This past weekend, we discussed the breakout of the markets to all-time highs.

The question I asked this past weekend was simply;

“The bull market is back, but can it stay?”

When I was growing up my father, probably much like yours, had pearls of wisdom that he would drop along the way. It wasn’t until much later in life that I learned that such knowledge did not come from books, but through experience. One of my favorite pieces of “wisdom” was:

“Exactly how many warnings do need before you figure out that something bad is about to happen?”

Of course, back then, he was mostly referring to warnings he issued for me “not” to do something I was determined to do. Generally, it involved something like jumping off the roof with a queen-sized bedsheet convinced it was a parachute.

My argument was always that “everyone else is doing it.”

After I had broken my wrist, I understood what he meant.

(What’s funny is that I am having the same conversations with my son today, and he is determined to figure out things the hard way simply because “everyone else is doing it.” Now, I truly understand what I put my Father through.)

Likewise, investors are currently rushing to get back into the market, after bailing out in December, with a near reckless disregard for the consequences.

Simply because “everyone else is doing it.”

So, before you go “jumping off the roof with a bed sheet for a parachute”, there are some warning signs to consider before taking that leap.

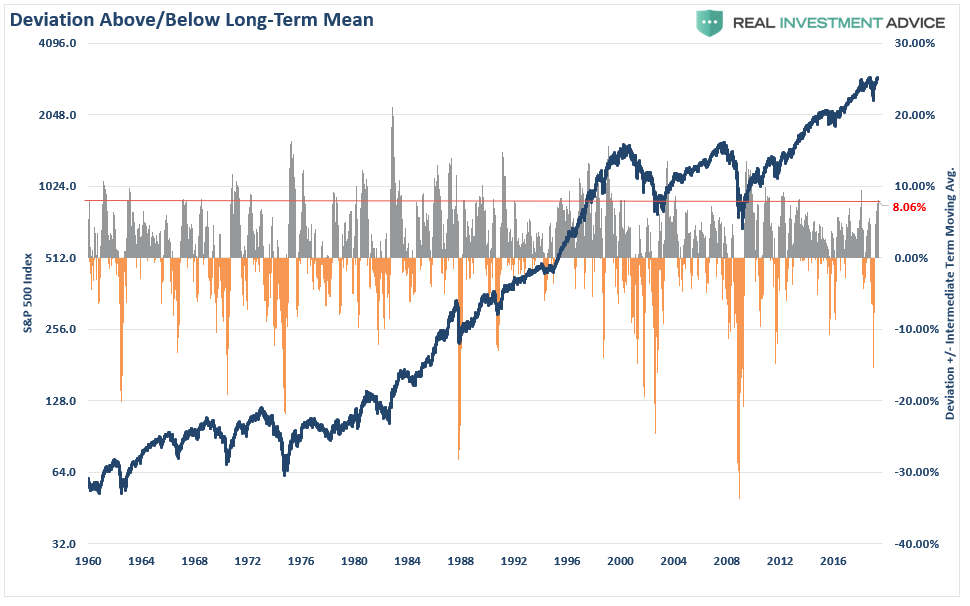

Warning 1: Deviations From The Mean

There is a funny story about a “defensive driving” class where the instructor asks the class how many thought they were “above average drivers.” About 80% of the class raised their hands. The funny thing is that all of them were in the class because of traffic violations or accidents. But more to the point, 80% of drivers cannot be above average. It is mathematically impossible.

Likewise, in investing, prices must be both above and below the “average price” over a set period of time for there to be an average. To many degrees “price” is bound by the laws of physics, the farther from the “average price” the current price becomes, the greater the pull back to, and generally beyond, the average. This is shown in the daily chart below.

Currently, the market is more than 8% above its longer-term daily average price. These more extreme deviations tend not to last an extraordinarily long time. Furthermore, reversions from these more extreme deviations tend to be rather quick.

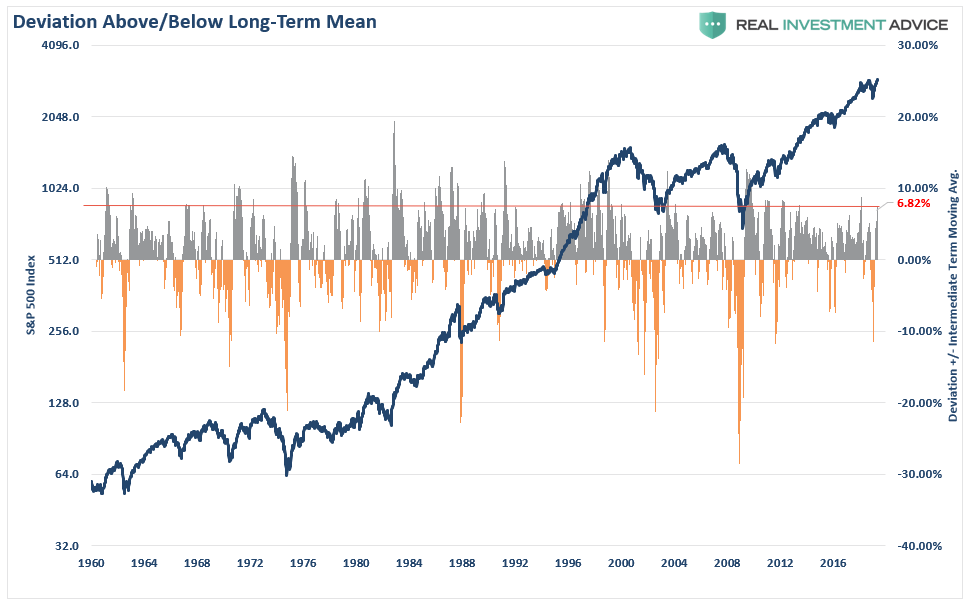

If we step out to a weekly basis, we see the same warning.

At almost 7% above the long-term weekly moving average, the market is currently pushing the upper end of historical deviations.

The important point to take away from this data is that “mean reverting” events are commonplace within the context of annual market movements.

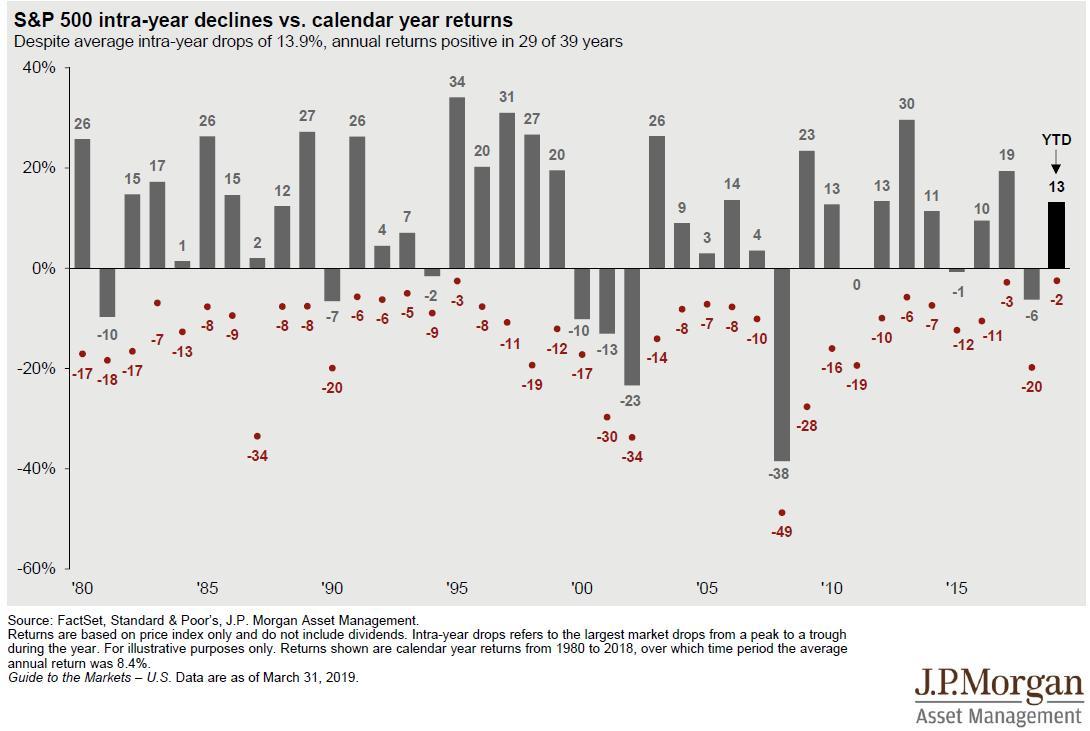

Currently, investors have become extremely complacent with the rally from the beginning of the year and are quick extrapolating current gains through the end of 2019.

As shown in the chart below this is a dangerous bet. In every given year there are drawdowns which have historically wiped out some, most, or all of the previous gains. While the market has ended the year, more often than not, the declines have often shaken out many an investor along the way.

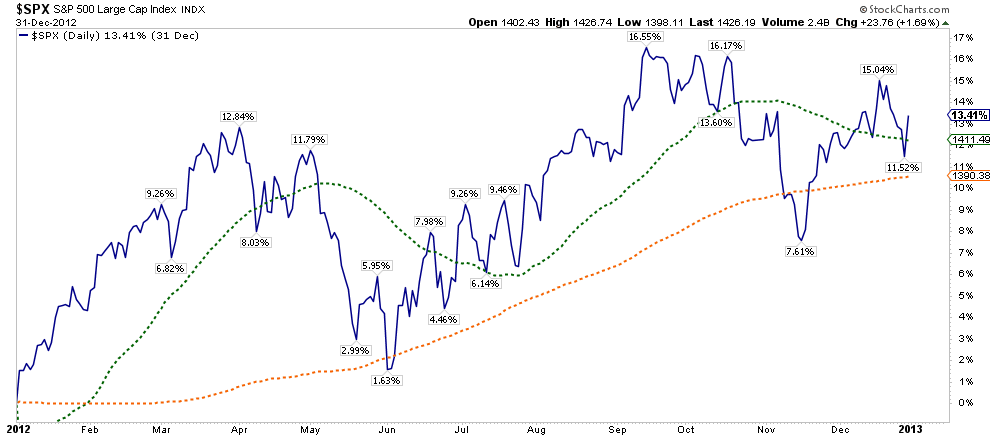

Let’s take a look at what happened the last time the market started out the year up 13% in 2012.

So far, it looks a whole lot like this year.

From a portfolio management standpoint, the reality is that markets are very extended currently and a decline over the next couple of months is highly likely. While, it is quite likely the year will end on a positive, particularly after last year’s loss, taking some profits now, rebalancing risks, and using the coming correction to add exposure as needed will yield a better result than chasing markets now.

