The Most Miserable Place On Earth: Disney Firing 28,000 Workers Tyler Durden

Tue, 09/29/2020 – 17:15

In what may be the biggest mass layoff in recent history, after the market close Walt Disney unveiled its transformation to the most miserable place on earth, announcing that it would lay off 28,000 workers in its U.S. resort business, in the latest confirmation that the covid pandemic continues to devastate all tourism and communal experiences.

“As heartbreaking as it is to take this action, this is the only feasible option we have in light of the prolonged impact of Covid-19 on our business,” Josh D’Amaro, the chairman of the parks division, said in a memo to workers.

The cuts span across the company’s various businesses including theme parks, cruise ships and retail businesses, Disney said on Tuesday. While the layoffs also include executive, they are focusing on part-time workers: 67% of those getting a pink slip are part-time workers.

As part of its farewell package, Disney will offer benefits to the workers being cut, including 90 days of severance.

The mass layoffs follow the furloughing of a massive 43,000 workers in April, when the company was first impacted by the covid pandemic.

In July, Disney triumphantly reopened several of its shuttered parks, including in Florida, although visits were a fraction of their pre-covid levels. Disney still hasn’t received clearance to restart operations at its two theme parks in Anaheim, California.

Before the pandemic, Disney’s domestic parks alone employed more than 100,000.

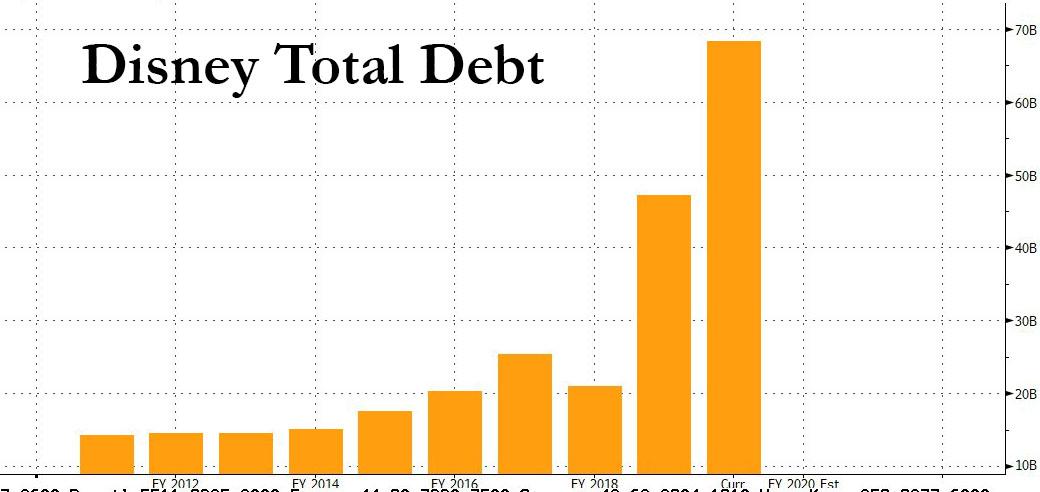

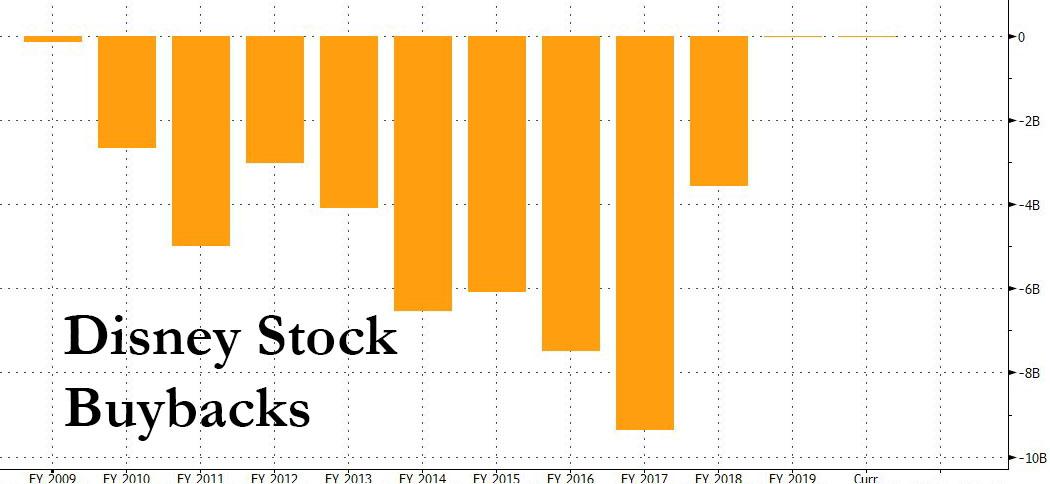

And while one can “understand” the plight of management, which is scrambling to boost cash flow after it saddled the company with record debt in recent years…

… it probably would make all those soon-to-be-laid off workers feel a little bit better if most of that newly issued debt hadn’t gone to pay for stock buybacks the benefited upper management.

Disney stock dropped on the news because it appears that buybacks won’t be coming back any time soon.

via ZeroHedge News https://ift.tt/3i9hKFe Tyler Durden

Verizon Looks To Dump Unprofitable “Huffington Post” As Traffic Sags Tyler Durden

Tue, 09/29/2020 – 17:05

The Huffington Post has already been gutted by several waves of layoffs since the left-leaning digital news aggregator was sold to Verizon as part of a deal to buy the rest of AOL’s assets in 2015. Now, the New York Post is reporting that the telecoms giant, which engineered the acquisition as part of a larger content play, is shopping around for a buyer.

But in one of the worst environments for bloated digital media outlets in ages, it appears Verizon is having trouble finding a seller.

To be fair, HuffPo essentially came with the rest of the furniture during Verizon’s $4.4 billion acquisition of AOL, a deal that has proven about as disastrous as one might expect.

Verizon has pitched the site to several companies, including Thrillist owner Group Nine Media, Rolling Stone published Penske Media, Bustle Digital Media and J2 Global, according to a report in Insider, a rival digital media publication which has itsef created headaches at its owner, German publisher Axel Springer.

To be fair, Verizon has gotten at least one nibble from Vox. Given the left-leaning editorial direction at Huffpo, it’s possible that some synergies might be found.

Unfortunately for HuffPo’s remaining employees, part of the sale will likely be based on whether the buyer is willing to take an axe to HuffPo’s “enormous” overhead costs.

Being a “reporter” at the Ariana Huffington-founded website is a notoriously thankless job featuring substandard pay and long hours, with employees essentially at the mercy of Ariana Huffington and her favored inner circle, according to a New York Times expose from a few years back which exposed Huffington’s hypocrisy in selling “work-life balance” while exploiting low-paid recent graduates, mostly from the Ivies and other top schools (an unspoken prerequisite for the job is having parents wealthy enough to help out with rent and pocket money, given the abysmal pay, which can be less than $40,000 a year.

Then again, one expert opined to the New York Post that the site is essentially worthless, reasoning that if Verizon can’t sell enough ads on the site, then nobody can.

“The brand means nothing anymore and it’s ultra partisan,” said one unnamed source.

via ZeroHedge News https://ift.tt/36hA9xb Tyler Durden

To put it simply, Palantir is one of the oldest private big data software companies.

Palantir sells software to businesses and government agencies to help them manage their data and make better connections.

For example, Palantir can find connections from thousands of unstructured data points (credit card purchases, phone calls, web browsing) to identify a potential terrorist for government agencies.

The company was built on government contracts and only recently has begun making a big push to diversify into corporate contracts.

Palantir’s product is most definitely valuable and in demand, but there are three major risks we see to continued growth and profitability that are keeping us on the sidelines for now.

THREE MAJOR RISKS TO GROWTH

#1: Reliance on Big Government Clients

Palantir is trying to diversify away from a dependence on government contracts but so far has not been successful.

