Bullion, Bonds, & Black Gold All Bid As Rate-Cut Hopes Ramp-Up

Inflation down (in Europe) and Growth up (in US) prompted more ‘goldilocks’ narrative calls today.

But, as Goldman’s Chris Hussey pointed out, 3Q GDP is in the rearview mirror, and the implications of the report (and other releases today) for 4Q GDP growth were not good. In fact, Goldman lowered their 4Q23 GDP growth forecast by 50bp to +1.4% today as the October trade and inventory reports – also released today – came in light and gross domestic income rose by only 1.5% in 3Q – well below the pace of GDP.

All of which pushed rate-cut expectations higher again (now 125bps of cuts priced in for 2024)…

Source: Bloomberg

…and the first rate-cut timing has now moved to May from June…

Source: Bloomberg

…and sent Treasury yields even lower on the week (once again led by the short-end, 2Y -9bps, 30Y -6bps)…

Source: Bloomberg

As we noted earlier, November is set to be bonds’ best month since 2008 as 10Y and 30Y Yields are down a stunning 65bps…

Source: Bloomberg

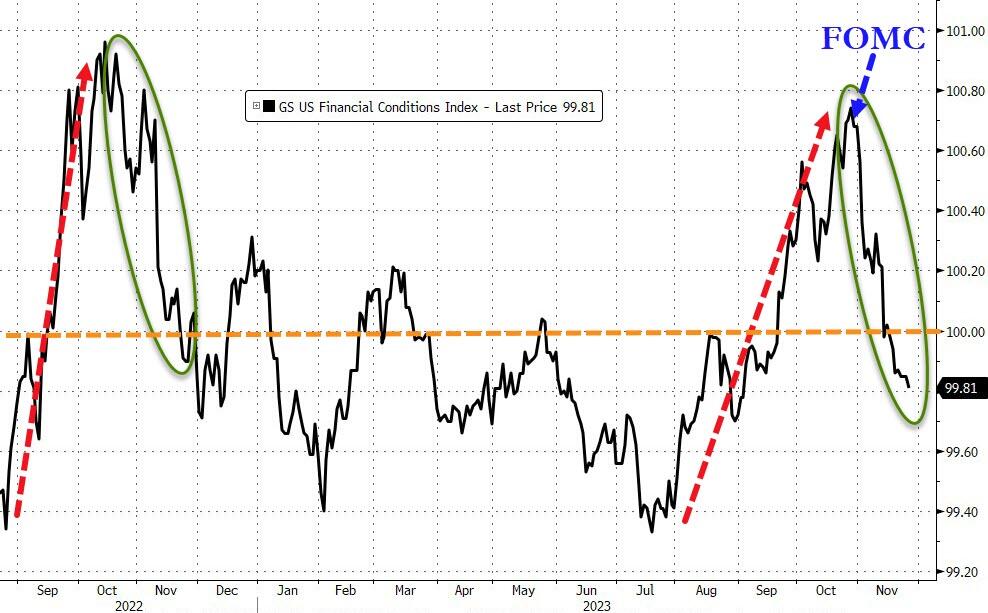

Sadly, The Fed seems completely disconnected and stuck with its old narrative as SF Fed’s Mester proclaimed that “broad tightening in financial conditions is helping curb demand”. That may well have been true until you muppets started jawboning about how “the market is doing The Fed’s job” and that you’re near the end of the cycle. Financial conditions have massively loosened in the last month…

Source: Bloomberg

As stocks remain on pace for their 4th best month in the last 12 years, early gains into the cash open were gradually sold into with Nasdaq and S&P the biggest losers and Small Caps holding on to decnet gains despite late-day selling-pressure (ahead of tomorrow’s PCE)…

‘Most Shorted’ stocks were squeezed again – up to recent resistance – and reversed modestly from there…

Source: Bloomberg

Meme stocks are soaring again as Goldman’s ‘Retail Favorites’ hits a new cycle high…

