Authored by Lance Roberts via RealInvestmentAdvice.com,

The Melt-up Continues

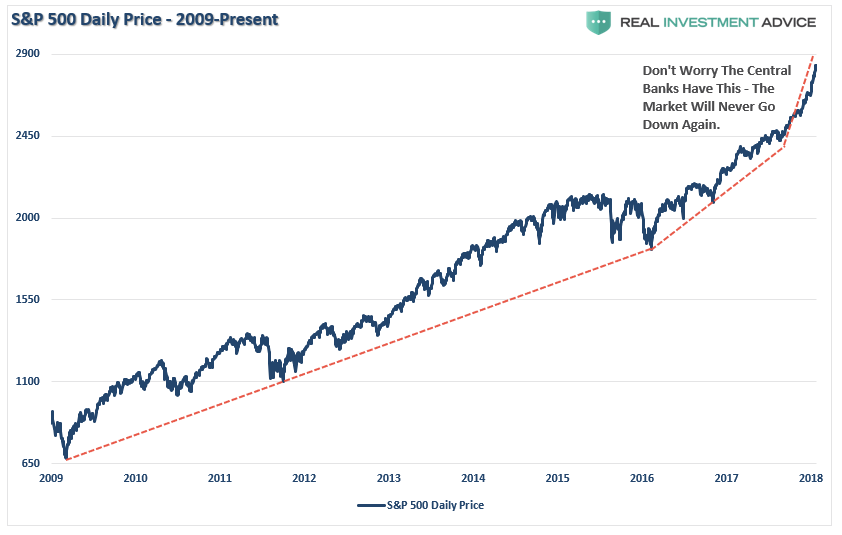

Since the beginning of the year, the acceleration in the markets has continued unabated. As I showed yesterday, the acceleration in the S&P 500 has now gone parabolic.

Of course, market melt-ups are symbolic of the final phases of “capitulation” as investors who feel like they “missed the boat,” finally jump back on board.

Such can be confirmed by the numerous emails from individuals asking me is “now the time to get back in?”

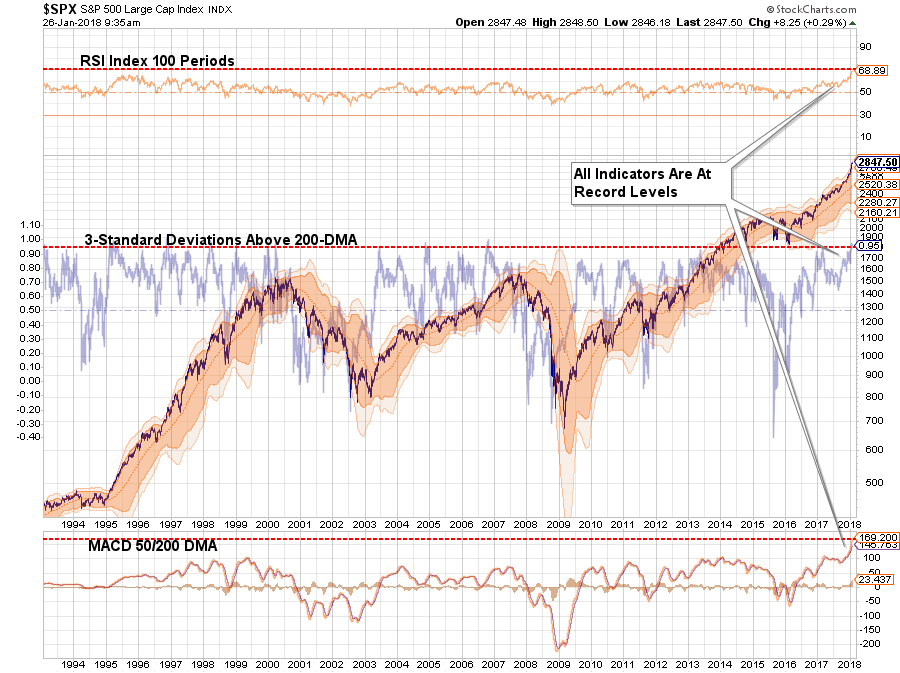

As shown in the chart below, such is the epitome of the “buy high, sell low” syndrome. Never before in recent history has the market been this overbought and extended from longer-term averages which suggests that a correction that reduces such conditions is highly likely in the near-term.