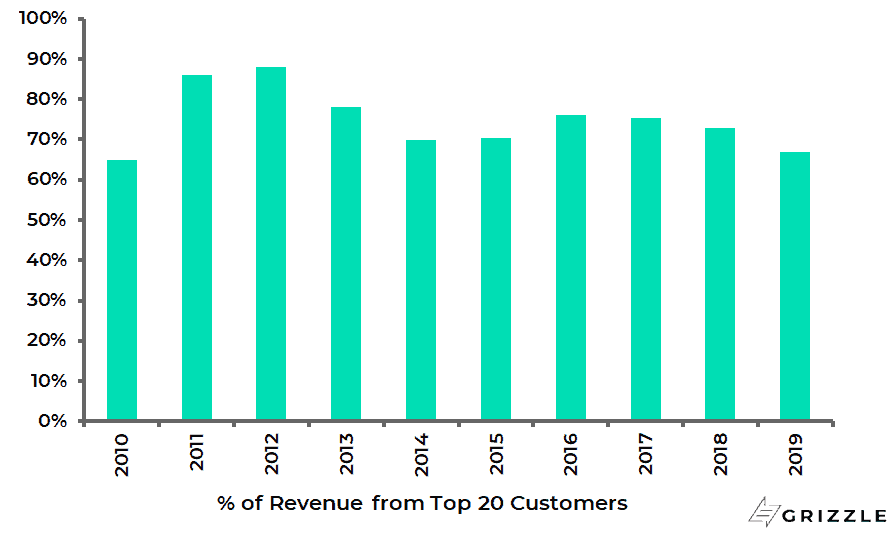

Looking at the % of revenue coming from the largest 20 clients (read governments) we don’t see a meaningful decrease in the weighting over the last few years.

A high concentration of customers means a loss of one can have a big impact on revenue growth and the stock price.

Investors don’t like surprises and Palantir’s customer concentration is currently an unwelcome feature of the company.

% OF REVENUE COMING FROM LARGEST 25 CUSTOMERS

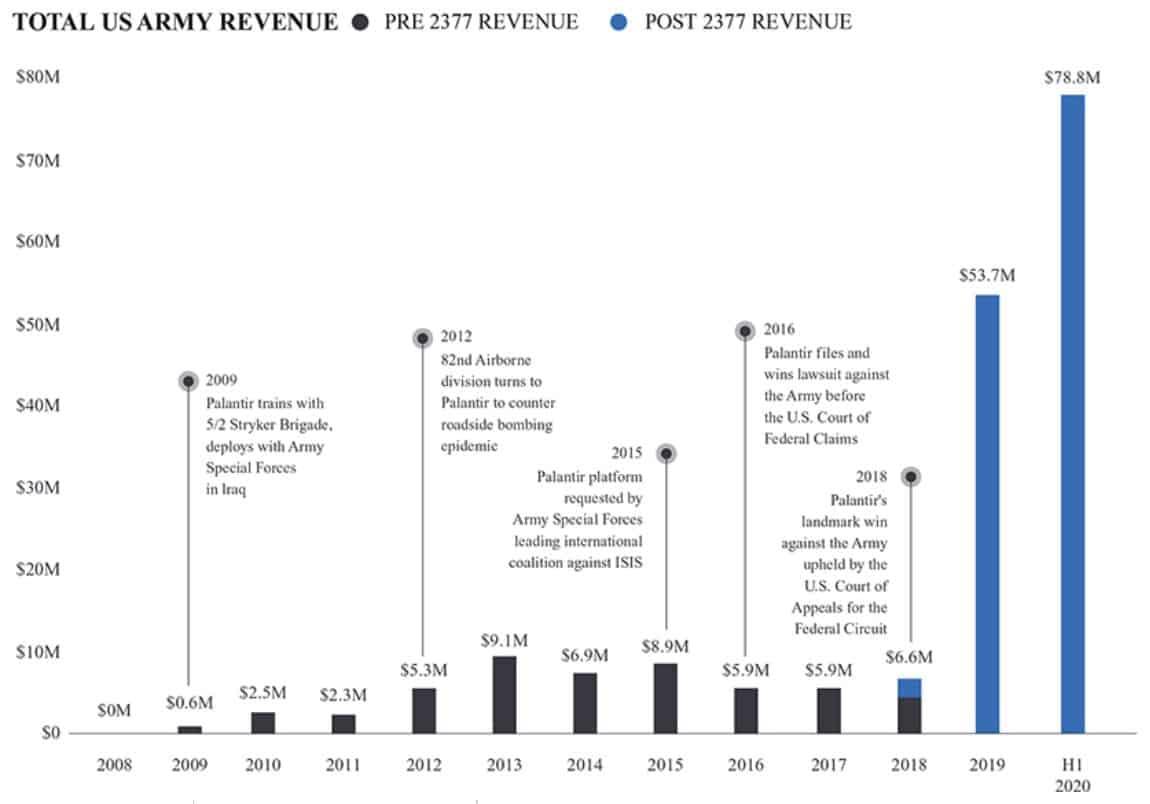

A contract with the U.S. Army made up a big part of that jump in government revenue.

The U.S Army alone went from 1% of revenue in 2018 to 16% today and was 30% of all revenue growth in 2019.

BIG JUMP IN GOVERNMENT REVENUE IN 2020

Source: Palantir S-1

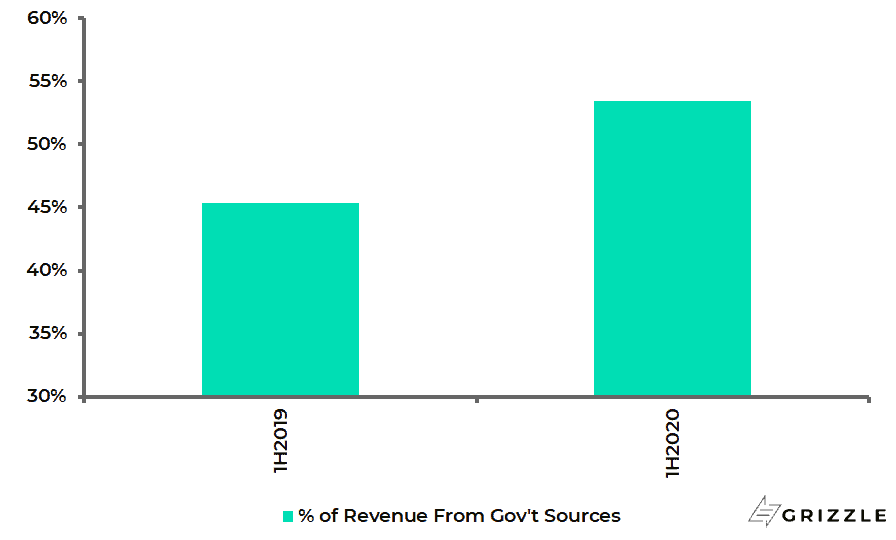

To drive our point home, government revenue increased from 45% of sales in 1H2019 to 53% in 1H2020.

COVID HAS ACTUALLY INCREASED GOV’T CONCENTRATION

Source: Palantir S-1

Corporate diversification is only in the early stages which could keep growth from showing the slow and steady results investors expect from SaaS companies.

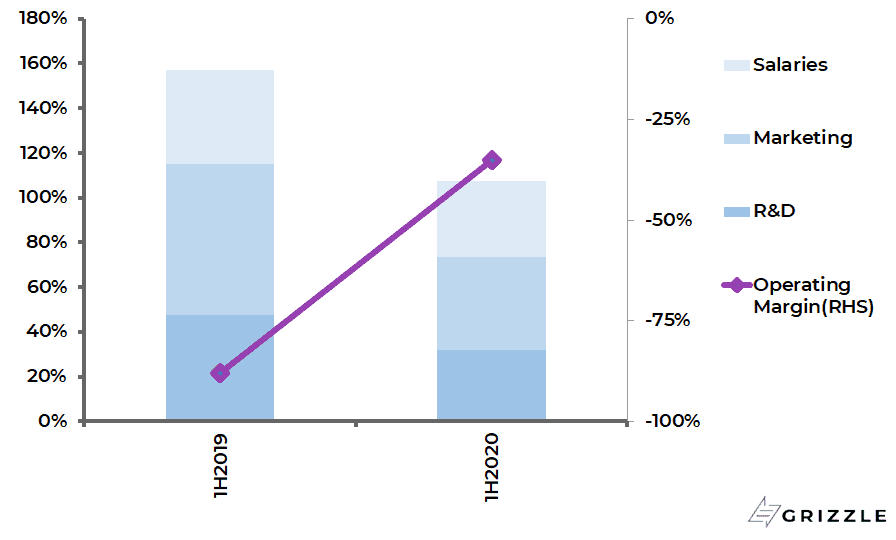

#2: The Recent Improvement in Margins Likely Won’t Last

Palantir has seen a big increase in profit margins in the last six months compared to last year.

