It’s bad enough, as has been evident for some time, that Donald Trump and his campaign were being spied upon by our own government, but it’s highly likely they were also subject to literal entrapment–at least a serious attempt was made.

I don’t mean the entrapment of promulgating the salacious Steele dossier both to the public and the FISA court as if it were the truth. That was more of a smear to justify a phony investigation. I mean something more subtle and LeCarré-like coming from the depths of our intelligence communities. It raises once more the question of the power of such agencies in a free society, a conundrum with no easy answers but of great significance to our lives.

For all his New York rough-and-tumble, Trump was an innocent abroad when he arrived in Washington. Way back in January 2017, he was warned by old-timer Chuck Schumer that “intel officials have six ways from Sunday at getting back at you.”

The Senate minority leader–Deep Stater par excellence–knew whereof he spoke. But Trump somehow survived the storm, although sometimes it seemed as if he wouldn’t. Now, some of the obvious parties –John K. Brennan and James Clapper with their apparatchik miens — have suddenly found themselves in the crosshairs, as the Washington Times notes:

Special counsel Robert Mueller’s finding that there was no Trumpcampaign conspiracy with Russia to steal the 2016 election has unleashed a tsunami of outrage toward Obama-era intelligence chiefs, particularly former CIA Director John O. Brennan and former FBI Director James B. Comey, who are accused of pushing the allegation during congressional hearings, in social media posts and in highly charged interviews on television over the past two years.

Former Director of National Intelligence James Clapper also leveled up highly publicized comments that President Trump could even be an “asset” of Russian President Vladimir Putin, part of a slew of remarks that critics say went far beyond the usual partisan sniping that can accompany a change of administrations.

More’s afoot here, however, considerably more because the entire American intelligence system and the unique power referred to by Schumer are also now in those same crosshairs, as they should be. But many of the men and women involved are less overtly Soviet in their style than Mssrs. Brennan and Clapper and slip more easily under the radar.

Notable among these, and perhaps able to reveal much of the McGuffin to the mystery of where this all started and how, is Stefan Halper. Mr. Halper is “an American foreign policy scholar and Senior Fellow at the University of Cambridgewhere he is a Life Fellow at Magdalene College and directs the Department of Politics and International Studies.” He is also a spook who worked for Nixon, Ford, and Reagan, no less, and was a principle American connection to the UK’s MI-6.

A top FBI official admitted to Congressional investigators last year that the agency had contacts within the Trump campaign as part of operation “Crossfire Hurricane,” which sounds a lot like FBI “informant” Stefan Halper – a former Oxford University professor who was paid over $1 million by the Obama Department of Defense between 2012 and 2018, with nearly half of it surrounding the 2016 US election.

“Crossfire Hurricane,” as most know, is the codename the wannabe hipsters at the FBI gave the Trump-Russia investigation. But more important is the word “before” in Ms. Cleveland’s title.

The Post further noted that the academic, since identified as Stefan Halper, first met with Trump campaign advisor Carter Page “a few weeks before the opening of the investigation,” and then after Crossfire Hurricane’s July 31, 2016, start, he met again with Carter Page and “with Trump campaign co-chairman Sam Clovis,” offering the latter his “foreign-policy expertise” for the Trump team. Then in September, Halper “reached out to George Papadopoulos, an unpaid foreign-policy adviser for the campaign, inviting him to London to work on a research paper.”

Papadopoulos and Page are the two naifs of the most obvious sort (sorry, guys) we have all seen on television who spent the last couple of years having to defend themselves against absurd charges. Considering the timing, it’s pretty obvious they were being set up (i. e. entrapped) on some level well back during the Obama administration.

Who ordered it is the obvious question, but I’m not going to leave it there. I suggest that an attempt was being made to implant Halper in the Trump campaign, one way or another, not just for spying purposes but actually to help create this collusion of the campaign with Russia–that is, to help manufacture it.

Putting it another way, someone or some group wanted to create — or, more subtly, to encourage the creation — of Trump-Russia collusion from the inside in order to destroy Trump before, or failing that, after he was elected.

How’s that for a nefarious plot? Worthy of LeCarré or maybe even Graham Greene. But is it true? I wouldn’t bet against it. Something close anyway.

By the way, if I am right, this won’t be the first time for Halper. And unfortunately for Republicans, the shoe was then on the proverbial other foot. As Glenn Greenwald wrote last year:

Four decades ago, Halper was responsible for a long-forgotten spying scandal involving the 1980 election, in which the Reagan campaign – using CIA officials managed by Halper, reportedly under the direction of former CIA Director and then-Vice-Presidential candidate George H.W. Bush – got caught running a spying operation from inside the Carter administration. The plot involved CIA operatives passing classified information about Carter’s foreign policy to Reagan campaign officials in order to ensure the Reagan campaign knew of any foreign policy decisions that Carter was considering.

Republicans can console themselves that their malfeasance was more benign, relatively. This new one was outright sedition involving a foreign power. It is a blow to the heart of our democratic republic. We need Halper, under oath and unredacted. Whether that’s possible is another question.

via ZeroHedge News https://ift.tt/2TKYcuD Tyler Durden

Hollywood starts have launched a boycott of nine Brunei-owned hotels after the tiny Islamic nation on the island of Borneo announced that they would be enforcing the death penalty for gay sex and adultery.

While the new laws were announced five years ago with the nation’s adoption of Sharia law, the death penalty for homsexual sex and adultery will begin on April 3, according to CNN.

Sultan Hassanal Bolkiah of Brunei with his wife Raja Isteri Pengiran Anak Saleha

Spearheaded by actor George Clooney, the boycott has been joined by the likes of Sharon Stone, Elton John, Jamie Lee Curtis, George Takei and others, who refuse to patronize the Brunei-owned establishments:

Here are the hotels to boycott:

The Dorchester, London

45 Park Lane, London

Coworth Park, UK

The Beverly Hills Hotel, Beverly Hills

Hotel Bel-Air, Los Angeles

Le Meurice, Paris

Hotel Plaza Athenee, Paris

Hotel Eden, Rome

Hotel Principe di Savoia, Mi

Please boycott the #BeverlyHillsHotel and the #HotelBelAir as this law has been restarted!!!!! This is the owner. Thank you. S

Brunei Bans Buggery; Gays To Be Stoned To Death Under Sharia Law | Zero Hedge https://t.co/g3Bu17QQtE

I stand with George Clooney, a good man doing the right thing, fighting an unjust and barbaric law. George Clooney: Boycott Sultan Of Brunei’s Hotels Laws Against LGBTQs | Deadline https://t.co/fjR2hv1sTb

“I commend my friend, George Clooney, for taking a stand against the anti-gay discrimination and bigotry taking place in the nation of Brunei – a place where gay people are brutalised, or worse – by boycotting the sultan’s hotels,” tweeted Elton John on Saturday.

The 72-year-old, a veteran gay rights campaigner, said his “heart went out” to staff at the hotels, but that “we must send a message, however we can, that such treatment is unacceptable”. –The Guardian

Last week Clooney called for the boycot, saying “Every single time we stay at or take meetings at or dine at any of these nine hotels, we are putting money directly into the pockets of men who choose to stone and whip to death their own citizens for being gay or accused of adultery.”

Brunei has been ruled for 51 years by Sultan Hassanal Bolkiah as an absolute monarchy. While homosexuality is already illegal there, it will now become a capital offense.

