from Latest – Reason.com https://ift.tt/2BX3Q6r

via IFTTT

another site

from Latest – Reason.com https://ift.tt/2BX3Q6r

via IFTTT

Futures Slide On Reports Top Chinese Officials Doubt Trade Deal Will Ever Happen

Contradicting a Reuters report published just a few hours prior, Bloomberg dropped one of the most discouraging scoops about the US-China trade talks that we’ve seen in months, sending stock futures lower around the world.

BBG reported Thursday morning that many senior Chinese officials quietly suspect that the “Phase 1” partial trade deal purportedly reached earlier this month in Washington will soon fall apart, and that the odds of the two sides reaching a more comprehensive final deal are effectively zero.

The report reads like a bad WaPo hit piece on Trump, accusing him of being unrealistic about Beijing’s willingness to compromise.

As it stands – or at least as it stood during President Trump’s most recent press conference with Vice Premier Liu He – the first phase of the trade deal is essentially this: Chinese purchases of US farm goods and other products such as aircraft. It’s also expected to include Chinese commitments to protect American intellectual property and an agreement by both sides not to manipulate their currencies. In return, Trump agreed to drop the planned October tariff hikes, while remaining open to dropping the December hike as well.

Earlier on Thursday, reports speculated that the cancellation of the upcoming APEC conference in Santiago, where the US and Chinese delegations were supposed to finalize the “Phase One” deal, might give the two sides to work out a broader deal.

According to BBG’s sources, this is the bare minimum that Beijing would accept to move ahead with Phase 1: a commitment from the Americans to removing tariffs in Phase 2, and agreeing to cancel the next round of tariffs, set to take effect in December.

The people familiar with China’s position said the tariffs don’t all have to be removed immediately, but they must be part of the next stage. China also wants Trump to cancel a new wave of import taxes due to take effect Dec. 15 on American consumer favorites such as smartphones and toys as part of the phase one deal, the people said.

The drop in eminis after the report wiped out half of yesterday’s post-Fed gains.

And offshore yuan, the most closely watched indicator of trade-deal sentiment, also dropped on the news.

While Beijing remains “open” to more talks, senior officials privately don’t see much of a point. Many of the big structural changes that Washington is demanding are simply unacceptable to Beijing, and have been since the beginning. With Washington refusing to budge on lifting all the new trade war tariffs, any big “asks” will likely be off the table, seeing as Beijing insists that removing all of the new tariffs be part of any final deal. Doing otherwise would simply be “politically unfeasible” for Xi.

Then again, it’s also possible that the story could be a plant by the White House. With two FOMC voters opposing yesterday’s rate-cut, and the central bank signalling that it’s done with its ‘mid-cycle adjustment’, after yesterday, perhaps the only way for President Trump to browbeat the central bank into more easing would be to come out and declare that the trade talks have failed.

Fed won’t cut again until Trump tweets that trade talks have collapsed

Hey @realDonaldTrump you know what to do

— zerohedge (@zerohedge) October 30, 2019

Tyler Durden

Thu, 10/31/2019 – 05:34

via ZeroHedge News https://ift.tt/2qZKlbe Tyler Durden

North Korea Fires Two Projectiles Towards Japan, Official Reports Say

North Korea has fired at least one “unidentified projectile” towards the sea of Japan on Thursday, read a statement from South Korea’s Joint Chiefs of Staff (JSC).

“North Korea fired two unidentified projectiles toward the East Sea (the Sea of Japan),” the JSC statement read.

JSC said the “projectiles were fired from areas in South Pyongan Province in the afternoon,” adding that, “Our military is monitoring the situation in case of additional launches and maintaining a readiness posture.”

#NorthKorea 🇰🇵: North Korea fired two suspected ballistic missiles into the Sea of Japan this morning. The launches are the second North Korean missile test this month. pic.twitter.com/4HSXwKjmsi

— Intelligence Fusion -Asia (@IF_Asia_) October 31, 2019

No details were given on the projectiles’ type and or flight range.