Investors new to the story may be tempted to pay a higher price for the stock to give the company credit for a new, higher-margin profile.

We think this would be a costly mistake.

If you dig a bit deeper you will see the margin increase was due to unsustainable cuts to operating expenses, not a change in the long-term profit potential.

The chart below shows that marketing spend as a % of revenue fell 25%, R&D spend fell 16% and salary expense fell 8%.

Palantir specifically called out the Coronavirus in their S-1 for keeping employees at home which has saved them lots of money on travel and marketing expenses.

In our opinion, these cost savings will largely reverse once the pandemic is over and sales and marketing ramps back up.

We are already seeing this with Marketing, R&D and G&A as a % of revenue up in the June quarter reversing some of the big fall in the quarter ending March.

The chart below shows that the improvement in the operating losses was almost exclusively due to lower spending on R&D and marketing, not a change in the underlying profitability of the business.

CUTS IN MARKETING AND PERSONEL SPENDING DROVE MARGIN GAINS IN 1H2020

Source: Palantir S-1

If costs rebound as the Coronavirus recedes it will slow or even reverse the recent profit improvements, denting the multiple investors are willing to pay and the stock price.

#3: To Grow You Need Clients, But Client Attrition is Concerning

Palantir’s average customer has been with the company for over six years, which is impressive and is typical among large government clients.

But to win these huge accounts, the company spends a lot more time selling the product before the customer will bite, six to nine months on average.

Also, the initial revenue from the contracts are tiny as Palantir proves the value of its software to customers who over time ramp up their usage and spending.

The initial losses are all fine if Palantir can hang onto clients for a long enough time, but recent data points to some lost customers as the Pandemic raged.

According to back of the envelope calculations below, Palantir went from 133 customers in 2019 to 125 today.

Palantir is not immune from the Coronavirus.

Based on my math they’ve lost around 8 customers in H1 2020 (comparing end of period 2020 customers with 2019 average) pic.twitter.com/RgXbz74y7Y

An article on Palantir’s push into Europe makes a concerning claim that of the 48 entities to have tried the service, 27 had already quit with the status of 8 others unknown.

Potentially losing 70% of your clients even if it is over a number of years doesn’t give us confidence in Palantir’s ability to hold onto clients long enough to generate solid profits from them.

Palantir’s business model gives up profits in the short term for cashflow on the backend, but it only works if customers don’t leave.

Given the lack of information around Palantir’s customer churn and 16 years of losses, we question if the profitability required to justify a $22+ billion valuation will ever arrive.

PALANTIR CHOSE A DIRECT LISTING INSTEAD OF AN IPO: WHAT’S THE DIFFERENCE?

Palantir management chose a different route to take the shares public than the traditional initial public offering (IPO) process.

The decision to pursue a direct listing over an IPO could have potentially huge implications for the future price of the stock.

The biggest practical difference between an IPO and a direct listing is that Palantir will not set an official price for the shares before trading begins.

In an IPO process, the management team travels all over the world meeting investors, explaining the story and drumming up buying interest.

Based on these meetings and conversations between the banks on the deal and their own clients, a price is decided on that balances supply, demand and the desire to see the stock price perform well, ie. go up, on the first day of trading.

A direct listing avoids all of this price discovery in favor of letting investor’s sort out the price for themselves through actual trades on the first day.

Now don’t think this means investors can just name any price they want for the stock until the equilibrium price is found.

Day 1 trades are still anchored to where the stock has been trading recently on the private markets.

Investors set their opening bids based on the private price of the stock, so these prior sales do have a big impact on early trading prices in a direct listing.

The market maker, the one who makes sure shares are trading hands in an orderly fashion, also sets a “reference price” on the first day based on buy and sell prices they are seeing.

This reference price also guides investors in what prices they offer on day 1.

Now the big difference between an IPO and a direct listing comes after the first public trade is done.

In a direct listing, all shareholders are free to sell their stock whenever they want at the prevailing market price.

This differs in a big way from an IPO where a majority of shares are restricted from trading for 180 days.

Direct listings can lead to more selling pressure than a typical IPO which means the stock price falls more in the month or two after going public than it would under an IPO process.

However, the market finds the stock price that balances supply and demand quicker than in an IPO where the share restrictions keep supply artificially low.

Looking at past direct listings will give us a flavor for how the Palantir stock price could perform in the days and months after it goes public.

HOW HAVE OTHER DIRECT LISTINGS PERFORMED?

There are two large direct listings we can use for reference here, Spotify and Slack.

Spotify went public in April 2018 while Slack’s direct listing was in April 2019.

Both companies did not put any restrictions on stock sales by employees and insiders, which is a big difference from the 180-day lockup Palantir is imposing on 80% of shares outstanding.

So how did buyers of the stocks on day 1 make out?

For Slack, the company gave investors a “reference price” before the direct listing of $26.

The stock opened at $42/sh, a 62% pop on day 1.

Spotify listed a reference price of $132/sh and also opened higher, up 25% to $165/sh.

So insiders were certainly happy but what happened to investor’s who bought at those prices?

In Slack’s case, the stock closed day 1 at $38.62/sh before eventually falling to $25 3 months later and bottoming at $22 in October, handing early investors a 40% loss.

Spotify closed the first day at $149.01/sh and was at $169/sh 3 months later, however, the stock bottomed at $109/sh in December handing investors early losses just like Slack.

Based on the track record of the two largest direct listings so far, investors should not be buying Palantir until the stock has been publicly traded for at least six months.

HOW DOES GROWTH AND PROFITABILITY STACK UP?

High growth software companies are valued by the market for their growth above all.

The faster you can grow the more the market likes you and the higher multiple of revenue they are willing to pay.

Cashflow, profits, free cashflow, whatever your name for profitability, they all come in a distant second.

The most important steps you can take to figure out where Palantir should trade on day 1 and 10 years from now is to figure out how revenue growth stacks up against other software competitors.

Best growth = best multiple, its really that simple.

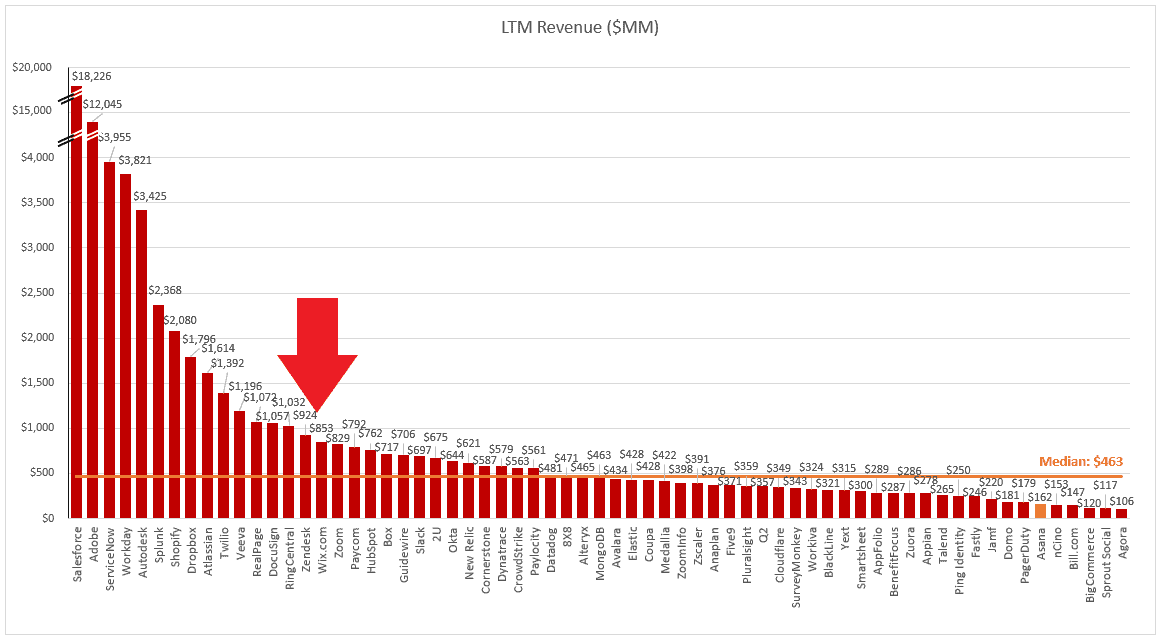

First, looking at the absolute size of Palantir, the company is on the larger side for a cloud software business.