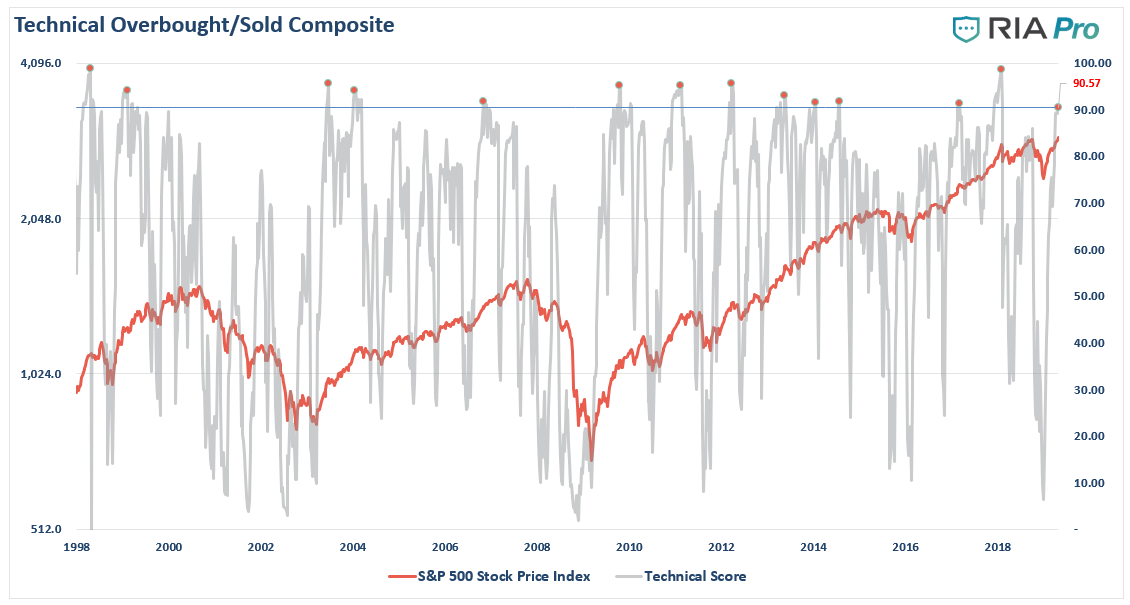

Warning 2 – Technical Warnings

The technical warnings also confirm our concerns about a near-term correction.

Each week, we post the chart below for our RIA PRO subscribers which is a composite index of our weekly technical measures including RSI, Williams %R, Stochastics, etc. Currently, the overbought condition of the market is near points which have denoted more significant corrections.

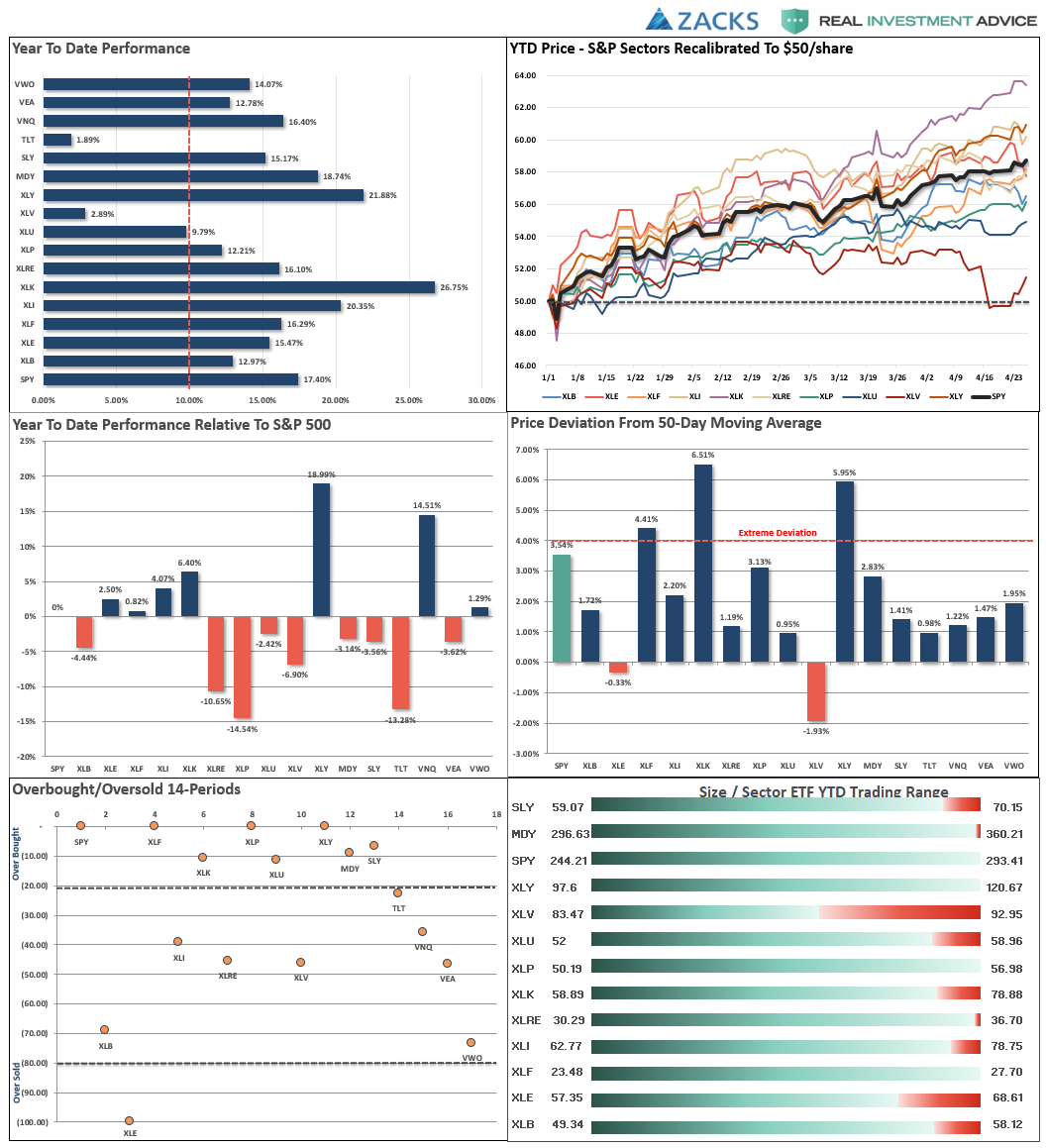

The market/sector analysis, which is also exclusive to RIA PRO members, shows the rather extreme price deviation in Technology, Discretionary, and Financials. Also, relative performance shows that it has primarily been Technology and Real Estate providing a bulk of the “alpha” year-to-date.

These are abnormalities that tend not to last long in isolation and rotations tend to occur rather quickly.

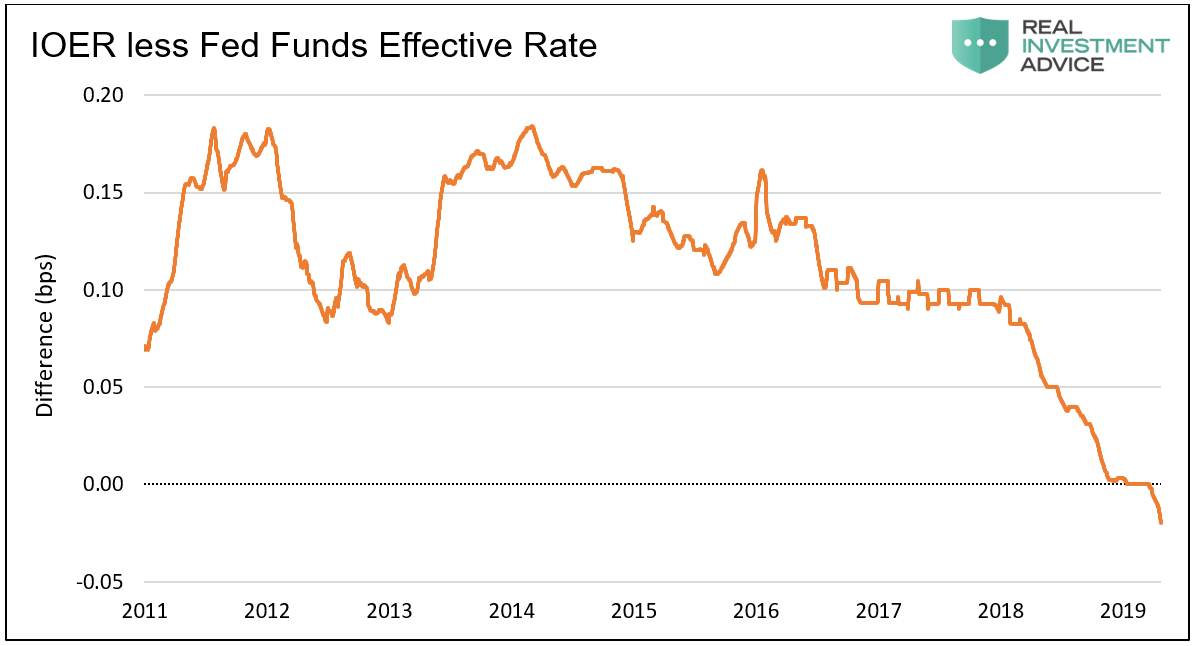

Warning 3 – Dollar Surge/Shortage

One of the lesser known issues with the markets currently was addressed by my co-portfolio manager, Michael Lebowitz, CFA:

When the Fed embarked on QE, they wanted to ensure that the money created to buy Treasuries and mortgages was being held by the banks as excess reserves and not being used to form loans. They also knew that controlling the Fed Funds rate would become problematic given the sharp increase in potential banking reserves. To help them keep the money on the sidelines and better control the Fed Funds rate, the Fed decided to pay banks interest on excess reserves (IOER). The IOER rate was set above the Fed Funds rate (the rate banks lend reserves to other banks on an overnight basis). The thought being that banks would rather collect a higher interest rate and take no risk than lend out money to other banks at a lower interest rate. On the flip side, if Fed Funds rose to the IOER rate, the banks would lend their reserves which should, in theory, provide a cap for Fed Funds.

The IOER premium over Fed Funds served its purpose in keeping excess reserves constant and in capping the Fed Funds rate from 2011 to 2017. However, as shown below, its effectiveness started eroding with the advent of QT in October of 2017

We believe the liquidity drain associated with QT created a shortage of dollars among foreign banks. Given this liquidity shortfall, foreign banks are likely being forced to pay higher interest rates for overnight funding. The Fed Funds rate is now higher than the IOER rate. That was not supposed to happen. Domestic banks either do not have the liquidity to lend or are being precautionary. Regardless of the reasons, a dollar shortage can become a dollar crisis if not addressed.

It is quite possible this situation will cause the Fed to stop QT before the scheduled September 30th end date. More importantly, it also raises the specter that QE, which injects liquidity into the banking system, is not as far off as we think. Watch the IOER/Fed Funds rate differential and the dollar for clues of further liquidity problems.

Warning 4 – Earnings

Lastly, as I discussed in this past weekend’s missive, earnings are not currently as “stellar” as the media makes them out to be. To wit:

“One of the reasons given for the push to new highs, and something we had previously said was highly probable, were the “better than expected” earnings reports coming in.

“Percentage of Companies Beating EPS Estimates (78%) is Above 5-Year Average

Overall, 15% of the companies in the S&P 500 have reported earnings to date for the first quarter. Of these companies, 78% have reported actual EPS above the mean EPS estimate, 5% have reported actual EPS equal to the mean EPS estimate, and 17% have reported actual EPS below the mean EPS estimate. The percentage of companies reporting EPS above the mean EPS estimate is above the 1-year (76%) average and above the 5-year (72%) average.”

Wow…that’s impressive and certainly would seem to be the reason behind surging asset prices.

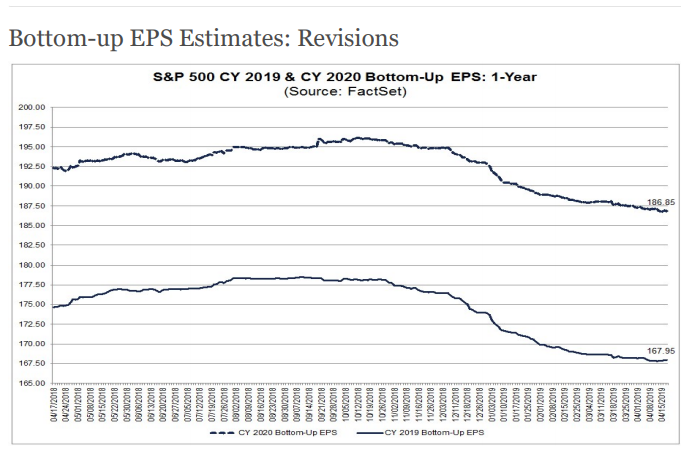

The problem is that “beat rate” was simply due to the consistent “lowering of the bar” as shown in the chart below:”

“As shown, beginning in mid-October last year, estimates for both 2019 and 2020 crashed.

