Australia is continuing down the path of the global low yield charge, about to approach its final percentage point of “interest rate ammunition”, according to Bloomberg.

The 10 year yield in Australia hit an all time low of 1.26% last week, which is more than a full percentage point under where they started the year. This means that every Australian bond – all the way out to the longest maturity in 2047 – is yielding less than the bottom of the central bank’s 2% to 3% inflation target.

And the speed with which the market environment is changing in Australia is catching the attention of many.

Richard Yetsenga, chief economist at Australia & New Zealand Banking Group Ltd. in Sydney said: “On the screen a minute ago, Aussie 10-year bond yields at 1.33? I mean, is that a typo? Even six months ago they were like 100 points higher.”

Additionally, the market is now pricing in an even chance that the Reserve Bank of Australia will cut its policy rate to 0.5% over the next year. Governor Philip Lowe will cut the cash rate by 25 bps on Tuesday, to 1%, according to 18 of 26 economists surveyed.

Sally Auld, a senior interest-rate strategist at JPMorgan Chase & Co. in Sydney said: “There is a sense of inevitability about where we are heading. We’ve seen this play out in a number of other big developed economies over the last decade. Rates have come all the way down to something close to zero, and they stay there for a very long time.”

The cash rate at 0.5% means that bank earnings could slide 15%, hurting the largest component of the country’s equity markets. Companies like annuities provider Challenger Ltd. have already felt the brunt of the lower rates, falling about 30% this year and citing “lower for longer” rates as the problem.

And Governor Lowe has telegraphed that he is open to further cuts, with Australia’s job market lagging full employment. Like the U.S., Australia is also concerned with “putting inflation on course”. Lowe says that QE right now is “really quite unlikely”, but with how things have been going, we wouldn’t be surprised to see that stance reversed fully within a matter of just months.

Rates at 1% have been what has prompted other unorthodox steps across the globe from the Federal Reserve and the Bank of England. Lowe has said that Australia’s lower level is at about 0.25% to 0.5%.

Paul Sheard, a senior fellow at Harvard University’s Kennedy School said:

“The potent policy then becomes monetary policy supporting fiscal policy”. It’s a more pragmatic kind of approach in Australia when it comes to cooperation among policy makers.”

While it is seen as a positive that a lower cash rate could flow quickly to households with floating rate mortgages, Australia finds itself again staving off a problem temporarily that will eventually and inevitably lead to a far worse, longer term problem. But as long as economists and central bankers fail to realize this, we can expect Australia, along with its central banking peers across the globe, to be doomed to repeat history – just an order of magnitude worse than the last crash.

via ZeroHedge News https://ift.tt/2xnftRM Tyler Durden

Canada is desperately trying to build the much-delayed Trans Mountain Expansion, but even as it tries to advance the ball on one front, another pipeline has found itself in the crosshairs.

Enbridge’s Line 5 pipeline carries more than a half a million barrels of oil and products per day from Alberta, across the border into the U.S., and ultimately to refineries back in Canada at the major refining and petrochemical hub of Sarnia, Ontario.

The 540,000-bpd pipeline may be in trouble, however. The state of Michigan just launched a lawsuit, which could force Enbridge to shut the pipeline down. Michigan is concerned about the possibility of a leak from the aging pipeline, which crosses under the Straits of Mackinac. A leak could threaten drinking water and spoil the scenic Great Lakes.

Governor Gretchen Whitmer promised to stop the “flow of oil through the Great Lakes as soon as possible.”

Enbridge has been trying to build a replacement for the pipeline, which is nearly 70 years old. But the replacement proposal has been a huge point of contention. Michigan’s attorney general is hoping to shut it down. The risk the state most fears is an anchor strike.

“The location of the pipelines…combines great ecological sensitivity with exceptional vulnerability to anchor strikes,” Michigan AG Dana Nessel said. An anchor strike occurred in 2018 and was viewed as a near disaster.

“This situation with Line 5 differs from other bodies of water where pipelines exist because the currents in the Straits of Mackinac are complex, variable, and remarkably fast and strong.”

Enbridge argues that it inked a deal with the former Michigan governor last year, which would have allowed Enbridge to build a tunnel underwater to house the pipeline and allow the system to continue to operate. The new Democratic administration has tossed that agreement aside.

“We remain open to discussions with the Governor, and we hope we can reach an agreement outside of court,” Enbridge said in a statement.

“We believe the Straits tunnel is the best way to protect the community and the Great Lakes while safely meeting Michigan’s energy needs.”

The issue may seem like a local problem, but it would have regional, national and international implications. For one, refineries in Sarnia would struggle to replace the oil flows. According to Stratas Advisors, the refineries would be able to find alternative supplies from Line 78B, a pipeline from the U.S. Midwest, but there would be significant disruptions.

“If Enbridge Line 5 closes, Line 78B will be able to provide enough light crude for Sarnia refineries. There would be a shortage of light crude supply for Montreal, Kinatone and Nanticoke refineries,” in Eastern Canada, Stratas Advisors wrote.

“If contractual restrictions between Enbridge and non-Sarnia refineries lead to a shortage of light crude supply to Sarnia refineries, trucks and railroads would be used to transport the required light crude. Until the whole supply chain comes to an equilibrium, the refineries will run at low utilization.”

S&P Global Platts also said that rail could help pick up the slack if the pipeline is shut down.

If Line 5 has to shut down, it “would cause a huge disruption of light crude supply to Eastern Canada and US Mid-Continent refineries,” Statas Advisors said.

Meanwhile, the disruption upstream would also be significant. Canada’s oil producers suffered from steep discounts last year because of midstream bottlenecks. Some rail capacity has eased the constraint, but the inability to build new pipelines has hurt the industry. Ultimately, Alberta implemented mandatory production cuts, which helped rescue depressed Western Canada Select prices.

Now, the Canadian government is hoping to build its nationalized Trans Mountain Expansion pipeline, although that project is still riddled with uncertainty, even with the latest approval from Ottawa. First Nations and environmental groups have vowed to fight the project. Even if all goes according to plan, it would not come online for several years at the earliest.

At the same time, Enbridge is also running into trouble with another of its aging pipeline. It has proposed building a replacement for its Line 3 pipeline, which also carries oil from Alberta to the U.S. The project has run into roadblocks in Minnesota, forcing delays in construction.