The Japan Coast Guard has requested all vessels operating in the Sea of Japan to remain alert and monitor news channels.

MORE: Missile from North Korea appears to have landed outside Japan’s exclusive economic zone – Japanese coast guard pic.twitter.com/xpQT3BoPVk

— Reuters (@Reuters) October 31, 2019

Thursday’s missile test comes after North Korea said on Oct. 03 that it test-fired a new type of submarine-launched ballistic missile.

“The new-type ballistic missile was fired in vertical mode,” State-run Korea Central News Agency (KCNA) reported earlier this month. “The test-firing scientifically and technically confirmed the key tactical and technical indexes of the newly-designed ballistic missile and had no adverse impact on the security of neighboring countries.”

Earlier this week, North Korea said it’s becoming impatient with Washington over the stalled nuclear talks.

The rogue nation has set a year-end deadline for possible denuclearization of the Korean Peninsula.

North Korean general Kim Yong Chol recently said there had been zero progress in U.S.-North Korea relations. He added that Washington would be “seriously mistaken” to overlook a year-end deadline to find mutual terms for a possible future denuclearization deal.

North Korea has said the missile tests have been necessary to defend the country against Washington and its allies surrounding it with fifth-generation fighter jets.

Tyler Durden

Thu, 10/31/2019 – 05:16

via ZeroHedge News https://ift.tt/2qSnNsK Tyler Durden

Why The World Will Remember Departing ECB President As The Not-So-‘Super’ Mario Draghi

Authored by Marshall Auerback via NakedCapitalism.com,

This article was produced by Economy for All, a project of the Independent Media Institute.

Mario Draghi ends his term as president of the European Central Bank (ECB) at the end of October. He will do so as the most consequential head of the ECB since the euro’s inception. By substantially expanding the role of the central bank, Draghi likely saved the eurozone from implosion. But much like the preservation of the Bashar al-Assad regime in Syria, it’s still unclear whether the preservation of the single-currency union was a worthwhile objective, or simply perpetuated a profoundly flawed system that created misery for millions.

In many respects, Draghi’s actions were akin to adding additional floors onto a structure with a poor foundation, violating the safety codes while doing so, even as he provided more living space so that the building could become marginally habitable. But in so doing, his actions have contributed to huge socioeconomic costs and, in the words of Fritz W. Scharpf, former director of the Max Planck Institute for the Study of Societies, “also had the effect of ‘destroying the democratic legitimacy of government.’” What happens next is likely to provoke three possible outcomes:

1) the EU agrees to let member nations redevelop national sub-currencies that could balance economic issues;

2) the national debts held by EU nations could be merged to produce a supranational treasury that would sustain a huge credit;

3) or, in the absence of those two policies, dithering could produce weakened legitimacy that could initiate a collapse of the European Union project itself.

Let’s take a step back: Since inception, there have been two related problems in the Eurozone.

One is the solvency issue (i.e., the individual countries can theoretically go bust, even Germany, because they are functionally like a Canadian province or U.S. state—they use the currency, but they don’t create it). Draghi basically solved the insolvency problem with his quantitative easing program, because as the issuer of the euro, the ECB was the only institution that could credibly backstop the national sovereign bonds and prevent a default. That’s why yield spreads compressed so dramatically and national borrowing costs plunged.

As successful as this measure became, it came at a great cost. The ECB would only step in to underwrite the bonds and thereby guarantee national solvency on condition that the recipient country carried out spending cuts. In effect, the right hand stole from the left hand, as the austerity measures simply exacerbated the problem of poor consumer and business demand and forced the governments concerned to issue yet more national debt. In fairness to Draghi, the austerity conditionality was probably crucial to securing a buy-in from Europe’s central economic players in Germany; Bundesbank officials were concerned about the so-called “free rider” problem, in which hitherto profligate governments would be rewarded with low interest credit, without having sound financial controls. Absent the Berlin acquiescence, the markets would have likely dismissed the Draghi pledge.

