At precisely 11am on November 11, 1918, in a nondescript railroad car in northeastern France, a group of senior military officers and government officials signed an armistice agreement that effectively ended World War 1.

The Great War had killed a staggering 9 million soldiers in four years. That’s more than nearly every major global conflict in the previous two centuries combined.

Yet right at the same time as the war ended, a mysterious new virus started spreading around the world that eventually became known as the Spanish Flu.

And in less than three years the Spanish Flu infected 500 million people and killed as many as 100 million people, roughly 5% of the entire world population at the time.

This made the Spanish Flu five times deadlier than World War 1. And that’s really scary to think about.

But let me be clear: the Coronavirus is not the Spanish Flu. Not even close.

It’s understandable and completely normal to be nervous about the Coronavirus. It’s starting to spread rapidly, infection rates are climbing, and financial markets are swooning.

But we are going to be just fine. Humanity as suffered through much worse.

Now, to shrug this off as ‘no big deal’ is frankly a bit silly. This is obviously a pretty big deal, and it’s having a major impact worldwide in some of the strangest ways.

For example, lately I have been negotiating the refinance of an approximately $8 million loan with a large European bank. But that deal has slowed to a crawl thanks to Coronavirus. (Fortunately, the loan continues to earn substantial interest, so the delay is quite profitable for us.)

In Hong Kong, I’m leading a civil lawsuit against a fraudulent investment scheme, but the courts have been closed for weeks and don’t look to be opening anytime soon.

And I expect the impact will only grow… so being a little bit nervous about this does not make you paranoid.

But just remember that, as human beings, we generally make HORRIBLE decisions when we’re emotional… especially when that emotion is FEAR.

It’s also very easy to succumb to a herd mentality at a time like this. When everyone else is freaking out and panicking, it’s even easier to freak out and panic.

So let’s step back for a moment and think rationally together about a few things:

First, don’t do anything drastic. Avoid reactionary decisions, especially related to your finances.

For example, if you’re thinking about dumping all of your stocks because of the Coronavirus, then why did you buy them in the first place?

Business is hard, and there are always going to be complications and challenges. You can’t expect everything to be smooth sailing 100% of the time.

Great businesses adapt and overcome. They thrive when others buckle, and they come out of turmoil stronger than ever.

So think twice before you follow the crowd and sell shares of a great business that’s managed by talented people of integrity.

Second– three weeks ago I wrote about the virus, saying that “It doesn’t hurt to have a Plan B. . . if the virus appears to be spreading, you can bet that there will be a run on surgical masks and potentially even food at the grocery store.”

That appears to be happening in a number of places that have heavy infection rates. And it’s very difficult to find N95 respirator masks now.

I’ll reiterate—there is no downside to stocking up on some extra food, especially non-perishables, and some medicine.

Last, I’ll tell you a quick story that you’ll hopefully find hilarious.

A few weeks ago when the virus started becoming more of a concern, I thought to myself, “if the virus really starts to spread, stock markets will take a big hit.”

So I bought some ‘out of the money’ put options on the S&P 500. If you’re not sure what that means, I was essentially betting a small amount of money that the stock market would fall. And if my prediction came true, the bet would have paid off probably 10x within 2-3 weeks.

The thing about options, though, is that they’re not open-ended. I had to bet that the market would fall by a specific date. And the date I chose was Friday, February 21st—last week.

Well, Friday February 21st came and went without any fuss whatsoever. So I lost all the money I bet.

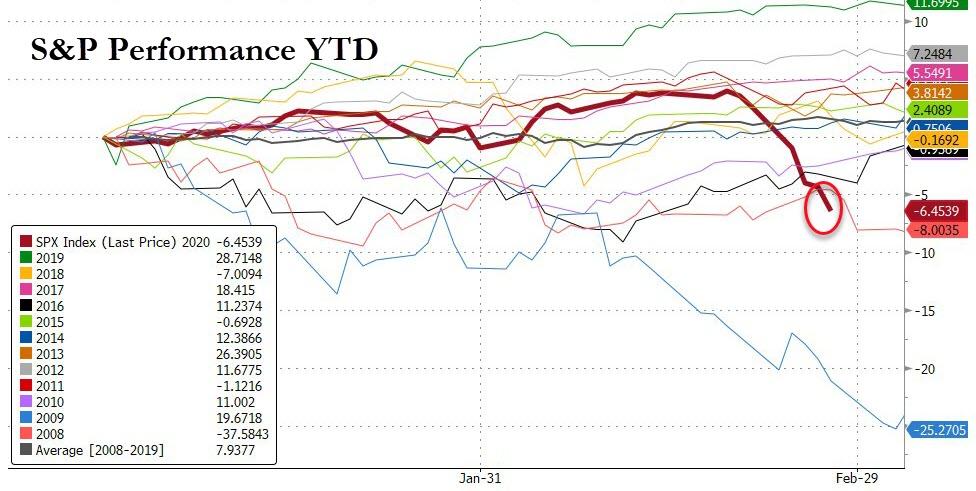

The very next trading day, Monday morning, the market tanked. And the day after that. And the day after that. And the day after that.

So I was right that the market would plummet. But I was just barely wrong about the timing. I was wrong by literally one trading day… and as a result I lost 100% of my investment.

The good news is that the amount of money I put down was trivial, so no big deal.

But it is a nice reminder that, even when you get the trend right, it’s damn near impossible to predict the timing.

Frankly I should have just bought more gold.

Gold has surged as a result of the virus spreading around the world because it’s a safe haven asset. On top of that, gold has several supply and demand fundamentals that support higher prices.

But we’ll talk more about gold soon, and why I think it has even more room to run.

from Sovereign Man https://ift.tt/2uzeQa0

via IFTTT