If Line 5 is forced to shut down, taking 540,000 bpd of takeaway capacity offline, it would almost surely exacerbate midstream bottleneck, and would likely steepen discounts that Canadian oil producers face.

via ZeroHedge News https://ift.tt/2KOqGn9 Tyler Durden

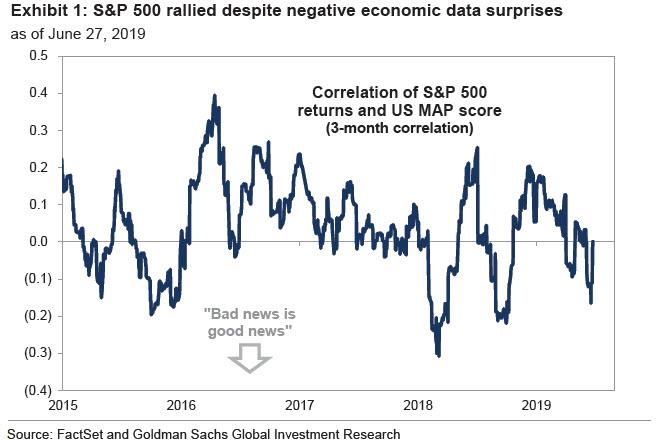

The S&P may have just enjoyed its best June in 84 years but not because of rising corporate profits and earnings. Quite the contrary: according to Goldman, while the S&P 500 rose 7% from its trough on June 3, valuation expansion accounted for 90% of the rally in response to the Fed’s becoming “impatient” and signaling an easing cycle has begun. As Goldman’s chief equity strategist David Kostin writes, the realized 3-month correlation between S&P 500 returns and the bank’s MAP index, a measure of economic data surprises, reached a low of -0.2 last week versus a 10-year average of +0.1.

Meanwhile, weak economic data – which validated the Fed’s easing bias – have generally been “good news” for equity valuations but “bad news” for earnings expectations during the past three months.

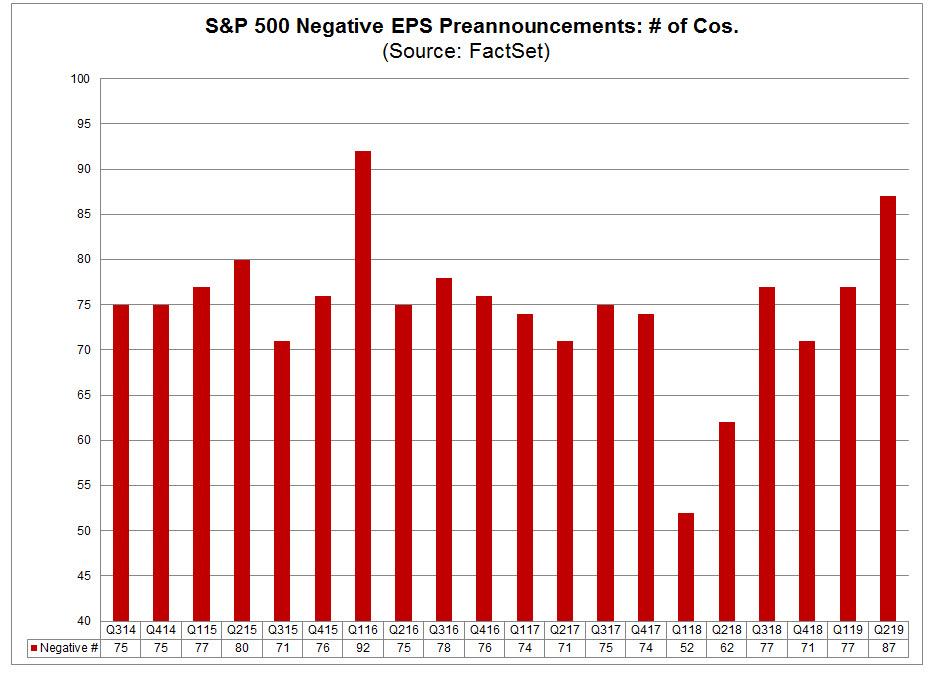

Indeed, if investors are looking for some upside from corporate fundamentals, they probably won’t find them in the upcoming Q2 earnings season, as consensus bottom-up 2019 EPS estimates have resumed their downward trend following a brief reprieve during 1Q earnings season. Consensus has lowered its estimate of 2019 EPS by $1 to $166 (+2% growth year/year) during the past six weeks, with Goldman noting that since the start of 4Q 2018, 2019 EPS growth expectations have declined from +10% to +2%. As we reported yesterday, companies issuing negative guidance has jumped to 87, the second highest on record, while 1-month EPS revisions have been most negative in Energy and Info Tech

So with 2Q earnings season kicking off in earnest on July 15, consensus expects aggregate EPS to decline by 1% year/year , and if realized, this would be the first year/year decline in quarterly EPS since 2016.

To be sure, consensus also expected a 2% decline in EPS at the start of earnings season in 1Q, however, realized growth ultimately equaled +2%, with the number saved by Trump’s tax cuts, as effective tax rates were lower than originally anticipated.

Meanwhile, excluding Financials and Utilities, S&P 500 sales are forecast to grow by 5% in 2Q but to be more than offset by an 86 bp decline in net profit margins. Consensus expects all 8 sectors to see positive sales growth and margin contraction in 2Q. Communication Services (+4%) and Financials (+3%) are forecast to post the fastest EPS growth.

Despite the broad-based drop in EPS, the median S&P 500 company is still expected to post modest growth and see its EPS grow by 4% year/year in 2Q. The culprit, perhaps unexpectedly, is Info Tech which has an outsized weight in the index, accounting for 20% of earnings, and is forecast to see EPS fall by 10% year/year this quarter driven by AAPL (-10%) and semiconductors (-28%). As a result, aggregate EPS growth distorts the fundamental outlook for the median company. Notably, within Info Tech, Software & Services 2Q EPS growth is expected to be healthy (+7% year/year).

Looking at the broader macro picture, the slowdown in economic growth during 2Q is consistent with expectations for a decline in EPS growth. With economic growth the primary driver of S&P 500 sales and earnings growth., during 2Q 2019, the Goldman Current Activity Indicator (CAI) averaged just 1.4%, a pace of growth that pales in comparison with the 3.4% growth during 2Q 2018. Global growth has also been weak amid heightened uncertainty and ongoing trade war between the US and China – which while did not escalate this weekend, continue as before – with the GS global CAI averaging 2.9% during the quarter versus 4.2% in 2Q 2018.