This is why I call it ‘Millennial Soccer.’

Earnings season is now a “game” where scores aren’t kept, the media cheers, and everyone gets a “participation trophy” just for showing up.”

Importantly, the issue of buybacks continues to obscure the issue.

Not surprisingly, stock buybacks create an illusion of profitability.

Once that impact is removed the “soft underbelly” of actual earnings is fully exposed. The risk investors are taking is ultimately paying far too much for every dollar’s worth of earnings given that much of it is manufactured. While it may not matter now, it ultimately will matter.

If They Don’t “Buy & Hold” – Why Should You?

Here is the market for you year to date (via David Rosenberg):

Alphabet +23%

Microsoft +28%

Apple +30%

Amazon +30%

Facebook +46%

(Disclosure: We are long Apple and Microsoft in our equity portfolio.)

These “warning signs” are just that. None them suggest the markets, or the economy, are immediately plunging into the next recession-driven market reversion.

But as David noted:

“The equity market stopped being a leading indicator, or an economic barometer, a long time ago. Central banks looked after that. This entire cycle saw the weakest economic growth of all time couple the mother of all bull markets.”

There will be payback for that misalignment of funds.

Past experience suggests that future returns will be far less than historical averages suggest. Furthermore, there is a dramatic difference between investing for 30-years, and whatever time you personally have left to your financial goals.

While much of the mainstream media suggests that you “invest for the long-term” and “buy and hold” regardless of what the market brings, that is not what professional investors are doing.

The point here is simple. No professional, or successful investor, every bought and held for the long-term without regard, or respect, for the risks that are undertaken. If the professionals are looking at “risk,” and planning on how to protect their capital from losses when things go wrong, then why aren’t you?

via ZeroHedge News http://bit.ly/2GSoxDY Tyler Durden

With the market recently digesting Microsoft’s stronger than expected earnings, pushing its market cap north of $1 trillion and making it the most valuable company in the world for however long, while patiently awaiting today’s Apple earnings after the close, yesterday’s report by the third largest company, Google parent Alphabet, left a decidedly bitter aftertaste in investors’ mouths after it missed across the board while reporting a sharp slowdown in ad revenue growth.

Making matters worse, analysts were left puzzled over the reasons behind Alphabet’sfirst-quarter revenue miss: as Bloomberg explains, a particular source of confusion was product changes in advertising that the Google-parent said led to a slowdown in revenue growth.

A lack of answers on the earnings call led to “frustration” for investors, Jefferies analysts wrote in a note. One concern is whether other online businesses are taking advertising share away from Google, given that paid clicks on Google ads rose at the slowest pace since 2016. Alphabet’s shares are down 7.8% in pre-market trading on Tuesday. The stock had climbed 24% this year and closed on Monday at an all-time high before tumbling.

Courtesy of Bloomberg, here’s what what analysts were saying this morning about Alphabet’s results:

JEFFERIES (Brent Thill); buy rating on Alphabet with a PT of $1,450

1Q results raise “more questions than answers”, with continued lack of transparency “troubling” to investors

While valuation is undemanding, Alphabet will need to rebound in 2Q to show 1Q was not a trend

Otherwise investors may be resigned to the view that Alphabet is a lower growth story, potentially losing share, though Jefferies doesn’t believe that is the case

MORGAN STANLEY (Brian Nowak); overweight recommendation, though lowers PT to $1,425 from $1,500

1Q Websites deceleration and uncertain forward trajectory highlight need for better transparency; this will likely remain key to long-term valuation

Unclear what changes Alphabet made in the quarter that drove the deceleration in growth, and this is something the Street must figure out

Remains positive on Alphabet’s ecosystem and valuation support

CITI (Mark May), buy rating, PT $1,325

Alphabet’s 1Q report was worse than expected, with revenue below consensus due to impact from FX headwinds

Operating income margin and adj. Ebitda margin were better than expected

Despite weak 1Q results, still believes Alphabet can post a 3-year forward CAGR of 18% and generate GAAP EPS of $50 in 2020

A hacker going by the name L&M says he has hacked into more than thousands of accounts belonging to users of GPS tracking apps, giving him the ability to monitor tens of thousands of vehicles – and even turn off the engines for some of them, while they’re in motion, according to Motherboard.

He has admitted to hacking into more than 7,000 iTrack accounts and more than 20,000 ProTrack accounts, two apps that companies use to monitor and manage fleets of vehicles through GPS tracking devices. He has tracked vehicles worldwide, even in countries like South Africa, Morocco, India, and the Philippines. The software on some cars can be used to turn off the engines of vehicles moving at 12 miles per hour or less.

Screenshot of one hacked account

L&M reverse engineered the ProTrack and iTrack Android apps to find out that all customers are given a default password of 123456 when they sign up. After finding “millions of usernames” the hacker then blasted them all with the default password. He wound up getting access to thousands of accounts as a result.

According to a sample of user data L&M shared, he has scraped information from ProTrack and iTrack customers, including: name and model of the GPS tracking devices they use, the devices’ unique ID numbers, usernames, real names, phone numbers, email addresses, and physical addresses. Four users included in the sample L&M shared confirmed the breach.

The hacker said: “My target was the company, not the customers. Customers are at risk because of the company. They need to make money, and don’t want to secure their customers.”

He continued: “I can absolutely make a big traffic problem all over the world. I have fully [sic] control hundred of thousands of vehicles, and by one touch, I can stop these vehicles engines.”

The apps have a feature to “stop engine,” according to a screenshot provided by the hacker – although he says he never has killed a car’s engine because it would “be too dangerous”. A representative for the makers of one of the hardware GPS tracking devices used by some of the users of ProTrack GPS and iTrack, confirmed that customers can turn off the engines remotely if the vehicles are going under 12 miles per hour.

Rahim Luqmaan, the owner of Probotik Systems, a South African company that uses ProTrack, said about the feature: “That makes it more dangerous. He can actually mess around with […] our clients and customers.”

ProTrack denied the data breach in an oddly worded email response to media inquiries: “Our system is working very well and change password is normal way for account security like other systems, any problem? What’s more, why you contact our customers for this thing which make them to receive this kind of boring mail. Why hacker contact you?”

That should instill their clients with confidence.

Meanwhile, L&M seems to have successfully held both companies for ransom. When he asked ProTrack for a “reward”, they responded: “If we pay you, you will give us the tool and will not hack our account again? How can we make sure about this? Sorry for too many questions, this is the first time we meet this disaster.”

The hacker said he “got what he wanted” from the company.

L&M concluded: “They warned after my attack [sic], and that was a success for me. To force them take care about security. They know now that their customers at risk, So they focused on how to secure their service, a little bit.”

via ZeroHedge News http://bit.ly/2DF6U8m Tyler Durden

As Howard Wasserman notes, in an intriguing post at PrawfsBlawg, a panel of the Ninth Circuit has ordered briefing on whether one national injunction renders another one moot. It’s remarkable that this is a novel question—it’s another reminder of how recent the widespread use of national injunctions really is.

The one point I want to add right now to Howard’s post is about the distinction between Article III mootness and what is sometimes called “equitable mootness.” This doctrine is discussed in my article The System of Equitable Remedies.

I list a number of doctrines and habits associated with equitable remedies, including: “A claim for equitable relief is subject to a stricter ripeness requirement” (545). “Equitable ripeness,” I note, “is required only for equitable ripeness” (549). The supporting footnote is as follows:

The equitable ripeness doctrine tends to be stated more crisply in the secondary sources. See Samuel L. Bray, The Myth of the Mild Declaratory Judgment, 63 DUKE L.J. 1091, 1133-37, 1140-43 (2014); Laura E. Little, It’s About Time: Unravelling Standing and Equitable Ripeness, 41 BUFF. L. REV. 933, 977-80 (1993); Gene R. Shreve, Federal Injunctions and the Public Interest, 51 GEO. WASH. L. REV. 382, 390-92 (1983). But see LAYCOCK, supra note 38, at 585-86. Even so, the case law also shows a greater concern about ripeness and other justiciability doctrines when courts are asked to give equitable remedies. See, e.g., City of Los Angeles v. Lyons, 461 U.S. 95, 103, 105, 109, 111-13 (1983) (treating equitable requirements as more strict than the general case-or-controversy requirement); O’Shea v. Littleton, 414 U.S. 488, 499 (1974) (same); United States v. Regenerative Scis., LLC, 741 F.3d 1314, 1325 (D.C. Cir. 2014) (requiring for injunction “a reasonable likelihood of further violations in the future”); Hodgers-Durgin v. De la Vina, 199 F.3d 1037, 1042 & n.3 (9th Cir. 1999) (en banc) (W. Fletcher, J.) (concluding that although plaintiff class may have had Article III standing, they failed to show the “likelihood of substantial and immediate irreparable injury” required for equitable relief); Beck v. Test Masters Educ. Servs. Inc., 994 F. Supp. 2d 98, 101 (D.D.C. 2014) (“The claimed injury must be both certain and great and of such imminence that there is a clear and present need for equitable relief to prevent irreparable harm.”) (emphasis in original); LJL 33rd St. Assocs., LLC v. Pitcairn Props., Inc., No. 13 CIV. 5673 (JSR), 2013 WL 5969139, at *1 (S.D.N.Y. Oct. 24, 2013) (holding that declaratory judgment claim was ripe though specific performance claim was not); Town of Monroe v. Renz, 698 A.2d 328, 333 (Conn. App. Ct. 1997) (“The extraordinary nature of injunctive relief requires that the harm complained of is occurring or will occur if the injunction is not granted.”); Howe v. Greenleaf, 320 P.3d 641, 652 (Or. Ct. App. 2014) (requiring for injunction that “the conduct to be enjoined is probable or threatened”) (alterations and citation omitted); 67A N.Y. JUR. § 167 (2d ed. 2000) (requiring for injunction a “violation of a right presently occurring, or threatened and imminent”). It is harder to distinguish ripeness and equitable ripeness for equitable restitutionary remedies, but there, too, the courts seem wary of speculative claims. See Bank of Am. v. Bank of Salem, 48 So. 3d 155, 158 (Fla. Dist. Ct. App. 2010) (“[A]llegations, which pertained only to promises of future conduct, are insufficient evidence of fraud to warrant a constructive trust.”); Nw. Props. Brokers Network, Inc. v. Early Dawn Estates Homeowner’s Ass’n, 295 P.3d 314, 325 n.7 (Wash. Ct. App. 2013) (rejecting unjust-enrichment counterclaim as unripe).

Later in the article, when discussing the constraints on equitable remedies, I have this passage (578-579, some footnotes omitted):

Given the greater cost and greater potential for abuse, the equitable remedies and equitable enforcement mechanisms need limits. These limits, even if not sharply defined, give a sense of shape to a plaintiff’s expectation of equitable relief. These “equitable constraints” are crucial to understanding equity:

Equitable Ripeness. There is a requirement of additional factual development for equitable remedies, which is represented by the equitable ripeness doctrine. There is obvious overlap here with constitutional doctrines of ripeness and standing, as well as abstention doctrines. The relationship between the constitutional doctrines and their equitable counterparts cannot be untangled here. It suffices to say that they overlap, and yet that a court may invoke equitable ripeness as an independent reason not to give equitable relief.251 Indeed, cases about constitutional standing, ripeness, or abstention often emphasize the plaintiff’s request for equitable relief, and many of those cases have suggested that these doctrines apply differently depending on whether legal or equitable relief is sought.252 Nor is this concern misplaced. Ripeness is especially important for equitable remedies because they can depend on facts that are changing and contingent, and can entangle the courts in the relationship of the parties, not just at the moment of decision but (at least potentially) on a continuing basis. Not only ripeness, but other justiciability doctrines, such as mootness, are also sometimes said to be more exacting for claims for equitable remedies.254

Among the supporting footnotes are the following:

251 For analysis related to the injunction and declaratory judgment, see Bray, supra note 85. The courts’ more exacting review of the ripeness of equitable claims may take place under other doctrinal headings, such as irreparable injury, equitable discretion, and lack of propensity. E.g., In re DDAVP Indirect Purchaser Antitrust Litig., 903 F. Supp. 2d 198, 209-11 (S.D.N.Y. 2012) (finding a failure to state a claim for injunctive relief).

