Presented with no comment…

via RSS http://ift.tt/2DRTR5X Tyler Durden

another site

Authored by Charles Hugh Smith via OfTwoMinds blog,

As I keep saying: the status quo has divested the working and middle classes.

The reason why the status quo has failed and is fragmenting is displayed in these three charts of wages, employment and assets: wage earners (labor) are in a rowboat trying to catch the yacht of those who own assets (capital).

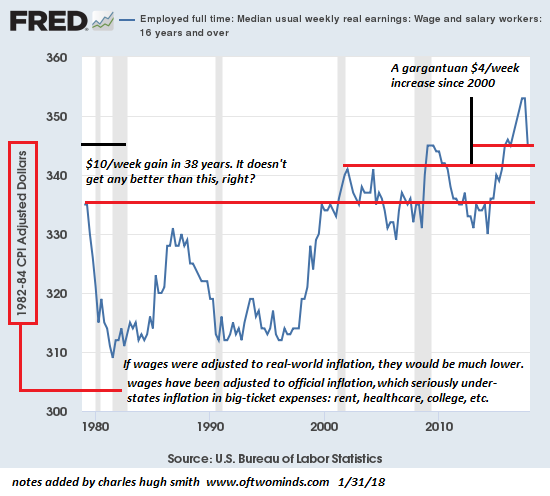

Here is a chart of weekly wages of those employed fulltime: up a gargantuan $4/week in the 18 years since 2000. Let’s see, $4 times 52 week a year–by golly, that’s a whole $208 a year. Brand new Ford F-150, here we come!

If we go back 38 years to 1980–an entire lifetime of work–we find real (adjusted for official inflation, which seriously understates big-ticket expenses such as rent, healthcare and college tuition/fees) wages have notched higher by $10/week–a gain of $500 annually.

If we adjusted wages by real-world income, we’d find wages have declined since 1980 and 2000.

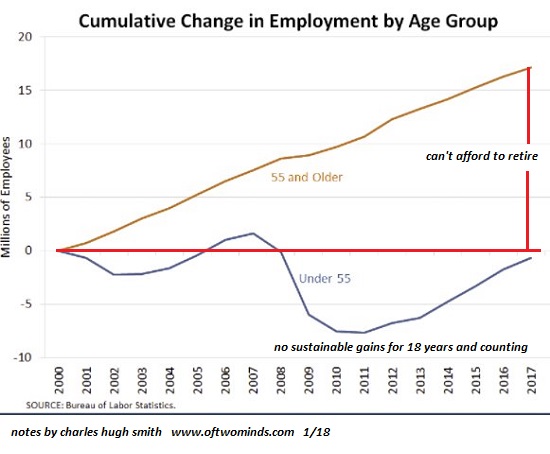

Here’s employment by age group since the year 2000. THose who can’t afford to retire are still dragging their tired old bones to work while employment for the under-55 cohort hasn’t even returned to the levels of 2000.

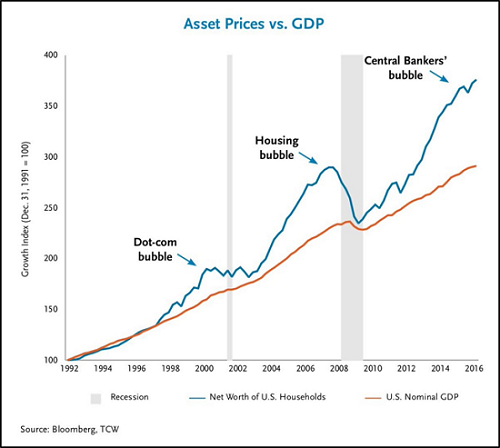

Meanwhile, asset valuations have soared. Those who own capital (assets) have done very, very well, those who trade their labor for dollars–they’ve gone nowhere.

Households with two regular jobs could afford to buy a house in Seattle, Brooklyn, or the San Francisco Bay Area in 1995. By 2005, they were priced out. Can a household with median income ($59,000 annually) afford a crumbling shack in any of the white-hot housing markets? You’re joking, right?