Qualifying at the main drivers of downside profitability, Kostin expects profit margins will contract as input costs continue to weigh on profitability. In part due to the one-time boost from tax reform, net profit margins reached an all-time high in 2018. However, margins contracted in 1Q 2019 for the first time since 2016. The unemployment rate stands at a 50-year low (3.6%) and average hourly earnings have grown by more than 3% in each of the last 8 months.

In addition to a tighter labor market, capacity constraints have led to higher transportation and logistics costs, as companies have been unable to keep pace with their prices; an NABE survey shows that the net share of respondents reporting rising wages (57%) and materials costs (36%) is well above the net share reporting rising prices charged (18%). Historically, this pattern has been a precursor to EBIT margin declines, as consensus expects in 2019.

At the same time, tariffs represent a significant source of uncertainty for corporate profit margins, with Goldman pointing out that “tariffs pose a greater risk to company profit margins than to sales” and adding that “if the trade war escalates and a 25% tariff is imposed on all imports from China, current consensus S&P 500 EPS estimates could be lowered by as much as 6%.” And while such an outcome has been averted for now thanks to Saturday’s ceasefire between Trump and Xi, it may still return, in which case S&P 500 firms would need to raise prices by around 1% to offset the impact of tariffs.

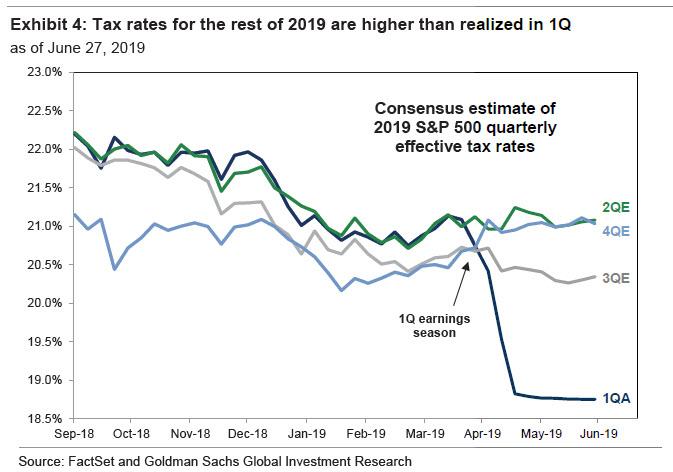

Yet while Trump’s tariffs are the primary source of risk to Q2 and H2 earnings, Trump’s tax cuts are the the primary source of upside risk to 2Q and full-year 2019 EPS estimates in the form of an even lower effective tax rate. Consider this: the S&P 500 effective tax rate during 1Q equaled 19%, compared with an estimate of 21% at the start of earnings season, and was a significant contributor to better-than-expected results in the quarter.

However, as Goldman notes, consensus estimates for the effective tax rate in the remaining three quarters of 2019 have remained largely unchanged. Consensus forecasts a 21% effective tax rate through year-end, but if tax rates remains at 1Q levels, it would lift 2019 EPS estimates by roughly $3 (from $166 to $169 or roughly +150 bp additional growth).

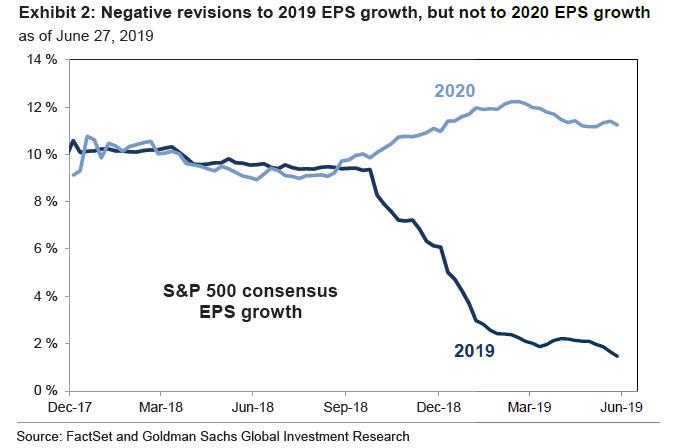

It is also worth noting that Wall Street’s bout of pessimism is expected to be a brief one, as while consensus has lowered 2019 EPS growth estimates, they have not adjusted 2020 estimates, which stand at 12% compared with 11% at the start of the year.

Here Goldman, which remains bullish on the overall market (despite the random strategist publishing an occasional bearish note expecting a market crash within the next 12 months), expects that “the macro environment will support an EPS growth acceleration in late 2019 and 2020 relative to the first three quarters of this year.” However, even Goldman forecasts just 4% EPS growth in 2020 and expects negative revisions to 2020 EPS estimates. To wit: on average since 1985, consensus EPS estimates have typically been lowered by an average of 8% from when analyst estimates are first published two years prior to the estimate year. And with Wall Street always eager to delay the moment of cutting its overly optimistic forecasts until the last possible moment, negative revisions to forward year EPS typically accelerate after the 2Q earnings season as investors and analysts shift their focus to the following calendar year.

With all that in mind, Goldman warns that while the dovish pivot from the Fed lifted equity valuations in every S&P 500 sector (furthermore, with a China-US trade deal now once again a possibility as the two sides are once again negotiating, there is a clear risk the Fed may not cut at all as this Bloomberg article details) but Goldman expects that fundamentals, i.e., earnings, will become an increasingly important driver of returns going forward for the simple reason that “earnings drive stocks over the long term.”

What does this means in practical terms? According to Kostin, a long/short factor of S&P 500 stocks with the highest versus lowest trailing FY2 EPS revisions has posted an average annualized return of 3.6% since 1980. But since January, the strategy has traded sideways as a dovish Fed has lifted US equity valuations broadly.

Finally, last quarter, the gap between performance of EPS beats and misses on the day after reporting earnings surged to 600 bps, the highest since at least 2006, and Kostin expect this trend will continue in 2Q as investors shift their focus from broad equity valuations to prospects for earnings growth in 2020.

via ZeroHedge News https://ift.tt/2ZXqMwf Tyler Durden

Despite nothing being achieved in Osaka apart from a resumption of more-of-the-same trade talks (and a fold by Trump), markets are decided ‘risk-on’ as they open this evening.

Treasuries are being dumped along with gold (because everything is awesome right?) and stocks and yuan are surging.