In this regard, “Super Mario” was almost too successful. His actions created a kind of moral hazard run amok in the Eurozone bond markets. The most vivid illustration of this phenomenon is the recent bizarre phenomenon of negative yields, in which certain sovereign countries, such as Germany, have actually been paid by creditors for the “privilege” of holding their paper. This in turn has created huge financial pressures among, for example, German financial institutions, such as banks, and national pension funds. How can they pay out income to their depositors, or annuities to their retirees, if these institutions are being charged for holding German bunds which, by law, they are required to buy? In the words of Ambrose Evans-Pritchard, the international business editor of the Daily Telegraph, Mario Draghi has created “the most deformed bond market in history… [and] has jumped from the frying pan into the freezer.”

The demand problem has remained even more problematic: the Eurozone has long had a case of insufficient demand (especially in long-suffering Mediterranean nations, such as Greece, Italy, Portugal and Spain, but now extending into Germany itself). This is a fiscal problem, but as noted previously, there is no “United States of Europe” treasury, so the individual Eurozone countries are still left to their own devices on spending decisions.

As the EU currency is divorced from each member state’s fiscal authorities, however, there are multiple components that create significant budget austerity pressures. One is the presence of the Stability and Growth Pact that arbitrarily sets borrowing and spending limits (with threatened financial penalties for those serial offenders who persistently refuse to comply with the rules). The second problem is directly related to euro’s weird supranational status: by agreeing to exchange their national currencies for the euro (a currency only issued by the ECB, not the national central banks), all single-currency members have relinquished their public sector’s capacity to provide high levels of employment and output. Like American states, these countries are limited in their ability to spend by taxation and bond revenues, and the markets can effectively shut them down if fiscal policy is deemed by them to be financially unsustainable. Market participants simply stop buying the bonds, yields skyrocket and bankruptcy becomes a real possibility. This is precisely what happened before Draghi’s “whatever it takes” speech seven years ago and the so-called “PIIGS crisis” was at its peak. The problem of demand paradoxically was exacerbated by the “resolution” of the solvency issue, which created a third pressure in favor of budget austerity. Countries “saved” by the ECB were like hobbled wrecks, whose legs were broken every time they tried to stand on their own two feet. They survived, but at what cost?

It is true that the decision of these countries to swap their national currencies for the euro took place well before Draghi took on the top job at the ECB, although he certainly played an active role during the early 1990s at the Italian treasury in order to ensure that Rome acquiesced to the rigid conditions of entry. As reported in Market Watch, according to European Union historians Kenneth Dyson and Kevin Featherstone, “Mario Draghi, currently president of the European Central Bank and then director general of the Italian treasury, ‘believed in his soul’ that the euro would enforce the discipline Italian governments needed.”

One man’s discipline is another man’s needless austerity obsession. “Super Mario” saw the euro as a means of breaking the country from its so-called addiction to fiscal profligacy, which is an economic way of describing national autonomy. During his time at the Italian treasury, questions have also been raised about Draghi’s role in a mysterious currency swap that took place between Italy and JP Morgan, just before the country joined the European Union’s Economic and Monetary Union. The swap allegedly helped the Italian government to secretly borrow billions and thereby enabled it to cook its books in advance of formal entry into the Eurozone. It is precisely this cavalier approach to legality that has long characterized the economic culture of the ECB (indeed, the European Union as a whole), despite its repeated (and often hypocritical) insistence on wayward countries adhering to a rules-based order. Draghi’s tenure as ECB president has done much to expand the central bank’s remit into legally questionable activities.

