S&P Futures roared to new record highs above 4,200 and Nasdaq futures jumped 1% on Thursday as Powell’s dovish assurances and blow-out earnings from Apple and Facebook powered a rally in tech stocks and cemented conviction the world’s largest economy is resurgent ahead of GDP numbers and jobless claims data which are expected to show further improvements. At 7:30 a.m. ET, Dow e-minis were up 130 points, or 0.38%, S&P 500 e-minis were up 28.00 points, or 0.67%, and Nasdaq 100 e-minis were up 144 points, or 1.03%.

Some notable premarket movers:

- Apple gained 2.7% in premarket trading after posting sales and profits ahead of Wall Street estimates, led by much stronger-than-expected iPhone and Mac sales.

- Facebook jumped 7.3% on beating analysts’ expectations for both quarterly revenue and profit, helped by a surge in digital ad spending during the pandemic, along with higher ad prices coupled with a 10% growth in active users.

- Other megacap companies, including Microsoft Corp, Alphabet Inc and Netflix Inc, rose between 0.2% and 1.1%.

- EV companies, including Tesla and Nikola rose 1.1% and 2.6%, respectively, as sales picked up speed in the first quarter, according to the International Energy Agency.

- Caterpillar rose 2.8% after the heavy equipment maker reported a rise in adjusted first-quarter profit.

- Merck slid 3.2% on posting a 1.2% fall in quarterly profit.

With almost half of the S&P 500 companies having reported results so far, about 88% have either met or beaten expectations.

Global shares extended gains after the Federal Reserve said it was too early to consider rolling back emergency support for the economy, and U.S. President Joe Biden proposed a $1.8 trillion stimulus package. On Wednesday, Powell acknowledged the economy’s growth but dismissed worries about price surges or anecdotes of labor shortage, implying the central bank is prepared to run the economy hot for a while; he said there was not yet enough evidence of “substantial further progress” – whatever that means – toward recovery to warrant a change in policy. He also glossed over soaring prices as “transitory.”

“Equities should continue to power higher but there will be bouts of volatility along the way,” Mehvish Ayub, State Street Global Advisors senior investment manager, said on Bloomberg TV. “Yields should continue to trend higher, and this is very much a reflection of better economic prospects so it’s not really a negative for equity markets.”

But while Powell may not be concerned about inflation, the bond market is and the 10-Year TSY yield headed for the biggest weekly increase since March 19, and a key gauge of commodities was on course for the longest daily rally in more than three years.

Reflation trades got a boost after Joe Biden unveiled a $1.8 trillion spending plan targeted at American families, adding to the economic optimism.

Europe’s benchmark Stoxx 600 index rose 0.4%, moving closer to a record reached earlier in April. Personal-care shares climbed after Unilever delivered a sales beat and announced a share buyback. Oil giants Total SE and Royal Dutch Shell Plc boosted their sector after reporting better-than-forecast profits. Here are some of the biggest European movers today:

- Unilever shares jump as much as 4%, most since Nov. 25, after the consumer-goods company reported 1Q sales that beat market expectations and announced plans for a share buyback that impressed most analysts.

- Nokia’s shares surged as much as 15% to their best day since getting caught up in a Reddit trader frenzy in January, after results surpassed analyst expectations. Analysts were particularly positive on Nokia’s adjusted gross margin, and were also reassured by the telecom equipment maker maintaining its guidance for 2021 and management pointing toward the higher end of the range.

- Straumann shares jump as much as 10.3% to a record high after the Swiss dental-implant maker reported 1Q sales that Mirabaud says were “super strong,” especially in APAC.

- Airbus shares gain as much as 3.5% in Paris trading and is the day’s best performer on the CAC 40; Bernstein says the company had a strong start to the year, with 1Q results better than expected on all key metrics.

- WH Smith shares fall as much as 5.8% after the U.K. retailer issued convertible bonds. Separately, its 1H results are better than expected, driven by a good performance in its high street business, RBC (outperform) writes in a note.