252 See Quackenbush v. Allstate Ins. Co., 517 U.S. 706 (1996); City of Los Angeles v. Lyons, 461 U.S. 95, 111-13 (1983); O’Shea v. Littleton, 414 U.S. 488, 499 (1974); Younger v. Harris, 401 U.S. 37 (1971); Burford v. Sun Oil Co., 319 U.S. 315 (1943); R.R. Comm’n of Tex. v. Pullman Co., 312 U.S. 496, 500-01 (1941). For discussion, see Anthony J. Bellia Jr., Article III and the Cause of Action, 89 IOWA L. REV. 777, 827, 827 n.216 (2004) (standing); Bray, supra note 85, at 1146 n.247 (ripeness); Louis Henkin, Is There a “Political Question” Doctrine?, 85 YALE L.J. 597, 617-22 (1976) (political question); see also Lochlan F. Shelfer, Note, Special Juries in the Supreme Court, 123 YALE L.J. 208, 234 (2013) (“Because the overwhelming majority of cases in the Supreme Court’s original jurisdiction sound in equity, the Court often refuses petitions on the equitable basis of alternative fora.”) (footnote omitted). For more skeptical views, see Martha A. Field, Abstention in Constitutional Cases: The Scope of the Pullman Abstention Doctrine, 122 U. PA. L. REV. 1071, 1138-43, 1139 n.177 (1974); Laycock, supra note 2, at 75; Martin H. Redish, Abstention, Separation of Powers, and the Limits of the Judicial Function, 94 YALE L.J. 71, 84-90 (1984).

254 See FTC v. Accusearch Inc., 570 F.3d 1187, 1201 (10th Cir. 2009) (“When, as in this case, a defendant has ceased offending conduct, the party seeking injunctive relief must demonstrate to the court ‘that there exists some cognizable danger of recurrent violation, something more than the mere possibility which serves to keep the case alive.”‘) (quoting United States v. W.T. Grant Co., 345 U.S. 629, 633 (1953)); Getty Images, Inc. v. Microsoft Corp., 61 F. Supp. 3d 296, 300 (S.D.N.Y. 2014) (“[T]he standard for establishing the need for injunctive relief is more stringent than the mootness standard.”); see also Pires v. Bowery Presents, LLC, 988 N.Y.S.2d 467, 472 (N.Y. Sup. Ct. 2014).

Finally, when discussing how different equitable rules, habits, and maxims help judges avoid the problems inherent in equitable remedies, I have this passage (584-585, footnotes omitted):

None of these equitable constraints is rigid . None is airtight. All are discretionary, and the discretion to invoke them is committed to the very judge they are intended to constrain—the judge deciding in the first instance whether to give an equitable remedy. This may cause some to deny that they are actually constraints. Surely they would not work for a judge who was intent on abuse of power. But not all constraints are fetters. These equitable constraints guide the responsible exercise of judicial power, both at the trial and appellate levels, by focusing a judge’s attention on certain situations where equitable remedies and enforcement mechanisms are most likely to be misused.

For example, one scenario in which judges are more likely to misuse their equitable powers is when they act with insufficient information, not just for generic reasons that might apply to every claim, but for reasons specific to equitable remedies. The commands inherent in equitable remedies are more likely to be factually involved and contingent because they need to be designed not only for present circumstances but also for future ones. The attention of judges is directed to this concern about factual development by the doctrine of equitable ripeness.

from Latest – Reason.com http://bit.ly/2GKOXGn

via IFTTT

As Howard Wasserman notes, in an intriguing post at PrawfsBlawg, a panel of the Ninth Circuit has ordered briefing on whether one national injunction renders another one moot. It’s remarkable that this is a novel question—it’s another reminder of how recent the widespread use of national injunctions really is.

The one point I want to add right now to Howard’s post is about the distinction between Article III mootness and what is sometimes called “equitable mootness.” This doctrine is discussed in my article The System of Equitable Remedies.

I list a number of doctrines and habits associated with equitable remedies, including: “A claim for equitable relief is subject to a stricter ripeness requirement” (545). “Equitable ripeness,” I note, “is required only for equitable ripeness” (549). The supporting footnote is as follows:

The equitable ripeness doctrine tends to be stated more crisply in the secondary sources. See Samuel L. Bray, The Myth of the Mild Declaratory Judgment, 63 DUKE L.J. 1091, 1133-37, 1140-43 (2014); Laura E. Little, It’s About Time: Unravelling Standing and Equitable Ripeness, 41 BUFF. L. REV. 933, 977-80 (1993); Gene R. Shreve, Federal Injunctions and the Public Interest, 51 GEO. WASH. L. REV. 382, 390-92 (1983). But see LAYCOCK, supra note 38, at 585-86. Even so, the case law also shows a greater concern about ripeness and other justiciability doctrines when courts are asked to give equitable remedies. See, e.g., City of Los Angeles v. Lyons, 461 U.S. 95, 103, 105, 109, 111-13 (1983) (treating equitable requirements as more strict than the general case-or-controversy requirement); O’Shea v. Littleton, 414 U.S. 488, 499 (1974) (same); United States v. Regenerative Scis., LLC, 741 F.3d 1314, 1325 (D.C. Cir. 2014) (requiring for injunction “a reasonable likelihood of further violations in the future”); Hodgers-Durgin v. De la Vina, 199 F.3d 1037, 1042 & n.3 (9th Cir. 1999) (en banc) (W. Fletcher, J.) (concluding that although plaintiff class may have had Article III standing, they failed to show the “likelihood of substantial and immediate irreparable injury” required for equitable relief); Beck v. Test Masters Educ. Servs. Inc., 994 F. Supp. 2d 98, 101 (D.D.C. 2014) (“The claimed injury must be both certain and great and of such imminence that there is a clear and present need for equitable relief to prevent irreparable harm.”) (emphasis in original); LJL 33rd St. Assocs., LLC v. Pitcairn Props., Inc., No. 13 CIV. 5673 (JSR), 2013 WL 5969139, at *1 (S.D.N.Y. Oct. 24, 2013) (holding that declaratory judgment claim was ripe though specific performance claim was not); Town of Monroe v. Renz, 698 A.2d 328, 333 (Conn. App. Ct. 1997) (“The extraordinary nature of injunctive relief requires that the harm complained of is occurring or will occur if the injunction is not granted.”); Howe v. Greenleaf, 320 P.3d 641, 652 (Or. Ct. App. 2014) (requiring for injunction that “the conduct to be enjoined is probable or threatened”) (alterations and citation omitted); 67A N.Y. JUR. § 167 (2d ed. 2000) (requiring for injunction a “violation of a right presently occurring, or threatened and imminent”). It is harder to distinguish ripeness and equitable ripeness for equitable restitutionary remedies, but there, too, the courts seem wary of speculative claims. See Bank of Am. v. Bank of Salem, 48 So. 3d 155, 158 (Fla. Dist. Ct. App. 2010) (“[A]llegations, which pertained only to promises of future conduct, are insufficient evidence of fraud to warrant a constructive trust.”); Nw. Props. Brokers Network, Inc. v. Early Dawn Estates Homeowner’s Ass’n, 295 P.3d 314, 325 n.7 (Wash. Ct. App. 2013) (rejecting unjust-enrichment counterclaim as unripe).

Later in the article, when discussing the constraints on equitable remedies, I have this passage (578-579, some footnotes omitted):

Given the greater cost and greater potential for abuse, the equitable remedies and equitable enforcement mechanisms need limits. These limits, even if not sharply defined, give a sense of shape to a plaintiff’s expectation of equitable relief. These “equitable constraints” are crucial to understanding equity:

Equitable Ripeness. There is a requirement of additional factual development for equitable remedies, which is represented by the equitable ripeness doctrine. There is obvious overlap here with constitutional doctrines of ripeness and standing, as well as abstention doctrines. The relationship between the constitutional doctrines and their equitable counterparts cannot be untangled here. It suffices to say that they overlap, and yet that a court may invoke equitable ripeness as an independent reason not to give equitable relief.251 Indeed, cases about constitutional standing, ripeness, or abstention often emphasize the plaintiff’s request for equitable relief, and many of those cases have suggested that these doctrines apply differently depending on whether legal or equitable relief is sought.252 Nor is this concern misplaced. Ripeness is especially important for equitable remedies because they can depend on facts that are changing and contingent, and can entangle the courts in the relationship of the parties, not just at the moment of decision but (at least potentially) on a continuing basis. Not only ripeness, but other justiciability doctrines, such as mootness, are also sometimes said to be more exacting for claims for equitable remedies.254

Among the supporting footnotes are the following:

251 For analysis related to the injunction and declaratory judgment, see Bray, supra note 85. The courts’ more exacting review of the ripeness of equitable claims may take place under other doctrinal headings, such as irreparable injury, equitable discretion, and lack of propensity. E.g., In re DDAVP Indirect Purchaser Antitrust Litig., 903 F. Supp. 2d 198, 209-11 (S.D.N.Y. 2012) (finding a failure to state a claim for injunctive relief).

252 See Quackenbush v. Allstate Ins. Co., 517 U.S. 706 (1996); City of Los Angeles v. Lyons, 461 U.S. 95, 111-13 (1983); O’Shea v. Littleton, 414 U.S. 488, 499 (1974); Younger v. Harris, 401 U.S. 37 (1971); Burford v. Sun Oil Co., 319 U.S. 315 (1943); R.R. Comm’n of Tex. v. Pullman Co., 312 U.S. 496, 500-01 (1941). For discussion, see Anthony J. Bellia Jr., Article III and the Cause of Action, 89 IOWA L. REV. 777, 827, 827 n.216 (2004) (standing); Bray, supra note 85, at 1146 n.247 (ripeness); Louis Henkin, Is There a “Political Question” Doctrine?, 85 YALE L.J. 597, 617-22 (1976) (political question); see also Lochlan F. Shelfer, Note, Special Juries in the Supreme Court, 123 YALE L.J. 208, 234 (2013) (“Because the overwhelming majority of cases in the Supreme Court’s original jurisdiction sound in equity, the Court often refuses petitions on the equitable basis of alternative fora.”) (footnote omitted). For more skeptical views, see Martha A. Field, Abstention in Constitutional Cases: The Scope of the Pullman Abstention Doctrine, 122 U. PA. L. REV. 1071, 1138-43, 1139 n.177 (1974); Laycock, supra note 2, at 75; Martin H. Redish, Abstention, Separation of Powers, and the Limits of the Judicial Function, 94 YALE L.J. 71, 84-90 (1984).

254 See FTC v. Accusearch Inc., 570 F.3d 1187, 1201 (10th Cir. 2009) (“When, as in this case, a defendant has ceased offending conduct, the party seeking injunctive relief must demonstrate to the court ‘that there exists some cognizable danger of recurrent violation, something more than the mere possibility which serves to keep the case alive.”‘) (quoting United States v. W.T. Grant Co., 345 U.S. 629, 633 (1953)); Getty Images, Inc. v. Microsoft Corp., 61 F. Supp. 3d 296, 300 (S.D.N.Y. 2014) (“[T]he standard for establishing the need for injunctive relief is more stringent than the mootness standard.”); see also Pires v. Bowery Presents, LLC, 988 N.Y.S.2d 467, 472 (N.Y. Sup. Ct. 2014).

