Record Percentage Of Central Banks Expect Gold Reserves To Increase In Next 12 Months

Today, the World Gold Council released their 2026 Central Bank Gold Reserves Survey. Amongst the insights, here is the punchline: a record 45% of respondents expect their own gold reserves will increase over the next 12 months

Central banks have accumulated an average of 1,000t of gold over the past four years, up significantly from the 500t average over the preceding decade. This marked acceleration in the pace of accumulation has occurred against a backdrop of geopolitical and economic uncertainty, which has clouded the outlook for reserve managers.

The WGC’s 2026 Central Bank Gold Reserves (CBGR) survey was conducted between 5 February and 19 May. With the majority of responses coming in after the start of the Middle East conflict, this year’s survey contains insights on how central bankers view gold in the light of ongoing geopolitical turmoil. The sample is highly representative of the overall central bank community, both geographically and in terms of gold owned. This robust participation is a powerful signal of engagement with gold amongst the central banking community.

Here are the key highlights:

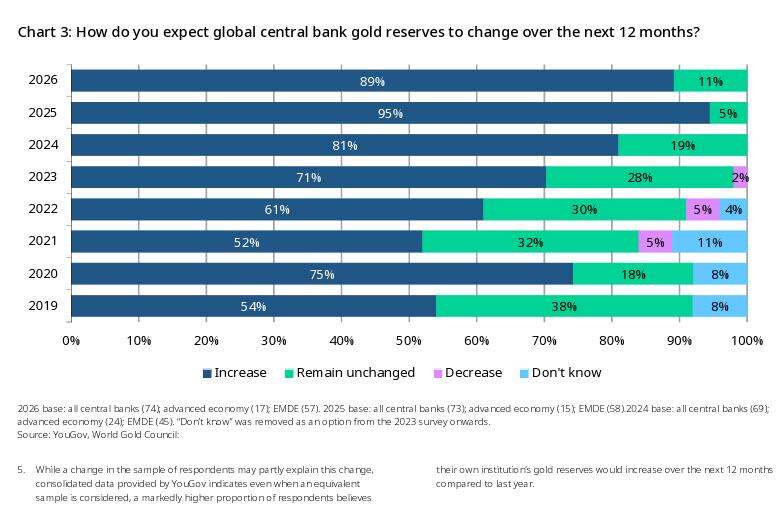

Similar to findings from previous surveys, central banks continue to hold favorable expectations on gold. Respondents overwhelmingly (89%) believe that global central bank gold reserves will increase over the next 12 months.

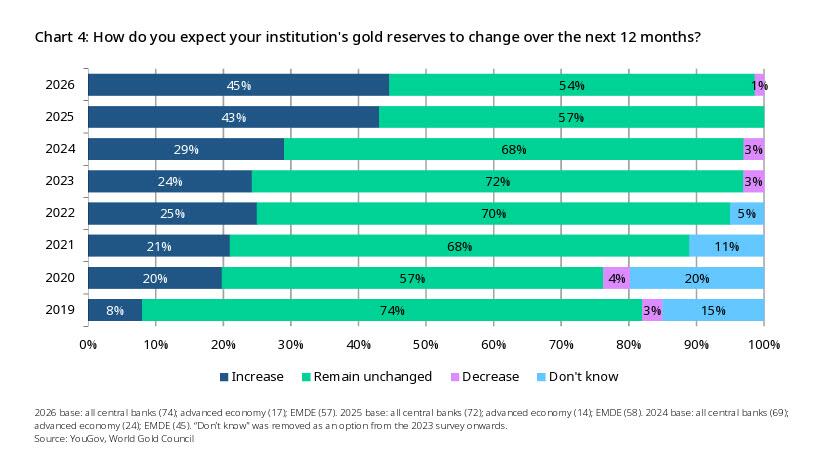

As noted above, this year, a record 45% of respondents expect their own gold reserves will also increase over the same period. The majority of the remaining respondents indicated they expect no change while 1% expect their institution’s gold reserves to decrease (hello, Turkey).

