Wyoming And Spokane Data Center Pauses Show NIMBY Fury Has Shifted From Nuclear To AI

The latest cracks in the data center buildout story arrived this month from opposite ends of the energy-rich West. Crusoe paused development activities on its 1.8 GW “Project Jade” campus near Cheyenne, Wyoming, at the explicit request of its customer.

Just days later, Avista announced it was pausing processing of a 500 MW data center request in Spokane County after more than 5,000 community complaints, a proposed city council moratorium, and concerns over ratepayer costs and legacy contamination at the former Kaiser Aluminum smelter site.

This all fits the pattern we’ve documented for over a year with proposed US data center capacity colliding with local political reality, transmission bottlenecks, and raw NIMBY resistance that now appears more intense than the peak opposition nuclear power plants faced in prior decades.

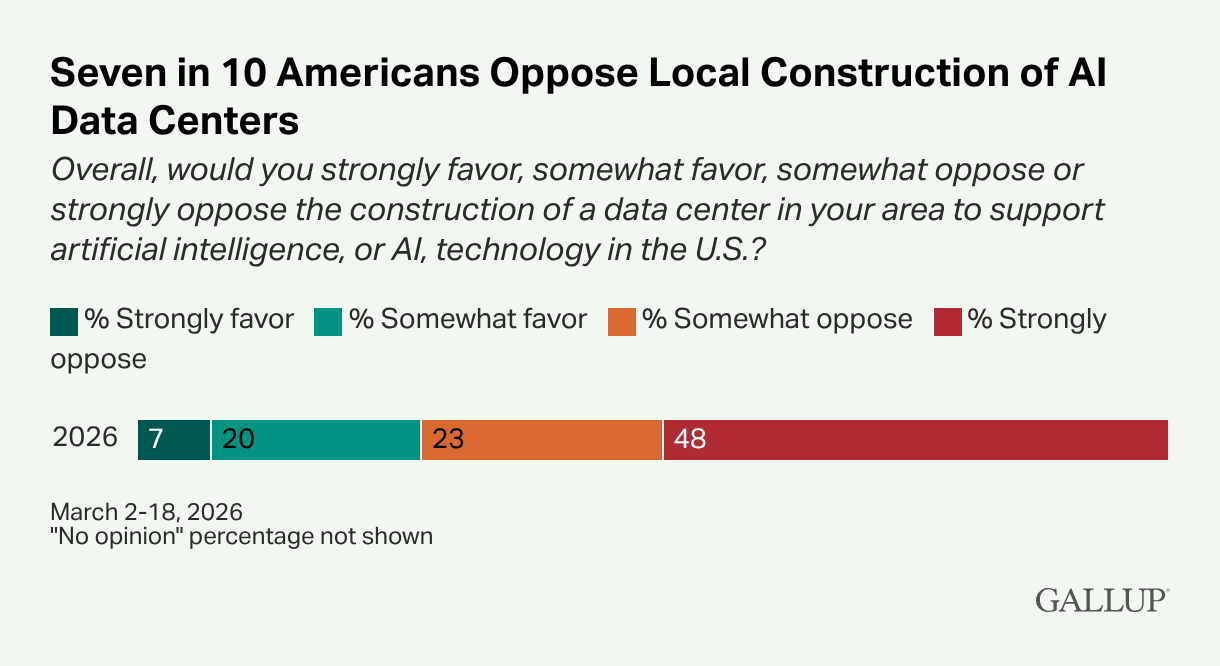

71% of Americans oppose construction of an AI data center in their local area, with 48% strongly opposed.

By comparison, opposition to a nuclear plant in the same backyard stands at 53%.

![]()

Data centers have managed to poll worse on local acceptance than nuclear facilities ever did at the height of their controversy.

We have been pounding the table on this long enough that we’re frankly surprised the table is still standing. Half of the US data center capacity originally slated to begin operations in 2026 faces delays or outright cancellation, according to Sightline Climate analysis we covered in April.

Contested projects are seeing roughly 40% cancellation rates in some analyses. Eminent domain fights over transmission lines have erupted in Maryland, Georgia, and elsewhere. Brookfield-backed Compass withdrew from a major Northern Virginia corridor. Community revolts have already killed or delayed billions in projects from Texas to the Midwest.

The Avista and Crusoe cases simply add fresh, high-profile confirmation that even brownfield sites with existing power infrastructure and willing utilities are not immune.

The investment implications for the nuclear sector are direct and near-term negative for sentiment, even if the long-term logic remains intact. The explosive AI-driven power demand narrative that helped lift names such as Oklo (OKLO), NuScale (SMR), NANO Nuclear (NNE), Cameco (CCJ), and the broader sector via URA, NLR, and NUKZ, has always rested on the assumption that hyperscale load growth would translate into contracted, financeable nuclear capacity on accelerated timelines.

When marquee data center campuses pause or reconfigure, that assumption gets stress-tested. Equity volatility in the nuclear complex has reflected exactly this uncertainty with profit-taking and narrative recalibration whenever friction in the demand side becomes visible.

None of this changes the structural math. The US still adds essentially zero new large reactors while China commissions multiple units per year. AI training and inference loads are real and growing. But the notion that private capital and hyperscaler demand alone would bulldoze through local opposition and grid constraints was always optimistic.

These latest pauses demonstrate that the problem is not unique to nuclear permitting. It is a systemic feature of American infrastructure development in the current political and regulatory environment.

Tyler Durden

Tue, 06/16/2026 – 18:00

via ZeroHedge News https://ift.tt/5eT7rRJ Tyler Durden