Will they also boycott Saudi properties?

There are now 11 countries in the world where homosexual acts are punishable by death, including Afghanistan, Iran and Saudi Arabia.

Kingom Hotel Investments, owned by Saudi Prince Alwaleed, owns nearly 50% of the Four Seasons hotel chain, while Microsoft co-founder Bill Gates’ Cascade Investment Management owns approximately the same amount.

***

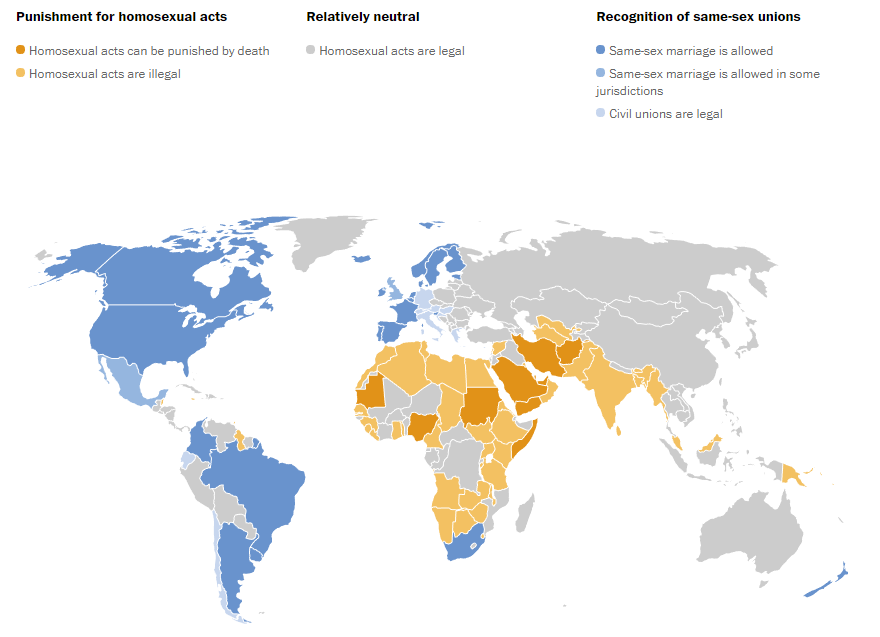

As we noted last week, here’s a map of mostly Islamic republics where homosexual acts are illegal and/or punishable by death.

Places where homosexual acts can be punished by death

Afghanistan

The Afghan Penal Code does not refer to homosexual acts, but Article 130 of the Constitution allows recourse to be made to Sharia law, which prohibits same-sex sexual activity in general. Afghanistan’s Sharia law criminalizes same-sex sexual acts with a maximum of the death penalty. No known cases of death sentences have been meted out since the end of Taliban rule.

Iran

In accordance with sharia law, homosexual intercourse between men can be punished by death, and men can be flogged for lesser acts such as kissing. Women may be flogged.

Nigeria

Federal law classifies homosexual behavior as a felony punishable by imprisonment, but several states have adopted sharia law and imposed a death penalty for men. A law signed in early January makes it illegal for gay people countrywide to hold a meeting or form clubs.

Qatar

Sharia law in Qatar applies only to Muslims, who can be put to death for extramarital sex, regardless of sexual orientation.

Saudi Arabia

Under the country’s interpretation of sharia law, a married man engaging in sodomy or any non-Muslim who commits sodomy with a Muslim can be stoned to death. All sex outside of marriage is illegal.

Somalia

The penal code stipulates prison, but in some southern regions, Islamic courts have imposed Sharia law and the death penalty.

Sudan

Three-time offenders under the sodomy law can be put to death; first and second convictions result in flogging and imprisonment. Southern parts of the country have adopted more lenient laws.

Yemen

According to 1994 penal code, married men can be sentenced to death by stoning for homosexual intercourse. Unmarried men face whipping or one year in prison. Women face up to seven years in prison.

Mauritania

Muslim men engaging in homosexual sex can be stoned to death, according to a 1984 law, though none have been executed so far. Women face prison.

United Arab Emirates

Lawyers in the country and other experts disagree on whether federal law prescribes the death penalty for consensual homosexual sex or only for rape. In a recent Amnesty International report, the organization said it was not aware of any death sentences for homosexual acts. All sexual acts outside of marriage are banned.

And now we can add Brunei.

—

There are 65 countries where homosexual acts are illegal

Noteworthy laws:

Pakistan

Death penalty laws exist but are unlikely to be implemented, according to the 2016 IGLA report.

Chad

A 2014 law makes same-sex relations a crime punishable by 15 to 20 years in prison.

India

A ban on same-sex relationships was tossed by the legal system in 2009 but reinstated in 2013. The supreme court said the government, not the courts, would have to change the law.

via ZeroHedge News https://ift.tt/2FMvzJZ Tyler Durden

Why is it that no one defends free markets, and socialism, despite all the evidence of its failures, comes back again and again? Unsurprisingly, the answer lies in politics, which have always led to a boom-bust cycle of collective behaviour. Furthering our understanding of this phenomenon is timely because the old advanced economies, burdened by a combination of existing and future debt, appear to be on the verge of an unhappily coordinated bust. But that does not automatically return us to the free markets some of us long for.

Cycles of collective behavior

Throughout history there have been few long-lasting periods of truly free markets. Contemporary exceptions are confined to some small island states, forced to be entrepreneurial by their size and position vis-à-vis the larger nations with which they trade. The governments of these islands know that the state itself is not suited to entrepreneurship. Only by the state guarding the freedom of island markets and the sanctity of property rights can entrepreneurs serve the people in these communities and create wealth for all.

This is not the normal condition for larger nations. Before the Scottish enlightenment which nurtured David Hume and Adam Smith, the benefits of free trade were barely understood. Since then, the wealth created by free trade and sound money has nearly always been the springboard for detrimental change. Sometimes a political strongman, like Mao or Lenin dictates to the people what they can and cannot do. Alternatively, a leader courts popularity by taxing heavily the few for the alleged benefit of the masses. This is the model of welfare states today. Debasement of the means of exchange is an extension of these socialising policies, furthering the transfer of personal wealth to the state.

To understand why free markets are more often than not unpopular, we must put them into a context of human behaviour. In this regard we can stylise a cycle of collective behaviour into three characteristic phases.

The first is a lawless condition of no secure ownership of property rights; in the absence of enforceable law the means of possession are necessarily violent and uncertain. It is the natural condition of tribalism and pre-civilisation societies. It is the condition to which humanity returns when the cycle completes.

The second phase is the consolidation of property ownership, with enforceable laws to define and protect it. Out of the chaos that fails to advance the condition of the people comes order, and with it the aggregation of the means of production. Capital in all the forms necessary for production accumulates, and being scarce, is used most efficiently. The backbone of this phase is freedom for the individual to dispose of his or her resources at will. The pace of improvement in the human condition is governed by the level of accumulated wealth and technological innovation.

The third phase is the abandonment of free markets in favour of state control. The state, whose primary function in economic terms is to act as provider and facilitator of the law, increasingly supresses commerce by extracting escalating levels of tax. Taxes are imposed to redistribute wealth from those that earned and conserved it to those that did not. The state takes control of money, issuing its own currency which it can print at will. The damages to the economy are covered up by all the artifices available to the state.

