By EconMatters

Short Squeezes – Easier Said, Than Done

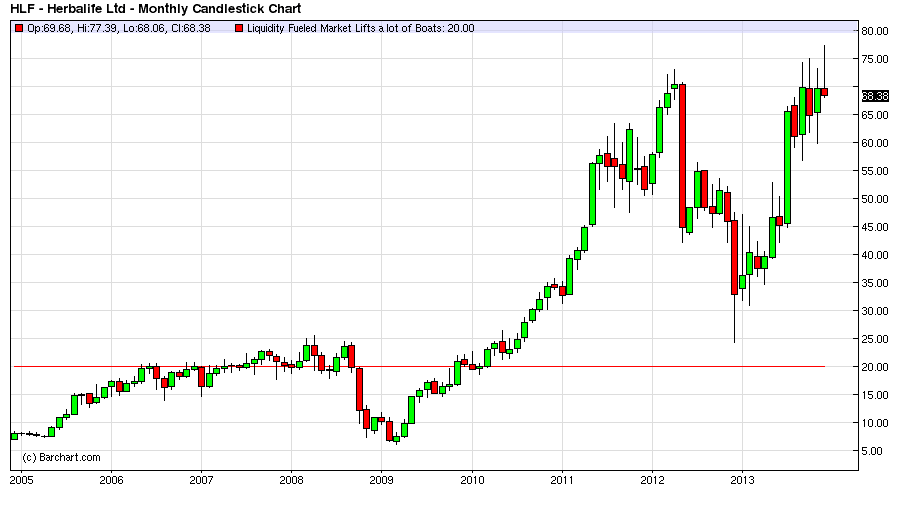

On December 5 Herbalife Ltd. (HLF) got as high as $76.43 and some investors might be thinking that they could get in on a short squeeze of Bill Ackman and Pershing Square Capital Management`s public and noteworthy short position on the company.

Well since then the stock has dropped to $68.36 in 6 trading days and longs shouldn`t look for any help in front of the all-important FOMC Meeting and Tapering decision on Wednesday of this upcoming week in the markets. The mood has been Risk-Off with investors taking considerable profits in many stocks the last 5 trading days.

Retail Investors shouldn`t Invest on Short-Squeeze Thesis

This just goes to show that even when the big players of the investing world are seemingly teaming up to cause Bill Ackman to cover his position and reap the benefits of a massive short squeeze, this should never influence an investor`s decision to invest in companies. An investor should first and foremost pick strong companies which are well run and have products in the marketplace that have a definitive strategic or competitive advantage.

Herbalife isn’t exactly GE Quality

I have done enough research on Herbalife to say definitively that this is not GE that you are investing in when it comes to a real genuine quality company. Herbalife is like the infomercial of stocks that comes on late at night to sell consumers products with all kinds of gimmicks and marketing sleight of hand.

Beware of Buying Credibility

Whenever a company spends so much money trying to make themselves seem credible it is because they aren`t in the first place. BMW doesn`t need to buy credibility, the quality of their products speak for themselves, and have for decades. GE doesn`t have to pay credible people to associate themselves with their products so as to gain credibility in the marketplace.

Just read the weekly press releases by Herbalife they are usually about trying to buy credibility. You see this with a lot of companies that are listed on the Pink Sheets, and many of these companies are borderline scam companies, or another way to put it would be un-investable.

Semantical Debate Meaningless

Whether one wants to label Herbalife a Ponzi scheme, a multilevel marketing firm, or some other derivation this is purely a semantical question an unimportant for investing purposes; the big picture is that this company doesn`t make for a good long-term investment because it doesn`t have a legitimate business model.

Herbalife`s Revenue Stream: Products versus Recruitment

I work out and like many people these days I buy fitness and health supplement products, but I and most people in the world do not buy overpriced commodity products from a multi-level marketer.

This is the age of the internet and many wholesale suppliers offer all the branded products that the consumer could possibly want in the health and fitness supplement industry online at much cheaper prices than the retail market.

Less price savvy consumers may buy some health products at their local gym or GNC outlet. Shoot Walmart even sells nutritional supplements these days and usually at very competitive retail prices. However, it is abundantly clear to all but the uninitiated that there is not a booming market for buying overpriced nutritional supplements from a multilevel marketing organization.

Greater Fools Theory

Consequently Herbalife isn`t making a fortune off of selling their products, they are making money off of predatory recruitment of greater fools, plain and simple Herbalife is a “Recruiting Company.” It is unfortunate that there happens to be an abundance of greater fools in the world to support this type of business model.

However, this is not an unusual phenomenon in the world, and it usually ends very badly when governments have to step in to protect the citizens from themselves. Alternatively, the marketing scheme ends when the economics crash on themselves because people will only participate in a scheme if there are legitimate financial incentives for the bulk of the recruitments, and/or the market runs out of foolish people to recruit.

Pink Sheets Methodology & Business Model

The business model that exemplifies Herbalife where they need so fanatically to purchase credibility with large sums of money is one of recruiting. The greater fool theory of recruitment where a few people at the top who managed to get many levels of recruited fools to buy into the scheme below them make some decent money off the backs of all the recruited fools under them, and each level down in the scheme represents larger proportions of members who make virtually nothing at all.

