Is Credit Whispering, Or Screaming?

By Peter Tchir of Academy Securities

Is Credit Whispering? Or Screaming?

For the past couple of years, it has been relatively safe to assume credit is well behaved and relatively range bound. It is unclear if that remains the case.

We may be in a situation where the AI spend, the AI displacement, and the Working Poor are forming a storm of some sort. How severe remains to be seen, but for the first time in a while it is a real concern for me. My inclination has been to “fade” any concerns and “buy the dip.” That is still my “gut,” but I don’t think we should trust that “gut” feeling here.

Bank Debt

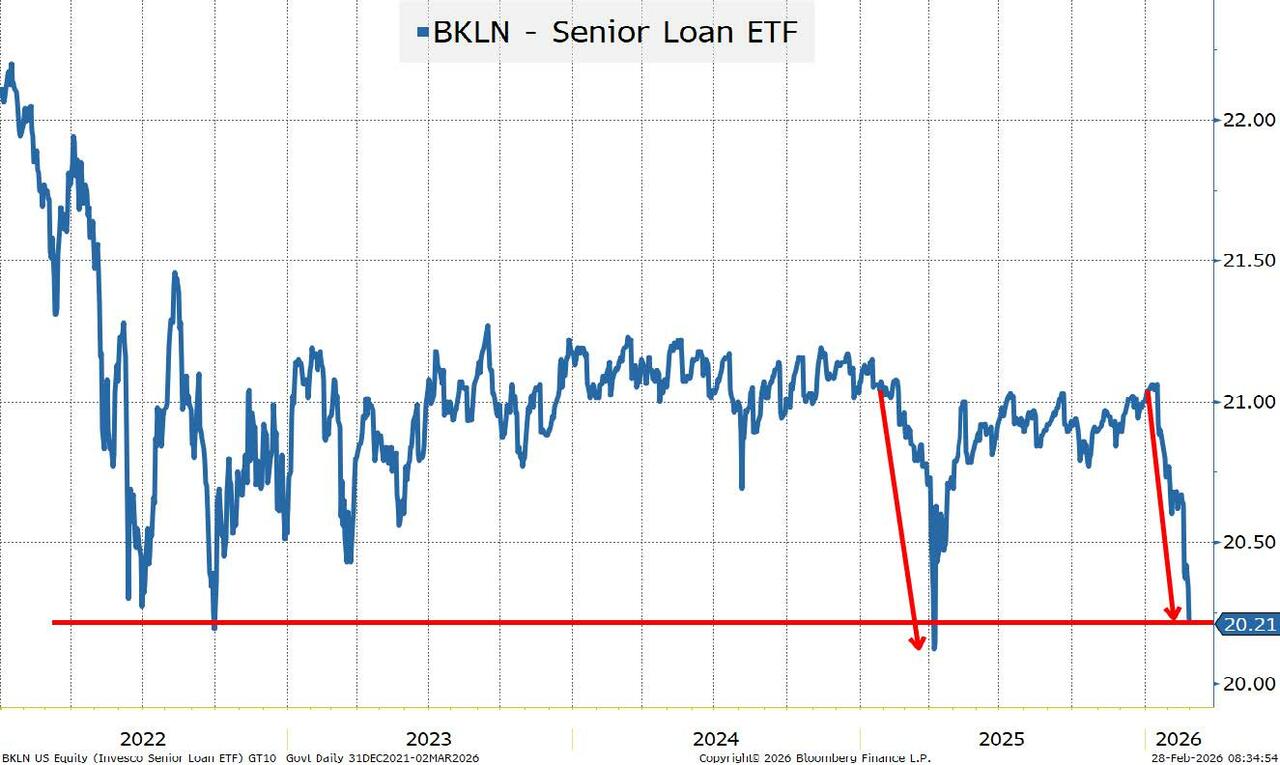

We are going to start with bank debt today. Senior secured leveraged loans (as opposed to debt issued by banks).

There are a few reasons to start with the leveraged loan (or bank debt) market and this ETF in particular:

- It is senior secured, so in theory is at the “top” of the capital structure (loan only issuers as well as covenant-lite deals have made that less of a truism than it once was).

