset values to an even more dangerous extreme.

Some evidence for that proposition seems to be extant in the modest financial turbulence incepting even now.

via Zero Hedge http://ift.tt/1F7dMp2 Tyler Durden