Earlier in the session, Asian stocks rose and were set for a second day of gains, with the MSCI Asia Pacific Index rising 0.3% led by material and energy shares, as investors cheered Joe Biden’s ambitious spending plans and buoyant earnings from U.S. tech giants like Apple. China stocks rose for a third session in their longest streak of gains this month, on the back of solid first-quarter earnings growth by financial and consumer staples companies. The CSI 300 Index gained 0.9%, while Hong Kong’s Hang Seng rose 0.8%. India’s S&P BSE Sensex Index pared an advance of as much as 1.3% and traded little changed as the South Asian country continued to report record daily coronavirus cases. The nation’s biggest conglomerates and global giants such as Amazon.com Inc. stepped in to help ease the country’s pandemic-induced crisis. Overall, the MSCI Asia Pacific Index rose 0.3% led by material and energy shares, getting a boost from Biden’s promise of tax increases on the wealthy to pay for plans to spend trillions of dollars on infrastructure, education and other Democratic priorities. Biden’s address to a joint session of Congress on Wednesday came after the Fed upgraded its assessment of the U.S. economy but said it was not ready to consider scaling back pandemic support. “I didn’t expect the degree to which Biden will embark on this incredible spending program,” Mark Mobius, co-founder of Mobius Capital Partners told Bloomberg Television. The spending plan will benefit global markets, he added, because it means the U.S. will be importing more and there are “opportunities for more exports” from China and India. Asian markets got a lift earlier this morning on a slew of tech earnings. Apple Inc. crushed revenue estimates and Facebook Inc. reported increases in sales and users. However, shares of Samsung Electronics and its suppliers fell even though South Korea’s largest company reported a better-than-forecast first quarter profit. Markets in Japan and Malaysia were closed on account of local holidays

In rates, Treasury futures traded near lows of the day heading into early U.S. session as post-FOMC gains are unwound. Yields were higher by nearly 4bps across intermediates, steepening 2s10s by 3.5bp, 2s5s by 2.5bp; 10-year around 1.65% underperforms bunds by ~2bp, gilts by ~1bp. Most of the move occurred when cash trading — closed in Asia as Japan’s Golden Week holiday begins — resumed in London. Volume light in both futures and cash. S&P 500 futures’ advance to record above 4200 and USD/JPY strength also weigh on Treasuries. Treasuries bull steepened on Wednesday, with markets showing a modest dovish repricing after Fed Chair Powell reiterated the central bank’s commitment to asset purchases while the economy is recovering.

In FX, the Bloomberg Dollar Spot Index edged up and the greenback advanced versus most of its Group-of-10 peers; the euro retreated after rising to a fresh one-month high of $1.2150. The pound advanced to the highest in over a week before paring gains; sterling was still among the top G-10 performers. Sweden’s krona largely ignored better-than-forecast economic tendency survey and GDP data out of the Nordic nation while Norway’s krone fell for the first day in five; the Scandinavian currencies are still set to be the best G-10 performers this month. The Australian dollar swung to a loss after rising as much as 0.4% earlier as U.S. President Joe Biden’s speech disappointed some traders betting on an additional stimulus announcement; bonds firmed into the central bank’s purchases in the 7-10 year sector.

In commodities, crude oil extended gains on a confident outlook on demand from OPEC and its allies, despite the threat from India’s Covid-19 crisis. The Bloomberg Commodity Index increased for a ninth day, nearing a three-year high on a closing basis.