And at what cost? Much of the continent is blighted by a lost generation of youth, who have never experienced anything remotely approaching secure, full-time employment or economic security. Double-digit unemployment is still rife in many parts of the EU, along with rising inequality, mounting political strife, and a revival of nationalist tensions, the elimination of which was supposedly the primary political aim of the “European ideal,” when the community was first envisaged in the aftermath of World War II. So diminished is the trust between the Eurozone member states that there is virtually no appetite for a full-on move to a “United States of Europe” fiscal authority, if the rise of intensely nationalist populist parties in France, Italy, Belgium, Hungary and Poland is anything to go by. In the past, I have likened the current scenario to Yugoslavia, prior to its dissolution in the early 1990s:

“The relatively rich republics of Yugoslavia (Slovenia and Croatia) resented policies that transferred of wealth to the relatively poorer republics, like Serbia, Macedonia, Montenegro, or the autonomous region of Kosovo. Once Tito’s organizing genius disappeared, the linkages stitching the country together became frayed and eventually snapped as old grievances manifested themselves in newer forms. The same type of evolution could happen to the European Union if it underwent a supranational fiscal union, where the rich countries feel they are being unfairly burdened—the beginnings of which are already in evidence.”

It may have created significant financial dislocation (as well as put him out of a job), but surely a better option for Draghi would have been to admit that monetary unions, absent an accompanying fiscal union, could never work. That was certainly the historic experience during the initial phase of American national independence under the Articles of Confederation, a union characterized by a weak central taxing authority and comparable squabbling amongst the original 13 colonies regarding the settlement of state debts and competing land claims. Instead of building on that weak structure, the entire articles were ultimately scrapped at the Constitutional Convention, during which a new Constitution was established that provided for a much stronger federal government by establishing a strong executive branch, national courts, and centralized taxing powers.

In an ideal world, Draghi and others would have made the case for coordinated action to reintroduce national currencies and immediately require all tax and other public contractual obligations within the nation to be denominated in that currency so as to create demand for these currencies. The problem, of course, is that Draghi was ultimately a prisoner of the austerity illusion against which he now rails in his dying hours as ECB president, belatedly understanding that monetary policy has finally reached a dead end.

In the end, Not-So-Super Mario was a man fooled by the austerity illusion… and a man willing to engage in the necessary cavalier policies of a central banker tasked with begetting a fiscal umbilical cord to the EU to fill a huge institutional hole that was never his to fill in the first place.

Tyler Durden

Thu, 10/31/2019 – 05:00

via ZeroHedge News https://ift.tt/36o8YOT Tyler Durden

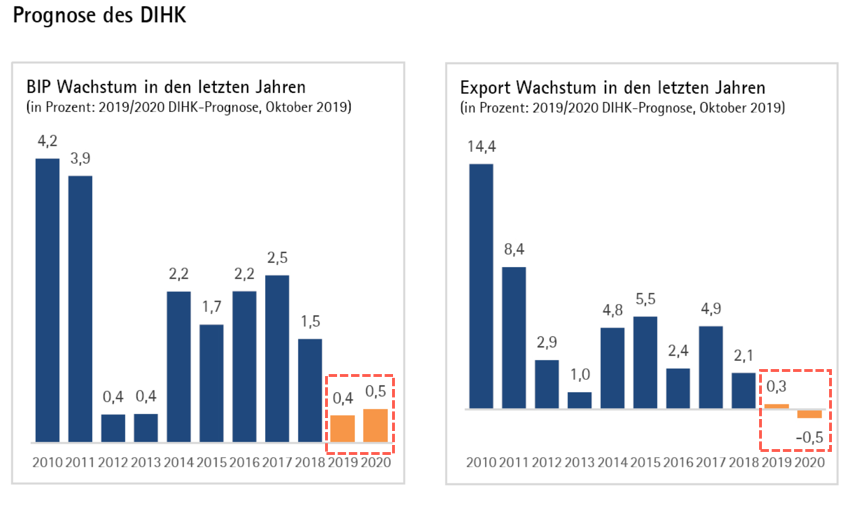

“Our Country Must Act:” Germany Exports To Shrink For The First Time Since 2008 Financial Crisis

The German economy could be headed for economic disaster, the German Chamber of Industry and Commerce (DIHK) warned in a new report Wednesday.