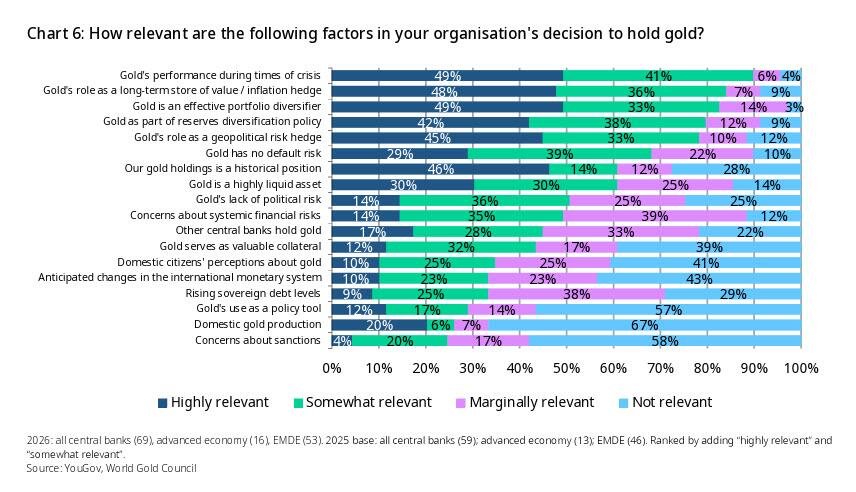

Gold’s performance during times of crisis, portfolio diversification and inflation hedging are some of the key factors for central banks to hold gold. In addition, gold as a geopolitical risk hedge and gold as part of a reserve diversification policy also feature as key reasons for increasing allocations to gold.