The state regulates. The state confiscates. The state deprives its people of their freedom. The state’s demands become so insatiable, so counterproductive, so impoverishing that the economy collapses back into the first phase of the next cycle.

That is our theoretical cycle of collective behaviour. Out of chaos is created progress. Out of progress lies the course to destruction. The best of these times is the free markets of the second phase. No one defends them.

Empirical evidence of the cycle.

The assembly of German states into a unified nation in 1871 gave credence to a new socialising phenomenon, whereby Bismarck, Germany’s first Chancellor, promoted the state as a socialising entity, superseding free markets. He was the first politician to create a welfare state, introducing accident and old-age insurance and socialised medicine. Shortly after unification, in the mid-1870s Bismarck abandoned free trade and introduced trade protectionism.

His policies echoed the principles of the German Historical School, which drove intellectual thought in the Prussian administration. The Historical School rejected the classical economics of Smith, Ricardo and Mill in favour of a controlling state, backed up by analysis of historical events, hence the name. These lessons were applied to the changing conditions at that time. Workers were moving from the land into new factories, and it was the German establishment’s outdated response to an entirely new social phenomenon.

The creation of a new German socialising state and the denial of economic liberalism inevitably led to the founding of Chartalism, the state theory of money, which stated that only the state has the right to determine the currency used by the people. Georg Knapp published his State Theory of Money in 1905. He handed Bismarck the key to unlock constraints on state spending. The state was then able to consolidate its potential, both in its bureaucracy and military armament. We all know what happened: it fed into to the First World War and in 1923 resulted in the collapse of the currency.

It is worth reflecting that a cycle of events occurred taking ordinary Germans to full state socialism from a freedom to improve their personal circumstances. The start of it was promising, with the introduction of the Zollverein, a customs union between independent German-speaking states. The roots of the Zollverein were in the 1830s, consolidated and formalised in 1861. It preceded the formation of a greater Germany in 1871. It was the gateway to political union, and statist economic management.

It is a doppelganger for the development of the European Union today, but the underlying point for EU-watchers is that it was a cycle of events, taking a nation through the erosion of laissez-faire to full state domination of economic activity and monetary affairs.

In Germany’s case, the political consequences of the First World War and the collapse of the currency were not the end of the story, or the cycle. The rise of extreme fascist socialism finally led to the destruction of the German state in 1945. The return to free markets under Ludwig Erhard’s guidance followed his appointment as Director of the Economic Council for the Occupation Zone and completed the cycle.

Cometh the hour, cometh the man. Soviet-occupied Germany was not so lucky. Erhard had to ignore the instincts and orders of his fellow American and British military committee members, who were stuck in a bureaucratic militaristic frame of mind. In July 1948, without consulting them, Erhard abolished all rationing and price controls. Almost instantly, shops reopened, food became available, the suppressed mood lifted, and people began to rebuild their lives. By way of contrast, victorious socialist Britain continued with rationing until 1954, when meat rationing finally ended.

The evolution in Germany from free markets through increasingly destructive statism and back again to free markets had taken nearly eighty years from unification in 1871. Russia suffered a similar, though initially more dramatic, socialist change from relatively free markets. Instead of a progressive introduction of state control and loss of personal freedom, it was sudden and absolute. After three years of civil war and using a ready-made Marxist template Lenin seized and consolidated control. Both Lenin and Stalin his successor were ruthless in their suppression of freedom. Tens of millions were deemed to be enemies of the state, which included those who merely disagreed or of the wrong race. They were executed or sent to the gulags. That suppression lasted until the soviets had impoverished their people to the point where there was nothing left. In 1989, after seventy-odd years the USSR finally collapsed.

The German and Russian experiences tell us in their own ways that because the beneficiaries of free trade fail to defend it, free trade does not last. Anyone reading about life in Vienna before the First World War would be struck by the widespread prosperity, freedom and artistic flowering of the age, which was destroyed by the war and a subsequent collapse of the currency. It is unfashionable in our socialist times to defend those pre-war years as good times.

I personally grew up with the free-market prosperity of Britain’s African colonies; a prosperity that benefited not just the better-off Europeans but indigenous African and Asian communities as well. That was destroyed by political imperatives, the call for independence from British rule by those who had benefited from the free markets they set out to then destroy. Fully-functioning free-market economies were replaced throughout Africa by corrupt elites that still steal their way to personal prosperity.

It is no accident that post-independence African leaders embraced socialism as the justification for their actions. They argued that the European landowners had seized property which was in the communal ownership of the tribes, and that a newly-independent state had the right to seize it back. But they ignored the fact that before the arrival of Europeans there was no ownership nor property law to define it. Occupation was by force. It is a no more than a common socialist justification for the state to acquire for itself private property.

In only fifty years, free markets had taken the ordinary native in the African heartlands from ignorance of the wheel to the age of jet engines and skyscrapers. Never before have tribal communities witnessed such rapid social change. We forget the appalling conditions and routine cruelty that existed before the introduction of western capitalism. Those conditions are best summed up in a quote from Tacitus, writing about the German tribes in 98AD: “It seems feckless, nay more, even slothful, to acquire something by toil and sweat which you could grab by the shedding of blood.” He could have been describing the cattle raids that still occur today in Kenya’s Northern Frontier District and Laikipia.

Nearly two millennia after Tacitus described tribal Germania, in Africa similar disorder reigned before white settlers developed the land. To escape a subsistence stasis that had seemingly existed for ever, disorder had to be replaced by the white man’s order. Through the introduction of capital and property ownership, free markets allowed the whole population to rapidly improve its condition.

Without these crucial ingredients there can be no progress. Socialism unwittingly returns civilisation to an unenlightened state by encroaching upon, then abolishing, both property ownership and the accumulation of capital. The economy is hindered in its progress, until it withers on the vine. A nation then returns to its pre-capitalist state of lawlessness, corruption, brutality and widespread poverty. Once again, cattle raiding and similar actions become the means of ownership.

But if this repetitive cycle is so obvious, why does humanity fall into the same cyclical trap time and again?

The psychology of denying free markets

Cycles of human behaviour require a build-up of human prejudice until it becomes unsustainable. One human prejudice which is little examined is why establishments frequently stick to their convictions while denying reasonable debate. As we have seen, much of the answer is that a version of self-serving economic dogma becomes central to the credibility of statist policies. We see it today with our post-Keynesian economic establishment driving economic and monetary policies, while denying the superiority of unfettered markets in these matters. Anyone who challenges the unreason of the establishment’s economics will risk personal vilification and be side-lined.

Create the belief structure and the government can justify any action. Leadership becomes more effective when it is based on prevailing doctrines, with minds firmly closed to all evidence to the contrary. All types of socialism demonstrate opinions insulated from inconvenient contradictions. A socialising government can then appear independent and fair-minded, serving the people when it actually serves itself.

New dogmas become entrenched. The government and also the public, like our hunter-gatherer forebears in their communal caves, huddle round the mutual safety of the new consensus. Concerning the government’s contradictions, comfort is sought by the public from the government itself. It becomes an iterative process that allows the state to drift remorselessly away from free markets, not only with public consent, but public encouragement. It is the basis of groupthink, the enemy of reason.