This doesn’t necessarily mean a “full blown” market crash, but even a correction back to the 200-dma, which is certainly within the scope of normal corrective actions, would currently entail a drawdown of almost -13%.

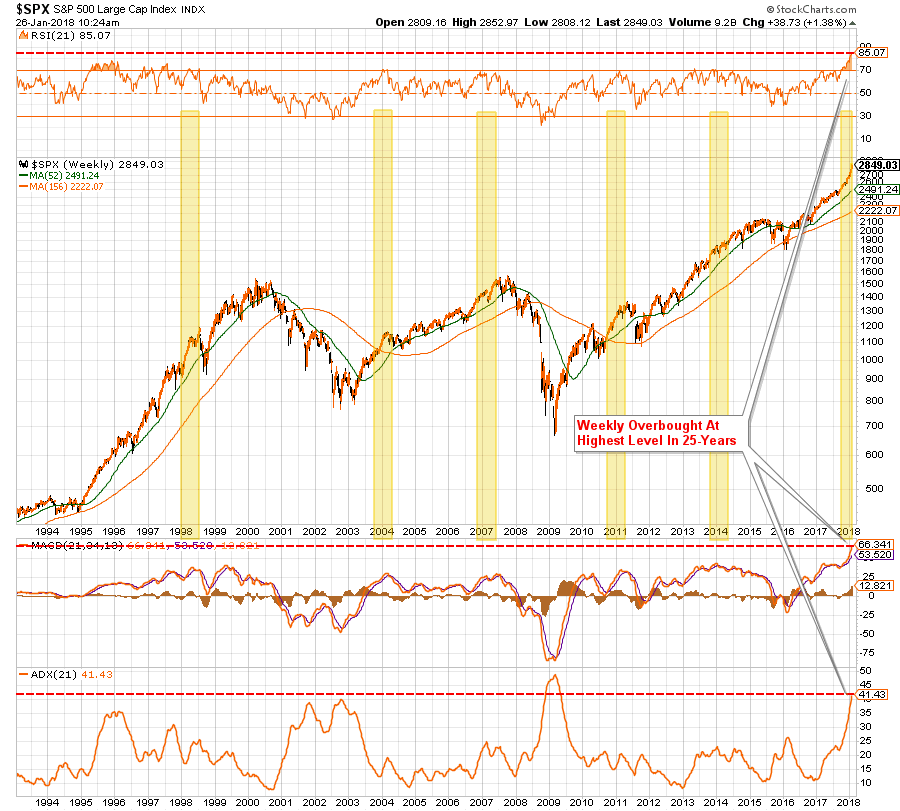

But let’s step back to a weekly chart and look at previous periods where historically high overbought conditions have existed previously.

On a weekly basis, a correction back to the 52-week moving average would require a bit more than a -14% decline while a correction back to the long-term trending average would be roughly -28% from current levels.

As I have said before, given we are now in the longest stretch in market history without even a 3% correction, 13% to 14% is going to “feel” worse than it is, and 28% will be equivalent to a full-fledged crash.

But just to keep that in perspective, a 28% decline from current levels only sets investors back to 2015. But, given that most investors are driven largely by emotion, those that have jumped in just recently, will be looking to “bail out” with that kind of a drop.

Buy high. Sell low.

Wash. Rinse. Repeat.

However, there’s nothing to worry about currently as long as the markets keep ratcheting up to new highs. As I penned last week in “The Honey Badger Market,”

“For now, it is hoped that historically high levels of stock valuations will be reduced by an explosion in underlying earnings growth due to the impact of tax reform.

While exuberance is currently ‘off the charts’ bullish, and our portfolios remain inherently long in the meantime, we are extremely cognizant of the risk of something ‘breaking.’

It is what always happens.

Yes, currently, everything is absolutely, positively, optimistic. Economic growth has picked up over the last couple of quarters due to an unprecedented level of natural disasters, oil prices have risen boosting production and corporate earnings, and employment is at historically high levels if you don’t count those out of the labor force.

The positive backdrop for stocks could not be currently better.”

Such is certainly the case for now.