Finally, when discussing how different equitable rules, habits, and maxims help judges avoid the problems inherent in equitable remedies, I have this passage (584-585, footnotes omitted):

None of these equitable constraints is rigid . None is airtight. All are discretionary, and the discretion to invoke them is committed to the very judge they are intended to constrain—the judge deciding in the first instance whether to give an equitable remedy. This may cause some to deny that they are actually constraints. Surely they would not work for a judge who was intent on abuse of power. But not all constraints are fetters. These equitable constraints guide the responsible exercise of judicial power, both at the trial and appellate levels, by focusing a judge’s attention on certain situations where equitable remedies and enforcement mechanisms are most likely to be misused.

For example, one scenario in which judges are more likely to misuse their equitable powers is when they act with insufficient information, not just for generic reasons that might apply to every claim, but for reasons specific to equitable remedies. The commands inherent in equitable remedies are more likely to be factually involved and contingent because they need to be designed not only for present circumstances but also for future ones. The attention of judges is directed to this concern about factual development by the doctrine of equitable ripeness.

from Latest – Reason.com http://bit.ly/2GKOXGn

via IFTTT

Multiple reports say a military coup attempt is ongoing Tuesday morning in Venezuela as an anti-Guaido militia loyal to opposition leader and US-backed Juan Guaidó tries to establish military control of key points across the capital of Caracas and other major cities.

Information Minister Jorge Rodriguez confirmed via social media the government is in the midst of putting down what’s being described as a “small coup” by military “traitors” working with the right-wing opposition.

File photo of Venezuela soldier in Caracas, via AFP

The AP has confirmed ongoing clashes between coup supporters and police inside Caracas, including reports of tear gas being fired, moments after Guaido issued statements in a video calling for a military uprising. Guaido was shown in the video accompanied by detained activist Leopoldo Lopez and surrounded by well-armed soldiers.

Crucially, Lopez said he was liberated from captivity where Maduro had put him under house arrest for leading opposition unrest in 2014, and in the video called on all Venezuelans to peacefully take to streets.

En el marco de nuestra constitución. Y por el cese definitivo de la usurpación. https://t.co/3RD2bnQhxt

In the three-minute video shot early Tuesday, Guaido said soldiers who took to the streets would be acting to protect Venezuela’s constitution. He made the comments a day before a planned anti-government rally.

“The moment is now,” he said, as his political mentor Lopez and several heavily armed soldiers backed by a single armored vehicle looked on.

“Everyone should come to the streets, in peace,” Lopez said further. The past months have seen multiple failed attempts to generate some kind of mass military and civilian uprising against Maduro, but so far all attempts have failed to generate any significant momentum, size, or staying power.

BREAKING NEWS: Interim President of Venezuela Juan Guaido has started a military coup against Maduro. Heavily armed military forces are in various locations across the capital and other major cities pic.twitter.com/9jTC2BLQXR

So far Venezuela authorities have confirmed only coming up against a handful of armed militia members, which suggests Tuesday morning’s anti-Maduro action will likely be short-lived.

developing…

via ZeroHedge News http://bit.ly/2vvkM0J Tyler Durden

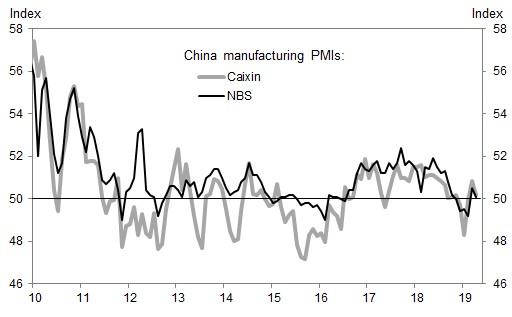

US futures were flat, while European equity markets and Asian stocks slipped on Tuesday as weak Chinese business surveys dampened appetite for risk, while a disappointing outlook and earnings at Samsung, the world’s biggest phone maker, and an ad revenue slowdown at Google sent tech stocks lower.

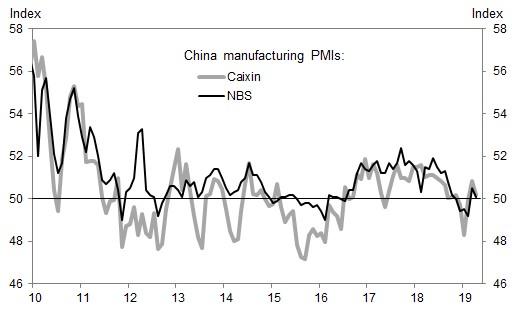

European shares followed Asian peers into the red after surveys on China manufacturing and services missed forecasts – another sign that Beijing’s efforts to spur growth n the world’s second biggest economy had yet to bear fruit, and that the rebound indicated by the spike in China’s PMI print last month was premature. As reported overnight, both official and private business surveys suggested slower Chinese factory growth this month, dashing hopes for a steady reading or even a faster expansion. Data also showed a slower expansion in its services sector. The full details again:

Chinese Manufacturing PMI (Apr) 50.1 vs. Exp. 50.5 (Prev. 50.5).

Chinese Non-Manufacturing PMI (Apr) 54.3 vs. Exp. 55.0 (Prev. 54.8)

Chinese Caixin Manufacturing PMI (Apr) 50.2 vs. Exp. 51.0 (Prev. 50.8)

And visually:

Asian markets fell after the poor Chinese data amid thin trading. MSCI’s index of Asia-Pacific shares outside Japan was off 0.5%. Bourses in South Korea and Hong Kong both fell. apan’s financial markets are closed throughout the week as Japanese Emperor Akihito prepares to abdicate in favor of his elder son, Crown Prince Naruhito.

The latest Chinese data underscored questions over prospects for the Chinese economy despite a record credit injections who impact appears to have fizzled early, while investors across the world are on edge over growing signs of a two-speed global economy where a robust United States outpaces its peers.

Adding to China’s economic disappointment were tech stocks, which slumped following Alphabet’s worse-than-expected results after the Monday close, and after Korean smartphone giant Samsung Electronics’s profit missed analysts’ recently reduced estimates and shared a worse than expected outlook. Equities in Hong Kong, South Korea and Australia all dropped, though trading was quieter than usual thanks to a holiday in Japan. As usual, bad news was good news, and shares rose in Shanghai despite poor Chinese manufacturing data.

The Asian weakness initially spread to Europe, where the Stoxx 600 index was off 0.2%, with British shares down 0.2% and bourses in Germany and France down 0.1 and 0.4% respectively in early trading, while futures on the S&P 500 also pointed to a soft open in New York.

The Stoxx Europe 600 nudged into the red, led by declines in telecommunication and mining shares, as futures on the S&P 500 also pointed to a soft open in New York. France reported steady growth for the first quarter, while Spain’s economy also grew faster than expected. Chipmaker AMS jumped 16% after beating forecasts for first-quarter profit. AMS is a supplier to Apple, which is due to report its results later. Banks dragged heavily on the Stoxx 600. Danske Bank, hit by money-laundering scandals, fell more than 6 percent after lowering its outlook for 2019, while No. 1 euro zone bank Santander also slipped after first-quarter net profit. In contrast, Standard Chartered climbed after unveiling plans for share buybacks of up to $1 billion, its first in at least 20 years. The euro added to gains after regional GDP beat estimates and inflation in some of Germany’s regions accelerated in April.

Tech stocks were hit following Alphabet’s worse-than-expected results after the Monday close, and after Korean giant Samsung Electronics’s profit missed analysts’ recently reduced estimates. Equities in Hong Kong, South Korea and Australia all dropped, though trading was quieter than usual thanks to a holiday in Japan. Shares rose in Shanghai despite poor Chinese manufacturing data.

“It’s not a stellar reporting season — I don’t think anyone expected that,” said Nick Nelson, head of European equity strategy at UBS, on Bloomberg television. “But it’s certainly better than the fourth quarter. And that fits with some of the stabilization in the broader data in the euro zone, in emerging markets and in China.”

Emerging-market stocks and currencies were weaker Tuesday following the disappointing Chinese PMI data and as investors awaited further news on progress in trade talks between the U.S. and China. Still, MSCI’s gauge of developing-nation equities remained on track for a fourth successive monthly gain, the longest streak since January 2018. The currency index, however, is set for a third consecutive drop. Seasonal data complied by Bloomberg suggests both measures may retreat in May, as they have in seven of the past 10 years.

In FX, the euro strengthened for a third day as the euro-area economy expanded more than forecast in the first quarter. The pound shrugged off a report that said U.K. Prime Minister Theresa May faces a challenge from activists within her own party opposing her leadership, and GBPUSD rose above 1.30 for the first time in a week. AUDUSD swung to a loss after an official release showed Chinese manufacturing PMI missed.

Elsewhere, South Korea’s won led currency declines, falling to a two-year low after a weak earnings report from Samsung. The Philippine peso was firmer after the country’s credit score was lifted one step at S&P Global Ratings. Turkey’s lira fluctuated as investors pondered the latest statements by central-bank chief Murat Cetinkaya. The focus now turns to the Federal Reserve policy meeting on Wednesday.

In rates, Treasuries unexpectedly reversed direction around the time Europe opened, and reversed gains that came on the back of weaker-than-forecast China manufacturing growth.

In commodity markets, oil prices reversed losses after Saudi Arabia said a deal between producers to withhold output, in place since January, could be extended beyond June to cover all of 2019. Brent crude futures were last at $71.25 per barrel, down 0.4 percent.

In overnight geopol news, North Korea’s Vice Foreign Minister said that their resolve for denuclearisation is unresolved, adding that denuclearisation will be possible only if the US changes their current calculations. If the US fails to present new positions the US will then see unwanted consequences.

In the latest Brexit news, UK PM May is said to be facing a grassroots vote demanding her resignation with Conservative party local chairman and activists calling for an extraordinary meeting with PM to demand her resignation. May’s office thereafter downplayed the significance of the meeting, suggesting that it would not be legally-binding and the outcome of the meeting wouldn’t necessarily be passed. Furthermore, there will have to be a 28-day wait until such a meeting is held.

Looking ahead, traders will be looking for signals from economic data, a Fed policy meeting on Wednesday and earnings reports from the likes of Apple and McDonald’s. Meanwhile, the next round of trade talks between the U.S. and China will get under way this week with significant issues still unresolved. But enforcement mechanisms are “close to done,” according to Treasury Secretary Steven Mnuchin, although this has been said on countless times before.

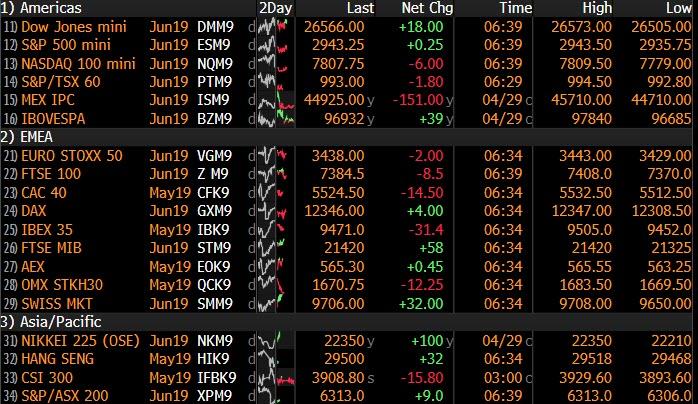

Market Snapshot

S&P 500 futures down 0.07% to 2,941.00

STOXX Europe 600 down 0.2% to 390.65

MXAP down 0.1% to 162.36

MXAPJ down 0.5% to 538.26

Nikkei down 0.2% to 22,258.73

Topix down 0.2% to 1,617.93

Hang Seng Index down 0.7% to 29,699.11

Shanghai Composite up 0.5% to 3,078.34

Sensex down 0.6% to 38,840.30

Australia S&P/ASX 200 down 0.5% to 6,325.47

Kospi down 0.6% to 2,203.59

German 10Y yield rose 2.7 bps to 0.03%

Euro up 0.2% to $1.1203

Brent Futures up 0.3% to $72.27/bbl

Italian 10Y yield unchanged at 2.213%

Spanish 10Y yield rose 2.0 bps to 1.033%

Brent Futures up 0.3% to $72.27/bbl

Gold spot up 0.4% to $1,284.33

U.S. Dollar Index down 0.2% to 97.65

Top Overnight News from Bloomberg

Yield-starved investors outside the U.S. are abandoning their currency hedges on American assets, and that’s good news for dollar bulls.