To the building self-ignorance is added an overestimation of understanding complex issues: an understanding-bias that is reinforced by debate on terms set by society itself, represented by the media. Editors select complex issues which they reduce to simplified choices, that are then discussed by invited participants. The debate always proceeds on the basis of which government intervention or regulation is most likely to achieve a given objective. Spoil the party by insisting that personal freedom is preferable to any government intervention, you damage the media ratings and you will be deemed a maverick, never to be invited back.

Contradiction becomes too difficult to take. A form of naïve realism develops, whereby talking heads promote themselves as supporting the assimilation of a consensus. Furthermore, they believe that those that do not subscribe to the consensus are irrational, biased, uneducated and ignorant. By these means, the benefits of free markets and individualism are increasingly suppressed. Economists are paid to promote policies in favour of the state’s control of money. The universities develop an anti-market bias, and free-market economists are unable to secure paid professorships.

The position these toadying experts occupy was summed up by John Ioannidis, a professor of medicine at Stamford University:

“Scientists in a given field may be prejudiced purely because of their belief in a scientific theory or commitment to their own findings… Prestigious investigators may suppress via the peer review process the appearance and dissemination of findings that refute their findings, thus condemning their field to perpetuate false dogma. Empirical evidence on expert opinion shows it is extremely unreliable.”

Disappointingly, we all assume scientists are disciplined in their specialisations and unbiased. Not so. In economics, there is the extra problem of human unpredictability, to which is added a total lack of precise definition. Soundly-reasoned theory is swept aside by the introduction of unreliable, and often extraneous statistics as the feedstock for mathematical equations. Reason, freedom and free markets are the casualties.

Instead of reasoning for ourselves and recognising the flaws in debate, we trust an elite to guide our thoughts with their knowledge. Alongside the elite there is a cadre of self-anointing experts consulted by the media. We place value on their independence. We see them as informed insiders, but we forget their privileged access depends solely on supporting the party line. It is a profitable after-life for those who had power, a self-congratulatory basis for the concealed promotion of social policy.

When it gets left behind by progress, the static socialist state eventually becomes the author of its own destruction. Only then might the psychological consensus of denying free markets be broken. If we are lucky, out of the ensuing chaos a new commitment to free markets rapidly emerges. More likely, it becomes the opportunity for extremism, as Germany showed in the aftermath of its inflation collapse of 1923.

Contemporary socialist evolutions

As economic historians, we observe the faults of others usually without recognising them in ourselves, mainly for the psychological reasons noted above. Most economic historians selectively approach the subject with the bias of their culture and generation. The story of Bismarck’s Germany is hardly known in English literature and the lessons are lost in an English-speaking world. The fall of communism in the USSR is fresh in our minds, but the struggles of the state under Yeltsin to replace it with a market-based economy and the ensuing corruption is more topical.

In Britain, many have forgotten the appalling services and products of nationalised monopolies: British Railways, British Telecom, British Leyland, to name just a few. Consequently, the Brits as well as other socialists in the West are never adequately deterred in their antagonism against free markets to change their minds. Bernie Sanders’ desire to run again for President and the Marxism of Jeremy Corbin are testament to the short-mindedness of the voting public. It is a wilful ignorance that defends socialism and never defends free markets.

In America, socialism is being challenged by President Trump. Without us examining his beliefs too closely, he obviously knows that the government establishment has been strangling the US economy. His dislike of the Democrats and their policies under Obama identifies him as an enemy of socialism. But as a free-marketeer, Trump does not defend free markets. Instead, he ends up defending crony-capitalism, military spending and monetary inflation. His trade protectionism, strongly echoing Bismarck’s policies in the late nineteenth century, is similarly socialism under the banner of nationalism. Far from rescinding the socialist tide, Donald Trump is swimming in it.

Trump’s trade policies, as I’ve argued in another article, are driving America and therefore the world into a deep recession. Under current monetary policies the result will be a spectacular increase in monetary inflation, which could lead to the destruction of the dollar. If this happens, Trump almost certainly will be blamed, not socialism. That being the case, the destruction of the American economy and perhaps the dollar with it will not be the end of socialism and the return to free markets. By not properly understanding free markets, President Trump risks condemning his nation and his legacy to a more intense post-crisis socialism similar to that which fuelled fascism in 1920s Germany.

If so, we can only hope the period will be brief. Economists in the free-market tradition can only forecast the likely economic and monetary consequences of current policies. The laissez-faire tradition tells us a failing government should stop intervening and restrict itself to ensuring basic criminal and contract law is enforced. It should stop monetary inflation. As Ludwig Erhard demonstrated in 1948, free markets left alone rapidly restore economic order. But that is not the socialising instinct. As long as there is breath in socialism free markets will continue to be supressed.

The foundation of the European Union echoes the tactical approach of Bismarck: corral a group of nations into a Zollverein customs union, then steer them towards political integration. As the German Historical School was for Bismarck, Marxist-socialism becomes the driving force for the EU, innocuously at first by encouraging free trade within the union. Free trade is then hampered by bureaucratic regulation in the names of common standards, fairness and further integration. Already planned are the imposition of new federal taxes to extend the power of the Brussels government, and the building of a new pan-European military force. Pure Bismarck, and pure Brussels.

Witness the struggle with Brexit, where it turns out the Westminster Parliament is comprised of an overwhelming majority of members who are committed to the EU’s socialising masterplan to the exclusion of democracy. Even a majority of Tory MPs, the party of free enterprise, prefers a federal socialist system to free markets.

It is the stuff of late-stage socialism. The whole world is in its grip, rather than just Germany, just the USSR, just America, just the EU, or just Britain. And these are only some among the traditionally advanced nations. Being cyclical, the bankruptcy of it all in time is for sure. It is set to throw up greater challenges than ever seen before because of its ubiquity. Assuming it does not end in a nuclear destruction of the human race, we will eventually turn our backs on the follies of socialising governments and go back to free markets. Then the cycle of humanity’s socialising madness will start all over again.

via ZeroHedge News https://ift.tt/2FEJ3Gn Tyler Durden

Rumors and questions about Apple’s secretive automotive project have been swirling for years. Does the company intend to build its own EV, or is it just focusing on autonomous driving software? Has “Project Titan” been killed off or is it still actively being pursued behind the scenes? Today, we have more clarity on the issue – as a result of yet another Tesla executive departure… and reapparance.

Tesla’s former head of electric powertrains, Michael Schwekutsch, who was reported to have left the company earlier this month, has re-surfaced at Apple.

Schwekutsch’s departure from Tesla was described as a “big loss for Tesla” by the pro-Tesla blog electrek back in early March. They described him as “a hardcore electric powertrain engineer” who helped engineer the Model 3 powertrain. While at Tesla he also worked on the development of “leading edge Drive Systems like the one of the Tesla Roadster II and Tesla Semi/Tesla Truck.”

He has now joined Apple’s Special Project Group, which includes the company’s Project Titan division, according to electrek. This seems to clear up any confusion as to whether or not Apple is actually working on vehicle hardware. It was previously believed that Apple’s Project Titan could only consist of a self-driving software system for other vehicles.

Bulls and bears will likely see this event through their respective lenses. Bears may claim it as proof that Apple’s coming EV project will act as direct competition to Tesla. Bulls will probably try to argue (the aggressive point) that this is foreshadowing for Tesla to eventually partner with, or be acquired by, Apple.