Dow is up over 250 points…

The biggest reaction for now is in Yuan, spiking to 8-week highs…

As a reminder, this is not news – but do not tell the algos…

“Stocks rally as China, US closer to a deal following G20”

Additionally, reported agreements between Russia and Saudi Arabia to extend the OPEC production cuts has spiked oil prices as they open this evening…

Oil producers from the OPEC+ alliance are moving toward extending their supply cuts for nine months into the first quarter of 2020, as they grapple with surging U.S. shale output and weakening growth in demand.

Since Russia and Saudi Arabia reached a deal on the margins of the Group of 20 summit on Saturday to roll over the curbs by six to nine months, other nations have voiced their support for an extension into next year.

“The longer the horizon, the stronger the certainty to the market,” OPEC Secretary-General Mohammad Barkindo said in Vienna on Sunday after meeting with Khalid Al-Falih, the Saudi oil minister. “It will be more certain to look beyond 2019. I think most of the forecasts that we are seeing now and most of the analysis are gradually shifting to 2020.”

Russian President Vladimir Putin – after meeting with Saudi Crown Prince Mohammed Bin Salman – opened the door to 2020 by mooting longer curbs.

via ZeroHedge News https://ift.tt/2ZTKrNE Tyler Durden

Chicagoans are buried under so much pension debt it’s impossible to see how their city can avoid a fiscal collapse without major, structural reforms. The futility of paying down those debts becomes obvious when you try to figure out just who’s going to pay for it all.

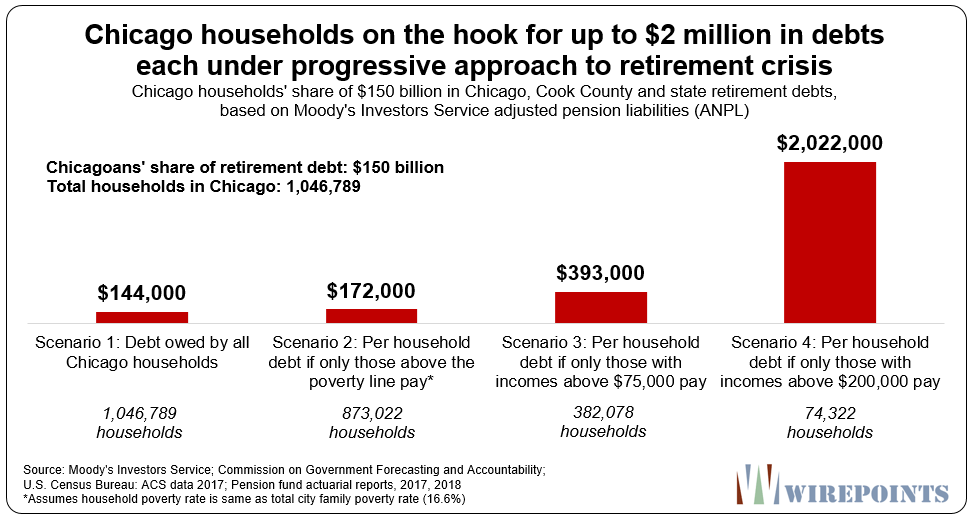

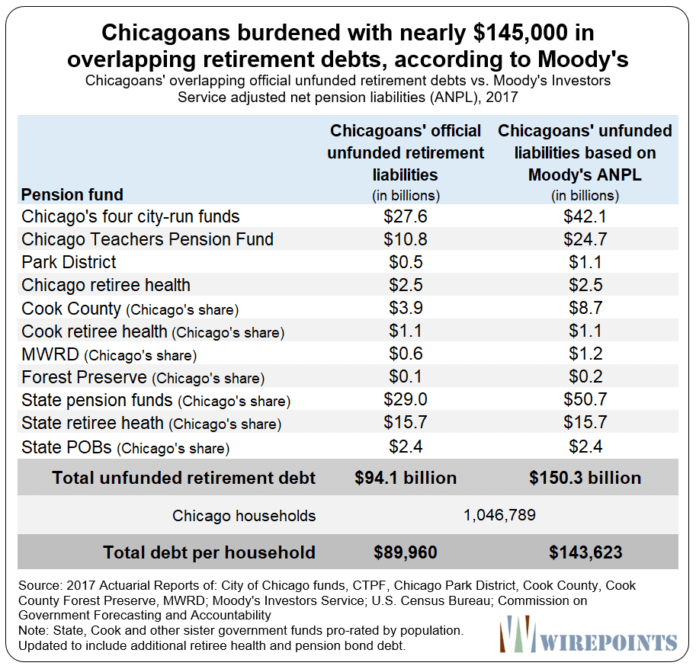

The total amount of city, county and state retirement debt Chicagoans are on the hook for is $150 billion, based on Moody’s most recent pension data. Split that evenly across the city’s one million-plus households and you arrive at nearly $145,000 per household.

That’s an outrageous amount, but it would be a clean solution if each and every Chicago household could simply absorb $145,000 in government retirement debt. The problem is, most can’t.

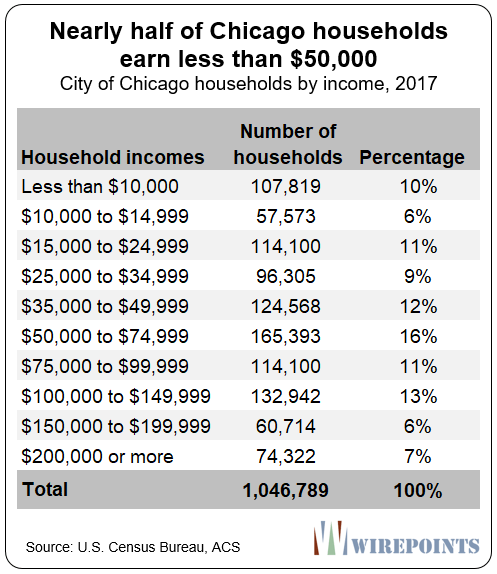

One-fifth of Chicagoans live in poverty and nearly half of all Chicago households make less than $50,000 a year. It wouldn’t just be wrong to try and squeeze those Chicagoans further, but pointless. They don’t have the money.

So if that won’t work, why not just put all the burden on Chicago’s “rich?” After all, Illinois lawmakers are pushing progressive tax schemes as the panacea for Illinois’ problems.

If households earning $200,000 or more are the target, they’ll be on the hook for more than $2 million each in government retirement debts. That’s an outrageous burden, too.