Economic growth in the euro area strengthened more than expected in the first quarter, buoyed by resilience in France and Spain.

Markets aren’t adequately pricing in the risks from higher oil costs, according to Morgan Stanley Wealth Management. Rallies in stocks and Treasuries that have taken the S&P 500 Index to a record high and 10-year yields down to around 2.5 percent illustrate that investors are complacent about crude prices.

The first official gauge of China’s manufacturing sector fell in April, signaling that the economic stabilization seen in the first quarter remains fragile

President Donald Trump sued to block Deutsche Bank AG and Capital One Financial Corp. from complying with congressional subpoenas targeting his bank records, escalating the president’s showdown with Democratic lawmakers investigating his finances

U.K. Prime Minister Theresa May will face a challenge from activists in her Conservative Party after enough signed a petition opposing her leadership and Brexit strategy to force an emergency vote on her future

The U.K.’s opposition Labour Party’s ruling council will seek to thrash out a Brexit strategy Tuesday as leader Jeremy Corbyn tries to head off a split that threatens to derail his election plans

A week after the U.S. flagged tighter sanctions on Iranian crude and spurred oil higher, prices are back down to where they were before the announcement

U.K. traders are ignoring risk of a hawkish BOE, JPMorgan says

Asian equity markets traded mostly lower following weaker than expected Chinese PMI data and as the region digested a heavy slate of earnings. ASX 200 (-0.5%) was negative in which commodity names led the declines seen across a broad range of sectors due to its high exposure to China and the disappointing factory activity, while KOSPI (-0.6%) suffered amid losses in index heavyweight Samsung Electronics after the Co.’s final Q1 results showed operating profit fell around 60% Y/Y. Elsewhere, Hang Seng (-0.7%) and Shanghai Comp. (+0.5%) diverged with Hong Kong dampened after Chinese Official Manufacturing, Non-Manufacturing and Caixin Manufacturing PMIs all fell short of estimates which overshadowed the earnings releases including the profit growth amongst the Big 4 banks, while the mainland remained afloat on month-end and pre-holiday position squaring as well as the increased hopes for more accommodative policy in the aftermath of the weak Chinese data.

Top Asian News

Jokowi Wants Indonesians to Have Say Picking New Capital City

Warning Signs Are Flashing in China Stock Market After Surge

China Triple Whammy Sees Stocks, Bonds, Yuan All Sink in April

Breaking Up: Asian Stocks Fall Out of Lockstep With U.S. Market

Major European bourses have drifted marginally lower since the EU open [Eurostoxx 50 -0.3%], following a mostly downbeat Asia-Pac lead and as the region digested a slew of pre-market earnings. Sectors are mixed with Telecom names lagging after France’s Orange (-3.5%) missed revenue forecasts and tumbled to the foot of the CAC 40. On the flip side, the energy sector is faring well amidst price action in the oil complex which aided BP (+0.4%), Shell (+0.2%) and Total (+0.1%) climb back into positive territory. Back to earnings, Standard Chartered (+5.7%) extended on opening gains after optimistic earnings coupled with a USD 1.0bln share buyback programme which is expected to reduce its CET1 ratio by around 35bps in Q2. Elsewhere, DSV (+6.8%), Beiersdorf (+2.3%), MTU Aero Engines (+2.2%), and Caixabank (-3.9%) are amongst the movers post-earnings. Finally, Danske Bank (-8.2%) shares fell to the foot of the Stoxx 600 after FT reported that Brussels vows to pursue a probe into the bank’s money laundering scandal.

Top European NEws

Greenpeace Norway Says Activists Have Left West Hercules Rig

Santander’s Bets on Latin America Pay off as Europe Stumbles

Biggest Nordic Banks Hit by Selloff After Bleak Results

Tria Says VAT Hike Could Be Inevitable Without Cuts: Il Fatto

In FX, the Dollar is softer across the board after Monday’s soft PCE inflation data and with rebalancing models for the last trading day of April flagging sells signals to varying degrees. Hence, the DXY has slipped back from 98.000+ levels again, and this time the index is probing somewhat deeper blow chart supports that were tested towards the end of last week, but not breached. If 97.544 (50% Fib) and 97.500 fail to hold, 97.460 is next on the radar before a stronger downside target and low from last week looms at 97.258.

GBP – The Pound is the best G10 performer and biggest beneficiary of month end Greenback weakness with one bank signalling especially strong Cable buying to balance portfolios. Subsequently, the pair has extended recovery gains from the low 1.2900 area to circa 1.2986 and through several DMAs including the 10, 100 and 200 levels (at 1.2940 and 1.2961 coincidentally).

EUR/JPY – Vying for 2nd place in the major ranks and both impacted by data, albeit diversely, as the single currency draws encouragement from firmer than forecast Eurozone GDP and inflation to reclaim the 1.1200 handle. However, the Jpy has now overcome strong resistance at 111.37 to peer above 111.30 in wake of disappointing Chinese PMIs overnight that spurred some risk-aversion and demand for the safe-haven Yen.

NZD/CHF/CAD – The next best G10s or gainers due to the more pronounced Usd downturn, with the Kiwi hovering near the top of a 0.6681-56 range and Franc back over 1.0200 within 1.0199-75 trading parameters, while the Loonie is pivoting 1.3350 ahead of Canadian data in the form of monthly GDP and PPI. Note also, BoC Governor Poloz and Wilkins are slated to speak later, and then NZ Q1 jobs and labour costs for Q1 are on tap before attention turns to Wednesday’s FOMC.

AUD – The Aussie is lagging on the aforementioned PMI misses from China and in particular the official and Caixin manufacturing reads that only just avoided stagnation. Aud/Usd is straddling 0.7050, as the Aud/Nzd cross slips a bit further below recent peaks of 1.0600+ towards 1.0565.

EM – The Try has been volatile again with further weakness vs the Usd in the run up and during the early part of the CBRT’s inflation presentation, but a partial recovery within a 5.9335-9835 band ultimately as Governor Cetinkaya clarified last week’s post-policy meet statement and guidance to maintain that tightening is still an option if upside inflation risks materialise.

In commodities, energy markets are trending higher, albeit remain relatively choppy in early EU trade following comments from Saudi Energy Minister Al-Falih who (in-fitting with reports) said that the Kingdom is ready to meet shortfalls caused by the expiry of Iranian oil waivers on May 2nd. However, with the upcoming JMMC meeting on May 19th (ahead of the OPEC+ meeting on June 26th) the Saudi Energy Minister also noted that a majority of the cartel’s oil ministers are tilting towards extending the global output deal. Analysts at BNP highlight that there is a “good chance” that OPEC countries and allies will decide to extent the supply curb deal in June, although some changes may be made to the current deal. The energy minister also noted that the nation’s oil output will be significantly lower than 10mln BPD (last recorded around 9.8mln BPD) until May-end, whilst exports will be below 7mln BPD (currently just under 7mln BPD). Meanwhile, IFX reported that Russia’s April oil output stood at 11.23mln BPD, slightly lower than March’s 11.3mln. This, coupled with a receding Dollar aided WTI and Brent futures to climb comfortably above USD 64.00/bbl and USD 72.50/bbl respectively. Elsewhere, precious metals are also benefitting from the weaker Greenback with spot Gold meandering just below its 100 and 200 DMAs at 1293.11 and 1297.40 respectively. Meanwhile, turning to base metals, downside seen from disappointing China Manufacturing data has been offset by the softer Dollar with copper now closer to intraday highs and just a whisker away from its 50 DMA at 2.9054.

US Event Calendar

8:30am: Employment Cost Index, est. 0.7%, prior 0.7%;

9am: S&P CoreLogic CS 20-City MoM SA, est. 0.2%, prior 0.11%; 20-City YoY NSA, est. 2.95%, prior 3.58%

9:45am: MNI Chicago PMI, est. 58.5, prior 58.7

10am: Pending Home Sales MoM, est. 1.45%, prior -1.0%

10am: Conf. Board Consumer Confidence, est. 126.8, prior 124.1; Pending Home Sales NSA YoY, est. -4.0%, prior -5.0%

The first couple of days of the week here in the UK have required a strict routine recently. Get through Monday avoiding all social media involving Game of Thrones until the evening when you can then rush home and watch it, and then speculate all day Tuesday with your colleagues about what happens next. As Jim was waiting for his house move to start series 8, we’ve had to remain tight-lipped but the flood gates have now opened since he’s been off, especially after last night’s blockbuster. We’ll politely refrain from saying any more and spoiling the plot for those who haven’t yet watched it.

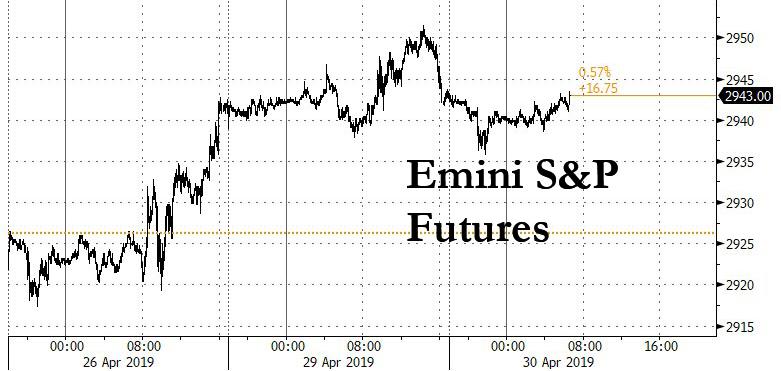

Markets are stuck in a similarly welcome routine of their own at the moment as US equities continue to nudge higher to fresh record highs. Last night’s +0.11% close for the S&P 500 was the third new closing high for the index in the last week while the NASDAQ (+0.19%) likewise closed at a new high – though it is trading lower overnight after Google’s tepid earnings. The DOW (+0.04%) is still -1.02% off its own all-time high; however, it does feel more like when rather than if it’ll eclipse that level. The VIX ticked +0.38pts higher to 13.11, but remains near the bottom of its year-to-date channel. Remarkably, the VIX has traded in an intraday range of just 3.36pts for all of April. The last time we had a smaller range during a month was February 2017. One key market indicator that has snapped out of its recent range is the US 2s10s yield curve, which rose +1.9bps yesterday to 23.7bps. That’s its steepest level since November, and it was accompanied by a general rise in yields yesterday. Yields on Treasuries and Bunds rose +2.8bps and +2.5bps, respectively. This helped bank stocks, which powered equity gains on both sides of the Atlantic, with bank stock indexes equally gaining +1.32% in both the US and Europe.

Anyway, a soft PCE inflation report in the US yesterday – albeit one which was largely baked in post Friday’s data – got the ball rolling;however, the relatively muted price action likely better reflected what is still an exhausting week ahead of big macro events and earnings.