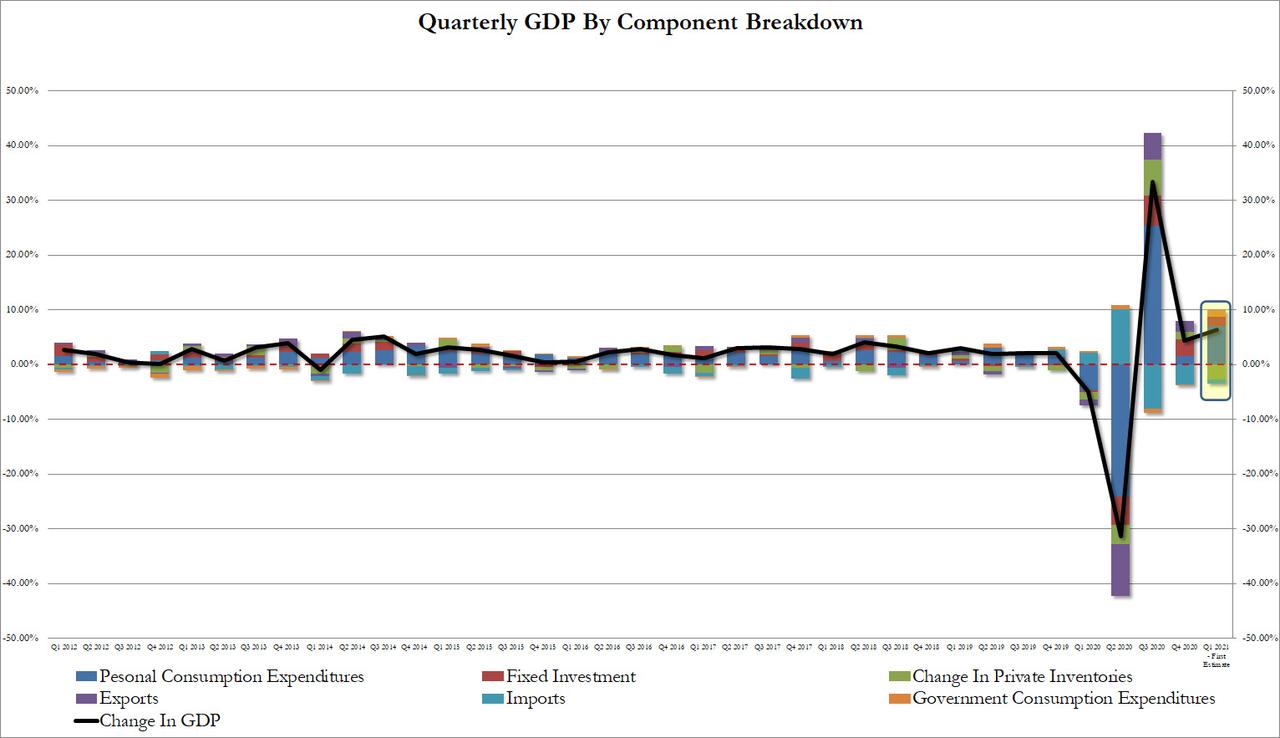

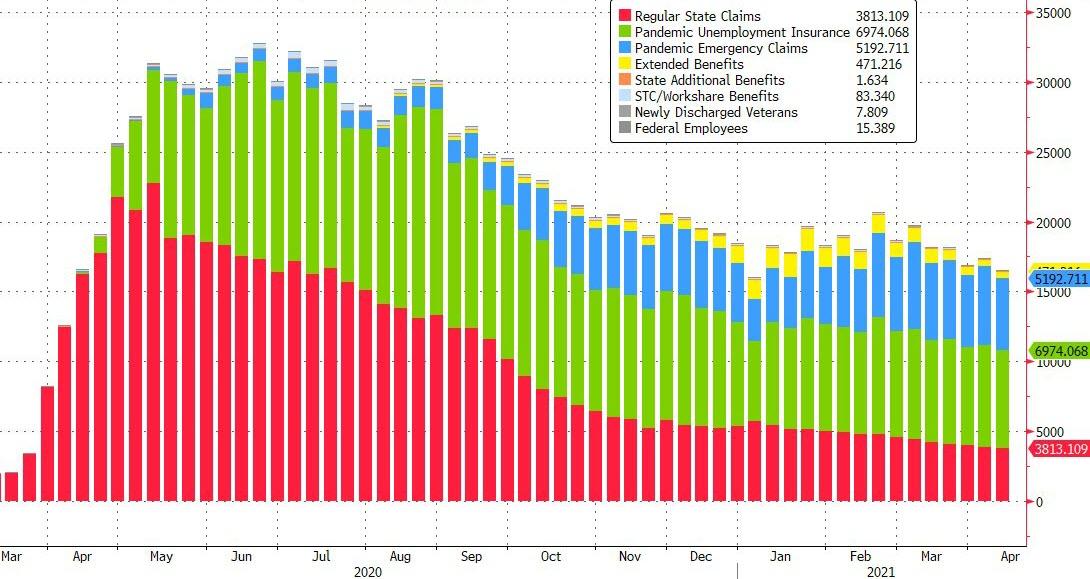

Looking at today’s calendar, we’ll get a fresh round of earnings releases with the highlights including Amazon, Mastercard, Comcast, Merck, Thermo Fisher Scientific, McDonald’s, Bristol Myers Squibb, Caterpillar, American Tower and Twitter. On the data front, we’ll get the advance estimate of Q1 GDP in the US, as well as the weekly initial jobless claims and March’s pending home sales. In Europe, we’ll get the change in German unemployment for April and the country’s preliminary CPI reading for that month, on top of the final Euro Area consumer confidence reading for April. Central bank speakers include Fed Vice Chair Quarles, ECB Vice President de Guindos, and the ECB’s Elderson and Holzmann.