The company has been in business for almost 20 years which explains its larger size.

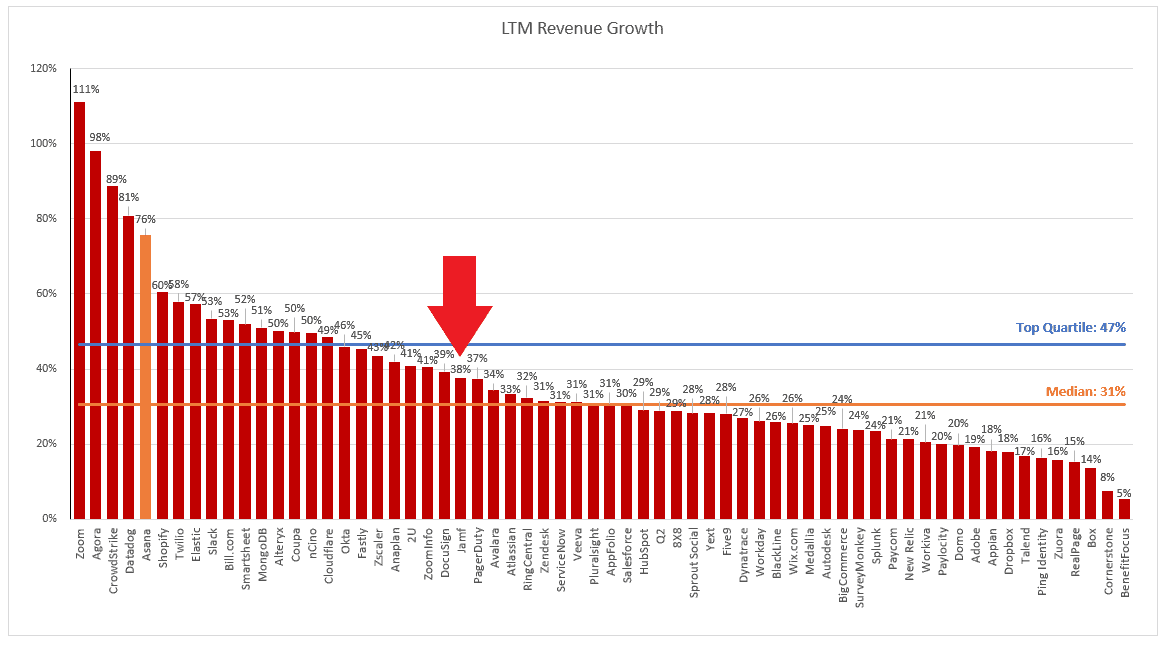

Growth is more important than the absolute level of revenue however and here Palantir puts up a decent showing based on the last 12 months of revenue growth.

Growth is above average but out of the top quartile and forecast to slow to 35% in the next 12 months, from 38% in the last 12.

The company is still losing money while also growing slower than a majority of software peers which is concerning.

We need to see a pickup in growth or a big increase in the cashflow margin for this stock to be worth a purchase when there are already so many attractive SaaS stocks growing faster for not much more money.

24% OF SHARES CAN BE SOLD ON DAY 1

The performance of Palantir in the first few weeks after going public will depend on how many shares can be freely sold by insiders.

In the direct listings for Slack and Spotify, more than 80% of shares could be freely sold as soon as the stocks started trading.

Palantir management no doubt saw the weak stock performance of both companies in the months after listing and is trying to avoid the same outcome.

To do this they’ve gotten shareholders of 75% of the stock to agree not to sell their stock until 3 business days after financial results for the year ending 2020 are released.

This means Palantir’s “share unlock” date will fall sometime in late January 2021.

With only 25% of shares free to be sold immediately, we think Palatir’s stock will behave more like it would in a typical IPO.

The scarcity of shares due to the lockup will prevent the stock from falling as much as we saw in the Slack example (40% fall), until the share unlock in January when the stock price will likely take another leg down until the equilibrium price is reached.

PALANTIR WORTH $9-$12/SH BASED ON PRIVATE TRADES BUT WILL OPEN 50%-75% HIGHER.

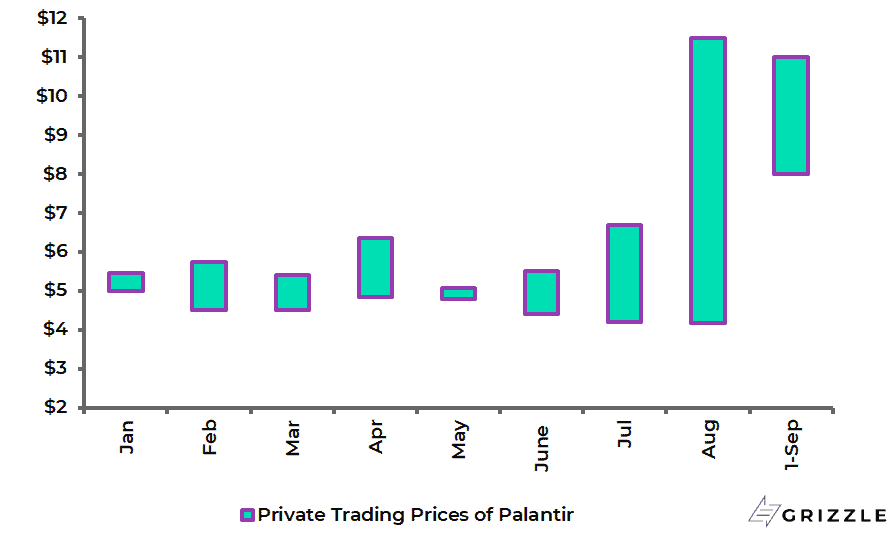

Palantir’s recent private transactions will set the tone for how high the stock trades on its first day.

Looking at private transactions over the past nine months we see a big increase in the value investors are willing to pay leading up to the direct listing.

Palantir stock traded for as much as $11.50/sh in late August and this will likely serve at the “reference price” for the stock on day 1.

RECENT PRIVATE TRADING PRICE OF PALANTIR STOCK

Source: Palantir S-1

Palantir’s revenue growth is above average but not best in class and is expected to slow to slightly above 30% next year according to management.