Source: Bloomberg

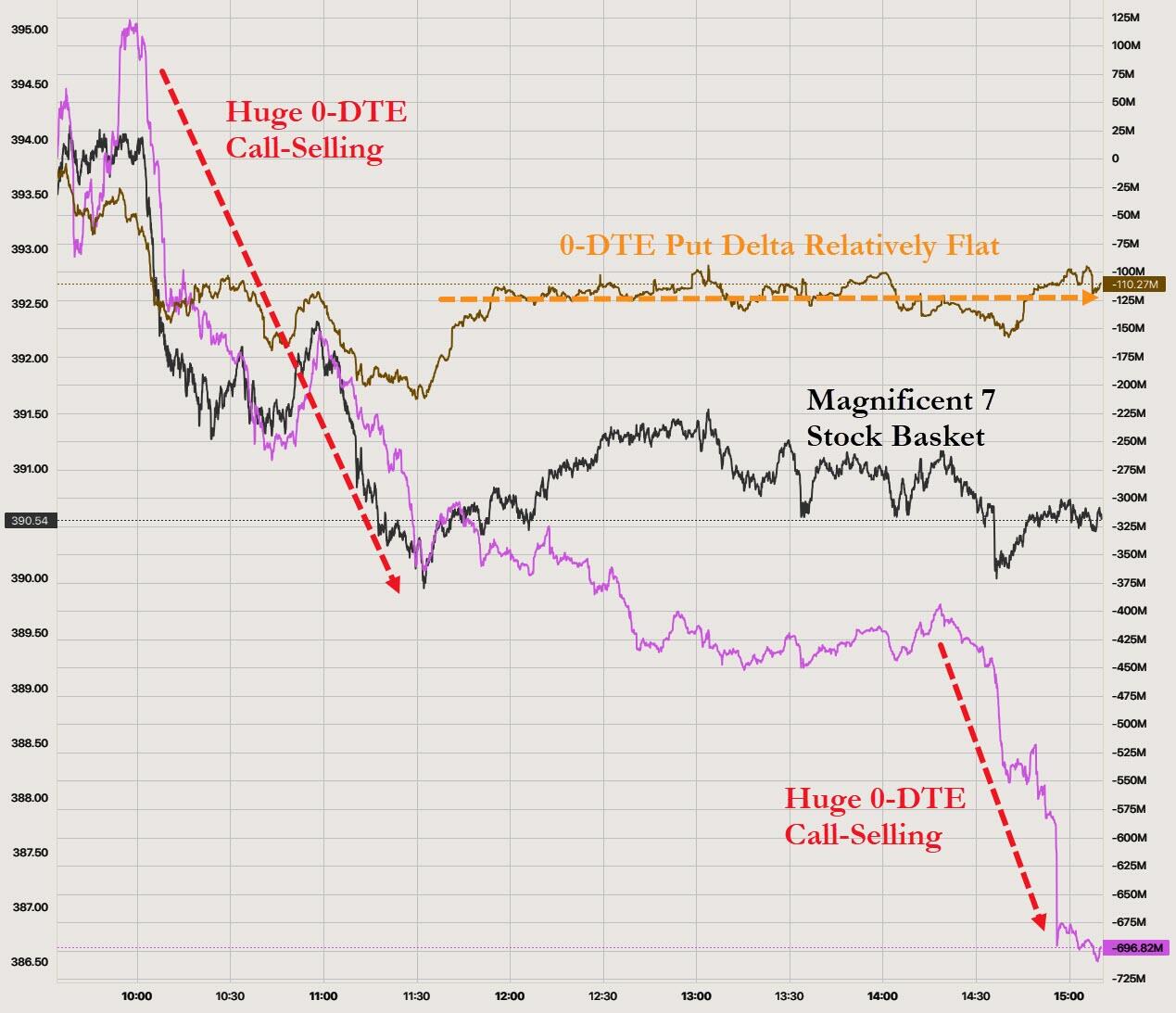

…But, the ‘Magnificent 7’ stocks were lower overall with huge 0-DTE call-covering early and late…