Market Snapshot

- S&P 500 futures up 0.6% to 4,202.00

- STOXX Europe 600 rose 0.3% to 441.25

- MXAP up 0.3% to 209.16

- MXAPJ up 0.4% to 706.99

- Nikkei up 0.2% to 29,053.97

- Topix up 0.3% to 1,909.06

- Hang Seng Index up 0.8% to 29,303.26

- Shanghai Composite up 0.5% to 3,474.90

- Sensex little changed at 49,765.82

- Australia S&P/ASX 200 up 0.2% to 7,082.28

- Kospi down 0.2% to 3,174.07

- Brent Futures up 0.89% to $67.87/bbl

- Gold spot down 0.25% to $1,777.20

- U.S. Dollar Index up 0.06% to 90.663

- German 10Y yield rose 1.2 bps to -0.219%

- Euro down 0.03% to $1.2122

Top Overnight News from Bloomberg

- Forty years ago, President Ronald Reagan and Federal Reserve Chairman Paul Volcker oversaw a root-and-branch restructuring of the U.S. economy. Today, Joe Biden and Jerome Powell are trying to do the same thing — only in reverse. In the Reagan-Volcker regime change, power in the economy shifted from the government to the market and from labor to the owners of capital. The emphasis was on efficiency, not equality, and on promoting supply, not demand

- China said its population increased in 2020, countering concerns that its upcoming census will show a possible decline as the nation ages rapidly

- German unemployment unexpectedly rose in April, signaling that the labor market is experiencing strains from lockdown restrictions that have been tightened

- The retreat in Treasury yields this month has revived demand for emerging-market carry trades with China and South Korea bonds looking among the most attractive targets in Asia

Quick look at global markets courtesy of Newsquawk

Asian equity markets traded positively in reaction to the continued dovish tone from the FOMC and beat on earnings amongst the tech giants including Apple, Facebook and Qualcomm. In addition, focus was also on President Biden’s first address to a joint session of Congress where he stated America is on the move again and that the American Jobs Plan is a blue-collar blueprint to build America, while he called on Congress to pass the USD 15/hour minimum wage and extend child tax credit through at least end-2025, as well as outlined the American Families Plan. This facilitated a continued upside in US equity futures to push the Emini S&P to a record high and briefly above the 4,200 level although gains for Asia bourses were tempered amid a heavy slate of earnings and with Japanese participants absent due to a holiday closure. ASX 200 (+0.3%) was positive with outperformance in gold miners amid a rebound in the precious metal in the aftermath of the dovish FOMC, but with gains in the index capped by losses in consumer stocks after weaker quarterly sales from Woolworths and with Treasury Wine Estates dampened by a 4% decline of Australian wine exports in the year to end-March. KOSPI (-0.2%) benefitted initially as its top constituent Samsung Electronics remained afloat following its final Q1 earnings results which topped forecasts for net profit and posted a slight increase in revenue from the preliminary. Hang Seng (+0.8%) and Shanghai Comp. (+0.5%) also gained with sentiment encouraged by earnings releases including China’s largest oil company Sinopec and big 4 bank China Construction Bank.

Top Asian News

- China Says Population Grew in 2020, Rebutting Report of Drop

- Singapore Finds 16 New Coronavirus Cases in Wider Community

- China Huarong Leaves Rating Firms Guessing on State Support (1)