The cold reality is wage-earners are tugging on the oars of a water-logged rowboat, trying to catch up with the sleek yacht of asset owners. The system has been rigged to reward those who own assets (capital) or who can borrow immense sums of nearly-free money (credit) to buy assets.

Can we be bluntly unpolitically correct for a moment and observe that the rowboat is never going to catch the yacht? No wonder the nation’s savings rate is near-zero; most households don’t earn enough to save much, and those that do are caught up in a nightmarish Red Queen’s Race in which they save $10,000 a year but the asset they hoped to buy rose by $50,000.

In other words, trying to save enough by pulling on the oars of a rowboat for 10 years while the yacht has accelerated and is now on the dim horizon is a fool’s game.

As I keep saying: the status quo has divested the working and middle classes. The laboring classes have no stake in America’s status quo except their entitlements and whatever assets they bought 20+ years ago around 1994-97. Those who weren’t able to buy assets 20 years ago have been in the wallowing rowboat watching the yacht pull farther away every day.

Even households making double or triple the median annual income ($120,000 to $180,000) are struggling to keep up in high-cost regions. This reality is driving social discord that will morph into social disorder.

Gordon Long and I discuss social disorder in Part 3 of our series 2018: Year of Accelerating Social Change (15 minutes):

* * *

My new book Money and Work Unchained is $9.95 for the Kindle ebook and $20 for the print edition. Read the first section for free in PDF format. If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

via RSS http://ift.tt/2BIhsQm Tyler Durden

The drama of a murder-suicide in a sleepy, Swiss town reached the main financial street in Zurich, after it emerged that the man who shot top lawyer and media man, Martin Wagner, in cold blood on Sunday, was a risk manager for the Swiss National Bank.

This is what happened: according to barfi.ch, on Sunday, the village of Rünenberg in Baselland was in shock following news of the tragic murder of media lawyer Martin Wagner, 57. Wagner was fatally wounded in a dispute with his neighbour.

The perpetrator is Martin G., 39-year-old family man. On Sunday morning, he had a loud argument with his wife, who fled from him to Wagner’s villa. There, G. first shot the 57-year-old Wagner, then killed himself.

Now, the hush which descended on the village after the murder has slowly given way to one question: why? The police stressed that there are personal reasons behind the murder-suicide.

“Investigations are still running at full capacity. People are being interrogated and different leads are being followed.” The murder weapon has already been found and seized by the police.

A team of around 70 personnel was called in to deal with the murder on Sunday, including the security police, the “Barrakuda” special unit, a forensics team, prosecutors, and the institute for judicial medicine.

“For tactical reasons we cannot say exactly how many people we consider as part of the investigation,” Michael Lutz, the investigator in charge of Baselland’s prosecution, said in a press release.

According to the investigative authorities in Baselland, the motive for the killing remains unclear. However, one assumption which was made on the day of the crime holds fast. “The police and prosecution can assert that, based on current results within the investigation, there are no hints that the crime was committed in the context of the professional activities of the victim,” a spokesperson for the investigation said.

What is now know, is that at the Swiss National Bank where he worked, Martin G. was a risk manager. He was part of a team of around 15 specialists, who take care of the huge positions on the SNB’s balance sheet.

As is well known, the SNB is one of the world’s largest hedge funds, behind the ECB, BOJ and the Fed, with some CHF800 billion swiss franc in asset holdings, of which $88 billion are held in US stocks.

Commenting on his work at the SNB, a partner told Inside Paradeplatz that Martin G. was considered a loner: “He was a funny guy.” On the 2nd floor of the SNB’s headquarters at Borsenstrasse 15 in Zurich, the future killer showed up with his colleagues from the Risk team, and would quietly eat his food.

Attempts to “lure him out of the bank” were met with silence. “You quickly realized that he was not a dumb guy.”

Martin G. left little public traces on the net: there is a record of his appearance at an event with many central bankers in Berlin in may 2009. There, G. was a panelist in a presentation on “Liquidity Risk Stress-Testing Framework with Interaction between Market and Credit Risks”.

Martin G. remained an authorized signatory – ever since 2009, when he was registered with the SNB – in the commercial register until the murder suicide on Sunday.