- Our longstanding view is that “financial” bubbles always start with “credit” bubbles, which start with a “safe” asset no longer being safe.

- To say the leveraged loan market was viewed as “safe” is a stretch, but could we argue that private credit took on an aura of “safeness?”

- The nature of this ETF creates more risk of an ETF Spiral™ than we see in some other credit ETFs, where that risk is also present.

This ETF is almost back to its Liberation Day lows in price terms.

One “excuse” for this has come up in some conversations:

- We’ve had 3 rate cuts and anticipate more, making floating rate products less interesting.

- FLOT, an investment grade, floating rate bond ETF, has not sold off at all. This isn’t just about rates. In fact, it isn’t about credit “generically,” it is about specific aspects of the credit market.

The ETF mechanics are important here as well.

- BKLN is $6.4 billion, so it is relatively small, which is good. By comparison, HY ETFs like HYG at $16.6 billion and JNK at $7.8 billion are larger, and have potentially more impact.

- The flipside of that is the leveraged loan market is less liquid (on many metrics) than the high yield bond market. The settlement process is different as well. So “price discovery” may be more impacted by flows into or out of this ETF, versus corresponding flows into or out of HY ETFs.

- BKLN does not do “like for like” creates or redeems. This is important.

- Shares of ETFs like HYG and JNK can be created, or redeemed (destroyed) via an exchange of a pool of bonds. So, someone who wants to redeem a large amount of one of these ETFs may be delivered a portfolio of bonds. This creates a “balance” of sorts, in that the “price discovery” mechanism is in the exchange.

- Due to the nature of loans, this mechanism does not exist (or certainly is not the primary mechanism) for loan-based ETFs and they rely on create/redeem versus cash. A large redemption would cause the manager of the ETF to go to the market to sell loans. I have always believed that in times of stress (of which there have been a few), this leaves the leveraged loan market more exposed to flows from the ETFs than other credit markets.

- So far, the ETF has been trading “close” to NAV. This is where the ETF Spiral risk comes into play. When an ETF trades at a discount to NAV, it creates an “arbitrage” opportunity, where someone sells or shorts the underlying portfolio (or a subset of it) and buys the ETF. While on the surface that is “risk neutral,” but we have seen time and again that it tends to amplify moves to the downside. The “new” owners of the underlying credit instruments are more fearful than the seller of the ETF. All it takes is a few buyers of the bonds or loans to get nervous and sell, and the spiral can renew itself. Even worse, some traders, at the end of the day, will hedge themselves by shorting the relevant ETF, perpetuating the spiral.

- We are NOT seeing evidence of this, but it is on my radar screen and wanted to try to explain why in case it does start.

Boring……

Yes, it has taken us two pages to set the table a bit, but now we can get to the more “interesting” parts.

Selling What You Need Meets Selling What You Can

Now, maybe we can get to understanding why we started today’s T-Report with a relatively small ETF and went at lengths to highlight some liquidity issues on that ETF and the underlying asset class.

There is often a battle of selling what you need to sell. These are the assets that are at the root of your concern. The ones you need to reduce exposure to, because your exposure is now too large, relative to your risk tolerance.

Selling what you can sell is what occurs when either you cannot sell what you need to, or the price has dropped so much on what you “need” to sell, that you sell some of the closest “proxies” to get overall exposure down.

I often “joke” that 9 of 10 high yield selloffs were sparked by emerging market selloffs. Not because they had much to do with each other, but they were often treated as the same “pool of capital” and once EM bonds were down 10%, someone would decide it is better to sell a high yield bond down 2% than hitting another “lowball” bid in EM.

What Portfolio Managers “Need” to Sell. Not every portfolio manager is in the same condition. Not all have reached similar conclusions. This is meant to be a “generality,” but a generality that is real and has potential ramifications.

- Exposure to software services. This is clearly the new bogeyman in the room.

Anything below Liberation Day levels warrants extra attention. Liberation Day was a largely “self-inflicted surprise” that ultimately the admin largely backed away from. This is a bit more worrisome. The sell-off started in Q4, but only now appears to be “rattling” credit markets (BKLN didn’t start selling off until the middle of January). My argument would be that the first part of the “correction” was a valuation adjustment. It is exactly why we had more concerns about stocks than credit. Equity valuations were so strong in some sectors that you could have equities come under pressure, without corresponding pressure on credit. But as that “valuation buffer” erodes, credit and equities will move more in line.