According to DIHK’s survey of 28,000 companies, German exports will shrink next year for the first time since the global financial crisis ten years ago.

Die DIHK-#Konjunkturumfrage zeigt: Deutlicher Einbruch bei den Geschäftserwartungen der Unternehmen. Betroffen ist nicht nur die exportorientierte Industrie, auch Handel und Dienstleister blicken sorgenvoll in die Zukunft. pic.twitter.com/u7UmOG51y9

— DIHK (@DIHK_News) October 30, 2019

DIHK’s economic outlook is more pessimistic than the Federal Government. It said Germany’s annual export growth would decline to .30% in 2019 from 2.1% in 2018. And for 2020, exports are to shrink by .50%, which would then tip it into contraction.

The “green shoots” economic rebound narrative for Europe’s largest manufacturing hub is likely dead in the water for next year.

“For our economy, with its strong industrial core, this is a huge challenge,” DIHK President Eric Schweitzer said.

“Since the financial crisis of 2008/2009, DIHK has not received such pessimistic replies from the companies,” Schweitzer said. He pointed out that Germany’s average export growth rate was usually around 5.5%.

DIHK has cut its 2019 GDP forecast to .40% from .60% previously. It estimates GDP growth of .50% for 2020, but the number will likely be revised lower in the coming months.

Commenting on Germany’s frightening export deterioration is Joerg Buck, the CEO & President of the German-Italian Chamber of Commerce, who said: “The DIHK Business Survey shows: Significant slump in business expectations. Not only the export-oriented industry is affected, but also trade and service providers are worried about the future.”

Last week, the Deutsche Bundesbank said the German economy might have entered a technical recession in September.

Schweitzer called on the Federal Government to take immediate action on the “worrying” economic development. The federal government should “act urgently.”

“Our country must take action” before the crisis arrives, he warned.

No matter how much the Bundesbank and ECB attempt to stimulate the Germany economy with countless rounds of monetary policy, the business cycle has overpowered monetary authorities. Germans must prepare for the worst in 2020, as the economy is expected to continue decelerating to crisis levels.

Tyler Durden

Thu, 10/31/2019 – 04:15

via ZeroHedge News https://ift.tt/2WxTiUL Tyler Durden

Two New York City police officers have been suspended without pay after one of them was accused of pointing a gun at a woman while off duty in a karaoke bar. Hyun Kim allegedly pointed his gun at the woman’s head and told her he’d shoot her if she didn’t hang out with them. He has been charged with two counts of menacing. His sergeant, Jun Kim, who was drinking with him, was also suspended.

from Latest – Reason.com https://ift.tt/2BVKGxF

via IFTTT

Two New York City police officers have been suspended without pay after one of them was accused of pointing a gun at a woman while off duty in a karaoke bar. Hyun Kim allegedly pointed his gun at the woman’s head and told her he’d shoot her if she didn’t hang out with them. He has been charged with two counts of menacing. His sergeant, Jun Kim, who was drinking with him, was also suspended.

from Latest – Reason.com https://ift.tt/2BVKGxF

via IFTTT

Trump Loses More Than Just The Battle Over Nordstream 2

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

For the past three years the U.S. has fought the construction of the Nordstream 2 pipeline from Russia to Germany every inch of the way.

The battle came down to the last few miles, literally, as Denmark has been withholding the final environmental permit on Nordstream 2 for months.

The U.S., especially under Trump, have committed themselves to a ‘whole of government approach‘ to stop the 55 bcm natural gas pipeline from making landfall in Germany.

I’ve literally documented every twist and turn of Nordstream 2 over the past few years here (check the archives), at Seeking Alpha and my former Newsletter at Newsmax.

Never once did I think the day wouldn’t come where the U.S. would eventually shut the pipeline down. The reason is simple. Europe, and specifically Germany, need the gas and there is no compelling reason for Germany to cave in the end if it wants to survive the 21st century a first world economy.

Russian piped gas is simply too cheap for any LNG to compete with.