According to Inside Paradeplatz, The SNB is in contact with the family members of its ex-risk manager. One question is how it will communicate his demise: whether the central bank’s name figures in his obituary remains open.

So far there is no indication what prompted the former SNB risk manager’s shooting spree.

via RSS http://ift.tt/2E1a6wO Tyler Durden

Authored by Simon Black via SovereignMan.com,

Earlier this month, General Electric took a $6.2 billion charge to its insurance unit for the fourth quarter. And the company said it will set aside another $15 billion over seven years to bolster reserves at GE Capital.

The charge had to do with long-term care policies (to pay for nursing homes and other late-life care) GE holds on its books.

So, one of the oldest and most highly-regarded companies in America just made a small, $21 billion miscalculation. Oops.

Keep in mind, GE’s entire market cap is only $140 billion.

The insurance charge, along with costs tied to the US tax plan, led GE to a $9.64 billion loss in the fourth quarter.

Then last week, GE announced the Securities and Exchange Commission (SEC) was investigating the company’s accounting practices (specifically how the company books revenue from long-term service contracts on things like power-plant repairs and jet-engine maintenance).

But this isn’t GE’s first run in with the SEC…

The company’s accounting practices have long been considered a “black box.” The New York Times even published a story in 2009 comparing the company to Enron – the energy giant brought down by fraudulent accounting.

And is all started with GE’s legendary former CEO Jack Welch.

Welch would regularly beat Wall Street’s earnings estimates by a penny or two. And he was named manager of the century by Fortune Magazine for his ability to pump GE’s stock.

And while Welch is lauded for his “six sigma” management, it seems his real talent was using GE’s many divisions to move assets around and goose earnings to hit short-term numbers.

The creative accounting caught up with GE in 2009, when the company paid $50 million to settle SEC allegations it had used improper accounting methods to boost numbers in 2002 and 2003.

Among the strategies GE used to make its 2003 numbers was selling railroad cars to banks, with side deals and verbal promises to assure the banks they couldn’t lose money on the deal.

Enron used the same trick in 1999 when it “sold” Nigerian barges to Merrill Lynch, allowing the company to fake a $12 million profit.

Today GE is a $140 billion company (shares are down by nearly half over the past 12 month). The company has nearly $160 billion in debt. And in fiscal year 2016, the company lost $41 billion in cash.

GE’s financial performance makes my favorite whipping boy, Netflix, look like a piker.

GE got here, in part, because the government guaranteed all of the company’s debts until 2012 to help it survive the Great Financial Crisis.

Then the Fed lowered interest rates and printed trillions of dollars to goose the economy.

Instead of using this beneficial environment to repair its horrible balance sheet, GE spent some $50 billion buying back stock and paying dividends… and allowed Welch’s successor, Jeff Immelt, to walk away with $211 million (despite the company erasing $150 billion of market cap value during his tenure).

GE has gotten away with this behavior because we’re in the middle of one of the largest asset booms in history. The markets are at all-time highs. And nobody asks the tough questions when they’re making money.

It doesn’t take a giant pin to prick the bubble. It just takes something unexpected… Nobody ever knows what will set off the next crisis.

But in GE’s case, you can bet there isn’t just one cockroach.

Plus, interest rates are rising today (the 10-year Treasury is above 2.7%) and the Fed is taking away the quantitative easing punch bowl. What will happen to overly indebted companies like GE (who are likely covering up more huge losses) when the credit dries up and debt service gets way more expensive?

Mind you, GE already can’t afford its debt.

GE is just one example of a potential crisis in the making.

Maybe a bank sets off the next crisis…

I just read a Wall Street Journal piece about “drive by appraisals.” When the big institutional investors, like private equity giant Blackstone, started buying tens of thousands of individual homes, they needed a quick way to appraise the properties to get loans.

Blackstone and its lender, Deutsche Bank, settled on these drive by appraisals, where brokers give their price opinion of the property. These assessments, called broker price opinions (BPOs) were outlawed by congress after the crisis.

But the prohibition doesn’t apply to investors buying tens of thousands of homes (of course you don’t want to have an accurate asset value for collateral behind really big loans).