We won’t discuss how much of this pressure is warranted or not. The view we discussed a couple of weeks ago remains my base case – this will largely be about margin compression. I find it hard to believe that this “conversation” isn’t occurring at some level.

C-Suite Executive. Get purchasing on the line and find out how much we are spending on software services.

Purchasing Manager. How much are we spending on software services? What is our budget for this year? Do you need to spend all of that?

Purchaser. Yeah, I’ve seen the reports. Yeah, we’ve played around with AI. None of it comes close to delivering what we get from providers. The providers have worked with us for years and not only have we customized the system, but it has also become integrated into so many things that we do, so we would be hard pressed to even think about changing, let alone change.

Purchasing Manager. Yes, but how much are we spending and do we need to spend it?

Purchaser. Ummmh, I thought I answered that. it is an integral part of our company at this point, I don’t see how, or why we’d change current spending.

Purchasing Manager to Purchaser. Ok, don’t do anything stupid and see what you can do to get costs down.

Purchasing Manager to C-Suite Executive. All under control. We are examining what we can do to keep costs down and explore new technology.

If I’m correct and this is the “conversation” that is taking place, it supports margin pressure, rather than something more dire. Discounts can be offered. Maybe “add-ons” for free, but possibly discounts. More resources can be provided to keep clients committed.

Equities lead credit lower, but is credit now dragging equities lower? That is potentially the case, which would explain the “need” to reduce exposure to this area.

- Exposure to hyperscalers and the data center/AI industry. This was an issue that was first brought to light in Q4 last year. I will use ORCL CDS as a proxy since it seems to be the easiest single thing to point to. There were some isolated concerns, and you saw some spreads widen a bit, but the investment grade bond market had no problem digesting some large new issues in 2026. It was a bit of a concern, but away from a few specific credits, it didn’t seem to illicit much action. I’m not sure it is still high on anyone’s “action” list, but people are likely revisiting exposure in this area.

- We could explore other areas or sectors that “need” to be sold, but let’s just use these two areas as the starting point.

Selling What “Needs” To Be Sold

Let’s assume for the moment that the market is now trying to sell these types of risks. Where are those risks?

- The leveraged loan market.

We already discussed the loans themselves and the ETF. You can sell the loans, but you cannot perfect a security interest in the loans, so if you want to “short” as a hedge (or a trade) you wind up needing to use a proxy (short interest in BKLN is growing). But that is not the only place these sorts of loans are making an appearance.