- India’s RBI May be Augmenting its T-Bill Holdings, Traders Say

Major bourses in Europe, for the most part, see gains (Euro Stoxx 50 +0.3%) although to varying degrees as earnings take the driving seat with the FOMC meeting and Biden’s speech are out of the way and heading into month-end. US equity futures meanwhile remain elevated with the NQ (+1.0%) leading the gains whilst its peers see broad-based upside. Heading into month-end, JPM forecasts balanced mutual funds to sell some USD 30bln of equity, although, by historical portfolio rebalancing standards, this is quite modest. Back in Europe, the AEX (+0.9%) narrowly outperforms among the majors as the index is propped up by heavyweights Unilever (+3.0%) and Shell (+2.0%) post-earnings, with the latter beating on the top and bottom lines whilst increasing its dividend. Conversely, the DAX (-0.1%) underperforms as losses in German autos keep gains capped, whilst post-earnings BASF (-1.6%) provides further pressure. Sectors are mostly higher but again it is hard to discern a particular risk tone or theme as idiosyncratic factors are at play. Autos sit at the bottom of the pile amid the ongoing chip shortage coupled with Ford (-2.7% pre-mkt) earnings that were not well received. Telecoms outperform as Nokia (+14%) and Swisscom (+5%) were bolstered following their metrics, whilst further tailwinds are felt from BT (+2.1%) amid reports the Co. is in talks with Amazon, Disney, and others regarding a potential sale of its sports arm. Oil & Gas also see a firm performance amid the numbers from Shell, Total (+1.4%), and Equinor (+3.3%), and against the backdrop of firmer oil prices. Individual movers are largely earning-oriented and include the likes of Lufthansa (-2.5%), Airbus (+2.2%), Standard Chartered (+5.7%), Natwest (-3%), Logitech (+1.3%) and Clariant (-3%).

Top European News

- NatWest Starts to Reverse Covid Provisions as Earnings Beat

- Cboe Opens Derivatives Venue in Amsterdam in Latest Brexit Shift

- Bankinter Bolsters Spanish Insurers With Spinoff

- Total Profit Surges to Pre-Pandemic Levels on Oil Recovery

In FX, the Dollar remains in a clear bear trend following another dovish message from the Fed and Chair Powell in the post-meeting press conference/Q&A, but perhaps there was enough in the latest official statement and assessment to indicate more confidence or less caution about the economic outlook. Indeed, the FOMC no longer deems downside risks to be considerable, upgraded activity levels to strengthening from turning up and acknowledged rising inflation, albeit still mainly due to transitory factors. Meanwhile, US President Biden’s first address to a joint Congress was largely as expected in terms of content and details of the America Families Plan, so no real surprises or reason for the Greenback and markets in general to dwell for too long. Hence, Treasuries have reverted to bear-steepening mode and are providing the Buck with some impetus to pare deeper losses after the DXY slipped to fresh April and cycle lows under 90.500 at 90.422 in the run up to a raft of data before Fed’s Williams appears at the NY Economic Club. The index is currently hovering just shy of a 90.721 recovery high amidst with the Dollar firmer vs most components and major counterparts.

- JPY – Holiday-thinned volumes may well be compounding price action, but the Yen is bearing the brunt of the aforementioned Greenback rebound and yield/curve retracement, as Usd/Jpy retests the 109.00 level vs sub-108.50. However, while Japan observes Showa Day, decent option expiries could keep the headline pair contained before Tokyo CPI, jobs and ip tomorrow given 1.9 bn and 1.3 bn rolling off at 108.50 and 109.00 respectively.

- AUD/NZD/CHF/EUR – Also handing back gains vs their US rival, with the Aussie back under 0.7800 irrespective of an acceleration in Q1 export prices and perhaps more conscious of comments by Treasurer Frydenberg putting a 4% handle on the jobless rate to generate stronger wages and inflation, while predicting that it will take 2 years before returning to full employment. Similarly, no sustained impetus for the Kiwi to reach 0.7300 via improvements in NBNZ business sentiment or the activity outlook after trade data showing an almost flat balance, as Nzd/Usd hovers below 0.7250. Elsewhere, the Franc is now straddling 0.9100 and the Euro has breached key chart resistance in the form of a descending trendline, but hit another obstacle at 1.2150 before waning amidst a barrage of mostly firmer than expected Eurozone data/surveys that should keep Eur/Usd afloat along with 1.1 bn option expiry interest either side of 1.2100 (1.2095-1.2105 specifically).

- GBP/CAD – Relative G10 outperformers, as the Pound rebounds firmly from midweek session lows to straddle 1.3950 vs the Buck and probe 0.8675 against the Euro, though again on little fundamental bar firmer oil prices that are boosting the Loonie around 1.2300 and even loftier multi-year peaks circa 1.2287.