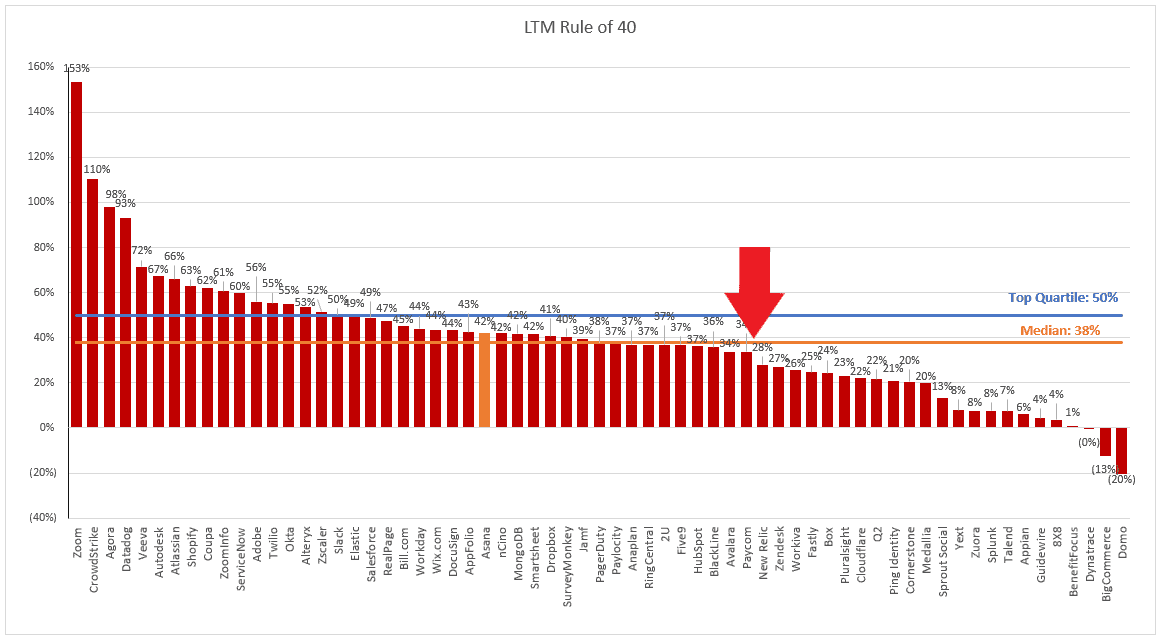

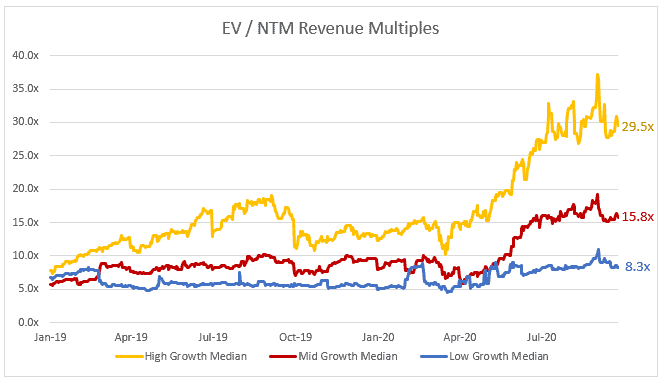

Looking at group multiples, Palantir shouldn’t trade higher than 25x revenue which would still put it firmly in the high-growth valuation bucket even though growth is closer to the Mid-growth bucket.

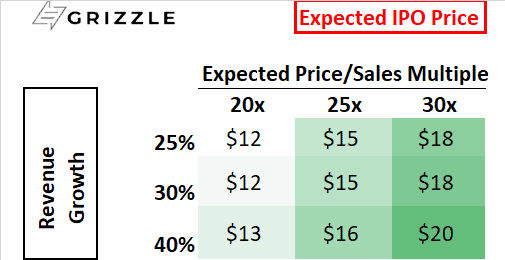

With expected revenue growth of 35% over the next twelve months and our expected revenue multiple of 25x, we think the best case price for Palantir on the first day of trading will be $16-$20/sh.

Where in that range will all depend on how investors are feeling that day, if markets are down, the stock could be on the low end, if markets are green the stock could hit $20.

EXPECTED PRICE RANGE ON DAY 1

Source: Grizzle Estimates

The range of $16-$20 is merely a trading price in the middle of a software bubble and during a period when demand for the stock likely exceeds artificially low supply.

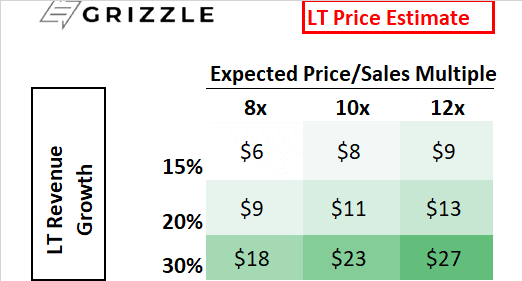

What matters longer-term for investors is what the stock is worth based on the fundamental cashflows of the business.

Here the stock is less compelling if it trades at $16/sh or above.

In the example below, we assume Palantir can keep growth steady at an average of 20% a year, which would put it in an elite league with the likes of Amazon, Microsoft, Salesforce, Adobe and other tech juggernauts.

This is a bullish forecast for a stock that was growing below 20% in 2017 and 2018.

Assuming a price to sales multiple of 8x-12x, in line with the long-term industry average and taking into account slower growth, Palantir isn’t worth more than $16.

Don’t forget that investors were valuing Palantir below $6.50/sh only three months ago and the stock has been at that price in private transactions for almost two years prior.

What has changed to justify a doubling in the value of this company?

Honesty we can’t find anything.

A $16 stock implies good growth, but most importantly significant profits over the next decade, compared to deep losses right now.

For Palantir to offer long term upside for investors who buy above $13/sh, the company will have to grow revenue at a 30% annual rate, or better, for the next 9 years, a heroic outcome based on how the business operates today.

THE FUNDAMENTAL VALUE OF PALANTIR

Source: Grizzle Estimates

Palantir is going to be an expensive stock out of the gate and investors should not be buying within the first six months until after the share unlock or if the stock falls below the reference price of $11.50.

via ZeroHedge News https://ift.tt/33c1m2o Tyler Durden

WTI Rebounds Above $39 After Surprise Crude Draw Tyler Durden

Tue, 09/29/2020 – 16:33

Oil prices tumbled today amid growing concerns of less stimulus and COVID second-wave fears driving expectations for less demand amid rising supply (overwhelming any Armenia-regional war premia). WTI tumbled back below $40 intraday.

“If they were to put new restrictions on areas of New York, that would surprise the market a little bit and knock it down,” said Michael Hiley, head of over-the-counter energy trading at New York-based LPS Futures.

Last week’s surprisingly large draws in gasoline and distillates will be closely watched this week…

API

Crude -831k (+1.9mm exp)

Cushing +1.61mm

Gasoline +1.623mm (-1.3mm exp)

Distillates -3.424mm (-1.7mm exp)

Another surprise crude draw last week according to API data but a surprise gasoline product build offset some of the excitement…

Source: Bloomberg

The sell-off in equities, “which have been propping up oil prices recently, is exposing the oil markets’ weak fundamental backdrop,” said Ryan Fitzmaurice, commodities strategist at Rabobank.

The Covid-19 situation continues to weigh on the market, as “Europe has seen notable uptick in virus cases recently and even New York has seen cases rise just ahead of the start of the scheduled indoor dining restart tomorrow.”

WTI was hovering around $39 ahead of the API data and bounced modestly on the data…

We do note that the clashes between Armenia and Azerbaijan have “kept markets on edge,” as an escalation in the conflict “could affect oil and gas exports from Azerbaijan,” said analysts at ICICI Bank.

Amid all this, Bloomberg reports that the chorus of downbeat oil demand predictions continued to grow. Three of the world’s biggest independent oil traders said consumption won’t meaningfully recover for at least another 18 months. That comes as Total SE said demand growth will end around 2030 and Pierre Andurand, chief investment officer and founder of Andurand Capital Management LLP, called for demand to peak in 2026.

via ZeroHedge News https://ift.tt/344tvry Tyler Durden

Although the results of a nationwide antibody study by the Centers for Disease Control and Prevention (CDC) have not been published yet, the initial findings reportedly indicate that less than 10 percent of the U.S. population has been infected by the COVID-19 virus. “The preliminary results on the first round show that a majority of our nation—more than 90 percent of the population—remains susceptible,” CDC Director Robert Redfield said during congressional testimony last week.

That finding is roughly consistent with the CDC’s most recent “best estimate,” based on studies of the epidemic’s impact in other countries, that the overall COVID-19 infection fatality rate (IFR)—the share of Americans infected by the virus who will die as a result—is about 0.65 percent. According to Worldometer’s tally, the current death toll in the United States is about 210,000. The CDC’s IFR estimate therefore implies that around 32 million Americans, a bit less than 10 percent of the U.S. population, have been infected.

Assuming that the CDC’s nationwide IFR estimate proves to be about right, there are still a couple of important complications. Regional antibody studies by the CDC, using blood drawn for routine tests unrelated to COVID-19, suggest that the IFR varies widely from one part of the country to another—from 0.1 percent in Utah to 1.4 percent in Connecticut as of early May, for example. Recent CDC estimates indicate that the IFR also varies dramatically by age—from 0.003 percent among people 19 or younger to 5.4 percent among people in their 70s.