Sometimes brokers will even outsource the process to India, where companies will use Google Earth and real estate website to come up with home values.

BPOs have been used to value homes backing more than $20 billion of bonds sold by companies like Blackstone.

As Warren Buffett says, “you never know who’s swimming naked until the tide goes out.”

Just know, there are major losses – and likely fraud – hiding out there today. But it’s gone largely ignored because of the one-way market we’ve experienced since 2010.

GE and these drive by loans are just two examples. And the worst is yet to come.

* * *

And to continue learning how to ensure you thrive no matter what happens next in the world, I encourage you to download our free Perfect Plan B Guide.

via RSS http://ift.tt/2rRnXRu Tyler Durden

The difficulties of running a state-legal recreational marijuana market when the substance is prohibited at the federal level are pushing California politicians to consider some less than ideal policy solutions.

The difficulties of running a state-legal recreational marijuana market when the substance is prohibited at the federal level are pushing California politicians to consider some less than ideal policy solutions.

California Treasurer and gubernatorial candidate John Chiang on Tuesday lent support to the idea of creating a publicly owned bank that would exclusively service the state’s cannabusinesses. “We are contending with the emergence of a multi-billion dollar cannabis industry that needs banking services, and a private banking industry that is stymied by federal law in meeting the needs of the new industry,” said Chiang in prepared remarks to reporters, adding that his office would be begin studying the practical hurdles involved in establishing a bank.

This idea is not unique to Chiang. His opponent in the race for governor, Lt. Gov. Gavin Newsom, likewise called for the creation of a state-owned bank in May, and similar proposals are currently being mulled by the cities of Los Angeles, Oakland, and San Francisco.

The idea is attracting interest from the industry as well, following Attorney General Jeff Session’s revocation of Obama-era guidance for banks on how to engage with cannabis clients without getting hit with federal money laundering and racketeering charges. That guidance had offered some measure of predictability for the industry by opening up at least some access to the financial sector.

But according to Josh Drayton of the California Cannabis Industry Association (CCIA), a number of marijuana-related businesses have had bank accounts closed since the reversal. That includes the CCIA, which—despite not directly engaging in any cannabis enterprise or ever handling the plant—was given notice that its account with a local California bank would be shut down.

“With the federal government intervening and threatening our industry, it takes the industry back to a gray area,” says Drayton. “The industry is definitely in support of a public banking solution.”

Even under the more lax Obama administration rules, cannabusinesses had an exceedingly difficult time securing basic financial services such as checking accounts, business loans, and insurance policies. Sessions’ move has made desperate policy solutions seem even more attractive.

However understandable the urge is, though, establishing a state-owned bank raises any number of practical, legal, and policy concerns. For starters, it could actually make it easier for the feds to crack down on state-legal marijuana businesses. Collecting the assets of all California cannabusinesses in one financial institution means the federal government could theoretically freeze the entire industry’s assets in one fell swoop.

A similar scenario is playing out now for Deferred Action for Childhood Arrivals (DACA) recipients. Desperate for protection from immigration enforcement, countless people who were brought to the U.S. illegally as children handed over reams of personal information to the federal government when Obama was president. Now the executive branch is overseen by someone with a decidedly different view on immigration who can use the data to expedite deportations among that community.

Drayton says the marijuana industry is not unaware of this risk, and would try to guard against it, possibly by pushing for the creation of a series of smaller, local government–owned banks.

A state-owned cannabis bank would also pose a real risk to taxpayers, as a November 2017 report by Chaing’s own Cannabis Banking Working Group makes clear. “The obstacles to creating a public financial institution are formidable, including the difficulty of getting deposit insurance, unknown start-up costs, investment likely to measure in the billions of dollars, and the probability of losses for several years or more that taxpayers would have to cover,” reads the report, which recommends further study of the idea.

And then there’s the possibility that a state bank, once created, would later be expanded into unrelated functions that libertarians are likely to find unpalatable. Newsom suggested such an institution could be used to finance health care facilities, student loans, and affordable housing. Another activist told the Los Angeles Times that talk of opening a cannabis bank was a boon to the idea of creating more state-owned banks in general. The discussion is “putting a spotlight on the glaring inequalities of the banking system and how inadequately it provides services to the economy,” he said.