Saddling just a few households with all the debt will give those residents all the more reason to leave. And that will make the burden all the more unbearable for the Chicagoans who remain.

The process to target Chicago’s “rich” already started earlier this year. That’s when state lawmakers passed a progressive tax scheme which, if approved by voters in 2020, will hit Illinoisans earning more than $250,000 with tax increases as large as 60 percent. Chicago’s special interest groups want to hit the rich as well. They’re demanding a dedicated city income tax and a financial transaction tax that will impact the city’s wealthier residents.

Trying to find some middle ground on divvying up Chicagoans’ pension debts is also impossible. If all lower and middle income households earning up to $75,000 are protected, that leaves just 37 percent of Chicago households to pay the $150 billion bill. The burden on them would total $393,000 each. Still crazy.

Slice up Chicago’s debts anyway you like it, but the result is the same. There’s simply too much of it for Chicagoans to bear. Without structural pension reforms, expect the city to continue its path deeper into junk territory and an eventual insolvency. That will inflict enormous pain not just on taxpayers, but on the workers counting on the government for their retirement security.

Adding up the debt

For decades, official government reports have understated the true amount of pension debt Illinoisans are on the hook for. Government calculations have been criticized by the likes of Warren Buffet and Nobel Prize winners for using improper actuarial assumptions. For that reason, Wirepoints’ uses pension debts calculated by Moody’s Investors Service. The rating agency takes a more conservative approach to measuring debts than state officials do.

Chicago has four city-run pension funds that collectively face a $42 billion shortfall. The Chicago Public Schools’ pension fund is short another $24 billion. In all, there’s a $70 billion shortfall in the city-based funds alone.

Chicagoans are also burdened with an additional $11 billion in debt – their share of debts owed by various Cook County governments.

And Chicagoans’ share of state retirement debts for pensions, retiree health and pension bonds adds another $69 billion.

In total, Chicago households are on the hook for $150 billion in combined retirement debts.

Chicago the outlier

Not only are those debts overly burdensome to Chicagoans, but the city’s debts alone make Chicago a major outlier nationally when it comes to retirement debt.

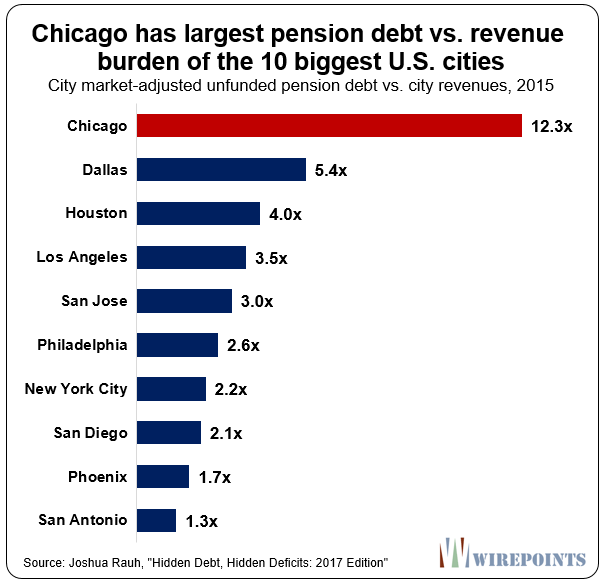

According to Joshua Rauh of the Hoover Institution, the city of Chicago’s pension debts are now 12 times the size of its annual revenues. No other major city faces such a burden.

In fact, according to JP Morgan, over 63 percent of the city’s budget should be going towards retirement payments. That’s the worst of any major city in the nation, by far.

Too much debt is the key reason Chicago’s credit ratings have collapsed. Moody’s already rates Chicago one notch into junk and the Chicago Public Schools five notches into junk. Detroit is the only major U.S. city rated worse than Chicago (See Appendix 2).

Impossible without reforms

The above numbers show the impossibility of stopping Chicago’s fiscal decline without serious, structural pension reforms.

Some pension proponents will find offense with our use of Moody’s debt numbers – they’ll say Moody’s assumptions are too pessimistic and overstate the problem.

But the debt burdens are still unworkable even if official government numbers are used. The average Chicago household is still on the hook for $90,000 in debt under the official numbers, while households making $200,000 or more would still face a burden of more than $1.2 million each.

Without structural changes, those numbers will only get worse.

For starters, lower discount rates and more conservative actuarial assumptions continue to show that pension debts are much larger than politicians say they are.

Second, as in-migration into Chicago slows and out-migration increases – a fair assumption given that Chicago has shrunk four years in a row – the debt burden on those who remain will rise.

And third, the risk of a recession is growing now that the nation’s economic expansion has lasted an unprecedented ten years. Any significant pull-back in the stock market would deal a major blowto Chicago’s deeply underfunded pension plans.

Only structural reforms, including changes to cost-of-living adjustments – will make the city affordable again for the ordinary Chicagoan. And that requires an amendment to the state’s constitutional protections.

via ZeroHedge News https://ift.tt/2NphFTT Tyler Durden

For many decades, the Supreme Court has chosen to avoid addressing some issues by ruling that they are “political questions,” and therefore not fit for resolution. Last week, in Rucho v. Common Cause, the Court concluded that political gerrymandering falls within that category. In cases such as Baker v. Carr (1962), the Court has said that political questions are issues that lack “judicially administrable standards” or ones where the decision in question has been left to the “nonjudicial discretion” of another branch of government.

I have been teaching the political questions doctrine in introductory constitutional law classes since 2002. But the more I think about it, the less sense it makes. In an excellent recent post at the Originalism Blog inspired by the gerrymandering decision, legal scholar Michael Ramsey outlines some of the flaws of the doctrine:

The Court, per Chief Justice Roberts, held that the constitutionality of political gerrymandering is a “political question” not suitable for judicial resolution, principally because it lacks judicially manageable standards. Once one grants that at least some consideration of political consequences is acceptable in redistricting decisions, how is one to say when it becomes too much consideration, and hence unconstitutional?

I’m entirely unpersuaded. Courts routinely draw difficult lines between borderline-acceptable behavior and borderline-unacceptable behavior. True, this is often messy. Justice Scalia, for example, famously wanted bright lines and hated balancing tests. But if the lack of a bright line makes a claim nonjusticiable, federal courts are going to have a great reduction in work load.