According to those “best estimates,” which were published this month as an update to the CDC’s COVID-19 Planning Scenarios, the IFR is 0.02 percent for 20-to-49-year-olds and 0.5 percent for 50-to-69-year-olds. The CDC did not include an IFR estimate for people 80 or older. But judging from crude case fatality rates (deaths divided by confirmed cases), the IFR for people in that age group would be substantially higher than 5.4 percent.

The CDC’s latest death counts indicate that the crude case fatality rate is around 28 percent for patients 85 or older and 18 percent for 75-to-84-year-olds. That rate falls to about 8 percent for 65-to-74-year-olds, 2 percent for 50-to-64-year-olds, 0.6 percent for patients in their 40s, 0.2 percent for patients in their 30s, 0.06 percent for patients in their late teens and early 20s, 0.02 percent for 5-to-17-year-olds, and 0.04 percent for children 4 and younger.

The CDC’s overall IFR estimate implies that COVID-19, while not nearly as lethal as many people initially feared, is about six times as deadly as the seasonal flu. But as with the flu, the risk is highest for the elderly, and the difference in the case of COVID-19 is huge. The estimated IFR for people in their 70s is 11 times the rate for 50-to-69-year-olds, 270 times the rate for 20-to-49-year-olds, and 1,800 times the rate for people younger than 20. In the latter two groups, the estimated IFR is lower than the overall IFR for the seasonal flu.

If the CDC’s estimates are in the right ballpark, they still do not settle the ongoing debate about how best to protect people in high-risk groups: through broad restrictions that aim to reduce virus transmission or more targeted measures that try to insulate older, less healthy individuals from the epidemic until effective vaccines can be deployed. But the stark differences reflected in age-specific fatality rates clarify what the main goal of government policy and private precautions should be.

from Latest – Reason.com https://ift.tt/3l1b9hM

via IFTTT

“I am sorry for the hurt, sadness, frustration, fatigue, exhaustion and pain this article has caused anyone, but specifically Black students in the higher education community and beyond,” writes the Ohio State University professor. “I am struggling to find the words to communicate the deep ache for the damage I have done.”

Yet finds them he does—in a lengthy article for Inside Higher Ed so hyperbolic and servile in tone that it verges on parody. Indeed, I emailed the professor to confirm that his apology was sincere; he did not respond to a request for comment. Perhaps he is busy with the “long process of antiracist learning” that he has pledged to undertake.

“I am designing a plan for change, for turning the ‘I am sorry’ to ‘I will change’—for moving Black Lives Matter from a motto to a pathway from ignorance and toward authentic advocacy,” Mayhew writes. “To do this, a colleague of mine asked me to center the question: What can I do to unlearn patterns that hurt and harm Black communities and other communities of color? My center is as a learner, so movement for me will involve unlearning and relearning by listening, reading, dialoguing, reflecting and writing as a means for increasing my awareness and knowledge about systemic racism and the experiences of people of color and people who hold marginalized identities different from my own.”

At this point, you’re probably curious about what crime Mayhew committed. You’re thinking, at the very least, this guy wore a heck of a lot of blackface 30 years ago.

Mayhew’s transgression is this: Last week, he penned an article for Inside Higher Ed titled “Why America Needs College Football.” It made the apparently controversial, venomously hateful, and insidiously racist claim that Football Is Good:

As college campuses attempt to find a new normal suitable for the COVID-19 realities, college athletics, especially college football, have garnered much attention. Debates continue about whether players should be required to play this fall season. Although many people have been outspoken about the financial and health ramifications of allowing—or requiring—players to gear up, few, if any, have addressed the essential role that college football may play toward healing a democracy made more fragile by disease, racial unrest and a contested presidential election cycle.

Essentializing college football might help get us through these uncharacteristically difficult times of great isolation, division and uncertainty. Indeed, college football holds a special bipartisan place in the American heart.

Mayhew’s piece—co-authored with a graduate student named Musbah Shaheen, who has YET TO ATONE as far as I can tell—is too bland and mawkish for my tastes. It’s filled with platitudes about how we may root for different teams, but deep down, blah blah, you get the idea. There’s little in the way of original analysis or research here. Criticizing the piece is perfectly fine.

It’s also true that the college football industry does not always put players first; that black athletes face unique challenges, including in terms of their health, and especially during the COVID-19 pandemic; and that the college athletics industry too often renders education a secondary mission of universities. In light of all that, I would accept Mayhew’s piece as a tad naive, or out of its depths.

But his apology goes well beyond that:

I learned that I could have titled the piece “Why America Needs Black Athletes.” I learned that Black men putting their bodies on the line for my enjoyment is inspired and maintained by my uninformed and disconnected whiteness and, as written in my previous article, positions student athletes as white property. I have learned that I placed the onus of responsibility for democratic healing on Black communities whose very lives are in danger every single day and that this notion of “democratic healing” is especially problematic since the Black community can’t benefit from ideals they can’t access. I have learned that words like “distraction” and “cheer” erase the present painful moments within the nation and especially the Black community.

More:

I am just beginning to understand how I have harmed communities of color with my words. I am learning that my words—my uninformed, careless words—often express an ideology wrought in whiteness and privilege. I am learning that my commitment to diversity has been performative, ignoring the pain the Black community and other communities of color have endured in this country. I am learning that I am not as knowledgeable as I thought I was, not as antiracist that thought I was, not as careful as I thought I was. For all of these, I sincerely apologize.

Even more:

I know it’s not anyone’s job to forgive me, but I ask for it—another burden of a white person haunted by his ignorance. To consider the possible hurt I have played a role in, the scores of others whose pain I didn’t fully see, aches inside me—a feeling different and deeper than the tears and emotions I’ve experienced being caught in an ignorant racist moment.

And those are just the highlights! Mayhew even thanks three academics who had evidently called him out initially for helping him come to terms with his racism.

“I know they are taking a risk by partnering with me on this pathway,” he writes, sounding very much like Winston Smith after a visit to Room 101. “I know that they are carrying a burden by even taking any time with me. I want to thank them.”

Is this real? Are James Lindsay, Helen Pluckrose, and Peter Boghossian up to their old tricks again? Can a person really be this sorry for… um… liking football?

Mayhew is a real person, according to OSU’s website. I emailed him to confirm that the apology is sincere. “Were you held hostage while you were writing it?” I asked. “Blink twice if this is actually you.” Alas, he did not respond.

On Twitter, New York magazine’s Jonathan Chait notes that such a dramatic public apology is obviously weird and bad. “The obsequious tone of the groveling should be a red flag that there’s something seriously awry with this mode of discussion,” says Chait.

Indeed, I find it odd that Inside HigherEd‘s editors published it. Maybe they, too, are sorry. So very sorry.

from Latest – Reason.com https://ift.tt/2HxBtBN

via IFTTT

Democrats Ro Khanna (Calif.), Don Beyer (Va.) and Joe Kennedy III (Mass.) unveiled the bill, the Supreme Court Term Limits and Regular Appointments Act, on Friday. If passed, the act would institute regular appointments to the Supreme Court every two years, with new justices serving for nonrenewable 18-year terms. After 18 years, appointees would become “senior justices” able to temporarily rejoin the court in the event of an unexpected vacancy. Although the current eight justices would be exempted, the two-year appointment cycle would take effect immediately, without waiting for them to retire.

For reasons outlined here, I very much support the idea of term limits for SCOTUS justices (see also Steve Calabresi’s recent NY Times column defending them). But enacting them by statute is both unconstitutional and likely to set a dangerous precedent. Legal scholar Michael Ramsey has an excellent discussion of the constitutional problems at the Originalism Blog:

The consensus of legal scholars seems to be that this is unconstitutional if done by statute. I’d like to be a contrarian and say otherwise, but I can’t. Indeed, I think this is another example…. where the Constitution’s text is clear, if read carefully and without a view to evasion.