Beyond all this, a state-run cannabis bank would be merely a Band-Aid for the larger problem of federal marijuana prohibition.

“I am not convinced that a public bank in California will solve the problems,” Hezekiah Allen, executive director of the California Growers Association, told the San Francisco Chronicle. “The problem is antiquated laws at the federal level. Congress must solve that issue.”

from Hit & Run http://ift.tt/2E157vY

via IFTTT

In a report that raises further questions about the US’s ability to respond to a ballistic missile attack from North Korea or one of its other adversaries, CNN said the US conducted an unsuccessful missile defense test on Wednesday.

The missile, which was launched from land in Hawaii, failed to intercept an incoming target. The Pentagon is not publicly acknowledging the failure of what’s supposed to be a crucial missile defense system. CNN’s anonymous sources blamed the Pentagon’s reticence on the upcoming Winter Games in Pyeongchang, South Korea, which are slated to begin Feb. 9.

Officials: US missile defense test failed in Hawaii early Weds. Pentagon not publicly acknowledging key ballistic missile defense test failure & officials tell @barbarastarrcnn there is a decision to not talk about it, in part because of sensitivities surrounding North Korea.

— Will Ripley (@willripleyCNN) January 31, 2018

US Department of Defense officials are trying to determine what went wrong, but so far, all the Pentagon will officially say is that a test took place.

“The Missile Defense Agency and US Navy sailors manning the Aegis Ashore Missile Defense Test Complex (AAMDTC) conducted a live-fire missile flight test using a Standard-Missile (SM)-3 Block IIA missile launched from the Pacific Missile Range Facility, Kauai, Hawaii, Wednesday morning,” Defense Department spokesman Mark Wright said.

To be sure, the missile, which is reportedly still in development, represents a key advancement in US defense capabilities as it is designed to eventually intercept the type of intercontinental range missile that North Korea has vowed to launch against the US.

The missile is used to target intermediate range missiles from adversaries – something that Trump has claimed works “97%” of the time.

Last year, the White House requested another $4 billion in funding for the Pentagon with the express purpose of improving the US’s missile intercepts along the West Coast, Alaska and Hawaii.

As Andrei Akulov of the Strategic Culture Foundation pointed out back in October, shortly after Trump made the “97%” remark, the notion that our missile defense system will be able to stymie a North Korean nuclear missile strike is a “dangerous illusion.”

The US is pushing ahead with expansion of the nation’s homeland ballistic missile defense (BMD). The effort enjoys strong bipartisan support in Congress and among experts. Many allies place a high value on BMD cooperation with the United States. However, there are ample reasons to question the efficiency of US missile defenses, especially the capability to protect against intercontinental ballistic missiles (ICBMs).

…

It is generally believed that it takes at least four-five interceptors to hit the target. It means President Trump is off base saying the hit probability is 97%. Prior to the ICBM test, the GMD system had successfully hit its target in only ten of 18 tests since 1999. A success rate is about 56%, not 97%. But even 56% is almost certainly an overstatement, given the less-than-realistic nature of the tests.

Defense News offered more details about the missile, identifying it as a SM-3 Block IIA. The missile was fired from an Aegis Ashore test site in Hawaii.

If confirmed, it would mark the second unsuccessful test of the Raytheon missile in the past year. It also deals a setback to US missile defense efforts as North Korea makes seemingly daily progress on it goal of striking the U.S. mainland with nuclear-armed missiles.

When reached for comment by DD, US Missile Defense Agency spokesman Mark Wright declined to comment on the outcome of the test.

“The Missile Defense Agency and U.S. Navy sailors manning the Aegis Ashore Missile Defense Test Complex (AAMDTC) conducted a live-fire missile flight test using a Standard-Missile (SM)-3 Block IIA missile launched from the Pacific Missile Range Facility, Kauai, Hawaii, Wednesday morning,” Wright said.