Schwekutsch will join other former Tesla executives like Doug Field and Bob Mansfield, both of whom were longtime engineering executives at Tesla. Apple is also being said to be hiring “several other former Tesla employees”.

More importantly, it looks like the nearly $1 trillion market cap behemoth – desperate for new avenues of “growth” – will build an EV from the ground up, introducing the question of what a real foray into technology EVs would look like when organized, run by a profitable company, and overseen by competent management.

If Apple winds up making an EV (as long as it’s not the Howard), one assumes that Apple’s eventual vehicle might actually deliver the unfulfilled promises and half truths that Tesla cultists have clung to for the last half decade. On top of that, Apple has the brand equity, engineering, resources and most importantly, unlimited capital to make a vehicle that could push Tesla into irrelevance.

In 2015, Elon Musk said about Apple:

“They have hired people we’ve fired. We always jokingly call Apple the ‘Tesla Graveyard.”

Let’s see how soon it is before Musk is eating those words.

via ZeroHedge News https://ift.tt/2TR9HAY Tyler Durden

There have been two conflicting themes in the market so far in 2019: the first one has been the relentless selling by equity investors since the start of the new year despite the market’s remarkable surge in 2019, offset by buying of fixed income securities in a scramble to lock up yield ahead of potential rate cuts and/or QE by the Fed later in 2019 or in 2020 (most recently discussed here).

The second theme, which is closely tied to the first, has been the market’s so-called “jaws”, where stocks have moved sharply higher while yields have tumbled to multi-year lows, sparking investor confusion: is the bond market right in anticipating a period of acute deflation and/or recession, or is it wrong and stocks, which are less than 5% below their all-time highs, correct in their optimistic outlook.

As Goldman’s David Kostin writes, it is this decoupling that is dominating client discussions:

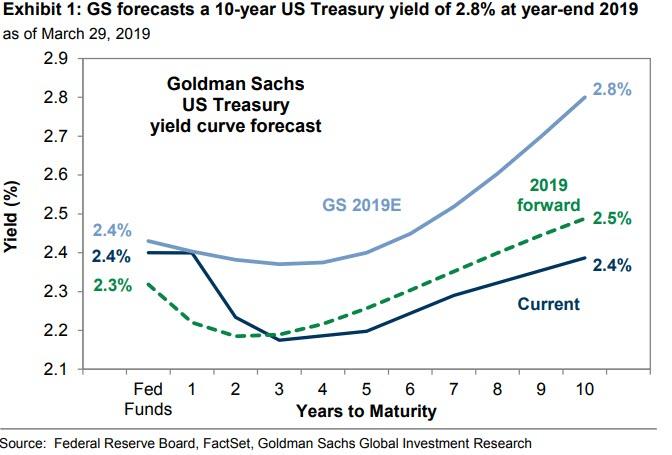

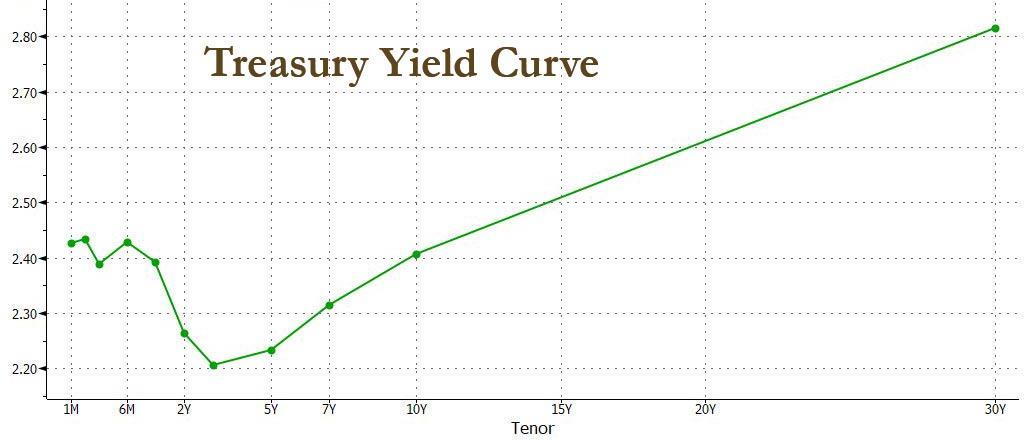

Ten-year US Treasury yields have plunged to 2.4%. From an investor perspective, stable equity prices coupled with falling interest rates means a wider earnings yield gap and implies a more attractive relative value for stocks assuming the economy does not fall into recession.

As Kostin recounts, one client told the chief Goldman equity strategist, that it all really “depends from which direction the jaws close – through higher rates or via lower equity prices.”

That’s the question that the bank tries to answer in its latest US Weekly Kickstart report.

For its part, Goldman remains as usual cautiously optimistic: The bank which last December incorrectly predicted no less than 4 rate hikes in 2019, now forecasts the 10-year US Treasury yield will rise to 2.8% at year-end 2019 (down from the previous forecast of 3.0%).

As Kostin adds, the lower rate would be conducive to equity valuations remaining at or above the current elevated level of 16.8x, which is in the 79th percentile in absolute terms versus the past 30 years but at just the 29th percentile relative to interest rates.

The 90 bp plunge in the 10-year Treasury yield since last September (3.2%) and 30 bp drop since year-end (2.7%) has caused the yield gap to widen to 350 bp, which is considerably above the 40-year average (230 bp).

Kostin then falls back on the bank’s Treasury forecast as one supporting risk assets, noting that “the reduced pace of rising yields to less than 5 bp per month is encouraging for equity investors” and explaining that “historically, the S&P 500 has posted positive returns when the 10-year Treasury yield has increased by less than one standard deviation relative to the prior 36 months.”

That’s the good news – inasmuch as Goldman is correct that the drop in yields is now over and won’t accelerate further, which in turn would strongly hint that at least the bond market is confident of an imminent recession; the bad news is the ongoing deterioration in everything from the economy at the macro level, to corporate margins and earnings at the micro.

Starting with the first, Goldman notes that “economic data have been sending mixed signals” and notes that “this week, below-consensus housing starts contributed to the continued negative reading of our US MAP index of economic data surprises. Consumer Confidence disappointed at 124 vs. consensus 132.”

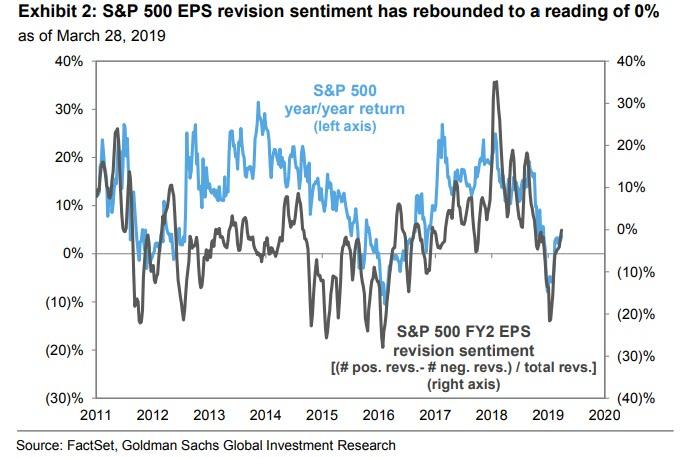

Next up is the deteriorating corporate earnings picture, with Q1 looking especially grim with the risk of a mini earnings recession on the horizon. To be sure, starting with Apple in early January, management teams have been tempering earnings expectations. In fact, more than 140 firms have reduced 2019 EPS guidance since the start of the year and 67 firms have cut guidance by more than 2%. As Goldman notes, earnings revisions have been more negative than usual. During the past three months, analysts have cut expectations for full-year 2019 S&P 500 EPS by 4%, nearly four times the usual rate of roughly 1% per quarter. On the other hand, 1-month revision sentiment has rebounded to a reading of 0%.