Article III, Section 1 provides:

The judicial Power of the United States, shall be vested in one supreme Court, and in such inferior Courts as the Congress may from time to time ordain and establish. The Judges, both of the supreme and inferior Courts, shall hold their Offices during good Behaviour…

I’ll assume here that the “good Behavior” standard means the judges hold their offices for life unless impeached and removed under Article II, Section 4…. So, as a starting point, a simple term-of-years for Supreme Court Justices is a constitutional non-starter.

The Khanna et al. proposal apparently tries to get around that restriction by redefining the “office” of Supreme Court Justice as hearing cases for 18 years (I’ll call it phase 1) and then serving as a backup “senior Justice” in case of temporary vacancies (phase 2). Rotating from phase 1 to phase 2 wouldn’t be a removal from office, it is argued, because the office, by definition, includes both phases of service.

This doesn’t work for me. Article III, Section 1 creates “Offices” of “Judges … of the supreme and inferior Courts.” Necessarily, holding the “Office” of judge of the supreme Court means acting in a judicial capacity as a member of the supreme Court, not simply having the title and filling in occasionally. This constitutionally defined office can’t be redefined by statute to mean the office of acting in a judicial capacity as a member of the supreme Court for a while and then doing something else for the balance of one’s tenure. (Otherwise, Congress could define the “Office” of Supreme Court Justice as serving as a Justice for 5 years and then serving as dogcatcher in East Outback, Alaska, for the rest of the time). And Article III, Section 1 goes on to say that the judges shall hold “their Offices”—that is, their offices as members of the Supreme Court—during good behaviour.

Ramsey’s critique implicitly highlights a possible negative consequence of assuming Congress has the power to impose term limits by statute: If Congress can impose an 18 year term limit, they can also impose much shorter ones, such as five year limit or a two year limit. That would make it easy for any party that controls both Congress and the White House to get rid of justices whose rulings they dislike, and replace them with more supportive jurists. And if Congress can impose term limits on all justices, they can also selectively impose them on specific justices it especially wants to get rid of, while leaving the others alone. For example, if a Democratic Congress wished to get rid of Gorsuch, Kavanaugh, or Amy Coney Barrett (assuming she gets confirmed), they could pass a law imposing very short terms on justices appointed in 2017, 2018, and 2020, respectively. Republicans could use similar tactics to target liberal justices who might otherwise become thorns in their side.

One can argue that politicians would be prevented from doing such things by political norms. But, as we have all seen in recent years, norms have a way of fraying and even collapsing in times of intense polarization. If you’re a Democrat, would you really trust Republicans to follow norms on this issue, when it becomes inconvenient for them to do so? If you’re a Republican, would you trust the Democrats to do the same?

I’m not suggesting that the Khanna proposal is itself motivated by such partisan calculations. To the contrary, I think he and his co-sponsors are acting in good faith. One indication is that they exempt current justices from the term limits, thus making it impossible to use the bill to get rid of current conservative justices liberals dislike. In theory, Amy Coney Barrett might be subject to the term limits if the Khanna bill passes before she gets confirmed. But in practice, such a scenario is highly unlikely.

But once it is generally accepted that Congress has the power to impose term limits on Supreme Court justices by creative redefinition of the office, that power can be also used in less scrupulous ways. And such tactics are likely to be attractive to politicians seeking partisan advantage.

And most politicians not exactly known for their principled adherence to inconvenient norms. The recent history of Supreme Court nominations and other judicial nomination battles shows that most aren’t even willing to stick to normsthey themselves embraced just a few years ago. Democrats and Republicans have repeatedly jettisoned their own professed principles on such matters as whether the Senate should consider nominations for vacancies that arise during an election year, whether it is appropriate to filibuster judicial nominees, whether senators can legitimately oppose nominees based on ideological considerations, and so on. The GOP’s egregious recent flip flop relative to their 2016 positions is just the latest in a long string of “hardball” tactics deployed in the ongoing political battle over judicial nominations.

By all means, adopt term limits for Supreme Court justices. But let’s do it by constitutional amendment. That is both the legally correct path, and the one less likely to create a dangerous slippery slope.

I criticized statutory term limits and related “rotation” proposals for Supreme Court justices in greater detail here and here.

from Latest – Reason.com https://ift.tt/2GkvaB0

via IFTTT

The New York Times on Sunday caused a stir with their report on President Donald Trump’s tax liability, or lack thereof. The analysis notes that Trump, whose net worth is estimated at $2.5 billion, “paid no income taxes at all in 10 of the previous 15 years,” and paid only $750 in both 2016 and 2017.

The story will likely come up during tonight’s presidential debate, and the consensus among the media and liberals broadly is that this is yet more evidence of Trump’s sketchy behavior. But focusing on Trump’s approach to reducing the amount he owes in taxes misses the larger point, which is that Trump’s returns are merely a symptom of a complex tax system that incentivizes filers to sniff out every legal strategy for reducing their tax burdens.

For context, let’s begin with Trump’s business model, which goes something like this: Launch several businesses, many of which hemorrhage millions of dollars each year, and use the publicity from those businesses to make money on personal branding. The latter is highly profitable, earning Trump $427.4 million between 2004-2018. The losses from the former—his hotels and resorts for instance—are then used to largely offset his tax liability.

The Times’ report does erode the savvy businessman brand Trump has sought to cultivate for himself, both commercially and as a candidate for office. The president is not necessarily the astute entrepreneur he claims to be, though he may be uniquely skilled at making money by wasting money. His most high-profile business successes—his golf courses—have reportedly lost $315 million since 2000. The Trump International Hotel in Washington, D.C., just opened in 2016, has already lost $55 million, both numbers according to the Times.

Losing money for a living is certainly an unorthodox business model, but that doesn’t make it illegal.

Trump’s deductions don’t stop there, however. There’s also the $9.7 million tax credit Trump claimed to renovate the Old Post Office building in Washington, D.C., which would later become the aforementioned Trump hotel. That fell under the historic preservation tax clause, an entirely legal tax incentive meant to encourage the redevelopment of old structures.

It could be legally problematic, or just another revealing symptom of U.S. tax law, that Trump has claimed millions of dollars in unspecified consulting fees on various business projects, which typically amounted to 20 percent of his income, according to the Times. Ivanka Trump was allegedly the recipient of hundreds of thousands of dollars in such consulting fees. The president also declared $1.4 billion in business losses in 2008 and 2009. An IRS audit is ongoing.

“Any good tax lawyer or accountant will give options to their client. Some of them will be clearly legal, clearly allowable,” says Joseph Bishop-Henchman, Vice President of Policy & Litigation at the National Taxpayers Union Foundation. “And then there’s gray area stuff,” he continues, noting that the “payments to the [Trump] kids,” as well as the $1.4 billion backward-looking net operating loss, may be a stretch.

It is also true that the wealthy almost always pay a hefty tax bill. Someone of Trump’s worth, that is, a person in the top 1 percent of all earners, would usually shell out more than a third of his income in taxes.

But as Bishop-Henchman reminds us, much of the behavior outlined by the Times report is not only legal but was enshrined by our lawmakers to encourage certain behaviors. He mentions the tax credits Trump received for the Old Post Office building renovation: “Congress wrote that law, and they made it available,” he says. “And it’s been on the books for 40 years, and it’s been used to rehabilitate tens of thousands of historic properties. When you write stuff on the books, billionaires are going to use it, and they’re going to use it to bring their tax liability down.”

Our tax code, which Bishop-Henchman says was written in the style of a “phone book,” is replete with overly complex rules and regulations meant to influence the public’s economic behavior. Former Vice President Joe Biden is no stranger to this. “I have nothing against Amazon,” he wrote in June of 2019, “but no company pulling in billions of dollars of profits should pay a lower tax rate than firefighters and teachers. We need to reward work, not just wealth.” The tech behemoth paid no federal taxes in 2018 after making use of legal tax incentives established by Congress, of which Biden was a member for 36 years. For example, Amazon invested $22.6 billion in research and development in 2017, something the legislature hopes will spur job creation and economic growth.