As we highlighted at the time, another SM-3 Block IIA test failed in June after a sailor on the destroyer John Paul Jones mistakenly triggered the missile’s self-destruct mechanism.

via RSS http://ift.tt/2DQWFMs Tyler Durden

Ignoring objections from the FBI and Deputy Attorney General Rod Rosenstein, President Donald Trump is by all accounts preparing to release the controversial “FISA memo”, which was assembled by House Intel Chairman Devin Nunes.

Top Democrats – who once echoed criticisms from inside the DOJ – now admit that the memo’s contents – once said to be “fabrications” – could prompt the firings of Rosenstein and even possibly Special Counsel Robert Mueller.

And as it so happens, with the Russia collusion narrative danging by a thread and the threatening to take what remains of the Democrats credibility with it, CNN is back with – what else? – another report fueling the tired narrative that Trump has asked those around him to take “loyalty oaths” and otherwise prove their fealty.

This time, CNN is claiming that President Trump wanted to know whether Rosenstein was “on my team” when the deputy attorney general – who appointed Mueller to run the Russia investigation in May – approached him in December about quashing Intel Committee Chairman Devin Nunes’ document demands.

Which is interesting, because the documents that were eventually turned over following months of resistance to those demands became the inspiration for the FISA memo.

But CNN doesn’t dwell on that. Instead, it moves next to Rosenstein’s incredulous response: “Of course, we’re all on your team, Mr. President,” he reportedly said.

CNN quickly reminds us that this isn’t the first time Trump’s prediliction with loyalty has been raised by the press:

The episode is the latest to come to light portraying a President whose inquiries sometimes cross a line that presidents traditionally have tried to avoid when dealing with the Justice Department, for which a measure of independence is key. The exchange could raise further questions about whether Trump was seeking to interfere in the investigation by special counsel Robert Mueller, who is looking into potential collusion by the Trump campaign with Russia and obstruction of justice by the White House.

At the December meeting, the deputy attorney general appeared surprised by the President’s questions, the sources said. He demurred on the direction of the Russia investigation, which Rosenstein has ultimate authority over now that his boss, Attorney General Jeff Sessions, has recused himself. And he responded awkwardly to the President’s “team” request, the sources said.

“Of course, we’re all on your team, Mr. President,” Rosenstein told Trump, the sources said. It is not clear what Trump meant or how Rosenstein interpreted the comment.

Rosenstein’s meeting with the President came as Rosenstein prepared to testify before the House Judiciary Committee. Trump appeared focused on Rosenstein’s testimony, and even reportedly fed questions to members of Congress, demanding that they ask them during Rosenstein’s testimony. Rosenstein originally incurred the president’s anger when he appointed Mueller, and the president has reportedly even considered firing him in recent weeks.

On Monday, Deputy FBI Director Andrew McCabe surprised his colleagues and the media by announcing his early exit as deputy director, saying he would instead use the remainder of his vacation time to allow him to still collect his full pension. Reports later confirmed that he was pushed out, and also that he is under an active DOJ investigation.

And if Adam Schiff’s claim during in an interview with Reuters published earlier this evening holds any weight, Rosenstein could very well be next.

via RSS http://ift.tt/2DNWs0u Tyler Durden

Authored by Mac Slavo via SHTFplan.com,

Peter Schiff recently attended the Vancouver Resource Investment Conference. While he was there, he did an interview with Daniela Cambone of Kitco News and Schiff said gold is going to soar.

But Schiff (who predicted the 2008 recession) also explains why he believes now may be a good opportunity to invest in physical gold. Schiff said that the standard sentiment shared by many is that once the Federal Reserve jacks up interest rates, gold will stay level and unaffected. But that didn’t happen. Schiff said that the yellow metal has surprised the initial expectations that it would fall when the Fed raised rates; gold has climbed 9% since the Fed hiked last month.

Gold has not really rallied. It’s been going up, right? But it’s been creeping higher. Now, everybody expected it to fall. Everybody believed that as soon as the Fed hiked rates, gold’s gonna tank. And it didn’t tank. It rallied. -Peter Schiff

Investors tend to sell the rumor of rate hikes and buy the fact when in reality, the higher interest rates are not bearish for gold. But as Peter points out, that mindset still exists in the market.