WTI and Brent front month futures continue edging higher in conjunction with the broader sentiment across markets following Powell and Biden’s appearances since the European close yesterday. The upside could also be supported by the overall bullish inventory data seen during the week, whilst eyes remain on India’s situations amid its rampant “double variant”, although the nation is receiving international support. On this note, analysts at ING suggest that Indian refiners are erring towards increased refined product exports in a bid to tackle a domestic glut. “Increased export flows from India are a risk to regional product cracks, with additional supply potentially weighing on them. This is particularly the case, given that refiners in the country so far appear to have made only marginal cuts to run rates.”, the Dutch bank states. WTI resides just around USD 64.75/bbl (vs low USD 63.35/bbl) and Brent hovers sub-USD 67.75/bbl (vs low USD 66.64/bbl). Elsewhere, spot gold and silver are mixed but price action during European trade has been pegged to the Buck, with the former still around the USD 1,775/oz and spot silver just north of USD 26/oz. Turning to base metals, LME copper remains firm after testing but failing to breach USD 10,000/t to the upside, with overnight prices again experiencing upside as Chinese players entered the market. LME nickel meanwhile topped the USD 17,000/t mark yesterday with some citing restocking ahead of the Chinese labour day holiday between May 1st and 5th.

US Event Calendar

- 8:30am: 1Q GDP Annualized QoQ, est. 6.6%, prior 4.3%;

- Personal Consumption, est. 10.5%, prior 2.3%

- PCE Core QoQ, est. 2.4%, prior 1.3%

- 8:30am: April Initial Jobless Claims, est. 540,000, prior 547,000; Continuing Claims, est. 3.59m, prior 3.67m

- 9:45am: April Langer Consumer Comfort, prior 54.2

- 10am: March Pending Home Sales YoY, est. 27.5%, prior -2.7%; Pending Home Sales (MoM), est. 4.4%, prior -10.6%

DB’s Jim Reid concludes the overnight wrap

The main event yesterday was the Federal Reserve meeting in the US, where expectations were low for there being much new information. The FOMC did announce upgraded forecasts for the US economy though, and Chair Powell noted in the ensuing press conference that “amid progress on vaccinations and strong policy support, indicators of economic activity and employment have strengthened.” However the FOMC kept both the pace of asset purchases and its key interest rate unchanged, with no change to the forward guidance. Powell softened some language and acknowledged that the recovery has been faster than previously expected but that “it remains uneven and far from complete” and that he viewed the economy as “a long way from our goals.” He once again noted that inflation metrics would be higher in coming months but that it remains a “largely” a transitory phenomenon. For more see our US economists report here.

The market was very steady going into the Fed announcement. The S&P was trading within a 13.3pt (0.3%) range before finishing slightly lower on the day (-0.08%) after gaining as much as +0.35% at the intraday highs which were reached at the beginning of the Powell presser. That marginal loss left the S&P just off its record levels, though cyclicals such as energy (+3.35%), retailing (+0.56%) and banks (+0.47%) continued to lead the index. Yields on US treasuries retreated to the lows of the day after being as much as +2.9bps higher just prior to the FOMC release. Afterward the FOMC announcement, they rallied through the rest of the US afternoon with 10yr yields finishing the day down -1.2bps at 1.609%. The fall in yields was driven by real yields (-2.9bps) falling back, even as inflation expectations rose even further (+1.6bps) with 10yr breakevens at fresh 8 year highs. The dollar index ending the day down -0.33%. Commodities were largely higher with copper (+0.22%), gold (+0.29%), and WTI (+1.46%) all gaining.

Tech shares largely traded lower yesterday with the NASDAQ down -0.28%, but this reversed after the US close, when we saw earnings from Apple and Facebook. Facebook was up +6.2% in after-market trading on a large revenue beat, with reported sales up 47% at $26.17bn (est 23.7bn). Investors seemed to respond well to a strong Q2 guidance and steady user growth. Apple rose +2.3% after the largest public company in the US announced strong revenues, up +54% to $89.6bn (est. $77.3bn). Sales were strong across their suite of products with the company reporting “revenue records in each of our geographic segments and strong double-digit growth in each of our product categories,” in the earning release. Nasdaq futures are now up +0.93%.

Biden delivered his first speech to a joint session of Congress yesterday outlining his plans on infrastructure, education and other party priorities. We actually got the contents of the American Families Plan from the White House ahead of the speech, which is a $1.8tn package that has $1tn in spending and $800bn in tax cuts. Among the measures are free universal pre-school for 3 and 4-year olds, two years of free community college, measures on paid leave and affordable childcare, and an extension of various tax credits. In terms of how they propose to pay for this, it would see the top tax rate go back up to 39.6%, and households earning over $1m would also face the same 39.6% rate on capital gains tax. The president tried to keep much of the focus on the job-making possibilities, especially for those without college degrees. “Nearly 90% of the infrastructure jobs created in the American Jobs Plan don’t require a college degree… and 75% percent do not require an associate’s degree.” President Biden also struck a more hawkish tone against Russia and China, particularly where he sees American interests being at risk – such as election tampering and the South China Sea. S&P futures rose around +0.6% after the start of the speech having already rallied slightly on the stronger tech earnings after the close.