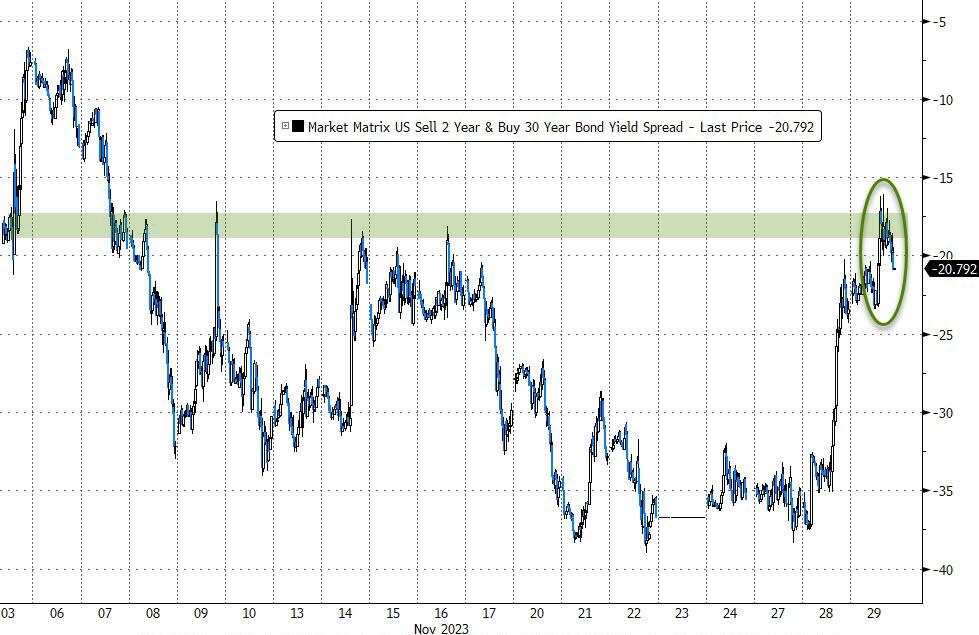

The bull-steepening continued in bond-land with 2s30s up to -16bps on the day…

Source: Bloomberg

…as 2Y yields fell to their lowest since June…

Source: Bloomberg

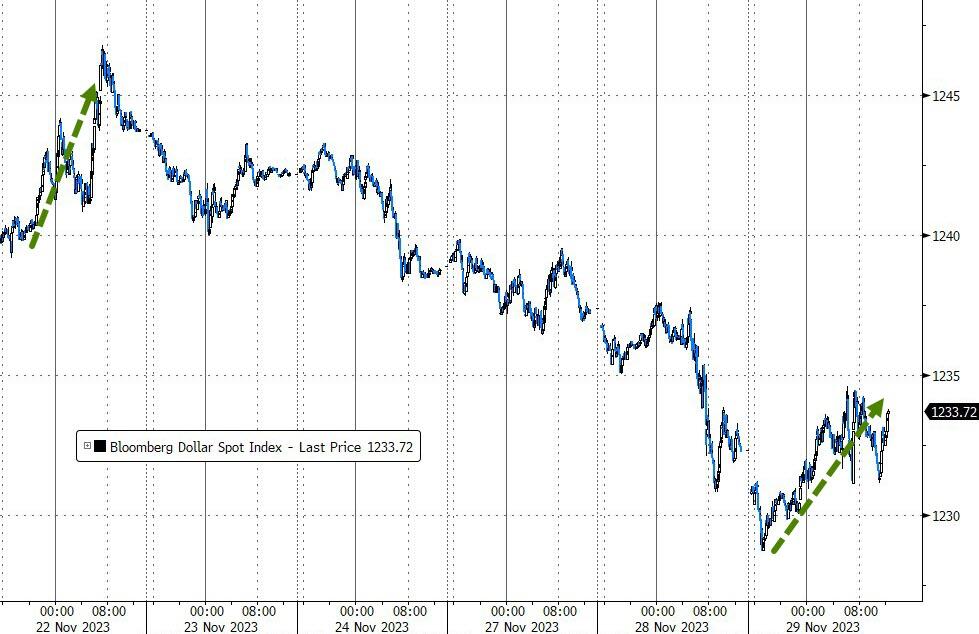

The dollar managed gains on the day after 4 down days in a row...