Indeed, this morning we’ve had China’s PMIs for April where both the official (50.1 vs. 50.5) and Caixin (50.2 vs. 50.9 expected) manufacturing readings have disappointed. They also dropped from 50.5 and 50.8, respectively, last month. The official non-manufacturing reading also declined half a point to 54.3 (vs. 54.9 expected) leaving the composite 0.6pts lower at 53.4. The good news is that the composite reading is still higher than the five months prior to March, while the manufacturing reading is above 50 for a second consecutive month, with underlying components including new orders looking healthy. So, consolidation following a big bounce in March is probably the most appropriate way to describe the data.

Equity markets in China are a little higher post that data with the Shanghai Comp up +0.43% and CSI 300 up +0.19%. Positive trade comments from Mnuchin appear to also be helping. He said on Fox News that the US has “made more progress than ever before” towards a real agreement. A reminder that Mnuchin and Lighthizer travel to Beijing today. Meanwhile, the rest of Asia is a little softer with the Hang Seng (-0.48%) and Kospi (-0.55%) down. The latter seems to be suffering following an earnings miss for Samsung. In FX, Sterling is little changed overnight after the Sun reported that more than 10% of chairmen and women of local parties had signed a petition calling for PM May to resign, thus meeting the threshold for an emergency meeting.

Meanwhile, after the close last night Alphabet’s results came in a bit soft, with revenues surprisingly missing expectations. The company reported overall sales of $29.5 billion, less than the $30.0 billion expected. Profits came in at $6.7 billion, down almost 30% versus the same period last year, but most of that was attributable to a $1.7 billion fine to the European Commission. The stock price, after closing at an all-time high in advance of the earnings report, fell as much as -7% in overnight trading, sending NASDAQ futures -0.25% lower this morning.

Turning back to yesterday, the USD was little changed; however, EM currencies including the Argentinian Peso (+3.50%) had a better day boosted by the announcement from Argentina’s central bank that it would start selling dollars to stabilize the currency. In Europe, the STOXX 600 (+0.08%) recovered from early losses to just about finish onside while the DAX rose +0.10%. Spain’s IBEX (+0.12%) erased losses from earlier in the day to close in line with the rest of Europe after the weekend election result, and 10y Spanish bond yields fell -1.2bps despite the broader bond selloff. Elsewhere WTI oil (+0.32%) rose after declining -4.52% over the preceding three sessions.

Just on the details of that inflation data in the US where the March core PCE deflator was confirmed at 0.0% mom in March compared with expectations for a +0.1% reading. The extra few decimals showed it was a more marginal miss at +0.046%; however, the annual rate, which nudged down from +1.7% to +1.6% yoy was +1.553% with the extra decimal places and so a whisker away from rounding down to an even lower +1.5%. Our US economists noted that the 3-month annualized change is now just +0.7% and the lowest since early 2015 too. Their full thoughts, parsing the various inflation measures and their associated implications for Fed policy, can be found here .

So clearly a soft set of data even if the market had priced much of it in post Friday’s Q1 details. That all being said, our US economists have noted that there are two reasons to expect core PCE to bounce back next month, however. The first is the read-through from the recent bounce in equities for financial services and portfolio management services following a plunge earlier this year, and the second is that core PCE has tended to outperform core CPI in April over recent years.

Other US data didn’t really move the needle. March personal spending rose +0.9% mom versus expectations for a +0.7% rise, but personal incomes rose only +0.1% versus +0.4% expected. Separately, the Richmond Fed manufacturing survey fell -4.9 points to 2.0, a notable decline but still above the negative levels seen in December-January.

Meanwhile, the European Commission’s April confidence indicators were hardly encouraging and underscored the problems facing the manufacturing sector, as the headline economic confidence reading fell -1pt to 104, its lowest level since September 2016. The industrial confidence reading dropped -2.5pts to -4.1, its lowest reading since September 2014. The consumer and services confidence readings were flat and above recent lows, but still a bit off their peaks from last year. Separately, March M1 money supply growth came in better than expected at +7.7%, up from +6.9% in February. Digging into the credit data, however, showed weak corporate loan flows, which pushed the credit impulse to -0.6pp of GDP, its fourth consecutive negative print.

In terms of the rest of the day ahead, all eyes this morning will be on the Q1 GDP reading for the Euro Area where the consensus is for a +0.3% qoq print. We’ll get the data for France prior to that while Italy is due out a little later. Also on the cards today are preliminary CPI data for France, Germany and Italy, while this afternoon we’ve got the Q1 ECI in the US along with the February S&P CoreLogic house price index data, Chicago PMI for April, March pending home sales and April consumer confidence. Away from that we’re due to get comments from the BoE’s Ramsden while Lighthizer and Mnuchin travel to Beijing for more trade talks. The big earnings highlight is Apple after the close tonight, while Pfzier, Merck, McDonalds, Airbus, General Electric and ConocoPhillips are also on the cards. So it should be a busy day.

via ZeroHedge News http://bit.ly/2IQC9lq Tyler Durden

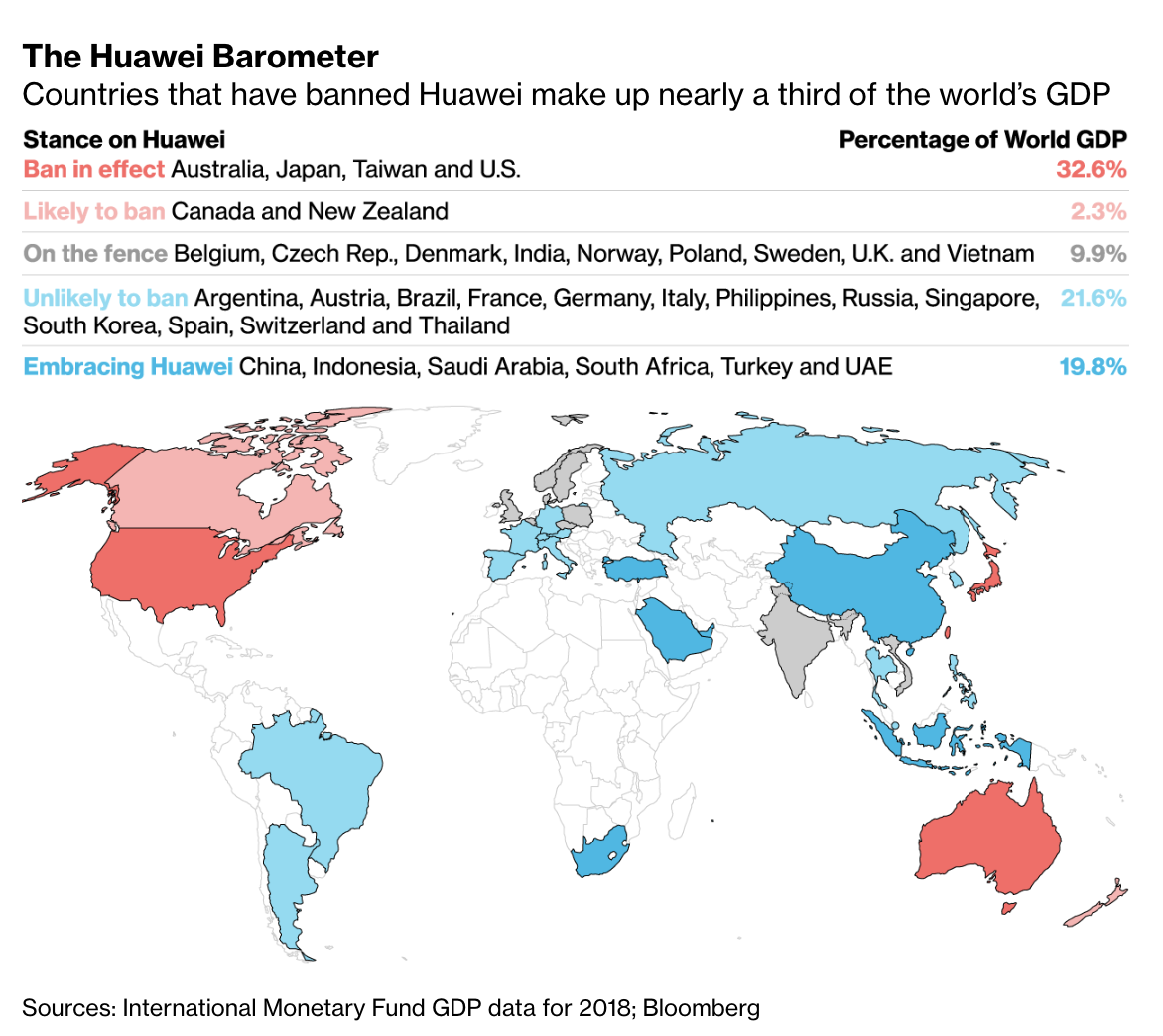

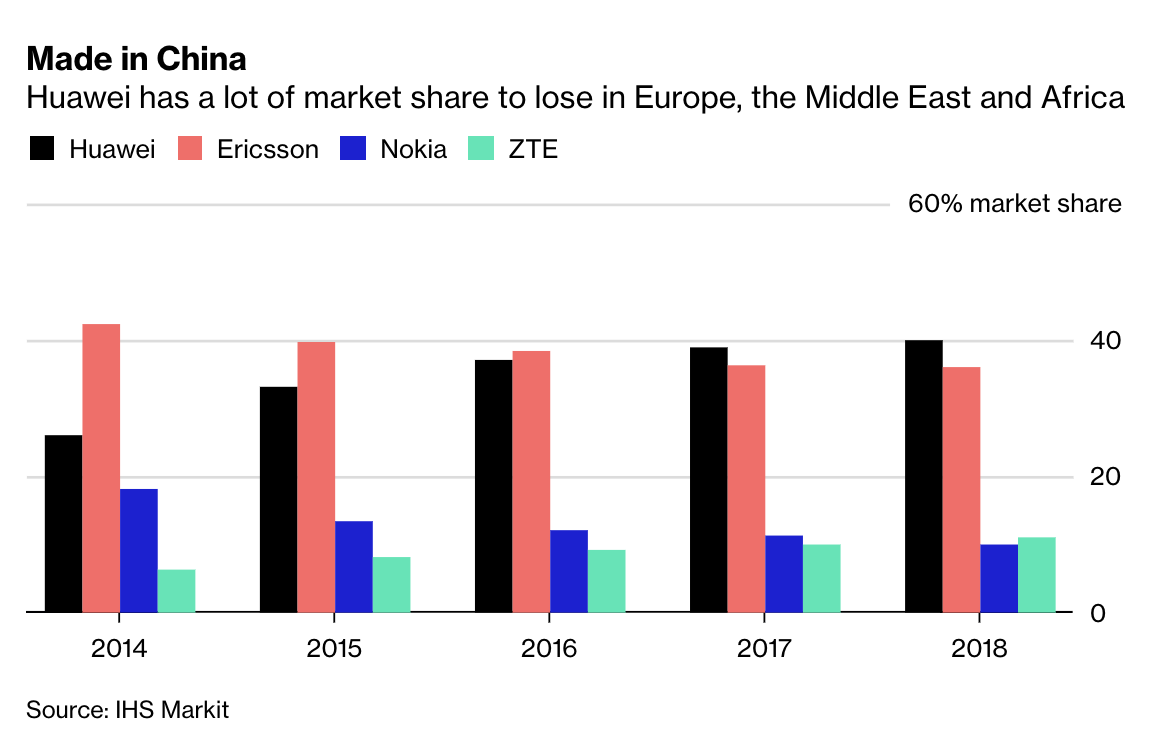

As Huawei denies Microsoft’s allegations that it discovered what appears to be a ‘backdoor’ built into the Matebook laptop series, Bloomberg on Tuesday reported on complaints from Vodafone, Europe’s largest wireless provider, about the discovery of what appear to be ‘backdoors’ discovered in Huawei equipment embedded in Vodafone’s Italian wireless network, potentially going back years.