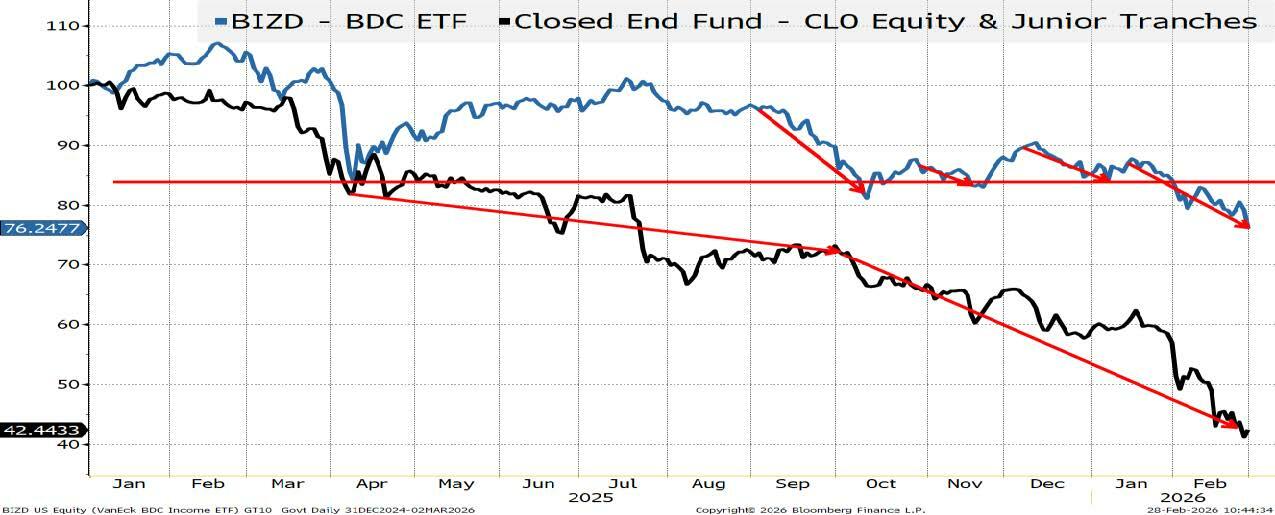

Business Development Corporations have leveraged exposure to the leveraged loan market (not exactly accurate, but close enough). This was one of the first asset classes to retest the Liberation Day lows. It has now broken through.

I was very reluctant to include the second chart here.

It is a closed end fund and quite small, making me question the pricing and understanding. Having said that, I did not have access to a CLO equity index that I could share. I would have preferred a CLO equity index, so I went with this closed end fund to illustrate a point, knowing that point was exaggerated. I honestly couldn’t figure out whether it was better to leave out (and not make a point about CLO equity) or include (and risk making the CLO equity issue a bigger deal than it really is). So, I erred on the side of leaving it in, as it makes the next chart more relevant.

You are now seeing the markets impact more senior tranches. As the equity buffer in the CLOs declines, more of the price action in the underlying asset class needs to be absorbed by more senior tranches.

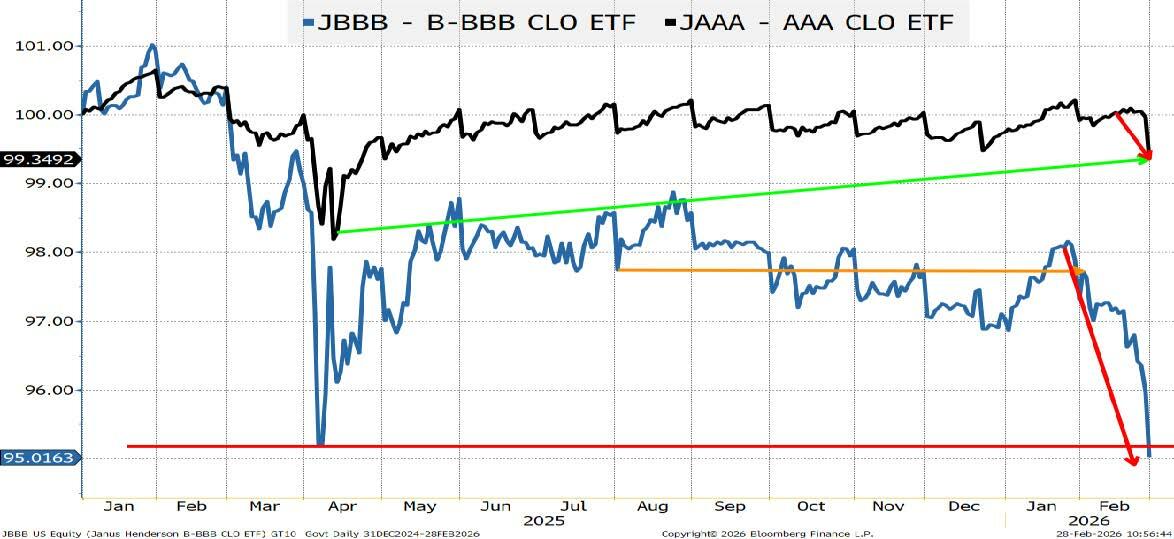

The “good” news is that JAAA, a fund that invests in AAA CLO paper, has not moved much and is well above the Liberation Day lows. The “bad” news is that may be changing as risk gets pushed up the spectrum. The AAA CLO does fit my definition of a “safe” asset. I believe that it is more difficult to have a credit loss in the AAA tranche of a cash flow (not market value) CLO than it is to pick a perfect bracket in the NCAA March Madness tourney pool. The deals done in the “old days” with fewer protections didn’t trigger at the investment grade level for any tranche, and the structures are even more difficult to break now. That does not preclude selling.