To take a couple of examples favored by center-right originalists, it’s not so easy to say when a law is sufficiently necessary and proper to the regulation of interstate commerce that it falls within Congress’ enumerated powers. Few people doubt that some federal regulation of local matters is justified due to their connection to interstate commerce, but how much connection is enough? This question isn’t considered a political question, nor should it be. And to take a very recent case, any re-invigoration of the nondelegation doctrine, as suggested by Gundy v. United States, involves deciding how much policymaking delegation by Congress is too much (it being undoubtedly true that some policymaking delegation is inevitable). It’s true that Justice Scalia thought this was sufficient reason to hold nondelegation claims basically nonjusticiable, but the current Court (including Chief Justice Roberts) seems prepared to reconsider. In neither of these situations (nor in many others I can think of) does the Constitution say exactly where the line should be drawn. But, generally speaking, courts still decide these cases, perhaps with a good bit of deference to the government in the gray areas. As I think a famous Justice said, the existence of twilight does not mean we cannot distinguish day and night.

No one interprets the political questions doctrine as forbidding judicial consideration of all issues that are governed by standards with potentially fuzzy boundaries, as opposed to bright-line rules. Indeed, even the late Justice Scalia often joined decisions applying such standards, despite his commitment to a legal philosophy that stresses the virtues of bright-line rules. But the doctrine simply doesn’t tell us how much fuzziness is too much. Thus, judges have little to go on besides their intuition and (in many situations), their ideological predilections.

To put it a different way, the “judicial administrability” prong of the political questions doctrine itself isn’t judicially administrable. Alternatively, if judges are capable of applying this incredibly vague standard, after all, then they are also capable of applying pretty much any other mushy standard, including figuring out how much political gerrymandering is too much. In that event, the standard may be judicially administrable, but also unnecessary.

The second standard prong of the political questions doctrine—commitment of the issue to another branch of government – is more defensible. But, as Ramsey explains, it is also superfluous:

The Court in Rucho does better in noting two points: (1) that founding-era Americans knew about partisan gerrymandering; and (2) that they nonetheless generally gave state legislatures power over districting, subject to oversight by Congress, but not subject to any other express limitations. One might say that this builds a case for application of the other prong of the political question doctrine—that a constitutional judgment is textually committed to another branch. But I doubt that approach as well. The fact that Congress has oversight does not mean the courts do not also have oversight.

Instead, I think the Court’s points about the text and history show something different: the Constitution does not limit partisan districting. At minimum, I would say that the originalist case for a constitutional limit on partisan districting is not proved… Put this way, districting is a political question, but not because of some arcane doctrine of justiciability. It is a political question because the Constitution did not address it, and thereby left it (like many other issues) to the political branches.

The courts do not need a special “political questions” doctrine to rule that a given law or regulation is constitutional because it falls within the authorized powers of that branch of government and nothing else in the Constitution forbids it. In fact, courts uphold legislation on that basis all the time, usually without any reference to the political questions doctrine.

Sometimes, the political questions doctrine is defended on the basis that it can be used to keep courts from involving themselves on issues where the legislature or the executive has superior expertise, particular questions involving immigration, foreign relations, and national security. The problem with that theory is that the political branches of government have superior expertise on nearly all areas of policy, and that immigration and national security are not actually unusual in that regard. The reason for judicial review is not that the judges have superior expertise on policy, but that they have different incentives, and are often more likely to protect long-term constitutional values and enforce minority rights. And, as with the “judicial administrability” issue, the Court has never come up with anything approaching a clear rule or standard for determining how big the gap in expertise has to be to require judges to avoid resolving a given issue.

On most constitutional questions—including most that involve fuzzy standards and issues where the political branches have superior expertise—courts resolve the relevant cases without even mentioning the political questions doctrine. Every once in a while, however, the Supreme Court will take it out for a spin in order to justify sidestepping some issue the majority would prefer to avoid. When that happens, those who like the result applaud, while dissenters argue that the doctrine has not been properly applied (as Justice Elena Kagan does in her forceful dissent in the gerrymandering case).

Both sides assume that the political questions doctrine is a useful tool for guiding judicial decision-making, or at least that it can potentially serve that role. The truth, however, is that it is an emperor walking around with no clothes. One of its main prongs is useless, while the other is superfluous.

There are, in my view, good constitutional arguments both for and against judicial policing of gerrymandering. Roberts and Kagan cover many of them in their respective opinions.

I am, perhaps, unusual in considering the issue to be a close question. Almost every other legal commentator seems to think it is a slam dunk, even as they vehemently differ over the issue of which side it’s a slam dunk for! Be that as it may, the political questions doctrine adds little of value to this debate—or any other.

from Latest – Reason.com https://ift.tt/3058PMB

via IFTTT

For many decades, the Supreme Court has chosen to avoid addressing some issues by ruling that they are “political questions,” and therefore not fit for resolution. Last week, in Rucho v. Common Cause, the Court concluded that political gerrymandering falls within that category. In cases such as Baker v. Carr (1962), the Court has said that political questions are issues that lack “judicially administrable standards” or ones where the decision in question has been left to the “nonjudicial discretion” of another branch of government.

I have been teaching the political questions doctrine in introductory constitutional law classes since 2002. But the more I think about it, the less sense it makes. In an excellent recent post at the Originalism Blog inspired by the gerrymandering decision, legal scholar Michael Ramsey outlines some of the flaws of the doctrine:

The Court, per Chief Justice Roberts, held that the constitutionality of political gerrymandering is a “political question” not suitable for judicial resolution, principally because it lacks judicially manageable standards. Once one grants that at least some consideration of political consequences is acceptable in redistricting decisions, how is one to say when it becomes too much consideration, and hence unconstitutional?

I’m entirely unpersuaded. Courts routinely draw difficult lines between borderline-acceptable behavior and borderline-unacceptable behavior. True, this is often messy. Justice Scalia, for example, famously wanted bright lines and hated balancing tests. But if the lack of a bright line makes a claim nonjusticiable, federal courts are going to have a great reduction in work load.