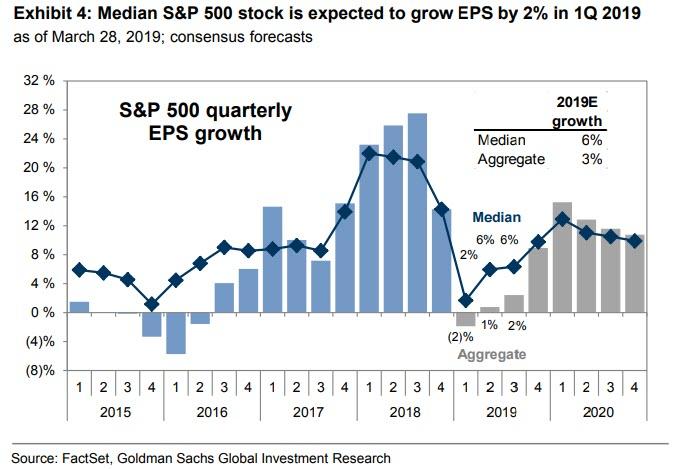

And while sellside earnings sentiment may have finally troughed, consensus now expects aggregate S&P 500 EPS to fall by 2% in 1Q, which would be the first year/year decline since 2Q 2016 even as consensus still expects strong 5% sales growth. One thing to note: while the average print will be negative, the median S&P 500 stock is expected to grow EPS by 2%, indicating that a few outsized firms (AAPL, MU, WDC, CVX, XOM, NVDA) are weighing on the aggregate measure according to Goldman. This dichotomy is also present for full-year 2019 EPS growth, with the median firm projected to grow EPS by 6% while the aggregate index grows by just 3%.

The weakness in Q2 earnings has two main causes: a sharp drop in international sales, arguably a consequence of the US-China trade war, and sliding profit margins, the result of rising labor costs and the highest wage growth since the financial crisis.

Regarding the first, Goldman observes that negative S&P 500 EPS growth in 1Q will be driven by sectors with the highest international revenue exposure: Materials (-18%), Energy (-18%), and Info Tech (-8%).

With at least 40% of revenues derived from outside the US, these sectors have been most exposed to the slowdown in global growth as our Global CAI slowed to an average of 3.2% in 1Q 2019 from 4.6% in 1Q 2018. Adding to the headwinds, the 13% year/year decline in the price of oil will weigh on Energy EPS. Previously, we highlighted the reduced price of oil as a potential risk to our 2019E S&P 500 EPS forecast of $173 (+6% vs. 2018), with potential downside of $5 to $168 (+3%).

As for shrinking margins, Goldman cautions that EBIT margins are expected to compress by 112 bp in 1Q 2019, the largest quarterly contraction since 4Q 2014, and adds that margin pressure will be felt in every sector except Consumer Staples, which is benefiting from the reclassification of lower-margin CVS into Health Care. Excluding this reclassification, Consumer Staples EBIT

margin would be flat (-2 bp) and Health Care would experience an even further reduction (-217 bp).

This is a major problem because in addition to a modest increase in the effective tax rate in 2019 to 21% from 19% in 2018, this decline in EBIT margins would contribute to the largest expected decline in S&P 500 net margins since the Financial Crisis. To be sure, executives have cautioned investors on margins as they reported 4Q 2018 earnings, citing both trade tensions with China and the continued tightening of the labor market as factors contributing to margin uncertainty in 2019.

And while despite the adversity of sliding margins and profits amid a global economic slowdown is not enough to dent Goldman’s optimis, with the bank issuing its reco du jour, and pointing out that as margin pressures mount, “investors should focus on companies that have demonstrated the ability to maintain margins through pricing power” one other bank is not so sure.

In his latest take on how much market complacency is now built into the market, JPMorgan’s Nikolaos Panigirtzoglou goes back to the question of the market “jaws” and comes out with a far less sanguine conclusion. Noting that the strong rally in equity, credit and commodity markets over the past quarter “has significantly reduced their cushion against growth downside risks”, the JPM strategist concludes that “there appears to be a disconnect between rate and risky markets at the moment with rate markets signaling more elevated growth and recessions risks, and equity, credit and commodity markets pricing in more optimistic scenarios.”

Finally, here is why the question of which was the market’s “alligator jaws” close that is keeping Goldman clients up at night, is so critical – according to JPMorgan calculations…

US equity markets appear to be currently pricing in only 15% chance of a typical US recession and discount only 3% decline in earnings.

In contrast, the 85bp fall in 5-year US Treasury yields from their early November peak points to 80% chance of a US recession.

In other words, stocks are pricing in smooth sailing while bonds are now certain a recession is coming. And while historically bonds have always been right in the end, this time equities have the explicit backstop of the Fed. So will 23-year-old momo traders and Jerome Powell be smarter than the “smartest traders in the room”, and will yields jump in the next few weeks? The answer may reveal itself as soon as mid to late April when the bulk of companies will report Q1 earnings and share their outlook for the rest of the year, which if it is anything like the start of 2019, would quickly cripple the growing stock market optimism.

via ZeroHedge News https://ift.tt/2FF9Ke4 Tyler Durden

A popular comedian seen as “soft” on Russia and who said he would actually sit down with Vladimir Putin to talk peace looks to upset Ukrainian politics, as he’s significantly leading in exit polls during Sunday’s presidential elections in Ukraine.

Volodymyr Zelenskiy, who incidentally played the president on TV as part of his comedy career has according to exit polls cited by the BBCreceived 30.4% of the vote, with current president Petro Poroshenko second with 17.8%.

Ukrainian comedian and presidential candidate Volodymyr Zelensky, via Pacifica Press.

“I’m very happy but this is not the final result,” Zelenskiy told the BBC moments after after the exit polls were announced, while incumbent Poroshenko, who has led Ukraine since the February 2014 Maidan conflict that toppled former pro-Russian President Viktor Yanukovych, described the forecast of his defeat as a “harsh lesson”.

Though there have been reports of election violations, President Poroshenko acknowledged Sunday’s presidential election as “free” and having legitimately “met international standards,” according to Reuters. The country of 44 million is choosing from a packed field of 39 presidential candidates; however Zlelenksy — already very familiar to much of the population through TV — has consistently polled as the front runner.

Ukraine’s president will be determined during the April 21 run-off, where Zelensky is projected to beat both Poroshenko and former Prime Minister Yulia Tymoshenko. The 41-year-old Zelensky is as pro-EU as much of the rest of the field, but has kept things deliberately light, presenting himself as part-politician, part satirical comic, who has done little to campaign beyond presenting himself as a “common sense” citizen.

Interestingly, his willingness to speak both Ukrainian and Russian in public forums has made him popular in the Russian-speaking east of the country, according to the BBC, which further reports:

Mr Zelenskiy is aiming to turn his satirical TV show Servant of the People – in which he portrays an ordinary citizen who becomes president after fighting corruption – into reality.