But you know, the Fed keeps raising rates a little bit, every once in a while, and everybody still believes that, well, the Fed is raising rates, so that’s bearish for gold. So, everybody expects gold to fall, yet it continues to creep higher. But I think once it overcomes some of this resistance – it has a lot of resistance around $1,350 – and I think if we can decisively move above that and then get above $1,400, just to make sure it’s cleared out, then I think it’s off to the races.

Schiff also touched on the optimism in the markets, as he so often does, claiming still that the tax cuts won’t help much because the size of government hasn’t shrunk. He also says the rising interest rates will suck up the benefits of those tax cuts either way.

These tax cuts are not going to provide the economic boost that everybody believes.

I think the impact of rising interest rates and rising consumer prices will more than offset whatever benefits are to be had from the tax cuts. So, I think the economy is going to be weaker despite the tax cuts. I still think we’re heading into recession.

It’s rare to have this much optimism, but there are more problems now than there’s probably ever been, yet everybody is overlooking that. So, at some point, people are going to rush into gold, and the problem is there’s no one that’s going to rush out. So the price, I think, is just going to soar. I think you’re going to see 50 or 100 dollar moves per day up in the price of gold, once we break out.

Schiff holds firm that the consequence of the Federal Reserve manipulating the economy will be the crash of the dollar.

They actually made the bubbles bigger than the ones that popped. So now, the dollar’s collapse is going to be that much bigger, because it’s now a bigger bubble with more air to come out of it. And I think they have no more tricks up their sleeves. When this happens – it’s over.”

via RSS http://ift.tt/2nq5A1j Tyler Durden

One person is dead after an Amtrak train chartered to carry Republican senators and congressmen to a retreat collided with a truck in Virginia.

One person is dead after an Amtrak train chartered to carry Republican senators and congressmen to a retreat collided with a truck in Virginia.Follow us on Facebook and Twitter, and don’t forget to sign up for Reason’s daily updates for more content.

from Hit & Run http://ift.tt/2Et81ra

via IFTTT

San Francisco District Attorney George Gascón announced today that his office will proactively expunge and seal the records of misdemeanor marijuana offenders, the San Francisco Chronicle reports. The office will also resentence offenders who received a felony pot conviction.

San Francisco District Attorney George Gascón announced today that his office will proactively expunge and seal the records of misdemeanor marijuana offenders, the San Francisco Chronicle reports. The office will also resentence offenders who received a felony pot conviction.

Proposition 64, the 2016 referendum item that legalized recreational marijuana in California, allows pot offenders to petition for resentencing if their crime would have received a different penalty, or no penalty at all, under the new law.

Rather than wait for petitions, Gascón’s office is searching for eligible cases.

“The district attorney said his office will dismiss and seal more than 3,000 misdemeanor marijuana convictions in San Francisco dating back to 1975,” reports the Chronicle‘s Evan Sernoffsky. His office will also likely resentence “thousands of felony marijuana cases.”

A member of the California Assembly has introduced a bill that would make all Prop. 64–related expungements and resentencings automatic.

Retroactivity is a powerful tool for righting drug war wrongs, but prosecutors are often opposed to the practice. In Colorado, another state that has legalized marijuana, Assistant Attorney General Kevin McReynolds has reportedly declared that there’s “nothing irrational about holding someone accountable for a crime under the law in effect at the time.” If voters had wanted legalization to apply retroactively, he said during a 2016 hearing on retroactivity, “all they had to do was say so.”

At the federal level, the United States Sentencing Commission voted in 2014 to let tens of thousands of federal prisoners apply for retroactive sentence reductions after the commission changed the guidelines for drug trafficking.

But Congress failed to extend retroactivity to federal crack cocaine prisoners convicted before the Fair Sentencing Act passed in 2010. The new law substantially increased the amount of crack required to trigger a mandatory minimum sentence, and the failure to make it retroactive has left thousands of prisoners serving sentences that Congress has deemed excessive.

from Hit & Run http://ift.tt/2DOTPYs

via IFTTT