To take a couple of examples favored by center-right originalists, it’s not so easy to say when a law is sufficiently necessary and proper to the regulation of interstate commerce that it falls within Congress’ enumerated powers. Few people doubt that some federal regulation of local matters is justified due to their connection to interstate commerce, but how much connection is enough? This question isn’t considered a political question, nor should it be. And to take a very recent case, any re-invigoration of the nondelegation doctrine, as suggested by Gundy v. United States, involves deciding how much policymaking delegation by Congress is too much (it being undoubtedly true that some policymaking delegation is inevitable). It’s true that Justice Scalia thought this was sufficient reason to hold nondelegation claims basically nonjusticiable, but the current Court (including Chief Justice Roberts) seems prepared to reconsider. In neither of these situations (nor in many others I can think of) does the Constitution say exactly where the line should be drawn. But, generally speaking, courts still decide these cases, perhaps with a good bit of deference to the government in the gray areas. As I think a famous Justice said, the existence of twilight does not mean we cannot distinguish day and night.

No one interprets the political questions doctrine as forbidding judicial consideration of all issues that are governed by standards with potentially fuzzy boundaries, as opposed to bright-line rules. Indeed, even the late Justice Scalia often joined decisions applying such standards, despite his commitment to a legal philosophy that stresses the virtues of bright-line rules. But the doctrine simply doesn’t tell us how much fuzziness is too much. Thus, judges have little to go on besides their intuition and (in many situations), their ideological predilections.

To put it a different way, the “judicial administrability” prong of the political questions doctrine itself isn’t judicially administrable. Alternatively, if judges are capable of applying this incredibly vague standard, after all, then they are also capable of applying pretty much any other mushy standard, including figuring out how much political gerrymandering is too much. In that event, the standard may be judicially administrable, but also unnecessary.

The second standard prong of the political questions doctrine—commitment of the issue to another branch of government – is more defensible. But, as Ramsey explains, it is also superfluous:

The Court in Rucho does better in noting two points: (1) that founding-era Americans knew about partisan gerrymandering; and (2) that they nonetheless generally gave state legislatures power over districting, subject to oversight by Congress, but not subject to any other express limitations. One might say that this builds a case for application of the other prong of the political question doctrine—that a constitutional judgment is textually committed to another branch. But I doubt that approach as well. The fact that Congress has oversight does not mean the courts do not also have oversight.

Instead, I think the Court’s points about the text and history show something different: the Constitution does not limit partisan districting. At minimum, I would say that the originalist case for a constitutional limit on partisan districting is not proved… Put this way, districting is a political question, but not because of some arcane doctrine of justiciability. It is a political question because the Constitution did not address it, and thereby left it (like many other issues) to the political branches.

The courts do not need a special “political questions” doctrine to rule that a given law or regulation is constitutional because it falls within the authorized powers of that branch of government and nothing else in the Constitution forbids it. In fact, courts uphold legislation on that basis all the time, usually without any reference to the political questions doctrine.

Sometimes, the political questions doctrine is defended on the basis that it can be used to keep courts from involving themselves on issues where the legislature or the executive has superior expertise, particular questions involving immigration, foreign relations, and national security. The problem with that theory is that the political branches of government have superior expertise on nearly all areas of policy, and that immigration and national security are not actually unusual in that regard. The reason for judicial review is not that the judges have superior expertise on policy, but that they have different incentives, and are often more likely to protect long-term constitutional values and enforce minority rights. And, as with the “judicial administrability” issue, the Court has never come up with anything approaching a clear rule or standard for determining how big the gap in expertise has to be to require judges to avoid resolving a given issue.

On most constitutional questions—including most that involve fuzzy standards and issues where the political branches have superior expertise—courts resolve the relevant cases without even mentioning the political questions doctrine. Every once in a while, however, the Supreme Court will take it out for a spin in order to justify sidestepping some issue the majority would prefer to avoid. When that happens, those who like the result applaud, while dissenters argue that the doctrine has not been properly applied (as Justice Elena Kagan does in her forceful dissent in the gerrymandering case).

Both sides assume that the political questions doctrine is a useful tool for guiding judicial decision-making, or at least that it can potentially serve that role. The truth, however, is that it is an emperor walking around with no clothes. One of its main prongs is useless, while the other is superfluous.

There are, in my view, good constitutional arguments both for and against judicial policing of gerrymandering. Roberts and Kagan cover many of them in their respective opinions.

I am, perhaps, unusual in considering the issue to be a close question. Almost every other legal commentator seems to think it is a slam dunk, even as they vehemently differ over the issue of which side it’s a slam dunk for! Be that as it may, the political questions doctrine adds little of value to this debate—or any other.

from Latest – Reason.com https://ift.tt/3058PMB

via IFTTT

John McAfee, the 73-year-old crypto-evangelist and all-around international-man-of-mystery, is exposing the ugly reality of western-media’s government-sponsored propaganda.

Mainstream American news outlets have had, pretty much, nothing good to say about Cuba since 1953, but as RT reports, annoyed by this endless stream of negativity, McAfee took to Twitter to correct some inaccuracies he detected in the reporting following a grocery run on Saturday.

“US government propaganda tells us, through the WSJ, that people in Cuba are starving, eating rats and nearly rioting for food,” McAfee said in a tweet on Saturday night.

“Went all over today and all I could find were food stands like this overflowing with food. Wake up America!”

U.S. government propaganda tells us, through the WSJ, that people in Cuba are starving, eating rats and nearly rioting for food. Went all over today and all I could find were food stands like this overflowing with food. Wake up America!@wsjusnewspic.twitter.com/K1nFykNTJI

Submitted by Eric Peters, CIO of One River Asset Management

Math

America’s state pension plans were underfunded by $1.35trln in 2016. The S&P 500’s +19% rally in 2017 helped reduce the underfunding to $1.26trln. But by the end of 2018, the gap had grown to a new $1.5trln high. It didn’t help that in 2018, every major asset class underperformed US Treasury Bills (that only happened at the outset of WWI, the Great Depression, and under Paul Volcker). You see, the average state pension assumes it will earn a 7.15% investment return every year, forever and ever.

Before the 2008 crisis, state pension plans were 14% underfunded. The avg plan lost -24% in 2008 and never fully recovered. The structural challenges facing these systems are so great that not even the longest economic expansion in US history, the most enduring equity bull market, record high corporate profits, and record low unemployment, has been sufficient to return the plans to health. The average state pension plan is now 31% underfunded. Kentucky is the worst and is 64% underfunded. CO, CT, IL, and NJ are roughly 50%.

20 state plans are less than 66% underfunded. From 2012-2017 their returns exceeded their 7.15% long-term forecasts, and so you would have expected them to have improved their funding ratios. In fact, their funding ratios deteriorated by another 5 points. In 2001, the average state contributed 3.7% of its revenue to its pension plans. That number has more than doubled to 7.4% today. Because pension costs have grown faster than revenues, states have had to divert $180bln since 2007 to make additional contributions. And still, the math does not work.