He has torn up the rulebook for election campaigning, staging no rallies and few interviews, and appears to have no strong political views apart from a wish to be new and different.

His extensive use of social media appealed to younger voters.

It could be Ukrainians are ready for a general calming of tensions over and against Poroshenko’s tough anti-Russian and pro-nationalist talk of “Army, Language, Faith” — and amid his corruption allegations and a recent scandal involving defense procurement.

Exit polling suggests Zelenskiy will face president Poroshenko in the 2nd round on April 21. Poroshenko will try to make the newcomer look stupid in TV debates, Zelenskiy will harp on the president’s wealth & corruption scandals. @RFERLpic.twitter.com/YjcNUm94Ok

Electing a comedian and political satirist certainly represents broad disillusionment with Ukraine’s political elite, which have overseen years of intermittent regional conflict and a stagnant economy. Zelenskiy is seen as a more familiar “common man” and political outsider with no experience, compared to chocolate magnate Poroshenko, who is among Ukrainian’s wealthiest people.

Zelenskiy said on Sunday just after casting his ballot in Kiev “A new life, a normal life is starting.” He added his hope for a new political landscape marked by “a life without corruption, without bribes.”

via ZeroHedge News https://ift.tt/2JVlgap Tyler Durden

Most likely Alexandria Ocasio-Cortez (AOC) is the future of the Democratic Party – and of the U.S.

Why?

She’s cute, vivacious, charming, different, outspoken, and has a plan to Make America Great Again. And she – or at least her handlers – is shrewd. She realized she could win by ringing doorbells in her district, where voter turnout was very low, and about 70% are non-white. There was zero motivation for residents to turn out for the tired, corrupt, old hack of a white man she ran against.

The things she says are politically astute, although she herself doesn’t seem very intelligent. In fact, she’s probably quite stupid. But let’s define the word “stupid.” Otherwise, it’s just a meaningless pejorative – name-calling. Which I want to avoid.

But in fact she doesn’t appear to have a very high IQ. I suspect that if she took a standardized IQ test, she’d be someplace in the low end of the normal range. But that’s just conjecture on my part, entirely apart from the fact a high IQ doesn’t necessarily correlate with success. Besides, there are many kinds of intelligence – athletic, aesthetic, emotional, situational…

A high IQ can actually be a disadvantage to getting elected. Remember it’s a bell-shaped curve, and the “average” person isn’t a rocket scientist. That’s compounded by the fact half the population has an IQ of 100 or less. They’re suspicious of anyone who’s more than, say, 15 points smarter than they are.

However, there are better ways to define stupid than “a low score on an IQ test,” that apply to Alexandria. Stupid is “the inability to predict not just the immediate and direct consequences of actions, but the indirect and delayed consequences of your actions.”

She’s clearly unable to do that. She can predict the immediate and direct consequences of the policies she’s promoting: her supporters are very excited about “liberating” other people’s wealth that just seems to be sitting around. Power to the People, and AOC! But she’s completely unable to see the indirect and delayed consequences of her policies – which I hope I don’t have to explain to anyone now reading this.

If you promise people unicorns, lollipops, and free everything, they’re going to say, “Gee, I like that, let’s do it.” She’s clever on about a third grade level.

But there’s an even better definition of stupid. Namely, “an unwitting tendency to self-destruction.” All the economic ideas that she’s proposing are going to wind up absolutely destroying the country.

It’s as if she thinks that what’s happened recently in Venezuela and Zimbabwe – not to mention Mao’s China, the Soviet Union, and a hundred other places – was a good thing.

That’s my argument for her being stupid. And ignorant as well. But perhaps I’m missing something. After all, Karl Marx – who would thoroughly approve of her ideas – was both highly intelligent, and extremely knowledgeable; he was actually a polymath. The same can be said of many academics, left-wing economists, and socialist theoreticians.

So perhaps a desire for “socialism” isn’t just an intellectual failing. It’s actually a moral failing.

Socialism – A Moral Failing

Socialism is basically about the forceful control of other people’s lives and property. In my view, that’s evil.

I’m afraid Alexandria is evil on a basic level. I know that sounds silly. How can that be true of a smiling young girl who says she wants just sunshine and unicorns for everybody? It’s too bad the word “evil” has been so compromised, so discredited, by the people who use it all the time – bible-thumpers, hysterics, and religious fanatics. Evil shouldn’t be associated with horned demons and eternal perdition. It just means something destructive, or recklessly injurious.

The world would be better off if she went back to waitressing and bartending. But she herself isn’t the problem. She’s fungible. Her handlers can easily replace her, as an individual. The problem is that voters like what she represents.

It really helps to be young, good looking, and affable. But those things do nothing to solve the immense problems plaguing the U.S., just under the surface. Wouldn’t it be nice if everybody had a job paying at least $15 an hour, free schooling, housing was a basic human right, free medical, free food, and 100% green energy? It doesn’t sound evil – it just sounds stupid. But it’s actually both.

The problem isn’t just that she got elected on this platform in a benighted – but increasingly typical – district. The problem is that most young people in the U.S. also have her beliefs and values.

The free market, individualism, personal liberty, personal responsibility, hard work, rationality, free speech – the values of western civilization – are being washed away, everywhere. But it’s hard to defend them, because the argument for them is intellectual, economic, and historical. While the mob, the capita censi, the “head count” as the Romans called them, is swayed by emotions. They feel, they don’t think. Arguments are limited to Twitter feeds. Or 30-second TV sound bites.

When somebody says, for instance, “Why can’t we have free school for everybody? The university buildings are already built. The professors are already there. So why can’t everybody just go to class, and learn about gender studies?” The same arguments are made for food, shelter, clothing, entertainment, communication – everything in fact.

To counter that, you have to come up with specific reasons for why not. You end up sounding like a Negative Nelly because you’re telling people they can’t have something.

I guess I’ve given too much credit to the goodwill and the common sense of the average American. The proof of that is the success of AOC. Her election brings the average American’s psychological aberrations to the fore.

It’s exactly the type of thing the Founders tried to guard against by restricting the vote to property owners over 21, going through the Electoral College. Now, welfare recipients who are only 18 can vote, and the Electoral College is toothless. Some want to totally abolish the College, and have even 16-year-olds and illegal aliens voting.

Nobody, except for a few libertarians and conservatives, is countering the ideas AOC represents. And they have a very limited audience. The spirit of the new century is overwhelming the values of the past.

Everybody Will Blame Capitalism

When the economy collapses – likely in 2019 – everybody will blame capitalism, because Trump is somehow, incorrectly, associated with capitalism. The country – especially the young, the poor, and the non-white – will look to the government to “do something.” They see government as a cornucopia, and socialism as a kind and gentle answer. Soon, they think, everyone will be able to drink lattes all day at Starbucks while they play with their iPhones, living on a Guaranteed Annual Income.

The people who control the government definitely won’t want to be seen as “do nothings.” Especially while the ship of state is sinking in The Greater Depression. They’ll want to be seen as forward thinkers, problem solvers, and social justice warriors.

So we’re going to see much higher taxes, among other things. There’s no other way to pay for these programs, except sell more debt to the Fed – which they’ll also do, by necessity.