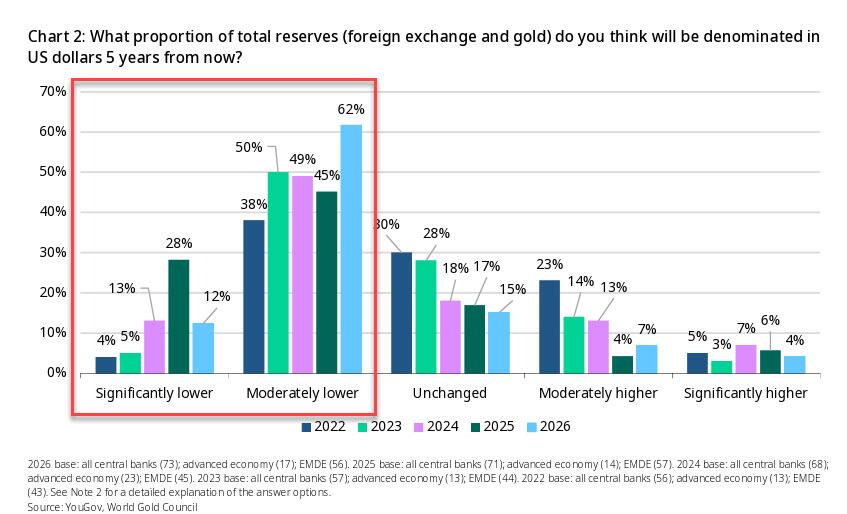

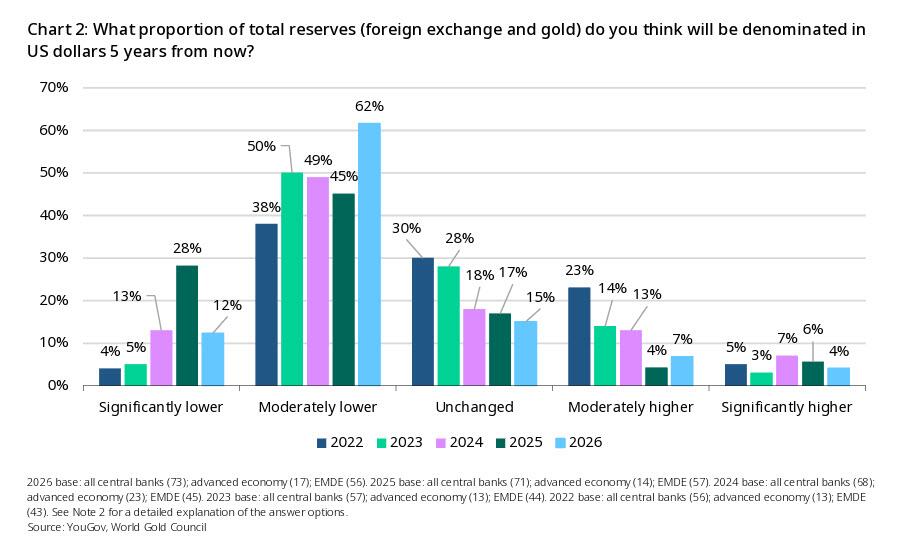

The majority of respondents (74%) see moderate or significantly lower US dollar holdings within global reserves over the next five years. Respondents also believe that the share of other currencies, such as the euro and renminbi will remain unchanged over the same period, while gold holdings will increase.

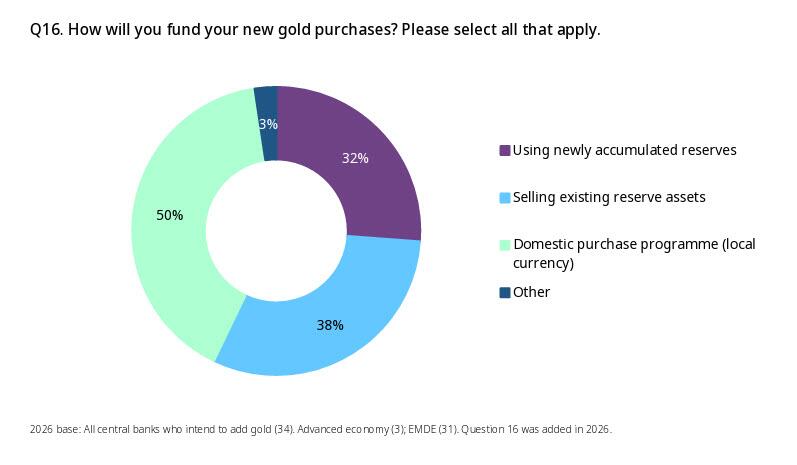

This year’s survey asked respondents how they would fund their new gold purchases. Half of respondents indicated through a domestic purchase program in local currency, while 38% indicated through selling existing reserve assets.

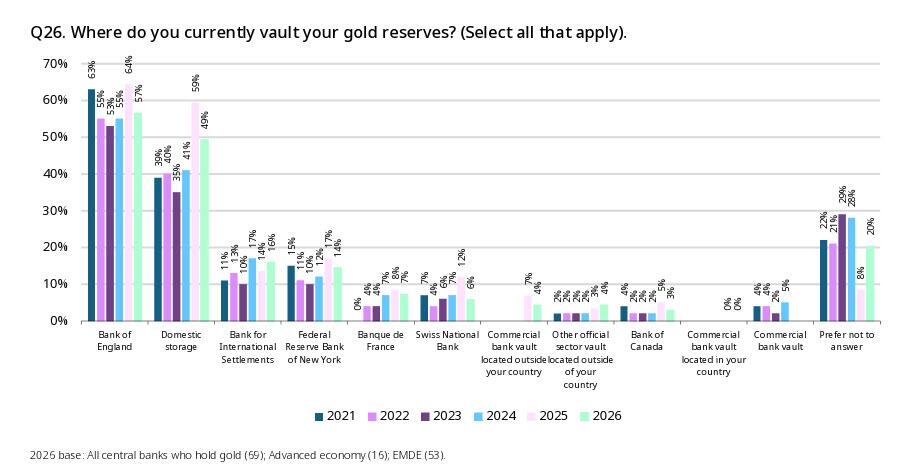

The Bank of England remains the most popular vaulting location among respondents at 57%, though central banks continue to diversify their storage across multiple locations. Domestic storage came in second at 49%, followed by the Bank for International Settlements at 16% (a slight uptick from last year). The Swiss National Bank saw a notable decline in preference, dropping to 6% from 12% in 2025.