Asian markets are also trading up this morning on the prospect of more stimulus from the US with the Hang Seng (+0.62%), Shanghai Comp (+0.17%), Kospi (+0.16%) and India’s Nifty (+1.04%) all up. Japan’s markets are closed for a holiday. European futures are also pointing to a positive open. Elsewhere, Reuters has reported that China is preparing to fine Tencent as part of its antitrust crackdown on the country’s internet giants. The report added that the fine could be as much as CNY 10bn.

In other news, the global chip shortage is worsening with Honda and BMW joining the growing list of automakers (including Jaguar Land Rover, Volvo and Mistubishi Motors) temporarily pausing production for a few days next month to deal with the crisis. Meanwhile, Ford has gone a step further and reduced its full year earnings guidance due to the shortage and has said that it now sees the shortage extending into next year. Elsewhere, tech giants like Apple and Samsung have also flagged production cuts and lost revenue as a result of the shortage in their earnings releases overnight. Apple’s CFO Maestri warned that supply constraints are crimping sales of iPads and Macs, two products that performed especially well during lockdowns. Maestri added that this will knock $3 bn to $4 bn off revenue during the fiscal third quarter.

Risk assets had performed well in Europe ahead of the Fed, with the DAX (+0.28%), the CAC 40 (+0.53%) and the FTSE 100 (+0.27%) all posting solid gains. The STOXX 600 (+0.02%) lagged behind somewhat thanks to an underperformance in Swedish equities, but still managed to close just shy of its all-time high. Separately, sovereign bond yields outside of the US climbed to their highest level in months, with yields on 10yr bunds up +1.8bps to -0.23%, their highest closing level in over a year, as those on 10yr OATs (+2.0bps) and BTPs (+5.1bps) similarly moved higher.

There wasn’t a great deal of news on the pandemic yesterday, though in New York, Governor Cuomo said that the 12am outdoor dining area curfew for bars and restaurants would be lifted from May 17, and that the 12am indoor curfew would go on May 31. Poland announced an easing of restrictions as well, with shopping malls partially open from May 4 and outdoor dining to recommence on May 15. Meanwhile on the Tokyo Olympics, it was announced that athletes will now be tested on a daily basis, though a decision on whether to have domestic spectators won’t be made until June. Sticking with Japan, the Nikkei has reported overnight that the country is considering making vaccines and medical treatments that have yet to be domestically approved available for emergency use in order to reduce regulatory delays to vaccination as cases are continuing to rise. Elsewhere, the US has issued a level 4 travel advisory for India overnight and have told its citizens to leave India as soon as possible and not to travel there because of the escalating coronavirus crisis. India reported 379k cases and 3645 fatalities over the past 24 hours, marking new record highs.

Here in the UK, yesterday saw the ONS published their latest antibody survey, which found that in England 68% of the adult population had tested positive for antibodies in the week ending April 11, the highest since they began running this survey late last year. The effects of the vaccination drive could be seen through the age breakdowns, as all the groups covering the over-50s had an antibody rate of higher than 80%. See the graph below for the breakdown. There was also late news in the UK that the government had secured a deal with Pfizer and BioNtech for an additional 60 million doses of its vaccine as part of a booster program to protect the most vulnerable ahead of the winter.

To the day ahead now, and we’ll get a fresh round of earnings releases with the highlights including Amazon, Mastercard, Comcast, Merck, Thermo Fisher Scientific, McDonald’s, Bristol Myers Squibb, Caterpillar, American Tower and Twitter. On the data front, we’ll get the advance estimate of Q1 GDP in the US, as well as the weekly initial jobless claims and March’s pending home sales. In Europe, we’ll get the change in German unemployment for April and the country’s preliminary CPI reading for that month, on top of the final Euro Area consumer confidence reading for April. Central bank speakers include Fed Vice Chair Quarles, ECB Vice President de Guindos, and the ECB’s Elderson and Holzmann.