Source: Bloomberg

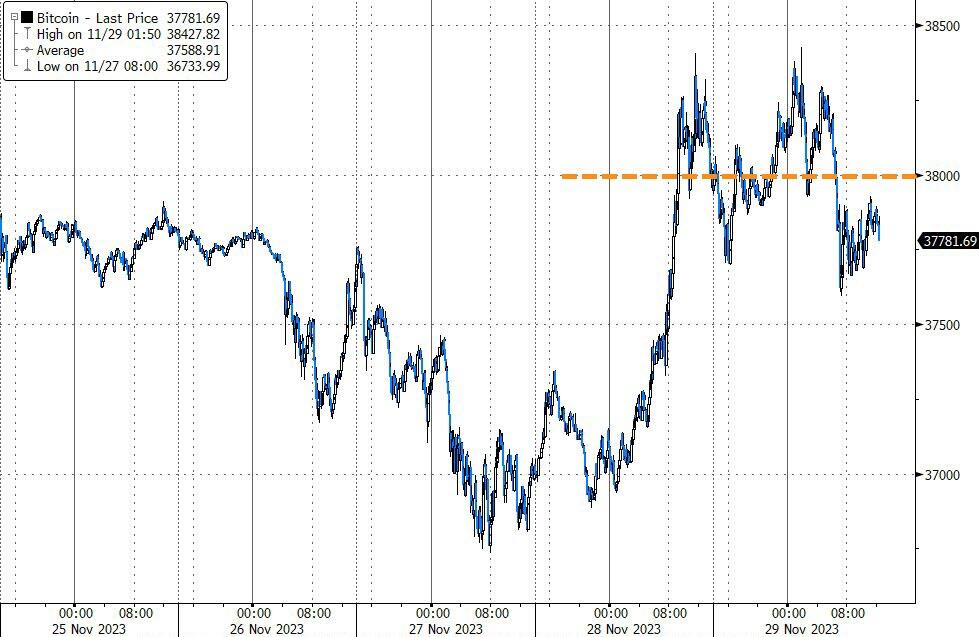

Crypto was marginally lower on the day with Bitcoin

Source: Bloomberg

Gold prices continued their charge towards new record highs…

Source: Bloomberg

And notably, silver has started to outperform very recently, breaking above its downtrend relative to gold…