Call it what you want but it is a very unsavory business model. It is highly predatory and probably should not be allowed to be listed on a major exchange. This is the type of company that investors need to be wary of on the Pink Sheets that releases all these monthly and weekly press releases trying to make them seem legitimate because they have no credibility that stands on its own, so they need to affiliate with credible and respected people to attract investors.

It is a whole different aspect as well, but shame on the credible people for selling out their integrity for a quick buck, but that`s where the size of the payments comes in, and Herbalife has spent quite a large sum of money to try and buy some marketplace credibility. Accordingly at high enough remuneration levels the temptation becomes too great for those who need the money – so they sell out the one quality that the multilevel marketing company needs to sell new recruits on this unique business opportunity – Market Credibility.

If you Don`t Know Anybody Who Buys Herbalife Products, then avoid Investing in Company

So needless to say Herbalife doesn`t offer any products that cannot be acquired through much cheaper means by consumers. They don`t offer any unique product offerings, they don`t own a whole bunch of patents, they don`t have one single revolutionary product. So you shouldn`t be investing in this company on its own merits.

Investing Options for Retail Strategy

Consequently is there any way to play this stock for the investor. The short answer is no, and here are the reasons why. The stock could by all accounts be a worthy short candidate, but with the big players who have publicly lined up against Bill Ackman, and once this has become an ego driven trade for some of these players, this for all practical purposes eliminates an investor taking a reasonable short position. Further exacerbated by the fact that if a short squeeze ever occurred, the stock could gap up so high that no effective stop loss could protect the investor.

Options Market: Hefty Premiums

I looked up the options prices even 16 months out, and there are no bargains to be found. The market makers are willing to sell the investor an option on the stock, but with a hefty insurance premium, in a liquidity fueled bull market that can keep poor company`s stocks afloat long after these options expire.

The investor would have to buy a strike for the option way out of the money, and hope that regulators step in, but this is a strategy that relies upon a lot of outside intervention – and I try to avoid those plays.

There are safer places to put your money as an investor than needing to have government or outside intervention for your position to work as an investor. This is a sign of a poor investment calculation, and more of a pure gambling play.

Game versus Investing

What about piggy backing upon the big players and try and force Ackman to cover his positions? Leave this to the big players as many of these players can hedge risk a lot cheaper than the average investor, and for some of these players it is more of a game than an investment.

Carl Icahn has more money than he will ever need in his remaining lifetime, he wants to win, but if he loses it is no big deal to his personal wealth as one of the wealthiest investors on Wall Street. This is a personal revenge issue between the two, and Icahn has the personal wealth to spare to play this game – regardless of the outcome; the Retail Investor doesn`t fit into this category.

Stock Gaps are Account Killers

Plus these guys are big, and they talk to each other discreetly, so they know when they are getting out of the stock, you as an average investor will be the last to know when the short squeeze party is over, or has failed altogether. The only sign you will receive is if the stock gaps down below your stop level, and forcing you to cover in a potentially account devastating manner on a crashing, free-falling stock that was at all-time highs.

Final Thoughts

In summation, the retail investor cannot go long the stock on its own merits, this is not an investable company with a great long-term future in product or market differentiation – this is not BMW or General Electric Company.

The retail investor cannot adequately control risk to play the short squeeze from a long standpoint on a short-term basis. In addition, the retail investor cannot take a short position in the stock because of the potential for the stock to gap above a reasonable stop on a short squeeze.

The options market is not a viable strategy either for the retail investor because the market makers are charg

ing too much premium for the possibility that some future volatility comes into play for this stock in either direction. So the risk reward equation makes no sense for the retail investor on this company.

There is no rational, sound investment theme for the retail investor in Herbalife. This is nothing to be sad about, this is part of investing, and there are plenty of legitimate investment opportunities in this market available that make sound investment sense for the retail investor.

Remember, it is just as important the money the investor doesn`t lose, than the money they could potentially make – always evaluate both sides of the equation when investing.

Article Update

We wrote this article before PricewaterhouseCoopers had finished re-auditing three years of Herbalife’s financial statements, and the stock soared to $81.75 on Friday December 20th. However, since then Herbalife has sold off contrary to the overall market, and now stands at $78.55 on December 24, 2013.

Again we think the audit news spurred some shorts to cover, and propelled some traders to take advantage of the news for a nice trade to the upside, but this will be short-lived in our opinion, as it seems to have presented a nice entry price for new shorts to put on a position to the downside. But experience has taught us that shorting in any market, let alone a bull market is not for the weak of heart, and we advise retail investors to just stay clear of this stock. However, in the end this is not going to end well for investors who are long the stock, Herbalife is just not a good company with a sustainable business model for the long term, and eventually this company and their lofty stock price comes crashing back to the level representative of a sham, multi-level marketing company with a finite supply of dimwitted recruits in the world.

Many Ponzi schemes work for a while, even create the illusion of great returns and earnings in the short-term, but as the legacy of such enterprises teaches investors, it is only a matter of time before the tide goes rolling out to Sea, and the newest investors are left shivering on the beach with no clothes on begging for justice.

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/RH-0utwPQWE/story01.htm EconMatters