Though Huawei has tried to cast these complaints, detailed in a series of emails obtained by Bloomberg, as innocuous glitches, but Vodafone’s acknowledgement of these concerns appears to support Washington’s warnings that Huawei equipment represents an international security risk – though the European Council and most individual states have done little to prevent Huawei equipment from being used in the Continent’s 5G wireless networks.

The vulnerabilities identified by Vodafone could grant Huawei access to the ‘fixed-line network’ in Italy, the system that provides Internet service to millions of homes and businesses, potentially exposing a large swath of the Italian population to spying by the Chinese.

After Vodafone approached Huawei in 2011 with its complaints, the Chinese telecoms giant offered assurances that the issues had been fixed; however, further testing revealed that Huawei had mislead Vodafone. What’s more, Vodafone also identified backdoors in its fiber-optic network, potentially exposing Internet traffic in Italy to Chinese spying.

Despite all of this, Vodafone did nothing after discovering backdoors throughout its Italian network and even catching Huawei in a lie when the company said it had fixed the issues, but Vodafone discovered that it hadn’t.

These concerns didn’t stop Vodafone for increasing its reliance on Huawei’s equipment, which underscores why European governments have been so reluctant to heed Washington’s warnings: Huawei is simply too important to Europe’s telecoms infrastructure. Spurning Huawei would put Europe at risk of falling behind the US and China in the race to build out 5G infrastructure.

Vodafone CEO Nick Read has joined peers in publicly opposing any restrictions on Huawei equipment in Vodafone’s 5G networks.

Most European countries are unlikely to crack down on Huawei over these security concerns.

And clearly, the issue didn’t sour the Italians on China, since Italy recently became the first G-7 country to join Beijing’s “Belt & Road Initiative”, which has been derided by critics as a “neocolonialist project.”

In addition to the security concerns in the core Italian network, Vodafone also complained about suspected vulnerabilities in routers shipped by the company. But both Huawei and Vodafone cautioned that these could have been the result of an unintentional flaw.

In a statement to Bloomberg, Vodafone said it found vulnerabilities with the routers in Italy in 2011 and worked with Huawei to resolve the issues that year. There was no evidence of any data being compromised, it said. The carrier also identified vulnerabilities with the Huawei-supplied broadband network gateways in Italy in 2012 and said those were resolved the same year. Vodafone also said it found records that showed vulnerabilities in several Huawei products related to optical service nodes. It didn’t provide specific dates and said the issues were resolved. It said it couldn’t find evidence of historical vulnerabilities in routers or broadband network gateways beyond Italy.

“In the telecoms industry it is not uncommon for vulnerabilities in equipment from suppliers to be identified by operators and other third parties,” the company said. “Vodafone takes security extremely seriously and that is why we independently test the equipment we deploy to detect whether any such vulnerabilities exist. If a vulnerability exists, Vodafone works with that supplier to resolve it quickly.”

In a statement, Huawei said it was made aware of historical vulnerabilities in 2011 and 2012 and they were addressed at the time.

But some of BBG’s other sources warned that backdoors were discovered in networks across Europe, and that Vodafone had sought to play down these discoveries.

However, Vodafone’s account of the issue was contested by people involved in the security discussions between the companies.

Vulnerabilities in both the routers and the fixed access network remained beyond 2012 and were also present in Vodafone’s businesses in the U.K., Germany, Spain and Portugal, said the people. Vodafone stuck with Huawei because the services were competitively priced, they said.

Emails obtained by BBG also revealed that some Vodafone executives were shocked by Huawei’s unwillingness to fix the backdoors, and its decision to lie about the issues being fixed.

“Unfortunately for Huawei the political background means that this event will make life even more difficult for them in trying to prove themselves an honest vendor,” Vodafone said in the April 2011 document authored by its chief information security officer at the time, Bryan Littlefair. He noted that Vodafone had made a recent security visit to Shenzhen and said he was surprised Huawei hadn’t given the matter a greater priority.

“What is of most concern here is that actions of Huawei in agreeing to remove the code, then trying to hide it, and now refusing to remove it as they need it to remain for ‘quality’ purposes,” Littlefair wrote.

Of course, Huawei has a lot of market share to lose in Europe, and therefore it’s incumbent on the firm to keep its customers happy.

But then again, if telecoms companies in Europe continued to use Huawei equipment in such sensitive capacities after this incident, then apparently switching to Ericsson or Nokia technology isn’t really an option.

via ZeroHedge News http://bit.ly/2V3sa2E Tyler Durden

Authored by former Lehman trader and current Bloomberg macro commentator Mark Cudmore.

U.S. Equity Optimism Is Starting To Look Misplaced

It’s time to turn bearish on the S&P 500, at least for a few weeks. The benchmark U.S. equity index just made a fresh record high, but it’s unlikely to keep ignoring warning signs coming from elsewhere in markets.

After having been staunchly bullish global stocks this year, I turned bearish on Asia equities on Monday last week. That negative sentiment will now spread across the Pacific. Asia, and notably China, has led the 2019 global stocks rally, and similarly has the capacity to lead a correction.

There’s not one single looming catalyst that will send equities reeling. The problem is that almost every factor is starting to look like a marginal negative. The positives from Fed dovishness, a solid earnings season and hopes of a trade deal are all generously priced in. Where’s the good news going to come from going forward?

Companies’ guidance hasn’t been encouraging and earnings estimates for later in the year continue to slide. The S&P 500 has a blended 12-months forward price-to-equity ratio of 17 versus the 10-year average of 15. Such a substantial premium is ripe for disappointment.

The data out of Asia over the past week has been terrible. Tuesday’s PMIs out of China emphasize that the market may have got over- optimistic on how quickly the economy can accelerate: All the PMI prints disappointed — private and official, manufacturing and services.

Dollar strength is another marginal negative. As is the surge in oil prices. This week’s lengthy holidays in the world’s second- and third-largest economies, China and Japan, don’t help. And, of course, May is historically a tough month for emerging markets.

Once you get in this mindset, it’s easy to see further warnings signs from the sudden surge in exceptionally large IPOs, or Alphabet’s earnings miss that came after the close on a day its stock price reached a record.

How is this week’s Fed meeting going to help stocks? With dovishness already priced, it will either confirm a gloomy economic outlook or force yields to move higher.

It’s difficult to pinpoint what will be the exact trigger for risk-aversion, and it may seem unnecessarily contrarian to turn bearish upon a record high close, but the facts are lining up for a nasty correction in the S&P 500.

via ZeroHedge News http://bit.ly/2J3yr73 Tyler Durden

Cattle ranchers who lease public land to graze their livestock tend to see free-roaming wild horses as nuisances, fueling conflict among commercial interests, bureaucrats, and animal advocates. A controversial agreement was hammered out last week—but, unsurprisingly, that has hardly settled the dispute.

That something had to change is granted by pretty much everybody involved in the wild horse debate. The government can’t just continue removing wild animals from the land and warehousing them at growing expense, as it has done for decades.

In “The Wild Free-Roaming Horses and Burros Act of 1971,” Congress announced “that wild free-roaming horses and burros are living symbols of the historic and pioneer spirit of the West; that they contribute to the diversity of life forms within the Nation and enrich the lives of the American people; and that these horses and burros are fast disappearing from the American scene.” Lawmakers ordered the Bureau of Land Management (BLM) and the U.S. Forest Service (USFS) to keep what was left of the population—perhaps 10,000 animals—alive and kicking.

Government officials sort of complied with the congressional mandate—the population of wild horses and burros has certainly grown, to over 80,000. But more of that population now lives in captivity than roams free, with holding costs consuming roughly half of the budget designated for protecting the herds.

The BLM, which inherited the lion’s share of the task, managed to turn a program intended to preserve a population of much-beloved wild animals into a scheme for corralling captive beasts that nobody wants and some interests positively dislike.

Return to Freedom, a wild horse and burro advocacy group, sees serious conflicts of interest at work. The group’s website points out:

The BLM and the USFS, among others, are responsible for managing the nation’s public lands and are foremost the managers of wild horses and burros. Their responsibilities also include issuing public land grazing permits to cattle ranchers. These grazing permits cover limited areas of public land that are available for lease. So, for every wild horse removed from a grazing permit allotment, a fee-paying cow gets to take its place, and a public land rancher gets the benefit of public land forage at bargain rates.

In 2013, the National Academy of Sciences (NAS) took a formal look at the management of the wild horse and burro population and agreed that officials have made a hash of balancing their responsibilities.

“The goal of managing free-ranging horses and burros to achieve the vaguely defined thriving natural ecological balance within the multiple-use mandate for public lands has challenged BLM’s Wild Horse and Burro Program since its inception,” the report found. Worse, BLM officials appear to have been making it up as they go along in terms of policies and procedures.

“The links between BLM’s estimates of the national population size and its actual population surveys—the data that underlie these estimates—are obscure,” the NAS assessment continued. “It seems that the national statistics are the product of hundreds of subjective, probably independent judgments and assumptions by range personnel about the proportion of animals counted during surveys, population growth rates, and other factors.”

If BLM hasn’t quite managed the challenges of conducting headcounts, it’s probably no surprise that management of the population has been equally sloppy. Removal and culling of herds to get them out of the way of competing interests even as those herds experience rapid growth—15 to 20 percent per year—is the result of ill-considered policies chasing themselves in a circle.

The NAS report adds:

Management practices are facilitating high rates of population growth. BLM’s removals hold horse populations below levels affected by food limits. If population density were to increase to the point that there was not enough forage available, it could result in fewer pregnancies and lower young-to-female ratios and survival rates. Decreased competition for forage through removals may instead allow population growth, which then drives the need to remove more animals.

To fix the problem, in addition to modifying removals, the NAS also recommended a fertility control campaign to control the horse and burro population. Birth control vaccines that prevent fertilization for females and chemical vasectomies for males, would be coupled with cross-breeding animals from different management areas to maintain diversity.

How “wild” the resulting population of neutered-and-bred horses and burros will be is an open question. But the herds have long been maintained more as museum exhibits of the wildness-that-was than as actual free-roaming beasts. Better management could have the benefit of being less self-defeating and more cost-effective in maintaining the populations. It would certainly be better than just fueling more population growth and spending ever-greater resources to warehouse or slaughter the results.

The deal that presented to BLM last week is supposed to achieve just that—better management of the not-so-wild horse and burro herds, bringing together competing groups and interests that have clashed over the issue for decades. Nonetheless, controversy continues.

On one side is the American Society for the Prevention of Cruelty to Animals (ASPCA), which calls the new agreement “a powerful, non-lethal path forward for these imperiled icons of the American West,” and The Humane Society of the United States (HSUS). The National Cattlemen’s Beef Association, Public Lands Council, American Farm Bureau Federation, and Society for Range Management have also signed on to the plan.

But others organizations aren’t convinced. Friends of Animals President Priscilla Feral accused ASPCA and HSUS of “throw[ing] in the towel when it comes to protecting America’s wild horses” by “capitulating to the Bureau of Land Management.”

An American Wild Horse Campaign statement called it “a bad deal [that] violates the Statement of Principles and Recommendations signed by more than 100 horse organizations.” The group complains that ranchers benefit the most, large-scale roundups will continue, and the agreement neglects to specify the most effective fertility-control methods, such as vaccines.

So the debate is only settled-ish, pending an assessment of the results in the years to come. But for now, federal officials have demonstrated yet again that they can mismanage anything—even herds of wild animals—into a public policy mess.

from Latest – Reason.com http://bit.ly/2J56gVk

via IFTTT

{kind=link}

{kind=link}