In a sense, this pipeline is Germany’s declaration of independence from seventy-plus years of U.S. policy setting. Never forget that Germany is occupied territory with more than 50,000 U.S. troops stationed there.

So it is supremely rich of President Trump to call Nordstream 2 something that could make Germany a “hostage of Russia” when it’s been a hostage of the U.S. since 1945.

Then again, history isn’t one of Trump’s strong suits.

Poland had been the tip of the U.S. spear in this battle, first declaring the joint venture between Russian gas giant Gazprom and five European oil and gas majors — Wintershall, Uniper, Royal Dutch Shell, ENGIE and OMV — illegal and then forcing through changes to the European gas transit rules.

Today Nordstream 2 is wholly-owned by Gazprom where the five companies listed above are investors as creditors in the pipeline, having put up €9.4 billion as loans versus as partners, thanks to Polish intransigence.

And even if they had backed out, Russian President Vladimir Putin was always clear that the money for Nordstream 2 was available. You have to realize that this pipeline cost roughly three weeks of Russia’s trade surplus.

Poland wants to virtue signal about buying gas from the U.S. to spite Russia. That’s their business. They have other reasons for opposing Nordstream 2, their names are Angela and Merkel.

Because Merkel will be happy to replace gas going through Ukraine with gas coming through Germany to keep the Poles in line on EU integration policy. Germany will control the quotas from Nordstream 2. This is part of the reason why the Poles are so adamantly against it and why they are so set on having their own supplies.

So, they worked with Trump and others to secure their energy future, paying higher prices for the leverage to keep Merkel out of their domestic policy. It’s smart. I get that angle. But they could have gotten a better deal from Putin if they’d been willing to bury the hatchet.

In the end, the Trump administration likely spent more money opposing this project than it cost Gazprom to build it, when you factor in all the other moves made to counter Russia in Ukraine, Afghanistan, Syria and across Europe.

And the goal here was always to stop Nordstream 2 to retain some leverage over Russia by Ukraine in their negotiations of a new gas transit contract which expires at the end of 2019.

The same time that Nordstream 2 was supposed to be completed. U.S. pressure delayed this by a couple of months here as the pipeline won’t be ready on January 1st, but now that the permit has been granted there is no real leverage to play against Russia in Ukraine talks.

The gambit was to stop Nordstream 2 and then lambaste publicly, if not sue, Gazprom for not meeting its contracted volumes for delivery. This would bind the company down for years in more frivolous lawsuits within the EU while the U.S. stepped in, like the white knight, to keep Europeans from freezing to death.

Fortunately, for the world, that plan failed.

Because starving Russia of gas revenues and sending them to the U.S. is not the only goal of opposing Nordstream 2. Europe’s gas needs are so acute that there is plenty of market share to go around.

Bulgaria and other eastern European states are negotiating with Gazprom right now for new trains following path of the Turkstream pipeline across the Black Sea. Serbia is already getting theirs because they are an important bulwark against NATO for Putin.

Putin is in Hungary today talking with Prime Minister Viktor Orban who is also keenly interested in gas from Turkstream.

By the time Gazprom and Putin are done not only will Nordstream 2 be bringing in 55bcm, but Turkstream will have all four projected trains operating bringing in another 68 bcm.

So, which one of these is the real prize?

In the end the story of Nordstream 2 has a happy ending. Because despite the ridiculous rhetoric about European energy security, nothing secures the long-term peace in Europe than stitching the continent together with Asia with energy pipelines.

If Nordstream 2 wasn’t the optimal solution to Europe’s needs blame the U.S. and the EU itself for forcing Russia to scuttle South Stream in 2014 and fomenting a coup and the subsequent failed state known today as Ukraine then as well.

We broke what didn’t need fixing. But the U.S./U.K. obsessions with blunting the rise of China and enacting revenge on Russia for not becoming a vassal state to Wall St. and City of London under Putin wouldn’t be appeased.