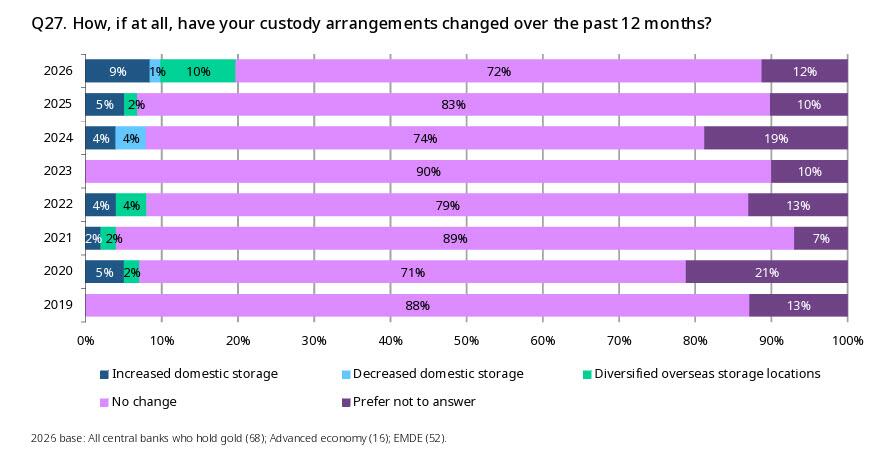

A notable increase in changes to vaulting locations was observed in this year’s survey, with 9% saying they have increased domestic storage and 10% saying they have diversified overseas storage locations in the past 12 months, compared with 5% and 2% respectively in last year’s survey. The trend is also observed in future plans for vaulting, with 7% saying they plan to increase domestic storage and 9% saying they plan to diversify overseas storage locations in the coming 12 months.

Summary:

This year’s survey reinforces the trend: central banks remain very positive on gold, highlighting its significance amid a volatile geopolitical and economic environment

The survey shows a continuation of the trend uncovered in previous years: central banks see gold making up a growing share of their reserve portfolios. 84% of respondents believe that gold will hold a (moderately or significantly) higher share of total reserves five years from now, up from 76% last year. Responses were also fairly consistent between central banks in advanced economies and EMDE (emerging markets and developing economies), with the majority anticipating that the proportion of total reserves held in gold would be moderately higher in five years’ time (Chart 1). Respondents were less sanguine on the US dollar. While it maintains its position as the dominant global reserve currency, data from the IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) shows that its share has been on a gradual decline. And respondents believe this trend will continue, with 74% expecting its share to be lower five years from now (Chart 2, p4). Both advanced economy and EMDE responses were aligned in this view.

When asked about expectations for how global central bank gold reserves will change over the next 12 months, respondents were almost unanimous, with 89% of respondents believing that official gold reserves will continue to increase (Chart 3). This sentiment was consistent across both advanced economy and EMDE respondents. It should be noted that 11% of central banks believe that gold’s proportion of total reserves would remain unchanged, up from 5% last year. In addition, 45% of respondents thought that their own institution’s gold reserves would rise over the next year, broadly in line with last year’s finding (43%).

Most respondents did not expect their gold reserves to change in the next 12 months. This marks a new record high in the proportion of central banks expecting to add gold to their own reserves with EMDE banks continuing to lead their advanced economy counterparts. Among EMDE respondents around half thought that their own gold reserves would increase in the next 12 months, while the other half anticipated they would remain unchanged.

The findings highlight that gold sentiment within the central banking community remains upbeat. Expectations point to continued gold buying over the next 12 months, reflecting sustained confidence in gold’s strategic role amid evolving geopolitical and macroeconomic dynamics.

Tyler Durden

Tue, 06/16/2026 – 17:20

via ZeroHedge News https://ift.tt/TbtGwMg Tyler Durden