Let’s never forget, far more money is lost in credit by being “forced” to sell (leverage, fear, overexposure, downgrades, etc.) than is lost from defaults.

JAAA at $27 billion is large in its own right, but is just one of many very successful AAA CLO ETFs. Again, the “safe” money aspect trickles in here. I was mildly surprised that JAAA has had inflows this year.

While I am not at all concerned about credit risk as this level, I am concerned about potential selling. My guess is if the selling occurs, it would be via misunderstanding by investors who have allocated to such ETFs.

While pricing pressure can be brought to bear on the more senior tranches, any sort of selling that sucks up the liquidity for senior tranches can impact the entire underlying asset class. CLO equity is the tail that is wagged by the dog (the leverage loan market). The CLO AAA tranche is the dog that wags the tail (the leveraged loan market).

So far, we have remained in the realm of being able to sell what you want or think you need to sell.

Private Credit

What part of the credit world seems to own a lot of what “needs to be sold”? Private Credit.

Again, we are not arguing that what “needs to be sold” really needs to be sold, but that is the current market sentiment, and that sentiment seems to be increasing. Part of why it may be increasing is because of the inability to reduce your exposure if you allocated to private credit.

There is always an element of “cohort” investing in credit. CLOs created around the same time tend to own a lot of the same loans. Often those loans are similar. It is the nature of the beast.

CLOs are designed to be ramped up and fully funded, so that you can move on to the next CLO.

The easiest way (and often the only way in a “hot” market) to ramp up quickly is to buy the new issues. So, there is a tendency for CLOs of a similar vintage to own the same loans – the new issues of the time.

There are times when you get a widely diversified batch of new issues. Ratings could be across the board. Industries across the board. There are times when there is a “flavor of the day” type of concentration in the new issue calendar.

We haven’t done the work of detailing this, but from conversations, there have been periods in the past few years, where there has been a focus on software and data centers, etc., in the loan market, creating concentration risk.

Everything we just described applies equally to “serial private credit funds.” Where a fund raises money, invests it, and raises a new fund.

The Biggest Risk to Public Credit is the “Need” to Hedge Private Credit

We are getting this nasty little intersection of leveraged loans, CLOs, BDCs, and Private Credit.

Is it overdone? Possibly, but the narratives seem to be gaining traction. The selling has only started and seems to have just started to “spread” and contaminate other markets.

We have seen bank stocks come off recent highs (looking at KRE – Regional Bank ETF). Is that directly related to anything we’ve been discussing today?

Bank CDS spreads are widening a bit, both here and abroad. Just inching higher, from very tight levels and nowhere near their Liberation Day levels, but something to keep an eye on.

Ignoring…

We didn’t even address the recent default in Europe that raised more questions about fraud and risks in the private credit market.

We didn’t touch on potential risk to various parts of the credit market from the “working poor.”

We didn’t spend a minute dwelling on the risk of losing more jobs from “efficiency” more quickly than alternative employment can be found.

We didn’t address the positives either and why this may already be overdone.

Bottom Line

I want to “buy the dip” in credit. I don’t think I can.

We might get a nice bounce in risk assets this week if the attacks in Iran lead to a deal rapidly, without disrupting the flow of oil.

There is a confluence of events and I really want to see stabilization before I can be really comfortable.

This interconnectivity, the perception of relative “safety,” and the lack of liquidity in both the underlying assets, but more importantly, the vehicles through which those underlying assets are owned, are concerning.

We’ve been pounding the table on a rotation to foreign stock markets, but think we need to be more cautious across the board.

When credit talks, all markets should listen. So far, credit is only “whispering” to equities, but if they decide to get louder, it will not be good for risk assets.

On rates, price in 3 cuts by the end of the September meeting and I’m kind of “indifferent” at 10s below 4%, but given everything we just wrote, it probably makes sense to stay long rates for a bit longer, even out the curve.

We can only hope that the events in the Middle East lead to a peaceful resolution, putting the Iranian people on a better path to prosperity and freedom, while minimizing the loss of life for everyone in the region.

Tyler Durden

Sun, 03/01/2026 – 16:41

via ZeroHedge News https://ift.tt/ki96xSq Tyler Durden