The government is bankrupt. But like all living things from an amoeba to a person to a corporation, its prime directive is to survive. The only way a bankrupt government can survive is by higher tax revenue and money printing. Of course, don’t discount a war; these fools actually believe that would stimulate the economy – the way only turning lots of cities into smoking ruins can.

I don’t see any way out of this.

via ZeroHedge News https://ift.tt/2FMqkdh Tyler Durden

New York state is nearing completion of a 2020 budget deal that’s going to result in “congestion tolls” in Manhattan, alongside a “mansion tax” and a ban on single-use plastic bags, according to Bloomberg. State leaders and Governor Andrew Cuomo agreed this week on a spending plan for 2020 that allocates for 2% budget growth for the ninth year in a row. The plan increases spending for education aid and provides tax relief for the middle class, according to the Governor.

Lawmakers will be discussing the budget again Sunday night to try and meet a midnight deadline to pass it. The proposed “congestion tolls” will make New York City the first American city to charge drivers for access. It’s projected to raise $1 billion, which will then be used to pay debt service (of course) on the $15 billion in Metropolitan Transportation Authority bonds outstanding.

MTA’s Triborough Bridge and Tunnel Authority has not yet released details on the toll program, which is expected to be implemented after December 2020.

In an attempt to drive even more wealthy New Yorkers to Florida, lawmakers will also be asked to approve a progressive tax on mansions with a combined top rate of 4.15% on the sale of properties valued at over $25 million:

The so-called mansion tax would establish a new scale of graduated levies, starting at 1 per cent on all New York City apartments selling for more than $1 million, rising at $2 million and reaching a top of 4.15 percent on $25 million. It’s expected to raise $365 million, to borrow about $5 billion. The old tax imposed a flat 1 percent rate at $1 million or more on all apartments.

Additionally, New York will follow California’s lead in banning disposable plastic grocery bags. This will force residents to pay for paper bags or reuse their own bags and is expected to be implemented by March 2020. 71,000 tons of plastic bags are used annually in New York City, according to the report.

The legislation will also include “elimination of cash bail for about 90 percent of defendants awaiting trial on misdemeanors and low-grade felony charges.”

Cuomo said of the budget: “From the beginning, I said we will not do a budget that fails to address three major issues that have evaded this state for decades — the permanent property tax cap, criminal justice reform and an MTA overhaul including Central Business District Tolling. I also said this budget must be done right — meaning it must be fiscally responsible and protect New York from the federal government’s ongoing economic assault on our state. I am proud to announce that together, we got it done.”

via ZeroHedge News https://ift.tt/2OB6ynD Tyler Durden

Submitted by Eric Peters, CIO of One River Asset Management

Three Worlds

“America’s yield curve inversion can mean one of three things,” said the CIO. “We’re either living in a world of secular stagnation and investors worry that central banks no longer have sufficient policy tools to spur growth and inflation,” he continued. “Or the economy is simply sliding toward recession and the inversion will persist until the Fed panics and spurs a recovery,” he said. “Or we’re living in a world, where the market is moving in ways that defy historical norms because of global QE. And if that’s the case, the curve is sending a false signal.”

“If we’re sliding toward recession, then it seems odd that credit markets are holding up so well,” continued the same CIO. “So keep an eye on those,” he said. “And if the curve is sending a false signal due to German and Japanese government bonds yielding less than zero out to 10yrs, then the recent Fed pivot and these low bond rates in America may very well spur a blow-off rally in stocks like in 1999.” A dovish Fed in 1998 (post-LTCM) and 1999 (pre-Y2K) provided the liquidity without which that parabolic rally could have never happened.

“But if investors believe America is succumbing to the secular stagnation that has gripped Japan and Europe, and if they’re growing scared that global central banks are no longer capable of rescuing markets, then we have a real problem,” said the CIO. “Because a recession is bad for markets, but not catastrophic provided that central banks can step in to spur recovery. But with global rates already so low, if investors lose faith in the ability of central banks to do what they have always done, then we’re vulnerable to a stock market crash.”

Sovereignty:

Turkish overnight interest rates squeezed to 300% on Monday. Then 600% on Tuesday. By Wednesday, they hit 1,200%. Downward pressure on the Turkish lira, and the government’s efforts to punish speculators fueled the historic rise. Erdogan allegedly wants to limit lira loses ahead of today’s elections. The pressures that drove the currency lower were mainly of Turkish origin. Of course, the Turks have every right to their own economic policies, but they must bear the consequences. That’s what comes with being a sovereign state.

The Greeks and Turks are neighbors. The Turks began negotiations to join the EU in 2005, with plans to adopt the Euro after their acceptance. Those negotiations stalled in 2016. As they look across the border at their Greek neighbors now, and see their interest rates stuck at -0.40%, are they envious? Perhaps. But having witnessed the 2011 Greek humiliation, would the Turks be willing to forfeit sovereignty for the Euro’s stability and stagnation? And how do the Greeks (and Italians) feel about having forfeited their sovereignty?

Anecdote:

“Only optimists start companies,” I answered. The Australian superannuation CEO had asked if I’m an optimist or pessimist. “I see the potential for technological advances to produce abundance in ways difficult to fathom. But I also see the chance of something profoundly dark,” I continued. He observed that people seemed consumed by the latter but spend so little time on the former. “That’s good. Humans are wonderful at solving problems of our own creation. The more we worry, the less goes wrong,” I said. So he asked what worries me most?

“Not the displacement of human labor by machines, we can solve the resulting social challenges. I worry that the only thing Americans seem to agree on now is that China is our adversary.” And pressing, he asked me to list the things I admire about China. “Okay. I admire China’s work ethic, drive, ambition, economic accomplishments. They’ve overtaken us in many advanced scientific fields. I admire that very much.” He smiled and asked me to carry on. “I’m grateful for their competition. It makes us better. And I admire that they’ve evolved communism to make it work while all others failed. The world is better with diversity of thought, philosophy – diversity increases resiliency, robustness. And democratic free-market capitalism will grow stronger with a formidable competitor.” He smiled.

“But China’s system values the collective over the individual. We value the opposite. And I’m concerned the two systems cannot peacefully coexist now that we’re the world’s two largest economies. I don’t want to live under their system, I don’t want their vision of the future for my children. They probably feel the same way. Both views are valid but incompatible, and increasingly in conflict,” I explained. He nodded and said, “I don’t want that for our children either.”

via ZeroHedge News https://ift.tt/2U4faZU Tyler Durden

Approximately 34% of attendees at President Trump’s Thursday night rally in Grand Rapids, Michigan were registered Democrats, according to Trump’s 2020 campaign manager Brad Parscale.

Speaking on Saturday with Fox News‘ Jesse Watters, Parscale explained that the campaign uses the phone numbers of attendees to look up their voter information.

“We had tens of thousands of registrants, I believe 34% of the people who came to the Michigan rally were Democrats,” said Parscale, adding “Almost half had only voted once in the last four elections.”

When asked if the campaign was still harvesting information on various demographics, Parscale said: “I’m harvesting nearly a million voters data information in key swing states every month.”

“That must terrify the Democrats,” interjected Watters.

“Yeah, we are – put it this way, we are four times ahead of where we were in 2016 and I plan on being 6 to 8 times ahead in data, that’s tens of millions of records.“

via ZeroHedge News https://ift.tt/2WzVie3 Tyler Durden

{kind=link}

{kind=link}