“It’s this conflict between we want to use the tax code to incentivize all these things,” says Bishop-Henchman. “And then we get upset when people use them very well.”

from Latest – Reason.com https://ift.tt/36eigzv

via IFTTT

Although the results of a nationwide antibody study by the Centers for Disease Control and Prevention (CDC) have not been published yet, the initial findings reportedly indicate that less than 10 percent of the U.S. population has been infected by the COVID-19 virus. “The preliminary results on the first round show that a majority of our nation—more than 90 percent of the population—remains susceptible,” CDC Director Robert Redfield said during congressional testimony last week.

That finding is roughly consistent with the CDC’s most recent “best estimate,” based on studies of the epidemic’s impact in other countries, that the overall COVID-19 infection fatality rate (IFR)—the share of Americans infected by the virus who will die as a result—is about 0.65 percent. According to Worldometer’s tally, the current death toll in the United States is about 210,000. The CDC’s IFR estimate therefore implies that around 32 million Americans, a bit less than 10 percent of the U.S. population, have been infected.

Assuming that the CDC’s nationwide IFR estimate proves to be about right, there are still a couple of important complications. Regional antibody studies by the CDC, using blood drawn for routine tests unrelated to COVID-19, suggest that the IFR varies widely from one part of the country to another—from 0.1 percent in Utah to 1.4 percent in Connecticut as of early May, for example. Recent CDC estimates indicate that the IFR also varies dramatically by age—from 0.003 percent among people 19 or younger to 5.4 percent among people in their 70s.

According to those “best estimates,” which were published this month as an update to the CDC’s COVID-19 Planning Scenarios, the IFR is 0.02 percent for 20-to-49-year-olds and 0.5 percent for 50-to-69-year-olds. The CDC did not include an IFR estimate for people 80 or older. But judging from crude case fatality rates (deaths divided by confirmed cases), the IFR for people in that age group would be substantially higher than 5.4 percent.

The CDC’s latest death counts indicate that the crude case fatality rate is around 28 percent for patients 85 or older and 18 percent for 75-to-84-year-olds. That rate falls to about 8 percent for 65-to-74-year-olds, 2 percent for 50-to-64-year-olds, 0.6 percent for patients in their 40s, 0.2 percent for patients in their 30s, 0.06 percent for patients in their late teens and early 20s, 0.02 percent for 5-to-17-year-olds, and 0.04 percent for children 4 and younger.

The CDC’s overall IFR estimate implies that COVID-19, while not nearly as lethal as many people initially feared, is about six times as deadly as the seasonal flu. But as with the flu, the risk is highest for the elderly, and the difference in the case of COVID-19 is huge. The estimated IFR for people in their 70s is 11 times the rate for 50-to-69-year-olds, 270 times the rate for 20-to-49-year-olds, and 1,800 times the rate for people younger than 20. In the latter two groups, the estimated IFR is lower than the overall IFR for the seasonal flu.

If the CDC’s estimates are in the right ballpark, they still do not settle the ongoing debate about how best to protect people in high-risk groups: through broad restrictions that aim to reduce virus transmission or more targeted measures that try to insulate older, less healthy individuals from the epidemic until effective vaccines can be deployed. But the stark differences reflected in age-specific fatality rates clarify what the main goal of government policy and private precautions should be.

from Latest – Reason.com https://ift.tt/3l1b9hM

via IFTTT

“I am sorry for the hurt, sadness, frustration, fatigue, exhaustion and pain this article has caused anyone, but specifically Black students in the higher education community and beyond,” writes the Ohio State University professor. “I am struggling to find the words to communicate the deep ache for the damage I have done.”

Yet finds them he does—in a lengthy article for Inside Higher Ed so hyperbolic and servile in tone that it verges on parody. Indeed, I emailed the professor to confirm that his apology was sincere; he did not respond to a request for comment. Perhaps he is busy with the “long process of antiracist learning” that he has pledged to undertake.

“I am designing a plan for change, for turning the ‘I am sorry’ to ‘I will change’—for moving Black Lives Matter from a motto to a pathway from ignorance and toward authentic advocacy,” Mayhew writes. “To do this, a colleague of mine asked me to center the question: What can I do to unlearn patterns that hurt and harm Black communities and other communities of color? My center is as a learner, so movement for me will involve unlearning and relearning by listening, reading, dialoguing, reflecting and writing as a means for increasing my awareness and knowledge about systemic racism and the experiences of people of color and people who hold marginalized identities different from my own.”

At this point, you’re probably curious about what crime Mayhew committed. You’re thinking, at the very least, this guy wore a heck of a lot of blackface 30 years ago.

Mayhew’s transgression is this: Last week, he penned an article for Inside Higher Ed titled “Why America Needs College Football.” It made the apparently controversial, venomously hateful, and insidiously racist claim that Football Is Good:

As college campuses attempt to find a new normal suitable for the COVID-19 realities, college athletics, especially college football, have garnered much attention. Debates continue about whether players should be required to play this fall season. Although many people have been outspoken about the financial and health ramifications of allowing—or requiring—players to gear up, few, if any, have addressed the essential role that college football may play toward healing a democracy made more fragile by disease, racial unrest and a contested presidential election cycle.

Essentializing college football might help get us through these uncharacteristically difficult times of great isolation, division and uncertainty. Indeed, college football holds a special bipartisan place in the American heart.

Mayhew’s piece—co-authored with a graduate student named Musbah Shaheen, who has YET TO ATONE as far as I can tell—is too bland and mawkish for my tastes. It’s filled with platitudes about how we may root for different teams, but deep down, blah blah, you get the idea. There’s little in the way of original analysis or research here. Criticizing the piece is perfectly fine.

It’s also true that the college football industry does not always put players first; that black athletes face unique challenges, including in terms of their health, and especially during the COVID-19 pandemic; and that the college athletics industry too often renders education a secondary mission of universities. In light of all that, I would accept Mayhew’s piece as a tad naive, or out of its depths.

But his apology goes well beyond that:

I learned that I could have titled the piece “Why America Needs Black Athletes.” I learned that Black men putting their bodies on the line for my enjoyment is inspired and maintained by my uninformed and disconnected whiteness and, as written in my previous article, positions student athletes as white property. I have learned that I placed the onus of responsibility for democratic healing on Black communities whose very lives are in danger every single day and that this notion of “democratic healing” is especially problematic since the Black community can’t benefit from ideals they can’t access. I have learned that words like “distraction” and “cheer” erase the present painful moments within the nation and especially the Black community.

More:

I am just beginning to understand how I have harmed communities of color with my words. I am learning that my words—my uninformed, careless words—often express an ideology wrought in whiteness and privilege. I am learning that my commitment to diversity has been performative, ignoring the pain the Black community and other communities of color have endured in this country. I am learning that I am not as knowledgeable as I thought I was, not as antiracist that thought I was, not as careful as I thought I was. For all of these, I sincerely apologize.

Even more:

I know it’s not anyone’s job to forgive me, but I ask for it—another burden of a white person haunted by his ignorance. To consider the possible hurt I have played a role in, the scores of others whose pain I didn’t fully see, aches inside me—a feeling different and deeper than the tears and emotions I’ve experienced being caught in an ignorant racist moment.

And those are just the highlights! Mayhew even thanks three academics who had evidently called him out initially for helping him come to terms with his racism.

“I know they are taking a risk by partnering with me on this pathway,” he writes, sounding very much like Winston Smith after a visit to Room 101. “I know that they are carrying a burden by even taking any time with me. I want to thank them.”

Is this real? Are James Lindsay, Helen Pluckrose, and Peter Boghossian up to their old tricks again? Can a person really be this sorry for… um… liking football?

Mayhew is a real person, according to OSU’s website. I emailed him to confirm that the apology is sincere. “Were you held hostage while you were writing it?” I asked. “Blink twice if this is actually you.” Alas, he did not respond.

On Twitter, New York magazine’s Jonathan Chait notes that such a dramatic public apology is obviously weird and bad. “The obsequious tone of the groveling should be a red flag that there’s something seriously awry with this mode of discussion,” says Chait.

Indeed, I find it odd that Inside HigherEd‘s editors published it. Maybe they, too, are sorry. So very sorry.

from Latest – Reason.com https://ift.tt/2HxBtBN

via IFTTT