The Davos Warnings

Meanwhile, in Davos, the confab of billionaires, world leaders, and the media have gathered for the annual confab in which the fate of the world is determined.

We were fortunate enough to obtain a clip from one of the speeches.

However, not all the views from Davos were of global tranquility and peace.

Barclays CEO Jes Staley, warned that financial markets remind him somewhat of what was seen before the 2008 crash.

“This feels a little bit like 2006. There are lots of reasons to be optimistic.

Global economic growth across the board is doing great at roughly 4%, unemployment rates in the U.K. and the U.S. are at almost record lows. All that is great. But all that comes amid ‘incredibly accommodating’ monetary policy, with interest rates that almost assume we’re still in recession.

If interest rates move too quickly and volatility whips around, things could get ‘interesting’ for markets over the next two years. It’s ‘concerning’ that people are selling short volatility even as it’s historically low, asset values are at all-time highs, and every major industry around the world last year grew by more than 20%.”

André Bourbonnais, chief executive of PSP Investments, which manages close to $112 billion USD of Canadian pension-fund assets, said:

“Everyone feels, despite the exuberance in the market, that we need to dial down on the risk.

Michael O’Sullivan, chief investment officer for international wealth management at Credit Suisse stated:

“The markets are being driven by a synchronized economic recovery in the U.S., Asia and Europe. Markets are focused on the business cycle rather than politics. Most asset markets are therefore ignoring politics—with the exception of the foreign-exchange market. One possible reason for the lack of market focus on politics may be the growth of automated trading as robots are much less interested in politics than humans.”

“The biggest concern I have is that most people think there’s no problem of a likely recession this year or early next year. Generally, when people are happy and confident, something wrong happens.’’

“If interest rates go up even modestly, halfway to their normal level, you will see a collapse in the stock market. I don’t know how everything from art and bitcoin to stock prices will react as interest rates go up.”

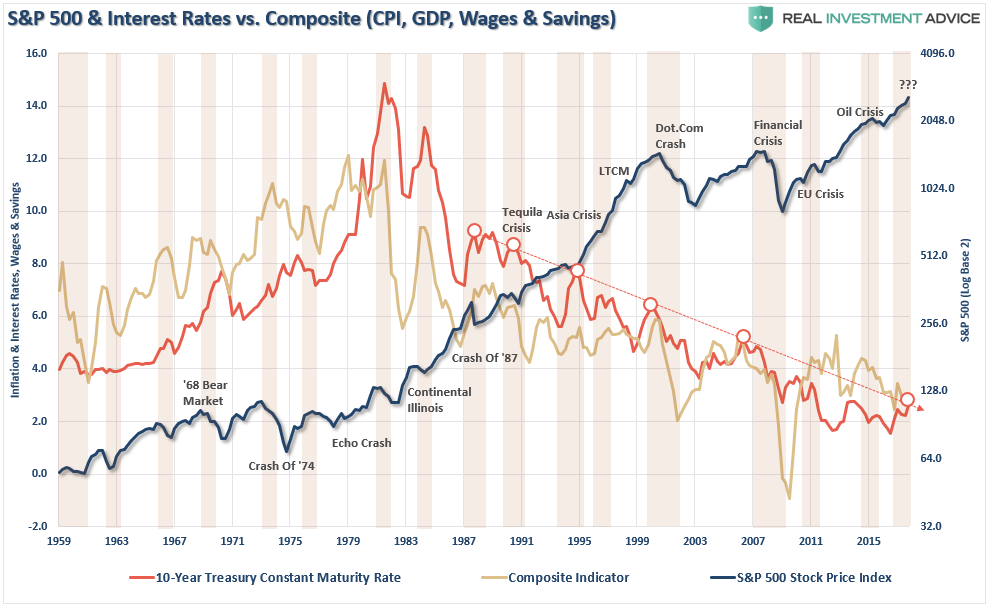

Of course, with interest rates around the globe at historic lows, companies have binged on cheap borrowing, easy credit terms and “seller’s market” as investor chase yield.

You will notice that each major market peak in history was accompanied by high-leverage ratios.

The biggest risk, as noted last week, is a significant rise in interest rates the “pricks” the debt-bubble.

via RSS http://ift.tt/2EfueZz Tyler Durden