Subtraction

GMO publishes 7yr real-return forecasts for various asset classes. They assume an average of 2% inflation. They now forecast -2.7% average real-returns for large cap US equities (each year for 7yrs). +0.1% average real-returns for US small cap equities. +1.2% for int’l large cap equities. +2.3% for int’l small cap equities. +5.0% for emerging mkt equities. +9.5% for emerging mkt value equities. -1.6% for US bonds. -3.5% for int’l bonds (currency hedged). -1.1% for US inflation linked bonds. +1.3% for emerging debt. And +0.2% for US cash.

Addition

Imagine that the GMO forecasts are somewhere in the right zip code. If you add any combination of their forecasts, you come up with an aggregate return far below the 7.15% that the average state pension plan estimates they’ll generate on their portfolio. The only asset class with a forecast above 7.15% is emerging market value equities (which will probably see inflows for this very reason). And as today’s underfunding grows inexorably with each passing year, the Federal Gov’t will be forced to add money, turning to MMT to make the math work.

Anecdote

Once upon a time they built a system. They promised state workers a pension. At the system’s birth, the nation was in a Great Depression, stocks were in free fall. So naturally, the system’s creators invested in safe bonds. For decades, system membership expanded, assets soared. World War II came and went. The cost to win was enormous, the federal government incurred a staggering debt. To grow its way out of that obligation, politicians repressed interest rates for decades.

The economy soared, the stock market too. Two decades after that war ended, the real (inflation-adjusted) value of stocks had tripled. So of course, the system voted to invest 25% of assets in equities. A devastating bear market ensued almost immediately. For the next couple decades, the real value of US equities fell by two-thirds, while interest rates soared along with inflation. In an act of investing genius, the system doubled down and lifted its statutory 25% limit on equities in 1984. For 15yrs the pension system made magnificent investment returns.

Into the 1999 market euphoria, the system voted to increase worker benefits, reduce the retirement age, and cut contributions. A market crash erupted immediately, knocking the system to its knees.

The next bear market arrived in 2008, delivering a mortal blow. The damage was so great that despite a 300% gain in the real value of equities from the 2009 lows, the system remained woefully underfunded, unable to meet its obligations in the absence of extraordinary future returns.

But Shiller PE stock valuations were at 30, equal to the 1929 high, and only surpassed in the dot com bubble. Worse yet 10yr interest rates were only 2%. So, unable to entirely ignore reality, the plan lowered its forecasts for future returns to 7.15%. But that forced the system’s participants to increase contributions. Which they agreed to do, but with the understanding that the system would take even greater investment risks to ensure it can meet future obligations.

via ZeroHedge News https://ift.tt/2Xfu94M Tyler Durden

President Trump and China’s President Xi reached an agreement at the G20 summit in Japan on Saturday to restart trade talks, the second ceasefire between the superpowers in two months. “We’re right back on track, and we’ll see what happens,” Trump told reporters after an 80-minute meeting with Xi.

Despite the somewhat positive news that Trump would refrain from slapping new duties on an additional $300 billion worth of Chinese goods – which would have sparked a full-blown trade war. Americans have recently become irritated with Trump’s tariffs and his self-proclaimed label as Tariff Man, new IBD/TIPP polling shows, and first reported by Investor’s Business Daily.

The IBD/TIPP Poll covered 900 responses from June 20-27, 16% of respondents said Trump should increase tariffs if there’s no China trade deal this summer. Another 33% said Trump should remove all tariffs on China, even if a near-term agreement can’t be reached, while 44% said Trump should leave the duties in place.

While the President continues to insist that China pays the tariffs, Americans are starting to become more spectacle that he could be deceiving them.

Of all respondents, 46% said the economy is set to deteriorate if a near-term deal isn’t reached, while 44% are convinced that China will be the biggest loser.

The poll found that 45% believe tariffs on Chinese goods is slowing the economy, while only 26% believe they help.

A National Bureau of Economic Research report shows that American consumers fully pay tariffs – and it’s one of the main reasons why respondents are becoming increasingly pessimistic about the trade war. The 2018 report noted, “The U.S. experienced substantial increases in the prices of intermediates and final goods, dramatic changes to its supply-chain network” and reduced availability of imports.

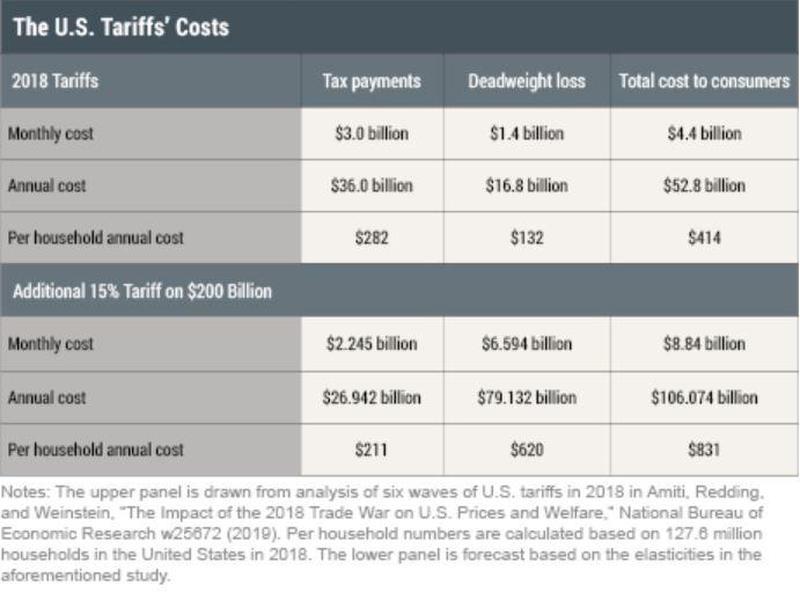

According to our reporting last month, a 25% tariff on $200 billion in Chinese goods would cost the average American household $831 per year, something that could anger many families as the overall economy is cycling down through summer.

Americans want a stable climate for business – not an environment where the government picks winners and losers. They also don’t want key trading partners to turn into enemies and endless shooting wars that can sometimes follow economic warfare [tarrifs].

via ZeroHedge News https://ift.tt/2xj3wN2 Tyler Durden