Source: Bloomberg

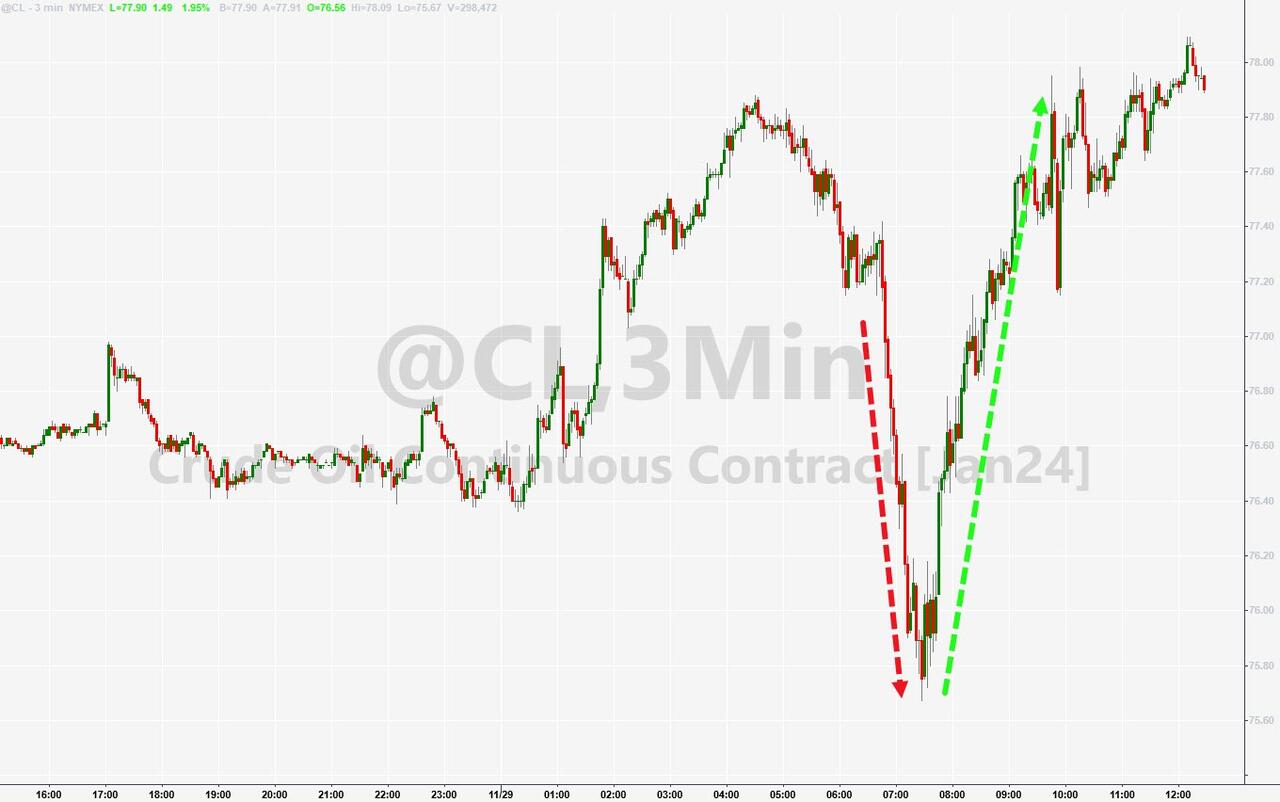

Oil prices pumped and dumped ahead of tomorrow’s OPEC+ meeting (after increased production cut rumors trumped across-the-board inventory builds and record US production)…

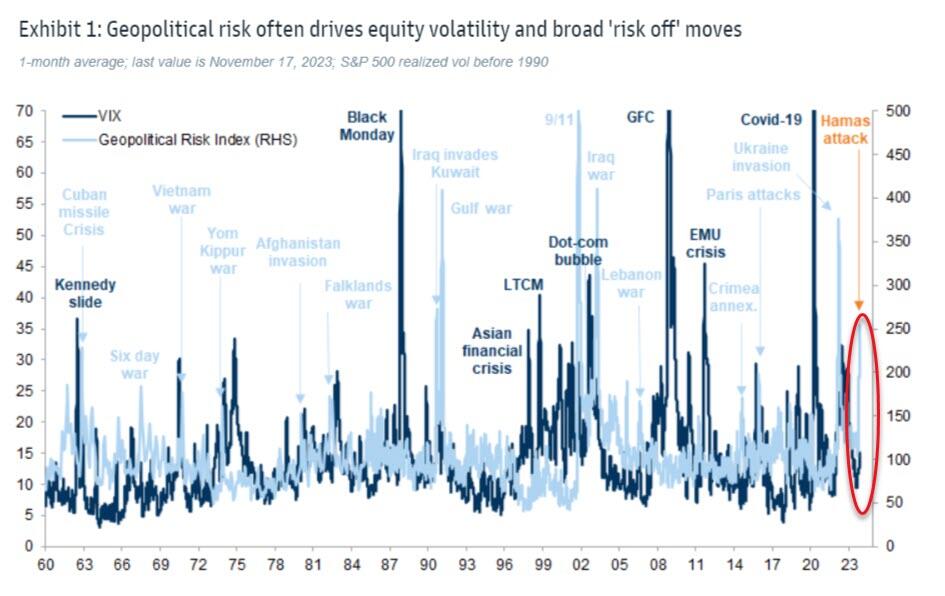

Finally, we note that historically, spikes in geopolitical risk have driven higher volatility. But, as Goldman Sachs points out in a note today, the latest spike in risk has not been accompanied by a meaningful spike in the VIX…

Source: Goldman Sachs

Goldman clearly doesn’t believe it’s different this time and recommends taking advantage of the low level of volatility in both equities and ‘safe assets’ (ex bonds) to focus on hedges.

Tyler Durden

Wed, 11/29/2023 – 16:00

via ZeroHedge News https://ift.tt/b2RxTki Tyler Durden