There had to be one last major push for central Asian chaos and Nordstream 2 was only of those major offensives, like Syria, the war against the Donbass, the invasion of Yemen and the isolation of Iran.

All of those projects are coming to their very rapid conclusion now. And the geopolitical map will be forever changed.

Nordstream 2 going forward means now that Ukrainian President Zelensky will come to a quick decision on a transit contract with Gazprom. He’s already accepted the ‘Steinmeyer Formula’ for settling the conflict in the Donbass.

He’ll meet with Putin and risk a coup by the Banderists to get this done. He has to or Ukraine will not survive.

After four plus years of stalemate on these issues, like Brexit, when crunch time happens, everyone folds their hands and cuts a deal.

Had somehow Poroshenko remained in power Ukraine would continue to sink into irrelevance as the U.S. would keep them on the same ruinous path out of spite and the vain hope of success in the future.

So the future of Nordstream 2 was written in stone years ago, as Poroshenko’s approval sank into the abyss.

Moreover, Trump has lost the whip hand over Merkel on energy which means a quick reversal of foreign policy positions with respect to Russia. Once the Donbass is solved and a gas transit contract signed/extended and Nordstream 2 completed, expect the EU to lift sanctions on Russia and resume normal trade relations.

The first two things will likely happen now before the end of the year. Sanctions will be lifted in 2020.

Had Nordstream 2 failed, none of these outstanding issues would resolve themselves in the next five years.

This is how important Nordstream 2 was to the future of Europe and it proves that a pipeline and mutually beneficial trade, more so any political union, is a more powerful weapon than all the tanks in the world.

This is one fight I’m glad Trump lost.

* * *

Join My Patreon if you want to understand how to profit from these tectonic shifts in the geopolitical landscape. Install the Brave Browser if you think Google shouldn’t decide whether we should talk about them.

Tyler Durden

Thu, 10/31/2019 – 03:30

via ZeroHedge News https://ift.tt/2C0gnpP Tyler Durden

ECB Official: Can Use Portfolio To Combat Climate Change

Central banks have been making all kinds of ridiculous climate change statements in the last several quarters. Some monetary authorities have even said, they could also expand balance sheets to purchase climate-related financial investments.

Sabine Lautenschläger, Member of the Executive Board and Governing Council of the European Central Bank (ECB), was quoted by Bloomberg on Wednesday in Düsseldorf, Germany, as saying the ECB is prepared to use its balance sheet to support the fight against climate change.

Bloomberg quoted Lautenschläge as saying:

• Sustainability criteria are already taken into account in our portfolios that are not held for monetary policy purposes: Lautenschlaeger

• The ECB needs to address all citizens, not just an expert audience – without ever becoming political

We’ve suggested in the past, that this is just a giant ruse to sneak through MMT and helicopter money under the virtue-signaling guise of fighting climate change.

Central banks, who’ve spent a decade expanding balance sheets, have plowed trillions of dollars into financial assets across the world.

The flawed policy lifted financial asset prices but only benefited a few who held stock, bonds, real estate, etc… Everyone else, which is a majority of the global population are considered non-asset holders, didn’t participate in the decades-long orgy of cheap money, thus created a massive wealth gap that can no longer be ignored.

As a result of the wealth gap, protectionism and nationalism are sweeping across the world.

Political uncertainty across the world is at the highest levels ever.

Millions of people are currently protesting from Asia, the Middle East, and South America, calling for change after a decade of flawed monetary policy by global central banks.

The only solution offered by financial elites is to create an economic narrative of how global warming will doom the world. Then to calm fears, offer a solution, that answer is MMT and helicopter money.

If you think balance sheets among central banks are large in today’s standards, just wait until the next global recession strikes, which could be as soon as next year, then central banks will use the narrative of climate change to expand balance sheets at record paces.

But printing money this time will be okay because it’ll save the world from climate change.

Tyler Durden

Thu, 10/31/2019 – 02:45

via ZeroHedge News https://ift.tt/2qawvm4 Tyler Durden